AI-Powered Marketing Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

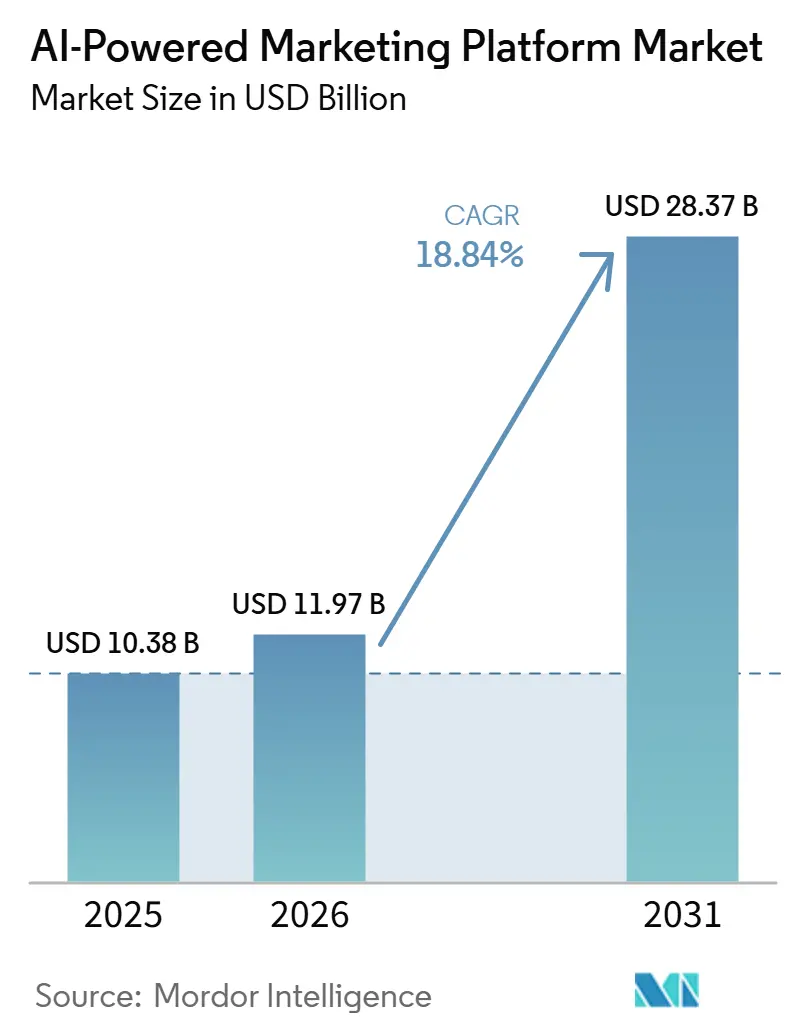

| Market Size (2026) | USD 11.97 Billion |

| Market Size (2031) | USD 28.37 Billion |

| Growth Rate (2026 - 2031) | 18.84% CAGR |

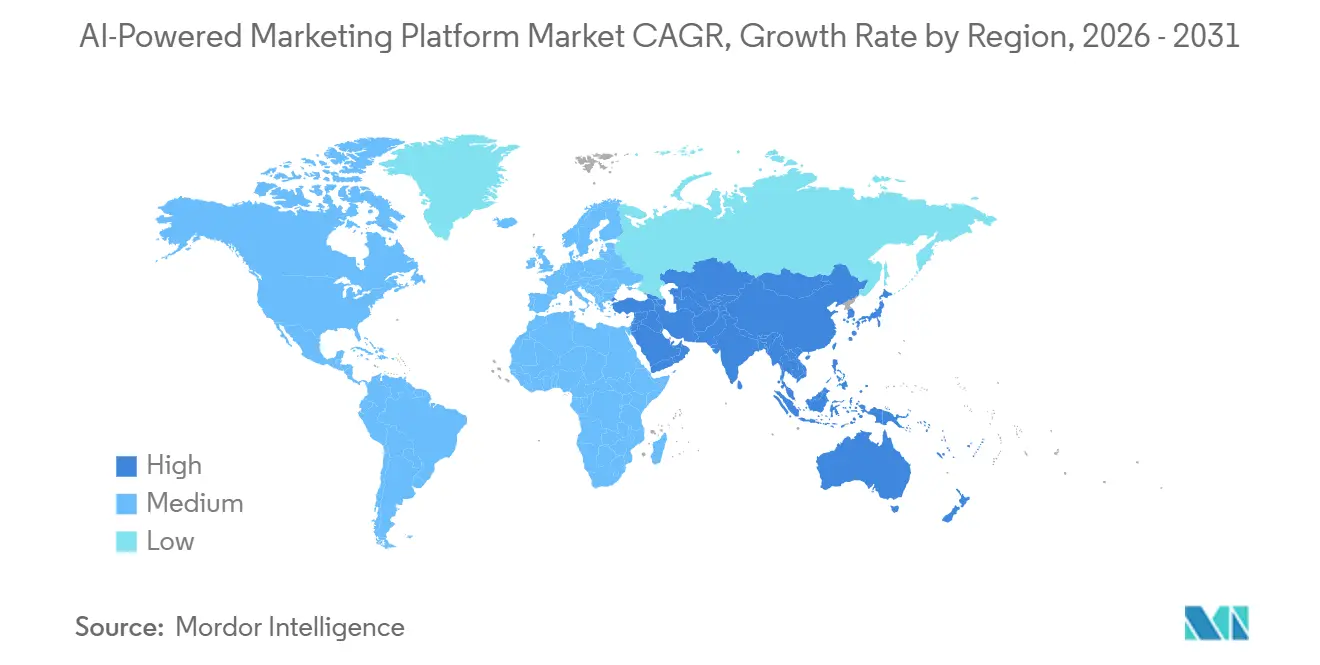

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Powered Marketing Platform Market Analysis by Mordor Intelligence

The AI-powered marketing platform market size is expected to grow from USD 10.38 billion in 2025 to USD 11.97 billion in 2026 and is forecast to reach USD 28.37 billion by 2031 at 18.84% CAGR over 2026-2031. Growth is being supported by a clear move away from fixed campaign rules and toward systems that respond to live customer behavior across channels. Buying decisions are also shifting toward platforms that sit within broader enterprise software environments, because this setup reduces tool overlap and speeds activation across content, data, and campaign workflows. Demand is widening beyond software licenses, since many buyers now need implementation support, data preparation, governance controls, and workflow design before AI features can be used at scale. Regional demand remains uneven, with North America benefiting from a mature digital advertising infrastructure and Asia-Pacific expanding faster as smaller businesses digitize and local platform ecosystems deepen. Competition remains active rather than locked, because large vendors have scale advantages, yet no single company leads every application, deployment model, and customer tier at the same time.

Key Report Takeaways

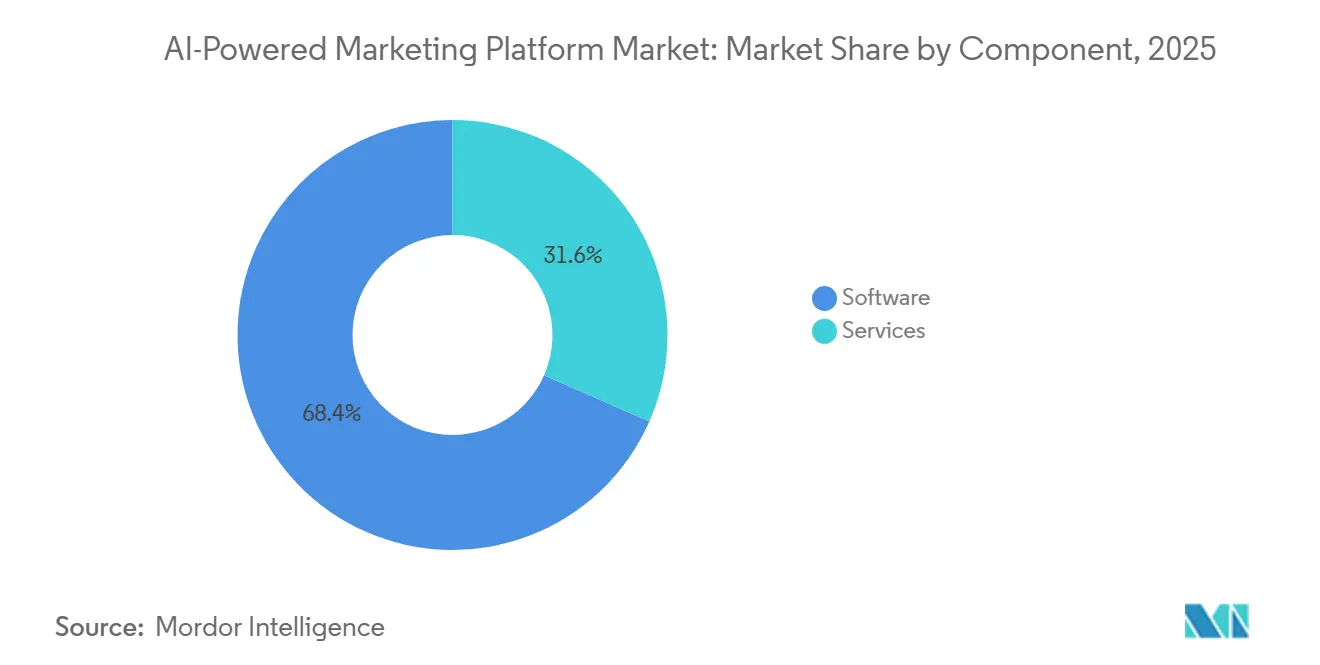

- By component, software held 68.41% share in 2025, while services are projected to expand at a 21.82% CAGR through 2031.

- By deployment mode, cloud-based architectures accounted for 72.19% of the market share in 2025, while hybrid configurations are projected to grow at a 20.43% CAGR through 2031.

- By application, marketing automation led with 24.36% share in 2025, while AI content generation is projected to expand at a 23.74% CAGR through 2031.

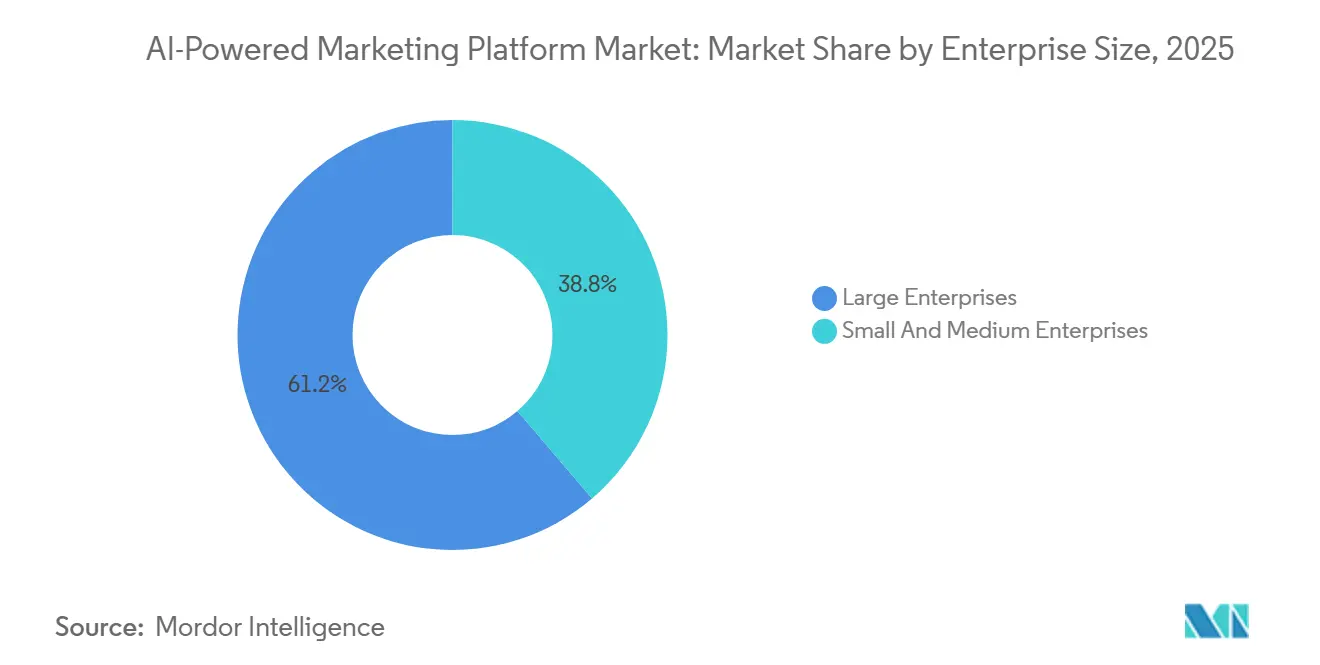

- By enterprise size, large enterprises held 61.24% share in 2025, while SMEs are projected to record the highest CAGR at 22.18% through 2031.

- By end-user industry, retail and e-commerce accounted for 26.83% of the market share in 2025, while media and entertainment is projected to advance at a 21.49% CAGR through 2031.

- By geography, North America held 34.62% of the AI-powered marketing platform market share in 2025, while Asia-Pacific is projected to expand at a 22.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Powered Marketing Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyper-Personalization Across Customer Journeys | +4.2% | Global | Medium term (2-4 years) |

| Shift From Rule-Based Campaigns to Agentic AI Workflows | +3.8% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| First-Party Data Activation as Third-Party Cookies Recede | +3.1% | North America, Europe, Australia | Medium term (2-4 years) |

| Generative Content Production at Enterprise Scale | +2.8% | Global, with early gains in North America and Western Europe | Short term (≤ 2 years) |

| Closed-Loop Attribution Pressure From ROI Scrutiny | +2.1% | North America, Asia-Pacific | Medium term (2-4 years) |

| Embedded AI in Marketing Cloud Suites Reducing Procurement Friction | +1.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyper-Personalization Across Customer Journeys

The AI-powered marketing platform market is benefiting from a broad reset in buyer expectations, as marketers no longer treat audience segments as ends in themselves in campaign design. Enterprises increasingly want systems that read intent signals, behavioral events, and engagement context as they happen, then update the next message without waiting for a manual campaign cycle. That requirement is pushing the AI-powered marketing platform market toward architectures that combine customer data, content generation, and activation within a single operating layer. Adobe positioned CX Enterprise Coworker as an orchestration layer across Experience Cloud, Real-Time CDP, and GenStudio, which shows how leading vendors are turning personalization into a connected operating process rather than a standalone feature.[1]Adobe, “Adobe Unveils CX Enterprise Coworker to Build Agentic-Enabled Workflows for Customer Experience Orchestration,” Adobe News, news.adobe.com As this model becomes more common, vendors with deeper workflow coordination and real-time data handling are likely to win larger platform decisions. It also raises the value of governance, because personalized interactions now depend on content quality, permission controls, and data consistency simultaneously.

Shift From Rule-Based Campaigns to Agentic AI Workflows

The AI-powered marketing platform market is also moving from assistant-led features toward autonomous workflows that can plan, generate, test, and optimize with less manual intervention. This shift matters because it changes the platform's role from a tool that supports campaign teams to a system that directly carries out parts of the operating workload. Adobe’s 2026 product direction centered on agent-enabled orchestration across customer experience workflows, reflecting how the AI-powered marketing platform market is being redesigned around agents rather than isolated automation rules. Microsoft and Publicis also expanded their partnership in 2026 to build a full-stack AI marketing solution, showing that large enterprise buyers are preparing for end-to-end operating models rather than narrow pilot programs.[2]Adobe, “Adobe Introduces Brand Intelligence and Expands GenStudio Content Supply Chain Solution for Customer Experience Orchestration,” Adobe News, news.adobe.com The result is a shorter distance between planning and execution, which supports more frequent testing, faster campaign adjustments, and stronger internal justification for follow-on investment. It also increases pressure on vendors that still rely on older rule sets, as those systems can appear rigid compared with agent-led alternatives.[3]Microsoft, “Microsoft and Publicis Groupe Expand Their Strategic Partnership to Power the Future of Agentic Marketing for Businesses Worldwide,” Microsoft Source, news.microsoft.com

First-Party Data Activation as Third-Party Cookies Recede

The AI-powered marketing platform market is seeing stronger demand for first-party data activation, even without a single global trigger event forcing every buyer to move at the same pace. Buyers are increasingly treating data control as a platform design issue, not just a media targeting issue, because content, segmentation, personalization, and measurement now depend on the same customer record. In the AI-powered marketing platform market, this favors vendors that connect customer data environments directly with activation layers and creative systems. Adobe’s recent emphasis on Real-Time CDP integration within its broader orchestration stack illustrates how first-party data is becoming central to enterprise marketing operations. The advantage of this approach is that it supports consent-aware execution and cleaner audience management across channels. It also helps buyers reduce the friction caused by campaign teams, analytics teams, and data teams working from separate records and workflows.

Generative Content Production at Enterprise Scale

The AI-powered marketing platform market is gaining momentum as companies seek to produce more content across more channels without adding the same level of headcount. Enterprises want content systems that can quickly create usable drafts, but they also want those systems tied to performance data, brand controls, and channel-specific activation tools. That requirement is making the AI-powered marketing platform market more centered on production workflows that connect ideation, asset creation, approval, and deployment. Adobe expanded GenStudio for Performance Marketing and added support for activation across conversational AI surfaces, which shows that content generation is becoming part of a larger operating chain rather than a standalone writing aid. Amazon’s rollout of Alexa+ Agentic Ads also points to a wider shift, because brands now need creative assets that fit conversational and shopping-oriented interfaces, not just traditional display and search environments. As these formats spread, vendors that can link content generation with audience selection and channel delivery are likely to capture a larger share of enterprise budgets.[4]Amazon Ads, “Amazon Introduces Alexa+ Agentic Ads,” Amazon Advertising, advertising.amazon.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy, Consent, and Cross-Border Governance Constraints | -3.5% | Europe, Asia-Pacific, North America | Long term (≥ 4 years) |

| Model Hallucination and Brand-Safety Risk in Automated Content Generation | -2.3% | Global | Short term (≤ 2 years) |

| Integration Complexity Across CRM, CDP, and MarTech Stacks | -1.8% | Global, concentrated in large enterprises | Medium term (2-4 years) |

| Limited In-House AI Operating Skills Among Mid-Market Buyers | -1.2% | Asia-Pacific, South America, Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy, Consent, and Cross-Border Governance Constraints

The AI-powered marketing platform market faces a significant restraint due to the growing complexity of consent management, data use rules, and cross-border operating requirements. Large organizations often run campaigns across several markets, yet their customer data practices, approval processes, and storage requirements do not always align across those regions. That slows the AI-powered marketing platform market because platform selection now depends on legal readiness and operating design, not only on feature depth. Vendors with stronger controls can turn this into an advantage, but many buyers still face delays as they reconcile identity systems, approval structures, and regional data-handling rules. This issue is especially visible in highly regulated sectors, where marketing teams cannot move quickly unless risk, compliance, and data teams approve the same workflow. It also favors hybrid and composable deployments because buyers often want more control over where data sits and how activation occurs.

Model Hallucination and Brand-Safety Risk in Automated Content Generation

The AI-powered marketing platform market is also constrained by concern over inaccurate, off-brand, or non-compliant automated outputs. This matters because the same systems that increase content speed can also multiply errors when one flawed instruction or template is reused across many assets. A 2026 Springer Nature chapter on AI hallucinations in marketing highlighted real risks to customer trust and brand perception, while also pointing to retrieval-augmented generation and human-in-the-loop review as the strongest mitigation methods. In the AI-powered marketing platform market, this shifts buying criteria toward audit trails, review checkpoints, and governance controls built into the content workflow. It also extends implementation time, because enterprises want clear approval logic before allowing automated systems to publish at scale. Vendors that treat quality control as a core product function are therefore better positioned than vendors that focus only on output speed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Accelerates as Deployment Work Deepens

Software held 68.41% of the AI-powered marketing platform market share in 2025, which confirms that licensed platforms remained the main revenue base across the category. The AI-powered marketing platform market still relies on software as its core execution system, since data ingestion, audience logic, campaign setup, and reporting are all anchored in the platform layer. At the same time, the AI-powered marketing platform market size for services is projected to expand at a 21.82% CAGR through 2031, indicating that buyers increasingly need support after the license is purchased. This shift reflects the reality that many deployments require data cleanup, workflow redesign, access control setup, and change management before teams can use AI functions consistently. Service demand also rises when enterprises try to connect marketing tools with CRM, CDP, analytics, and commerce environments, because these integrations often require dedicated implementation expertise.

The service opportunity is not limited to installation work, because buyers increasingly want long-term operating support after the platform goes live. In the AI-powered marketing platform industry, this raises the importance of advisory and managed services that help customers refine prompts, set review logic, and monitor content quality over time. It also creates a revenue path for vendors and partners that can stay embedded in the customer account well beyond the initial deployment window. For buyers, this model can reduce the time needed to move from pilot use to daily use, especially when internal teams lack deep AI operating experience. For vendors, it makes retention more durable because service relationships tie the platform more tightly to the customer’s operating process. Over the forecast period, the component mix is therefore likely to become more balanced even if software remains the larger revenue base.

By Deployment Mode: Hybrid Gains as Buyers Balance Scale and Control

Cloud-based architectures accounted for 72.19% of 2025 revenue, underscoring buyers' preference for scalable deployments with lower upfront infrastructure costs. The AI-powered marketing platform market continues to lean toward cloud models because they support faster feature delivery, easier updates, and tighter links with external AI services. Even so, hybrid configurations are projected to grow at a 20.43% CAGR through 2031, suggesting a different priority among buyers with stricter control needs. In the AI-powered marketing platform market, hybrid models are becoming more relevant where customer data cannot move freely across systems or jurisdictions. That is especially important in banking, healthcare, government, and other settings where teams need both modern activation tools and closer control over sensitive records.

This trend is pushing vendors to offer more flexible architecture rather than a simple public-cloud choice. Databricks launched CustomerLake in 2026 as an agentic customer data platform built natively on its lakehouse environment, which reflects wider demand for governed data activation without forcing a full shift away from existing enterprise data estates. Although the broader AI-powered marketing platform market still favors cloud deployment, hybrid designs are gaining traction because they let buyers keep critical records closer to home while still using advanced orchestration and automation layers. This also reduces resistance from risk teams that might otherwise block broader platform adoption. Over time, a hybrid may absorb part of the demand that would once have remained fully on-premise. That makes deployment flexibility a more important buying factor than the older cloud-versus-on-premises debate alone.

By Application: Automation Leads While AI Content Generation Expands Fastest

Marketing automation accounted for 24.36% in 2025, indicating that workflow execution remained the largest application base in the AI-powered marketing platform market. This leadership reflects years of investment in email flows, lead scoring, campaign triggers, and multichannel journey management. Even within that established base, the AI-powered marketing platform market is changing because older automation rules are being reworked into agent-led decision systems. AI content generation is projected to grow at a 23.74% CAGR through 2031, making it the fastest-expanding application as buyers seek more scalable content production across paid, owned, and conversational channels. The shift is not just about faster writing; enterprises also want content systems linked to compliance reviews, performance data, and channel-specific formatting.

Other application areas remain important, but they are developing at different time scales and with different operating needs. Predictive analytics is gaining relevance where buyers want clearer links between campaign activity and commercial outcomes, while customer intelligence tools remain essential for audience understanding and journey design. The AI-powered marketing platform market is also seeing more attention on conversational surfaces as discovery and shopping behavior move into assistant-led environments. Adobe added support for ChatGPT Ads in GenStudio for Performance Marketing, demonstrating how content creation and activation are beginning to extend into conversational interfaces. Amazon’s Alexa+ Agentic Ads offering points in the same direction, because it creates demand for campaigns that respond to spoken or conversational prompts rather than only search or display inputs. As a result, application growth in the AI-powered marketing platform market is likely to favor use cases that connect content, intent, and action within a single operating loop.

By Enterprise Size: SME Momentum Builds on Easier Access and Faster Adoption

Large enterprises accounted for 61.24% of revenue in 2025, indicating that big organizations still dominate the installed base through scale, larger budgets, and established procurement structures. They remain central to the AI-powered marketing platform market because they manage broader channel footprints, more customer records, and more complex campaign coordination needs. At the same time, SMEs are projected to grow at a 22.18% CAGR through 2031, indicating that adoption is widening beyond the traditional enterprise core. The AI-powered marketing platform market is becoming more reachable for smaller firms as pricing models, packaged workflows, and faster onboarding reduce earlier cost and complexity barriers. This is changing the revenue mix because smaller buyers often enter through focused use cases, such as campaign automation, content generation, or customer engagement, rather than full-suite replacements.

The SME story also matters because it changes how vendors design products and support structures. OECD data showed that SME AI adoption more than doubled from 8.7% in 2023 to 20.2% in 2025, reinforcing the idea that smaller firms are moving from experimentation toward wider operational use. In the AI-powered marketing platform market, tools that favor shorter setup times, lower integration burdens, and clearer default workflows are preferred. It also creates greater demand for onboarding, managed support, and education, as many SMEs lack dedicated AI operations teams. Vendors that can simplify adoption without removing control are likely to perform well in this customer tier. Over time, SME expansion could become one of the strongest volume drivers for the AI-powered marketing platform market, even if large enterprises remain the largest source of revenue.

By End-User Industry: Retail and E-Commerce Lead While Media and Entertainment Scales Faster

Retail and e-commerce accounted for a 26.83% share in 2025, maintaining the sector's leading position in end-user demand. This leadership makes sense because the AI-powered marketing platform aligns well with retail needs, including personalization, campaign timing, product promotion, and measurable conversion paths. Retail users also tend to have richer customer interaction data, which supports more frequent testing and more immediate optimization. In contrast, media and entertainment are projected to grow at 21.49% CAGR through 2031, reflecting stronger demand for audience retention, subscriber engagement, and personalized recommendation-related outreach. The AI-powered marketing platform market, therefore, serves two distinct but related needs: direct conversion support in commerce and continuous attention management in media.

Other industries are expanding with different limits and different priorities. BFSI users are interested in next-best-action and retention workflows, but they often move carefully because review, risk, and governance requirements are stricter. Healthcare and life sciences are exploring more compliant engagement models, especially where communication quality and data handling need closer control. IT and telecom remain relevant because churn prediction, upgrade campaigns, and service recommendations fit well with AI-led decision systems. Manufacturing and public-sector use cases are smaller today, yet they can grow as digital engagement maturity improves and internal workflows become more data-ready. Across sectors, the AI-powered marketing platform industry is gradually shifting from broad experimentation to more use-case-specific deployment, which should support steadier adoption quality over the forecast period.

Geography Analysis

North America held 34.62% of the AI-powered marketing platform market share in 2025, which made it the largest regional contributor. The region benefits from dense digital advertising activity, a large installed base of enterprise software, and proximity to several major platform vendors and cloud providers. In the AI-powered marketing platform market, that combination supports faster product rollout, stronger partner networks, and broader enterprise familiarity with martech buying models. The United States remains the main regional driver because large organizations there are moving quickly from testing AI features to redesigning workflows around them. Canada and Mexico add incremental demand, particularly where retail, financial services, and customer engagement use cases continue to digitize. Even so, North America is no longer the only center of momentum, as other regions are expanding their adoption base through distinct demand patterns.

Asia-Pacific is projected to expand at 22.93% CAGR through 2031, giving it the strongest growth rate in the AI-powered marketing platform market size during the forecast period. Growth is being supported by faster SME digitization, expanding online commerce activity, and a broader willingness to adopt newer operating tools that rely on lighter legacy infrastructure. China stands out as a distinct environment within the AI-powered marketing platform market because domestic ecosystems and local platform structures shape vendor access differently from open global markets. India is emerging as a major open-access opportunity, helped by a broadening digital business base and more technology adoption among smaller firms. Japan and South Korea remain important because they combine high digital expectations with mature consumer engagement environments. Southeast Asia and Australia also contribute through rising investment in customer data foundations and campaign modernization across regional businesses.

Europe remains a major part of the global AI-powered marketing platform market, although buying behavior there is often shaped by stricter governance expectations and more deliberate rollout processes. Germany and the United Kingdom are central regional markets because they combine large enterprise bases with meaningful demand for customer engagement and digital experience tools. The AI-powered marketing platform market in Europe is therefore attractive, but vendors often need stronger compliance positioning and more careful deployment planning to grow consistently. South America is smaller, yet it continues to build relevance through digital commerce growth and rising interest in measurable marketing activation. The Middle East and Africa are still emerging, though investment is improving as brands and agencies modernize customer engagement models. Across all three regions, the AI-powered marketing platform market is advancing unevenly, indicating that vendors need localized commercial strategies rather than a single global playbook.

Competitive Landscape

The AI-powered marketing platform market is moderately consolidated at the top, with Salesforce, Adobe, HubSpot, Oracle, and Microsoft collectively controlling an estimated 45-50% of 2025 revenue. That concentration is meaningful, but it still leaves room for many specialized vendors because no single company leads every use case, customer segment, or deployment model. The AI-powered marketing platform market, therefore, combines large enterprise suites with a wide field of focused providers that compete on speed, industry depth, or workflow specialization. One major line of competition now centers on who can connect customer data, content generation, orchestration, and activation most effectively within a single operating environment. This is pushing large vendors to position their products less as isolated applications and more as connected execution systems. It also favors firms that can show clearer operating value rather than only broader feature counts.

Recent strategic moves show how the leading group is trying to strengthen that position. Adobe unveiled CX Enterprise Coworker in April 2026 as an orchestration layer across Experience Cloud, Real-Time CDP, and GenStudio, signaling a stronger push to unify data, content, and agent-led execution inside its ecosystem. Microsoft and Publicis expanded their strategic partnership in April 2026 to build a full-stack AI marketing solution, underscoring the importance of aligning cloud infrastructure, productivity software, and agency execution within a single commercial model. Sprinklr’s Spring ’26 release added broader AI agents, conversational analytics, and stronger compliance controls, showing that governance and telemetry are becoming competitive features rather than back-end support tools. These moves suggest that future competition in the AI-powered marketing platform market will depend as much on operating design and trust controls as on campaign functionality alone. They also show that vendors are trying to reduce friction between planning, production, approval, and activation.

A second competitive shift is emerging around conversational discovery and commerce environments. Amazon introduced Alexa+ Agentic Ads in 2026, indicating that the AI-powered marketing platform market is moving toward interfaces where customers explore, compare, and purchase through ongoing dialogue rather than fixed search steps. That change creates new opportunities for providers that can adapt content, targeting logic, and measurement to conversational surfaces. It also raises the value of interoperability, because brands will expect campaign assets and audience logic to move across more systems without manual rebuilding. Mid-market challengers still have room to compete when they offer faster implementation or stronger vertical fit, especially for buyers who do not want a full-suite commitment. Overall, the AI-powered marketing platform market remains open enough to support new wins, but scale, data connectivity, and governance discipline are becoming harder advantages to challenge.

AI-Powered Marketing Platform Industry Leaders

Adobe Inc.

Salesforce, Inc.

HubSpot, Inc.

Oracle Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Amazon introduced Alexa+ Agentic Ads at Cannes Lions 2026, launching conversational and agentic ad formats in beta on Echo Show devices, with Papa Johns and The Orchard as early brand partners and Fire TV expansion planned for the second half of 2026.

- April 2026: Adobe announced support for ChatGPT Ads in GenStudio for Performance Marketing on April 20, 2026, enabling brands to assemble and activate ads directly across conversational AI surfaces, extending the content supply chain into agent-mediated consumer discovery.

- April 2026: Adobe unveiled CX Enterprise Coworker at Adobe Summit on April 20, 2026, building an agentic orchestration layer across Experience Cloud, Real-Time CDP, and GenStudio using open MCP and A2A standards with interoperability across Amazon Web Services, Anthropic, Google Cloud, Microsoft, and OpenAI.

- April 2026: Microsoft and Publicis Groupe expanded their strategic partnership on April 8, 2026, to build a full-stack AI marketing solution. The deal equips all 114,000+ Publicis employees worldwide with Microsoft 365 Copilot, designates Microsoft Azure as Publicis' preferred cloud provider, and appoints Publicis as Microsoft's global media agency of record.

Global AI-Powered Marketing Platform Market Report Scope

The AI-powered marketing platform market encompasses software solutions and associated services that leverage artificial intelligence, machine learning, and natural language processing to automate, optimize, and enhance marketing processes. These platforms enable organizations to move beyond traditional rule-based marketing by leveraging advanced algorithms for AI-generated content, predictive marketing analytics, customer intelligence and personalization, campaign management and optimization, marketing automation, and conversational marketing (such as intelligent chatbots). Deployed across cloud, on-premises, and hybrid environments, these platforms cater to large, medium, and small enterprises across industries such as retail, BFSI, and healthcare. By analyzing vast amounts of customer data in real-time, AI-powered marketing platforms empower businesses to deliver highly personalized customer experiences, optimize marketing spend, accurately predict consumer behavior, and drive higher engagement and conversion rates.

The AI-Powered Marketing Platform Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Application (AI Content Generation, Predictive Marketing Analytics, Customer Intelligence and Personalization, Campaign Management and Optimization, Marketing Automation, and Conversational Marketing), Enterprise Size (Large Enterprises, and Small And Medium Enterprises), End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| AI Content Generation |

| Predictive Marketing Analytics |

| Customer Intelligence and Personalization |

| Campaign Management and Optimization |

| Marketing Automation |

| Conversational Marketing |

| Large Enterprises |

| Small And Medium Enterprises |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | Cloud-Based | ||

| On-Premise | |||

| Hybrid | |||

| By Application | AI Content Generation | ||

| Predictive Marketing Analytics | |||

| Customer Intelligence and Personalization | |||

| Campaign Management and Optimization | |||

| Marketing Automation | |||

| Conversational Marketing | |||

| By Enterprise Size | Large Enterprises | ||

| Small And Medium Enterprises | |||

| By End-User Industry | Retail and E-Commerce | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| IT and Telecom | |||

| Media and Entertainment | |||

| Industrial Manufacturing | |||

| Government and Public Administration | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the AI-powered marketing platform market size in 2026?

The AI-powered marketing platform market was estimated at USD 11.97 billion in 2026 and is forecast to reach USD 28.37 billion by 2031, growing at an 18.84% CAGR over 2026-2031.

What is driving growth in AI-powered marketing platforms?

Demand is being driven by real-time personalization, broader use of agent-led workflows, first-party data activation, and the need to produce more content across more channels without similar headcount growth.

Which application area is leading revenue today?

Marketing automation held the largest application share at 24.36% in 2025, reflecting its long-standing role in campaign workflows, lead management, and multichannel execution.

Which application is expanding the fastest through 2031?

AI content generation is projected to grow at a 23.74% CAGR through 2031 as enterprises connect content creation with review, activation, and conversational delivery surfaces.

Which customer group is creating the strongest growth opportunity?

SMEs are projected to grow at a 22.18% CAGR through 2031, showing that adoption is spreading beyond large enterprises as pricing, onboarding, and packaged use cases become more accessible.

Which region offers the strongest growth outlook?

Asia-Pacific is expected to record the fastest regional expansion at a 22.93% CAGR through 2031, while North America remained the largest region with a 34.62% share in 2025.

Page last updated on: