Sales Enablement Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.04 Billion |

| Market Size (2031) | USD 12.35 Billion |

| Growth Rate (2026 - 2031) | 19.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

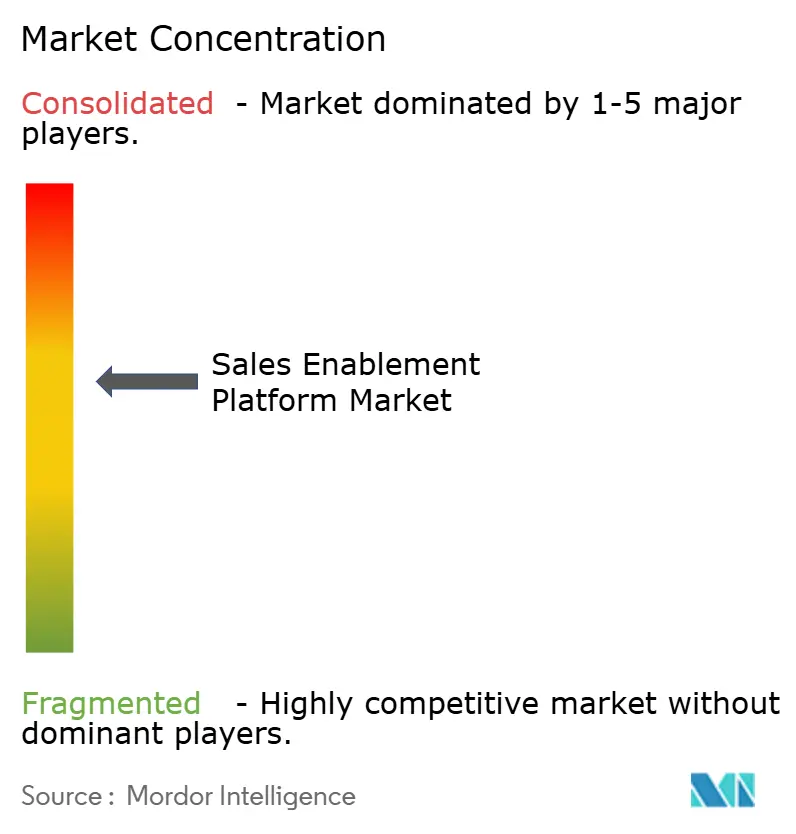

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sales Enablement Platform Market Analysis by Mordor Intelligence

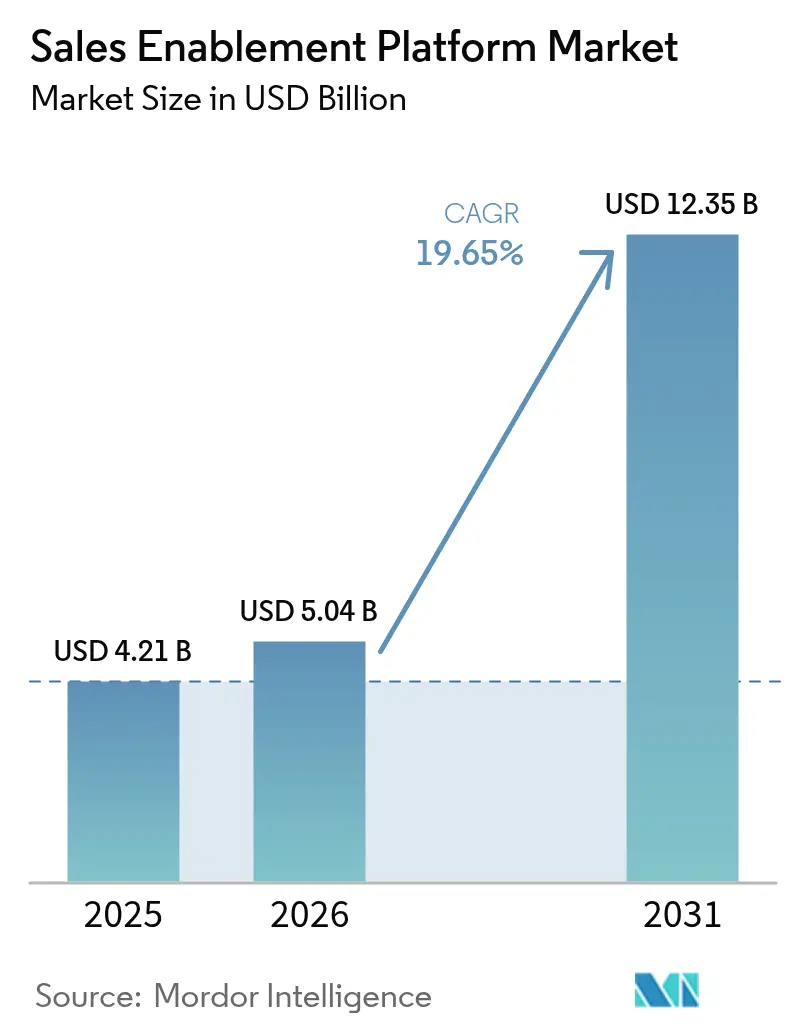

The sales enablement platform market size was valued at USD 4.21 billion in 2025 and estimated to grow from USD 5.04 billion in 2026 to reach USD 12.35 billion by 2031, at a CAGR of 19.65% during the forecast period (2026-2031). The up-swing is driven by enterprises replacing activity-based selling with AI-orchestrated revenue workflows, the normalization of hybrid workforces, and intensifying pressure on sales-productivity metrics. Platform vendors that embed generative AI, real-time analytics and copilots now position their solutions as strategic revenue engines rather than utility software, widening the gap between innovators and feature-parity followers. Cloud deployment continues to dominate because it delivers the elastic compute required for large-language-model workloads while removing infrastructure friction for both large enterprises and resource-constrained SMEs. Private-equity-backed consolidation is compressing the vendor landscape, accelerating the shift toward end-to-end revenue orchestration suites that collapse previously siloed martech and sales tech categories. [1]Seismic Software Inc., “Seismic achieves record growth fuelled by customer momentum,” seismic.com

Key Report Takeaways

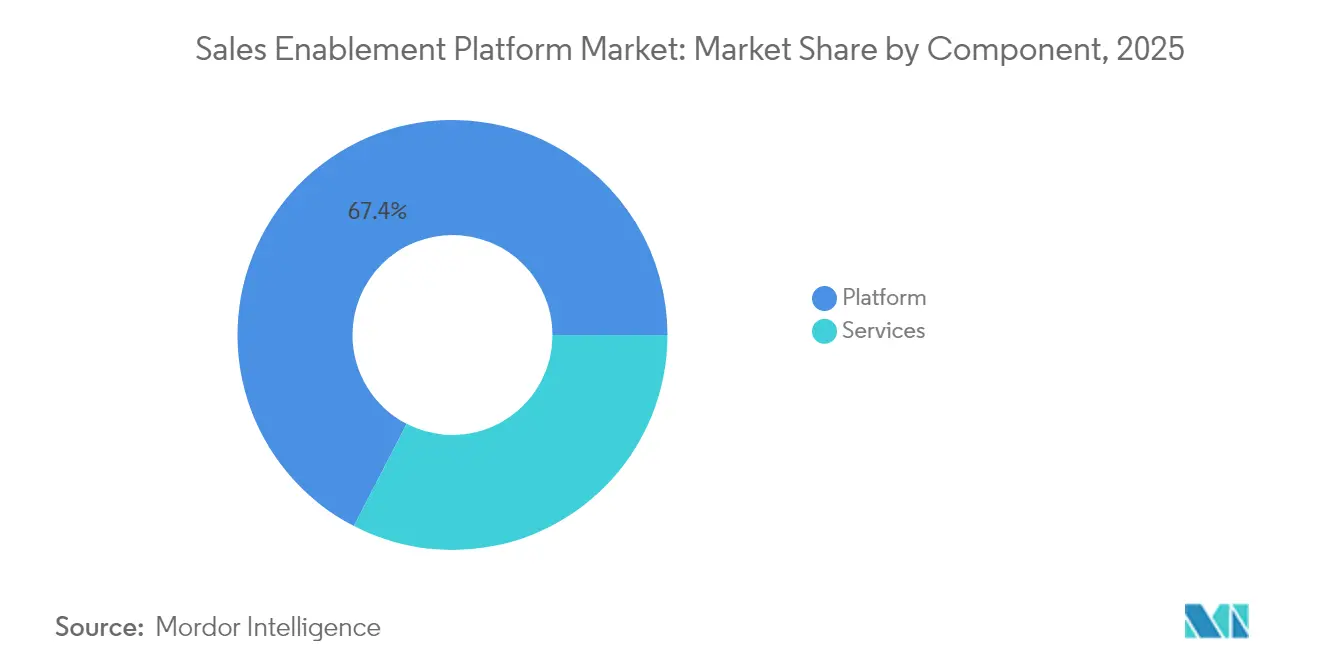

- By component, platform software held 67.42% of the sales enablement platform market share in 2025, while services are forecast to grow the fastest at a 24.2% CAGR through 2031.

- By organization size, large enterprises commanded 58.31% of revenue in 2025; small and medium enterprises are projected to expand at a 26.6% CAGR, more than double the overall sales enablement platform market CAGR.

- By deployment mode, cloud solutions accounted for 82.18% of the sales enablement platform market size in 2025 and are set to rise at a 22.8% CAGR to 2031.

- By industry vertical, IT & telecom led with 21.08% revenue share in 2025, whereas healthcare and life sciences are advancing at the fastest 23.9% CAGR to 2031.

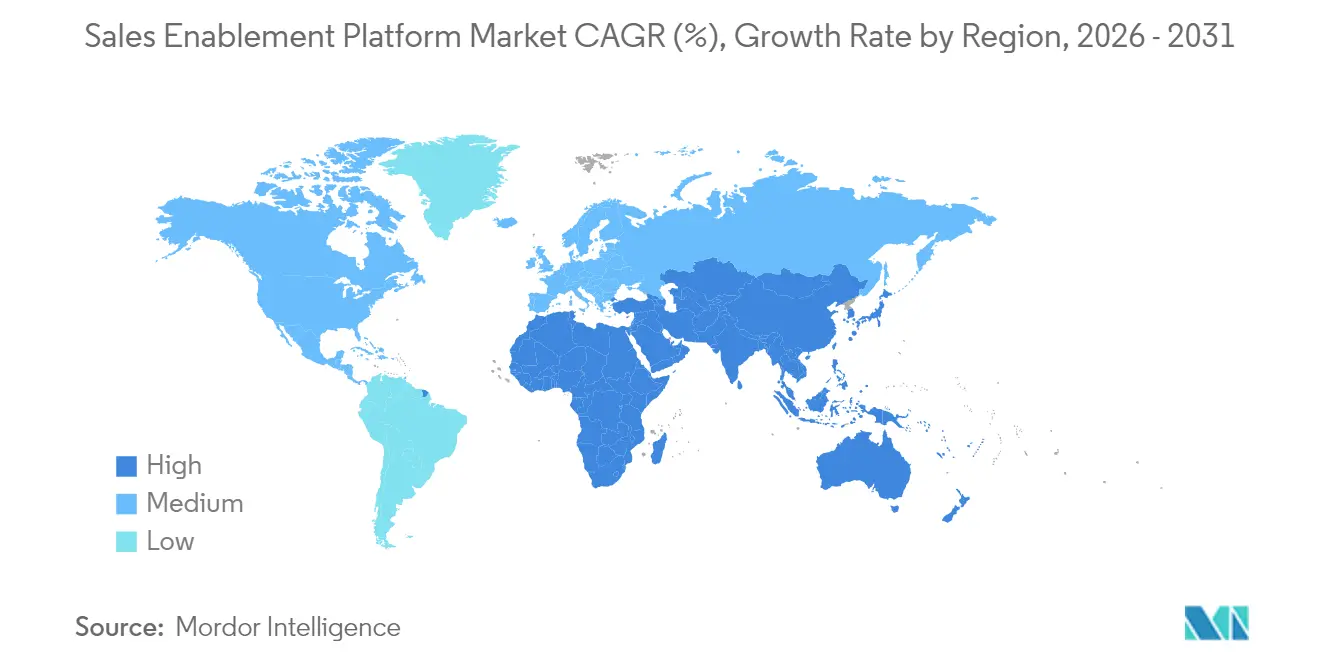

- By geography, North America retained 42.70% of global revenue in 2025; Asia-Pacific is the fastest-growing region at a 21.8% CAGR through 2031.

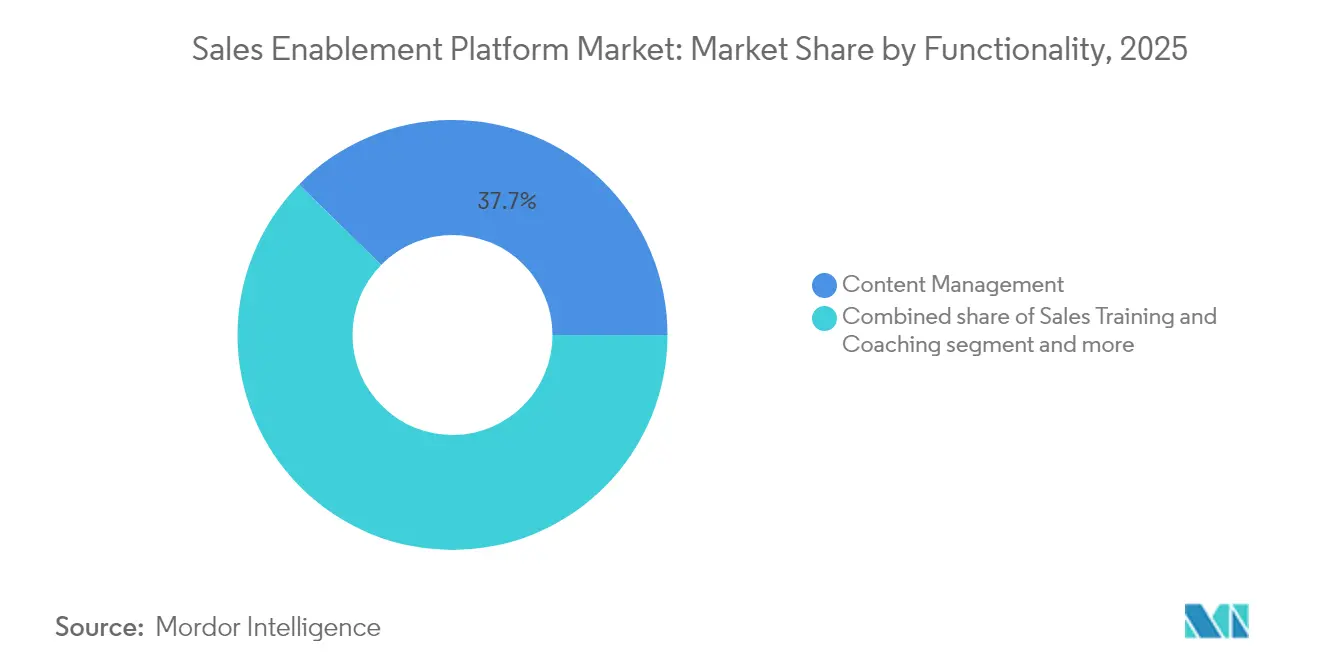

- By functionality, content management is the largest segment, yet analytics and reporting are the fastest-expanding sub-segment through 2031.

- Seismic, Highspot, Bigtincan, Salesloft and Drift together represent an estimated 45% of global revenue, signalling a moderately concentrated landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sales Enablement Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift to insight-driven selling workflows | 4.20% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Surge in hybrid/remote sales teams post-COVID | 3.80% | Global, particularly strong in APAC & North America | Short term (≤ 2 years) |

| Integration of AI copilots and Gen-AI content automation | 5.10% | North America & EU leading, APAC following | Medium term (2-4 years) |

| Vendor consolidation across martech and salestech stacks | 2.90% | Global, driven by North America & EU markets | Long term (≥ 4 years) |

| ISO/IEC 42001 AI-management standard de-risks adoption | 1.70% | EU & North America primarily, expanding to APAC | Long term (≥ 4 years) |

| EU "Right-to-disconnect" laws amplify need for asynchronous seller enablement | 1.40% | EU primarily, with spillover to other regulated markets | Medium term (2-4 |

| Source: Mordor Intelligence | |||

Rapid shift to insight-driven selling workflows

Revenue teams are retiring generic activity metrics and adopting AI insights that map seller actions to deal progress. Platforms ingest clickstream, CRM and conversation data to recommend next-best actions, boosting pipeline generation by 15% and seller efficiency by 33% for Docket AI clients. Adoption is strongest in technology, BFSI and professional-services firms where buyers demand data-grounded value propositions. [2]Docket AI, “Clone your best sales engineers!,” docketai.com

Surge in hybrid/remote sales teams post-COVID

Permanent hybrid models heighten demand for asynchronous enablement that spans time zones and devices. Platforms now embed micro-learning, role-based content tips and short video coaching that sellers can access on demand. Spekit deepened its “just-in-time enablement” play by acquiring Cquence to surface CRM-extracted insights mid-call. Flexible training reduces ramp time without sacrificing compliance tracking. [3]Spekit, “Spekit Acquires AI Startup Cquence Ushering a New Era of Enablement Intelligence,” spekit.com

Integration of AI copilots and Gen-AI content automation

Generative AI evolved from pilot features to table-stakes functionality. Embedded language models auto-draft emails, personalize collateral and predict deal win-likelihood within sellers’ workflow. GTM Buddy users report 50% higher lead conversion and 30% productivity gains after activating AI copilots. Model quality, guardrails against hallucinations and proprietary data sets are key differentiation levers.

European regulations limiting after-hours contact push sales teams toward asynchronous communications and coaching. Enablement platforms that facilitate self-paced learning and auto-generated recaps align with labour-policy mandates, boosting vendor traction in France, Germany and Spain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget compression amid SaaS rationalization | -3.20% | Global, particularly acute in North America & EU | Short term (≤ 2 years) |

| Fragmented CRM and CMS ecosystems hamper data quality | -2.10% | Global, with varying intensity by market maturity | Medium term (2-4 years) |

| Rising Gen-AI hallucination risk triggers stricter IT governance | -1.80% | North America & EU primarily, expanding globally | Medium term (2-4 years) |

| Seller resistance to in-workflow micro-coaching alerts | -1.30% | Global, with cultural variations by region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Budget compression amid SaaS rationalization

CFOs scrutinize software portfolios as SaaS inflation climbs to 11.3%. Vertice finds 45.7% of paid licenses idle, compelling finance teams to demand clear ROI before renewal. Enablement vendors now lead with revenue attribution dashboards showing lift in win-rates and cycle times.

Fragmented CRM and CMS ecosystems hamper data quality

Many enterprises operate multiple CRMs and content repositories following acquisitions, hindering AI model performance. Implementation timelines lengthen when 60-70% of effort goes to data cleansing. Vendors with robust APIs and data-normalization layers gain an edge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform dominance drives service innovation

Platform software held 67.42% of the sales enablement platform market in 2025, reflecting enterprise preference for unified suites that embed content, engagement and analytics in one interface. Services revenue is growing at a 24.2% CAGR as organizations seek expertise in AI model tuning, workflow redesign and change management. Vendors increasingly bundle advisory retainers for continuous optimization, converting one-off projects into subscription-like annuities. This shift widens total contract value and deepens customer lock-in.

The services segment benefits from the complexity of generative-AI deployments that require careful prompt engineering, domain-specific model fine-tuning and ethical-use policies. Specialist partners now train client administrators on governing hallucination risk and interpreting model outputs. As a result, enterprises allocate larger enablement budgets to professional services, driving cross-sell opportunities for platform vendors and systems integrators.

By Organization Size: SME adoption accelerates through cloud democratization

Large enterprises account for 58.31% of revenue owing to complex multi-product sales motions that benefit most from AI analytics. SMEs, however, are the fastest-growing buyers at a 26.6% CAGR as subscription pricing removes historical CAPEX barriers. Tata Steel’s 2,000-seller rollout of BigSpring’s multilingual learning hub illustrates scale adoption beyond Fortune 500 boundaries.

SMEs favour vendor UX simplicity, rapid onboarding and pre-built integrations that reduce administrative overhead. Vendors that package “click-to-deploy” playbooks and offer outcome-based pricing win share among growth-stage tech startups and mid-market manufacturers that want enterprise-grade features without heavy IT lift. The momentum of SMEs will gradually dilute large-enterprise share, although absolute spend remains skewed toward global conglomerates.

By Deployment Mode: Cloud supremacy reinforces scalability imperatives

Cloud deployments captured 82.18% of the sales enablement platform market share in 2025 and continue expanding at a 22.8% CAGR. Elastic compute allows vendors to run transformer models and real-time speech analytics that on-premises infrastructure cannot handle cost-effectively. Enterprise security concerns are now outweighed by the upside of instantaneous feature releases and worldwide content delivery networks.

Vendors differentiate through zero-trust architectures, bring-your-own-key encryption and region-based data residency—capabilities once exclusive to legacy on-premises products. Meanwhile, the total cost of ownership favours cloud because vendors amortize compute across customers and pass on economies of scale. On-premises solutions persist only in ultra-regulated sub-segments such as defense contracting, where air-gapped networks remain mandatory.

By Functionality: Analytics integration transforms decision-making

Content management remains the entry gate for most buyers, yet analytics and reporting now grows the fastest as leaders insist on tying enablement activities to pipeline influence. High spot and Seismic embed dashboards that correlate content engagement with deal velocity, allowing CROs to prune low-impact assets in real time.

Sales training and coaching gains momentum through AI-driven micro-coaching that detects conversational gaps and pushes corrective prompts mid-call. Guided selling and playbooks, though smaller today, are poised to rise as embedded copilots convert predictive insights into prescriptive next steps. The fusion of analytics, coaching and guided selling ultimately makes static content libraries obsolete, re-positioning platforms as revenue-operating systems.

By End-User Industry: Healthcare compliance drives specialized adoption

IT & telecom leads the sales enablement platform market with a 21.08% revenue slice, thanks to complex product catalogues and large, dispersed sales forces. Healthcare and life sciences, however, are the growth pacesetters at a 23.9% CAGR as strict regulatory oversight demands granular content approval, real-time audit trails, and role-based access controls. Bayer’s EUR 250 million (USD 293.02 million) “Data-Powered Sales” program exemplifies the vertical’s investment in compliant personalization.

Other high-growth verticals include BFSI, where evolving KYC requirements force accurate document governance, and manufacturing, where multilingual playbooks accelerate channel-partner enablement. Vendors with industry-specific modules—like pre-approved medical-legal review workflows—secure premium pricing and lower churn by embedding deeply into regulated processes.

Geography Analysis

North America generated 42.70% of global revenue in 2025 as multibillion-dollar enterprises prioritized AI-powered enablement to sustain quota attainment. Seismic alone counts 85 million-dollar-plus ARR customers in the region, highlighting the scale of deployments. Cloud maturity, venture-capital funding and early enterprise appetite for generative AI maintain North America’s lead.

Asia-Pacific is the fastest-growing region at 21.8% CAGR through 2031, propelled by government incentives for digital transformation, surging cloud spend and abundant green-field SME demand. Tata Steel’s multilingual enablement initiative underscores regional innovation in scaling training across diverse languages and time zones. India and Southeast Asia, in particular, leapfrog legacy tooling by adopting mobile-first, cloud-native platforms.

Europe’s trajectory is shaped by stringent privacy regulations and emerging labour laws such as the right-to-disconnect, which drive uptake of asynchronous enablement. Vendors that offer granular data-sovereignty controls and localized language support gain advantage. Meanwhile, Latin America, the Middle East and Africa contribute smaller shares today but present long-term upside as multinationals expand and regional champions modernize sales operations.

Competitive Landscape

The sales enablement platform market is moderately concentrated yet rapidly consolidating. Seismic surpassed USD 375 million in annual revenue and secured a USD 500 million credit facility to fund acquisitions and AI R&D. Vista Equity merged Salesloft and Drift, signalling a strategic pivot toward unified revenue orchestration.

Competitive differentiation hinges on generative-AI model depth, proprietary training data and embedded analytics that tie enablement to revenue. Allego 8 unveiled AI-powered productivity tools targeting highly regulated verticals, while Outreach partnered with SAP to embed AI-guided workflows into ERP environments.

Intellectual-property filings focus on clickstream-based interest prediction and real-time knowledge retrieval, raising entry barriers for new vendors. Yet white-space remains in under-served mid-market segments and geographies requiring localized support. Vendors able to quantify ROI, offer frictionless integrations and deliver vertical-specific compliance capabilities will outpace peers as spending tightens. [4]FoundHQ, “Salesloft Didn't Really Acquire Drift, They Merged,” foundhq.com

Sales Enablement Platform Industry Leaders

Seismic Software Inc.

Highspot Inc.

Bigtincan Holdings Ltd.

Showpad NV

Salesloft Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Salesloft and Drift complete integration under Vista Equity, launching a single revenue orchestration platform.

- June 2025: Seismic secures a USD 500 million credit line from PNC Bank to fuel global expansion.

- May 2025: Allego rolls out Allego 8 with AI-powered coaching and content productivity features.

- April 2025: Outreach introduces an AI revenue workflow platform and global SAP partnership.

Global Sales Enablement Platform Market Report Scope

Sales enablement is a strategic, cross-functional discipline designed to increase sales results and productivity by providing integrated content, training, and coaching services for salespeople and front-line sales managers along the entire customer's buying journey, powered by technology.

The Sales Enablement Platform Market is Segmented by Component (Platform and Services), Organization Size (Large Enterprises and Small and Medium-Sized Enterprises), Deployment Type (Cloud and On-premises), End-user Industry (BFSI, Consumer Goods and Retail, IT and Telecom, Media and Entertainment, Healthcare and Life Sciences and Manufacturing), and Geography.

| Platform |

| Services |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Cloud-based |

| On-premises |

| BFSI |

| Consumer Goods and Retail |

| IT and Telecom |

| Media and Entertainment |

| Healthcare and Life Sciences |

| Manufacturing |

| Others (Energy, Public Sector, etc.) |

| Content Management |

| Sales Training and Coaching |

| Analytics and Reporting |

| Guided-Selling/Playbooks |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Platform | |

| Services | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By Deployment Mode | Cloud-based | |

| On-premises | ||

| By End-user Industry | BFSI | |

| Consumer Goods and Retail | ||

| IT and Telecom | ||

| Media and Entertainment | ||

| Healthcare and Life Sciences | ||

| Manufacturing | ||

| Others (Energy, Public Sector, etc.) | ||

| By Functionality | Content Management | |

| Sales Training and Coaching | ||

| Analytics and Reporting | ||

| Guided-Selling/Playbooks | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the sales enablement platform market?

The market stands at USD 5.04 billion in 2026 and is forecast to hit USD 12.35 billion by 2031.

Which deployment mode is growing fastest?

Cloud-based deployments lead with 82.18% revenue share in 2025 and are expanding at a 22.8% CAGR through 2031.

Why are services growing faster than platform revenue?

Enterprises need specialized expertise for AI model tuning, data integration and change management, driving services at a 24.2% CAGR.

Which region shows the highest growth potential?

Asia-Pacific is advancing at 21.8% CAGR due to accelerated digital transformation and SME cloud adoption.

How are budget constraints affecting platform adoption?

SaaS rationalization pressures vendors to prove ROI, with Vertice noting 11.3% software inflation and 45.7% unused licenses.

What differentiates leading vendors?

Depth of generative-AI capabilities, proprietary training data, vertical-specific compliance modules and unified analytics that tie enablement to revenue.

Page last updated on: