Digital Textile Printing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

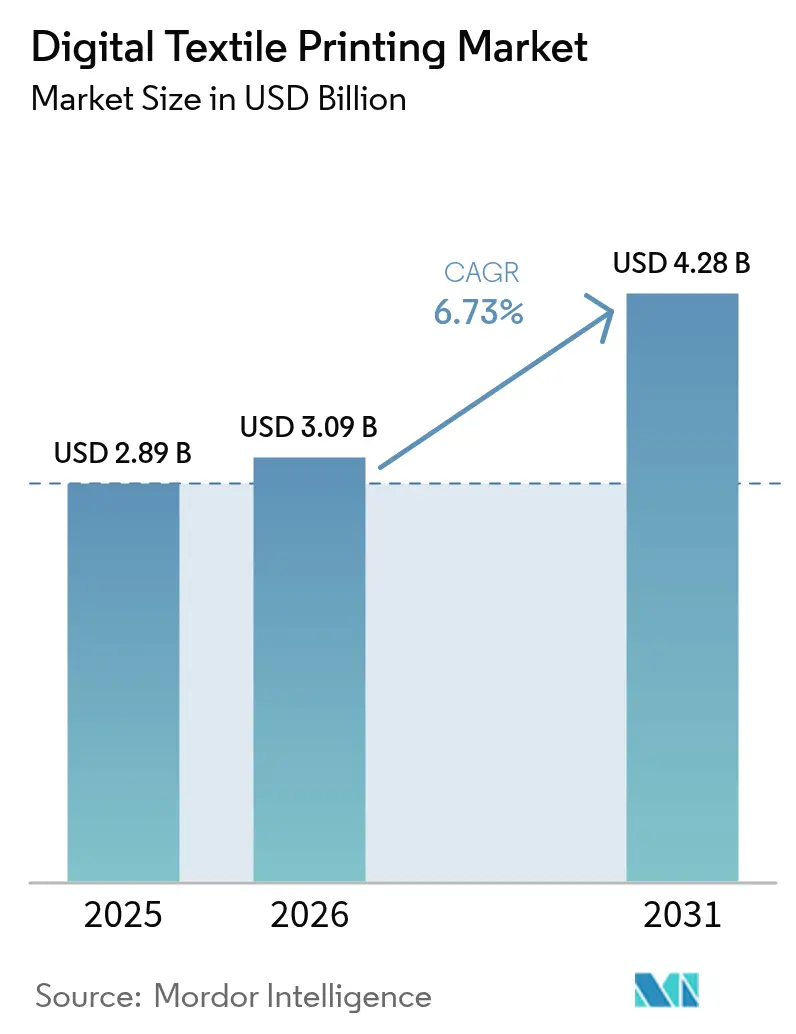

| Market Size (2026) | USD 3.09 Billion |

| Market Size (2031) | USD 4.28 Billion |

| Growth Rate (2026 - 2031) | 6.73% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Textile Printing Market Analysis by Mordor Intelligence

The digital textile printing market size is projected to be USD 2.89 billion in 2025, USD 3.09 billion in 2026, and reach USD 4.28 billion by 2031, growing at a CAGR of 6.73% from 2026 to 2031. Accelerating technology cycles, notably single-pass lines running 90–100 meters per minute, are compressing design-to-shelf lead times for fashion brands from weeks to days, reshaping contract manufacturing economics. Stricter European Union limits on per- and polyfluoroalkyl substances (PFAS) under EN 17681-1:2025 are compelling ink and equipment suppliers to re-engineer formulations and workflows. At the same time, print-on-demand platforms that handled about 150 million customized garments in 2025 continue to scale, driving demand for water-efficient, quick-changeover machinery. Asia-Pacific led with 33.71% revenue in 2025, but Gulf Cooperation Council investments are propelling the Middle East and Africa to the fastest 2026-2031 growth at 7.79%. Equipment vendors are responding with subscription “print-as-a-service” offers that shift large capital needs into predictable operating charges, broadening adoption in emerging regions.

Key Report Takeaways

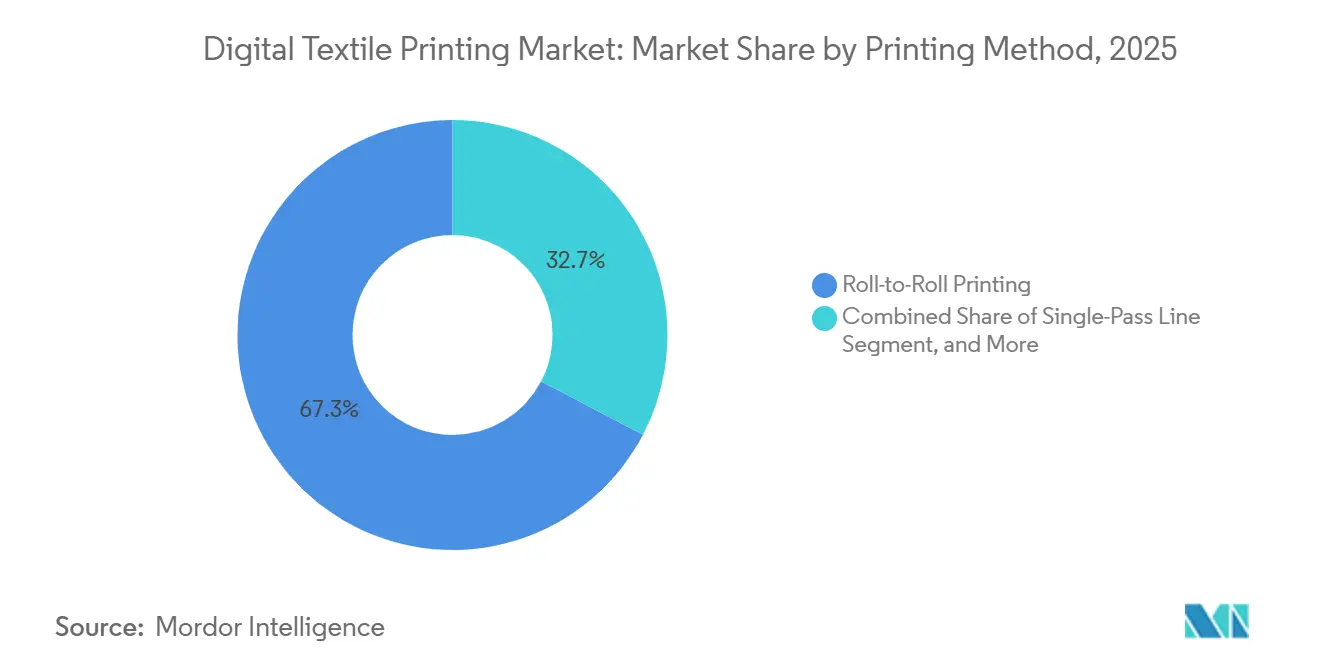

- By printing method, roll-to-roll systems led with 67.33% of the digital textile printing market share in 2025, while single-pass lines are forecast to expand at a 7.71% CAGR to 2031.

- By ink type, sublimation inks accounted for 53.47% of the digital textile printing market in 2025; pigment inks are projected to grow at a 7.74% CAGR through 2031.

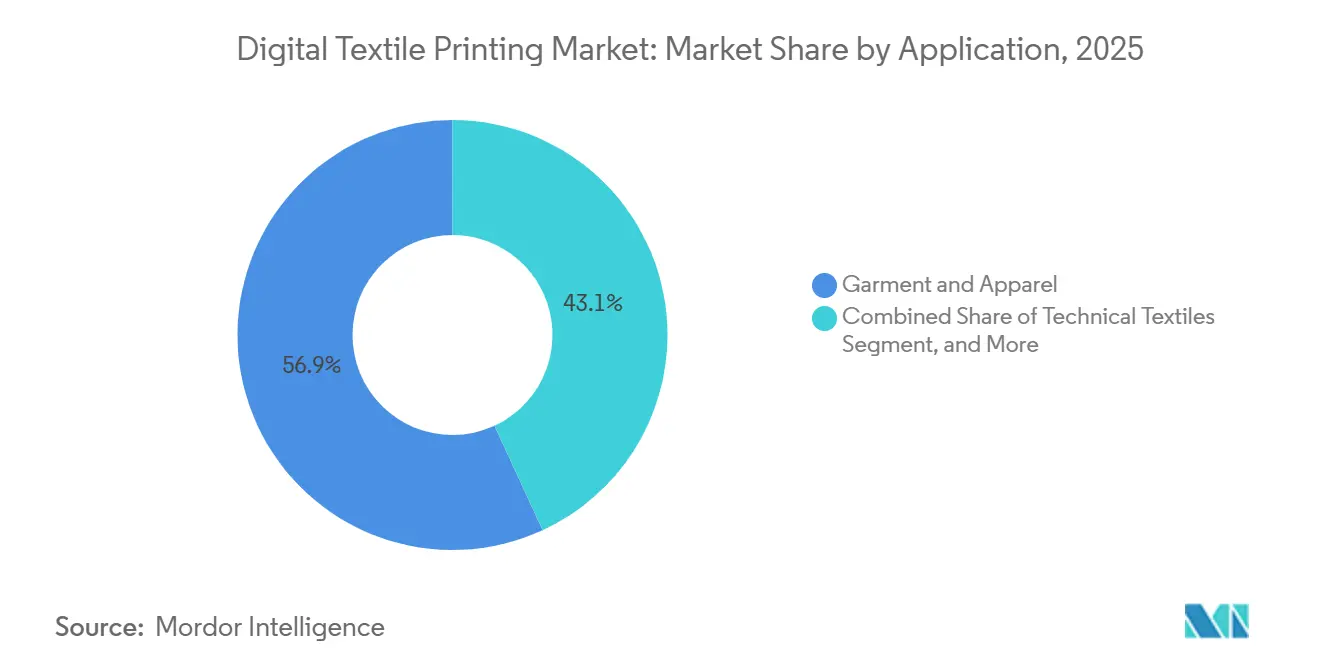

- By application, garment and apparel commanded 56.89% revenue in 2025, whereas technical textiles are poised for the quickest 7.56% CAGR between 2026-2031.

- By substrate, cotton accounted for 42.36% of volume in 2025, yet polyester is expected to grow at a 7.83% CAGR during 2026-2031.

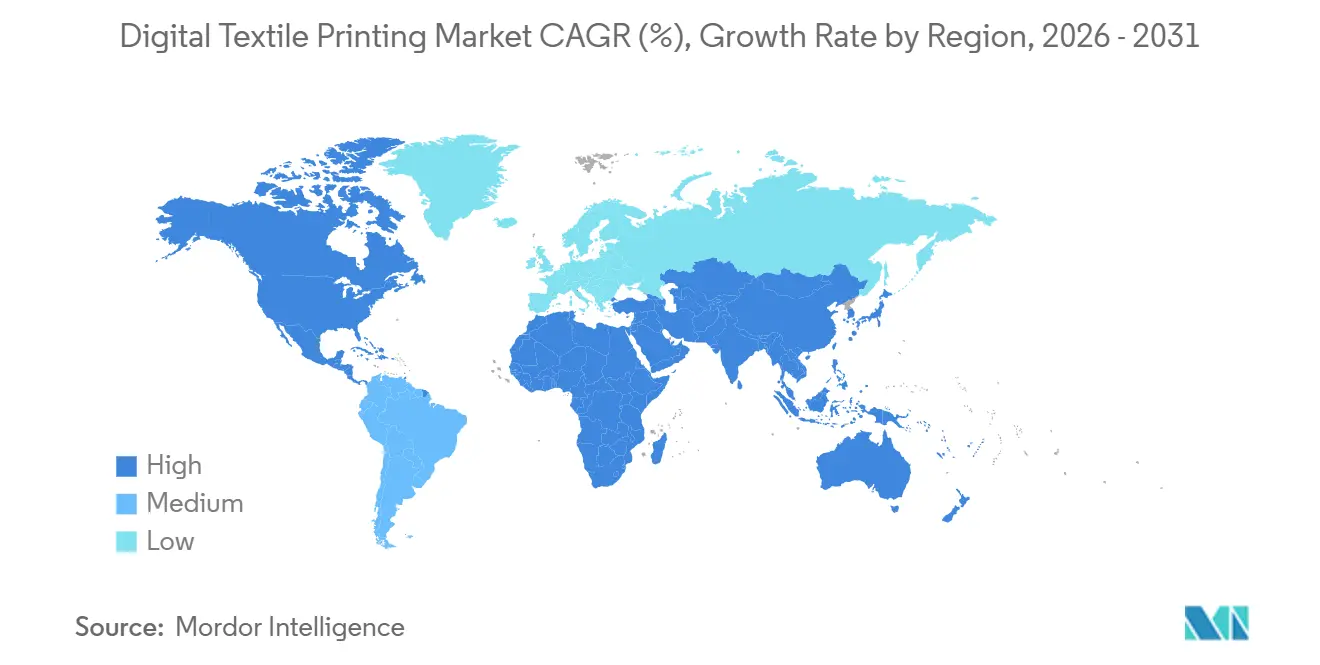

- By geography, Asia-Pacific dominated with a 33.71% share in 2025, but the Middle East and Africa region is projected to be the fastest-growing at 7.79% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Textile Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Personalization-Led Micro-Collections Boom | +1.2% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Single-Pass Inkjet Productivity Leap | +1.4% | Europe and North America industrial hubs | Short term (≤ 2 years) |

| E-Commerce Print-on-Demand Fulfillment | +1.0% | North America and Europe e-commerce ecosystems | Medium term (2-4 years) |

| Water-Saving Compliance Mandates | +0.9% | Asia-Pacific core, expanding to the Middle East and Africa | Long term (≥ 4 years) |

| AI-Driven Color Calibration Shrinking Rework | +0.7% | Quality-focused segments worldwide | Medium term (2-4 years) |

| Print-as-a-Service Leasing Models | +0.6% | South America and Southeast Asia emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Personalization-Led Micro-Collections Boom

Fast-fashion labels now approve designs and deliver finished garments to stores within one week, a pace unreachable with screen printing. Inditex documented an 18% drop in unsold inventory in 2024, thanks to digital presses that enabled its Zara unit to trial 50–100-piece runs before scaling production. Nike reported that customized items accounted for 12% of its direct-to-consumer revenue in 2025, up from 7% in 2023, demonstrating that buyers are willing to pay premiums for unique pieces.[1]Nike, “Investor Presentation 2025,” nike.com Reduced setup costs and the elimination of minimum order quantities enable microbrands to compete with incumbents, intensifying market fragmentation. The model also supports sustainability goals, because shorter runs prevent overproduction and lower end-of-life disposal fees under extended producer responsibility rules in Europe.

Single-Pass Inkjet Productivity Leap

New single-pass platforms such as EFI Reggiani BOLT sustain 95 meters per minute, tripling the output of the scanning heads that dominated in 2023.[2]Electronics For Imaging, “Reggiani BOLT Specifications,” efi.com SPGPrints PIKE lets converters toggle speed between 3 and 60 meters per minute, matching job requirements while preserving quality. Konica Minolta’s NASSENGER installations in 2025 integrated inline color measurement, enabling 24-hour unmanned shifts and cutting labor costs per square meter. Higher throughput narrows the cost gap with rotary screen printing for 1,000-meter orders, accelerating adoption across Italian and Turkish mills facing rising wages and strict water regulations. Contract manufacturers now secure same-week turnaround contracts that would have been impractical two years ago.

E-Commerce Print-on-Demand Fulfillment

Print-on-demand platforms processed about 150 million customized textile items in 2025 as integrations with Shopify and Wix removed entry barriers for online sellers.[3]Printful, “Annual Report 2024,” printful.com Printful cut average turnaround to 3.2 days in 2024, aided by Brother’s GTX-600 Pro Bulk printers that feature 1.8-liter ink tanks for uninterrupted runs. The European Union’s extended producer responsibility rules, effective 2025, make brands financially liable for unsold goods, further steering them toward on-demand workflows. Small creators can now offer hundreds of SKUs without holding inventory, while large retailers use the same networks for seasonal or influencer-led drops. The growth of this fulfillment model is expanding the total addressable print volume even in mature Western markets.

Water-Saving Compliance Mandates

Digital presses use 60–80 liters of water per kilogram of fabric, compared with 200 liters for screen printing, a 60% reduction that helps mills in water-stressed regions stay compliant. Tiruppur manufacturers increased their digital capacity by 35% in 2025 after the Tamil Nadu Pollution Control Board ordered a 40% cut in industrial water draw by 2027. The European Union’s revised Industrial Emissions Directive set discharge thresholds in 2024 that effectively require water-efficient technology for new textile facilities. Brands sourcing from India, Spain, and Portugal now demand proof of water savings in bid documents, making digital capability a prerequisite for large orders. Compliance pressure is therefore translating directly into equipment spending and retrofit projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex for Industrial Systems | -0.8% | South America, Africa, Southeast Asia emerging markets | Medium term (2-4 years) |

| Ink-Fabric Compatibility Hurdles | -0.6% | Global, especially blended substrates | Short term (≤ 2 years) |

| Color-Fastness QA Bottlenecks on High-Speed Lines | -0.4% | Europe and North America quality-sensitive customers | Medium term (2-4 years) |

| PFAS-Linked Pigment Regulatory Risk | -0.5% | Europe and North America with spillover to Asia-Pacific exporters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex for Industrial Systems

Industrial single-pass or roll-to-roll lines cost USD 500,000–2,000,000 before installation and training, far exceeding the budgets of many converters in South America and Africa. Interest rates above 10% in several emerging markets raise the effective price once financing charges are added, stretching payback periods beyond five years. Under-utilization is common; mills often run below 50% capacity for the first 18 months as they build customer pipelines. Leasing programs help but remain scarce in areas with high local credit risk, limiting access to the latest machines. The capital hurdle, therefore, slows regional adoption and concentrates market share among well-funded incumbents.

Ink-Fabric Compatibility Hurdles

Reactive dyes need alkaline pre-treatment and post-wash fixation, adding 15–20% to processing costs and extending lead times by up to 48 hours. Pigment inks bond to many fibers but can fade after just 15 laundry cycles on polyester blends, well short of the 40-cycle expectation in apparel supply contracts governed by ISO 105 standards. Converters must stock multiple ink sets and sometimes switch printheads, depressing asset utilization. Additional quality-assurance cycles raise rework rates and eat into thin margins on fast-fashion orders. These chemistry gaps limit digital’s addressable volume until new binders or hybrid workflows close the durability deficit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printing Method: Single-Pass Lines Reshape Industrial Economics

Roll-to-roll systems accounted for 67.33% of the digital textile printing market share in 2025, while single-pass lines are forecast to record a 7.71% CAGR between 2026-2031, the fastest among all printing methods. The productivity jump to 90–100 m/min lets converters match mid-tier rotary screen output, narrowing cost gaps and encouraging mills in Italy and Turkey to retire analog lines. Fast throughput also absorbs surges in micro-collection orders with five-day lead times from fashion retailers, minimizing queue bottlenecks and overtime costs.

Single-pass adoption is strongest where labor and compliance costs are high, because platforms such as EFI Reggiani BOLT integrate inline vision and tension control, enabling 24-hour unmanned shifts. SPGPrints PIKE offers variable speed from 3–60 m/min, letting converters balance color saturation with delivery promises. Hybrid machines combining digital heads with rotary stations remain niche because the increased workflow complexity offsets savings from specialty effects. Direct-to-garment units continue to attract startups, but the lack of material-handling automation caps volume, leaving high-run work to single-pass or roll-to-roll lines.

By Ink Type: Pigment Formulations Gain on Substrate Versatility

Sublimation inks held 53.47% of the digital textile printing market share in 2025, reflecting polyester’s pull in sportswear and signage segments. Brands emphasize the durability of sublimation, which can withstand up to 50 washes. Advanced 3.2-meter printers, such as the HP Stitch S1000, have extended the application of this technique to home-textile widths. However, the chemical process used in sublimation is compatible only with polyester materials, necessitating the use of alternative methods for cotton and blended fabrics.

Pigment inks are projected to grow at 7.74% annually through 2031 as advances in polymer binders raise wash fastness on both natural and synthetic fibers. Their ability to print cotton, polyester, and blends without pre-treatment trims cycle times by up to two days, freeing capacity during peak seasons. Reactive and acid inks hold their own on premium silk and deep-shade cotton, yet pre-wash and steaming steps increase water use, an issue under Europe’s stricter discharge limits. Formulators are also stripping PFAS from pigment recipes ahead of the 25 ppb threshold in EN 17681-1:2025, a shift that tightens collaboration between ink makers and equipment OEMs.

By Application: Technical Textiles Leverage Performance Mandates

Garments and apparel accounted for 56.89% of the digital textile printing market share in 2025, cementing the sector’s reliance on fast fashion and customized merchandise. Digital workflows, which eliminate the need for screen setup and facilitate 50-piece test runs, are increasingly being adopted due to the pressures associated with shorter lead times. This transition not only enhances operational efficiency but also aligns with the sustainability objectives of retailers, who are committed to minimizing dead stock and reducing environmental impact.

Technical textiles are forecast to post the fastest 7.56% CAGR during 2026-2031 as automotive, aerospace, and medical supply chains demand precise pattern placement, flame-retardant inks, and ISO-traceable lot codes. Car makers deploy digital printing for seat covers and headliners to localize trims per model variant, trimming inventory of pre-printed rolls. In medical fabrics, ISO 13485 compliance requires validation of every colorant batch, a process simplified when printers deposit exact amounts under closed-loop spectrophotometry. Home-textile growth is steadier because price-sensitive buyers weigh digital’s higher ink cost against its design flexibility, whereas display graphics keep expanding on the back of trade-show and retail-fixture refresh cycles.

By Substrate: Polyester Gains on Fiber Economics and Performance

Cotton represented 42.36% of 2025 volume, but polyester substrates are projected to climb at a 7.83% CAGR, the highest among materials, supported by their 60% share of world fiber production in 2024. Polyester's dimensional stability and moisture-wicking properties make it highly suitable for use in performance apparel. Additionally, sublimation inks provide vibrant and long-lasting graphics that do not bleed, even after multiple washes.

Water-intensive cotton faces rising scrutiny: irrigation costs add volatility, and brands track farm-level data to meet ESG scorecards. Blended fabrics complicate chemical choices, reactive dyes do not bind to polyester portions, and sublimation will not bond to cotton. Pigment inks bridge that gap, though durability trails mono-fiber solutions by roughly 10 laundry cycles. Luxury silk stays a premium niche; digital heads with 1,200 dpi resolution capture micro-floral motifs that command high margins despite low yardage. Nylon penetrates activewear thanks to its stretch and quick-dry properties, with acid inks providing the required vibrancy but at the expense of higher pH control.

Geography Analysis

Asia-Pacific held 33.71% of the digital textile printing market share in 2025, anchored by large-scale investments in China’s Shengze hub and rising installations across India’s Tiruppur cluster. Government water-saving mandates in Tamil Nadu are pushing mills toward machines that cut consumption by 60%, accelerating regional demand. The Middle East and Africa region is forecast to post the fastest CAGR of 7.79% through 2031, as the United Arab Emirates and Saudi Arabia channel petrochemical revenues into value-added textile parks that bundle tax holidays with subsidized utilities. New factories in Dubai Industrial City and Riyadh’s MODON zones often specify single-pass lines up-front, avoiding costly retrofits later.

North America benefits from near-shoring strategies that let apparel brands trim trans-Pacific lead times from 30 days to under 10. Contract printers in Mexico and the southern United States favor roll-to-roll pigment systems that handle cotton-rich blends common in regional fashion programs. Europe remains the most regulated environment; the revised Industrial Emissions Directive requires tight effluent ceilings for new finishing plants, effectively steering converters in Italy, Spain, and Portugal toward water-efficient platforms. Brands sourcing from these countries also face end-of-life fees under the 2025 extended producer responsibility rules, so they now insist on on-demand production to cap excess inventory.

Currency volatility and double-digit borrowing costs have slowed capital spending in South America, yet print-as-a-service contracts that wrap equipment, ink, and maintenance into pay-per-meter fees are gaining traction among Brazilian and Argentine converters. Africa remains a patchwork market: Egypt and South Africa run export-oriented mills that retrofit digital heads onto existing lines, while Ethiopia and Kenya court greenfield projects through duty-free access to the U.S. under the African Growth and Opportunity Act. These new clusters often import Chinese single-pass units priced 30–40% below European models, trading lower acquisition cost against thinner local service networks. As a result, the digital textile printing market size in emerging African and South American corridors is growing from a small base but still trails the scale achieved in Asia or Europe.

Competitive Landscape

The competitive field remains moderately fragmented; no supplier exceeded 15% revenue in 2025, leaving room for regional challengers. Dedicated inkjet specialists such as Kornit Digital and Epson focus on direct-to-garment and industrial roll-to-roll systems, while diversified imaging giants HP and Canon leverage broad service footprints to win multisite deals. Traditional screen-printing vendors like SPGPrints retrofit digital heads onto legacy frames, selling hybrid machines that let customers preserve sunk assets yet tap variable-data jobs.

Strategic moves concentrate on vertical integration and ecosystem partnerships. EFI Reggiani bundles workflow software and remote diagnostics with its BOLT platform, locking in consumables revenue and smoothing customer onboarding. Mimaki Engineering links its Tiger-1800B MkIII to color-management suites that cut pre-press time, and Konica Minolta’s subscription contracts include ink, service, and automatic firmware upgrades, turning capital expense into a predictable operating charge. Chinese entrants such as Shenzhen Homer pitch single-pass units at 30–40% lower list prices than European peers, but buyers in quality-critical automotive and medical segments worry about after-sales parts availability.

Mergers and alliances are also reshaping the supplier map. In September 2025, EFI Reggiani signed a memorandum of understanding with Turkey-based Sanko Textile to install three BOLT lines, which will increase Sanko’s digital capacity by 30% once operational. HP opened its Barcelona demonstration center in June 2025 and launched PFAS-free latex pigment sets for the Stitch S1000, giving converters an EU-compliant option a year before stricter chemical limits bite. In November 2025, Kornit Digital rolled out the Atlas Max Poly Plus firmware upgrade, which increases wash fastness on recycled polyester and was delivered over the air to subscribers at no extra cost. These moves illustrate how suppliers use technology refreshes, pilot installations, and consumables innovation to cement share in a market that still rewards speed, flexibility, and regulatory foresight.

Digital Textile Printing Industry Leaders

Seiko Epson Corporation

Kornit Digital Ltd.

Mimaki Engineering Co. Ltd.

Durst Group AG

Roland DG Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Kornit Digital rolled out the Atlas Max Poly Plus firmware and ink upgrade, enabling high-wash-fastness printing on recycled polyester; the enhancement was distributed to existing users through an over-the-air software update included in subscription contracts.

- September 2025: EFI Reggiani signed a memorandum of understanding with Turkey-based Sanko Textile to install three BOLT single-pass systems by year-end, a move expected to raise the mill’s digital output capacity by 30%.

- June 2025: HP opened a digital-textile demonstration center in Barcelona and released a PFAS-free latex pigment ink set for the Stitch S1000 line, giving converters an EU-compliant option ahead of 2026 regulatory deadlines.

- April 2025: Epson introduced the Monna Lisa ML-32000 industrial textile printer, a next-generation platform that boosts throughput by 20% over the prior model and completed its first commercial installation at an Italian fashion converter.

Global Digital Textile Printing Market Report Scope

The Digital Textile Printing Market Report is Segmented by Printing Method (Roll-to-Roll Printing, Direct-to-Garment, Single-Pass Line, Hybrid, Other Printing Methods), Ink Type (Sublimation, Pigment, Reactive, Acid, Disperse), Application (Garment and Apparel, Home Textiles, Technical Textiles, Display and Signage), Substrate (Cotton, Polyester, Silk, Nylon, Blends), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Roll-to-Roll Printing |

| Direct-to-Garment |

| Single-Pass Line |

| Hybrid |

| Other Printing Methods |

| Sublimation |

| Pigment |

| Reactive |

| Acid |

| Disperse |

| Garment and Apparel |

| Home Textiles |

| Technical Textiles |

| Display and Signage |

| Cotton |

| Polyester |

| Silk |

| Nylon |

| Blends |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Printing Method | Roll-to-Roll Printing | ||

| Direct-to-Garment | |||

| Single-Pass Line | |||

| Hybrid | |||

| Other Printing Methods | |||

| By Ink Type | Sublimation | ||

| Pigment | |||

| Reactive | |||

| Acid | |||

| Disperse | |||

| By Application | Garment and Apparel | ||

| Home Textiles | |||

| Technical Textiles | |||

| Display and Signage | |||

| By Substrate | Cotton | ||

| Polyester | |||

| Silk | |||

| Nylon | |||

| Blends | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the digital textile printing market today and where is it heading?

The digital textile printing market size stands at USD 3.09 billion in 2026 and is projected to reach USD 4.28 billion by 2031 at a 6.73% CAGR.

Which printing method is expanding fastest?

Single-pass lines are the fastest-growing configuration, projected to post a 7.71% CAGR during 2026-2031 thanks to throughputs of up to 100 m/min.

What ink chemistry is gaining share beyond sublimation?

Pigment formulations are advancing at 7.74% per year because they work on cotton, polyester, and blends without fabric-specific pre-treatment.

Why is Middle East and Africa growth outpacing other regions?

Diversification programs in the UAE and Saudi Arabia, combined with tax incentives and new industrial parks, are driving a 7.79% regional CAGR.

How are water-saving rules influencing technology adoption?

Mandates that cut water use by 40% in areas like Tiruppur favor digital printing, which needs 60–80 L per kg of fabric versus 200 L for screen printing.

What business model innovations lower entry barriers?

Print-as-a-service contracts convert USD 500 k-plus capital costs into monthly fees of USD 5 k-15 k, enabling small converters to access industrial equipment.

Page last updated on: