Food Processing Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

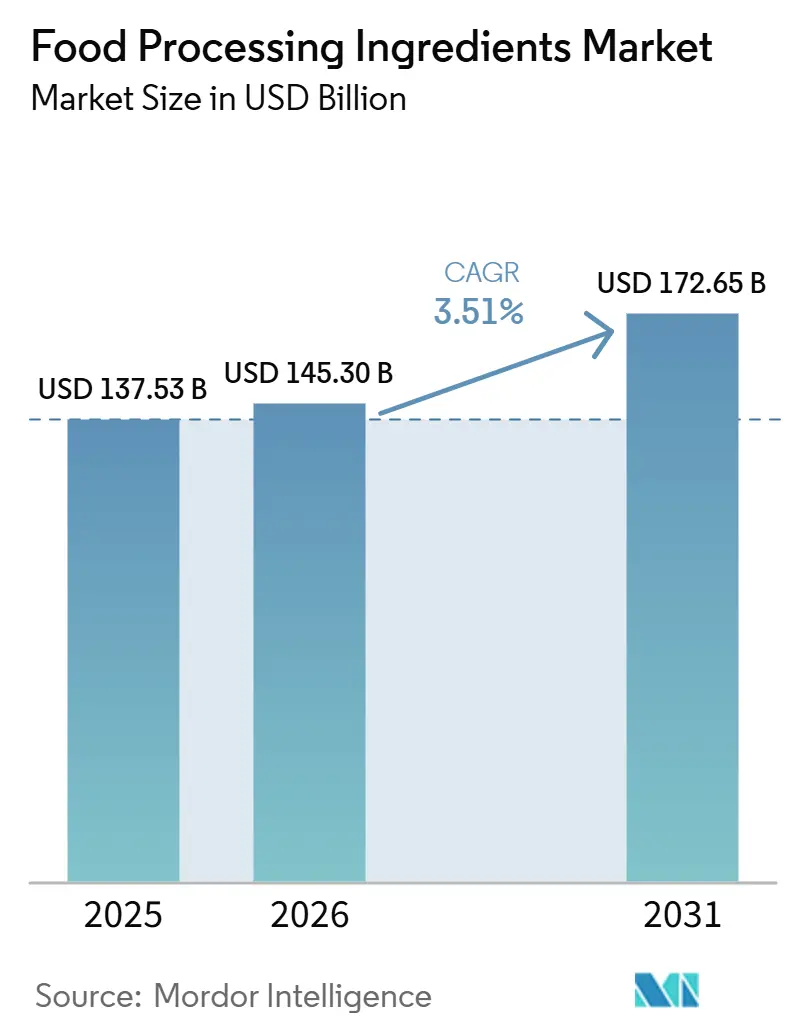

| Market Size (2026) | USD 145.30 Billion |

| Market Size (2031) | USD 172.65 Billion |

| Growth Rate (2026 - 2031) | 3.51% CAGR |

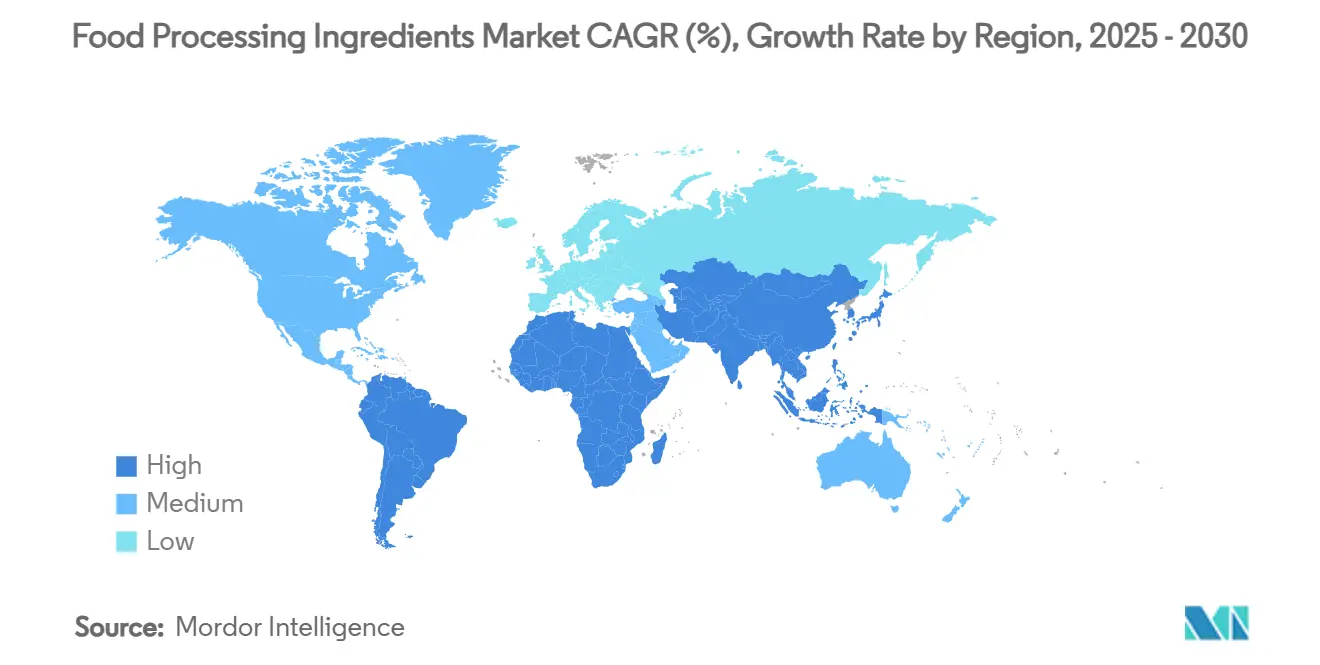

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

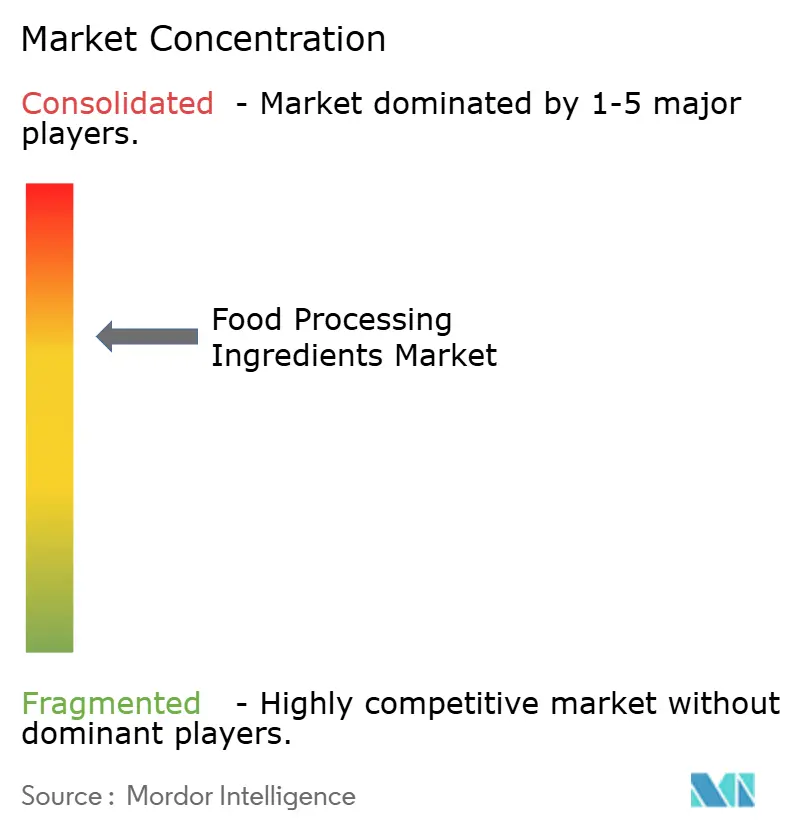

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Processing Ingredients Market Analysis by Mordor Intelligence

The Food Processing Ingredients Market is projected to grow from USD 137.53 billion in 2025 to USD 145.30 billion in 2026 and reach USD 172.65 billion by 2031, registering a CAGR of 3.51% during 2026–2031. The market is experiencing steady growth as food manufacturers increasingly adopt advanced ingredient solutions to improve product quality, processing efficiency, shelf life, nutritional value, and sensory characteristics. Rising production of processed and convenience foods, increasing demand for clean-label formulations, and continuous innovation in functional ingredients are contributing to this growth. Advancements in biotechnology, enzyme engineering, and fermentation technologies are further enabling manufacturers to develop high-performance formulations while supporting more sustainable and efficient food production processes.

Key Report Takeaways

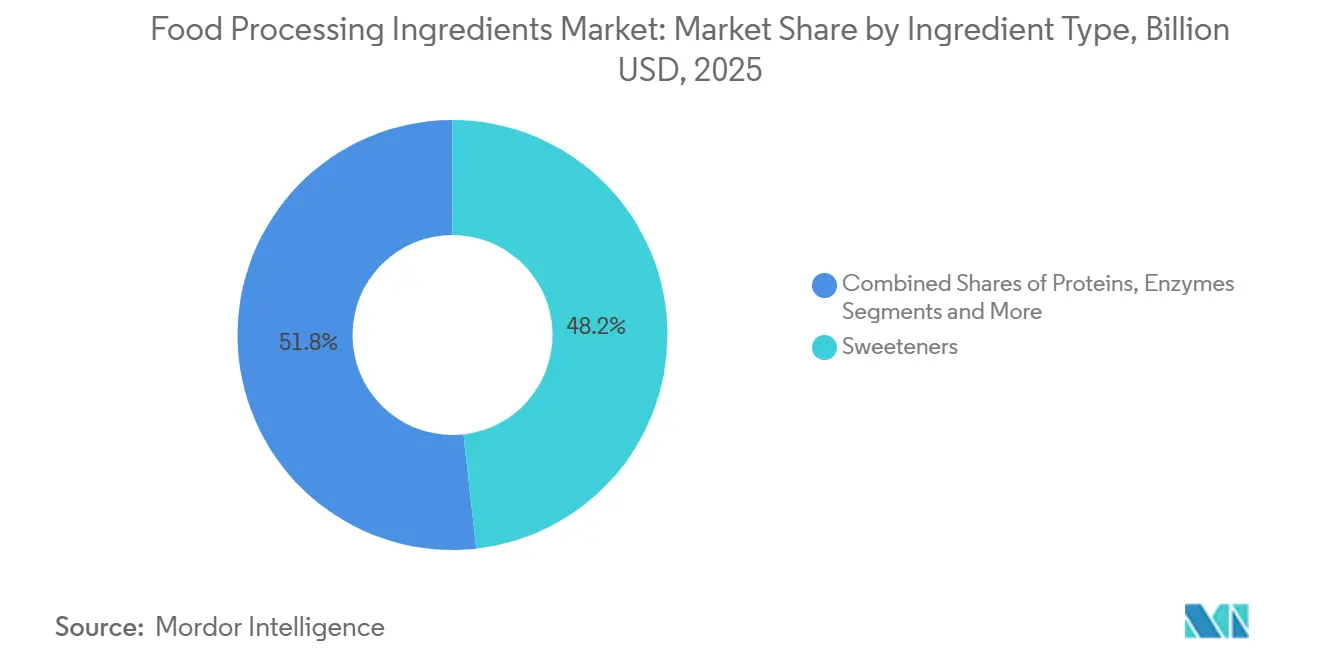

- By ingredient type, sweeteners held 48.23% share in 2025, while enzymes are projected to grow at a 5.23% CAGR through 2031.

- By source, natural ingredients held 57.35% share in 2025, and natural ingredients are also projected to record the fastest 5.95% CAGR through 2031.

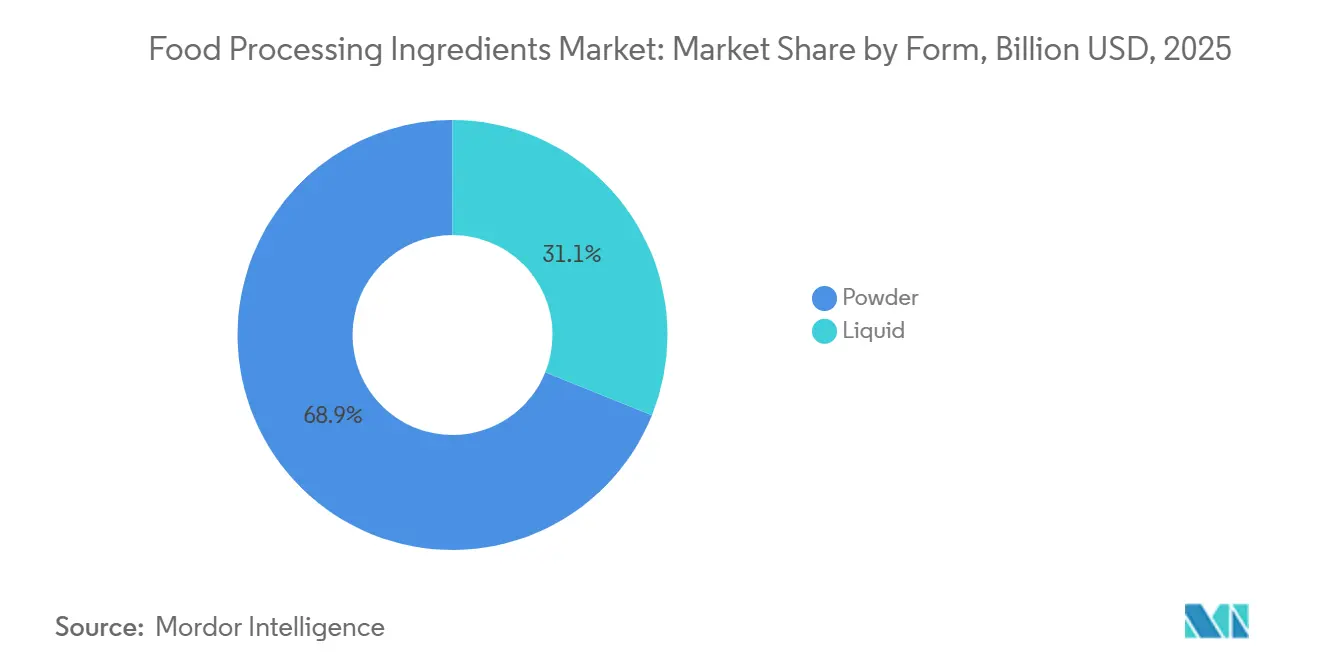

- By form, powder held 68.91% share in 2025, while liquid ingredients are projected to expand at a 4.81% CAGR through 2031.

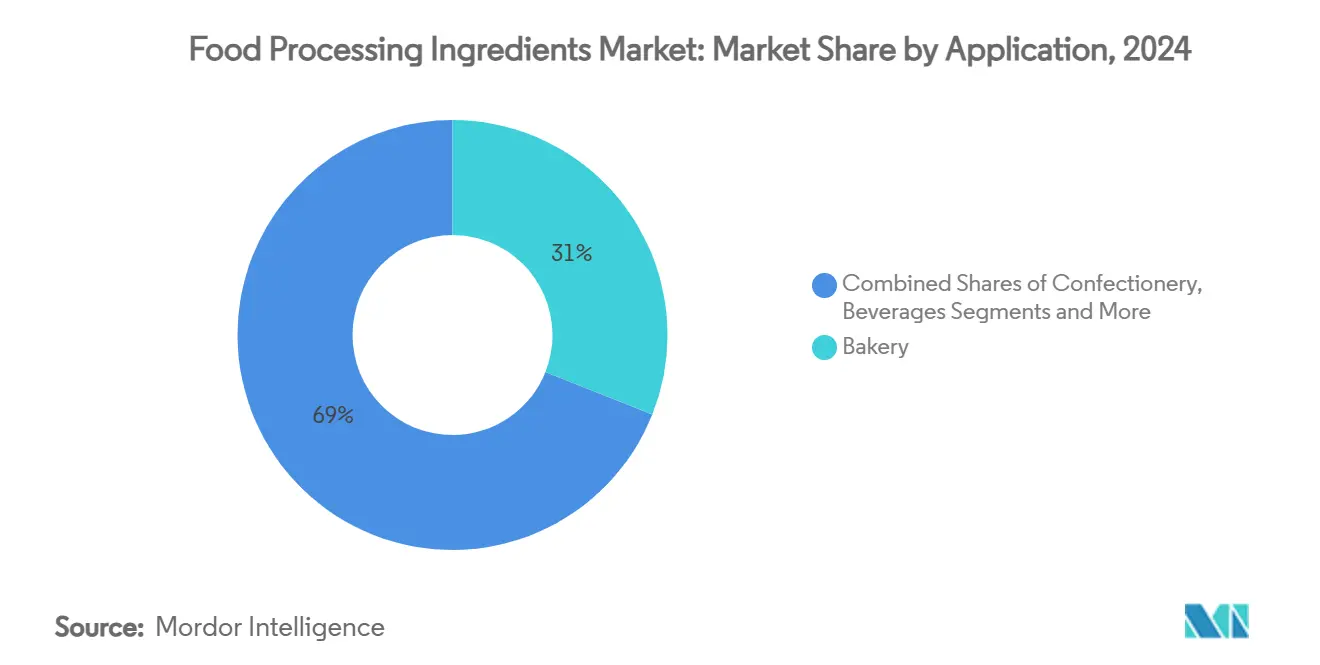

- By application, bakery held 32.06% share in 2025, while convenience and ready meals are projected to grow at a 4.74% CAGR through 2031.

- By geography, Asia-Pacific held 33.45% share in 2025, while South America is projected to expand at a 5.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Food Processing Ingredients Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for processed and convenience foods | +1.0% | Global; strongest in Asia-Pacific and developing markets in Middle-East and Africa | Medium term (2-4 years) |

| Growing consumer preference for clean-label products | +0.6% | Global; led by North America and Europe | Long term (≥ 4 years) |

| Consumer demand for sugar reduction and healthier formulation | +0.5% | Global; led by Europe and North America | Long term (≥ 4 years) |

| Growth in plant-based and alternative protein formulations | +0.4% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Advances in food processing technologies | +0.4% | Global; early adoption concentrated in North America and Europe | Long term (≥ 4 years) |

| Growing emphasis on extending product shelf life | +0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for processed and convenience foods

The rising demand for processed and convenience foods is a major driver of the food processing ingredients market. Manufacturers increasingly rely on functional ingredients to enhance product quality, taste, texture, shelf life, and manufacturing efficiency. Rapid urbanization, changing lifestyles, and the growing preference for ready-to-eat and easy-to-prepare food products are accelerating packaged food production, thereby increasing the consumption of enzymes, preservatives, sweeteners, emulsifiers, flavors, and texturizers. According to the United Nations, 68% of the global population is projected to live in urban areas by 2050 [1]Source: United Nations, "68% of the world population projected to live in urban areas by 2050", un.org. This trend is expected to further increase demand for convenient food options and strengthen the need for food processing ingredients that enable large-scale, consistent, and high-quality food production.

Growing consumer preference for clean-label products

Growing demand for clean-label ingredient solutions is driving the food processing ingredients market as food manufacturers increasingly reformulate products to eliminate artificial additives while maintaining functionality, processing efficiency, and shelf life. This transition is accelerating the adoption of naturally derived enzymes, starches, texturizers, and flavor systems that can deliver equivalent performance to conventional ingredients. Ingredient suppliers are responding by expanding their clean-label portfolios through biotechnology, fermentation, and natural extraction technologies to help manufacturers meet regulatory requirements and product reformulation goals. For instance, Ingredion Incorporated offers the NOVATION range of clean-label functional native starches designed to improve texture, stability, and processing performance in food manufacturing without the use of chemically modified starches.

Growth In plant-based and alternative protein formulations

The rapid growth in plant-based and alternative protein formulations is driving the food processing ingredients market, as food manufacturers increasingly require specialized ingredients to replicate the taste, texture, appearance, and functionality of conventional animal-based products. Plant-based food production relies heavily on functional proteins, starches, hydrocolloids, enzymes, emulsifiers, natural flavors, colors, and binding agents to achieve desirable product characteristics and maintain processing stability. As manufacturers expand their portfolios of plant-based meat, dairy, bakery, and ready-to-eat products, demand for high-performance processing ingredients is increasing to improve formulation efficiency and product consistency. This trend is further supported by rising consumer preference for clean-label and minimally processed foods, prompting ingredient suppliers to develop solutions that meet both functional and labeling requirements.

Growing emphasis on extending product shelf life

The growing emphasis on extending product shelf life is a significant driver of the food processing ingredients market. Food manufacturers seek to reduce food waste, improve distribution efficiency, and maintain product quality across increasingly complex supply chains. Processing ingredients such as natural preservatives, antioxidants, enzymes, antimicrobial cultures, acidity regulators, and stabilizers play a critical role in delaying microbial growth, controlling oxidation, preserving freshness, and maintaining texture, flavor, and nutritional quality during storage and transportation. As global trade expands and cold chain infrastructure varies across regions, the demand for effective shelf-life extension solutions has intensified. Manufacturers distributing products across longer distances and diverse climatic conditions require ingredients that ensure consistent product performance from production to consumption.

Restraints Impact Analysis of Food Processing Ingredients Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food safety and labeling regulations | -0.5% | Global; North America and Europe primarily | Long term (≥ 4 years) |

| Fluctuations in the availability of natural and specialty raw materials | -0.6% | Global; Asia-Pacific and South America supply chains most exposed | Medium term (2-4 years) |

| High formulation and product reformulation costs | -0.4% | Global | Medium term (2-4 years) |

| Ingredient compatibility issues in complex food formulations | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent food safety and labeling regulations

Stringent food safety and labeling regulations restrain the food processing ingredients market by increasing compliance costs, extending product approval timelines, and requiring continuous reformulation of ingredient portfolios. Ingredient manufacturers must invest significantly in safety assessments, toxicological studies, labeling compliance, and regulatory documentation before introducing new ingredients or modifying existing formulations. Evolving regulatory requirements are particularly challenging for ingredient categories transitioning from synthetic to naturally derived alternatives, as manufacturers must demonstrate equivalent safety, functionality, and product performance. For example, under Regulation (EC) No. 1333/2008, the European Food Safety Authority (EFSA) conducts periodic re-evaluations of approved food additives, which can lead to revised usage limits, additional safety requirements, or withdrawal of authorization based on updated scientific evidence.

Fluctuations in the availability of natural and specialty raw materials

Fluctuations in the availability of natural and specialty raw materials restrain the food processing ingredients market by disrupting production continuity, increasing sourcing complexity, and creating uncertainty in ingredient manufacturing. Many food processing ingredients, including natural flavors, colors, starches, plant proteins, hydrocolloids, and botanical extracts, depend on agricultural commodities that are highly vulnerable to adverse weather conditions, crop diseases, seasonal variations, and supply chain disruptions. Variability in the quality and availability of these raw materials can affect ingredient consistency, manufacturing schedules, and long-term supply agreements with food manufacturers. When raw material supplies tighten, ingredient manufacturers face higher procurement costs, longer lead times, and the need to qualify alternative suppliers, all of which add operational complexity and cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Food Processing Ingredients Market Segment Analysis

By Ingredient Type:

Sweeteners Anchor Volume but Enzymes Define the Growth FrontierSweeteners accounted for 48.23% of the food processing ingredients market by value in 2025, reflecting their widespread use across processed food categories, including industrial baking, beverages, and confectionery. High-fructose corn syrup, sucrose, and glucose/dextrose continue to drive volume in bulk food processing, while high-intensity sweeteners, including stevia, monk fruit extract, and sucralose, are gaining formulation share as manufacturers respond to sugar-reduction mandates. Sugar polyols such as erythritol and xylitol are seeing increased uptake in functional confectionery and dental health applications. The scale of the sweeteners segment creates a structural drag on overall market growth, as traditional sugar volumes grow at a modest pace relative to specialty ingredient categories.

Enzymes represent the fastest-growing ingredient category, forecast to advance at a CAGR of 5.23% over 2026–2031. Growth in this segment is driven by increasing adoption of enzyme-based processing solutions that improve manufacturing efficiency, product consistency, and production sustainability. Enzymes allow food manufacturers to optimize processing conditions by accelerating natural biochemical reactions, resulting in higher production yields, reduced processing times, lower energy consumption, and minimized raw material losses. They also enhance product attributes such as texture, flavor development, moisture retention, and stability, while supporting consistent quality across production batches.

By Source:

Natural Dominance Reflects a Structural Formulation TransitionNatural ingredients held 57.35% of the food processing ingredients market by value in 2025 and are forecast to expand at a CAGR of 5.95% during 2026–2031. The segment's growth is driven by the increasing shift toward clean-label food products and the preference for ingredients derived from natural sources, aligned with evolving consumer expectations for transparency and minimal processing. Food manufacturers are increasingly replacing synthetic additives with natural alternatives to maintain functionality such as flavor enhancement, preservation, coloring, and texture improvement, while enhancing product appeal. Natural ingredients also support product differentiation by enabling manufacturers to develop formulations with recognizable ingredient lists and fewer artificial components.

Synthetic ingredients continue to maintain a significant market presence owing to their consistent quality, functional reliability, and cost-effective performance in large-scale food manufacturing. Synthetic ingredients offer precise functionality, enabling manufacturers to achieve standardized taste, texture, color, stability, and shelf-life extension across high-volume production. Their stability under varying processing and storage conditions makes them well suited for complex manufacturing environments where formulation consistency is critical. In addition, synthetic ingredients are often easier to produce at scale, ensuring a dependable supply and reducing variability associated with naturally sourced raw materials. Ongoing innovations in ingredient chemistry are also improving their safety profiles, performance characteristics, and compatibility with modern processing technologies.

By Form:

Powder Remains the Industrial Backbone While Liquid Formats Gain GroundPowder ingredients accounted for 68.91% of the food processing ingredients market by value in 2025. The dominance of this segment is driven by superior storage stability, extended shelf life, ease of handling, and compatibility with large-scale food manufacturing processes. Powdered ingredients are easier to transport and store due to their lower moisture content, which reduces the risk of microbial growth and minimizes preservation requirements. They also enable precise dosing, uniform blending, and better process control, which are essential for maintaining product consistency across production batches. Additionally, powdered formats are versatile and can be readily incorporated into dry mixes or reconstituted during processing, offering manufacturers greater flexibility in formulation.

Liquid ingredients represent the fastest-growing form segment, projected to expand at a CAGR of 4.81% during 2026–2031. Growth in this segment is driven by increasing demand for ingredients that provide rapid dispersion, uniform distribution, and enhanced functionality during food processing. Liquid ingredients simplify production by eliminating additional dissolution or hydration steps, improving manufacturing efficiency and reducing processing time. They offer greater formulation flexibility, enabling accurate mixing, consistent product quality, and better integration into automated processing systems. Advancements in stabilization technologies and aseptic handling have also improved the shelf life and performance of liquid ingredients, supporting their wider adoption in modern food manufacturing.

By Application:

Bakery Sustains Volume Lead While Convenience Meals Redefine Growth DynamicsBakery accounted for a 32.06% share of the global food processing ingredients market by value in 2025. The segment's position is driven by the extensive use of food processing ingredients to enhance product quality and processing efficiency across a wide variety of baked goods. Increasing demand for premium, clean-label, fortified, and gluten-free bakery products is further encouraging manufacturers to develop innovative ingredient formulations that deliver superior taste and texture without compromising production efficiency. Additionally, strong consumer preference for baked snacks, cakes, pastries, breads, and other bakery products continues to sustain ingredient demand. According to the Defra – Department for Environment, Food and Rural Affairs, consumers in the United Kingdom spent an average of 103 pence per person per week on cakes, buns, and pastries in 2024, reflecting sustained consumption of bakery products that supports continued demand for food processing ingredients [2]Source: Department for Environment, Food and Rural Affairs, "Average expenditure per person per week on cakes, buns and pastries in the United Kingdom", gov.uk.

Convenience and ready meals represent the fastest-growing application segment, forecast to expand at a CAGR of 4.74% during 2026–2031. The segment's growth is driven by increasing demand for foods that offer longer shelf life, consistent quality, and minimal preparation time while maintaining desirable taste, texture, and nutritional value. Food processing ingredients play a vital role in preserving freshness, preventing microbial spoilage, enhancing flavor, improving texture, and maintaining product stability throughout processing, storage, and distribution. Manufacturers are increasingly utilizing advanced ingredient solutions to develop products with clean-label claims, improved nutritional profiles, and enhanced sensory characteristics while ensuring compatibility with automated, high-volume production systems.

Geography Analysis

APAC Food Processing Ingredients Market

The Asia-Pacific region demonstrates market leadership with a substantial 36.94% share in 2024. This dominance stems from several key factors, including accelerated industrialization across major economies, significant expansion of middle-class populations, and widespread adoption of processed foods in China, India, and Japan. The region's market position is further strengthened by its robust domestic ingredient production infrastructure, well-established food processing industries, and increasing consumer expenditure on convenience and premium food products. China, in particular, exhibits remarkable growth in its food processing sector, with consumers increasingly gravitating toward healthier and premium food options, which has resulted in enhanced domestic processing capabilities and a growing demand for specialized ingredient imports.

South America Food Processing Ingredients Market

South America has emerged as the most dynamic region in the market, achieving an impressive growth rate of 7.66% CAGR through 2030. This exceptional growth trajectory is underpinned by significant developments in the region's food processing industries, substantial improvements in export capabilities, and a notable increase in domestic consumption of processed foods. The region's rapid advancement reflects its evolving consumer preferences, modernizing food production infrastructure, and increasing integration into global food supply chains.

North America and EMEA Food Processing Ingredients Market

North America and Europe continue to maintain substantial market positions through their advanced processing technologies, rigorous quality standards, and focus on high-value ingredient segments, despite experiencing moderate growth rates due to market maturity and complex regulatory environments. These regions serve as innovation hubs for premium ingredient development, clean-label solutions, and biotechnology applications, establishing benchmarks that eventually influence emerging markets. The Middle East and Africa regions present emerging opportunities driven by demographic growth, accelerating urbanization, and increased investments in food security initiatives. However, their growth potential remains partially constrained by infrastructure limitations and economic fluctuations in certain markets.

Competitive Landscape

The global food processing ingredients market is moderately consolidated, with major players such as Cargill, Incorporated, Archer Daniels Midland Company, Ingredion Incorporated, International Flavors & Fragrances Inc., and Kerry Group plc competing through broad product portfolios, global manufacturing capabilities, and strong technical expertise. Companies are increasingly focusing on developing multifunctional ingredient solutions that improve taste, texture, stability, nutritional value, and processing efficiency while meeting evolving regulatory and clean-label requirements.

Competitive strategies are centered on expanding ingredient portfolios through mergers, acquisitions, strategic partnerships, and capacity expansions to strengthen regional presence and address evolving customer requirements. Major manufacturers continue to invest in biotechnology research and development, enzyme engineering, fermentation technologies, and precision ingredient manufacturing to develop next-generation functional ingredients. Additionally, sustainable sourcing initiatives, traceable supply chains, and environmentally responsible production practices are becoming key competitive differentiators as food manufacturers increasingly prioritize sustainability alongside product performance.

The market continues to offer significant growth opportunities in biotechnology-derived ingredients, natural preservation technologies, clean-label functional ingredients, and advanced formulation solutions that support healthier and more sustainable food products. Growing demand for plant-based foods, sugar and sodium reduction technologies, and ingredients that enhance product shelf life without compromising sensory quality is creating new avenues for innovation. Companies that successfully combine scientific innovation, regulatory expertise, sustainable sourcing, and customized ingredient development are expected to strengthen their competitive position and capture emerging opportunities in the global food processing ingredients market.

Food Processing Ingredients Industry Leaders

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Ingredion Incorporated

-

International Flavors & Fragrances Inc.

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Food Processing Ingredients Market Companies Covered in this Report

- Cargill, Incorporated

- Archer Daniels Midland Company

- Ingredion Incorporated

- International Flavors & Fragrances Inc.

- Kerry Group plc

- Tate & Lyle PLC

- dsm-firmenich AG

- Corbion N.V.

- Bunge Global SA

- Associated British Foods plc

- Givaudan SA

- Novonesis A/S

- BASF SE

- Roquette Freres

- Symrise AG

- Sensient Technologies Corporation

- Takasago International Corporation

- Carbery Group Ltd

- Merck KGaA

- GNT Group B.V.

Recent Industry Developments in Food Processing Ingredients Market

- April 2026: Kerry Group opened its expanded biotechnology manufacturing facility in Carrigaline, Co. Cork, significantly increasing its capacity to produce lactase enzymes at industrial scale.

- April 2026: Symrise opened its upgraded Food and Beverage site in Parets del Vallès, near Barcelona. The investment expands capacity for powdered food and beverage solutions and strengthens application expertise, connecting Southern Europe with Africa and the Middle East.

- February 2026: Roquette launched NUTRALYS Pea 850F, a pea protein isolate designed to improve sensory performance in plant-based formulations. Developed to address common formulation challenges, this ingredient enables food and beverage manufacturers to create plant-based alternatives with cleaner, more neutral taste profiles.

Global Food Processing Ingredients Market Report Scope

Food processing ingredients are the raw materials, additives, and intermediate components used to manufacture, preserve, and flavor commercial food products. The food processing ingredients market is segmented by ingredient type, source, form, application, and geography. Based on ingredient type, the market is segmented into starches and texturizers, proteins, enzymes, sweeteners, flavors, colorants, emulsifiers, preservatives, and others. Based on source, the market is segmented into natural and synthetic. Based on form, the market is segmented into powder and liquid. Based on application, the market is segmented into bakery, confectionery, meat, poultry and seafood, dairy and frozen desserts, beverages, convenience and ready meals, and others. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

Segmentation Overview

| Starches and Texturizers | ||

| Proteins | ||

| Enzymes | ||

| Sweeteners | Traditional Sugar | Sucrose |

| High-Fructose Corn Syrup (HFCS) | ||

| Glucose/Dextrose | ||

| Others | ||

| Sugar Polyols | Sorbitol | |

| Maltitol | ||

| Xylitol | ||

| Erythritol | ||

| Others | ||

| High Intensity Sweeteners | Aspartame | |

| Sucralose | ||

| Stevia | ||

| Monk Fruit Extract | ||

| Others | ||

| Rare and Novel Sugar | ||

| Others | ||

| Flavors | ||

| Colorants | ||

| Emulsifiers | ||

| Preservatives | ||

| Others | ||

| Natural |

| Synthetic |

| Powder |

| Liquid |

| Bakery |

| Confectionery |

| Meat, Poultry and Seafood |

| Dairy and Frozen Desserts |

| Beverages |

| Convenience and Ready Meals |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Ingredient Type | Starches and Texturizers | ||

| Proteins | |||

| Enzymes | |||

| Sweeteners | Traditional Sugar | Sucrose | |

| High-Fructose Corn Syrup (HFCS) | |||

| Glucose/Dextrose | |||

| Others | |||

| Sugar Polyols | Sorbitol | ||

| Maltitol | |||

| Xylitol | |||

| Erythritol | |||

| Others | |||

| High Intensity Sweeteners | Aspartame | ||

| Sucralose | |||

| Stevia | |||

| Monk Fruit Extract | |||

| Others | |||

| Rare and Novel Sugar | |||

| Others | |||

| Flavors | |||

| Colorants | |||

| Emulsifiers | |||

| Preservatives | |||

| Others | |||

| By Source | Natural | ||

| Synthetic | |||

| By Form | Powder | ||

| Liquid | |||

| By Application | Bakery | ||

| Confectionery | |||

| Meat, Poultry and Seafood | |||

| Dairy and Frozen Desserts | |||

| Beverages | |||

| Convenience and Ready Meals | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the expected value of the food processing ingredients market by 2031?

The food processing ingredients market is projected to reach USD 172.65 billion by 2031, rising from USD 145.30 billion in 2026 at a 3.51% CAGR over 2026-2031.

What was the size of the food processing ingredients market in 2025 and 2026?

The food processing ingredients market stood at USD 137.53 billion in 2025 and is valued at USD 145.30 billion in 2026.

Which region led the food processing ingredients market in 2025?

Asia-Pacific led the food processing ingredients market with a 33.45% share in 2025.

Which region is expected to grow the fastest through 2031?

South America is forecast to register the fastest growth, with a 5.58% CAGR over 2026-2031.

Page last updated on: