Offset Printing Blankets Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

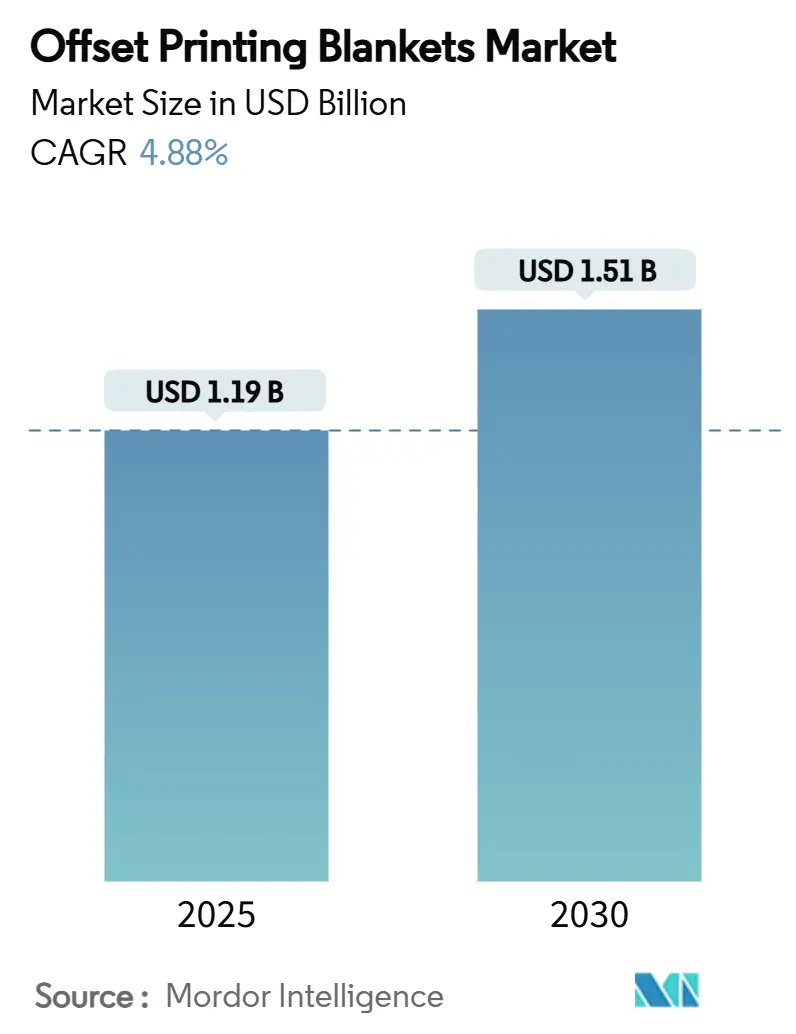

| Market Size (2025) | USD 1.19 Billion |

| Market Size (2030) | USD 1.51 Billion |

| Growth Rate (2025 - 2030) | 4.88% CAGR |

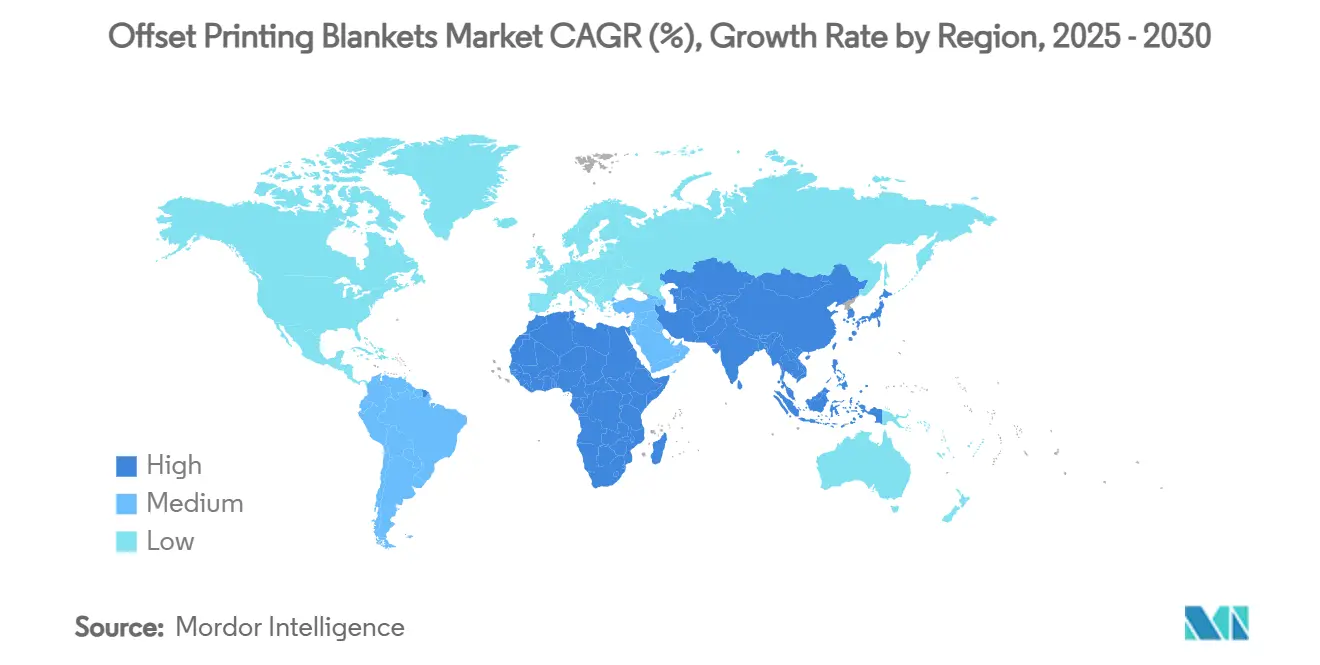

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Offset Printing Blankets Market Analysis by Mordor Intelligence

The Offset Printing Blankets Market size is estimated at USD 1.19 billion in 2025, and is expected to reach USD 1.51 billion by 2030, at a CAGR of 4.88% during the forecast period (2025-2030). Rising demand from packaging converters, rapid uptake of UV-LED presses, and sustained investments in Asia-Pacific printing capacity underpin this expansion. Sheetfed presses remain the workhorse for high-volume commercial work, yet the pivot toward packaging accelerates blanket replacement cycles, lifts average selling prices, and compels vendors to offer higher-performance, specialty coatings. Hybrid UV/H-UV compatible products are gaining traction because they enable printers to switch between conventional and energy-curable inks without costly blanket changes. Supply-side innovations, multi-layer compressible carcasses, solvent-resistant surface layers, and recycling programs help printers meet productivity and sustainability targets. Meanwhile, raw-material volatility and digital cannibalization in mature book and newspaper segments temper growth but do not derail the broader upward trajectory of the offset printing blankets market.

Key Report Takeaways

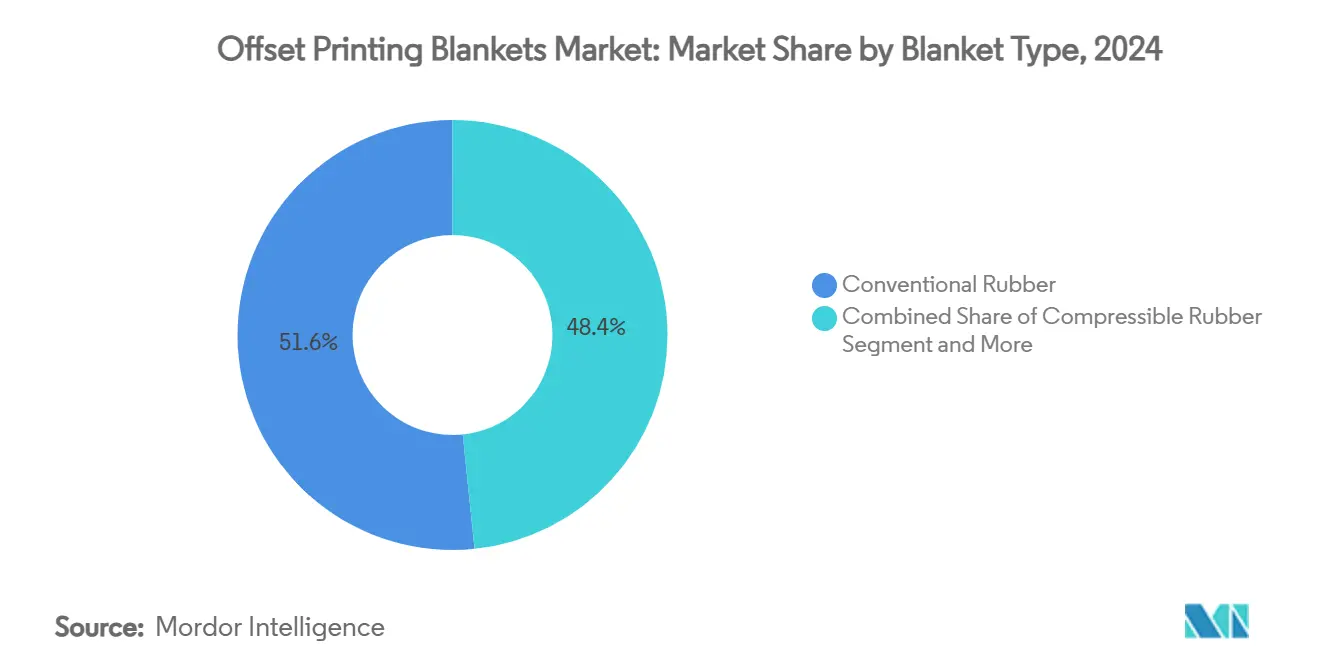

- By blanket type, conventional rubber retained the largest 51.63% offset printing blankets market share in 2024.

- By printing process, packaging and label offset is projected to expand at a 5.92% CAGR between 2025-2030.

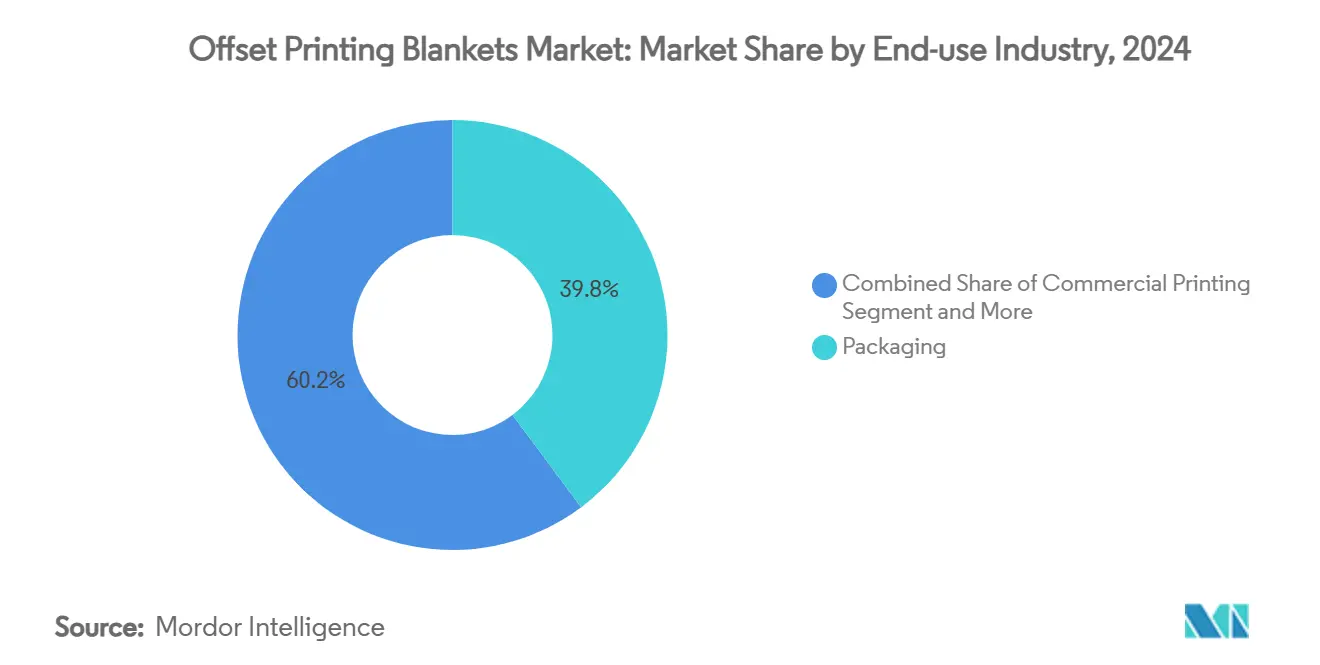

- By end-use industry, packaging commanded 39.78% of the offset printing blankets market share in 2024.

- By geography, Asia-Pacific is projected to grow at 6.15% CAGR between 2025-2030.

Global Offset Printing Blankets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for offset packaging printing | +1.8% | Global (APAC lead) | Medium term (2-4 years) |

| Technological advances in compressible blankets | +0.9% | North America and Europe | Long term (≥ 4 years) |

| Growing capacity additions in emerging-market commercial print | +1.2% | APAC core, MEA spill-over | Short term (≤ 2 years) |

| Adoption of hybrid UV-LED offset presses | +0.7% | Europe and North America early adopters | Medium term (2-4 years) |

| Surge in metal container offset decoration | +0.4% | Global, beverage focus | Short term (≤ 2 years) |

| Sustainability-driven recyclable blanket programs | +0.3% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Offset Packaging Printing

Packaging converters are scaling offset capacity to meet e-commerce growth, quick-service food trends, and brand owners’ sustainability mandates. The packaging end-use segment already controls 39.78% of revenue and will grow at a 6.01% CAGR as printers invest in multi-color, large-format presses that require durable blankets capable of handling recycled, coated, and kraft substrates.[1]Heidelberg Press Release, “Packaging Drives Heidelberg Revenue,” heidelberg.comHeidelberg notes packaging now delivers more than half of its turnover, and Crown Holdings logged 6% beverage-can volume growth in 2024 on the back of two new United States lines.[2]Crown Holdings Investor Sheet, “North American Beverage Growth,” crowncork.com Government procurement rules favor fiber-based formats, intensifying offset-printed board demand.

Technological Advances in Compressible Blankets

Material science breakthroughs, including precision-engineered micro-cell layers and solvent-resistant elastomers, boost blanket longevity on high-speed packaging presses. Continental’s 2024 investor deck underlined a push toward customized compressible profiles that cut dot gain while resisting gauge loss under 1,500 N/cm squeeze loads. Research on bio-based polyisoprene from Scorzonera tau-saghyz feeds future formulations that mitigate crude-oil price swings.

Growing Capacity Additions in Emerging-Market Commercial Print

China, India, and Indonesia are commissioning new 16-page web offset lines and two-meter-wide sheetfed presses to serve education materials and export packaging. World Bank trade data show the United States imported USD 409.25 million of paper and board in 2023, underscoring cross-border supply chains that ripple back to blanket suppliers. Rapid installations translate to higher initial blanket pull-through, while shorter replacement cycles fuel recurring revenue.

Adoption of Hybrid UV-LED Offset Presses

Printers seeking low-energy curing, no-powder finishes, and expanded substrate latitude are migrating to LED systems that demand UV-compatible blankets capable of handling 450 nm irradiance without embrittlement. European OEMs now offer retrofits that let operators switch from conventional to LED inks in minutes, spurring blanket makers to release dual-purpose surfaces. The U.S. Environmental Protection Agency links LED curing to a 50% cut in VOC emissions compared with mercury-arc UV lamps, giving adopters regulatory relief and energy savings.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital printing cannibalization of long-run offset | -1.4% | Global, with North America and Europe most affected | Medium term (2-4 years) |

| Raw-material (synthetic rubber, fabric) price volatility | -0.8% | Global supply chain impact | Short term (≤ 2 years) |

| Press automation extending blanket life cycles | -0.6% | North America and Europe advanced markets | Long term (≥ 4 years) |

| Nitrile-rubber supply-chain disruptions | -0.5% | Global, with Asia-Pacific production concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital Printing Cannibalization of Long-Run Offset

Inkjet sheetfed presses now hit 25,000 sph, eroding run lengths below 2,000 sheets. Heidelberg projects the accessible digital segment for its portfolio will climb from EUR 5 billion (USD 5.4 billion) in 2025 to EUR 7.5 billion (USD 8.1 billion) by 2029, a clear signal that some offset blankets will come off pressroom shopping lists.[3]Heidelberg Annual Report 2025, heidelberg.com Newspapers and catalogs remain most exposed, compelling blanket vendors to refocus on packaging niches where digital economics still lag.

Raw-Material Price Volatility

Synthetic nitrile, butadiene, and cotton duck prices jumped 16% year on year in 2024 on petrochemical feedstock spikes and shipping bottlenecks. The White House supply-chain review flagged tires, hoses, and printing blankets as areas vulnerable to geopolitical shocks, prompting OEMs to dual-source and increase stock buffers. Smaller regional converters struggle to absorb surcharges, slowing blanket changeovers during inflationary spikes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Blanket Type: UV-Compatible Technology Gains Momentum

Conventional rubber solutions occupied 51.63% of 2024 revenue, affirming their entrenched role in book, directory, and mainstream commercial work. Yet UV/H-UV engineered products will outpace every other category with a 5.89% CAGR because hybrid presses need surfaces that endure both oxidative and energy-curable chemistries without glazing. The offset printing blankets market size for UV/H-UV variants is forecast to rise from USD 342 million in 2025 to USD 456 million in 2030, fueled by printers wanting one blanket for mixed-ink jobs. Compressible carcass designs cushion substrate roughness, lowering makeready waste and helping converters hit sustainability KPI targets. Metal-backed styles thrive inside beverage-can decorators where their dimensional stability withstands 600 m/min line speeds. Hybrid designs that marry a litho surface to a strippable photopolymer under-layer remain niche but illustrate how R&D is stretching performance boundaries within the offset printing blankets market.

Second-generation UV/H-UV products feature low-swelling EPDM blends, nanoparticle top coats for chemical resistance, and lapped-joint carcasses that limit vibration. Continental’s Multi-Density sleeve technology gives variable compressibility zones so operators can calibrate image and non-image areas independently. Suppliers now bundle spectral-tuning databases that guide printers in choosing blanket-ink combinations, shrinking trial-and-error downtime. End-of-life programs pick up used sheets, strip aluminum bars, and recover EPDM crumbs for playground flooring, integrating circularity into the offset printing blankets market. The net result is a segment rapidly migrating from commodity black blankets to differentiated, higher-margin skews that underpin supplier profitability.

By Printing Process: Packaging Applications Drive Growth

Sheetfed offset systems contributed 43.14% of 2024 turnover, underpinned by ubiquitous B1 and B2 presses that churn out brochures, folding cartons, and premium magazines. Nevertheless, packaging and label lines will register the quickest 5.92% CAGR as brand owners shift from plastic to fiber-based formats. The offset printing blankets market share for packaging/label presses is projected to edge from 27.8% in 2025 to 31.4% in 2030 as converters roll out seven-color configurations, inline cold-foil, and LED varnishing. Heatset web lines that once dominated catalogs now face volume leakage; however, double-width coldset presses find new life printing corrugated pre-print liners, keeping blanket demand steady.

Process innovation is visible in in-line color control, autonomous plate changes, and AI-driven inspection that raise OEE beyond 85 %. These platforms need blankets with tighter thickness tolerances (< ± 0.015 mm) and minimal gauge loss over 3 M impressions. Printers moving into corrugate top-sheet lamination are championing softer blankets to compensate for flute variations. Label houses adopt dedicated small-format sheetfed units to reclaim jobs previously handled on flexo. Blanket vendors respond with portfolio breadth-waterless silicone-based variants for shrink sleeves, and metal-backed offset sleeves for wide web pre-print. Collectively, these shifts reinforce why packaging remains the gravitational center of the offset printing blankets market.

By End-use Industry: Packaging Sector Leads Market Evolution

Packaging held a 39.78% revenue slice in 2024 and is scaling at a 6.01% CAGR, driven by the increasing demand for e-commerce parcels, meal-kit sleeves, and beverage can graphics. The offset printing blankets market size serving packaging applications is expected to expand from USD 475 million in 2025 to USD 639 million in 2030. Commercial print retains relevance for corporate collateral and direct mail but faces run-length shrinkage that pushes printers to optimize blanket life over maximizing inventory turns. Newspaper and directory work remains in structural decline, driving blanket makers to sunset many newsprint-oriented SKUs.

Metal packaging, specifically two-piece can decoration, provides a high-volume niche where blanket exchange intervals align with cylinder refurb cycles, offering predictable replacement revenue. Security print-tax stamps, visas, and anti-counterfeit layers require blanket surfaces that support magnetic inks and optically variable pigments without linting. Fiber-based flexible packs emerge as an adjacent growth zone because they leverage offset’s fine-screen capability while answering plastic-reduction mandates. Billerud’s pulp-based barrier papers exemplify substrates that offset printers are now adopting, catalyzing demand for softer, low-smash blankets. Across these verticals, sustainability and substrate variety continue to steer R&D spend within the offset printing blankets market.

Geography Analysis

Asia-Pacific accounted for 33.37% of global revenue in 2024 and will pace the field with a 6.15% CAGR to 2030, driven by China’s carton mega-plants, India’s rising literacy, and ASEAN’s consumer boom. Domestic OEMs supply mid-tier presses, while European builders capture the high-end folding-carton segment, resulting in a hybrid installed base that multiplies blanket SKUs. Local natural-rubber availability in Thailand, Vietnam, and Malaysia keeps freight costs low and lets suppliers offer rapid make-to-order service. Government incentives such as China’s “Green Printing” certification push converters toward low-VOC UV chemistries, accelerating UV-ready blanket sales. Regional players often sign technical-licensing deals with Western brands, ensuring technology transfer but intensifying price competition within the offset printing blankets market.

North America remains sizable but mature; packaging growth offsets softness in publication volumes. The Biden administration’s supply-chain resilience blueprint encourages dual sourcing, nudging converters to favor United States-based blanket slitters. LED-retrofit grants in California and New York stimulate demand for dual-cure blankets. Meanwhile, Europe anchors high-margin opportunities, propelled by extended-producer-responsibility laws that reward recyclable blanket programs. Germany and Italy maintain leadership in press engineering, enabling tight supplier–OEM partnerships that speed new blanket approvals.

South America and the Middle East/Africa together hold under 15% revenue today yet show double-digit unit growth as consumer staples packaging proliferates. Brazilian cartonboard mills commission additional sheeters, requiring regional blanket stocks to avoid costly imports. In the Gulf Cooperation Council, beverage can plants in Saudi Arabia and the UAE lift demand for metal-backed blankets. Africa’s newspaper consolidation frees press capacity for educational textbook work, increasing blanket changeovers. Despite logistical hurdles, these regions represent the next frontier for volume gains, prompting multinational suppliers to establish satellite refurb hubs and digital tech-support platforms to serve the expanding offset printing blankets market.

Competitive Landscape

Competition is moderately fragmented: the top five vendors control roughly 50% of sales, leaving ample headroom for regional specialists. Trelleborg AB leverages its SEK 34 billion diversified portfolio and proprietary polymer labs to cross-sell blankets into food, beverage, and security print, reinforcing stickiness through service contracts. Continental pushes a material-science narrative, marketing multi-density compressible structures and bio-based elastomers to differentiate beyond price. Flint Group couples blanket supply with plate chemistry, exploiting bundled procurement deals with multi-site packaging groups.

Midsize challengers in China and Turkey undercut on price yet climb the value ladder via joint ventures with Japanese carcass weavers. European SMEs focus on bespoke, small-lot blankets-niche web widths, ceramic-coated tops, and specialty heat-resistant backings, catering to security and banknote printers. Technology raceways now center on UV-compatibility, surface-energy tuning, and closed-loop recycling. Vendors incorporating RFID-tagged serial numbers into blankets enable predictive maintenance, an emerging service play that locks in customers for multi-year supply agreements.

Strategic maneuvers since 2024 include Heidelberg’s long-term supply contract with a leading blanket maker to secure UV-H-UV variants for its forthcoming B1 hybrid press line; Trelleborg’s acquisition of a Brazilian blanket refurbisher to bolster Latin American reach; and Continental’s minority stake in an Indian natural-rubber plantation to hedge against feedstock volatility. Collectively, these moves highlight how vertical integration, sustainability, and geographic adjacency define winning strategies in the offset printing blankets market.

Offset Printing Blankets Industry Leaders

Trelleborg AB (Vulcan, Rollin, Printec)

Continental AG (PHOENIX Xtra Blankets)

Flint Group (Day International)

Kinyo (Kinyosha Group)

Fujikura Rubber Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Heidelberger Druckmaschinen AG reported FY 2024/25 sales of EUR 2,280 million (USD 2,467 million) with 7.1% EBITDA margin and signaled a FY 2025/26 sales target of EUR 2,350 million (USD 2,543 million).

- April 2025: Billerud’s Q1 2025 report posted SEK 11,101 million (USD 1,049 million) in net sales, a 7% year-on-year rise, driven by United States cartonboard demand.

- January 2024: Heidelberger Druckmaschinen AG outlined a EUR 300 million (USD 324 million) growth roadmap to 2029 focused on packaging and digital press segments.

- September 2024: United States Department of Commerce issued final anti-dumping margins of 91.83% on Japanese aluminum lithographic plates, affecting upstream offset consumables pricing.

Global Offset Printing Blankets Market Report Scope

| Conventional Rubber |

| Compressible Rubber |

| UV / H-UV Compatible |

| Hybrid Blankets |

| Metal-Backed |

| Sheetfed Offset |

| Heatset Web Offset |

| Coldset Web Offset |

| Commercial and Publishing Offset |

| Packaging and Label Offset |

| Packaging |

| Commercial Printing |

| Newspaper and Publishing |

| Metal Cans and Beverage |

| Label and Security Printing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Blanket Type | Conventional Rubber | ||

| Compressible Rubber | |||

| UV / H-UV Compatible | |||

| Hybrid Blankets | |||

| Metal-Backed | |||

| By Printing Process | Sheetfed Offset | ||

| Heatset Web Offset | |||

| Coldset Web Offset | |||

| Commercial and Publishing Offset | |||

| Packaging and Label Offset | |||

| By End-use Industry | Packaging | ||

| Commercial Printing | |||

| Newspaper and Publishing | |||

| Metal Cans and Beverage | |||

| Label and Security Printing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the offset printing blankets market?

The market is valued at USD 1.19 billion in 2025 and is projected to rise to USD 1.51 billion by 2030.

Which end-use industry drives the strongest growth?

Packaging leads with a 39.78% revenue share in 2024 and a forecast 6.01% CAGR, reflecting e-commerce and sustainability momentum.

Why are UV/H-UV compatible blankets gaining popularity?

Hybrid UV-LED presses require blankets that withstand both conventional and energy-curable inks, pushing demand for UV-ready surfaces that also enable lower VOC printing.

How is Asia-Pacific influencing global demand?

Asia-Pacific holds 33.37% of revenue and logs a 6.15% CAGR, supported by large-scale press installations and domestic natural-rubber supply chains.

Page last updated on: