Compressible Printing Blankets Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

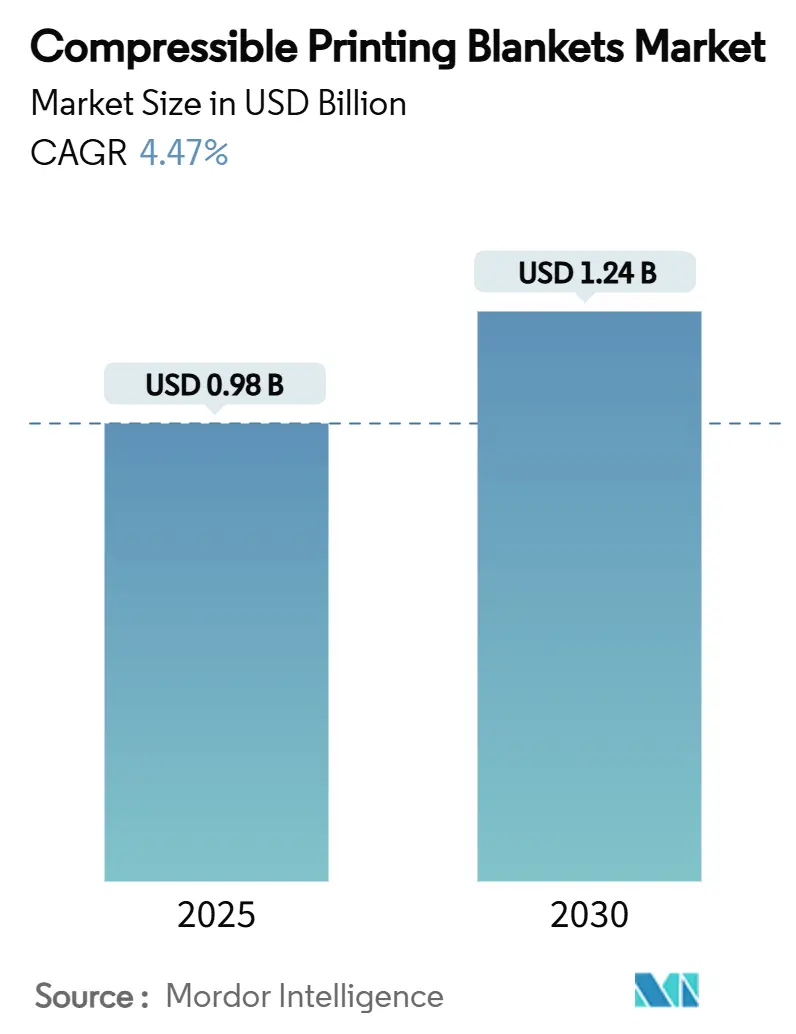

| Market Size (2025) | USD 0.98 Billion |

| Market Size (2030) | USD 1.24 Billion |

| Growth Rate (2025 - 2030) | 4.47% CAGR |

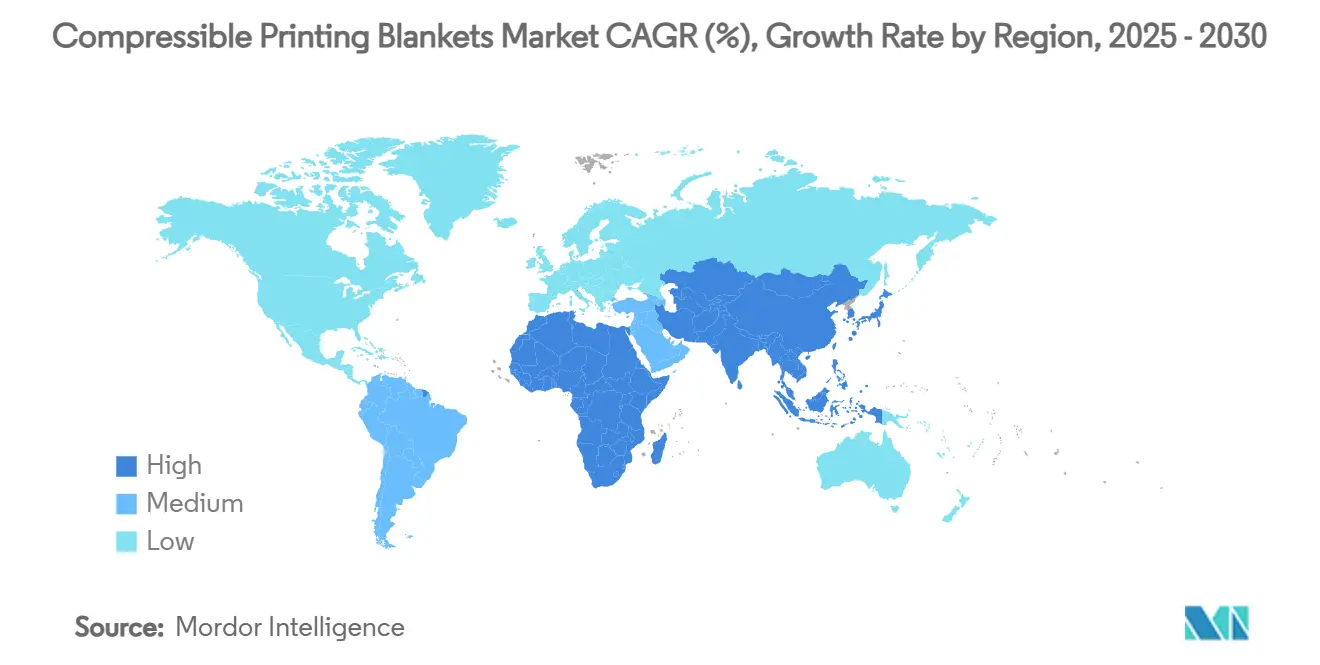

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Compressible Printing Blankets Market Analysis by Mordor Intelligence

The Compressible Printing Blankets Market size is estimated at USD 0.98 billion in 2025, and is expected to reach USD 1.24 billion by 2030, at a CAGR of 4.47% during the forecast period (2025-2030). Shifts toward paper-based packaging, the rapid installation of hybrid UV and LED-UV offset presses, and regulatory mandates that shorten blanket replacement cycles are the primary growth catalysts for the compressible printing blankets market. Packaging printers account for the largest share of blanket demand because folding cartons and labels require consistent ink transfer, dimensional stability, and high color fidelity. Manufacturers have responded with UV-resistant compounds that extend service life under aggressive curing conditions, even as rubber feedstock inflation exerts cost pressure. At the same time, the compressible printing blankets market continues to benefit from re-shoring initiatives in Europe and North America, where buyers value local technical support and compliance with evolving volatile organic compound (VOC) limits.

Key Report Takeaways

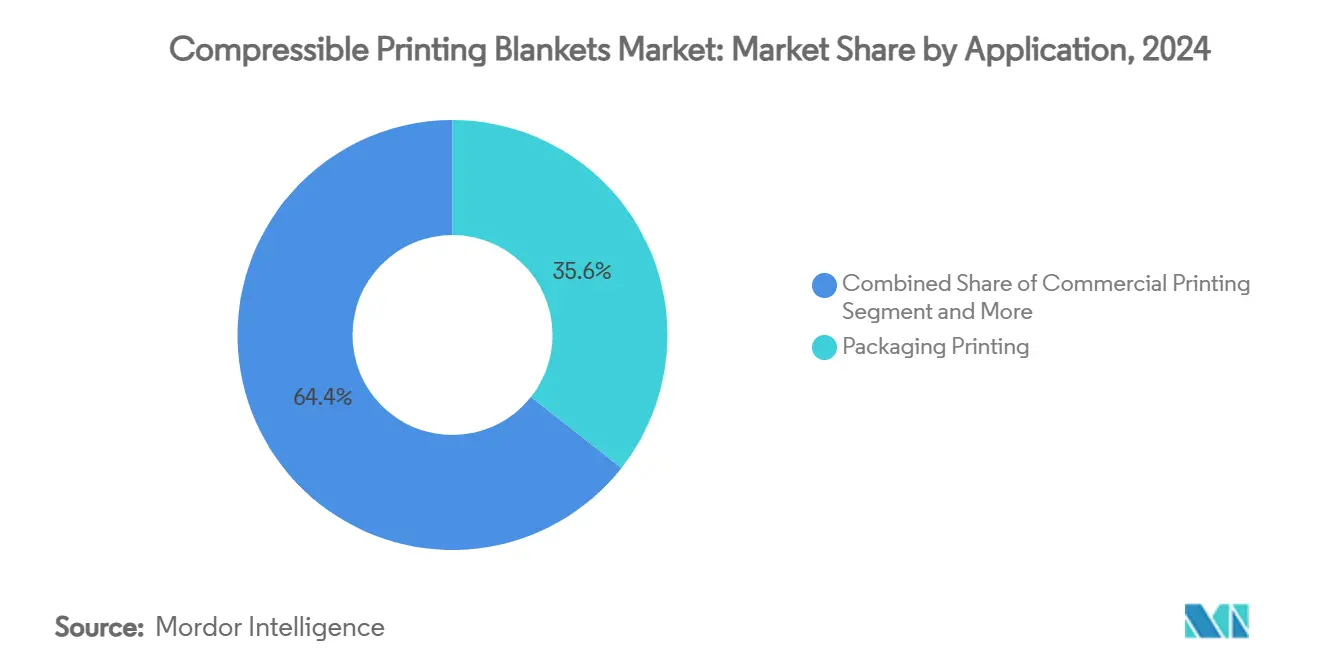

- By application, packaging printing led with 35.62% of the compressible printing blankets market share in 2024.

- By printing press type, digital-hybrid offset presses are projected to grow at 5.76% CAGR between 2025-2030.

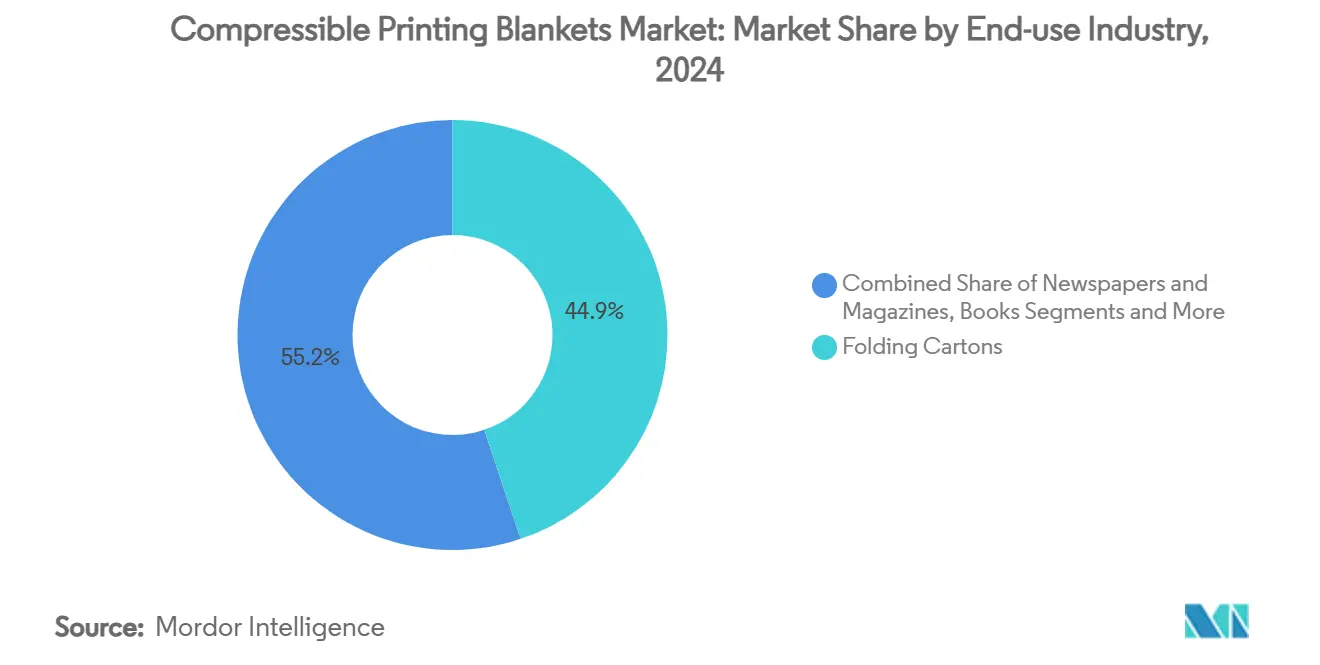

- By end-use industry, folding cartons commanded 44.85% of the compressible printing blankets market share in 2024.

- By material composition, nitrile rubber (NBR) retained 32.14% of the compressible printing blankets market share in 2024.

- By geography, Asia-Pacific is projected to grow at 6.17% CAGR between 2025-2030.

Global Compressible Printing Blankets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for premium packaging print quality | +1.2% | Global, with early gains in Asia-Pacific and North America | Medium term (2-4 years) |

| Growth of hybrid UV and LED-UV offset presses | +0.8% | Europe and North America core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Rapid expansion of on-demand book manufacturing | +0.6% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Tightening VOC rules driving blanket change-outs | +1.1% | Global, strictest in North America and Europe | Short term (≤ 2 years) |

| Automation of blanket cleaning systems | +0.4% | North America and Europe, gradual in Asia-Pacific | Medium term (2-4 years) |

| Re-shoring of print supply chains | +0.3% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Premium Packaging Print Quality

E-commerce growth and plastic-reduction mandates elevate brand owners’ expectations for vivid graphics, clean solids, and precise registration. Heidelberg’s packaging solutions platform has already achieved more than 60% cumulative growth since 2015 and the company intends to add EUR 300 million (USD 336 million) in incremental packaging sales by fiscal 2029[1]Heidelberger Druckmaschinen AG, “Heidelberg Strategy 2029,” heidelberg.com. Premium folding cartons and labels therefore stimulate recurring blanket demand because print defects such as mottle or ghosting are less tolerated. The move toward recyclable fiber-based substrates magnifies this requirement, given their higher surface variation. Consequently, the compressible printing blankets market witnesses accelerated adoption of blankets engineered with harder surface layers and improved micro-cell structures for optimal ink transfer. Printers also favor blankets incorporating closed-cell compressible layers that recover quickly after impression, preserving dot integrity through long runs.

Growth of Hybrid UV and LED-UV Offset Presses

UV and LED-UV curing technologies enhance throughput and enable printing on filmic substrates but expose blankets to chemically aggressive inks and higher surface temperatures. This dynamic drives the fastest rise in UV-resistant compounds inside the compressible printing blankets market. Labels and Labeling reports a 6.11% CAGR for such materials as converters invest in presses that accommodate both conventional and energy-curable inks[2]Labels and Labeling, “Energy-curable Materials Gain Ground,” labelsandlabeling.com. Blanket manufacturers respond by blending NBR with EPDM and specialty polymers that withstand swelling, while adding ozone-resistant top coats to extend service life. Hybrid configurations further boost demand for blankets compatible with inline digital imprinting units that impose additional thermal cycles.

Rapid Expansion of On-Demand Book Manufacturing

Print-on-demand workflows eliminate large inventories yet introduce frequent job changeovers and shorter runs—conditions that heighten blanket fatigue. Heidelberger Druckmaschinen values the digital printing market for book production at EUR 5 billion in 2025, with expectations of EUR 7.5 billion by 2029[3]Heidelberger Druckmaschinen AG, “Heidelberg Strategy 2029,” heidelberg.com. Publishers still require offset quality for text and halftone images, prompting investment in sheet-fed presses paired with continuous-feed inkjet lines. Compressible blankets with refined micro-ground surfaces and resilient compressible layers help printers cut makeready time and reduce waste. Demand also rises for blanket-to-blanket and blanket-to-steel systems that allow duplex printing in a single pass, saving floor space and operator intervention.

Tightening VOC Rules Driving Blanket Change-outs

The Environmental Protection Agency banned methylene chloride in July 2024, forcing printers to switch from solvent-based to water-based blanket washes. Water-based formulations leave more pigment residue, so blankets glaze faster and require earlier replacement, thereby swelling the overall volume of the compressible printing blankets market. In December 2024 the EPA finalized a 10-year phase-out of perchloroethylene, intensifying compliance costs and reinforcing the same replacement trend. California's Proposition 65 update, effective 2028, demands transparent chemical disclosures on pressroom consumables, encouraging printers to buy low-VOC blankets despite higher upfront cost[4]PRINTING United Alliance, "California Prop 65 Amendments for Printing Supplies," printing.org. Producers answer with rapid-decurl technology and surface coatings that resist swelling under frequent water-based cleaning cycles.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking newspaper and magazine run-lengths | -0.9% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Cost-competitive digital print for <5k runs | -0.7% | Global | Medium term (2-4 years) |

| Volatility in synthetic rubber feedstock prices | -0.5% | Global | Short term (≤ 2 years) |

| Lack of skilled offset press operators | -0.4% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shrinking Newspaper and Magazine Run-lengths

Newspaper circulation and magazine pagination have contracted sharply since 2020, leading to permanent press closures. The U.S. Bureau of Labor Statistics counted 353,900 employees in printing and allied services in 2024, down from earlier peaks, underscoring structural change. Fewer coldset web offset hours translate into lower blanket pull-through. Although some publishers pivot to branded supplements and sponsored content, the absolute loss in newsprint tonnage outweighs these gains. Blanket makers attempt to offset the volume drop by marketing higher-margin products to packaging and label converters.

Cost-Competitive Digital Print for Short Runs

Inkjet and electrophotographic systems now match offset economics at runs of 5,000 impressions in commercial work. These platforms eradicate plate imaging and make-ready, eroding offset’s advantage in job turnaround, thereby limiting potential expansion of the compressible printing blankets market. Nonetheless, digital presses struggle with heavy board and metallic substrates common in premium folding cartons, so offset retains dominance in packaging. Blanket suppliers therefore focus on niches where offset remains unrivaled, bundling consumables with pressroom service contracts to defend share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Packaging Printing Drives Market Evolution

Packaging printing accounted for 35.62% of total revenue in 2024, reinforcing its position as the anchor of the compressible printing blankets market. E-commerce demand and corporate sustainability targets amplify run volumes for folding cartons, multi-layer labels, and premium flexible packaging. Packaging printing is projected to register a 5.84% CAGR to 2030, outpacing every other application segment. Brand marketers require scuff resistance, color consistency, and tight registration over large repeat lengths, attributes that elevate blanket performance requirements. Conversely, commercial printing remains sizeable but endures margin squeeze because variable data digital presses remove significant portions of smaller-lot volumes.

Labels and tags exhibit the fastest unit growth at 6.03% CAGR as food, beverage, and personal care producers seek compliance with serialization and traceability mandates. Specialty tags for retail hold-up labels and cold-chain identification also demand low-surface-energy blankets for accurate ink lay-down on plastic films. Publication printing’s share continues to shrink, creating surplus heatset capacity that some operators redeploy to retail inserts and catalogs. Security and specialty printing, including banknotes and tax stamps, stay resilient due to counterfeit deterrence needs and thereby keep a niche yet stable role within the compressible printing blankets market.

By Printing Press Type: Web Offset Dominance with Digital-Hybrid Growth

Web offset (heatset) lines captured 42.31% of industry turnover in 2024, capitalizing on their ability to deliver long-form jobs such as catalogs and high-graphic retail supplements at competitive costs. Integrated dryers solidify inks, permitting immediate finishing and reducing set-off. Nevertheless, the most rapid expansion stems from digital-hybrid offset platforms, advancing at a 5.76% CAGR between 2025 and 2030. These presses allow variable imprinting alongside traditional offset units, a feature that heightens blanket requirements for heat fluctuation tolerance and chemical resistance.

Sheet-fed presses retain relevance for high-end commercial pieces and micro-flute carton work where format flexibility matters. Web offset coldset volumes are contracting with newspaper declines, but some presses pivot to book manufacturing, aided by inline gluing and folding units. Blanket suppliers design multi-layer products tuned to each configuration, using latency-free compressible foams to dampen vibration in high-speed heatset units and harder carrier layers for digital-hybrid presses that face repeated imaging cylinder temperature cycling. These developments create premium revenue opportunities within the compressible printing blankets market.

By End-use Industry: Folding Cartons Lead with Labels Accelerating

Folding cartons held 44.85% of blanket consumption in 2024, anchored in fast-moving consumer goods, pharmaceuticals, and cosmetics. Brand owners reward converters capable of running extended gamut inks and post-press embellishments, tasks that necessitate dimensionally stable blankets. Carton makers also migrate to recycled fiberboard, intensifying surface porosity challenges and pushing adoption of blankets with micro-grind profiles that improve density without over-inking. Labels and tags form the momentum engine for the compressible printing blankets market thanks to CAGR of 6.03% through 2030, fueled by beverage-grade pressure-sensitive labels and serialization mandates for medical devices.

Other end-uses such as book covers, stationery, and playing cards depend on offset for tactile quality and color parity but contribute modest growth. Corrugated pre-print remains niche because digital single-pass machines gain share in on-demand box printing. Nonetheless, offset lamination liners for high-graphic corrugated continue to require wide-width blankets, which command premium pricing due to limited manufacturing capacity. Blanket makers therefore balance volume in mainstream folding cartons with value capture in these specialized niches, ensuring a diversified yet focused product roadmap.

By Material Composition: Nitrile Rubber (NBR) Dominance with UV-Resistant Innovation

Nitrile rubber (NBR) comprised 32.14% of 2024 shipments, favored for its resistance to conventional mineral-oil inks and affordability. However, rapid uptake of energy-curable systems boosts demand for complex polymer blends fortified with acrylonitrile content and cross-linked EPDM. UV-resistant compounds represent the fastest climber at 6.11% CAGR, reflecting printers’ willingness to pay for extended blanket uptime under aggressive photoinitiators. The compressible printing blankets market size for UV-grade materials is forecast to approach USD 315 million by 2030 up from USD 235 million in 2025 delivering a high-margin proposition for suppliers.

Feedstock volatility cannot be ignored: natural rubber prices escalated 46.4% year on year in 2024 while the Producer Price Index for synthetic rubber touched 257.346 in May 2025. This inflation incentivizes blanket producers to optimize compound recipes, substituting high-cost elastomers with engineered fillers without sacrificing resilience. Suppliers deploy nano-silica reinforcement to improve compression set and reduce solvent swell, extending blanket lifespan to counterbalance elevated unit costs. Sustainability pressures also spur experimentation with bio-based polyols, though commercial adoption remains nascent.

Geography Analysis

By Geography: Asia-Pacific Leadership with Sustained Growth

Asia-Pacific generated 39.78% of global blanket revenue in 2024, a lead attributed to its dominant role in consumer goods manufacturing and export packaging. Regional converters invest in large-format heatset and sheet-fed presses to serve multinational brand owners that demand consistent global quality standards. China retains the largest national share, yet Southeast Asian countries are closing the gap as supply chains diversify. Regional CAGR of 6.17% through 2030 places Asia-Pacific ahead of every other geography, ensuring that the compressible printing blankets market continues to pivot toward eastern demand centers.

North America holds a mature but technologically advanced install base. Press modernization favors automation, closed-loop color management, and LED-UV retrofits, supporting premium blanket sales even though overall unit volumes grow modestly. Europe mirrors this pattern but is additionally shaped by stringent VOC and chemical safety frameworks that drive interest in low-swelling blanket compounds. Western European converters fighting energy cost inflation increasingly replace compressed-air-powered blanket washers with electromechanical systems, subtly shifting blanket surface treatment needs.

Latin America and the Middle East/Africa represent emerging territories. Larger Brazilian and Mexican converters pursue folding carton upgrades for domestic fast-moving consumer goods, while Middle Eastern investors build new plants to supply food and personal care sectors. Political and currency volatility restricts purchasing power, so suppliers often enter with value-priced NBR products before migrating customers to UV-grade solutions. This staged approach gradually deepens penetration of the compressible printing blankets market across new geographies.

Competitive Landscape

Global supply is moderately concentrated among technology-driven incumbents that possess in-house polymer science, precision calendaring, and worldwide distribution. Trelleborg Printing Solutions, Continental AG’s ContiTech, and Flint Group leverage branded product portfolios and embedded pressroom support teams to lock in multi-year contracts with leading converters. Continental’s spin-off of ContiTech into an independent legal entity in April 2025 aims to simplify decision-making and accelerate industrial innovation, though the division’s sales fell 9.9% to EUR 1.5 billion in Q3 2024 amid sluggish capital expenditure in Europe and North America.

Innovation remains the chief competitive weapon. Trelleborg AB commercialized its Vulcan Eco-UV blanket range featuring bio-based plasticizers and claims 20% longer life in LED-UV presses under identical conditions. Flint Group’s dayGraphica line focuses on easy cleaning top coats compatible with water-wash systems mandated by recent solvent bans. XSYS acquired MacDermid Graphics Solutions in September 2024, enhancing photopolymer plate chemistry know-how that feeds into blanket surface coatings for higher energy-curable ink compatibility. Asian producers such as Kinyo and Yuncheng Plate Making exploit lower labor and raw-material costs to capture price-sensitive segments but still lag Western competitors in brand perception for high-definition print.

Strategically, suppliers complement product launches with value-added services. Remote blanket performance monitoring, predictive replacement alerts, and operator training packages differentiate offerings in a market where unit price gaps narrow. As environmental compliance tightens, benchmarking of blanket waste and cradle-to-gate carbon footprints is emerging as a new battleground. These dynamics collectively signal that the compressible printing blankets market will reward companies equipped to couple material science leadership with robust technical services infrastructure.

Compressible Printing Blankets Industry Leaders

-

Trelleborg AB

-

Kinyo Rubber Industrial Co.

-

Fujikura Rubber Ltd.

-

Flint Group - Day International (dayGraphica)

-

Continental AG (Phoenix Xtra)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Environmental Protection Agency (EPA) finalized perchloroethylene regulation under TSCA, initiating a 10-year phase-out for most commercial uses, including printing blanket cleaning.

- July 2024: Environmental Protection Agency (EPA) methylene chloride ban took effect, eliminating a widely used solvent for blanket maintenance and increasing reliance on water-based systems.

- June 2024: AstroNova showcased AQUAFLEX packaging presses and TrojanLabel T2-PRO digital label systems at Drupa 2024, expanding equipment that utilizes compressible blankets.

- May 2024: Baldwin Technology launched Unity LED, a curing module promising 60% energy savings versus mercury UV units.

- March 2024: Algenesis Corporation and UC San Diego developed a biodegradable thermoplastic polyurethane aimed at eco-friendly pressroom consumables.

Global Compressible Printing Blankets Market Report Scope

| Commercial Printing |

| Packaging Printing |

| Publication Printing |

| Security and Specialty Printing |

| Sheet-fed Offset |

| Web Offset (Heatset) |

| Web Offset (Coldset) |

| Digital-Hybrid Offset |

| Newspapers and Magazines |

| Books |

| Folding Cartons |

| Labels and Tags |

| Corrugated Packaging |

| Other End-use Industries |

| Nitrile Rubber (NBR) |

| NBR/PVC Blends |

| EPDM and Other Synthetics |

| UV-Resistant Compounds |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Application | Commercial Printing | ||

| Packaging Printing | |||

| Publication Printing | |||

| Security and Specialty Printing | |||

| By Printing Press Type | Sheet-fed Offset | ||

| Web Offset (Heatset) | |||

| Web Offset (Coldset) | |||

| Digital-Hybrid Offset | |||

| By End-use Industry | Newspapers and Magazines | ||

| Books | |||

| Folding Cartons | |||

| Labels and Tags | |||

| Corrugated Packaging | |||

| Other End-use Industries | |||

| By Material Composition | Nitrile Rubber (NBR) | ||

| NBR/PVC Blends | |||

| EPDM and Other Synthetics | |||

| UV-Resistant Compounds | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the compressible printing blankets market?

The compressible printing blankets market is valued at USD 0.98 billion in 2025 and is on track to reach USD 1.24 billion by 2030.

Which application segment contributes the most revenue?

Packaging printing leads, representing 35.62% of global demand in 2024, and is expected to post a 5.84% CAGR through 2030.

Why are UV-resistant blanket compounds growing so quickly?

Hybrid UV and LED-UV presses expose blankets to aggressive chemistries and higher temperatures, prompting printers to adopt UV-resistant compounds that deliver longer life and lower downtime.

How do regulatory changes in the United States affect blanket replacement cycles?

EPA bans on methylene chloride and the phase-out of perchloroethylene reduce solvent cleaning efficiency, causing blankets to glaze sooner and necessitating earlier replacement.

Which region is expanding the fastest?

Asia-Pacific holds 39.78% of global revenue and exhibits the quickest 6.17% CAGR owing to expanding manufacturing and packaging demand.

Page last updated on: