Printing Blanket Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.04 Billion |

| Market Size (2031) | USD 1.29 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Printing Blanket Market Analysis by Mordor Intelligence

The printing blanket market size is projected to expand from USD 0.99 billion in 2025 and USD 1.04 billion in 2026 to USD 1.28 billion by 2031, registering a CAGR of 4.29% between 2026 to 2031. Demand is pivoting from newspaper and magazine presses toward packaging converters that need blankets tolerant of LED-UV chemistry, short changeovers, and micron-level register. Manufacturers are securing multi-year natural-rubber contracts and blending synthetic elastomers to hedge the fifth straight year of global rubber deficits. Asia-Pacific leads in flexible packaging and serialized pharmaceutical labels, while North America and Europe invest in UV-compatible and sensor-embedded products that cut downtime and meet stricter food-contact rules. Competitive focus has shifted to compounds that reach one-million-impression life, resist waterless-offset solvents, and feed real-time data into Industry 4.0 workflows.

Key Report Takeaways

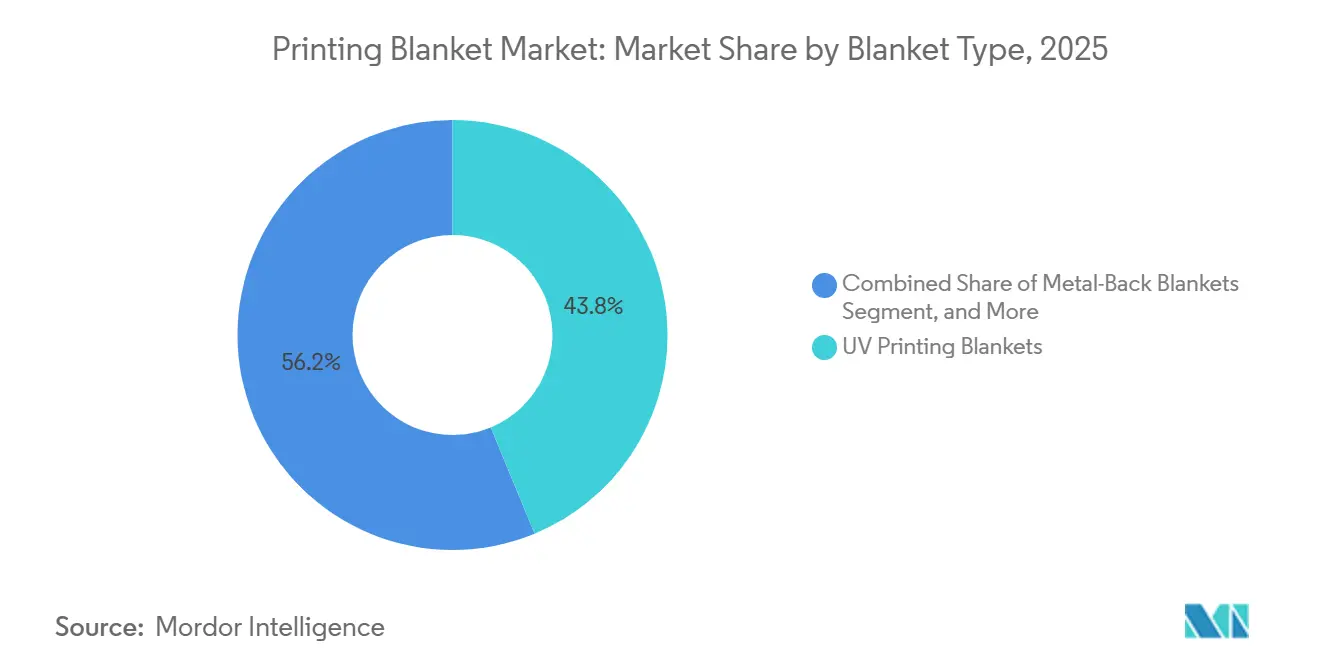

- By blanket type, UV printing blankets led with 43.76% revenue share in 2025, while metal-back blankets recorded the fastest 5.33% CAGR through 2031.

- By substrate, paper and board printing accounted for a 47.23% share of the printing blanket market size in 2025, whereas plastic and film printing advanced at a 5.27% CAGR.

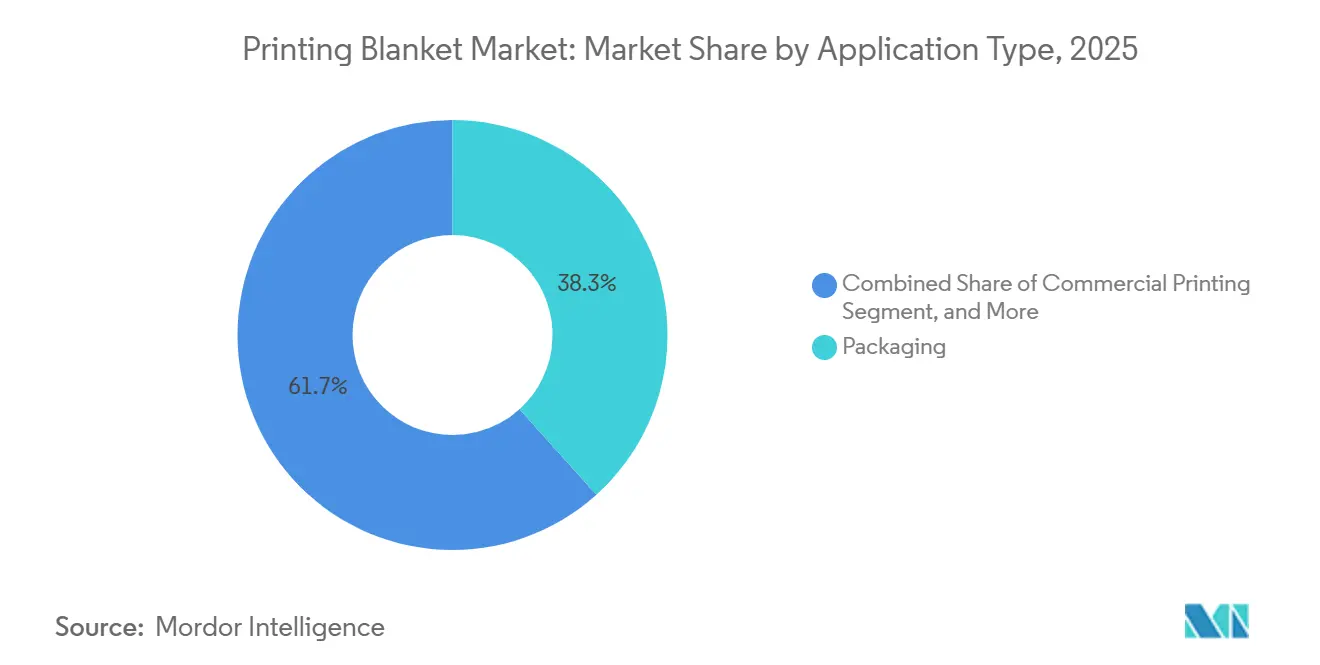

- By application, packaging dominated with 38.32% of the 2025 volume, and the flexible-packaging sub-segment expanded at a 5.43% CAGR.

- By printing process, sheetfed offset held 42.41% of the 2025 demand, and digital offset thermal blankets grew the quickest at a 5.41% CAGR.

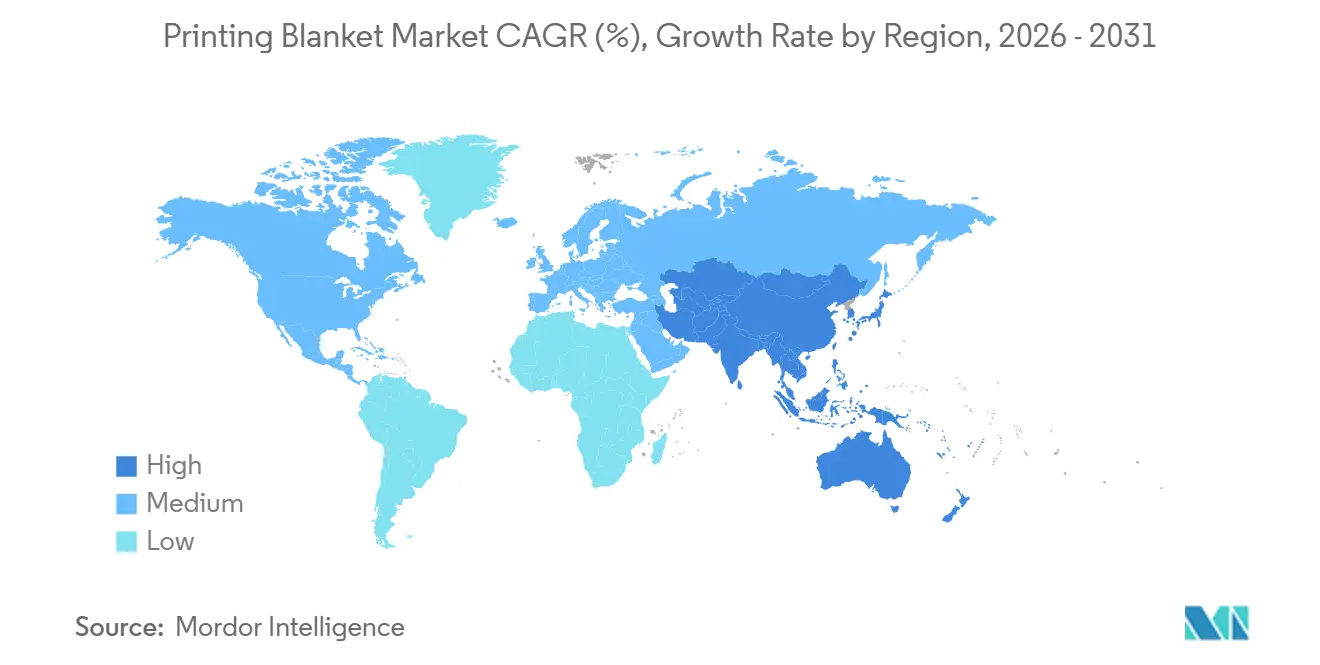

- By geography, Asia-Pacific accounted for 44.92% of revenue in 2025 and is set to grow at a 5.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Printing Blanket Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand For UV-Compatible Blankets In LED-UV And H-UV Presses | +1.2% | North America, Europe, Asia-Pacific | Medium Term (2–4 Years) |

| Boom In Short-Run, Customized Packaging Driving Frequent Blanket Changeovers | +0.9% | North America, Western Europe, Urban China And India | Short Term (≤ 2 Years) |

| Rapid Growth Of Flexible-Packaging Applications In Food And Beverage | +0.8% | Asia-Pacific, Middle East And Africa, South America | Long Term (≥ 4 Years) |

| Rising Quality Requirements For High-Definition Graphics | +0.6% | Europe, North America, Asia-Pacific | Medium Term (2–4 Years) |

| Adoption Of Smart Sensor-Embedded Blankets Enabling Predictive Maintenance | +0.4% | North America, Europe, Japan, South Korea | Long Term (≥ 4 Years) |

| Expansion Of Waterless Offset In Pharma And Security Printing Requiring Specialized Blankets | +0.3% | Europe, Japan, North America | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Surging Demand for UV-Compatible Blankets in LED-UV and H-UV Presses

LED-UV and H-UV systems cure inks instantly, but the chemistry imposes surface-energy thresholds under 32 dyn/cm and higher nip pressures that conventional rubber cannot tolerate. Blanket suppliers released low-energy-release compounds in 2024 that resist oligomer build-up, letting food-contact packages run powder-free and remain compliant with EU Regulation 10/2011.[1]European Commission, “Regulation (EU) No 10/2011 on Plastic Materials,” eur-lex.europa.eu Brand owners now specify UV presses for 60% of new folding-carton lines, locking in recurring demand for UV-rated blankets.

Boom in Short-Run, Customized Packaging Driving Frequent Blanket Changeovers

A 2024 survey found 40% of brand owners increasing SKU counts and 60% cutting batch sizes, forcing converters to swap jobs up to five times per shift. Each swap stresses blankets through solvent washes and tension cycling, so printers upgrade to compressible or hybrid designs that survive beyond one million impressions, offsetting higher unit prices with less downtime. Labor rates above USD 25 per hour in North America and Western Europe magnify the cost of every makeready minute, accelerating adoption of longer-life blankets.

Rapid Growth of Flexible-Packaging Applications in Food and Beverage

Flexible pouches reduce shipping weight and shelf footprint, prompting offset presses to move to plastic films, where low-compression-set blankets prevent ghosting. Trials with waterless plates achieved 80% energy savings compared to gravure.[2]Toray Industries, “Energy Savings with Waterless Offset Plates,” toray.com Asia-Pacific leads this shift as single-serve snacks and beverages proliferate in India and Southeast Asia, while Middle East and Africa retailers modernize shelf formats, sustaining blanket demand well past 2031.

Rising Quality Requirements for High-Definition Graphics

Regulations and technological advances are reshaping the role of printing blankets into precision-critical components rather than simple consumables. Standards like ISO 22382:2018 on tax stamps require sub-10-micron-resolutio graphics to thwart counterfeiting, forcing blanket makers to engineer surfaces with extreme dimensional stability. In pharmaceuticals, serialization codes with 0.25 mm modules require blankets to maintain Shore A hardness tolerances within ±2 points, since even slight deviations can compromise machine readability and regulatory compliance. Meanwhile, press builders have integrated AI-driven color loops (2024) that improve register accuracy by 20%, yet the success of these systems still depends on blankets that can rebound instantly after every impression to prevent ghosting and misalignment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Shift To Digital Inkjet Printing (Blanket-Free) | -0.8% | North America, Western Europe | Short Term (≤ 2 Years) |

| Decline In Newspaper And Magazine Print Volumes | -0.6% | North America, Europe, Asia-Pacific | Long Term (≥ 4 Years) |

| Proliferation Of Reusable Blanket Sleeve Systems Reducing Replacement Demand | -0.4% | Europe, Japan, North America | Medium Term (2–4 Years) |

| Supply Chain Risk From Regionalized Rubber Compounding Capacity | -0.3% | Global | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Accelerating Shift to Digital Inkjet Printing (Blanket-Free)

High-speed inkjet presses for commercial print and labels grew double digits annually to 2025, removing blankets entirely and slashing makeready from 30 minutes to five. Label converters now cross over to digital runs below 1,000 linear feet, curbing blanket volumes that once fed coldset and heatset web lines. Offset still wins on long runs, but declining consumable prices keep moving the breakeven point upward.

Decline in Newspaper and Magazine Print Volumes

U.S. newspaper circulation dropped 50% between 2005 and 2020.[3]Pew Research Center, “Newspapers Fact Sheet,” pewresearch.org Magazine advertising has undergone a steep contraction, with spend falling 35% between 2019 and 2023, leaving press utilization at less than 40% capacity. This decline means blankets are lasting longer before replacement, as fewer impressions are run, and in some cases, publishers are retiring entire web lines, eliminating blanket demand altogether. While Asia-Pacific newspapers provide some cushion thanks to their higher baseline circulation, the overall structural headwind remains strong, driven by the global shift in media consumption and advertiser migration to digital platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Blanket Type: UV Chemistry Drives Specialization

UV printing blankets held 43.76% of 2025 revenue, anchored by presses that must release instant-cure inks cleanly. Metal-back designs, though smaller in volume, posted the fastest 5.33% CAGR because a thin steel or aluminum layer locks register on 12-hour pharmaceutical blister runs. Conventional blankets still dominate legacy newspaper presses, but their slice of the printing blanket market is shrinking as those presses close. Compressible variants command a premium because their microcell structure prevents hickeys on recycled paper, which is common in Europe and North America.

Hybrid blankets blend UV-compatible surfaces with metal backing, suiting plants that swap between polyethylene film and coated board each shift. Higher unit costs and the technical tightrope of balancing ink release with tack-slow adoption, yet mid-sized converters embrace them to cut inventory complexity. Flint Group’s 2024 launch aimed squarely at this mixed-substrate cohort, signaling more such introductions ahead.

By Substrate Type: Film Printing Outpaces Paper

Paper and board applications still accounted for 47.23% of the printing blanket market share in 2025, driven by folding cartons and corrugated boxes. Plastic and film, however, grew at a 5.27% CAGR on the back of snack pouches and beverage sachets. Offset on films needs low-compression-set blankets built from high butadiene synthetic rubber so that the image stays crisp when webs stretch, a spec especially popular among Indian sachet producers. Metal decorating blankets maintain high hardness above 80 Shore A for beverage cans, a stable but slow-growing niche, as some promotional runs move to direct-to-metal inkjet.

Textile runs for luxury scarves in Japan and Italy keep a foothold, though rotary screen and digital dominate wider fabric output. Exotic substrates like wood veneer and leather form a residual market, usually in specialty décor shops. Asia-Pacific’s urban growth and sachet culture ensure film printing will keep eroding paper’s lead beyond 2031.

By Application Type: Flexible Packaging Leads Growth

Packaging owned 38.32% of the 2025 volume. Within it, flexible formats posted a 5.43% CAGR thanks to lighter shipping loads and reduced shelf space. Eliminating USD 2,000-5,000 gravure cylinders makes offset blankets the economical option for mid-volume runs. Rigid cartons grow more slowly, constrained by saturation in developed economies and by competition from digital for small batches. Commercial printing accounts for around one-quarter of volume, yet contracts as catalogs and bills migrate online, though high-end coffee-table books preserve a premium tier.

Newspaper consumption has dwindled to a single-digit share of overall media, eroding one of the traditional pillars of blanket demand. At the same time, security printing continues to uphold strict tolerances for precision and durability, but its relatively small tonnage volumes mean it cannot offset the decline in mainstream publishing. The growth momentum instead lies in labels and tags, which are buoyed by the expansion of e-commerce logistics and the regulatory push for drug serialization. These applications increasingly rely on UV-compatible blankets engineered to withstand the intense heat generated during inline die-cutting, ensuring durability while maintaining print fidelity.

By Printing Process: Digital Offset Gains Momentum

Sheetfed offset retained a 42.41% share in 2025, prized for color fidelity on cartons and brochures. Digital offset thermal blankets, critical to HP Indigo and Kodak NexPress units, grew 5.41% CAGR as variable-data packaging spread. These blankets wear out in as few as 50,000 impressions, amplifying consumable revenue despite smaller press footprints. Web heatset serves long-run inserts yet declines in tandem with retail catalog cuts, while coldset for newspapers fades fastest.

Press manufacturers are increasingly layering AI-driven controls and inline inspection systems into their newest press models, raising the bar for blanket performance. To unlock the full potential of these register guarantees, blankets must deliver Shore A hardness precision and tight caliper tolerances, ensuring that every impression rebounds consistently and maintains dimensional accuracy under high-speed conditions. This heightened demand for precision makes ISO 12636 testing protocols, which validate blanket properties such as hardness, thickness, and resilience, an essential benchmark for quality assurance.

Geography Analysis

Asia-Pacific generated 44.92% of 2025 revenue, and its 5.21% CAGR keeps the region at the forefront of the printing blanket market. China’s online retail share hit 52% in 2025, fueling flexible packaging volumes across e-commerce SKUs. India’s Track and Trace rules for drug exports lifted serialized-label demand, while Japan leads in premium sheetfed jobs that rely on Kinyo and Kinyosha specialty compounds. South Korea’s VOC limits speed waterless offset uptake, further raising blanket needs tailored to that chemistry.

North America held a 25% share. Newspaper and magazine retreats outpaced global averages, but folding-carton and UV-sheetfed investments cushion the fall. U.S. plants are early adopters of sensor-embedded blankets that feed ERP dashboards, justified by high labor costs and tight FSMA food-safety audits. Canada mirrors trends on a smaller scale, clustered around Ontario and Quebec packaging hubs.

Europe produced one-fifth of global income, anchored by Germany, the United Kingdom, and Italy. Germany’s automated Mittelstand printers specify smart blankets and waterless plates to reduce volatile organic compound emissions, aligning with strict EU limits on isopropyl alcohol. The Single-Use Plastics Directive accelerates the pivot from rigid containers to lightweight film, opening space for UV-capable blankets built for PE and PET webs. South America, led by Brazil, holds a mid-single-digit stake, constrained by currency swings yet buoyed by modern retail making shelf-ready packaging mainstream. Middle East and Africa remain the smallest slice, but security-printing investments in Gulf states and packaging growth in South Africa provide high-margin niche orders.

Competitive Landscape

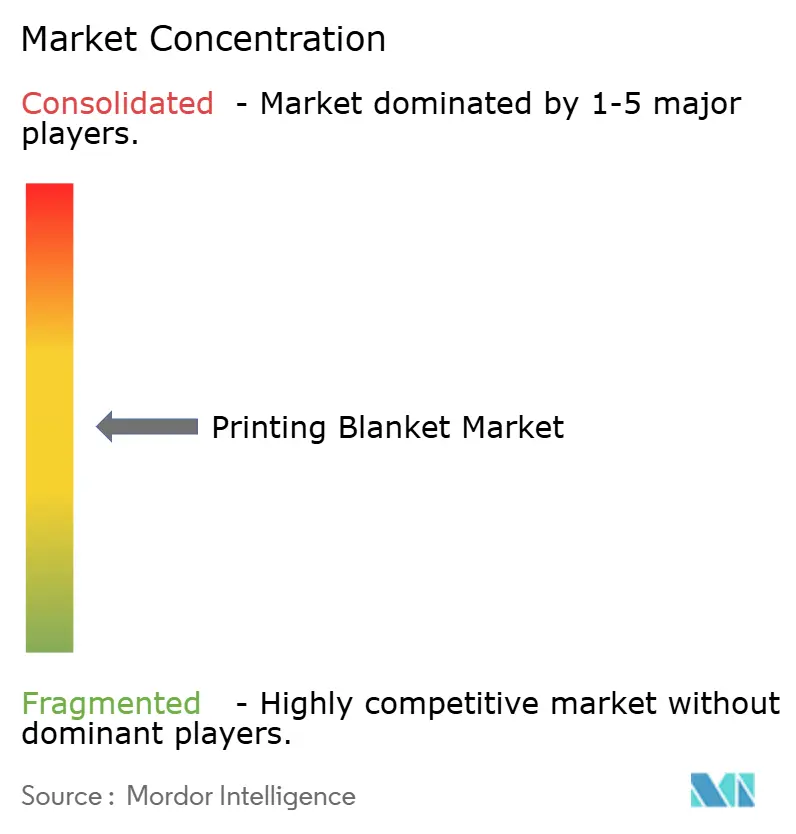

Continental, Flint Group, Kinyo, and Kinyosha together command near-half of global revenue, placing the printing blanket market in moderately concentrated territory. Continental’s 2023 takeover of Trelleborg’s division vaulted it to an estimated 18% share and deepened its European reach. Flint Group differentiates through dayGraphica compounds rated for 800,000 food-contact impressions, while Kinyo and Kinyosha export premium blends into Southeast Asia for luxury cosmetics labels.

Technology rivalry now centers on extending blanket life beyond one million impressions and embedding sensors that predict failure. Habasit’s seamless sleeves with linear encoders cut unplanned downtime by 15% but cost 30% more than standard products, a gap that narrows as volume scales. Vertical integration is rising as press builders partner with blanket suppliers to pre-spec formulations for new models, creating captive aftermarket channels that bypass distributors.

Price competition simmers at the lower end, where Chinese compounders undercut Western incumbents by up to 30% in commodity newspaper and catalog work. Quality standards such as ISO 12636 exist, yet enforcement varies, and small producers may skip full certification. The next front in differentiation is reusable sleeves that grinders can resurface twice before retirement, halving replacement cycles, though printers worry about learning curves and mounting-hardware inconsistencies.

Printing Blanket Industry Leaders

Continental AG

Trelleborg AB

Flint Group Germany GmbH

Habasit AG

Felix Böttcher GmbH and Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Continental AG committed EUR 15 million (USD 16.5 million) to expand UV-compatible blanket production at its Northeim facility in Germany.

- December 2025: Habasit launched sensor-embedded seamless sleeves that stream live tension and temperature data to press controls, delivering measured 15% downtime cuts in North American beta sites.

- November 2024: Flint Group Germany introduced an advanced compressible blanket series with improved dimensional stability for security and luxury packaging.

- November 2024: Toray scaled production of IMPRIMA FR waterless plates for flexible packaging, increasing demand for matching low-tack blankets.

- June 2024: Graphius Group invested EUR 12 million (USD 13.0 million) in a Heidelberg Speedmaster 106 equipped with AI color control, targeting pharma packaging that depends on UV-ready blankets.

Global Printing Blanket Market Report Scope

The Printing Blanket Market Report is Segmented by Blanket Type (UV Printing Blankets, Conventional Printing Blankets, Compressible Printing Blankets, Combination and Hybrid Blankets, Metal-Back Blankets), Substrate Type (Paper and Board Printing, Metal Printing, Textile/Fabric Printing, Plastic and Film Printing, Other Substrate Types), Application Type (Packaging [Flexible Packaging, Rigid Packaging], Commercial Printing, Newspaper Printing, Security Printing, Labels and Tags, Other Application Types), Printing Process (Sheetfed Offset, Web Heatset Offset, Coldset Offset, Digital Offset [Thermal Blanket], Flexographic Rubber-Sleeve, Gravure/Spot-Coating), and Geography (North America [United States, Canada], South America [Brazil, Argentina], Europe [Germany, United Kingdom, France, Italy, Spain, Russia, Rest of Europe], Asia-Pacific [China, Japan, India, South Korea, Rest of Asia-Pacific], Middle East [Saudi Arabia, United Arab Emirates, Rest of Middle East], Africa [South Africa, Rest of Africa]). The Market Forecasts are Provided in Terms of Value (USD).

| UV Printing Blankets |

| Conventional Printing Blankets |

| Compressible Printing Blankets |

| Combination and Hybrid Blankets |

| Metal-Back Blankets |

| Paper and Board Printing |

| Metal Printing |

| Textile/Fabric Printing |

| Plastic and Film Printing |

| Other Substrate Types |

| Packaging | Flexible Packaging |

| Rigid Packaging | |

| Commercial Printing | |

| Newspaper Printing | |

| Security Printing | |

| Labels and Tags | |

| Other Application Types |

| Sheetfed Offset |

| Web Heatset Offset |

| Coldset Offset |

| Digital Offset (Thermal Blanket) |

| Flexographic Rubber-Sleeve |

| Gravure / Spot-Coating |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Blanket Type | UV Printing Blankets | |

| Conventional Printing Blankets | ||

| Compressible Printing Blankets | ||

| Combination and Hybrid Blankets | ||

| Metal-Back Blankets | ||

| By Substrate Type | Paper and Board Printing | |

| Metal Printing | ||

| Textile/Fabric Printing | ||

| Plastic and Film Printing | ||

| Other Substrate Types | ||

| By Application Type | Packaging | Flexible Packaging |

| Rigid Packaging | ||

| Commercial Printing | ||

| Newspaper Printing | ||

| Security Printing | ||

| Labels and Tags | ||

| Other Application Types | ||

| By Printing Process | Sheetfed Offset | |

| Web Heatset Offset | ||

| Coldset Offset | ||

| Digital Offset (Thermal Blanket) | ||

| Flexographic Rubber-Sleeve | ||

| Gravure / Spot-Coating | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the printing blanket market by 2031?

It is forecast to reach USD 1.28 billion by 2031, expanding at a 4.29% CAGR from 2026.

Which blanket type is growing fastest?

Metal-back blankets post the highest 5.33% CAGR because their dimensional stability suits long-run pharmaceutical and security jobs.

Why are UV-compatible blankets gaining traction?

LED-UV and H-UV presses cure inks instantly, remove powder sprays in food-contact packs, and therefore need low-energy-release blankets that resist oligomer build-up.

Which region leads demand?

Asia-Pacific commands 44.92% revenue and grows the fastest at a 5.21% CAGR, propelled by flexible packaging in China and serialized drug labels in India.

How are smart sensor-embedded blankets changing maintenance?

They stream live tension and temperature data, enabling predictive replacement schedules that have cut unplanned downtime by 15% in early installations.

What is the main threat to blanket demand?

Rapid adoption of high-speed digital inkjet presses in commercial print and labels removes the need for blankets, curbing growth in those segments.

Page last updated on: