Direct-to-Garment Printing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

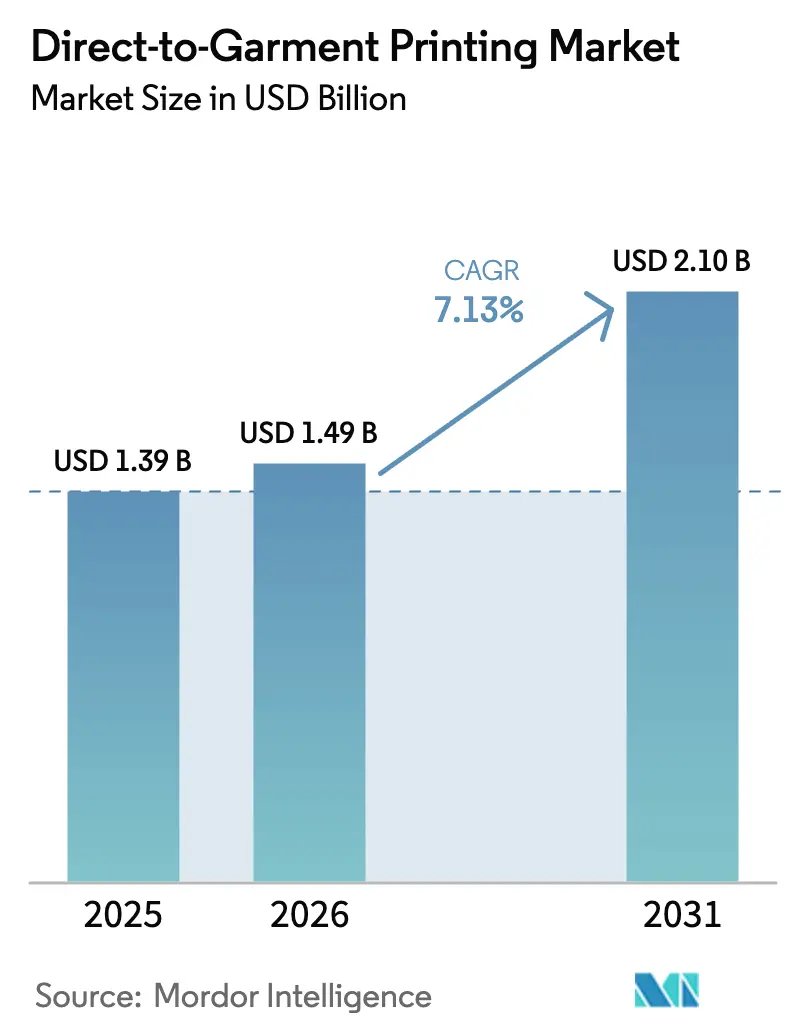

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 2.1 Billion |

| Growth Rate (2026 - 2031) | 7.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

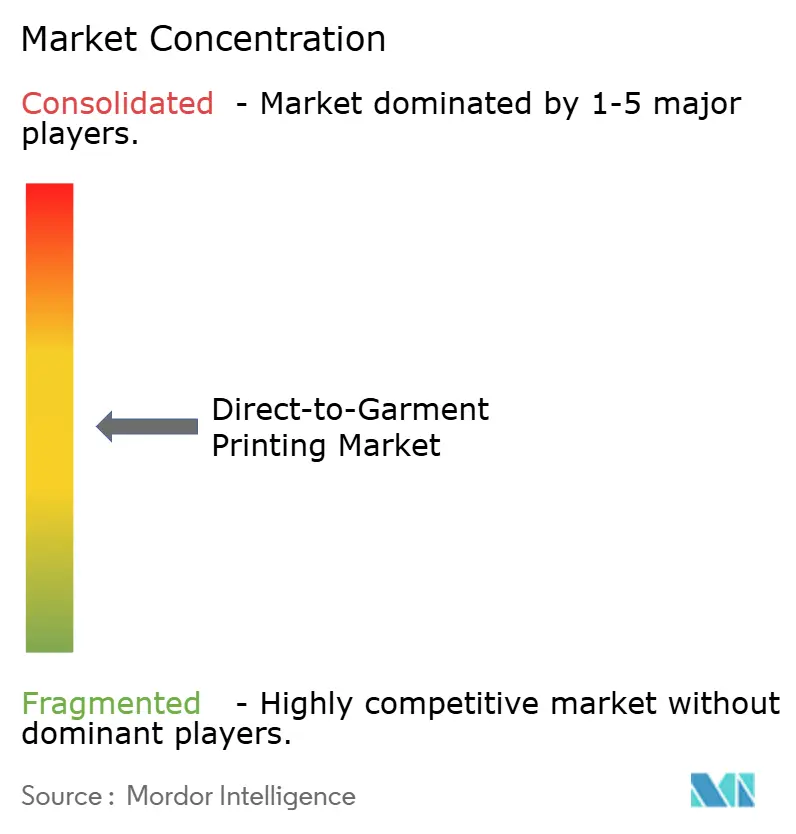

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Direct-to-Garment Printing Market Analysis by Mordor Intelligence

The Direct-to-Garment Printing market size was valued at USD 1.39 billion in 2025 and estimated to grow from USD 1.49 billion in 2026 to reach USD 2.10 billion by 2031, at a CAGR of 7.13% during the forecast period (2026-2031). The shift from analog screen print methods toward fully digital workflows underpins this advance, as e-commerce brands demand rapid personalization, lower inventory risk, and micro-factory proximity to end users. Adoption accelerates where industrial automation merges with pigment-inkjet technology, dropping per-print costs enough to make even single-unit jobs profitable for print service providers. Asian governments add momentum through targeted subsidies for digital textile equipment, shortening payback periods and pushing factories to upgrade their production floors. Meanwhile, the competitive field remains moderate: leading vendors differentiate primarily on throughput, ink chemistry, and automation suites rather than on headline price.

Key Report Takeaways

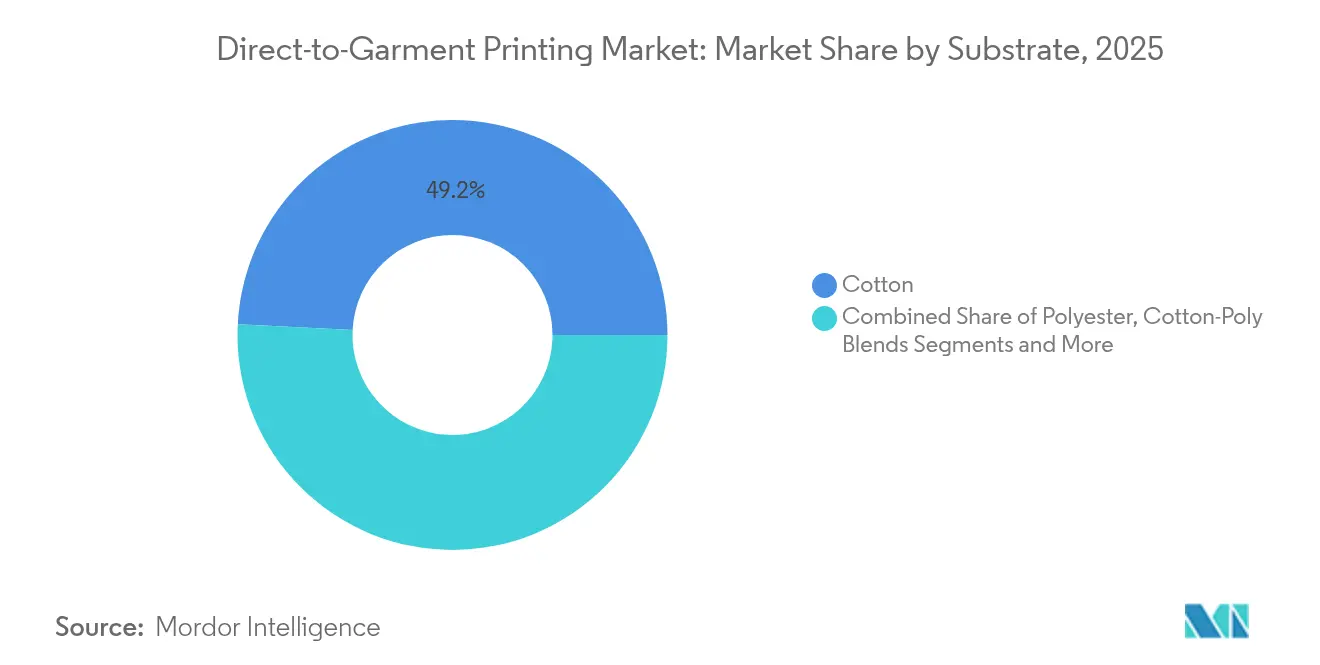

- By substrate, cotton retained 49.20% of Direct-to-Garment Printing market share in 2025, whereas polyester is projected to grow at a 7.27% CAGR between 2026-2031.

- By ink type, pigment formulations led with a 60.45% share of the Direct-to-Garment Printing market size in 2025; disperse inks are expected to climb at an 8.05% CAGR to 2031.

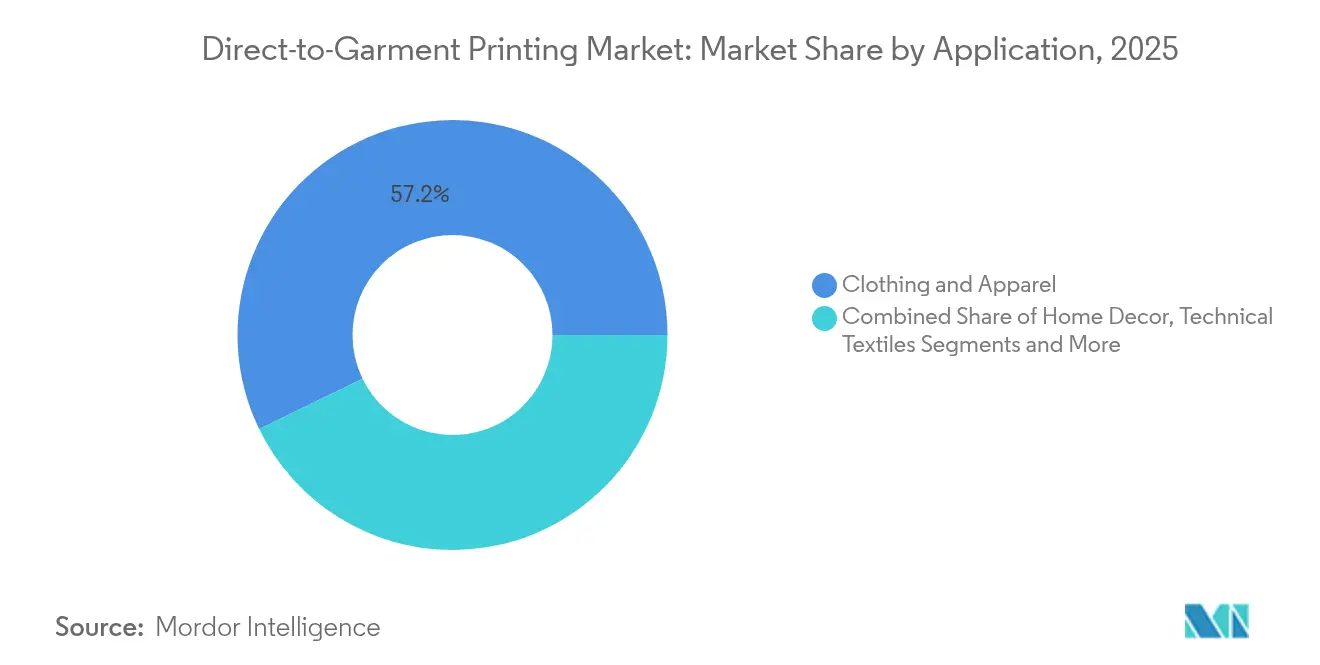

- By application, clothing and apparel captured 57.20% of Direct-to-Garment Printing market size in 2025, while technical textiles register the quickest advance at 8.43% CAGR.

- By sales channel, print service providers held 65.10% of Direct-to-Garment Printing market share in 2025, yet online fulfilment platforms are forecast to expand at 8.83% CAGR.

- By geography, North America commanded 39.10% of the Direct-to-Garment Printing market in 2025; Asia-Pacific is set to post a 7.55% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Direct-to-Garment Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mass-customisation boom in e-commerce apparel | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Shift from screen-print to pigment inkjet for micro-runs | +1.5% | Global, particularly Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Declining cost-per-print of industrial DTG lines | +1.2% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Government subsidies for digital textile equipment in Asia | +1.0% | Asia-Pacific core, spill-over to emerging markets | Long term (≥ 4 years) |

| Adoption of micro-factory models by fashion brands | +0.9% | North America and EU, expanding to urban centers globally | Medium term (2-4 years) |

| Bio-based pigment-ink compliance mandates | +0.8% | Europe leading, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mass-customisation boom in e-commerce apparel

Brands scale new on-demand models by plugging DTG APIs directly into storefront checkouts, so a shopper’s design flows straight to the press queue without human touchpoints. This immediacy eliminates minimum order quantities and allows real-time trend testing, cutting unsold stock while lifting full-price sell-through rates. Gen Z clients value individuality and reduced waste, making personalization a core purchase driver. Because platforms batch single orders from globally dispersed consumers into efficient production runs, they stabilize equipment utilization around the clock, reinforcing the Direct-to-Garment Printing market’s transformation from niche novelty to dependable manufacturing backbone.

Shift from screen print to pigment-inkjet for micro-runs

Analog screen set-up fees between USD 50-200 per color tip cost curves sharply upward as run sizes fall below 100 pieces. High-chroma pigment jetting reaches commercial wash fastness while bypassing screens entirely, letting printers turn profitable on single-item jobs. Customers of Kornit’s Apollo lines, such as Hybrid Digital in Florida, now drive mixed queues of 1-500 units without pausing for tool changes, a production agility screen presses cannot match.

Declining cost-per-print of industrial DTG lines

Hardware outlays per square meter continue to drop as printhead durability improves and closed-loop ink recirculation slashes waste. Epson’s SureColor G6070, introduced at USD 13,995, exemplifies this cost curve while bundling auto-maintenance firmware that pushes operator intervention to weekly instead of daily checks. Predictive analytics on nozzle health further reduces unplanned downtime, nudging the total cost of ownership below that of small automatic screen carousels in many plants.[1]Epson America, “SureColor G6070 Launch Details,” epson.com

Government subsidies for digital textile equipment in Asia

China’s Ministry of Industry and Information Technology mandates 70% digitalized textile capacity by 2025, while India’s 2025 Union Budget removes import duty on specific digital printers and grants quicker depreciation benefits. These policies can trim ROI horizons to 18-24 months for small and mid-sized converters, accelerating adoption in the Direct-to-Garment Printing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited pre-treatment compatibility with blended fabrics | -0.8% | Global, particularly affecting polyester-cotton blends | Short term (≤ 2 years) |

| High print-head replacement cost | -0.6% | Global, with higher impact in price-sensitive markets | Medium term (2-4 years) |

| Waste-water discharge regulations for small PSPs | -0.5% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Rising competition from DTF transfer systems | -0.7% | Global, with rapid adoption in cost-sensitive segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited pre-treatment compatibility with blended fabrics

Operators report color bleed and poor wash fastness when standard cotton pre-treat suites meet polyester-rich garments, forcing dual-line setups or costly reworks. Although suppliers such as Kyocera showcase single-step solutions, reliable mass-scale performance on tri-blends remains elusive. As a result, throughput drops and reprint rates climb, tempering Direct-to-Garment Printing market expansion on athleisure blends.

Rising competition from DTF transfer systems

Direct-to-film presses deposit inks on a carrier film before heat pressing to fabric, avoiding both fabric pre-treat and white-ink sediment issues. They run acceptably across cotton, polyester, and nylon, eroding DTG’s competitive moat, particularly among start-ups that value lower capex and simplified workflows. DuPont’s P1600 DTF inks underscore the technology’s mainstream trajectory, intensifying pressure on incumbent DTG vendors to speed R&D and lower consumable pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate: Cotton Dominance Faces Polyester Challenge

Cotton’s 49.20% command of Direct-to-Garment Printing market share in 2025 stems from predictable ink fixation and proven pre-treatment chemistries. However, polyester volumes accelerate at a 7.27% CAGR as performancewear and athleisure brands prioritize moisture management and durability. Producers of Direct-to-Garment Printing inks for polyester now leverage high-energy disperse pigments, while Kyocera’s FOREARTH platform, with its innovative technolgy implementation, prints these filaments without separate pre-treat cycles, saving water and energy per linear meter.

The hybrid cotton-poly segment advances fastest within polyester, marrying comfort with resilience for mid-market apparel. Silk and hemp remain niche yet profitable pockets because luxury brands value their tactile differentiation. Vendors who tune jetting algorithms for these emergent fibers gain early-mover prestige, laying ground for future revenue streams as sustainable textiles scale.

By Ink Type: Pigment Leadership Challenged by Disperse Innovation

Pigment liquids captured 60.45% of Direct-to-Garment Printing market size in 2025, propelled by rising compliance with global wastewater directives and simplified single-step workflows. EFI Reggiani’s ecoTERRA illustrates pigment chemistry’s evolution, bundling binder polymers that bond at lower cure temperatures while freeing lines from separate pre- and post-treat stations.

Conversely, disperse sets dash ahead at an 8.05% CAGR as polyester sportswear leaps forward. Because these dyes sublimate into synthetic fiber matrices, they deliver vibrant hues resistant to abrasion and chlorine exposure, traits vital in activewear. Reactive and acid recipes keep footholds in linen, wool, and silk but account for shrinking shares as brands consolidate ink inventories around versatile pigment and disperse families.

By Application: Technical Textiles Emerge as Growth Engine

Clothing and apparel still own 57.20% of Direct-to-Garment Printing market size, pooling demand from fashion labels, merch resellers, and influencer storefronts. Yet technical textiles sprint at 8.43% CAGR through 2031 thanks to automotive interiors, safety vests, and medical wraps that require crisp variable data prints for traceability codes and regulatory markings.

Home décor rides a parallel wave, with short-run drapery and upholstery patterns flying straight from digital design suites to DTG decks, bypassing rotary screens and their hefty minimums. Promotional eventwear and team kits likewise thrive, exploiting overnight turnarounds to capture last-minute orders traditional presses must decline.

By Sales Channel: Platform Models Disrupt Traditional PSPs

Print service providers still generated 65.10% of Direct-to-Garment Printing market revenue in 2025, but online fulfilment platforms outpace them at 8.83% CAGR. API-driven aggregators channel global demand into regional production nodes, smoothing seasonal load swings and unlocking incremental margin for small creators.

Meanwhile, brand-owned micro-factories spring up inside retail HQs, integrating sample approval, cutting, sewing, and DTG in one conveyor-style cell. These verticalized setups chop weeks from concept-to-rack cycles and gather real-time sell-through data to schedule replenishment prints automatically.

Geography Analysis

North America commands 39.10% of the Direct-to-Garment Printing market by leveraging entrenched e-commerce culture, a consumer base willing to pay for bespoke apparel, and integrated logistics that facilitate two-day delivery across the continent. Federal chemical regulations remain lighter than Europe’s, easing adoption of new ink sets, although corporate ESG pledges accelerate the shift to water-based systems. Nearshoring into Mexico and Canada further cements regional print volumes by slashing cross-Pacific transit costs.

Europe, while smaller in sheer volume, exerts outsized influence through strict REACH rules and Ecolabel criteria that spur global ink innovation. Germany and the UK pilot closed-loop pigment lines paired with renewable-energy curing tunnels, aligning with the bloc’s circular-economy directives. Luxury houses in France and Italy exploit DTG for on-demand monogramming and capsule collections, where razor-sharp detail trumps high-run economies.

Asia-Pacific posts the fastest advance at 7.55% CAGR as Beijing’s 70% textile-digitization mandate, India’s duty waivers on digital equipment, and Vietnam’s supplier-upgrade grants kick in. These policies buffer capital risk for mills pivoting from commoditized bulk export toward value-added customized runs. IFC’s USD 100 million financing to EPIC Group in Bangladesh and India underscores development-bank confidence in this digital pivot.

Competitive Landscape

Competition centres on throughput, ink chemistry, and workflow automation rather than race-to-bottom pricing. Kornit Digital’s automated Apollo cell prints up to 400 garments per hour with minimal operator input, giving customers predictable unit economics while retaining the flexibility of a digital file-driven process.[3]Kornit Digital, “Apollo Platform Overview,” kornit.com Epson broadens flank coverage by launching direct-to-film devices that tap adjacent polyester markets and shield share against DTF insurgents.

Brother Industries’ bid for Roland DG highlights growing consolidation as vendors seek synergies across wide-format graphics, textile, and industrial print segments. Ricoh builds European labs for textile-specific R&D and service, signalling deeper regional commitment amid tightening EU sustainability mandates. Start-ups focusing on AI-generated artwork and cloud-based order routing partner with OEMs to bundle software subscriptions that lock customers into their ecosystems.

Strategic moves stretch beyond hardware. Kornit’s USD 100 million share buyback signals confidence in margins tied to consumables and cloud services. Avient’s purchase of Magna Colours deepens its roster of water-based ink chemistries, reinforcing environmental credentials and widening channel reach among eco-conscious print shops.

Direct-to-Garment Printing Industry Leaders

Mimaki Engineering Co., Ltd.

Ricoh Company, Ltd.

Seiko Epson Corporation

The M&R Companies

aeoon Technologies GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Roland DG released the DIMENSE Module for Roland DG Connect Designer, introducing tactile 3-D texture capability for premium DTG pieces.

- May 2025: Mimaki Engineering unveiled UV-curable inks ELH and ELS that exclude SVHC and CMR substances to satisfy EU chemical-safety rules.

- April 2025: Epson set an official ship date for the SC-G6050 DTF printer, expanding its footprint into polyester-heavy segments.

- February 2025: Ricoh formed Ricoh Printing Solutions Europe Limited to consolidate industrial print lines and bolster regional technical support.

Global Direct-to-Garment Printing Market Report Scope

Direct-to-garment printing is the method used to print custom graphics and images directly onto pre-made clothing instead of rolls of textiles. Direct-to-garment printing technology extracts images directly from digital files for printing. This method empowers DTG printers to achieve a broad spectrum of colors with exceptional resolution and sharpness. DTG technology is versatile and can print on various fabrics, from traditional cotton to modern polyester and even blends. However, it excels particularly in natural fabrics. It offers highly detailed short production run prints for custom printing. Direct-to-garment (DTG) printing technology is at the forefront, delivering clear, high-quality images. Avoiding traditional setups and printing directly from digital files offers excellent flexibility, allowing textiles to be produced in any quantity. This new digital printing technology redefines aspects such as efficiency, quality, and customization options in the printing industry.

The direct-to-garment printing market is segmented by substrate (cotton, silk, polyester, and other substrates), ink (reactive, acid, and other inks), application (clothing and apparel, home decor, technical textiles, and other applications), and geography (North America [United States and Canada], Europe [United Kingdom, Germany, France, Italy, and Rest of Europe], Asia-Pacific [China, India, Japan, Australia and New Zealand, and Rest of Asia-Pacific], Latin America [Brazil, Mexico, Argentina, and Rest of Latin America], and Middle East and Africa [Saudi Arabia, South Africa, United Arab Emirates, and Rest of the Middle East and Africa]). The report offers market forecasts and size in value (USD) for all the above segments.

| Cotton |

| Polyester |

| Cotton-Poly Blends |

| Silk |

| Other Substrates |

| Pigment |

| Reactive |

| Acid |

| Disperse |

| Clothing and Apparel |

| Home Décor |

| Promotional and Sportswear |

| Technical Textiles |

| Print Service Providers (PSPs) |

| In-house/Brand-owned |

| Online Fulfilment Platforms |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Substrate | Cotton | ||

| Polyester | |||

| Cotton-Poly Blends | |||

| Silk | |||

| Other Substrates | |||

| By Ink Type | Pigment | ||

| Reactive | |||

| Acid | |||

| Disperse | |||

| By Application | Clothing and Apparel | ||

| Home Décor | |||

| Promotional and Sportswear | |||

| Technical Textiles | |||

| By Sales Channel | Print Service Providers (PSPs) | ||

| In-house/Brand-owned | |||

| Online Fulfilment Platforms | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Direct-to-Garment Printing market?

The market totals USD 1.49 billion in 2026 and is forecast to reach USD 2.10 billion by 2031.

Which substrate segment is expanding fastest?

Polyester is growing at a 7.27% CAGR, reflecting advances in pre-treat chemistry and sportswear demand.

How big is the opportunity for online fulfilment platforms?

While print service providers still dominate, platform-based channels are projected to rise at 8.83% CAGR through 2031, driven by direct-to-consumer business models.

Why are disperse inks gaining traction?

Disperse formulations bond effectively with polyester fibers, supporting bright colors and durability, and therefore expand at an 8.05% CAGR.

What role do Asian government policies play in adoption?

Subsidies and digitization mandates in China, India, and Vietnam shorten ROI periods to under two years, accelerating equipment uptake in the region.

Is direct-to-film technology a threat to DTG?

Yes. DTF’s compatibility with diverse fabrics and lower maintenance draws price-sensitive entrants, pressuring DTG vendors to innovate.

Page last updated on: