Digital Printing Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

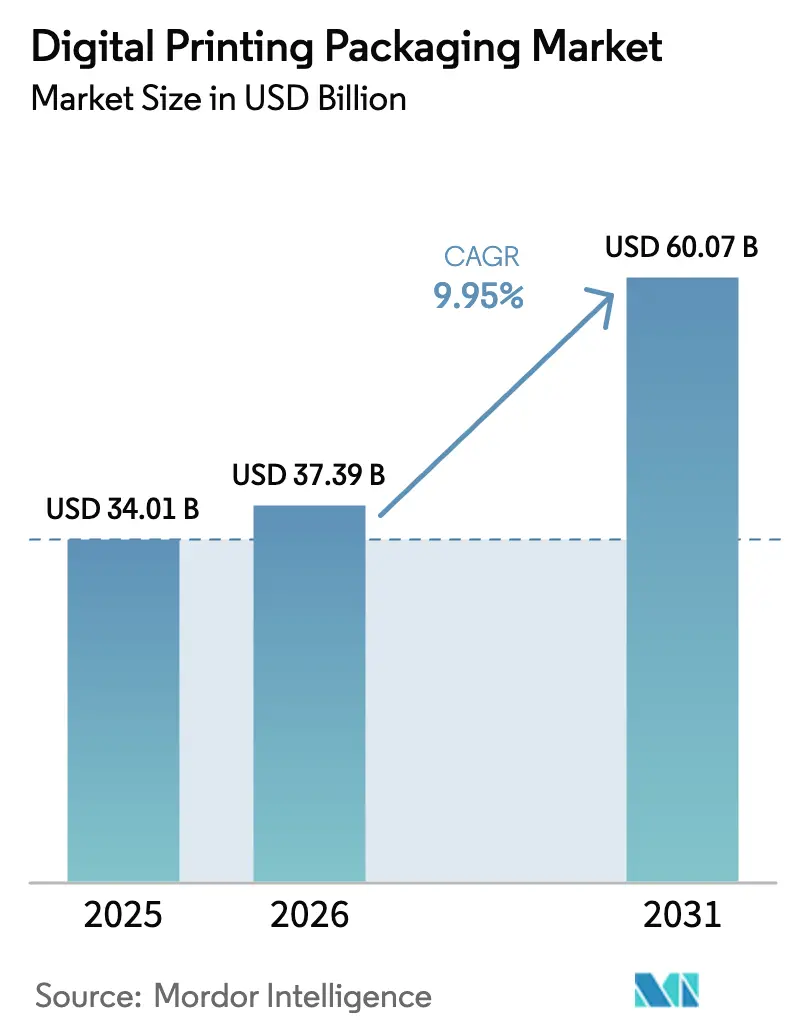

| Market Size (2026) | USD 37.39 Billion |

| Market Size (2031) | USD 60.07 Billion |

| Growth Rate (2026 - 2031) | 9.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

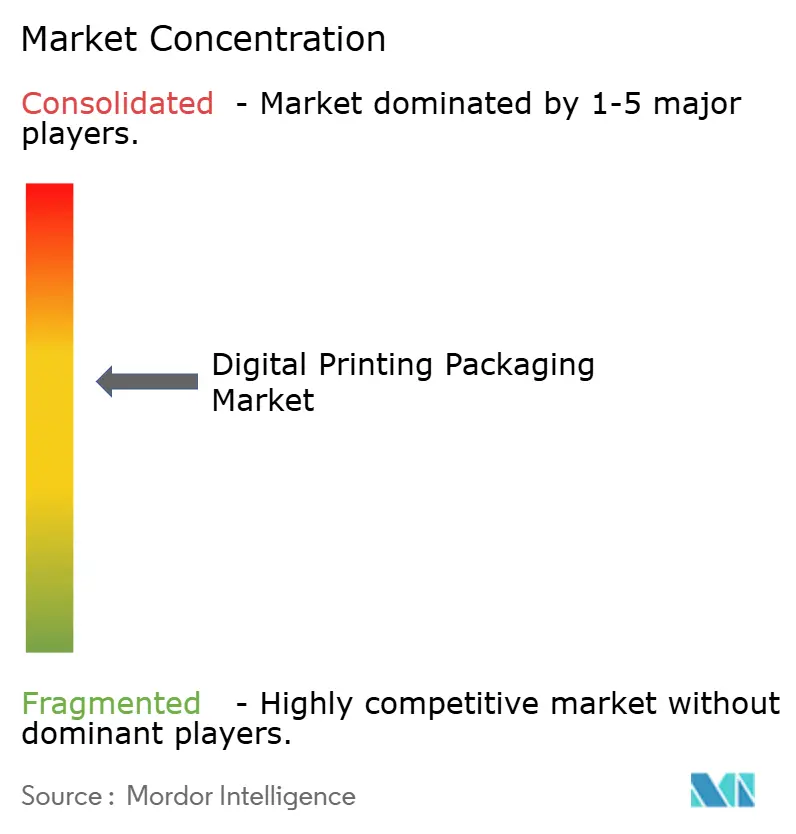

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Printing Packaging Market Analysis by Mordor Intelligence

The digital packaging printing market size was valued at USD 34.01 billion in 2025 and estimated to grow from USD 37.39 billion in 2026 to reach USD 60.07 billion by 2031, at a CAGR of 9.95% during the forecast period (2026-2031). Surging e-commerce sales, regulatory mandates for recyclable materials, and press speeds now exceeding 120 m/min are reshaping production economics. Brand owners are shifting from analog to plate-less workflows to capture mass-customization opportunities, reduce waste, and cut set-up time. Liquid-toner electrophotography currently leads volumes, yet inkjet systems are narrowing the quality gap while surpassing former speed barriers, which expands the addressable digital packaging printing market. Supply-chain pressures on inks and substrates persist, but automation and inline embellishment help converters safeguard margins through premium pricing, reinforcing the sector’s positive outlook.

Key Report Takeaways

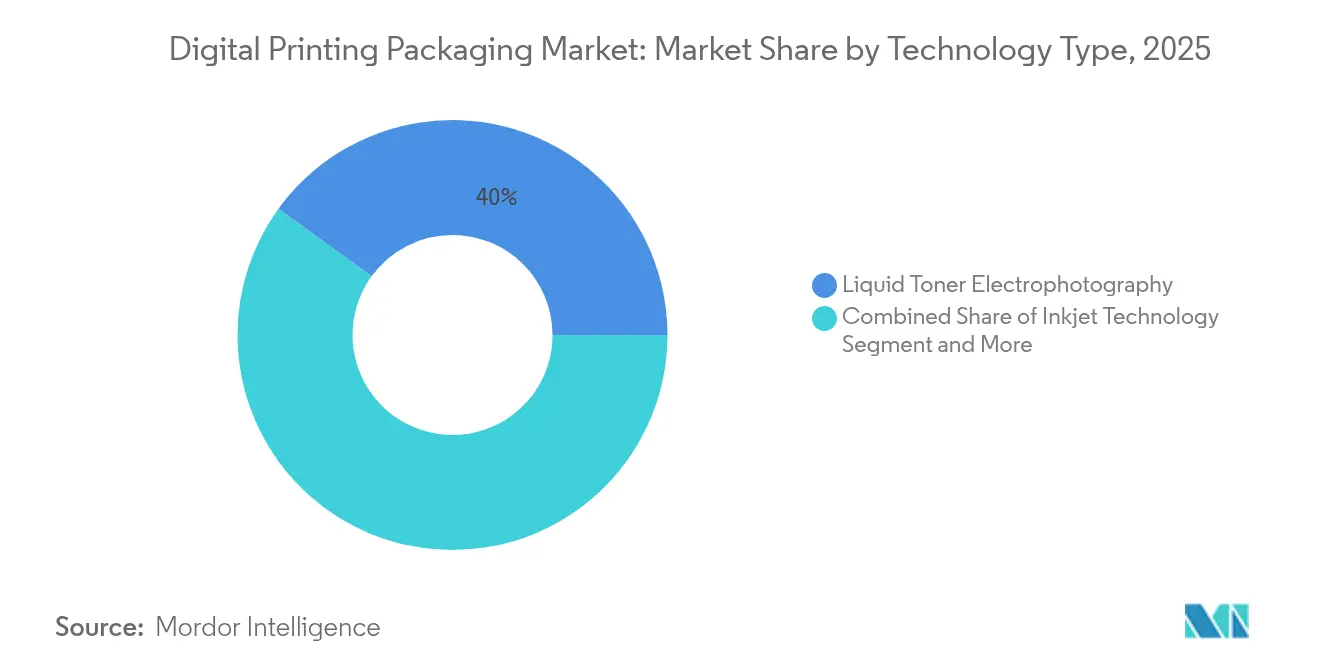

- By technology type, liquid-toner electrophotography held 40.02% of the digital packaging printing market share in 2025, while inkjet technology is set to post the fastest 14.25% CAGR through 2031.

- By product type, labels accounted for 35.12% of the digital packaging printing market size in 2025; flexible packaging is forecast to grow at a 12.87% CAGR to 2031

- By end-user industry, food maintained 30.10% revenue share in 2025; beverages are expected to expand at a 15.18% CAGR through 2031.

- By ink type, UV-cured formulations captured 44.20% revenue in 2025 and are rising at a 14.12% CAGR.

- By geography, North America led with 32.10% share in 2025, whereas Asia-Pacific is projected to climb at a 14.63% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Printing Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth in e-commerce and on-demand short runs | +2.1% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Sustainability push favoring plate-less digital presses | +1.8% | European Union, North America | Medium term (2-4 years) |

| Brand demand for mass-customised promotions and VDP | +1.4% | Global (FMCG-led) | Medium term (2-4 years) |

| Rapid press speed gains (> 120 m/min) | +1.2% | Manufacturing hubs in Asia-Pacific and North America | Short term (≤ 2 years) |

| Inline digital embellishment unlocking premiumisation | +0.9% | Premium consumer markets in North America and EU | Long term (≥ 4 years) |

| Personalised medicine and micro-fulfilment packaging | +0.7% | Developed healthcare markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth in E-commerce and On-Demand Short Runs

E-commerce parcel counts continue to climb, and average order quantities are shrinking. Digital presses profitably handle runs of 100 units compared with the 5,000-unit economic floor for flexography, giving converters the agility to win niche brand projects. American Packaging Corporation’s January 2025 commissioning of its HP Indigo 200K line typifies how converters reorganise operations to win these contracts. [1]American Packaging Corporation, “Introduces End-to-End Flexible Packaging Digital Unit,” whattheythink.com Corrugated packaging, used in 80% of e-commerce shipments, is projected to approach USD 400 billion in 2027, and digital print supports fit-to-product box formats that minimise void fill and reduce freight. Personalised box art increases customer engagement by up to 20%, reinforcing marketing ROI.

Sustainability Push Favoring Plate-Less Digital Presses

Regulators are imposing recyclability and recycled-content rules that favour plate-free print technologies. Europe’s Packaging and Packaging Waste Regulation requires all packaging to be recyclable by 2030, spurring a shift to digital presses that can vary print layouts without chemical plates. [2]European Commission, “New EU Regulation Promotes Sustainable Packaging,” green-forum.ec.europa.eu France’s phase-out of mineral-oil inks and Germany’s 15.3% eco-ink share underscore this momentum. OSP Group’s water-based inkjet line delivers 100 m/min while eliminating organic solvents, proving sustainability can coexist with throughput.

Brand Demand for Mass-Customised Promotions and VDP

Variable-data capability supports hyper-targeted campaigns and serialisation mandates. Breweries use shrink-sleeve labels for seasonal SKUs, and craft brands rely on digital print to test new designs with no plate charges. Connected-packaging elements such as QR codes are forecast to reach USD 83.02 billion by 2034, and digital presses embed these graphics in real time, enhancing supply-chain transparency.

Rapid Press Speed Gains Exceeding 120 m/min

Press suppliers have overcome historic speed barriers. The HP Indigo V12 matches flexo throughput at 120 m/min while preserving the set-up-free economics of digital printing. Epson’s new Akita printhead plant triples capacity, signalling confidence in accelerating industrial inkjet demand. These innovations widen the cost-competitive run-length window and expand mid-run applicability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile specialty-ink and substrate pricing | -1.6% | Global; acute in supply-constrained areas | Short term (≤ 2 years) |

| High capex / TCO versus flexo in long runs | -1.3% | Cost-sensitive Asia-Pacific and Latin America | Medium term (2-4 years) |

| Cyber-security downtime on Industry 4.0 presses | -0.8% | Connected facilities worldwide | Medium term (2-4 years) |

| VOC/NIAS regulation limiting ink chemistry options | -0.6% | EU & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Specialty-Ink and Substrate Pricing

Corrugated board increased by USD 70 per ton in January 2025, eroding digital converters’ thin margins.[3]Creative Edge Packaging, “Corrugated Cardboard Cost Increase,” cepkg.com Low-migration inks needed for food packs attract 20-30% premiums, and China’s 15% export dip on packaging substrates has tightened supply. Such volatility pressures short-run printers that lack buying scale.

High Capital Expenditure Versus Flexographic Printing in Long Runs

Although digital print eliminates plates, per-unit ink costs remain higher. RRD’s upgrade of its Georgia plant required sizeable investment in HP Indigo 120K and PageWide Advantage systems, a hurdle for smaller converters. The economics still favour flexo for very large jobs, capping digital’s penetration in commodity packaging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: Liquid Toner Dominance Faces Inkjet Disruption

Liquid-toner presses held 40.02% of the digital packaging printing market in 2025, thanks to HP’s LEP platform delivering 97% PANTONE coverage. Inkjet rivals, however, are clocking 14.25% CAGR, luring converters with wider substrate latitude and faster job changeovers. Canon’s varioPRESS iV7 entry symbolises the cross-over of electrophotography leaders into inkjet territory. Hybrid flexo-digital models address medium runs but add operational complexity.

Inkjet’s trajectory hinges on printhead advances and aqueous-ink chemistry that now meets food-pack regulations. Growth in this segment enlarges the digital packaging printing market size for converters aiming to serve flexible-pack and corrugated jobs. Yet LEP maintains a quality edge in high-accuracy colour work, securing its niche among premium label converters, which helps balance the technology mix longer term.

By Product Type: Labels Lead While Flexible Packaging Accelerates

Labels commanded 35.12% revenue in 2025, bolstered by serialisation laws in pharma and batch-coded nutraceutical lines. Craft brewers use shrink sleeves to differentiate SKUs, sustaining demand for roll-to-roll presses. As a result, labels still anchor the digital packaging printing market size across geographies.

Flexible packaging, projected to grow 12.87% annually, benefits from portion-control pouches and premium snack packs that require eye-catching graphics. Faster inkjet webs make short-run pouches cost-effective, and converters cite gains in foil-and-film adhesion. This shift elevates flexible packaging’s share of the digital packaging printing market as brands pursue lighter, reclosable formats.

By End-User Industry: Food Dominance Challenged by Beverage Growth

Food applications retained 30.10% revenue in 2025, owing to high-volume pouch and flow-wrap output. Export-oriented processors appreciate digital print’s rapid language changeover for multi-market SKUs. Beverage packs, notably craft beer cans, are accelerating at 15.18% CAGR as sleeve labels enable limited-edition designs with minimal inventory risk.

Pharma remains a steady adopter due to serialised cartons and tamper-proof seals. Körber’s supply-on-demand concept aligns with micro-lot drug production. Cosmetics exploit digital platforms for influencer collaborations. Collectively, diversification of end-users expands the digital packaging printing market, diluting reliance on any single vertical.

By Ink Type: UV-Cured Inks Dominate Across Applications

UV formulations controlled 44.20% share in 2025 and are still outpacing overall market growth at 14.12% CAGR. Instant curing helps converters meet tight lead times for moisture-sensitive beverage wraps. Water-based inks, once niche, now earn a foothold within regulatory-heavy food segments, aided by HP’s true water-based series.

Solvent inks persist in regions without stringent VOC rules, while latex and resin variants serve flex-pack jobs requiring high elongation. Ongoing R&D on compostable inks supports upcoming legislation, underpinning the long-term health of the digital packaging printing market.

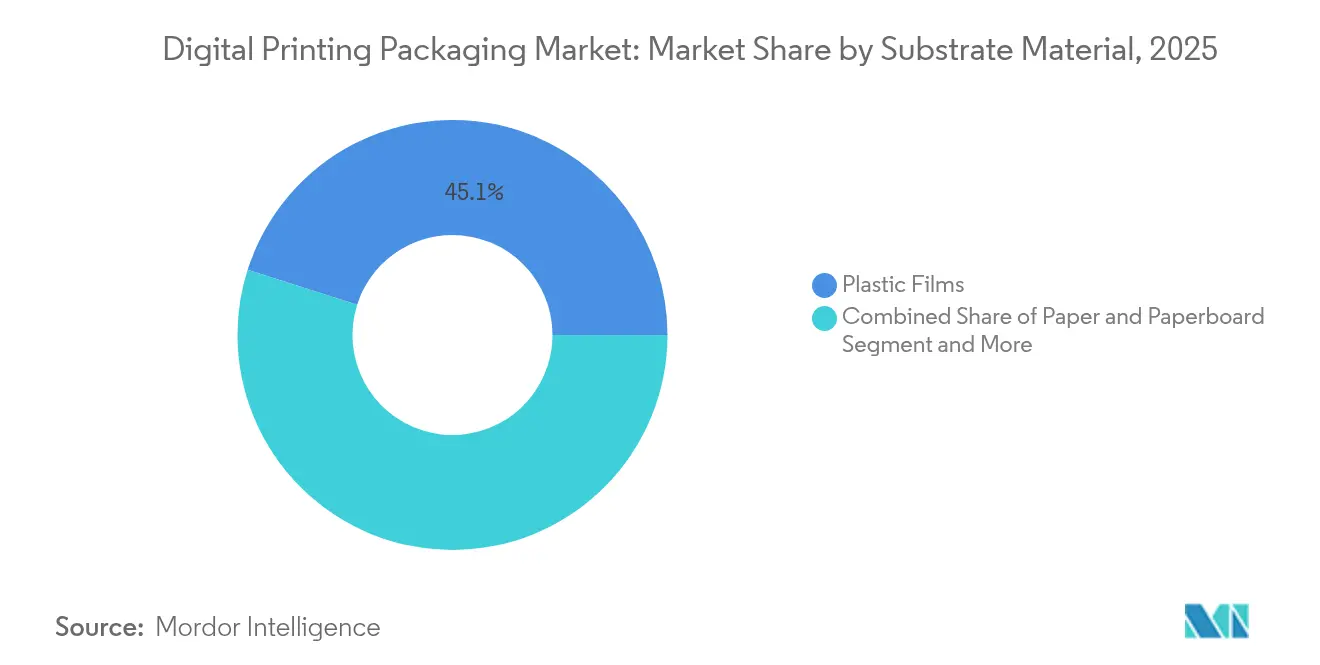

By Substrate Material: Plastic Films Lead Sustainability Transition

Plastic films represented 45.10% share in 2025, driven by snack and personal-care pouches. Paper and paperboard, however, are growing 14.88% annually as brands prepare for EU recyclability rules. Metal cans gain from direct-to-shape print innovations that let microbreweries order 1,000 customised units without labels. Glass and specialty synthetics sit in niche roles. Siegwerk’s compostable-ink roadmap supports fibre-based formats and keeps the digital packaging printing market aligned with circular-economy goals.

By Packaging Format: Primary Packaging Drives Innovation

Primary packs held 38.25% share in 2025, as consumer-facing graphics and regulatory data converge on the pack front panel. Serialisation, barcodes, and marketing codes often coexist, making digital print indispensable. Secondary packs enable retailer-specific promos without adding obsolete inventory, while tertiary packs—corrugated shipper boxes—are rising 12.28% each year, fuelled by e-commerce unboxing strategies. These dynamics fortify the relevance of digital packaging printing market solutions across the fulfilment chain.

Geography Analysis

North America captured 32.10% of the digital packaging printing market in 2025, anchored by mature e-commerce ecosystems and pharma compliance rules. HP, Xerox, and Domino maintain R&D hubs here, ensuring early access to latest presses. Canada and Mexico supplement growth through near-shoring and trade-focused plants, yet adoption rates trail the United States.

Asia-Pacific, forecast at a 14.63% CAGR, benefits from manufacturing digitisation programmes and rising FMCG consumption. China’s domestic demand offsets prior export softness, while Japan’s printhead capacity boom secures component supply. India’s pharma expansion and food-processing push attract investments in variable-data carton lines, broadening the digital packaging printing market footprint regionally.

Europe’s growth is steadier but regulation-driven. Germany’s eco-ink leadership and France’s mineral-oil ban incentivise converters to pivot to water-based systems. Nordic countries embed ecolabel criteria that reward digital workflows. Middle East and Africa show nascent but accelerating demand, especially in Gulf e-commerce hubs. South America posts incremental gains, constrained by currency volatility yet buoyed by food-export pack needs.

Competitive Landscape

The digital packaging printing market is moderately consolidated. HP, Canon, and Xerox retain scale advantages through integrated hardware, RIP software, and consumables. HP’s LEP franchise secures high-end label accounts, while Canon’s inkjet push through varioPRESS series widens reach. Specialist players—Xeikon, Domino, Landa—differentiate via narrow-web expertise or nanography, and partnerships like Landa–Gelato extend fulfilment reach.

Hybrid flexo-digital systems from Uteco and Koenig & Bauer Durst allow converters to toggle between analog cost efficiencies and digital agility. Ink suppliers such as INX International practice vertical moves, acquiring coating assets to bundle solutions. Cyber-secure press controllers and predictive-maintenance analytics are emerging battlegrounds.

Investment intensity is climbing: RRD’s Georgia revamp doubled staffing around HP digital lines, integrating robotics for near-lights-out workflows. Xerox’s pending Lexmark acquisition will merge A4 color platforms and supply chains, hinting at greater scale and R&D synergies.

Digital Printing Packaging Industry Leaders

HP Inc.

Mondi PLC

Huhtamaki Oyj

ePac Holdings LLC

International Paper

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: American Packaging Corporation launched an end-to-end flexible packaging digital unit built on HP Indigo 200K technology.

- January 2025: Heidelberger Druckmaschinen entered its 175th year, targeting over EUR 300 million in new sales from digital and packaging lines.

- February 2025: Ricoh, ETRIA, and OKI created a joint venture to develop cost-efficient LED-head multifunction printers.

- March 2025: Epson completed a new Akita printhead factory, tripling PrecisionCore capacity.

- April 2025: OSP Group began high-spec water-based inkjet production for flexible packs, eliminating organic solvents.

Global Digital Printing Packaging Market Report Scope

Digital printing allows for greater customization of packaging designs, which is crucial in the market where personalized experiences matter to consumers. Digital printing packaging refers to using digital printing technology to create packaging materials, such as labels, boxes, bags, and other containers. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The digital printing packaging market is segmented by technology type (Liquid Toner Electrography Printing, Nano-Graphic Printing, Inkjet Technology and Other Technologies), by product type (Labels, Flexible Packaging, Corrugated Packaging, Folding Cartons, Bottles & Jars and Other Products), by end-user industry (Food, Beverage, Pharmaceutical, Personal Care & Cosmetics, Electrical, Automotive and Other End-User Industries) and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa). The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

| Liquid Toner Electrophotography |

| Inkjet Technology |

| Nano-Graphic Printing |

| Other Technologies |

| Labels |

| Flexible Packaging |

| Corrugated Packaging |

| Folding Cartons |

| Bottles and Jars |

| Other Product Type |

| Food |

| Beverage |

| Pharmaceutical |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Automotive |

| Other End-User Industry |

| Solvent-based Inks |

| UV-cured Inks |

| Aqueous Inks |

| Latex and Resin-based Inks |

| Other Ink Types |

| Paper and Paperboard |

| Plastic Films |

| Metal |

| Glass |

| Other Substrate Material |

| Primary Packaging |

| Secondary Packaging |

| Tertiary / Transit Packaging |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| Spain | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Technology Type | Liquid Toner Electrophotography | ||

| Inkjet Technology | |||

| Nano-Graphic Printing | |||

| Other Technologies | |||

| By Product Type | Labels | ||

| Flexible Packaging | |||

| Corrugated Packaging | |||

| Folding Cartons | |||

| Bottles and Jars | |||

| Other Product Type | |||

| By End-User Industry | Food | ||

| Beverage | |||

| Pharmaceutical | |||

| Personal Care and Cosmetics | |||

| Electrical and Electronics | |||

| Automotive | |||

| Other End-User Industry | |||

| By Ink Type | Solvent-based Inks | ||

| UV-cured Inks | |||

| Aqueous Inks | |||

| Latex and Resin-based Inks | |||

| Other Ink Types | |||

| By Substrate Material | Paper and Paperboard | ||

| Plastic Films | |||

| Metal | |||

| Glass | |||

| Other Substrate Material | |||

| By Packaging Format | Primary Packaging | ||

| Secondary Packaging | |||

| Tertiary / Transit Packaging | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| France | |||

| Italy | |||

| Spain | |||

| United Kingdom | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the size of the digital packaging printing market today and where is it headed?

The market stands at USD 37.39 billion in 2026 and is forecast to reach USD 60.07 billion by 2031, reflecting a 9.95% CAGR.

Which printing technology is expanding at the fastest pace?

Inkjet systems are advancing at a 14.25% CAGR through 2031, outpacing other platforms as press speeds and substrate versatility improve.

What single factor is most responsible for accelerating adoption of digital presses?

Explosive e-commerce growth is driving demand for profitable short runs and customized packaging, adding an estimated +2.1% to the overall CAGR.

How dominant are UV-cured inks in the market?

UV formulations hold 44.20% revenue share in 2025 and continue to climb at a 14.12% CAGR thanks to instant curing and broad substrate compatibility.

Page last updated on: