Premium Cosmetics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

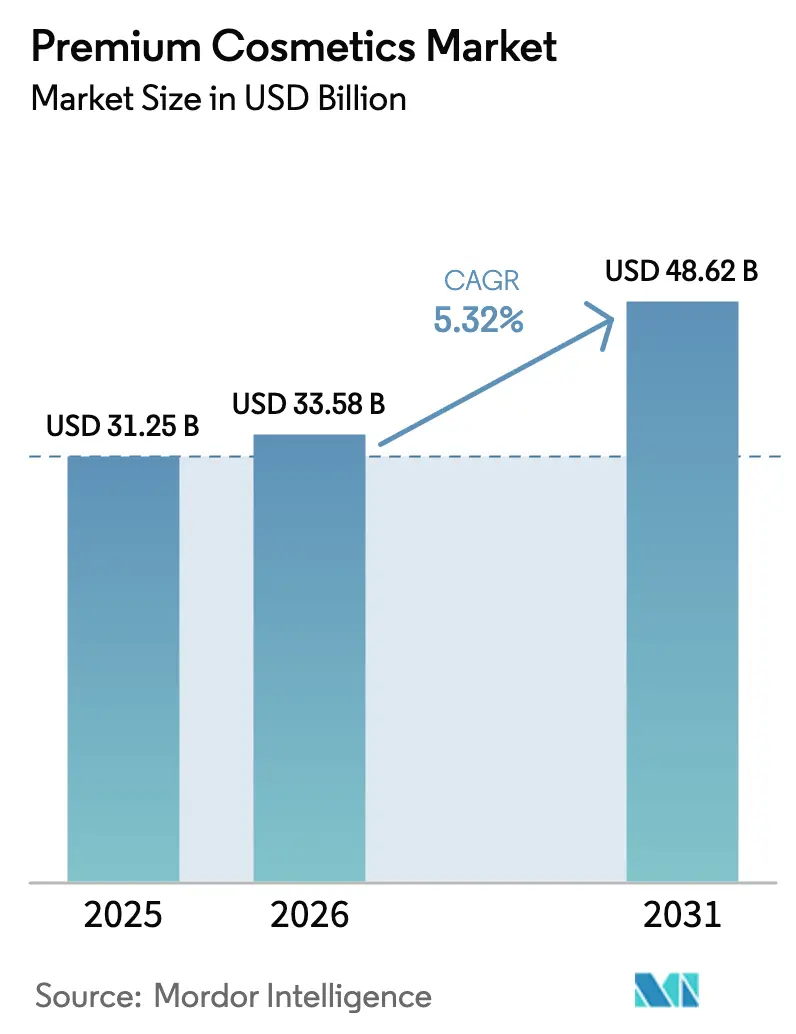

| Market Size (2026) | USD 33.58 Billion |

| Market Size (2031) | USD 48.62 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

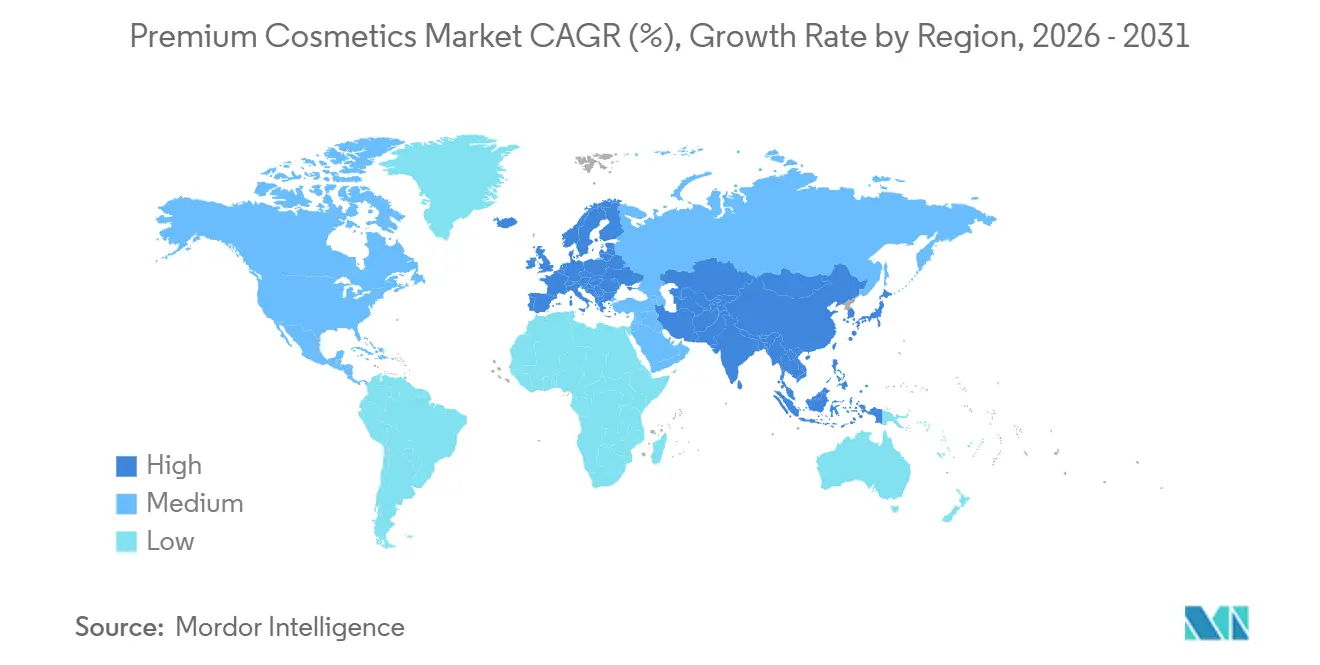

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Premium Cosmetics Market Analysis by Mordor Intelligence

The premium cosmetics market size is projected to expand from USD 31.25 billion in 2025 and USD 33.58 billion in 2026 to USD 48.62 billion by 2031, registering a CAGR of 5.32% between 2026 to 2031. Multinational brands are rebuilding research pipelines around biotech actives, while data-driven personalization and regulatory scrutiny are redefining competitive advantage. Lab-grown skin models, AI peptide design, and precision-fermentation inputs are shortening product-development cycles and reducing reliance on animal or petrochemical sources. At the same time, consumer insistence on clean-label formulations is pushing suppliers to re-engineer preservatives and colorants that meet COSMOS standards without compromising performance. Europe continues to anchor brand prestige through heritage storytelling, yet Asia-Pacific’s accelerated adoption of clinical-grade K-beauty concepts is shifting innovation gravity eastward. Counterfeit infiltration, escalating compliance costs under the FDA’s MoCRA, and social-commerce fragmentation add layers of operational risk that favor scale players capable of absorbing overhead.

Key Report Takeaways

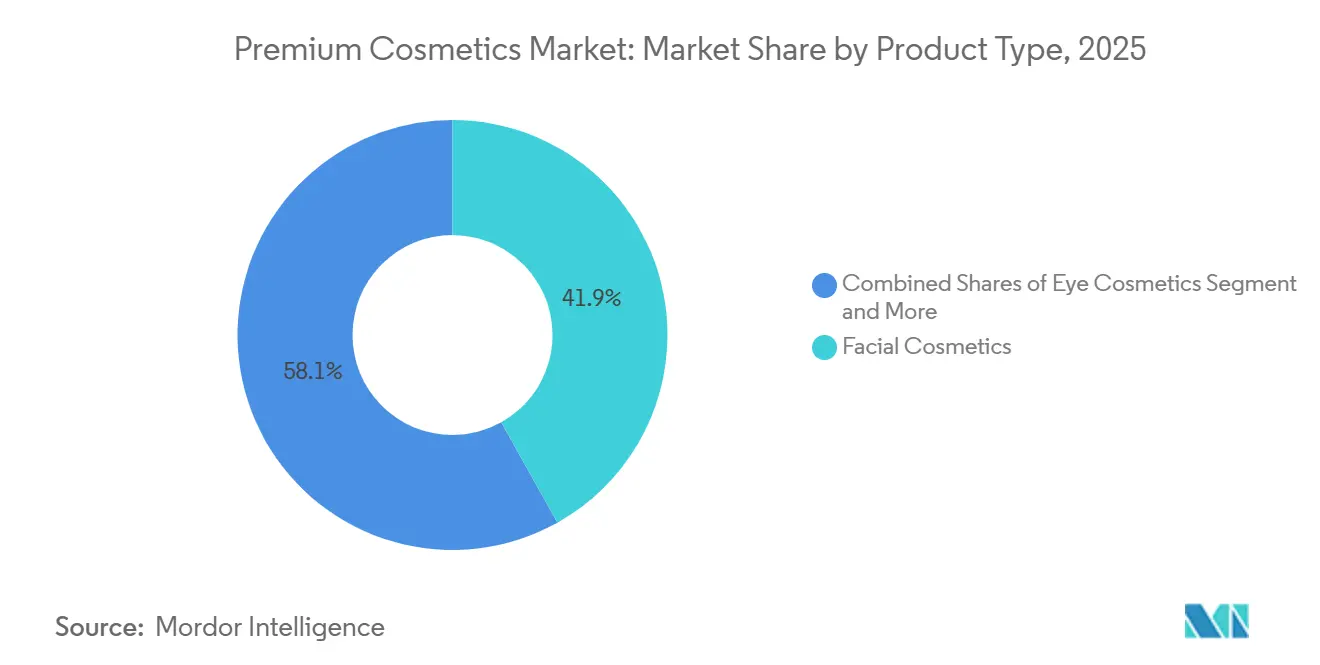

- By product type, facial cosmetics held 41.89% of the premium cosmetics market share in 2025, while eye cosmetics are advancing at a 6.58% CAGR through 2031.

- By category, organic and natural products commanded 57.52% of the premium cosmetics market size in 2025 and are expanding at a 6.42% CAGR to 2031.

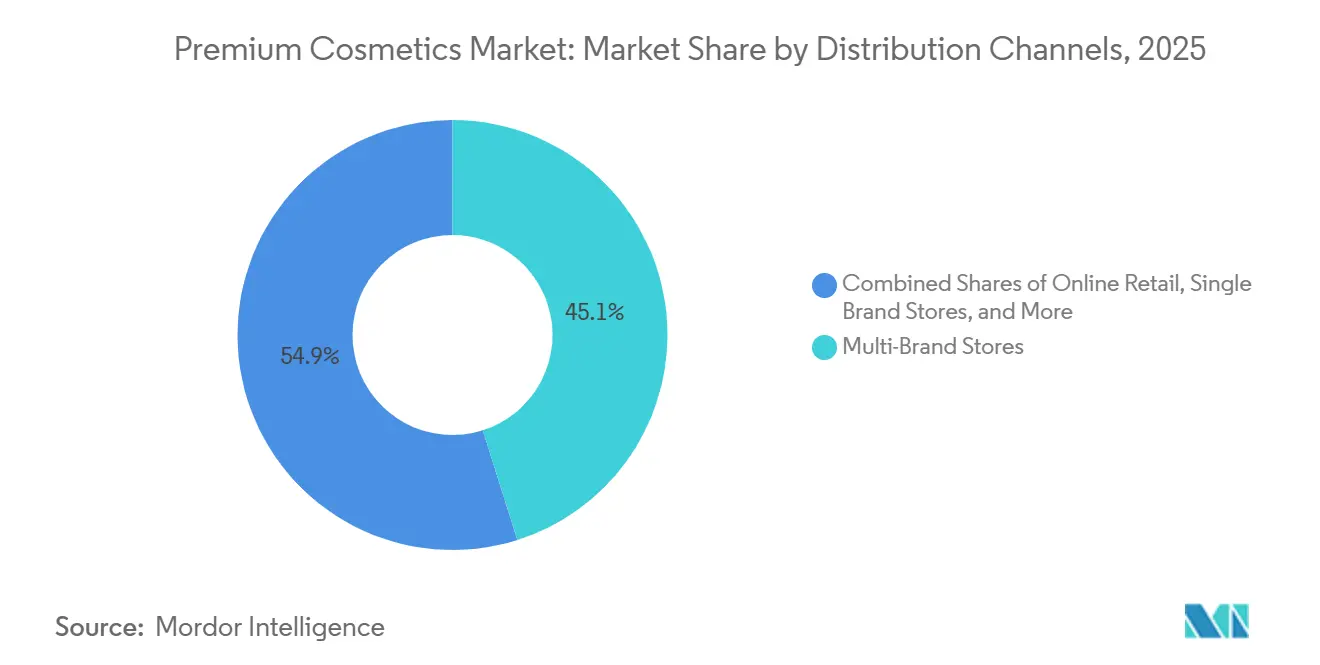

- By distribution channel, multi-brand stores led with 45.11% of revenue in 2025, but online retail is forecast to grow at a 6.77% CAGR between 2026 and 2031.

- By geography, Europe contributed 32.35% of 2025 sales, whereas Asia-Pacific is set to post the fastest regional CAGR at 7.57% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Premium Cosmetics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Brand Prestige and Exclusivity Appeal | +0.9% | Global, with concentration in Europe and North America | Medium term (2-4 years) |

| Premium Packaging and Sensory Experience | +0.7% | Europe and Asia-Pacific luxury hubs | Short term (≤ 2 years) |

| Rising Demand for Clean and Natural Ingredients | +1.2% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rising Social Media Influence and Viral Marketing | +1.1% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Advanced Biotech and AI-Driven Formulations | +0.8% | North America and Europe R&D centers | Long term (≥ 4 years) |

| Increasing Personalization Through Custom Beauty Solutions | +0.6% | North America and Asia-Pacific urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Brand Prestige and Exclusivity Appeal

As Gen Z consumers, set to represent 40% of luxury spending by 2030, lean towards brand storytelling over mere ingredient lists, heritage narratives, and scarcity tactics are proving more effective than product efficacy in justifying price premiums. In 2024, Chanel's move to restrict online access to select lipstick shades, making them exclusive to physical boutiques, resulted in a 25% surge in foot traffic to its flagship stores in Paris and Tokyo. This underscores the potency of artificial scarcity in mitigating e-commerce's encroachment. Meanwhile, LVMH's Perfumes & Cosmetics division, boasting a 2024 revenue of EUR 8.13 billion with a 2% organic growth, credits its resilience to a strategy that marries age-old French perfumery traditions with discreet biotech active reformulations. This blend of a heritage façade with an innovative core empowers established brands to command markups of 300 to 500% over their mass-market counterparts, all without facing consumer backlash. Following suit, smaller entities like Maison Francis Kurkdjian are elevating fragrances to the status of olfactory art, a narrative that shields their pricing from the whims of ingredient-cost fluctuations.

Premium Packaging and Sensory Experience

As EU regulations clamp down on single-use plastics, brands are compelled to redesign their primary packaging or risk penalties. Refillable compacts and airless pump dispensers have evolved from mere sustainability gestures to essential competitive tools. In 2024, Chanel introduced its Les Beiges refillable cushion foundation, achieving a 60% reduction in per unit. Yet, it retained the tactile weight and magnetic closure synonymous with luxury. Guerlain's Abeille Royale serum, encased in a glass bottle adorned with a gold-plated bee emblem, showcases the power of sensory cues. Features like heft, metallic accents, and audible clicks justify its EUR 150 (USD 160) price tag, even though the active ingredients are produced for under EUR 5. While post-consumer recycled (PCR) materials have become the norm in prestige lines, brands are learning a crucial lesson: consumers may shun "eco-friendly" packaging if it lacks a premium feel. Responding to this insight, Estée Lauder in 2024 transitioned to a heavier PCR glass for its Advanced Night Repair. The takeaway is evident: sustainability should elevate the unboxing experience, turning first-time buyers into loyal customers.

Rising Demand for Clean and Natural Ingredients

COSMOS-certified formulations captured 57.52% of the premium cosmetics market in 2025, yet this dominance masks a brewing tension: natural actives often underperform synthetic alternatives in stability and penetration, forcing brands to choose between efficacy and certification. Bakuchiol, marketed as a gentler retinol substitute, demonstrates only 40-50% of retinol's collagen-stimulation capacity in peer-reviewed trials, yet commands 20% price premiums because consumers conflate "natural" with "safe". Ecocert and USDA Organic certifications require that 95% of agricultural ingredients be organically farmed, a threshold that eliminates high-performing peptides like Matrixyl and Argireline from clean-beauty SKUs. Brands are responding by bifurcating portfolios: Kora Organics targets the clean-beauty cohort with COSMOS-certified oils, while sister brands under the same corporate umbrella deploy synthetic actives for performance-focused consumers. This segmentation strategy allows conglomerates to capture both demographics without diluting brand equity, but it requires parallel supply chains that inflate overhead by 15-20%.

Rising Social Media Influence and Viral Marketing

Influencer-generated content delivered USD 1.6 billion in media impact value for L'Oréal Paris in 2024, surpassing the brand's paid advertising spend and confirming that third-party endorsements now drive purchase intent more effectively than owned media. Huda Beauty's USD 945.8 million in 2024 MIV demonstrates how founder-led brands can monetize personal followings without traditional retail distribution; the brand's #FauxFilter foundation became TikTok's most-searched makeup product in Q2 2024 despite zero TV advertising. Yet this channel is fragmenting: Gen Alpha's "Sephora Kids" phenomenon, 10-to-14-year-olds who spent USD 4.7 billion on skincare in 2023- signals that influencer marketing must now target parents and tweens simultaneously, a dual-audience challenge that legacy brands struggle to navigate. The strategic risk is over-reliance on a handful of mega-influencers; when one creator's scandal can erase months of brand-building, diversification across micro-influencers (10,000-50,000 followers) becomes a risk-mitigation imperative rather than a reach-maximization tactic.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Presence of Counterfeit Products and Brand Dilution | -0.8% | Global, concentrated in Asia-Pacific and online channels | Short term (≤ 2 years) |

| Stringent Global Regulatory Compliance | -0.6% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| High Research and Development Costs | -0.5% | Global, most acute for mid-tier brands | Medium term (2-4 years) |

| Allergic Reactions and Skin Sensitivities | -0.4% | Global, heightened scrutiny in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Presence of Counterfeit Products and Brand Dilution

In 2024, counterfeits nearly identical to genuine products without lab testing cost the premium cosmetics industry an estimated USD 3.2 billion in lost revenue. Luxury skincare serums and exclusive makeup palettes bore the brunt of these counterfeit attacks. A 2024 campaign by the UK Intellectual Property Office highlighted alarming instances, such as counterfeit MAC lipsticks containing lead levels exceeding the EU safety threshold by tenfold[1]Source: UK Intellectual Property Office, “Anti-Counterfeiting Campaign 2024,” gov.uk. These incidents not only led to hospitalizations but also tarnished the brand's reputation, despite the UK IPO facing no blame. Analysis from MarqVision uncovered a troubling trend: 33% of consumers, after unknowingly buying fake prestige cosmetics, chose not to repurchase the authentic version, mistakenly linking quality defects to the brand itself. While brands are turning to solutions like NFC chips, QR code authentication, and blockchain tracking to combat counterfeiting, these measures come at an added cost of USD 0.50 to 1.50 per unit. This price increase poses a challenge for mid-tier brands, making it difficult to absorb without adjusting their prices. Brands now face a critical choice: invest in anti-counterfeiting measures that might go unnoticed by consumers or watch their brand value diminish as fakes spread on social commerce platforms with weak enforcement.

Stringent Global Regulatory Compliance

Under the FDA's Modernization of Cosmetics Regulation Act (MoCRA), brands must register their facilities by December 2023 and list their products by July 2024[2]Source: U.S. FDA, “Modernization of Cosmetics Regulation Act Implementation,” fda.gov. Compliance with these mandates has averaged costs of USD 150,000 to 300,000 per brand, covering legal reviews, IT system upgrades, and monitoring protocols for adverse events. In the EU, regulations stipulate that every formulation undergoes safety assessments by qualified toxicologists. This assessment, costing EUR 5,000 to 15,000 per SKU, can delay product launches by 3 to 6 months, as noted by the European Commission. In China, the NMPA registration process for imported cosmetics offers animal testing exemptions solely to brands with local R&D facilities. This stipulation forces Western companies into a dilemma, balancing ethical commitments against market access. Smaller brands are feeling the pinch: dedicating 15 to 20% of their revenue to compliance leaves them with scant capital for marketing. This dynamic creates a regulatory moat, fortifying the position of established players. The EU's 2024 prohibition on 26 fragrance allergens, such as linalool and limonene, found in 70% of luxury perfumes, demands reformulations that could alter signature scents. If these changes are noticeable, they risk provoking a consumer backlash.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Cosmetics Lead, Eye Segment Accelerates

In 2025, facial cosmetics accounted for 41.89% of the premium cosmetics market, driven by the demand for anti-aging serums and foundations. These products increasingly feature retinol alternatives, such as bakuchiol, and peptide complexes like Matrixyl. These ingredients boost collagen synthesis, offering benefits without the irritation often linked to traditional retinoids. Meanwhile, eye cosmetics are expected to grow at an annual rate of 6.58% through 2031. This growth is supported by advancements like tubing mascara technologies. These technologies create water-resistant polymers around individual lashes, preventing smudging and eliminating the need for oil-based removers, which can sometimes cause periorbital dermatitis. In the lip and nail cosmetics segment, there is a significant focus on long-wear formulations. For example, modern liquid lipsticks now use film-forming polymers to ensure color lasts 12-16 hours. They also include encapsulated hyaluronic acid spheres for added hydration. Additionally, K-beauty's "glass skin" trend, which emphasizes a translucent, dewy complexion, has influenced Western brands to reformulate their foundations. These now incorporate light-diffusing pigments and fermented ingredients, such as galactomyces, known for improving skin texture with consistent use.

The beauty industry is witnessing a shift toward multi-functional products. BB creams and cushion compacts, which combine foundation, sunscreen, and skincare actives, are increasingly replacing traditional facial cosmetics in the Asia-Pacific region. This trend is prompting brands to reevaluate their product strategies. A notable example is Shiseido's Synchro Skin line. By integrating SPF 30 and hyaluronic acid into its foundation, the line has eliminated the need for separate primer and moisturizer steps. This innovation resulted in an 18% year-over-year growth in 2024. However, the eye cosmetics segment faces distinct challenges. The rising popularity of lash-extension services and semi-permanent tints is leading affluent consumers to reduce their daily mascara usage. In response, brands are focusing on developing lash-conditioning serums enriched with peptides, which promise visible growth in 8-12 weeks. Meanwhile, the lip product market is evolving. On one side, there is growing demand for ultra-matte liquid lipsticks designed for all-day wear. On the other side, glossy balms infused with plant oils are gaining popularity, reflecting a divide in consumer preferences between longevity and comfort.

By Category: Organic Dominance Masks Efficacy Trade-Offs

In 2025, natural and organic cosmetics accounted for 57.52% of the premium market, with a projected growth rate of 6.42% through 2031. This growth is primarily driven by consumers' belief that plant-based ingredients are safer than synthetic ones, a perception that persists despite dermatological studies showing similar sensitization rates. The COSMOS certification, which requires 95% of agricultural inputs to be organically sourced and bans over 2,500 synthetic ingredients, has become a critical standard. Brands targeting clean-beauty sections at retailers like Whole Foods and Sephora now consider this certification indispensable. Brands like La Mer justify their USD 350 (for a 30ml) price point for synthetic-heavy creams by emphasizing proprietary fermentation processes and clinical trial results, a strategy that helps them remain competitive against clean-beauty offerings.

The tension between these categories is most evident in active ingredients. For example, synthetic peptides like Argireline (acetyl hexapeptide-8) have demonstrated measurable wrinkle-reduction benefits in double-blind studies but are excluded from COSMOS-certified products. This exclusion forces brands to choose between certification and efficacy claims. Ecocert's approval of certain biotech-derived actives, produced through fermentation rather than petrochemical synthesis, offers a potential middle ground. However, consumer understanding of these distinctions remains limited. Certifications like Nordic Swan and USDA Organic add further complexity. A product may achieve COSMOS certification but fail to meet USDA Organic standards if non-agricultural ingredients, such as water or minerals, exceed 5% of its weight. To maximize retail opportunities, brands are increasingly pursuing multiple certifications. However, the associated audit fees ranging from EUR 3,000 to 8,000 annually per certification place a financial strain on smaller companies.

By Distribution Channel: Online Surge Challenges Retail Incumbents

In 2025, multi-brand stores represented 45.11% of the premium cosmetics distribution market by implementing experiential retail formats. These formats allow consumers to try products under professional lighting and receive customized consultations. Online retail is projected to grow at an annual rate of 6.77% through 2031. Direct-to-consumer platforms, such as Charlotte Tilbury's website, are forecast to generate over USD 635 million in 2024 by retaining 40-50% of the wholesale margins typically given up to department stores. Ultra-luxury brands like Chanel and Hermès, which prefer single-brand stores, restrict online availability to maintain exclusivity and discourage price comparisons. Meanwhile, third-party e-retailers, including Sephora's digital platform and Tmall Luxury Pavilion, are narrowing the gap between D2C and wholesale by providing brands with co-marketing opportunities and access to first-party data in return for reduced commission rates.

The rise of D2C is pressuring multi-brand retailers to validate their intermediary role. For instance, Sephora's Beauty Insider program, which generated USD 2.1 billion in additional sales in 2024 through its points-based rewards system, demonstrates how loyalty programs can counter D2C's margin benefits. Ulta Beauty has strategically partnered with Target, introducing mini-stores in over 800 locations. This strategy expands their physical presence without the significant investment required for standalone stores. Other channels, such as duty-free shops, hotel spas, and airline retail, continue to contribute to the market but face challenges. As travel patterns evolve, consumers are increasingly prioritizing convenience over in-transit shopping. The key factor in this shifting landscape is data ownership. D2C brands utilize zero-party data preferences voluntarily shared by consumers—to inform product development. In contrast, multi-brand retailers compile transaction data across competitors, creating network effects that individual brands struggle to replicate. Brands that master omnichannel strategies, such as using online quizzes to encourage in-store visits or leveraging in-store skin scans to initiate personalized email campaigns are well-positioned to capture significant value from both channels.

Geography Analysis

In 2025, Europe accounted for 32.35% of the premium cosmetics market, supported by France's EUR 18 billion beauty industry and Italy's renowned fragrance houses. These Italian producers, known for their traditional distillation techniques, command price premiums that mass-market brands struggle to match. The EU's rigorous Cosmetics Regulation, which requires safety assessments by certified toxicologists and prohibits over 1,300 ingredients, creates a compliance barrier that benefits established companies with in-house regulatory teams, as noted by the European Commission[3]Source: European Commission, “EU Cosmetics Regulation Updates 2024,” ec.europa.eu. In Germany, the preference for dermocosmetics, clinically validated products sold through pharmacies, has led brands like La Roche-Posay and Vichy to focus on ingredient transparency and strict patch-testing protocols. This approach appeals to Northern European consumers, who are often skeptical of exaggerated marketing claims. Meanwhile, the UK's post-Brexit regulatory divergence has introduced challenges; brands must now manage separate REACH chemical registrations for Great Britain and the EU, increasing compliance costs by 15-20% for companies operating in both markets.

Asia-Pacific is projected to grow at an annual rate of 7.57% through 2031. This growth is largely driven by China's Hainan duty-free zone, which generated over CNY 60 billion (USD 8.4 billion) in cosmetics sales in 2024. Domestic consumers took advantage of tax exemptions, purchasing luxury skincare at 30-40% discounts compared to mainland prices. South Korea's beauty industry, where dermatologists collaborate with brands to develop prescription-strength actives for over-the-counter sales, has established Seoul as a leader in trends like "glass skin" and peptide serums. In Japan, the premium cosmetics market, led by Shiseido and KOSÉ, achieved JPY 1.8 trillion (USD 12.1 billion) in sales in 2024. With the nation's median age exceeding 49, the anti-aging segment has seen significant growth. In India, the luxury cosmetics market is expanding at double-digit rates, driven by higher disposable incomes and social media influence. However, distribution challenges, such as inconsistent cold-chain logistics for temperature-sensitive serums, limit growth beyond tier-1 cities. North America's mature market is experiencing modest growth, with the U.S. contributing the majority of regional revenue. The FDA's MoCRA regulations are prompting smaller brands to consolidate or exit the market, inadvertently strengthening the positions of larger players like Estée Lauder and L'Oréal, which have the resources to manage regulatory requirements.

In South America, the premium cosmetics market is undergoing a shift. Brazilian companies like Natura and O Boticário dominate the mass-premium segment by utilizing locally sourced Amazonian ingredients, while European brands capture the ultra-luxury market in cities like São Paulo and Rio de Janeiro. Mexico's proximity to the U.S. facilitates cross-border shopping, which often undercuts local prices. This forces brands to either align their pricing strategies or face the risk of gray-market arbitrage. In the Middle East and Africa, luxury cosmetics growth is concentrated in the UAE and Saudi Arabia. Halal certification, which requires alcohol-free formulations and strict supply-chain audits to prevent cross-contamination, has become a critical requirement for market entry. Sephora Middle East's plan to expand to over 150 stores by the end of 2024 highlights the potential for Western retail formats in the region. However, success depends on adapting to local preferences, such as offering private shopping suites for women and fragrance-free zones for those with sensitivities. Despite Turkey's economic instability, which has reduced demand for premium cosmetics due to currency depreciation, the country remains a key manufacturing hub. European brands are increasingly turning to Turkey for production, attracted by its lower labor costs.

Note: Segment shares of all Individual segments will be available upon report purchase

Competitive Landscape

Power in the sector is moderately consolidated, with multinational giants like Chanel Limited, Estée Lauder Inc., L’Oréal, LVMH Moët Hennessy Louis Vuitton SE, and Shiseido Co., Ltd. dominating the landscape. These key players are expanding their product portfolios by introducing innovative textures, eco-friendly formulations, and diverse shade ranges to attract a broad consumer base. The market remains highly dynamic, as brands capitalize on trend-driven launches amplified by social media influencers and celebrity endorsements to enhance their market presence and build consumer loyalty. Premiumization strategies, including luxury packaging and exclusive collaborations, enable these brands to maintain a high-end image and justify premium pricing.

While established players benefit from global distribution networks and significant R&D investments, the rise of innovative direct-to-consumer brands is intensifying competition. Brands like Fenty Beauty have gained prominence by emphasizing diversity and authenticity, while others focus on cruelty-free, vegan, or natural products to meet evolving consumer preferences. Digital platforms, particularly social commerce and virtual try-on technologies, have become critical for customer acquisition, allowing smaller brands to compete effectively with legacy players.

Sustainability, ingredient transparency, and technological advancements are key drivers of differentiation in the premium segment. Consumers, especially Millennials and Gen Z, are increasingly seeking products that combine luxury with ethical values and visible performance. This shift has prompted brands to adopt refillable packaging, strengthen ESG initiatives, and integrate technologies such as AI-driven personalization tools and advanced beauty devices. To stay competitive and capture growth in both mature and emerging markets, companies are increasingly pursuing strategic acquisitions, collaborations, and capacity expansions.

Premium Cosmetics Industry Leaders

Chanel Limited

L’Oréal

LVMH Moët Hennessy Louis Vuitton SE

Shiseido Co.,Ltd.

The Estee Lauder Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Estée Lauder announced its official launch in the Amazon.ca Premium Beauty store. This launch enabled broader access to Estée Lauder's high-performance skin care, best-in-class makeup and iconic fragrances to customers across Canada with the ease and convenience of Amazon.

- May 2025: Dior Beauty opened a new boutique at Brickell City Centre in Miami, which featured the brand's fragrance, makeup, and skin care offerings. It was the latest brick-and-mortar expansion for the LVMH Moët Hennessy Louis Vuitton-owned brand.

- March 2025: Charlotte Tilbury - the award-winning global luxury makeup, skincare and fragrance brand founded by British entrepreneur and makeup artist to the stars, Charlotte Tilbury MBE - launched at United States luxury beauty retailer Bluemercury, in key stores nationwide and on its website.

- January 2025: Nars became the latest prestige brand to launch on Indian e-commerce platform, Nykaa. The brand was made available online and in store, with a range of its popular products, including Orgasm Blush, Natural Radiant Longwear Foundation and Radiant Creamy Concealer.

Global Premium Cosmetics Market Report Scope

| Facial Cosmetics |

| Eye Cosmetics |

| Lip and Nail Make-Up Cosmetics |

| Natural / Organic |

| Conventional / Synthetic |

| Single Brand Stores | |

| Multi-Brand Stores | |

| Online Retail Stores | D2C (Direct-to-Consumer) |

| Third-party E-retailers | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Facial Cosmetics | |

| Eye Cosmetics | ||

| Lip and Nail Make-Up Cosmetics | ||

| By Category | Natural / Organic | |

| Conventional / Synthetic | ||

| By Distribution Channel | Single Brand Stores | |

| Multi-Brand Stores | ||

| Online Retail Stores | D2C (Direct-to-Consumer) | |

| Third-party E-retailers | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the premium cosmetics market by 2031?

The premium cosmetics market is projected to reach USD 48.62 billion by 2031.

Which region will grow fastest in premium beauty through 2031?

Asia-Pacific is set to post the highest CAGR at 7.57%, led by China’s duty-free channel and Korea’s R&D ecosystem.

Which product segment currently leads sales?

Facial cosmetics lead with 41.89% of 2025 revenue thanks to anti-aging serums and foundation innovations.

How big is the organic share within premium cosmetics?

Organic and natural SKUs captured 57.52% of 2025 revenue and continue to outpace conventional products.

Page last updated on: