Programmatic Job Advertising Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

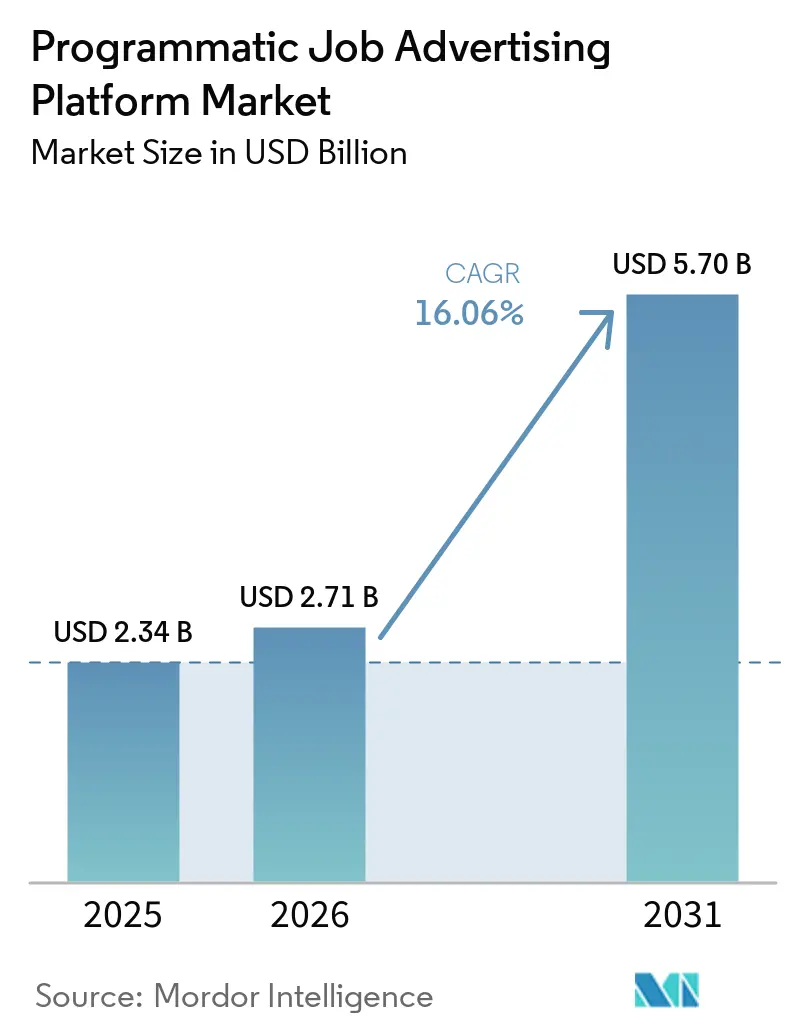

| Market Size (2026) | USD 2.71 Billion |

| Market Size (2031) | USD 5.70 Billion |

| Growth Rate (2026 - 2031) | 16.06% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Programmatic Job Advertising Platform Market Analysis by Mordor Intelligence

The programmatic job advertising platform market size is projected to expand from USD 2.34 billion in 2025 and USD 2.71 billion in 2026 to USD 5.70 billion by 2031, registering a CAGR of 16.06% between 2026 to 2031. Recruiters are migrating budgets from manual postings toward AI-orchestrated, performance-priced campaigns that optimize spend around cost per qualified applicant, freeing recruiter capacity for candidate engagement. Growing privacy regulation and third-party cookie loss are steering platforms toward first-party data integrations, contextual placements, and direct integrations with job boards. Large enterprises continue to anchor demand, yet cloud-native self-service options are lowering entry barriers for smaller firms that now demand outcome-based pricing and real-time attribution. Competitive pressure is intensifying as incumbent vendors embed conversational AI and predictive analytics that refine bid decisions and improve candidate quality at scale.

Key Report Takeaways

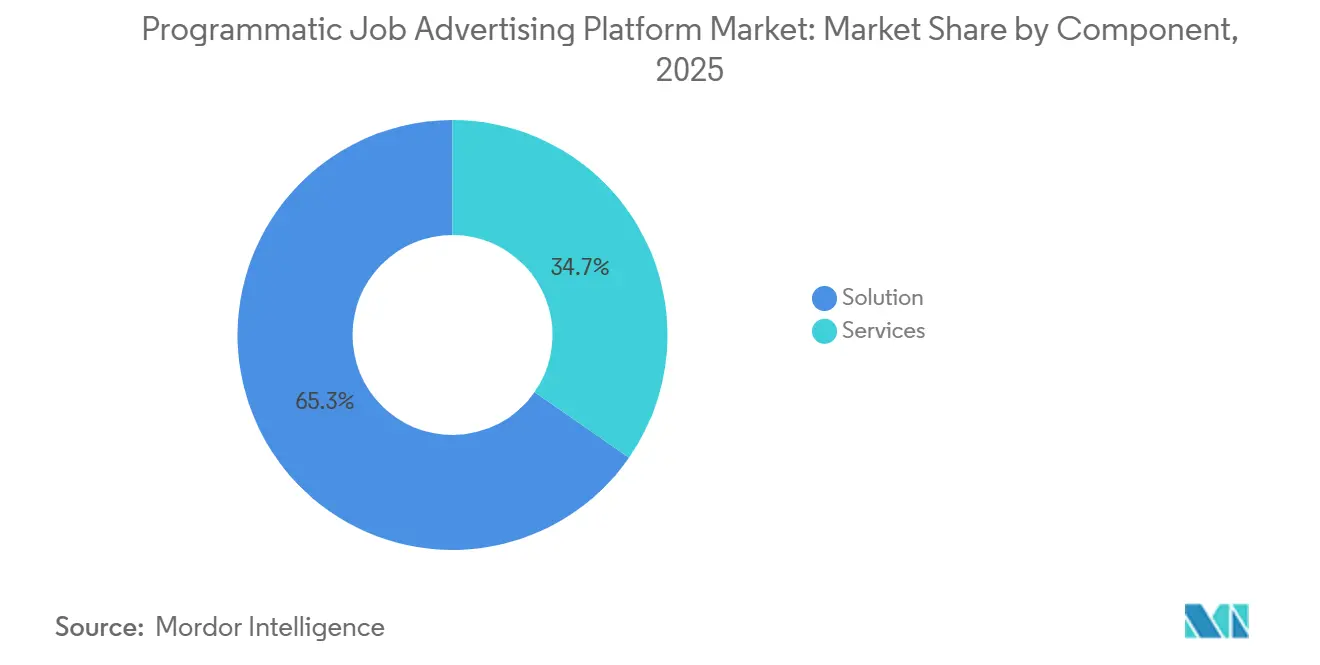

- By component, solution offerings led with 65.33% revenue in 2025, while services are advancing at a 19.03% CAGR through 2031 as employers seek managed campaigns and privacy-compliant integrations.

- By deployment mode, on-premise installations held 58.45% of 2025 revenue, but cloud platforms are expanding at an 18.35% CAGR thanks to rapid implementation and continuous feature delivery.

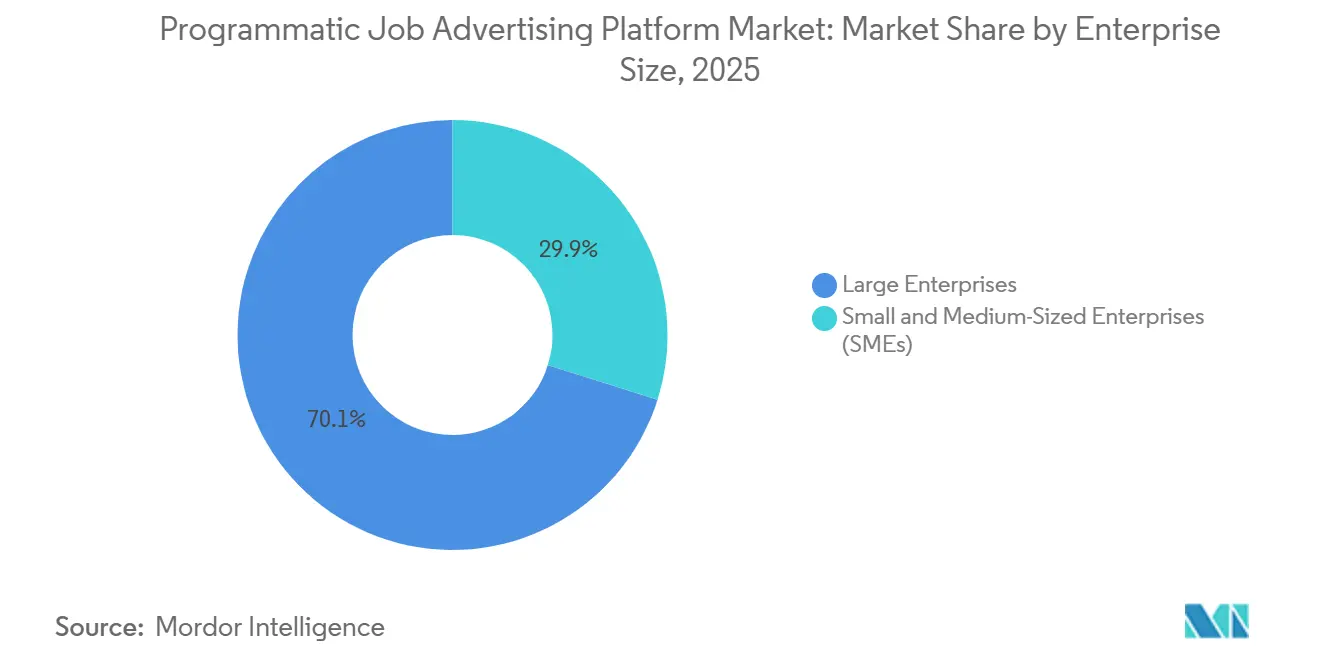

- By enterprise size, large organizations generated 70.14% of 2025 sales, yet small and medium-sized enterprises are growing at an 18.66% CAGR as self-service tools reduce minimum spend and automate job distribution.

- By industry vertical, IT and telecom produced 36.44% of 2025 demand, while healthcare is forecast to achieve the fastest 17.92% CAGR as hospitals rely on qualified-candidate pricing to mitigate nursing shortages.

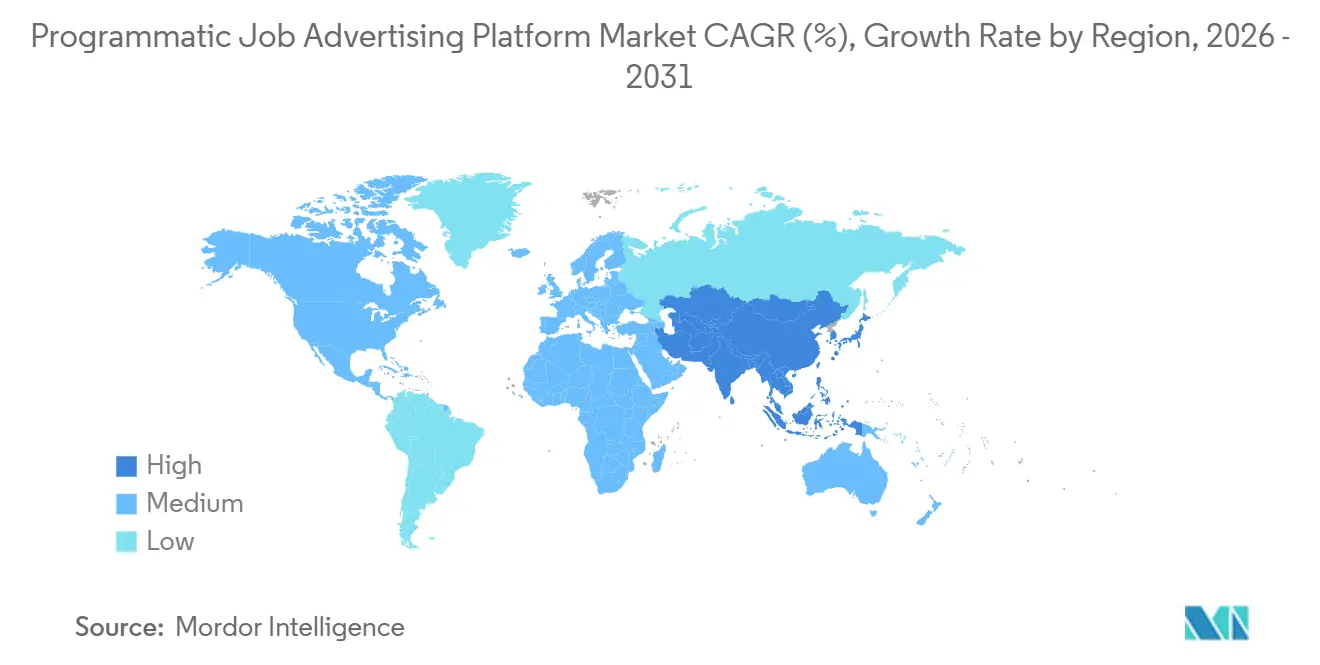

- By geography, North America commanded 38.52% share in 2025, whereas Asia-Pacific is projected to record a 17.43% CAGR on the back of soaring AI adoption across India, Singapore, and Australia.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Programmatic Job Advertising Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Programmatic Shift Toward Performance-Based Recruitment Advertising | +4.2% | Global with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Growing Adoption of AI-Driven Talent Acquisition Workflows | +3.8% | Asia-Pacific, North America, Europe | Short term (≤2 years) |

| Tight Labor Markets in Specialized Skills Segments | +3.1% | North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Rising Importance of Employer Branding Across Digital Channels | +2.4% | Global, most visible in tech and healthcare hiring hubs | Medium term (2-4 years) |

| Emergence of Unified Omnichannel Recruitment Campaign Management | +1.6% | North America and Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| Proliferation of Privacy-Compliant First-Party Data Partnerships With Job Boards | +1.3% | North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Programmatic Shift Toward Performance-Based Recruitment Advertising

Employers are reallocating budgets toward platforms that charge only for completed applications, a change that cut cost-per-qualified-candidate by 15% and reduced time-to-fill by 25% in deployments combining automated quality tracking with programmatic bidding.[1]Appcast, “News and Press,” appcast.ioThe ability to distribute vacancies across thousands of boards and halt spend on under-performing sources enables recruiters to redeploy 38% of the time previously spent on manual posting toward candidate engagement.

Growing Adoption of AI-Driven Talent Acquisition Workflows

Eighty-four percent of talent acquisition leaders plan to deploy agentic AI by 2026, with Asia-Pacific showing recruiter AI uptake above 75% in India, Singapore, and Australia. Conversational bots embedded in programmatic platforms now screen and schedule around the clock in more than 100 languages, trimming manual coordination by over 90% for Radancy clients.

Tight Labor Markets in Specialized Skills Segments

U.S. job-opening rates for technical roles kept average time-to-fill above 55 days in early 2026, while BLS data showed healthcare adding 76,000 jobs in March 2026 alone, reinforcing persistent demand for qualified talent. Employers unable to wait out lengthy vacancies are adopting programmatic bidding tools that target passive candidates in niche forums and benchmark wages against real-time data feeds from ATS integrations.

Rising Importance of Employer Branding Across Digital Channels

Appcast’s 2025 brand marketing module links upper-funnel awareness campaigns to downstream application quality, giving talent teams the analytics they need to justify brand spend. Generation Z’s preference for flexibility and development opportunities over base salary has prompted recruiters to A/B-test value-proposition messaging within programmatic creatives, elevating employer branding from a soft initiative to a quantifiable lever.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cookie Deprecation Impact on Audience Targeting Accuracy | -2.8% | North America and Europe | Short term (≤2 years) |

| Persistent Data Silos Across ATS and Programmatic Platforms | -2.1% | Global mid-market enterprises | Medium term (2-4 years) |

| Inflation-Driven Hiring Freezes in Key End-Use Industries | -1.4% | North America and Europe | Short term (≤2 years) |

| Escalating Publisher Floor Prices on High-Traffic Job Boards | -0.9% | Global tech and healthcare hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cookie Deprecation Impact on Audience Targeting Accuracy

Chrome’s phase-out of third-party cookies is eroding behavioral targeting signals, and California’s Automated Decision-Making Technology rules now require fresh privacy assessments for algorithmic tools, raising vendor compliance costs. Platforms that integrate first-party ATS data and server-side conversion tracking are mitigating signal loss but smaller vendors lacking engineering depth risk margin compression.

Persistent Data Silos Across ATS and Programmatic Platforms

Legacy on-premise ATS deployments often limit API access, delaying feedback loops essential for real-time bid adjustments. The U.S. Chamber of Commerce Foundation’s Jobs and Employment Data Exchange is drafting common schemas, yet adoption remains voluntary. Until standards mature, employers depend on managed-service models that warehouse candidate data and surface compliant attribution dashboards, adding cost and slowing self-service expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Complexity Rises

Services represented 34.67% of the Programmatic job advertising platform market in 2025, but their 19.03% CAGR through 2031 signals a decisive pivot toward outcome-linked campaign management and privacy consulting. Buyers lean on vendor teams for ATS mapping, taxonomy harmonization, and quality-of-hire analytics that validate spending. Implementation packages often run parallel with change-management programs that reskill recruiters for data-driven workflows. Managed-service offerings have widened as Appcast and Radancy incorporate search, social, and video interviewing, creating bundled propositions attractive to resource-strained talent teams.

Software licenses will keep anchoring topline revenue, yet services are evolving from optional extras into indispensable accelerators of time-to-value. Enterprises facing multi-country regulatory regimes rely on vendor experts to localize consent flows and bias documentation. As a result, services revenue is poised to contribute a larger slice of the Programmatic job advertising platform market size even while software margins remain stable.

By Deployment Mode: Cloud Gains as Scalability Trumps Control

On-premise environments retained a majority 58.45% share in 2025 because financial services and healthcare employers prefer in-house custody of candidate data. However, cloud platforms grew almost triple the overall market thanks to elastic capacity, zero-downtime upgrades, and API-level connections to large publisher ecosystems. Vendors now default to cloud-native releases, ensuring parity of features and security patches across their entire user base.

Hybrid adoption is rising, with sensitive applicant records remaining on internal servers while bid optimization, reporting, and AI agents execute in the vendor cloud. California’s new audit-trail obligations make centralized logging easier in software-as-a-service environments, nudging risk-averse sectors toward at least partial cloud usage. This interplay of regulatory pressure and product innovation is widening the total addressable Programmatic job advertising platform market without compromising data sovereignty.

By Enterprise Size: SMEs Adopt as Barriers Fall

Large employers generated over two-thirds of platform revenue in 2025, propelled by multi-language campaigns that span hundreds of boards. Even so, small and medium-sized firms now contribute the fastest growth as pay-as-you-go billing meets hiring-on-demand cycles. Self-service dashboards guide non-specialist recruiters through campaign setup in minutes, while integrated AI agents propose bid ceilings calibrated to budget constraints.

SMEs gain levered returns because automation covers posting, performance analysis, and budget reallocation, duties that would otherwise demand scarce staff. Joveo’s AI Maturity Model, rolled out in 2025, exemplifies a prescriptive onboarding toolkit targeted at this cohort. As entry hurdles lower, the SME share of the Programmatic job advertising platform market size will progressively erode enterprise dominance, deepening the user base and diversifying use cases.

By Industry Vertical: Healthcare Leads Growth Amid Shortages

Tech employers accounted for 36.44% of 2025 spending, yet tight clinician supply is accelerating healthcare uptake. U.S. hospitals added 15,000 positions in March 2026 and continue to struggle with nursing gaps, catalyzing investments in performance-priced job ads that guarantee qualified applicant flow.[2]U.S. Bureau of Labor Statistics, “Employment Situation News Release,” bls.gov Platforms fine-tune bids toward licensed professionals across state lines and embed flexibility messaging that resonates with shift-based roles.

Manufacturing, logistics, and construction are also expanding usage as blue-collar sourcing becomes data-driven. Vendors that map skills taxonomies and integrate wage-benchmark alerts are positioned to capture vertical diversification. The interplay of chronic skill scarcity and programmatic precision will keep the healthcare and industrial cohorts at the forefront of Programmatic job advertising platform market growth.

Geography Analysis

North America generated 38.52% of 2025 revenue, underpinned by the world’s most mature ATS ecosystem and early adoption of AI-driven recruitment marketing. BLS figures indicate the region maintained unemployment near a tight 3.8% in early 2026, sustaining employer urgency despite isolated hiring slowdowns in financial services. Federal employment reductions trimmed public-sector demand, yet technology and healthcare hiring pipelines remain resilient.

Asia-Pacific is forecast to post a 17.43% CAGR as India, Singapore, and Australia display recruiter AI adoption rates above 75%, outpacing global benchmarks. High application volumes per posting compel employers to rely on automated quality scoring to sift candidates, making programmatic tools central to recruiter workflow. Startups in Bengaluru and Sydney are piloting outcome-based pricing that pays vendors only for hires, demonstrating the region’s willingness to experiment with aggressive commercial models.

Europe’s trajectory is shaped by balanced regulation and AI optimism. A European Central Bank survey of 5,000 firms showed AI adopters were 4 percentage points more likely to expand headcount, indicating complementarity with job creation rather than substitution.[3]European Central Bank, “Artificial Intelligence: Friend or Foe for Hiring in Europe Today?” ecb.europa.euThe continent’s stringent GDPR regime continues to steer vendors toward privacy-by-design architectures that are now being exported to other regions. South America, Middle East, and Africa represent emerging corridors where mobile-first hiring and government digitalization programs will gradually lift adoption, though informal labor structures still limit immediate scale.

Competitive Landscape

The Programmatic job advertising platform market features moderate fragmentation. Leaders such as Appcast, Joveo, and Radancy differentiate on AI maturity, depth of ATS integrations, and global publisher reach. Radancy’s 2025 acquisition of myInterview added video interviewing to its cloud suite, cutting client time-to-hire by more than 70%. Appcast’s connected layer, AppcastEngage, launched in late 2025, now tracks the full applicant journey, positioning the vendor for end-to-end attribution.

Midsize challengers emphasize vertical specialization or white-label alignments with staffing firms. PandoLogic’s integration of conversational AI through earlier acquisitions enables fully automated screening, while Broadbean competes on breadth of board connections and legacy ATS connectivity. Compliance readiness has emerged as a new battleground: platforms offering turnkey bias-audit reports and CCPA audit logs are edging out rivals with opaque models.

Outcome-based commercial terms are reshaping buyer expectations. Vendors comfortable underwriting campaign performance rely on extensive historic datasets and diversified traffic portfolios to manage risk, erecting scale barriers against newcomers. Nevertheless, blue-collar and gig-economy recruitment remains underpenetrated, leaving room for disruptors that combine geofenced mobile ads with instant-messaging engagement to reach hourly workers. As feature sets converge, brand equity built on transparent metrics and rapid customer success response times is becoming a decisive loyalty driver.

Programmatic Job Advertising Platform Industry Leaders

Appcast, Inc.

Joveo, Inc.

PandoLogic, Inc.

Talroo, Inc.

Recruitics, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Joveo acquired We Are Yoke, expanding European managed-service capabilities and reinforcing its platform-plus-services strategy.

- February 2026: Joveo launched Ask Joveo, a natural-language analytics agent that delivers predictive forecasts and ROI recommendations inside its talent intelligence suite.

- February 2026: Appcast issued its 10th Recruitment Marketing Benchmark Report, adding candidate disposition metrics to guide performance optimization.

- September 2025: Radancy bought myInterview, integrating video assessments and conversational scheduling into its Talent Acquisition Cloud.

Global Programmatic Job Advertising Platform Market Report Scope

Automated recruitment advertising tools dominate the Programmatic Job Advertising Platform Market, employing algorithms and AI for real-time bidding to optimize job ad placements. These platforms adeptly allocate budgets, pinpoint ideal candidates, and modify campaigns based on performance metrics, all to reduce cost-per-applicant and boost hiring efficiency. By integrating with ATS platforms, programmatic systems offer a cohesive view of sourcing analytics and campaign reports. The market's expansion is driven by the automation of recruitment, a scarcity of talent, and a demand for performance-centric media buying.

The Programmatic Job Advertising Platform Market Report is Segmented by Component (Solution, and Services), Deployment Mode (Cloud-Based, and On-Premise), Enterprise Size (Small and Medium-Sized Enterprises [SMEs], and Large Enterprises), Industry Vertical (IT and Telecom, Banking, Financial Services and Insurance [BFSI], Healthcare, Retail and E-Commerce, Manufacturing, and Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solution | |

| Services | Implementation Services |

| Managed Services | |

| Support and Maintenance Services |

| Cloud-Based |

| On-Premise |

| Small and Medium-Sized Enterprises (SMEs) |

| Large Enterprises |

| IT and Telecom |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare |

| Retail and E-Commerce |

| Manufacturing |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Solution | |

| Services | Implementation Services | |

| Managed Services | ||

| Support and Maintenance Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| By Enterprise Size | Small and Medium-Sized Enterprises (SMEs) | |

| Large Enterprises | ||

| By Industry Vertical | IT and Telecom | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare | ||

| Retail and E-Commerce | ||

| Manufacturing | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current Programmatic job advertising platform market size and how fast will it grow by 2031?

The Programmatic job advertising platform market size is projected to expand from USD 2.34 billion in 2025 and USD 2.71 billion in 2026 to USD 5.70 billion by 2031, reflecting a 16.06% CAGR over 2026-2031 (Mordor Intelligence).

Which component category is expanding fastest through 2031?

Services are advancing at a 19.03% CAGR as employers seek managed campaigns and compliance support, outpacing standalone software solutions (Mordor Intelligence).

Why is Asia-Pacific expected to lead regional growth?

Recruiter AI adoption rates exceed 75% in India, Singapore, and Australia, driving a 17.43% CAGR as employers automate screening and optimize bids at scale.

How are privacy regulations influencing platform strategy?

California CCPA and similar rules are pushing vendors to embed audit logging, shift toward first-party data, and offer turnkey bias-mitigation reporting to reduce compliance risk.

Which industry vertical is forecast to experience the highest growth rate?

Healthcare is projected to post a 17.92% CAGR as hospitals rely on guaranteed qualified-candidate flows to close clinician gaps (Mordor Intelligence).

Page last updated on: