Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.93 Billion |

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 2.53 Billion |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Cosmetic Products Market Analysis by Mordor Intelligence

The Canada cosmetic products market size was valued at USD 1.93 billion in 2025 and estimated to grow from USD 2.02 billion in 2026 to reach USD 2.53 billion by 2031, at a CAGR of 4.59% during the forecast period (2026-2031). Canada's aging cohort, 19.5% of the population aged 65 or older in 2025, is projected to hit 32% by 2030, driving sustained demand for anti-aging solutions, yet the same consumers increasingly scrutinize ingredient lists and demand transparency. Meanwhile, immigration patterns that will push the foreign-born share to roughly one-third of the population by 2030 are forcing brands to rethink shade ranges, formulation pH levels, and marketing narratives to serve South Asian, East Asian, Middle Eastern, and African diaspora communities. High-income seniors are accelerating demand for peptide-rich anti-aging creams, while Gen Z and millennial shoppers reward brands that prove clinical efficacy through AI-enabled R&D pipelines. Premiumization is widening profits as households trade up for high-impact “hero” serums yet retain mass mascara habits when budgets tighten. Specialty retailers still anchor discovery, but the pandemic-era shift to virtual try-on is raising online penetration every quarter. Finally, ingredient transparency is a durable driver, nudging formulators toward natural preservatives that extend shelf life without compromising microbial safety.

Key Report Takeaways

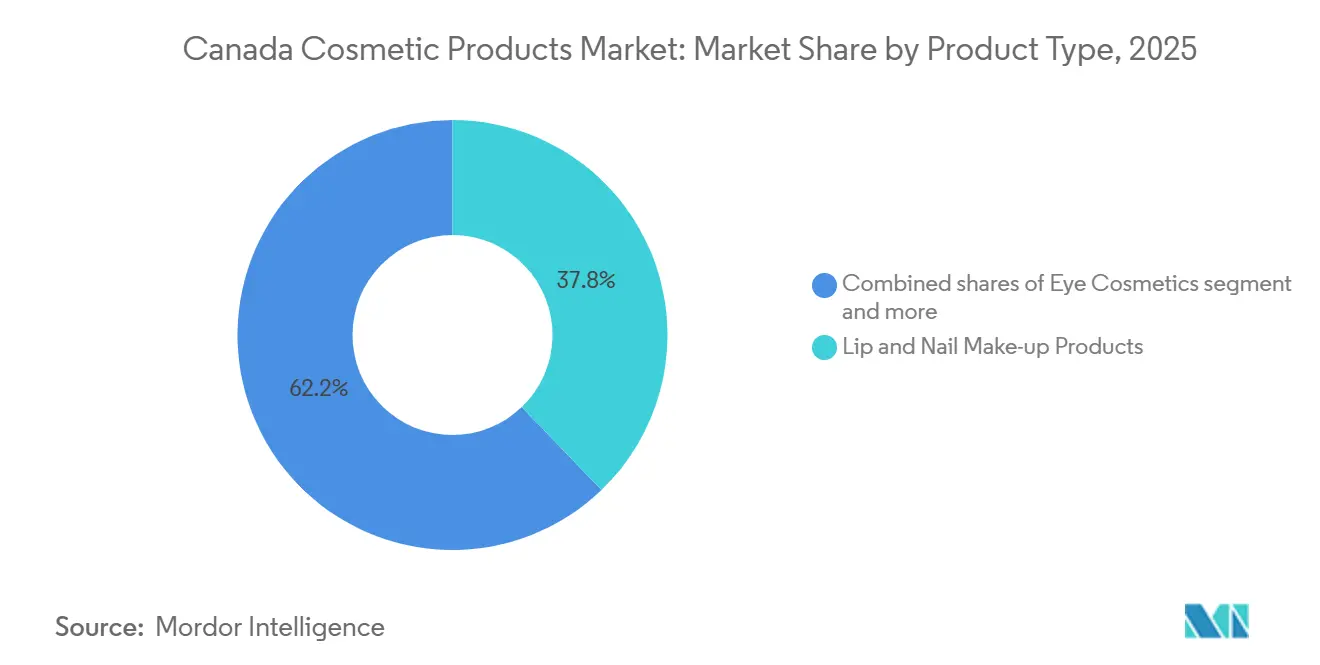

- By product type, lip and nail make-up products captured 37.81% of Canada cosmetics product market share in 2025, while eye cosmetics are expanding at a 5.32% CAGR through 2031.

- By category, conventional/synthetic lines held 68.73% of the Canada cosmetics product market size in 2025, but natural/organic products are advancing at a 6.16% CAGR to 2031.

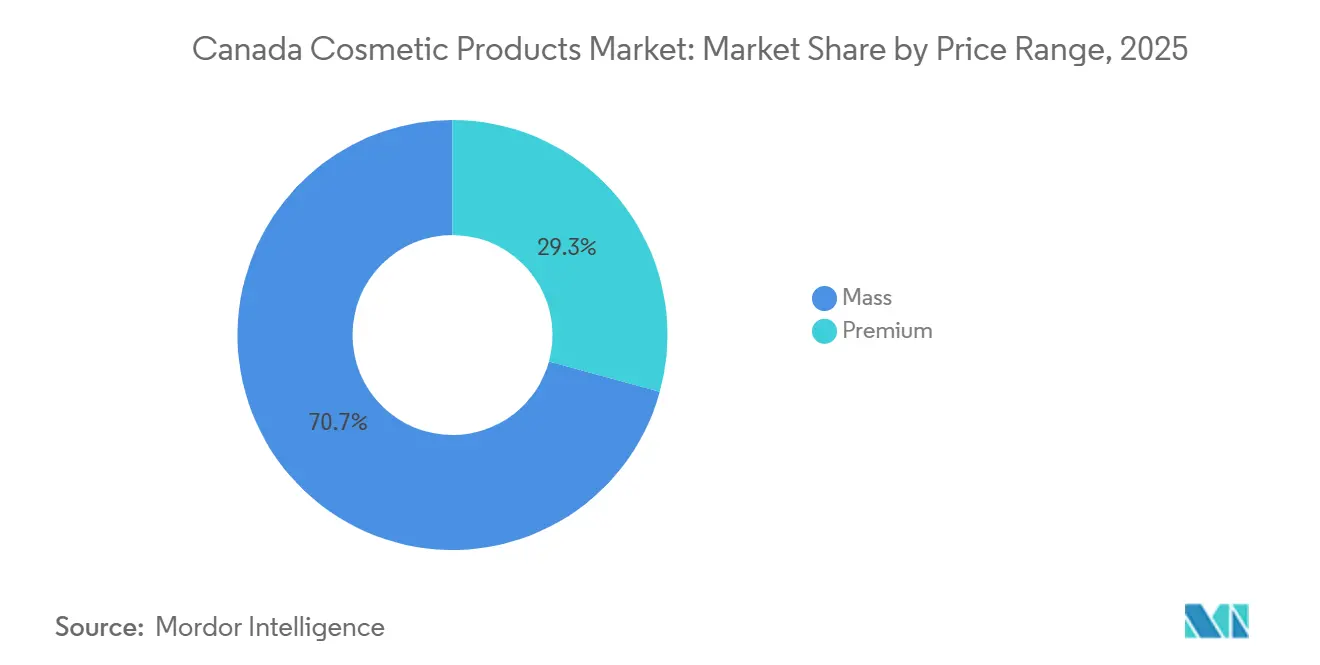

- By price range, mass offerings commanded 70.74% of the Canada cosmetics product market size in 2025, whereas the premium tier is projected to grow at a 6.07% CAGR during 2026-2031.

- By distribution channel, specialty stores led with 46.77% revenue share in 2025, yet online retail is forecast to post a 5.84% CAGR through 2031, the fastest of all channels.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Cosmetic Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer focus on anti-aging solutions | +1.2% | National, with concentration in urban centers | Medium term (2-4 years) |

| Technological advancements in product formulations | +0.9% | National, with Research and Development centers in Toronto and Montreal | Long term (≥ 4 years) |

| Expansion of premium beauty segment | +1.1% | National, with higher penetration in metropolitan areas | Medium term (2-4 years) |

| Multicultural consumer base driving product diversity | +0.8% | National, with emphasis on Toronto, Vancouver, Montreal | Long term (≥ 4 years) |

| Sustainable beauty product trends | +0.7% | National, with stronger adoption in British Columbia and Ontario | Medium term (2-4 years) |

| International and local brand developments | +0.6% | National, with focus on major retail markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Focus on Anti-aging Solutions

Canada had approximately 4.07 million women aged 65 and over in 2023, according to Statistics Canada, representing a key demographic segment driving the anti-aging market[1]Source: Statistics Canada, "Population estimates on July 1, by age and gender", 150.statcan.gc.ca. This aging female population has generated increased market demand for anti-aging makeup and skincare products. The anti-aging segment is responding with formulations that blend retinoids, peptides, and bakuchiol, a plant-derived retinol alternative that avoids the photosensitivity and irritation associated with traditional vitamin A derivatives. Lancôme's Rénergie H.P.N. 300-Peptide Cream, launched in March 2024, exemplifies this trend by delivering a tri-peptide complex that targets collagen synthesis at the dermal-epidermal junction. The median age of 40.6 years means that a substantial share of the market is entering the "preventative aging" phase, where consumers in their late 30s and early 40s adopt anti-aging routines before visible signs appear. This preventative mindset is expanding the addressable market beyond the traditional 50-plus demographic and pulling forward purchase timelines. Brands that fail to communicate efficacy through clinical trials or third-party testing risk losing credibility in a category where consumers are increasingly literate about active ingredients and their mechanisms of action.

Technological Advancements in Product Formulations

Formulation science is undergoing a step-change driven by artificial intelligence, bioprinting, and green chemistry. L'Oréal's investment of USD 140 million to USD 160 million in its New Jersey Research and Innovation center, operational since 2024, houses 550-plus scientists and features a bioprinted skin platform that replicates human dermal responses without animal testing. The company files approximately 700 patents annually, many of which focus on stabilizing volatile actives, such as ascorbic acid and niacinamide, in anhydrous or low-water formulations that extend shelf life and maintain potency. Shiseido's VOYAGER AI platform, launched in September 2024, ingests over 500,000 R&D data points to predict formulation stability, sensory profiles, and consumer acceptance scores before a single batch is mixed. These advancements are not incremental; they represent a shift from empirical formulation to data-driven design, compressing development cycles from 18 months to under 12 and enabling brands to respond faster to emerging trends.

Expansion of Premium Beauty Segment

Premium beauty products, defined as those retailing above CAD 50 per unit, are capturing share despite broader economic headwinds. The premium segment is forecast to grow at a 6.07% CAGR through 2031, outpacing the mass segment's implied growth rate. This divergence reflects a "lipstick effect" variant: consumers constrain discretionary spending on apparel and dining but maintain or increase outlays on small luxuries that deliver visible self-care benefits. Coty's November 2024 acquisition of a stake in Orveon, the parent of Bare Minerals, Laura Mercier, and Buxom, signals a strategic bet that clean, prestige positioning can command premiums even as input costs rise. The premium segment also benefits from higher gross margins, which allow brands to absorb tariff increases and freight volatility without passing full costs to consumers. The risk is that prolonged inflation or a recession could trigger trading down, but current data suggest that premium buyers are sticky, particularly when products deliver measurable results or align with personal values like sustainability or cruelty-free sourcing.

Multicultural Consumer Base Driving Product Diversity

Canada's multicultural population growth influences product diversity in the cosmetics market, as companies adapt to meet the beauty requirements of diverse consumers. According to the International Monetary Fund (IMF), as of 2025, Canada's population reached 41.53 million residents, with ethnic diversity at its highest level[2]Source: Statistics Canada, “Canada's population estimates, fourth quarter 2024”, 150.statcan.gc.ca. Canadian consumers represent various skin tones and cultural beauty traditions, prompting companies to expand their product lines with inclusive shade ranges and specialized skincare solutions. The demand for foundations, concealers, and powders matching diverse skin tones has led international and local brands to broaden their product ranges. Marketing campaigns now feature diverse models and influencers to reflect Canadian demographics. The market has expanded to include gender-neutral beauty products, serving a broader consumer base. Multicultural consumers also drive demand for products with specific certifications, including halal, vegan, and cruelty-free options, as well as products incorporating ingredients from traditional beauty practices worldwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer concerns about chemical ingredients | -0.8% | National, with higher impact in health-conscious regions | Short term (≤ 2 years) |

| Limited shelf life of natural products | -0.5% | National, affecting natural/organic segment growth | Medium term (2-4 years) |

| Supply chain challenges affecting operations | -0.7% | National, with greater impact on import-dependent brands | Short term (≤ 2 years) |

| Strong competition from established international brands | -1.2% | National, with intensified competition in premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Concerns About Chemical Ingredients

The Canadian cosmetics market experiences significant growth constraints due to heightened consumer scrutiny of product formulations and comprehensive regulatory requirements. Health Canada's enhanced regulatory framework for cosmetic ingredient disclosure imposes substantial operational complexities and financial implications for manufacturers. For instance, companies must invest in reformulating products and updating packaging to comply with new standards. In 2024, Health Canada implemented comprehensive modifications to the Cosmetic Regulations under the Food and Drugs Act, establishing more rigorous protocols for consumer protection, market transparency, and manufacturer accountability. The regulations mandate detailed allergen documentation requirements. Effective April 12, 2026, all cosmetic products must present comprehensive ingredient declarations, incorporating 24 specific EU-designated fragrance allergens[3]Source: Statistics Canada, "Cosmetic advertising, labelling and ingredients", canada.ca. This regulatory harmonization with European Union standards demonstrates Canada's commitment to protecting consumers with documented allergic sensitivities to specific cosmetic components.

Supply Chain Challenges Affecting Operations

Raw material shortages and logistics disruptions continue to constrain the Canada cosmetics product market, even as pandemic-era bottlenecks ease. Natural emollients, such as shea butter, argan oil, and jojoba oil, face supply volatility due to climate-driven crop failures in West Africa and the Mediterranean, regions that supply the majority of global volumes. Lead times for specialty ingredients like peptides or encapsulated retinoids have stretched from 8 weeks to 16 weeks, forcing brands to carry higher safety stock and accept lower inventory turns. Freight costs, while off their 2021-2022 peaks, remain elevated due to geopolitical tensions and capacity constraints on trans-Pacific routes. Brands sourcing from Asia-Pacific, particularly South Korea and Japan, which dominate innovation in cushion compacts and sheet-mask-inspired formulations, face tariff uncertainty and port congestion. The shift toward natural and organic ingredients exacerbates these challenges; plant-based actives often require cold-chain logistics and have shorter shelf lives than synthetic alternatives, increasing the risk of spoilage in transit. Sephora's January 2025 opening of a Canadian distribution center in Mississauga, Ontario, is a strategic response to these pressures, enabling the retailer to consolidate inbound shipments, reduce cross-border customs delays, and improve last-mile delivery speed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Eye Cosmetics Lead Innovation Race

Eye cosmetics are the fastest-growing segment at 5.32% CAGR through 2031, a trajectory fueled by mascara formulations that embed lash-conditioning peptides and eyeliner innovations that deliver 16-hour wear without smudging or flaking. Yves Saint Laurent's Lash Clash mascara, launched in 2024, uses a tubing polymer that wraps individual lashes and resists humidity, a technical feat that required 18 months of stability testing to ensure the formula did not dry out in the package. The category benefits from frequent repurchase cycles; consumers replace mascara every 3 to 4 months due to hygiene concerns, and low unit prices reduce purchase hesitation. Liquid eyeliners with felt-tip applicators, popularized by Korean beauty brands, are gaining share in Canada as consumers seek precision and ease of application. Facial cosmetics, encompassing foundations, concealers, and blushes, remains the largest segment by volume but faces headwinds from the "no-makeup makeup" trend, where consumers favor lightweight tints and BB creams over full-coverage foundations.

Lip and nail make-up products command a 37.81% share in 2025, a dominance rooted in versatility and impulse-purchase dynamics. Lip products, lipsticks, glosses, and stains are replenished frequently, often as discretionary purchases that provide immediate gratification. Nail lacquers benefit from seasonal color trends and the rise of at-home manicure kits during the pandemic, a behavior that has proven sticky even as salons reopened. Long-wear lip formulations, which use silicone elastomers to create a flexible film that resists transfer, are capturing share from traditional bullet lipsticks, particularly among younger consumers who prioritize convenience over reapplication rituals.

By Category: Natural/Organic Gains Despite Shelf-Life Trade-Offs

Conventional/synthetic products hold 68.73% share in 2025, a reflection of their cost efficiency, longer shelf life, and established supply chains. Synthetic preservatives like phenoxyethanol and benzyl alcohol extend microbial stability to 2 to 3 years, enabling brands to manage inventory without write-offs and to distribute through channels with slower turnover, such as rural pharmacies or discount retailers. Synthetic pigments offer color consistency and intensity that plant-based alternatives struggle to match, particularly in high-impact categories like eye shadow and liquid lipstick. However, the natural/organic segment is growing at a 6.16% CAGR through 2031, driven by consumers, particularly millennials and Gen Z, who prioritize ingredient transparency and environmental impact over price or convenience.

Symrise's Mindera platform, also introduced in March 2025, uses fermentation to produce plant-based actives with batch-to-batch consistency, solving a longstanding challenge where natural ingredients exhibit variability in potency and sensory attributes. Elate Cosmetics, a Canadian indie brand, has built its positioning around refillable bamboo compacts and formulations free of synthetic fragrances, parabens, and talc, resonating with environmentally conscious buyers in British Columbia and Ontario. The economic headwind is clear: natural ingredients often cost 2 to 3 times more than synthetic equivalents, and shorter shelf lives increase the risk of spoilage before sale. Brands that cannot pass these costs to consumers, or that lack the scale to absorb them, face margin compression. The regulatory environment is also tightening; Health Canada's Cosmetic Ingredient Hotlist bans or restricts over 600 substances, pushing brands toward cleaner formulations even when consumer demand is ambiguous.

By Price Range: Premium Outpaces Mass Despite Economic Headwinds

Mass products command 70.74% share in 2025, a function of their accessibility, wide distribution through drugstores and supermarkets, and price points, typically under CAD 20, that align with the budgets of younger consumers and those in lower-income brackets. Brands like Revlon, which exited Chapter 11 bankruptcy in 2024, compete on value and ubiquity, stocking thousands of retail doors and leveraging promotional pricing to drive volume. The mass segment is also the entry point for new category users, particularly teenagers experimenting with makeup for the first time. However, the premium segment is growing at 6.07% CAGR through 2031, a divergence that reflects a "lipstick effect" variant: consumers constrain discretionary spending on apparel and dining but maintain or increase outlays on small luxuries that deliver visible self-care benefits. Estée Lauder's acquisition of Tom Ford Beauty, finalized in the 2023-2024 transition period, brought a portfolio of ultra-premium fragrances and color cosmetics that command CAD 80 to CAD 150 price points and appeal to affluent consumers in Vancouver, Toronto, and Calgary.

Coty's November 2024 acquisition of a stake in Orveon, the parent of Bare Minerals, Laura Mercier, and Buxom, signals a strategic bet that clean, prestige positioning can command premiums even as input costs rise. Premium products benefit from higher gross margins, which allow brands to absorb tariff increases and freight volatility without passing full costs to consumers. The risk is that prolonged inflation or a recession could trigger trading down, but current data suggest that premium buyers are sticky, particularly when products deliver measurable results or align with personal values like sustainability or cruelty-free sourcing. Brands that straddle both segments, such as L'Oréal, which operates mass brands like Maybelline alongside prestige labels like Lancôme, can hedge against economic volatility and capture share across income tiers.

By Distribution Channel: Online Retail Gains as Specialty Stores Adapt

Specialty stores retain 46.77% share in 2025, a dominance rooted in experiential retail, the ability to test textures, compare shades under controlled lighting, and receive personalized consultations from trained staff. Sephora's 360-plus stores across Canada offer services like Color IQ skin-tone matching and Skincare IQ diagnostics, creating a differentiated experience that pure-play e-commerce cannot replicate. Shoppers Drug Mart, with over 1,300 locations, serves as the primary distribution channel for mass and mid-tier brands, leveraging its pharmacy footprint to capture impulse purchases and prescription-linked shopping trips. However, online retail is expanding at a 5.84% CAGR through 2031, driven by convenience, wider assortments, and virtual try-on technologies that reduce purchase hesitation. Sephora's January 2025 opening of a dedicated Canadian distribution center in Mississauga, Ontario, was designed to cut last-mile delivery times to under 48 hours for 90% of the population and to support same-day delivery pilots in Toronto and Vancouver.

Estée Lauder's partnership with Shopify, set to launch in Q1 2026, will integrate augmented reality try-on tools directly into brand websites, enabling consumers to visualize lipstick shades or foundation matches using their smartphone cameras. L'Oréal's ModiFace AI platform, operational since 2024, powers virtual try-on experiences for over 30 brands, processing 10 million sessions per month and converting at rates 20% higher than static product pages. The shift to online is not uniform; prestige brands with complex shade ranges or texture-dependent products, such as foundations or cream blushes, still see higher conversion rates in physical stores where consumers can test before buying. Supermarkets/hypermarkets and other distribution channels, which include independent beauty boutiques and direct-to-consumer models, account for the remaining share. Cheekbone Beauty, a Canadian indie brand founded by an Indigenous entrepreneur, bypasses traditional retail entirely, selling through its own website and pop-up events that emphasize community engagement and cultural storytelling. This direct model captures higher margins and builds brand loyalty, but it sacrifices the scale and discoverability that mass retail provides.

Geography Analysis

The Canada cosmetics product market exhibits regional variations driven by demographic composition, income levels, and cultural preferences, though the absence of explicit geographic segmentation in the table of contents suggests a nationally integrated market with localized nuances. Toronto's role as a retail hub, with flagship stores for Sephora, Holt Renfrew, and Shoppers Drug Mart, creates a testing ground for new launches and limited-edition collections that later roll out nationally. British Columbia, particularly Metro Vancouver, exhibits the highest per-capita spending on natural and organic cosmetics, a reflection of the province's environmental consciousness and younger demographic skew. Elate Cosmetics, headquartered in British Columbia, leverages this regional preference by offering refillable bamboo compacts and formulations free of synthetic fragrances, parabens, and talc.

Quebec presents a distinct dynamic due to language and cultural factors; bilingual labeling is mandatory under Health Canada regulations, and brands that fail to localize marketing, both linguistically and tonally, struggle to gain traction. The province's francophone majority exhibits loyalty to European beauty brands, particularly French labels like L'Oréal Paris and Lancôme, which benefit from cultural affinity and heritage positioning. Montreal serves as a secondary retail hub, with a concentration of prestige boutiques and indie brands that cater to fashion-forward consumers. The Prairie provinces, Alberta, Saskatchewan, Manitoba, and Atlantic Canada account for smaller shares but exhibit faster growth in e-commerce adoption, driven by limited brick-and-mortar options and the convenience of home delivery.

Cross-border shopping dynamics also shape the market; proximity to the United States enables consumers in border cities, Windsor, Niagara Falls, and Surrey, to access U.S. retailers and brands not yet available in Canada, creating competitive pressure on domestic players to match assortments and pricing. The rise of online retail has partially mitigated this leakage by expanding access to international brands through Canadian e-commerce platforms, but tariffs and shipping costs still favor in-person cross-border purchases for high-value items. These regional subtleties require brands to tailor assortments and promotional strategies, a complexity that favors national players with the scale to manage SKU proliferation over smaller indie brands with limited distribution.

Competitive Landscape

The Canadian cosmetics market exhibits a sophisticated competitive landscape characterized by established international corporations and domestic companies. International firms, notably L'Oréal S.A., Shiseido Company, Limited, and The Estée Lauder Companies Inc., maintain market dominance through substantial research and development capabilities while systematically adapting their marketing strategies to address Canadian consumer preferences. Domestic companies, with Groupe Marcelle as a prominent player, maintain their competitive position through comprehensive regional market understanding and streamlined operational structures.

The market dynamics have necessitated that both international and domestic organizations implement quarterly product introduction cycles, replacing traditional annual launch schedules. This operational modification has required financial departments to establish enhanced working capital management protocols and implement precise cash flow forecasting methodologies. The strategic convergence of premium and mass market segments into "masstige" has fundamentally altered competitive parameters, requiring companies to adapt their operational strategies.

Mass market organizations expanding into premium segments have implemented enhanced service protocols, particularly professional beauty consultation services previously exclusive to premium retail establishments. This strategic transformation has necessitated a shift in workforce deployment from transaction-oriented to consultation-based operational models, resulting in increased labor cost metrics. Companies are optimizing operational costs through the strategic implementation of digital assistance systems, contingent upon the successful integration of artificial intelligence platforms with existing sales infrastructure.

Canada Cosmetic Products Industry Leaders

-

L'Oréal S.A.

-

Coty Inc.

-

Shiseido Company, Limited

-

Chanel Limited

-

Revlon, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The Canadian Government announced the elimination of PFAS (per- and polyfluoroalkyl substances) from consumer products, including cosmetics, starting in 2027. The regulation mandated cosmetics manufacturers to reformulate their products to comply with the new standards.

- March 2025: Prada Beauty established its cosmetics line in Canada, implementing a technology-focused product range that integrated functionality with design innovation. The collection incorporated skincare, complexion, eye, and lip products, providing consumers essential beauty items with a distinct approach.

- October 2024: Cosmetica Laboratories Inc. signed a manufacturing agreement with makeup artist Katie Jane Hughes to produce a dual-purpose lip and cheek cosmetic stick for KJH.Brand. The product will launch in five color variants and marks the second product release in the KJH.Brand portfolio.

- May 2024: Lawless Beauty expanded its presence in Sephora by 2.5 times through expansion into Sephora at Kohl's locations and entry into the Canadian market. The company introduced six shades of Pinch My Cheeks Soft-Blur Cream Blush. The product combined powder formulation with cream-like application properties, providing a soft-diffused, blurred appearance that set automatically.

Canada Cosmetic Products Market Report Scope

The makeup products market encompasses cosmetic formulations designed to enhance or modify facial and body appearance. The product portfolio includes foundation, lipstick, eyeshadow, mascara, and blush, which function to accentuate features and deliver specific aesthetic outcomes. The market serves both daily consumer requirements and occasion-specific applications.

The Canadian cosmetic products market is segmented based on product type, category, ingredient type, and distribution channel. Based on product type, the market is segmented into face cosmetics, eye cosmetics, lip & nail make-up products. Based on category, the market is segmented into premium products and mass products. Based on ingredient type, the market is segmented into natural & organic and conventional/synthetic. Based on distribution channels, the market is segmented into specialty stores, supermarkets/hypermarkets, online retail, and other distribution channels. The market sizing has been done in value terms in USD for all the abovementioned segments.

Product Type

| Facial Cosmetics |

| Eye Cosmetics |

| Lip and Nail Make-up Products |

Category

| Natural/Organic |

| Conventional/Synthetic |

Price Range

| Mass |

| Premium |

Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail |

| Other Distribution Channels |

| Product Type | Facial Cosmetics |

| Eye Cosmetics | |

| Lip and Nail Make-up Products | |

| Category | Natural/Organic |

| Conventional/Synthetic | |

| Price Range | Mass |

| Premium | |

| Distribution Channel | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the current value of the Canada cosmetics product market?

The Canada cosmetics product market size stands at USD 2.02 billion in 2026.

How fast is the premium segment growing?

Premium beauty items are forecast to expand at a 6.07% CAGR from 2026 to 2031.

Which product type shows the quickest growth trajectory?

Eye Cosmetics lead with a projected 5.32% CAGR through 2031.

How important are natural and organic formulations in Canada?

Natural/Organic products, though 31.27% of value in 2025, are growing at 6.16% CAGR as consumers demand clean labels.

Page last updated on: