Influencer Advertising Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 39.03 Billion |

| Market Size (2031) | USD 73.77 Billion |

| Growth Rate (2026 - 2031) | 13.58% CAGR |

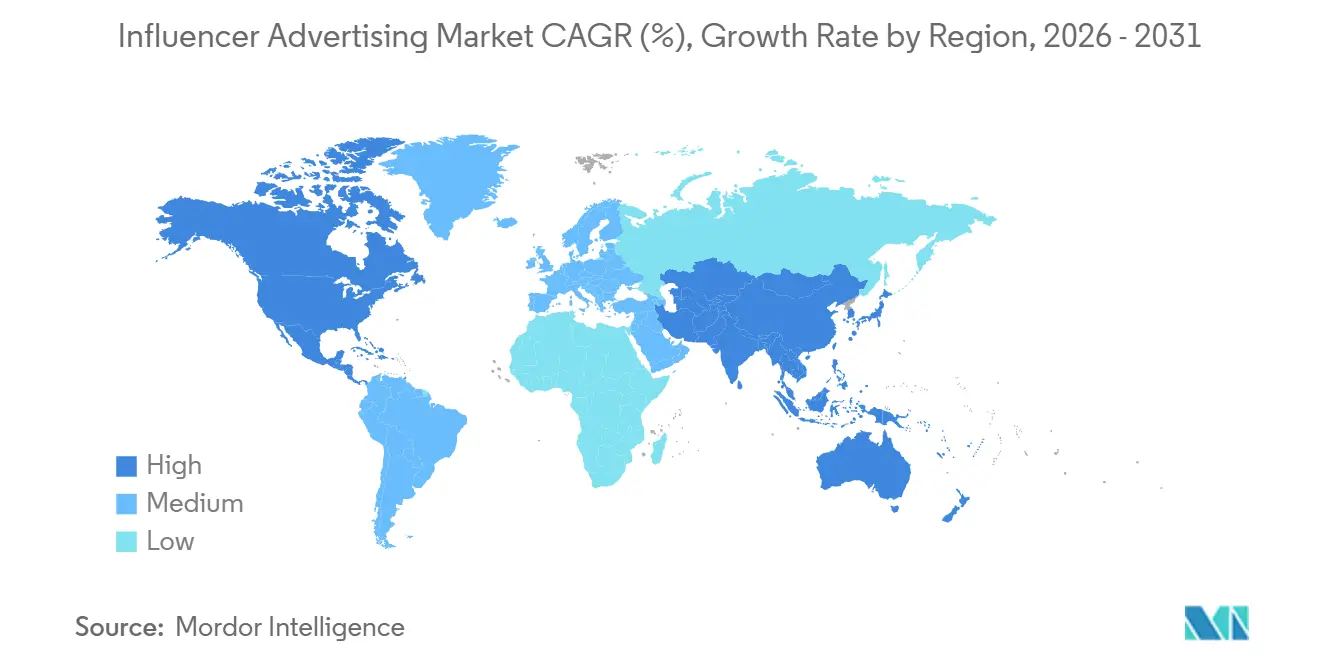

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Influencer Advertising Market Analysis by Mordor Intelligence

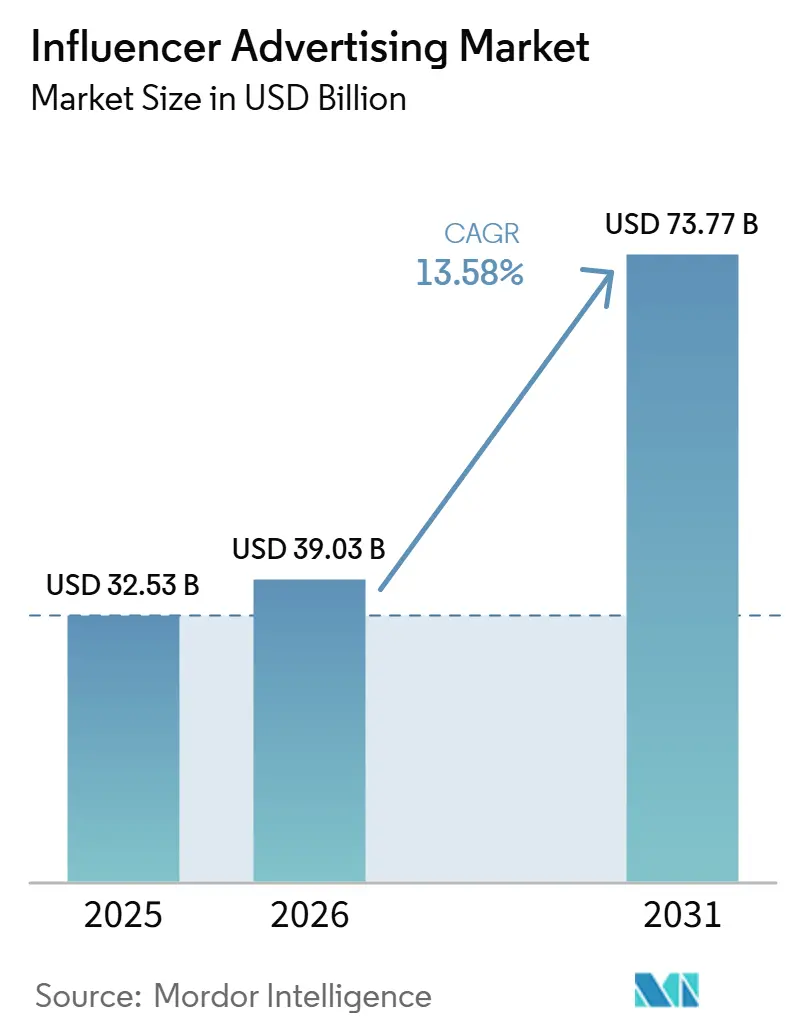

The Influencer Advertising Market size is expected to increase from USD 32.53 billion in 2025 to USD 39.03 billion in 2026 and reach USD 73.77 billion by 2031, growing at a CAGR of 13.58% over 2026-2031. The Influencer advertising market is growing as media buyers continue to move budgets toward creator partnerships that feel more personal and often generate stronger engagement than brand-owned content. It is also moving closer to performance media because brands are putting more weight on affiliate structures, commerce links, and direct conversion tracking instead of relying on reach alone. The Influencer advertising market is becoming more organized at the enterprise level as platforms add creator discovery, workflow management, audience checks, and attribution tools, while larger service groups acquire specialist firms to bring those capabilities into wider client systems. This shift is opening space in live shopping, regulated creator programs, and cross-platform campaign management, especially in categories where trust and repeated creator exposure shape buying decisions. The main limits remain fragmented measurement rules across major platforms and continuing concerns around fraud, both of which still slow how quickly some large budgets move into the Influencer advertising market.

Key Report Takeaways

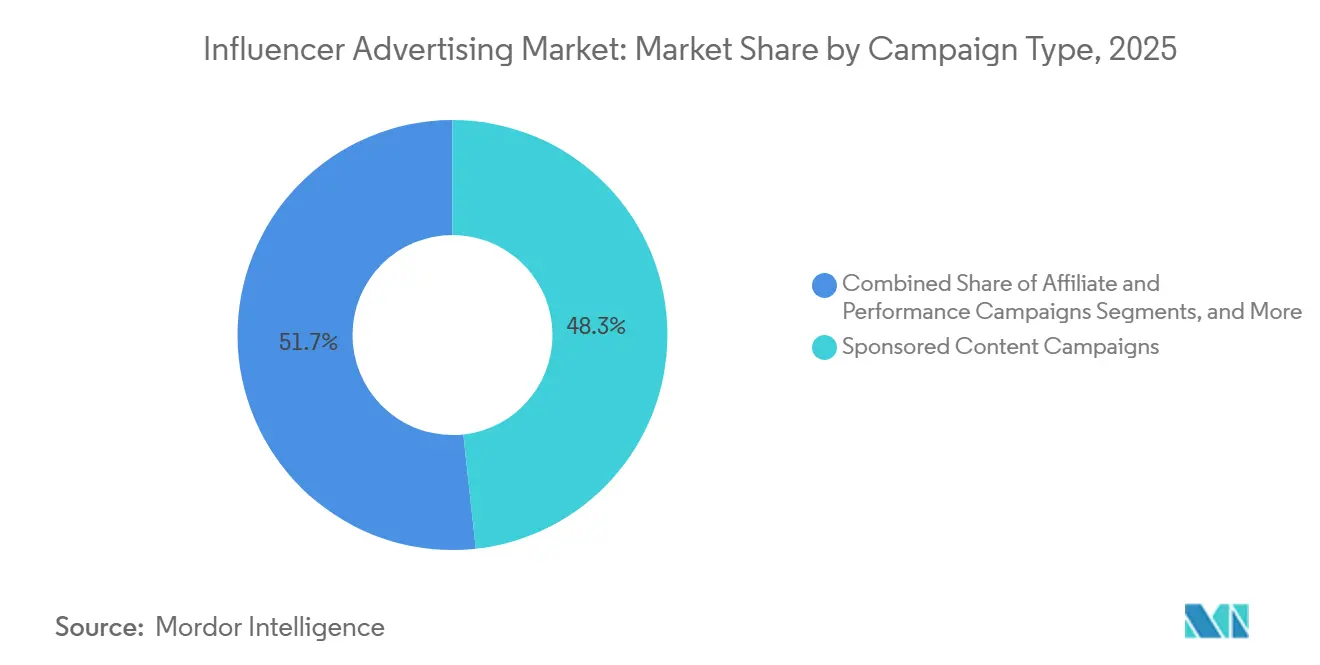

- By Campaign Type, sponsored content campaigns held 48.27% share in 2025, while affiliate and performance campaigns are projected to expand at a 17.78% CAGR through 2031.

- By Content Format, video content accounted for 51.72% of the Influencer advertising market size in 2025, while live streaming content is projected to grow at a 16.57% CAGR through 2031.

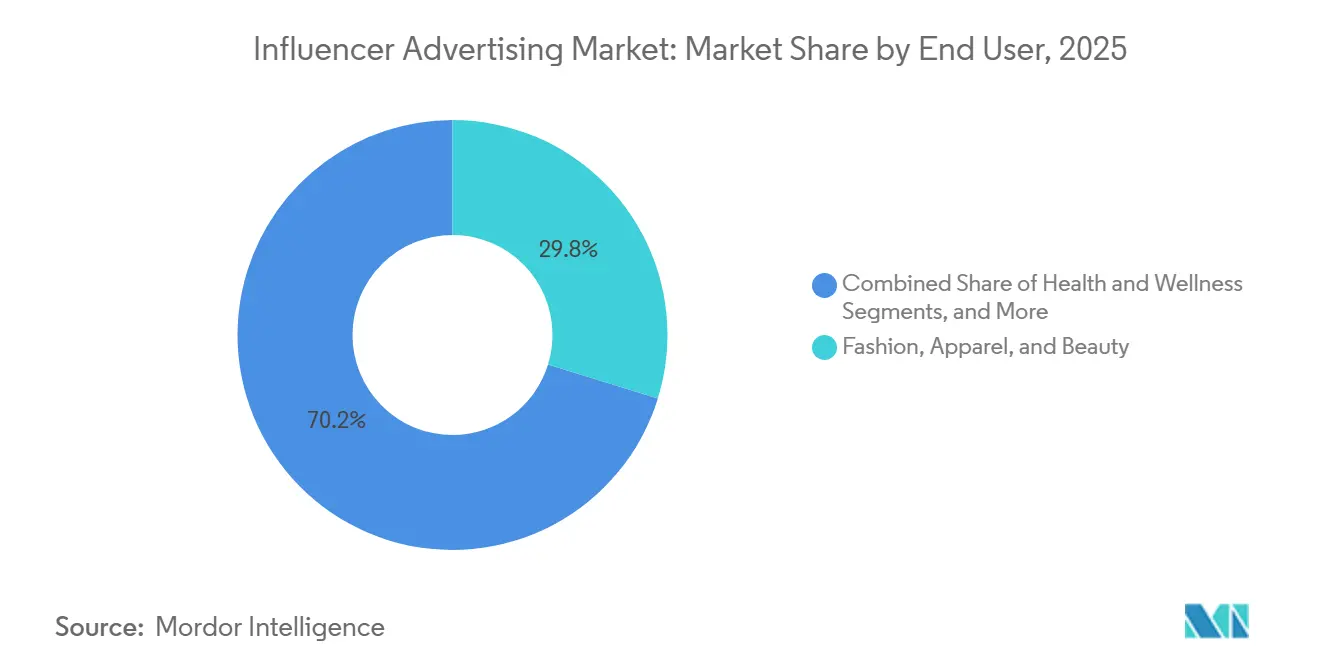

- By End User, fashion, apparel, and beauty held 29.78% of the Influencer advertising market share in 2025, while health and wellness is projected to grow at a 17.18% CAGR through 2031.

- By Geography, North America captured 35.44% share in 2025, while Asia-Pacific is projected to advance at a 16.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Influencer Advertising Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Brand Demand for Authentic Creator-Led Content | +3.8% | Global | Short term (≤ 2 years) |

| Expansion of Short-Form Video Monetization | +2.9% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Shoppable Content and Social Commerce Integration | +2.5% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Performance-Based Influencer Budget Allocation | +1.9% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growth of Creator Discovery and Workflow Platforms | +1.3% | North America, Asia-Pacific core, spillover to Europe | Medium term (2-4 years) |

| Higher Adoption of Cross-Platform Campaigns | +0.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Brand Demand for Authentic Creator-Led Content

The Influencer advertising market is benefiting from a steady change in how brands define effective communication, with creator content now treated as a core channel rather than a side experiment. CreatorIQ reported that a 2025 BCG consumer survey ranked influencers as the leading source shaping purchase decisions, ahead of online search, owned social content, traditional media, and word of mouth, which shows how strongly creator voices now affect buying behavior. This shift favors content that looks natural, is lightly produced, and feels close to the way people already use social platforms, which helps creators maintain stronger audience trust. LTK stated in 2025 that 70% of Gen Z and millennial consumers preferred mobile-first social shopping, with creators acting more as trusted guides than interruptive advertisers, which supports the growing role of creator-led recommendations in purchase journeys.[1]LTK, “LTK Releases 2025 Creator Marketing Trends Report,” Business Wire Aspire also reported that brand ambassador programs delivered the highest ROI among campaign structures in 2025 despite low campaign volume, which shows that longer creator relationships can outperform one-off placements when brands need repeat trust and stronger conversion intent. As a result, the Influencer advertising market is seeing higher value flow toward creators who can hold audience confidence over time rather than only deliver a large top-line reach number.

Expansion Of Short-Form Video Monetization

The Influencer advertising market continues to gain momentum from short-form video because this format combines brand storytelling, product demonstration, and shopping behavior in the same viewing session. Gigapay reported that TikTok Shop gross merchandise value is projected to reach USD 112.2 billion in 2026, nearly double the 2025 level, which shows how quickly commerce-linked video is scaling around creator participation.[2]Gigapay, “2026 Creator Pay Report,” Gigapay The same source noted that TikTok and YouTube structured creator payouts in ways that support a steady flow of original video output, which gives advertisers a large and renewable supply of branded inventory. This matters because creators who earn from both platform programs and sponsorships can post more often, test more formats, and respond faster to brand briefs. That operating model helps the Influencer advertising market pull more spend toward formats that can carry both attention and action. It also raises the commercial importance of video-led buying paths compared with formats that stop at awareness.

Shoppable Content and Social Commerce Integration

The Influencer advertising market is also expanding because shoppable creator content shortens the distance between discovery and purchase, which makes the channel easier for brands to justify. When the product link, checkout path, and creator content remain inside the same platform, brands can track user behavior more directly than they can in campaigns that end outside a buying environment. Influencer-driven spend during Cyber Week 2025 increased by 51% year over year, while social media influencers nearly doubled their share of total orders, demonstrating how effectively shoppable formats convert consumer attention into transactions. This shift gives platforms with native commerce tools a clear operating advantage because they can provide both exposure and purchase evidence in one system. It also explains why the Influencer advertising market is seeing stronger growth in regions where content and checkout already sit close together. Over time, this reduces the gap between creator marketing and measurable commerce activity.

Performance-Based Influencer Budget Allocation

The Influencer advertising market is moving toward stricter return expectations as more brands replace fixed fees with payouts linked to clicks, conversions, or verified sales. Aspire reported that 74% of marketers plan to increase their influencer marketing budgets, reflecting growing confidence in creator partnerships that deliver measurable business outcomes. This shift tends to support micro and nano creators because their audiences are smaller but often more responsive, which can improve efficiency per dollar spent. It also changes how buyers evaluate creator partnerships, because proof of action now matters more than visibility alone. In practice, the Influencer advertising market is moving away from flat-fee exposure and toward structures that reward measurable outcomes. As reporting discipline tightens, creators who can demonstrate verified conversions are likely to capture a larger share of future advertising spend.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Measurement Fragmentation Across Walled Gardens | -2.4% | Global | Short term (≤ 2 years) |

| Rising Fraud, Fake Followers, and Engagement Manipulation | -1.8% | Global, highest intensity in Asia-Pacific and South America | Short term (≤ 2 years) |

| Regulatory Scrutiny on Endorsement Disclosure | -1.2% | North America and Europe | Medium term (2-4 years) |

| Brand Safety Risks From Unpredictable Creator Behavior | -0.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Measurement Fragmentation across Walled Gardens

The biggest operational problem in the Influencer advertising market is that brands still struggle to compare results across platforms with a consistent set of definitions. IAB stated in January 2026 that major platforms continue to control their own view rules, impression logic, and conversion windows, which makes cross-platform ROI analysis difficult for advertisers trying to compare spend at scale.[3]Interactive Advertising Bureau, “As-Is Measurement Landscape in the Creator Economy,” IAB The same analysis outlined eight structural upgrades needed for finance-grade accountability, including common impression standards, better third-party verification, and clearer supply-path transparency across creator technology stacks. This gap explains why some large advertisers still limit creator budgets even when campaign-level engagement looks strong, because budget approval at enterprise scale depends on comparable evidence. Partial fixes such as promo codes, clean rooms, and first-party pixels help on specific campaigns, but they do not yet replace a broad measurement system that works across major platforms. Until the Influencer advertising market closes this reporting gap, the pace of budget migration from more standardized digital channels will remain restrained.

Rising Fraud, Fake Followers, and Engagement Manipulation

The Influencer advertising market also faces a credibility problem when brands cannot confirm whether creator audiences are real, active, and properly disclosed. A 2025 peer-reviewed synthesis published in Zenodo found that 63% to 78% of sponsored content lacked clear advertising labels, which shows that disclosure quality remains inconsistent across creator activity and complicates trust and compliance reviews.[4]Zenodo, “The Authenticity Crisis in Influencer Marketing Advertising Disclosure, Fraudulent Engagement, and Consumer Trust Erosion,” Zenodo Weak labeling can sit alongside inflated engagement signals, which makes it harder for advertisers to separate genuine community response from manipulated activity or poorly disclosed sponsorships. This risk becomes more serious in categories where trust matters more than impulse buying, such as health, finance, and other regulated areas. It also pushes brands toward platforms that can verify audiences, standardize disclosure checks, and flag suspicious performance patterns before campaigns go live. If these controls do not improve, the Influencer advertising market will continue to lose some budget to channels with cleaner verification and stronger reporting discipline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Campaign Type: Affiliate Models Shift Spending Toward Accountability

Sponsored content campaigns held 48.27% of segment spend in 2025, which kept them as the largest campaign structure in the Influencer advertising market because they fit awareness goals across fast-moving consumer goods, fashion, and financial services. Their scale also reflects habit, because many brand teams already use sponsorship-based briefing models, pricing logic, and agency workflows that were built before conversion-led creator buying became common. That installed process matters because it slows rapid share shifts even when other campaign types grow faster and attract stronger attention from finance teams. Affiliate and performance campaigns are projected to grow at a 17.78% CAGR through 2031, which makes them the fastest-moving campaign category as advertisers seek clearer sales attribution and tighter payout discipline. This change is gradually moving the Influencer advertising market away from flat-fee exposure and toward structures that reward measurable outcomes.

Brand ambassador programs still play an important role because repeated creator relationships can deliver stronger commercial value than one-off activations when brands need trust and continuity. Product seeding and gifting also remain useful because they lower upfront campaign cost and help brands widen reach across many creators at once. Modash reported that 65.7% of influencer marketers prioritized gifting and seeding for brand awareness initiatives, which helps explain why this model remains active even as performance budgets rise. As campaign economics tighten, the Influencer advertising industry is likely to keep a mixed structure where sponsorship remains large, gifting supports scale, and affiliate models take a growing share of new spending. That balance reflects buyer demand for both upper-funnel visibility and lower-funnel accountability inside the same creator program.

By Content Format: Video and Live Commerce Reset Format Priorities

Video content held 51.72% share in 2025, which placed it at the center of the Influencer advertising market because it supports demonstration, emotion, entertainment, and direct response in one format. Brands also favor video because it can be reused across short-form feeds, paid amplification, and commerce placements, which improves content utility across more than one objective. This broad use case has made video the default format for many creator campaigns, especially when brands want to connect discovery, consideration, and action. Live streaming content is projected to grow at a 16.57% CAGR through 2031, showing that the Influencer advertising market size for commerce-led video is still expanding rapidly where creators can answer questions and move viewers directly to purchase. That growth is strongest where live shopping tools sit close to checkout and where audiences already treat creators as shopping companions rather than only entertainers.

Image-based content still matters in fashion and beauty because visual styling, product placement, and quick lifestyle cues remain effective in those categories. Blog and written content, along with podcasts and audio shows, serve more specific audiences that often need longer explanations, stronger disclosure space, or category education before conversion. Gigapay reported that LinkedIn and specialized audio environments can command much higher CPMs in technology and finance niches, which helps explain why these smaller formats remain commercially relevant despite video dominance. The Influencer advertising industry therefore continues to center on video, but it still preserves room for slower formats when trust, detail, or compliance matter more than fast-scroll attention. This leaves format strategy closely tied to the buying context rather than to platform popularity alone.

By End User: Health and Wellness Gains Ground While Beauty Stays Largest

Fashion, apparel, and beauty held 29.78% share in 2025, which made it the largest end-user group in the Influencer advertising market because visual discovery, routine product launches, and lifestyle content kept this segment highly active. The category benefits from steady demand for tutorial content, reviews, seasonal launches, and creator-led product trials that fit naturally into everyday social use. At the same time, the scale of beauty-related activity also exposes the segment to higher scrutiny around disclosure quality and audience authenticity, which means large budgets in this vertical often require more careful creator screening. Health and wellness is projected to grow at a 17.18% CAGR through 2031, making it the fastest-growing end-user segment as more consumers turn to creators for fitness, nutrition, patient experience, and health education content. This is one reason the Influencer advertising market is extending beyond lifestyle categories into areas where credibility and topic expertise directly shape response.

Open Influence reported that healthcare brands working with credentialed creators achieved stronger engagement while still operating within medical compliance expectations, which supports growth in more structured creator programs for this segment. Food and beverage, consumer electronics, and travel and hospitality remain significant users of creator spending because each category has a clear content format that aligns with audience behavior, from recipes and reviews to unboxings and destination storytelling. Automotive also shows room for deeper adoption where creator recommendations shape shortlisting and purchase consideration, even though buying cycles remain longer than in many consumer categories. Financial services and entertainment remain active as well, but they often require tighter brief controls and clearer disclosure standards, which can lengthen campaign design compared with lifestyle verticals. This mix shows that the Influencer advertising market is broadening, while the pace of expansion still depends heavily on trust, format fit, and compliance demands.

Geography Analysis

North America held 35.44% share in 2025, which kept it as the largest regional component of the Influencer advertising market because advertiser tools, agency processes, and disclosure expectations are more established than in most other regions. The United States continues to anchor that position through high brand participation, stronger attribution infrastructure, and a deeper base of enterprise-grade creator platforms. FTC guidance on endorsements and influencer disclosures has also given brands and agencies a clearer operating framework, which reduces uncertainty when they scale creator programs across multiple campaigns. That clarity matters because large advertisers are more willing to commit budget when campaign rules are understood before activation rather than interpreted after the fact. It also supports more structured use of the Influencer advertising market size in planning decisions where brand teams need stronger accountability before releasing spend.

Asia-Pacific is projected to grow at a 16.22% CAGR through 2031, making it the fastest-growing region in the Influencer advertising market as mobile-first behavior and social commerce continue to converge. Japan’s domestic influencer marketing market exceeded JPY 102.1 billion in 2025, which was equivalent to USD 672 million using the 2025 average exchange rate of JPY 152 per USD, and campaign activity on TikTok increased after TikTok Shop launched in Japan in 2025. India’s influencer marketing market reached INR 3,000-3,500 crore in 2025, which was equivalent to USD 357-417 million using the 2025 average exchange rate of INR 84 per USD, and it is projected to reach INR 4,500-5,000 crore (USD 0.47-0.52 billion) by 2027 at a 22% CAGR. India’s language mix also matters because 68.2% of active creators work in Hindi and 23.9% in regional languages, which expands access to Tier-2 and Tier-3 audiences that English-led strategies often miss. Across APAC, campaigns measured by sales and conversions rose from 28.24% in 2023 to 42.47% in 2025, which shows that the Influencer advertising market is becoming more accountable as commerce tools improve.

Europe remains a major part of the Influencer advertising market, with the United Kingdom showing especially strong buyer appetite and higher planned creator use than the broader regional average. Germany stands out because a larger share of brands still manage influencer work in-house and fewer rely on platform tools, which leaves room for vendors that can prove workflow savings and compliance support. The European Parliament Research Service also noted that the European Union operates through a layered set of platform, consumer protection, and national disclosure rules, which raises coordination needs for cross-border creator programs. The Middle East is emerging through luxury, tourism, and public-facing campaigns, while Africa remains earlier in development but continues to build mobile-first creator activity in markets such as South Africa, Nigeria, and Egypt.

Competitive Landscape

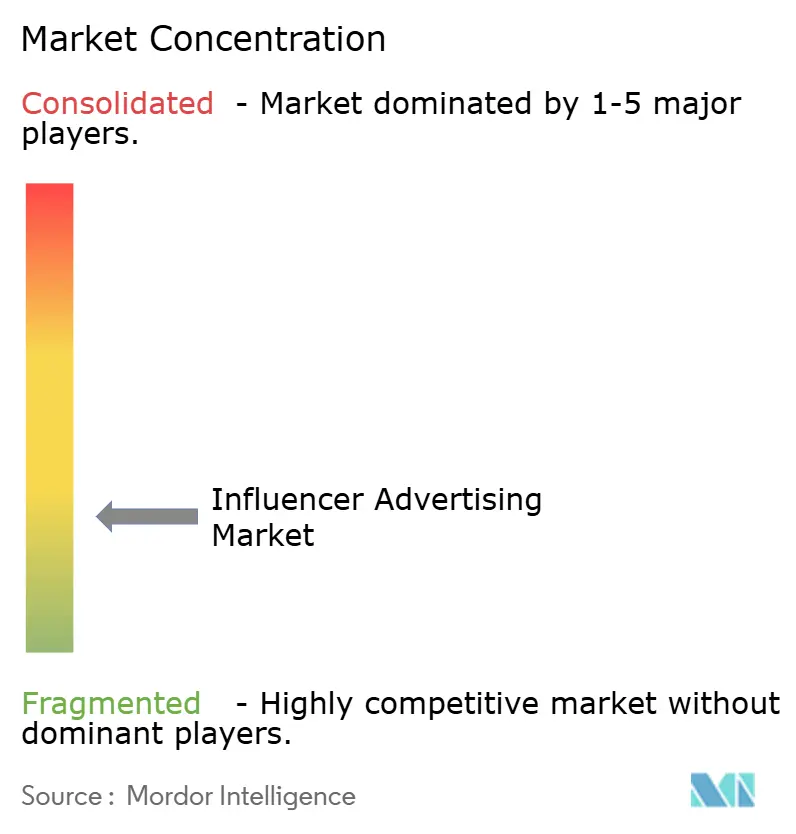

The Influencer advertising market remains moderately fragmented, with no single platform controlling more than a low single-digit share globally, yet competition is tightening as enterprise customers prefer broader and more integrated service stacks. Vendors are increasingly competing on creator discovery, audience quality screening, relationship management, multi-platform reporting, and commerce-linked attribution instead of on creator databases alone. This has made platform breadth more important because large advertisers want fewer handoffs between discovery, campaign execution, compliance review, and measurement. The result is a market where scale still matters, but operating depth and integration quality matter just as much. That balance explains why the Influencer advertising market still looks fragmented on the surface even while consolidation is rising in the enterprise layer.

Companies like CreatorIQ, GRIN Technologies, Upfluence, Traackr, Captiv8, IZEA Worldwide, Meltwater, Kolsquare SAS, and Influencity compete across creator discovery, campaign management, relationship workflows, audience verification, and multi-platform measurement. CreatorIQ, GRIN Technologies, Upfluence, and Traackr are positioned as core enterprise-grade platforms, serving brands that need scale, process control, and stronger reporting across large creator programs. Mid-market and regional vendors are differentiating through commerce integrations, niche creator databases, compliance support, and faster campaign execution.

Competitive activity has increasingly centered on acquisitions and partnership-led expansion. Publicis Groupe acquired Captiv8 in May 2025, adding a platform connected to 15 million creators across 120 countries and strengthening its end-to-end creator capabilities. Accenture agreed to acquire Whalar in June 2026, showing that creator and social capabilities are now being treated as core client delivery assets rather than optional services. CreatorIQ also deepened its market position through its June 2026 partnership with dentsu, linking audience strategy with creator selection and measurement inside a more unified operating model. These moves indicate that scale alone is no longer enough, and vendors now need tighter integration between data, creator access, and campaign accountability.

IZEA Worldwide showed a different competitive path by exiting lower-margin SMB activity, improving profitability, and entering 2026 with USD 50 million in cash and no debt, which supported its enterprise focus and acquisition capacity. Meltwater strengthened its offering in 2025 by integrating verified non-public YouTube data from creators in the YouTube Partner Program, which addressed growing demand for better data transparency. Upfluence also expanded its platform capabilities with Jaice, its AI-powered campaign co-pilot, reflecting the market-wide push toward faster and more automated campaign execution, although this example comes from a less authoritative source in the shared draft and should be treated more cautiously than company-issued disclosures. Overall, the influencer advertising market is favoring players that combine creator access, usable workflow tools, stronger verification, and commerce-linked measurement without forcing brands to manage too many separate systems.

Influencer Advertising Industry Leaders

CreatorIQ

GRIN Technologies Inc.

Upfluence Inc.

Traackr, Inc.

IZEA Worldwide, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Accenture agreed to acquire Whalar, a leading creator and social agency from Whalar Group. Whalar, with over 170 team members across the United States, the United Kingdom, Ireland, Germany, and Spain, will join Accenture Song, adding scaled creator and influencer engagement to its customer growth capabilities. The deal reflects the broader thesis that creator strategy and social commerce are inseparable from enterprise customer experience design.

- June 2026: Dentsu and CreatorIQ announced a first-of-its-kind data partnership integrating dentsu.Audiences with CreatorIQ's AI-enabled platform, allowing brands to directly match target audience attributes with creator follower or viewership data. The integration eliminates guesswork in creator selection and is the first initiative connecting audience intelligence, creator discovery, and measurement within a single ecosystem.

- May 2026: Meltwater released its 2026 Mid-Year Product Update, embedding AI-powered trend detection across TikTok, Instagram, YouTube, and news channels with no custom setup required, and launching AI-powered pitch personalisation for media relations, extending the platform's intelligence layer from influencer discovery into broader brand narrative management.

- January 2026: PMG announced its acquisition of Digital Voices, a London- and New York-based influencer marketing agency recognized for integrating data, creativity, and technology to deliver campaigns with measurable business impact. As the influencer marketing industry is projected to grow tenfold over the next 8 years, the acquisition underscores PMG’s continued commitment to customer-centric, full-funnel marketing solutions at a global scale. The companies did not disclose the transaction terms.

Global Influencer Advertising Market Report Scope

The Influencer Advertising Market Report is Segmented by Campaign Type (Sponsored Content Campaigns, Affiliate and Performance Campaigns, Product Seeding and Gifting Campaigns, and Brand Ambassador Programs), Content Format (Video Content, Image-Based Content, Live Streaming Content, Blog and Written Content, and Podcasts and Audio Shows), End User (Fashion, Apparel, and Beauty, Food and Beverage, Consumer Electronics, Travel and Hospitality, Health and Wellness, Automotive, Financial Services, Entertainment and Media, and Other End User), and Geography ( North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Sponsored Content Campaigns |

| Affiliate and Performance Campaigns |

| Product Seeding and Gifting Campaigns |

| Brand Ambassador Programs |

| Video Content |

| Image-Based Content |

| Live Streaming Content |

| Blog and Written Content |

| Podcasts and Audio Shows |

| Fashion, Apparel, and Beauty |

| Food and Beverage |

| Consumer Electronics |

| Travel and Hospitality |

| Health and Wellness |

| Automotive |

| Financial Services |

| Entertainment and Media |

| Other End User |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Campaign Type | Sponsored Content Campaigns | |

| Affiliate and Performance Campaigns | ||

| Product Seeding and Gifting Campaigns | ||

| Brand Ambassador Programs | ||

| By Content Format | Video Content | |

| Image-Based Content | ||

| Live Streaming Content | ||

| Blog and Written Content | ||

| Podcasts and Audio Shows | ||

| By End User | Fashion, Apparel, and Beauty | |

| Food and Beverage | ||

| Consumer Electronics | ||

| Travel and Hospitality | ||

| Health and Wellness | ||

| Automotive | ||

| Financial Services | ||

| Entertainment and Media | ||

| Other End User | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size of the influencer advertising market in 2026?

The Influencer advertising market stands at USD 39.03 billion in 2026 and is projected to reach USD 73.77 billion by 2031 at a 13.58% CAGR.

Which campaign type leads spending in influencer advertising?

Sponsored content campaigns led with a 48.27% share in 2025 because they fit broad awareness goals and align with established brand and agency workflows.

Which content format is growing fastest in creator-led advertising?

Live streaming content is projected to grow at a 16.57% CAGR through 2031, while video already led the format mix with a 51.72% share in 2025.

Which end-user group offers the strongest growth opportunity?

Health and wellness is projected to grow at a 17.18% CAGR through 2031 as consumers increasingly rely on creators for fitness, nutrition, and health education content.

Which region is expanding fastest for influencer advertising?

Asia-Pacific is the fastest-growing region, with a projected 16.22% CAGR through 2031, supported by mobile-first behavior, social commerce, and local-language creator ecosystems.

What is slowing faster enterprise adoption of creator advertising programs?

The main barriers are fragmented measurement across major platforms, uneven disclosure standards, and continued concerns around fake followers and manipulated engagement.

Page last updated on: