Non-woven Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

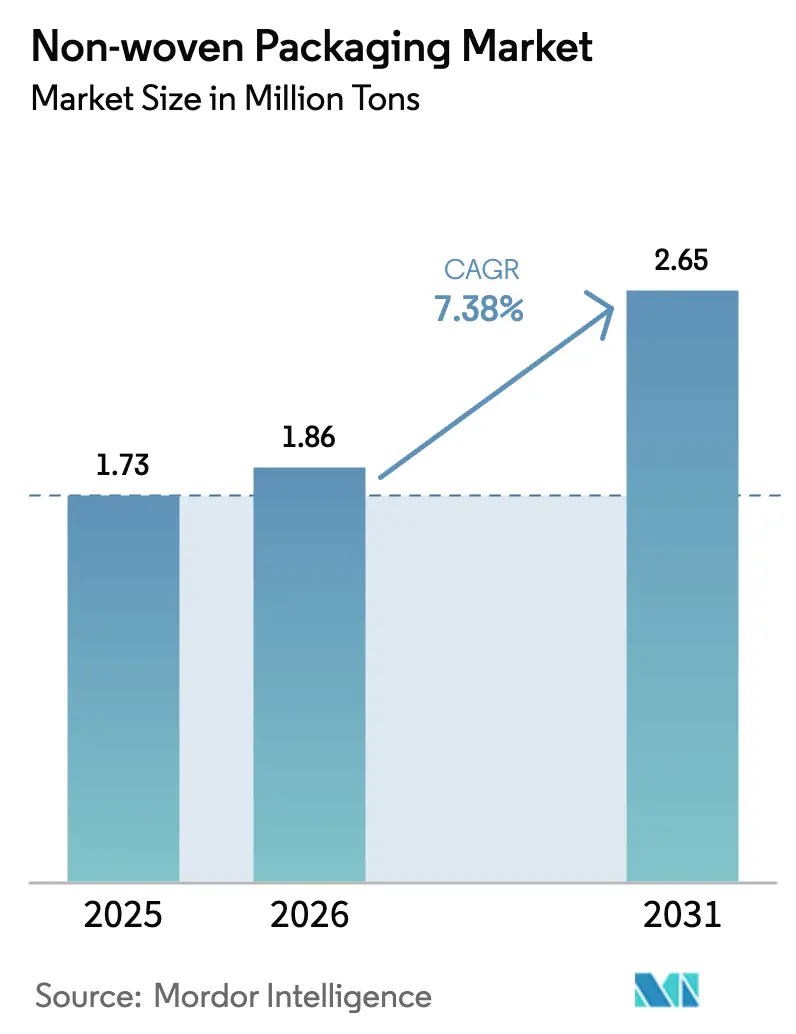

| Market Volume (2026) | 1.86 Million tons |

| Market Volume (2031) | 2.65 Million tons |

| Growth Rate (2026 - 2031) | 7.38% CAGR |

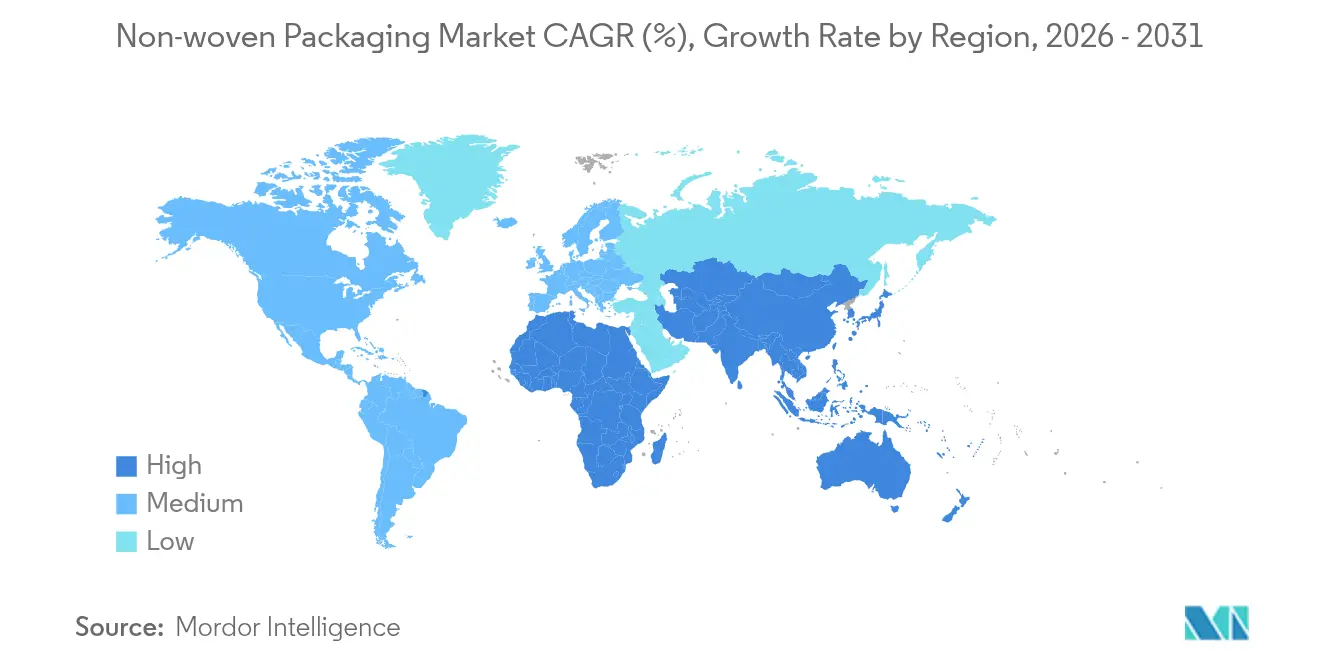

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

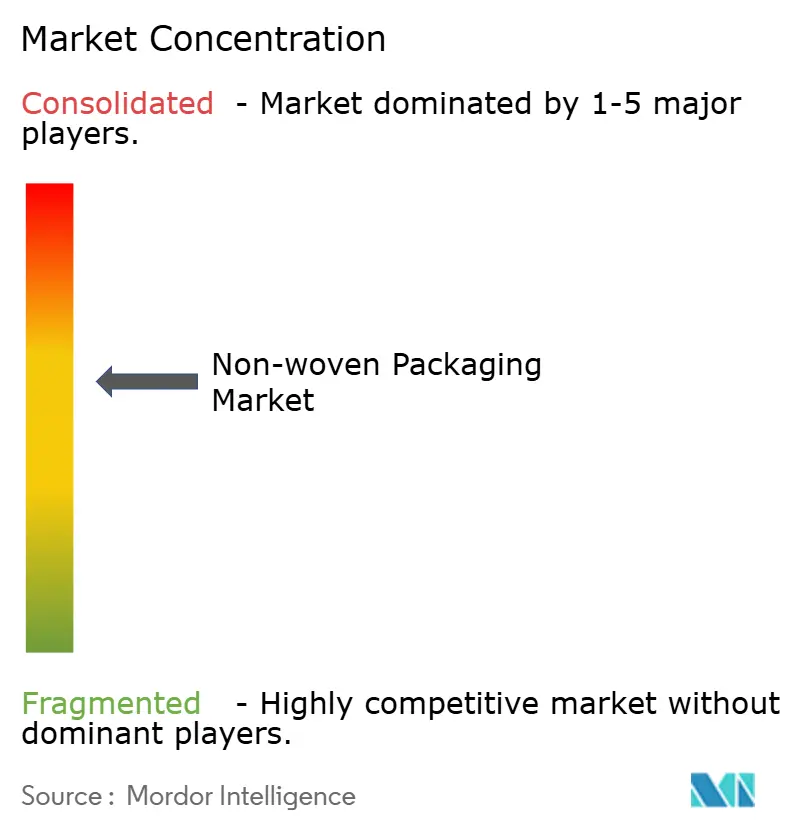

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-woven Packaging Market Analysis by Mordor Intelligence

The non-woven packaging market size was valued at 1.73 billion tons in 2025 and estimated to grow from 1.86 billion tons in 2026 to reach 2.65 billion tons by 2031, at a CAGR of 7.38% during the forecast period (2026-2031). Demand accelerates as regulators outlaw difficult-to-recycle plastics, e-commerce volumes swell, and healthcare, food, and agricultural users look for lighter, stronger, and readily recyclable wraps, sacks, and sterilization systems. Spun-laid production keeps costs low for mass-market formats, while melt-blown lines scale quickly for filtration-grade webs needed in medical and high-barrier food packs. Asia-Pacific maintains output leadership, yet African producers post the fastest gains on the back of new non-woven mills, better logistics corridors, and rising intra-regional trade. Consolidation continues, led by Amcor’s USD 8.4 billion agreement to absorb Berry Global, and Berry’s spin-off with Glatfelter that created a USD 3.6 billion specialty materials entity. Feedstock cost swings and tougher end-of-life rules remain the chief constraints, pushing converters toward bio-based polymers and monomaterial laminates that simplify recycling.

Key Report Takeaways

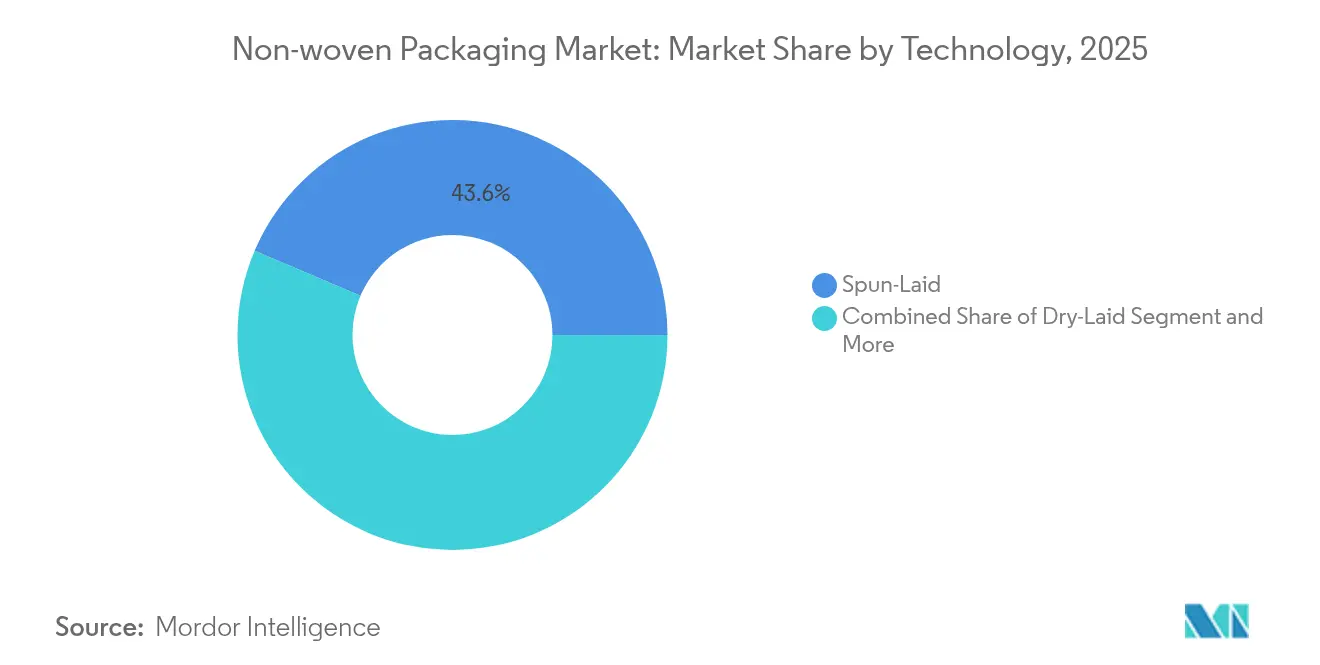

- By technology, spun-laid dominated with 43.60% of non-woven packaging market share in 2025; melt-blown is projected to advance at an 8.12% CAGR through 2031.

- By end-user packaging application, food and beverage held 37.10% revenue share in 2025, while medical and healthcare is forecast to grow at a 9.11% CAGR to 2031.

- By geography, Asia-Pacific led with 31.75% share in 2025; Africa is set to expand at an 7.99% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Non-woven Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable packaging mandates | +1.8% | North America and EU | Medium term (2-4 years) |

| Food-grade sacks, bags and wrap demand | +1.2% | Asia-Pacific and MEA | Short term (≤ 2 years) |

| E-commerce protective formats | +1.5% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Growth in medical PPE and sterilization wraps | +0.9% | Developed markets | Medium term (2-4 years) |

| Mono-material recyclable laminates | +0.8% | Europe and North America | Long term (≥ 4 years) |

| Bio-based polymer breakthroughs | +0.5% | Global early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Environmentally Sustainable Packaging

California’s SB 1046 bans single-use plastic carry-out bags that lack recyclability from January 2025, forcing retailers to shift to compostable non-woven substitutes that meet strict biodegradation criteria. Vermont’s statewide ban cut plastic bag consumption by 91% and achieved strong public approval, reinforcing the policy momentum that favors compostable PLA or cellulose non-woven formats.[1]University of Vermont, “The Impact of Vermont’s Single-Use Plastics Ban,” uvm.edu The Fraunhofer Institute demonstrated commercial-scale PLA film that fully decomposes under industrial composting and won the 2024 Joseph von Fraunhofer Prize, giving converters a proven high-performance substrate.

Rising Consumption in Food-Grade Sacks, Bags and Wrap

Retailers boost lightweight spunbond polypropylene sacks for staples, sauces, and ready meals to curb transport weight and avoid condensation. Non-woven crop and seed bulk bags unlock longer shelf life by regulating humidity inside the weave, a feature especially valued by Asian rice exporters. EU single-use rules further accelerate compostable pouch launches based on PLA webs with embedded non-woven filters for applications such as coffee pods released by NatureWorks in 2024.[2]NatureWorks LLC, “Ingeo PLA Compostable Coffee Pod Solution,” natureworksllc.com

E-Commerce Boom Fuelling Protective Non-Woven Formats

Parcel volumes surged in 2025 as global e-commerce packaging spending crossed USD 90 billion. Shippers replace bubble wrap with laminated spunbond sleeves that resist puncture yet recycle with PE film streams, reducing void space and freight costs without extra board liners. Chinese and Indian express operators adopt fanfold corrugated backed by melt-blown cushioning pads to standardize packaging lines and tame landfill taxes.

Proliferation of Medical PPE and Sterilization Wraps

Hospitals demand low-lint, gamma-stable sterilization wraps, steering melt-blown capacity toward finer fiber diameters. Kimberly-Clark’s Impervon range improved microbial barrier performance and withstands steam cycles, supporting pharmacy kit sterilization compliance. FDA-cleared vacuum-sealed aluminum alloy containers challenge porous wraps but still rely on non-woven filters at vent ports to equalize pressure without microbial ingress.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polypropylene and PET feedstock prices | -1.2% | Global, higher in Asia-Pacific | Short term (≤ 2 years) |

| Tightening single-use plastic legislation | -0.8% | Europe and North America | Medium term (2-4 years) |

| Competition from paper and bioplastic alternatives | -0.6% | Developed markets | Medium term (2-4 years) |

| Limited recycling infrastructure for composite webs | -0.4% | Developing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Polypropylene and PET Feedstock Prices

Raffia-grade polypropylene averaged USD 980 per metric ton in South Asia in March 2025, a 4% quarter-on-quarter rise that squeezed converter margins.[3] Polymerupdate, “South Asia Polypropylene Price Snapshot March 2025,” polymerupdate.com Crude-linked PTA and MEG hikes ripple into PET sheets, prompting moth-balled lines in Europe to curb losses. These gyrations push buyers toward fixed-price bio-based feedstocks, especially when carbon-tax exposure is considered.

Tightening Single-Use Plastic Legislation

California SB 54 compels a 25% cut in single-use plastic packaging by 2032 and places full recycling cost on producers. Germany’s mandatory reusable container rule lifted market share only to 1.6% in its first year, underlining consumer convenience hurdles yet signaling policymakers’ resolve. Non-woven suppliers must redesign laminated pouches so that entire substrates qualify for curbside collection or composting channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Spun-Laid Processes Sustain Cost Leadership

Spun-laid lines captured 43.60% of 2025 throughput on the strength of integrated fiber spinning and web consolidation that lowers unit cost and allows fabric weights below 15 gsm without sacrificing tensile strength. This cost edge keeps commodity sacks and agriculture row covers in the spun-laid camp. Melt-blown plants post the fastest gains at an 8.12% CAGR to 2031 as filtration-grade diameters below 2 µm become essential for sterile wraps and high-barrier snack packs. Dry-laid and hydro-entangled substrates retain niches in premium gift wraps and consumer wipes where hand feel counts. DiloGroup’s patent on energy-saving intense needling reduces kWh per kilogram by one-third versus water-jet bonding, offering converters a profitability booster once the design scales.

A deeper technology mix reduces supply risk and cushions raw-material volatility. Spun-laid output relocates closer to resin sources in the Gulf Cooperation Council, while melt-blown specialists co-locate near medical device hubs in North America and East Asia. These moves shorten lead times and prune freight emissions. Consequently, spun-laid remains pivotal in the non-woven packaging market as the preferred choice for cost-sensitive bulk formats, yet melt-blown gains relevance in value-added protective

By End-User Packaging Application: Food and Beverage Hold the Crown

Food and beverage occupied 37.10% of 2025 revenue. Non-woven sacks for grains, tea envelopes, and ready-to-eat pouches replace heavier multi-wall papers, cutting transport weight by up to 30%. Medical and healthcare, though smaller, is projected to expand at 9.11% CAGR on the back of stricter sterility norms and aging populations that inflate surgical kit volumes. Industrial bulk packaging keeps steady demand for flexible intermediate bulk containers lined with spunbond PP that withstand forklifts. Agriculture adoption rises as seed breeders choose breathable non-woven vacuum-formed trays that improve germination by channeling water yet blocking soil-borne pathogens.

Consumer goods benefit from e-commerce; brand owners switch to non-woven padded mailers that pass drop-tests without extra fillers and ship flat to fulfillment centers. While automotive and construction remain niche, smart labeling and RFID-embedded webs anticipate growth once traceability mandates mature. Taken together, the diversified demand base insulates the non-woven packaging market from single-sector downturns.

Geography Analysis

Asia-Pacific led the non-woven packaging market in 2025 with 31.75% share due to integrated resin-to-fabric hubs in China, India, and Malaysia. China’s packaging converters enjoyed low-cost energy and massive e-commerce parcel flow that justified new spun-laid lines of 10,000 tons per year. India’s flexible packaging expansion, valued at USD 49 billion in 2023, created downstream pull for specialty webs as local food giants replace PVC film with recyclable PP non-wovens. Japan and South Korea leveraged high-precision melt-blown expertise for medical consumables bound for the United States and Europe.

Africa recorded the quickest growth at 7.99% CAGR owing to government incentives for domestic manufacturing and continental free-trade corridors that ease movement of finished bags. New lines in Nigeria and Egypt feed regional grain exporters, reducing reliance on imported jute sacks. South Africa’s retailers trial compostable PLA carry-bags that comply with extended producer responsibility fees. These moves push capacity utilization past 70% on recently installed spunbond machines by 2026, giving Africa a distinctive growth narrative within the non-woven packaging market.

Competitive Landscape

Non-woven packaging shows moderate concentration as the top five players hold roughly 40% revenue. Amcor, DuPont, Kimberly-Clark, Freudenberg, and Berry-Glatfelter leverage global resin contracts, proprietary bonding know-how, and regulatory lobbying muscle. Amcor’s USD 8.4 billion move to buy Berry Global adds high-speed spun-laid assets in Asia and deepens RandD funds earmarked for compostable laminates. Berry-Glatfelter’s merger delivers USD 50 million cost synergies in year three by rationalizing European slitting and coating plants.

Kimberly-Clark earmarked USD 2 billion through 2030 to automate Ohio and South Carolina mills, cutting make-ready times by 40% and expanding melt-blown fabric for PPE. DuPont invests in ionomer-based tie layers that boost heat-seal integrity of mono-material pouches without compromising recyclability. Mid-tier challengers such as Avgol and Ahlstrom focus on region-specific innovations like low-gsm elastic side gussets for diaper wraps.

Non-woven Packaging Industry Leaders

Novipax Buyer, LLC

EAM Corporation (Domtar Corporation)

Glatfelter Corporation

Felix Nonwovens

Dupont de Nemours, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Amcor and Berry Global shareholders approved their USD 8.4 billion combination to form a USD 24 billion revenue packaging group targeting USD 650 million annual synergies.

- February 2025: Novolex and Pactiv Evergreen announced a merger to strengthen food-service packaging with a focus on recyclable and compostable non-woven wraps.

- January 2025: Kimberly-Clark confirmed a USD 2 billion five-year domestic expansion covering a new Warren, Ohio non-woven facility and an extended Beech Island, South Carolina site, adding 900 skilled automation positions.

- January 2025: Veritiv acquired Orora Packaging Solutions for USD 1.19 billion, adding 70 sites and bolstering non-woven converting capacity.

Global Non-woven Packaging Market Report Scope

Non-woven refers to a fabric-like material comprising staple fibers that have been mechanically, chemically, thermally, or solvent-bonded together. The study captures the demand for non-woven materials based on the various market dynamics, technology trends, and demand-supply conditions worldwide. The study covers the non-woven packaging market tracked in terms of volume in million tonnes. This report analyzes the factors that impact geopolitical developments in the market, which were studied based on the prevalent base scenarios, key themes, and end-use application-related demand cycles. The estimates exclude the weight of the content that is or is to be packed inside the non-woven packaging solutions.

The scope is limited to non-woven material in packaging. Non-woven shopping bags are not considered part of the scope. The global non-woven packaging market is segmented by technology (dry-laid, spun-laid, and other technologies), end-use packaging applications (food packaging, industrial, medical, and other end-uses), and geography. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period.

The non-woven packaging market is segmented by technology (dry-laid, spun-laid, other technologies), by end-user packaging applications (food packaging, industrial, medical, other end user packaging applications), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The report offers market forecasts and size in volume (tonnes) for all the above segments.

| Dry-Laid |

| Spun-Laid |

| Melt-blown |

| Hydro-Entangled |

| Other Technologies |

| Food and Beverage |

| Industrial |

| Medical and Healthcare |

| Consumer Goods |

| Agriculture |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Indonesia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | UAE |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Technology | Dry-Laid | ||

| Spun-Laid | |||

| Melt-blown | |||

| Hydro-Entangled | |||

| Other Technologies | |||

| By End-user Packaging Application | Food and Beverage | ||

| Industrial | |||

| Medical and Healthcare | |||

| Consumer Goods | |||

| Agriculture | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Indonesia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | UAE | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the non-woven packaging market?

The non-woven packaging market stands at 1.86 billion tons in 2026 and is projected to reach 2.65 billion tons by 2031.

Which technology segment leads the non-woven packaging market?

Spun-laid processes account for 43.60% of 2025 throughput, benefiting from integrated fiber spinning and web bonding that keeps costs low.

Which end-user sector is growing fastest?

Medical and healthcare packaging is forecast to grow at a 9.11% CAGR between 2026 and 2031 due to rising sterilization and PPE demand.

Which region shows the strongest growth outlook?

Africa is set to record an 7.99% CAGR through 2031 owing to new manufacturing lines and expanding intra-continental trade.

Page last updated on: