Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

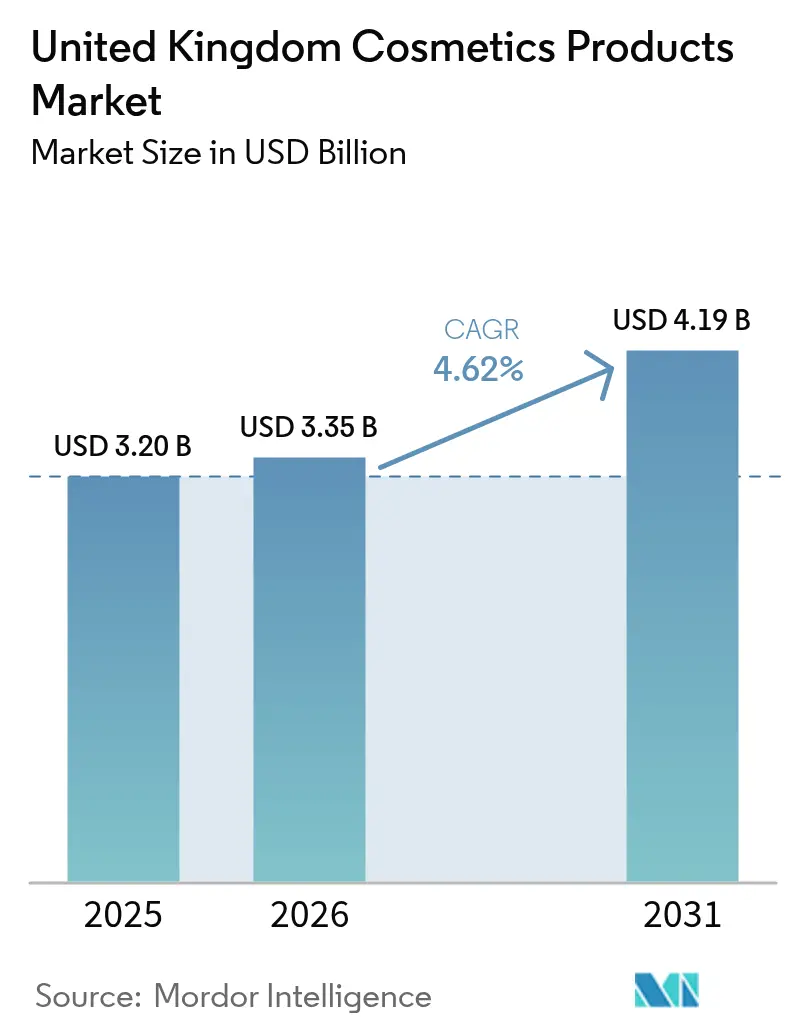

| Base Year Market Size (2025) | USD 3.20 Billion |

| Market Size (2026) | USD 3.35 Billion |

| Market Size (2031) | USD 4.19 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

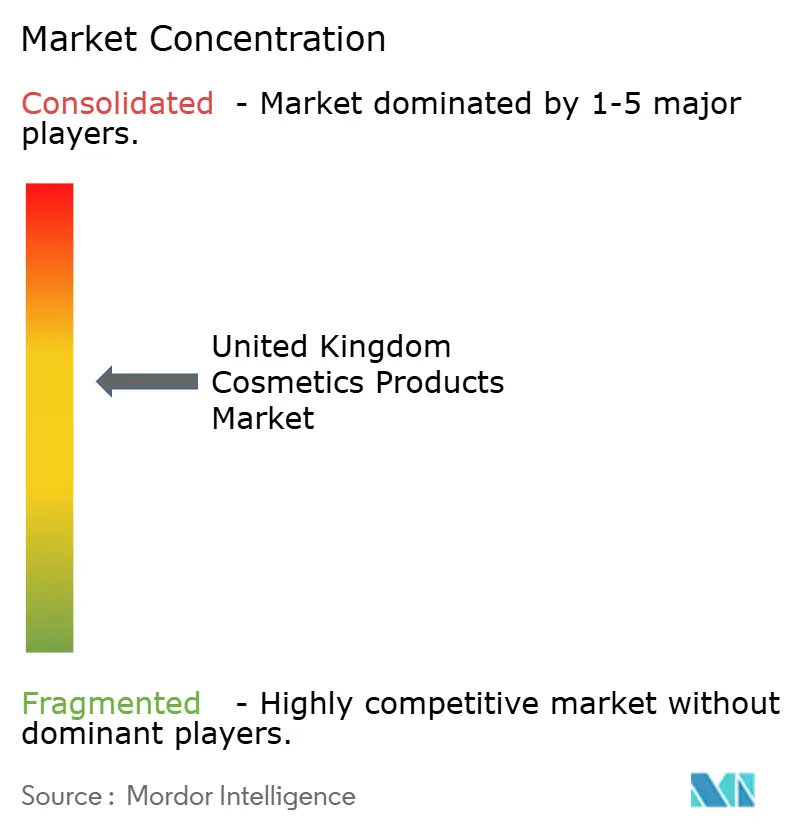

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Cosmetics Products Market Analysis by Mordor Intelligence

The United Kingdom Cosmetics Products Market size market size in 2026 is estimated at USD 3.35 billion, growing from 2025 value of USD 3.20 billion with 2031 projections showing USD 4.19 billion, growing at 4.62% CAGR over 2026-2031. This growth is largely driven by rising demand for high-quality, premium cosmetics, advancements in technology that allow for personalized beauty solutions, and the introduction of more inclusive shade ranges to meet the needs of diverse consumers. The market is also evolving in response to changing consumer lifestyles. In terms of product types, facial cosmetics are expected to see the highest growth, while eye makeup products are also gaining popularity. In terms of categories, premium cosmetics are expanding rapidly, while mass-market cosmetics continue to maintain steady demand. Organic and natural products are growing quickly as more consumers prioritize sustainability and health-conscious choices, though conventional products still dominate the market due to their affordability and widespread availability. In terms of distribution channels, online retail is growing at a fast pace; however, specialty beauty stores remain an important channel, as they offer expert advice and curated product selections that many consumers value. The market is moderately concentrated, with the top five suppliers accounting for a significant share of the revenue.

Key Report Takeaways

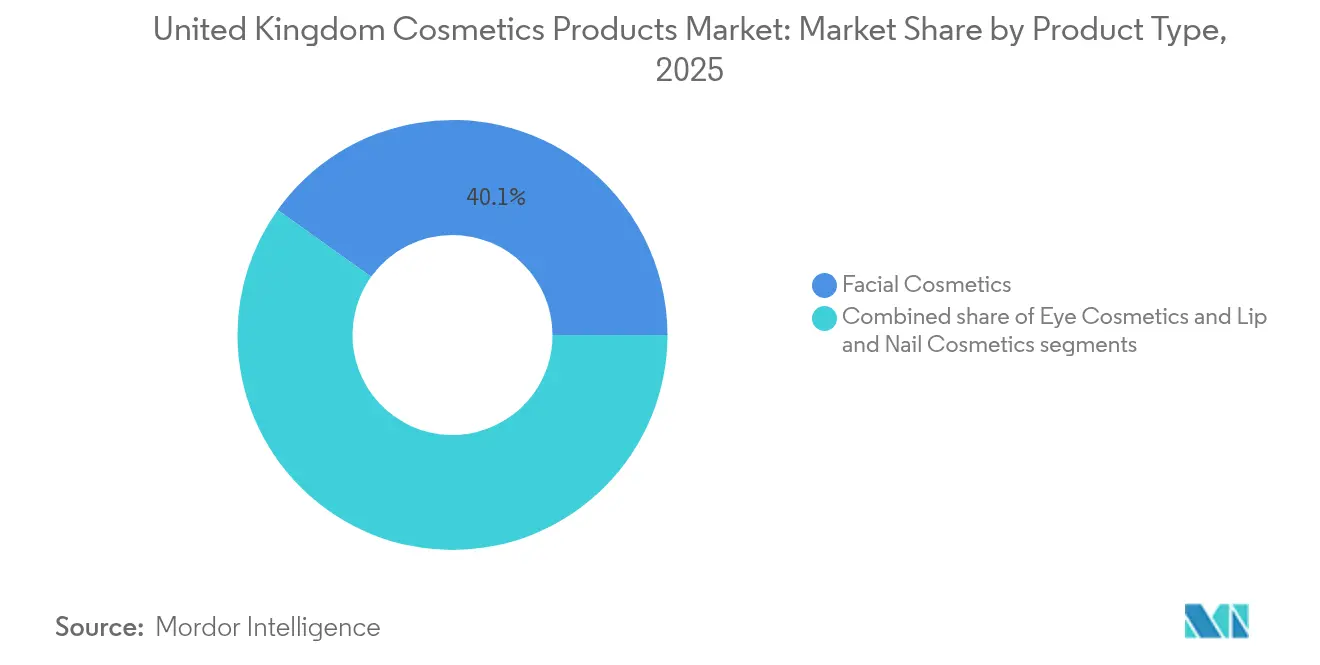

- By product type, facial cosmetics led with 40.12% of the United Kingdom cosmetics products market share in 2025, while lip and nail cosmetics are advancing at a 5.55% CAGR through 2031.

- By category, the mass segment held 64.20% revenue in 2025; the premium tier is forecast to climb at a 6.66% CAGR to 2031.

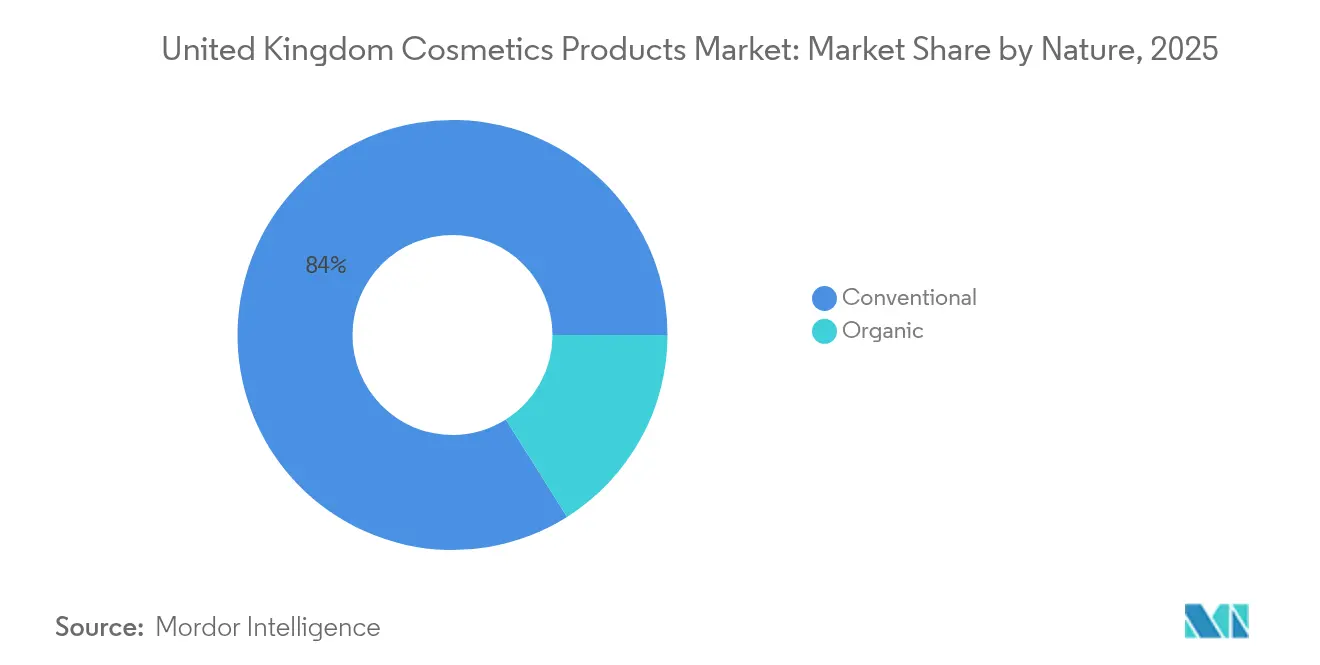

- By nature, conventional items accounted for 83.95% of the United Kingdom's cosmetics products market size in 2025, whereas organic lines are expanding at a 6.88% CAGR over the outlook.

- By distribution channel, specialty beauty stores captured a 37.40% share in 2025, and online retail is projected to grow at a 6.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Cosmetics Products Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing consumer inclination toward natural and organic products | +1.2% | United Kingdom-wide, stronger in urban areas | Medium term (2-4 years) |

| Rising male grooming and unisex trends | +0.8% | National, with concentration in metropolitan areas | Long term (≥ 4 years) |

| Advancements in technology driving product innovation | +1.5% | United Kingdom-wide, led by major retailers and brands | Short term (≤ 2 years) |

| Social media influence to boost the market | +1.0% | National, strongest among Gen Z demographics | Short term (≤ 2 years) |

| Convenience and multi-functional products preference | +0.7% | United Kingdom-wide, particularly in urban centers | Medium term (2-4 years) |

| Inclusive shade ranges driven by multicultural demographics | +0.9% | National, concentrated in diverse metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing consumer inclination toward natural and organic products

In the United Kingdom, consumer preferences are increasingly leaning toward natural and organic products as people become more conscious of product ingredients and sustainability. Studies show that while many consumers consider sustainability when purchasing beauty products, only a small percentage fully trust the claims made by brands. About 30% of United Kingdom consumers are willing to pay up to 10% more for products that are sustainable, highlighting the rising importance of ethical and environmentally friendly options. This trend is supported by the country’s relatively high purchasing power, with per capita income standing at 4,450 USD according to the International Monetary Fund (IMF), which allows consumers to afford slightly higher prices for products that align with their values[1]Source: International Monetary Fund, "United Kingdom Datasets", imf.org. The success of brands like Wild Cosmetics, which has grown quickly, positioning itself as a trustworthy alternative to traditional products, demonstrates this shift.

Social media influence to boost the market

Social media has become a significant sales channel in the United Kingdom, with social commerce generating GBP 7.3 billion in sales in April 2025. Platforms like TikTok and Instagram are playing a major role in influencing consumer behavior. On TikTok, trends such as “get-ready-with-me” videos encourage spontaneous purchases, while Instagram serves as a virtual storefront where consumers discover and buy products. Studies show that higher TikTok usage is linked to more impulsive buying in the beauty category, highlighting the platform's impact on driving unplanned purchases. This trend is further supported by the United Kingdom's high internet penetration, with 96% of the population using the internet in 2023, according to the World Bank[2]Source: World Bank, "Individuals Using The Internet (% of Population) - United Kingdom", worldbank.org. With such widespread connectivity, beauty content, influencer campaigns, and peer reviews reach a large audience, prompting brands to invest more in social media marketing.

Convenience and multi-functional products preference

In the United Kingdom cosmetics products market, consumers are increasingly drawn to convenient and multi-functional products that simplify their beauty routines. These products, such as BB and CC creams that combine skincare and coverage, or dual-purpose lip and cheek tints, are gaining popularity as they save time and reduce the need for multiple items. This trend is driven by a growing preference for cost-effectiveness, making multi-use products appealing for their practicality and value. Brands are responding by introducing products that emphasize versatility, catering to the needs of modern consumers. For example, Erborian’s 2024 launch of the Super BB Concealer-Serum in the United Kingdom combines concealing and SPF protection in one product. This reflects the increasing importance of multifunctionality in the market. This shift is encouraging higher spending per product, as buyers prioritize quality and functionality over the number of items they purchase.

Rising male grooming and unisex trends

In the United Kingdom cosmetics products market, the growing popularity of male grooming and unisex trends is expanding the consumer base and driving market growth. Male grooming is no longer limited to basic hygiene products, as younger men increasingly adopt skincare routines and even explore color cosmetics. This shift is also influenced by intergenerational acceptance, which is helping normalize grooming habits across different age groups. According to the Office for National Statistics, there were approximately 30.3 million males in England and Wales as of mid-2024, representing a significant potential consumer base[3]Source: Office for National Statistics, "Population Estimates for England and Wales: Mid-2024", ons.gov.uk. The rising demand for unisex and gender-neutral products is encouraging brands to create more inclusive product lines. Companies are investing in targeted marketing campaigns and repositioning their offerings to appeal to a broader audience.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Regulatory complexity and compliance costs | -0.9% | United Kingdom-wide, affecting all market participants | Long term (≥ 4 years) |

| Growth of counterfeit products availability | -0.6% | National, concentrated in online channels | Medium term (2-4 years) |

| Supply chain disruptions | -0.8% | United Kingdom-wide, affecting manufacturing and retail | Short term (≤ 2 years) |

| High costs associated with premium and organic products | -0.5% | National, impacting price-sensitive segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of counterfeit products availability

In the United Kingdom cosmetics products market, the rise of counterfeit goods has become a major issue, affecting both consumer trust and the reputation of brands. Counterfeit products are often sold through online platforms, making it easier for fake cosmetics to reach unsuspecting buyers. These fake items pose serious health risks, as some consumers have reported adverse reactions after using counterfeit products. To address this growing problem, the United Kingdom government introduced the "Choose Safe not Fake" campaign in March 2024, as per the Cosmetic, Toiletry and Perfumery Association[4]Source: Cosmetic, Toiletry and Perfumery Association, "How To Spot A Counterfeit Cosmetic Online", ctpa.org.uk. This initiative focuses on raising awareness about the dangers of counterfeit beauty and hygiene products while encouraging respect for intellectual property rights. Enforcement actions, such as Interpol’s Operation Pangea, have played a key role in tackling the issue. Authorities have shut down 43 United Kingdom-specific illegal websites and seized counterfeit shipments during raids in cities like Bolton, Wigan, and Glasgow.

Regulatory complexity and compliance costs

In the United Kingdom cosmetics products sector, navigating regulatory requirements has become increasingly challenging and costly for brands. Since Brexit, companies must comply with separate regulations for the United Kingdom and European markets. This includes appointing a United Kingdom Responsible Person and submitting product notifications for each market, which adds significant administrative and operational work. Even with support from industry organizations like the Cosmetic, Toiletry, and Fragrance Association, businesses face high expenses for legal assistance, product labeling, safety testing, and maintaining proper documentation to meet these regulations. These requirements not only increase costs but also delay product launches, reduce flexibility in managing product portfolios, and require constant monitoring of regulatory updates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Lines Anchor Growth, Eye Makeup Leads Momentum

In the United Kingdom cosmetics products market, facial cosmetics continue to lead the market, contributing 40.12% of revenue in 2025. These products are highly favored due to their dual functionality, combining skincare benefits with makeup features. Items like tinted moisturizers, BB/CC creams, and hybrid foundations are particularly popular as they offer hydration, sun protection, and coverage in one product. Consumers increasingly prefer such multifunctional solutions, making facial cosmetics a daily essential across various age groups. Both premium and mass-market brands are expanding their product lines in this category, focusing on quality formulations and convenience to meet evolving consumer demands and maintain loyalty.

Lip and nail cosmetics, on the other hand, are emerging as the fastest-growing segment, with a projected CAGR of 5.55% through 2031. Growth is being fueled by social media trends, influencer tutorials, and a desire among consumers, especially younger demographics, to experiment with bold, creative looks. Products such as vibrant lipsticks, glosses, nail polishes, and nail art kits are gaining traction, while brands launch limited-edition shades, seasonal collections, and multifunctional products. Retailers are curating engaging displays and experiences to showcase these items, positioning lip and nail cosmetics as key drivers of revenue growth and increased per-consumer spending.

By Category: Premium Acceleration Amid Mass Stability

In the United Kingdom cosmetics products market, mass-market brands continue to dominate, holding a significant 64.20% share. These brands excel due to their affordability, wide availability, and frequent product launches that cater to budget-conscious consumers. Their ability to offer discounts, bundle deals, and seasonal promotions keeps shoppers engaged and encourages repeat purchases. Mass-market brands benefit from strong distribution networks, ensuring their products are accessible both online and in physical stores. This broad reach and affordability make them a key driver of market volume in the United Kingdom.

On the other hand, premium cosmetics, while occupying a smaller share of the market, are expected to grow at a robust 6.66% CAGR through 2031. Consumers are increasingly drawn to premium products for their high-quality ingredients, innovative formulations, and the sense of luxury they provide. Many premium brands use loyalty programs and exclusive offers to attract and retain customers, making these products more appealing and accessible. Furthermore, premium cosmetics often emphasize brand storytelling and exclusivity, which resonate with consumers seeking aspirational products. This growing interest in premium offerings highlights their potential to capture a larger share of the market in the coming years.

By Nature: Organic Options Scale Quickly, Conventional Core Remains Firm

In the United Kingdom cosmetics products market, conventional formulations remain the most widely used, accounting for 83.95% of the market in 2025. These products are popular because they are affordable, effective, and have a longer shelf life compared to other options. Large brands rely on well-tested ingredients and preservatives, which provide consumers with a sense of safety and reliability. Their availability across various retail channels, including supermarkets and online platforms, ensures easy access for a broad range of customers. This combination of affordability, trust, and convenience makes conventional cosmetics a consistent choice for many households in the United Kingdom.

On the other hand, organic and natural cosmetics are gaining traction, growing at a strong 6.88% CAGR as more consumers prioritize sustainability and transparency. Certifications like Soil Association and Cosmos help build trust by verifying the authenticity of these products. Many emerging brands are using direct-to-consumer models to highlight their eco-friendly practices, such as ethical sourcing and reduced carbon footprints. Features like refillable packaging are particularly appealing to environmentally conscious buyers, especially younger urban consumers. Brands are using tools like QR codes to educate customers about the differences between natural and synthetic ingredients, encouraging informed purchases and gradually increasing the adoption of organic cosmetics.

By Distribution Channel: Online Surges as Specialty Beauty Stores Retain Authority

In the United Kingdom cosmetics products market, specialty beauty outlets captured 37.40% of the market share in 2025, primarily due to their ability to offer personalized and engaging in-store experiences. These stores provide hands-on services such as texture demonstrations, shade matching, and tailored product recommendations through trained beauty advisors. Such interactions help build consumer trust and encourage higher spending per visit. Flagship stores in major cities like London and Manchester host exclusive launch events that attract significant attention on social media, driving both foot traffic and online engagement.

On the other hand, the online channel is growing steadily, with a projected CAGR of 6.65%, driven by the convenience it offers and advancements in digital shopping tools. Online platforms now use AI-powered features to recommend products based on customer preferences, such as skin tone or uploaded selfies, making the shopping experience more personalized. Consumers also benefit from faster delivery options and the ability to explore a wide range of products from the comfort of their homes. Many brands are integrating online and offline experiences, such as offering tutorials on social media, quizzes on websites, and click-and-collect options at physical stores.

Geography Analysis

Regional sales trends in the United Kingdom cosmetics market vary significantly based on economic and demographic factors. Greater London stands out as the leader in premium spending, supported by a high influx of tourists and a dense network of luxury retail stores. Popular shopping areas like Covent Garden and Knightsbridge are adopting advanced technologies, such as augmented reality (AR) mirrors, which allow customers to virtually try on products and receive personalized shopping recommendations via email. These innovations are helping to enhance customer experiences and drive higher sales. Other major cities, including Manchester, Birmingham, and Glasgow, are also seeing growth, particularly in mid-priced independent brands showcased in renovated department stores.

In Northern England and Wales, consumers tend to favor affordable options, with supermarket private labels and frequent promotional discounts dominating the market. However, there is a noticeable rise in demand for inclusive shade ranges in cities like Leeds and Cardiff, where diverse, multi-ethnic populations are growing. Northern Ireland, on the other hand, operates under European cosmetics regulations, which require dual labeling for products sold across borders. This regulatory requirement adds complexity to logistics but ensures compliance with both United Kingdom and European standards, enabling brands to cater to a wider customer base.

E-commerce is growing rapidly in densely populated areas, especially in the southeast, where same-day delivery services are widely accessible. In rural regions, such as parts of Scotland and coastal communities, consumers rely more on pharmacy chains and mail-order catalogs for their beauty purchases. Social commerce, driven by platforms like Instagram and TikTok, is gaining traction across the country, but urban Gen Z consumers are leading the way in video-driven shopping. To meet these demands, brands are using geo-targeted live-streaming sessions and collaborating with local convenience stores to offer pick-up options. The widespread use of smartphones and strong broadband connectivity is helping to bridge the gap between online and offline shopping, creating a seamless and convenient experience for consumers.

Regulatory Landscape

Cosmetics placed on the Great Britain market are regulated under retained EU Regulation (EC) No 1223/2009, with enforcement led by the Office for Product Safety and Standards (OPSS). After Brexit, compliance requires a UK Responsible Person, a Cosmetic Product Safety Report (CPSR), and product notification via the Submit Cosmetic Product Notification (SCPN) service. This effectively adds UK-specific administrative and labeling steps for brands operating across both UK and EU regimes.

The restrictions framework has continued to tighten through statutory instruments, including the Cosmetic Products (Restriction of Chemical Substances) Regulations 2025 (in force 30 September 2025), which restricted methyl salicylate levels with transitional sell-through to 31 March 2026 for existing products. In 2026, The Cosmetic Products Regulation (EC) No 1223/2009 (Restriction of Chemical Substances) (Amendment and Transitional Provisions) Regulations 2026 (SI 2026 No. 23) came into force from 15 July 2026, prohibiting 3-(4-methylbenzylidene)-camphor and updating warning and labeling thresholds for formaldehyde-releasing preservatives, followed by additional CMR-related prohibitions effective 15 August 2026. The staggered dates increase the need for portfolio reviews, reformulation planning, and stock management aligned to transitional provisions.

Value Chain Analysis

The United Kingdom cosmetics products value chain covers ingredient and packaging sourcing, formulation and manufacturing (in-house and via contract manufacturers), regulatory assurance (Responsible Person, CPSR, and SCPN notification), and multichannel go-to-market across specialty beauty stores, supermarkets/hypermarkets, pharmacies, and online retail. The UK remains meaningfully import-reliant in physical supply, with domestic cosmetics manufacturing at 53K tons in 2024 compared with imports of 177K tons. This raises the importance of supplier qualification, customs readiness, and documentation quality for inbound flows.

Distribution and commercialization are increasingly shaped by omnichannel execution. Brands balance physical trial and advisory services in specialty stores with online discovery and conversion, including social commerce. Post-Brexit trade friction and dual compliance (UK and EU) can introduce delays at the border and add administrative steps, so compliance management and demand planning become central to chain execution. This includes reformulation timelines driven by substance restriction updates (including 2024-2025 restrictions with transitional dates into early 2026) and inventory allocation across Great Britain and Northern Ireland, where EU rules continue to apply.

Competitive Landscape

The United Kingdom cosmetics market is moderately consolidated, with the top 5 companies accounting for a valuable share of the total revenue. Global giants like L’Oréal, Estée Lauder, and Unilever dominate the market through their strong focus on innovation, robust supply chains, and strategic acquisitions. Meanwhile, domestic brands such as No7 and Charlotte Tilbury maintain their market share by leveraging their heritage and quickly adapting to omnichannel strategies. Direct-to-consumer start-ups are gaining traction by using social media storytelling to build their presence. Once they establish a strong digital footprint, these start-ups often partner with retailers like Boots or Sephora to expand into physical stores.

Investments in artificial intelligence (AI) are distinguishing market leaders. For instance, L’Oréal collaborates with IBM to develop AI models that can create low-impact formulations in hours instead of months, significantly speeding up product development. Similarly, The Hut Group (THG) uses customer journey data to optimize product bundles, increasing the average order value. Sustainability is also becoming a critical focus for companies. Unilever, for example, highlights its progress in using biodegradable ingredients and packaging made from post-consumer recycled materials, aligning with consumer demand for eco-friendly products.

Merger and acquisition activity remains strong in the United Kingdom cosmetics market. The Hut Group’s acquisition of Acheson & Acheson has enhanced its control over contract manufacturing, enabling faster product launches. Boots has fully integrated Soap & Glory into its portfolio, aligning the brand with its loyalty programs and broader product assortment. At the same time, supermarkets are expanding their private-label offerings, putting pressure on mid-tier brands. This trend is creating a "barbell" market structure, where value-oriented and ultra-premium products are thriving, while mid-range brands face challenges in maintaining their market position.

United Kingdom Cosmetics Products Industry Leaders

-

L'Oréal SA

-

Estée Lauder Companies Inc.

-

Unilever PLC

-

Coty Inc.

-

Kao Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory change is opening space for reformulation services, compliant ingredient substitution, and clearer on-pack communication. This is particularly relevant after the UK introduced additional restriction updates through SI 2026 No. 23, effective from 15 July 2026 with further prohibitions from 15 August 2026. Brands and manufacturers that can translate OPSS-led rule changes into reformulated SKUs, updated labels, and SCPN maintenance have a clearer route to continuity of supply, while slower-moving portfolios face higher changeover costs and greater discontinuation risk.

Packaging and circularity programs are also becoming more operational. The British Beauty Council launched The Great British Beauty Clean Up 2026 in March 2026, partnering with MYGroup to provide zero-landfill recycling solutions for hard-to-recycle cosmetic components such as pumps and mascara tubes. MYGroup works with retailers including Boots, Harrods, Cult Beauty, LOOKFANTASTIC, Selfridges, and Superdrug, and reported over 40,000 tonnes diverted from landfill. In parallel, the CTPA introduced a digital sustainability handbook in June 2026 (developed with Forum for the Future), giving companies tools to prioritize sustainability actions and identify innovation opportunities. The government also signaled supply-chain due diligence direction through the Great Britain Deforestation Regulation (GBDR) announcement in June 2026, which increases operational focus on traceability and supplier data readiness for qualifying businesses.

Recent Industry Developments

- June 2026: The Estee Lauder Companies announced a strategic investment to integrate luxury candle and home fragrance manufacturing into its UK Whitman Facility in Petersfield, including assuming a lease from its partner Contract Candles. The move strengthens UK-based production control for adjacent beauty lifestyle categories and supports faster supply response into local retail and e-commerce channels.

- May 2026: Unilever completed a GBP 150 million upgrade at its Port Sunlight campus, adding a new automated distribution centre and manufacturing upgrades supporting home and personal care brands. The investment improves domestic logistics capability and operational efficiency, helping shorten lead times and reduce disruption risk across UK fulfillment.

- September 2025: Boots expanded its beauty assortment by adding Catrice, Essence, and SheGlam across stores nationwide, introducing more than 400 new cosmetics products. The rollout broadened accessible trend-led choice in mass cosmetics and increased the role of large drugstore chains in amplifying social-led brands beyond online-only discovery.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the value of cosmetics products sold to consumers within the United Kingdom across offline and online channels, counted at the point of sale and reported in USD terms.

Scope exclusions: This sizing does not count salon service revenue, clinical aesthetic procedures, or non-cosmetic personal care items that are not positioned and purchased as cosmetics.

Segmentation Overview

-

By Product Type

- Facial Cosmetics

- Eye Cosmetics

- Lip and Nail Cosmetics

-

By Category

- Mass

- Premium

-

By Nature

- Organic

- Conventional

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Beauty Stores

- Online Retail Channels

- Other Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the first version of the market map and to set realistic guardrails for demand and supply, before any assumptions are finalized. We mainly rely on public UK and international statistics to understand consumer spend direction, trade movement for relevant product groups, and the retail environment that cosmetics typically moves through.

Common reference points include official publications and data portals such as the UK Office for National Statistics, HM Revenue and Customs trade statistics, the UK government product safety and regulatory guidance, international sources such as UN Comtrade, and peer reviewed journals that track consumer and formulation trends. We also reviewed company annual reports, investor presentations, and reputable press coverage to sense-check channel momentum, pricing changes, and category mix shifts. In addition, a paid subscription for company financials and a patent database were used selectively to validate growth patterns and the pace of product innovation. These desk sources are illustrative only, and we also used other public and paid references for cross-checking and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the model with real market behavior, especially where public data is broad or delayed. We spoke with a mix of brand-side teams, distributors, and retailers, along with industry specialists across the United Kingdom, so assumptions on channel splits, premium versus mass mix, and price ladders could be confirmed and corrected.

Feedback was also used to triangulate what is driving category shifts, such as shade range expansion, sustainability claims, and online purchasing habits, and to align the forecast path with what practitioners expect to hold steady versus change quickly.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 14% | |

| Mid tier: 52% | Functional/Unit leaders: 34% | |

| Smaller Players: 21% | Managers: 52% |

Market-Sizing & Forecasting

Sizing starts with a top-down rebuild of the UK demand pool by combining category-level consumer expenditure signals with channel structure, followed by adjustments that reflect cosmetics-specific purchase frequency and pricing. To keep totals realistic, results are corroborated with selective bottom-up approximations, such as sampled price-point checks by channel and roll-ups of visible brand revenues where disclosures allow.

Inputs that mattered most for this market included premium versus mass mix, online retail share, the split between color cosmetics and hair styling and coloring, typical price ladders by format, and the pace of trade-up into premium lines. Where gaps show up in bottom-up cross-checks, we apply conservative fill-ins using proxy mixes from close categories and then re-test them through additional channel feedback.

For forecasting, scenario analysis is used so the outlook can reflect how sensitive the market is to consumer confidence, inflation-driven price changes, and e-commerce momentum. The final forecast path is anchored on what primary respondents view as the most likely trajectory, and it is kept consistent with the market's observed historical growth rhythm.

Data Validation & Update Cycle

Validation is done in layers so the estimate is not driven by a single data series or one set of interviews. We run consistency checks across channel totals, price and volume logic, and year-over-year movements, and then we investigate outliers until a clear explanation is documented.

Before sign-off, the model and assumptions go through a second analyst review, followed by targeted re-contacts when a data point is material and still uncertain. Reports are refreshed annually, and interim updates are made when major events occur, such as sharp currency movement, regulatory changes affecting product claims, or visible shifts in retailer strategy. Right before delivery, we complete a final pass to confirm the latest public updates are reflected in the numbers.

Mordor Intelligence's United Kingdom Cosmetics Products Market Market Size Compared With Other Published Estimates

Different published numbers for the UK cosmetics products market are common because sources often group product baskets differently and use different base years, which then changes how growth is applied. Another frequent reason is that retail value can be counted at different points in the chain, and currency conversion timing can further widen the spread.

Skincare and broader personal care baskets sit outside Mordor Intelligence's scope here, which is why some larger published figures are not directly comparable even when the geography is the same. In addition, some estimates blend conservative and aggressive scenarios without clearly stating the implied price progression, whereas this study keeps price ladders and channel splits visible so each step can be rechecked.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.20 B (2025) | |

| Global Consultancy A | USD 15.76 B (2025) | Uses a broader cosmetics definition that also bundles skincare and related personal care categories, which inflates the addressable value versus a cosmetics-only basket. |

| Industry Publisher B | USD 14.30 B (2025) | Combines cosmetics with personal care and also reports at a wider category level, so channel mix and price ladder assumptions are not separable for cosmetics products alone. |

The table shows that most of the difference comes from how wide the product basket is, not from a small modeling tweak. By keeping the scope tight and cross-checking totals using channel-level signals and practical price assumptions, the estimate stays traceable and easier to replicate when conditions change.

Key Questions Answered in the Report

What is the current value of the United Kingdom cosmetics products market?

It is valued at USD 3.35 billion in 2026 and is projected to rise to USD 4.19 billion by 2031.

Which product segment leads sales?

Facial cosmetics hold 40.12% of revenue, making them the leading segment.

Which channel is growing fastest for beauty purchases?

Online retail is expanding at a 6.65% CAGR through 2031 on the back of AI-driven personalization and rapid delivery.

How fast is the organic cosmetics segment growing?

Organic lines are advancing at a 6.88% CAGR, the quickest among the nature segments.

Page last updated on: