Switzerland Cosmetic Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

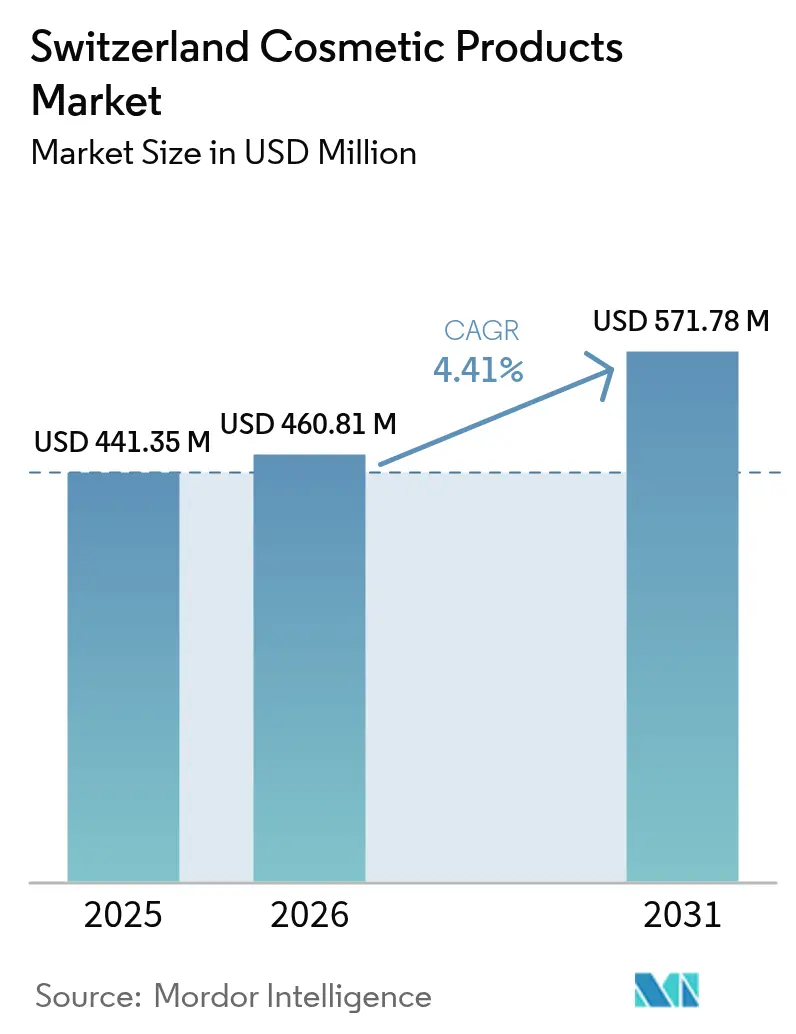

| Base Year Market Size (2025) | USD 441.35 Million |

| Market Size (2026) | USD 460.81 Million |

| Market Size (2031) | USD 571.78 Million |

| Growth Rate (2026 - 2031) | 4.41% CAGR |

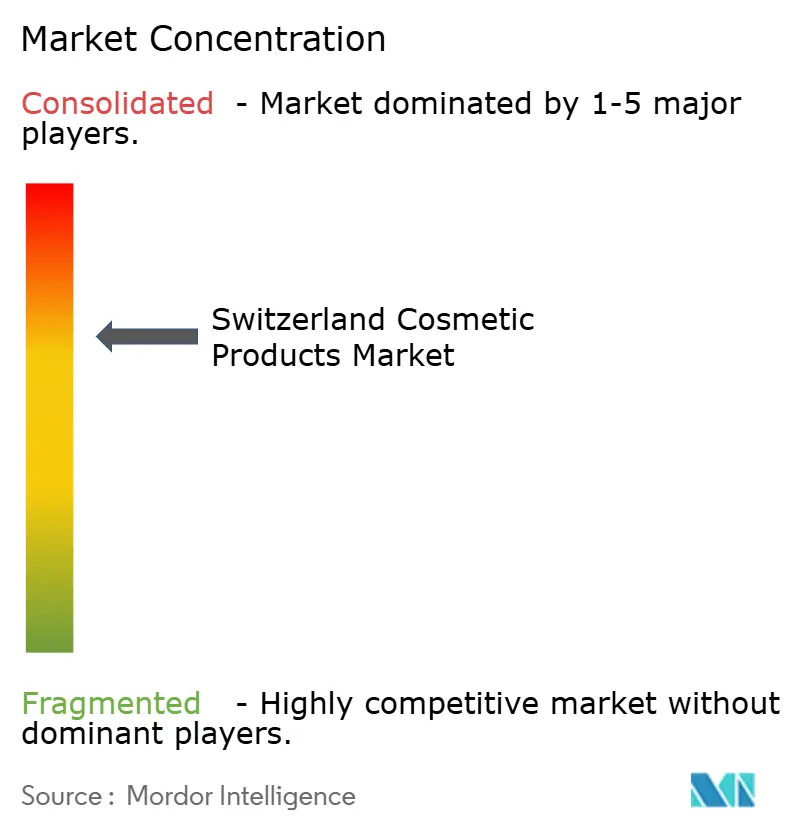

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Switzerland Cosmetic Products Market Analysis by Mordor Intelligence

The Switzerland cosmetics products market size was valued at USD 441.35 million in 2025, increased to USD 460.81 million in 2026, and is projected to reach USD 571.78 million by 2031, registering a CAGR of 4.41% during the forecast period. The market's growth is primarily driven by a strong culture of personal grooming and consistent daily-use habits. In Switzerland, cosmetics are closely associated with hygiene, a neat appearance, and professional presentation, rather than being limited to occasional beauty use. Additionally, the market benefits from a growing emphasis on product quality, safety, and credibility. Swiss consumers are cautious and well-informed, favoring trusted products backed by scientific research, which drives brands to invest in research, testing, and product development. Furthermore, demand is bolstered by increasing interest in natural product positioning, sustainability awareness, and ethical consumption patterns.

Key Report Takeaways

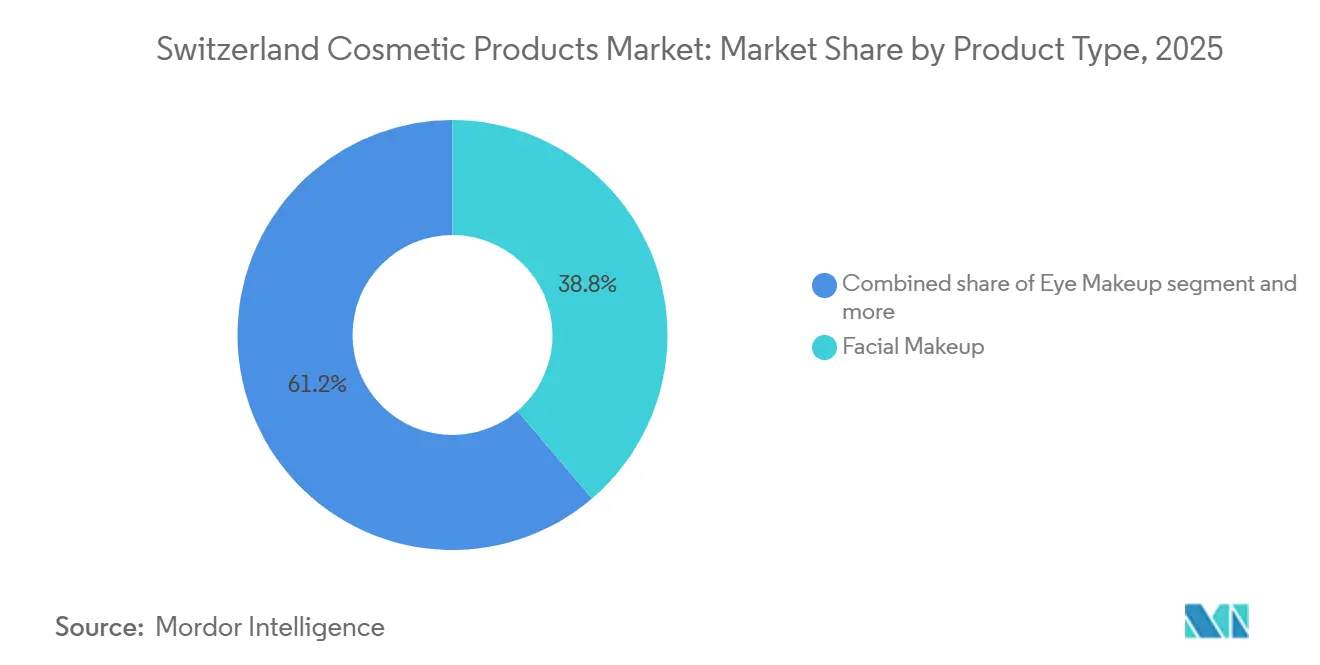

- By product type, facial makeup led with 38.76% of Switzerland cosmetics products market share in 2025, while eye makeup posts the fastest 4.76% CAGR through 2031.

- By category, the mass segment held 71.39% of the Switzerland cosmetics products market size in 2025; premium lines advance at a 5.65% CAGR to 2031.

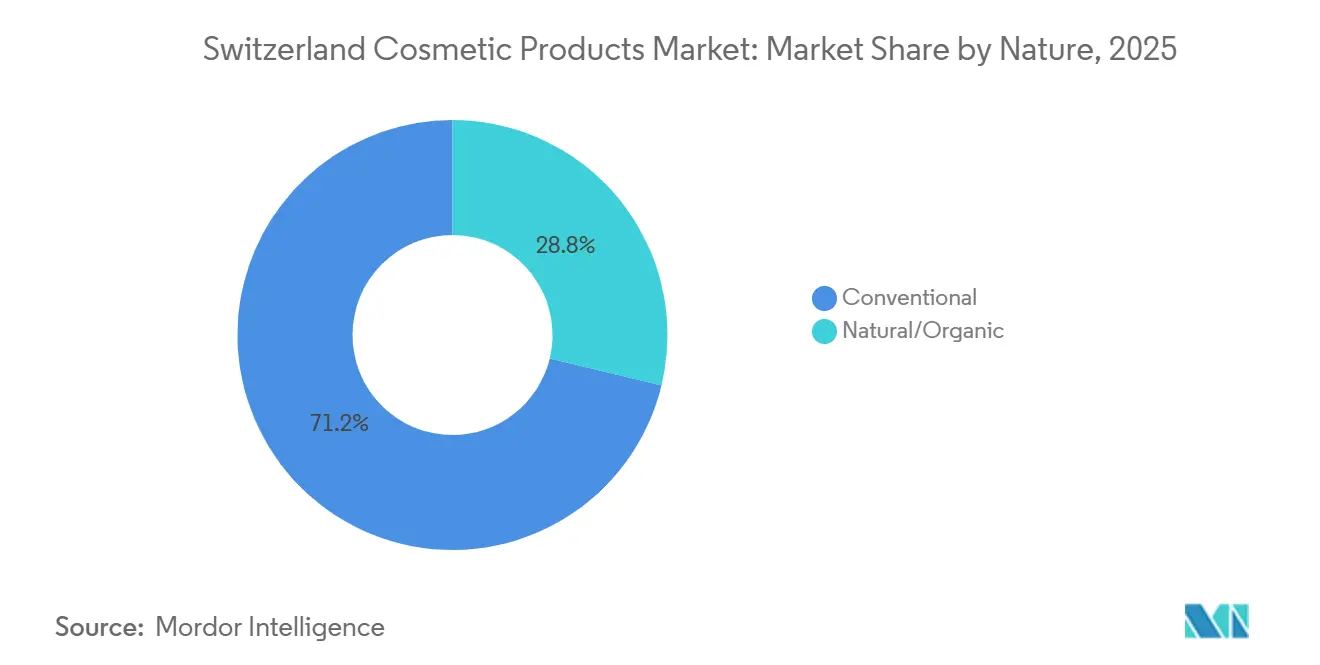

- By nature, conventional formulas accounted for 71.22% share in 2025, whereas natural/organic ranges are set to widen at a 5.81% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets controlled 34.43% of the 2025 value, but online retail expanded at 6.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland Cosmetic Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong preference for natural and organic ingredients | +0.8% | National, with concentration in German-speaking cantons | Medium term (2-4 years) |

| Anti-aging and skin-health orientation | +0.7% | National, particularly urban centers (Zurich, Geneva, Basel) | Long term (≥ 4 years) |

| Growing demand for premium, high-performance formulations | +0.6% | National, strongest in high-income cantons | Medium term (2-4 years) |

| Dermatological safety and sensitive-skin suitability | +0.5% | National | Long term (≥ 4 years) |

| Influence of social media and beauty influencers | +0.4% | National, skewed toward 18-35 age cohort | Short term (≤ 2 years) |

| Increasing focus on sustainability, eco-friendly packaging | +0.5% | National, with early adoption in Romandy region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong preference for natural and organic ingredients

The increasing preference for natural and organic beauty products is a key driver of the Switzerland cosmetics products market. Consumers are paying closer attention to product labels, favoring formulations perceived as safer, gentler, and environmentally sustainable. This trend has prompted brands to expand their offerings of plant-based and minimally processed products. The shift is driven by growing awareness of long-term skin care, preventive grooming practices, and concerns about synthetic chemicals, leading consumers to actively seek products marketed as clean and nature-focused. Retailers have adapted by allocating dedicated shelf space and providing clearer labeling for natural cosmetics, enhancing product visibility and simplifying purchasing decisions. As consumer trust and familiarity with these products grow, repeat purchases increase, and brands continue to introduce new product lines, solidifying the natural and organic trend as a significant contributor to market growth.

Anti-aging and skin-health orientation

The increasing emphasis on maintaining healthy and youthful skin is a significant driver of the Switzerland cosmetics products market. Consumers are prioritizing preventive grooming and long-term skin care, integrating skincare and appearance-enhancing products into their daily routines rather than reserving them for occasional use. This trend is closely linked to the country’s aging demographic. According to the Federal Statistical Office, individuals aged 65–79 years constituted 13.8% of Switzerland’s population in 2024 [1]Source: Federal Statistical Office, "Permanent resident population by age and dependency ratio, in 2024", bfs.admin.ch. Consequently, a substantial portion of consumers actively seeks products aimed at preserving skin condition, enhancing appearance, and boosting confidence in both social and professional settings. The focus on healthy aging, coupled with high awareness of skincare practices and professional guidance, promotes consistent product usage and repeat purchases, positioning the anti-aging and skin-health segment as a key driver of market growth.

Growing demand for premium, high-performance formulations

Consumer preference for high-quality, performance-oriented beauty products is significantly driving market growth. Swiss consumers are highly selective and brand-conscious, placing strong emphasis on product credibility, visible effectiveness, and trusted brand reputation rather than following fleeting trends. Many buyers actively seek cosmetics marketed as advanced or professional-grade, encouraging brands to prioritize innovation, expand product portfolios, and introduce more sophisticated and effective solutions. Specialty beauty retailers, department stores, and beauty consultation counters play a crucial role in this trend by offering expert guidance and personalized recommendations, which further enhance consumer confidence in premium products. As shoppers increasingly associate premium cosmetics with reliability, safety, and superior results, they are not only more inclined to transition from basic alternatives but also demonstrate strong loyalty to established and reputable brands.

Dermatological safety and sensitive-skin suitability

Swiss consumers are increasingly focused on product safety and skin compatibility, showing heightened caution regarding skin reactions. They prefer cosmetics that are perceived as gentle and suitable for sensitive skin, driving the routine use of products designed for skin comfort and protection. Trust significantly influences purchasing decisions, with pharmacy recommendations, professional guidance, and scientifically backed brands fostering consumer confidence and encouraging repeat purchases. This trend is mirrored in industry initiatives. For example, in March 2025, L’Oréal Groupe introduced L’Oréal Act for Dermatology, a EUR 20 million five-year program led by its Dermatological Beauty Division to enhance access to skin health solutions for the 2.1 billion people globally affected by skin diseases. Such initiatives increase awareness of dermatological care and emphasize the importance of safe, skin-friendly cosmetics, motivating consumers to integrate these products into their daily grooming routines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory frameworks on product safety | -0.4% | National | Long term (≥ 4 years) |

| Strong scrutiny over animal testing and ethical sourcing | -0.3% | National, with spillover to EU export markets | Medium term (2-4 years) |

| Product claims verification challenges | -0.3% | National | Medium term (2-4 years) |

| Prevalence of counterfeit products | -0.4% | National, concentrated in cross-border e-commerce | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory frameworks on product safety

Strict regulatory oversight serves as a restraint in the Switzerland cosmetics products market. Switzerland's cosmetics regulations align closely with EU Regulation (EC) No. 1223/2009, which mandates comprehensive requirements for product safety assessments, ingredient restrictions, labeling standards, and documentation before market entry. Companies are required to conduct toxicological evaluations, maintain product information files, and adhere to approved ingredient lists, adding complexity and time to product development and market entry processes. Changes in formulation or packaging often necessitate additional verification and administrative procedures, which can extend innovation cycles and delay product launches. This compliance burden is particularly challenging for smaller companies and new entrants, increasing operational difficulties and hindering rapid expansion.

Strong scrutiny over animal testing and ethical sourcing

Consumer concerns about animal welfare and responsible sourcing are limiting the growth of the cosmetics products market in Switzerland. There is a growing expectation for cosmetics to adhere to cruelty-free standards and maintain transparency in sourcing practices throughout the supply chain. Brands are required to verify the origins of raw materials, secure ethical certifications, and ensure that suppliers comply with welfare and sustainability guidelines. These requirements add complexity to procurement and documentation processes. A lack of clear communication regarding these practices can harm brand reputation and result in product rejection by both retailers and consumers. Consequently, companies must undertake additional monitoring, auditing, and certification efforts, which extend development timelines and increase operational challenges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Multifunctional Eye Products Gain Momentum

The facial makeup segment is expected to hold a 38.76% share of the Switzerland cosmetics products market in 2025, driving and dominating the market due to its alignment with the country’s beauty culture. This culture emphasizes a polished, well-groomed, and naturally refined appearance. Swiss consumers typically prefer subtle enhancements to their complexion and even skin tone over bold or dramatic cosmetics, making facial makeup an everyday necessity rather than an occasional purchase. The segment benefits from high usage frequency, as base makeup products are integrated into daily grooming routines for work, social interactions, and professional settings. Additionally, strong beauty awareness, personal care consciousness, and the importance of maintaining a neat personal image in both corporate and public environments encourage consistent daily use. This results in steady replacement cycles and repeat purchases.

The eye makeup segment is projected to grow at a CAGR of 4.76% through 2031, driven by increasing consumer use of eye-focused cosmetics to enhance facial expression while adhering to Switzerland's preference for understated beauty. In everyday social and professional settings, defining the eyes is seen as an effective way to achieve a refined and presentable appearance without relying on heavier cosmetic routines, supporting frequent usage. The trend toward simplified grooming habits has further strengthened this category, as many consumers prioritize a few visible, high-impact cosmetic steps. Eye makeup provides quick results with minimal time commitment, making it a preferred choice for many.

By Category: Premium Gains Share Through Efficacy Narratives

The mass category accounted for a 71.39% market share in 2025, primarily due to its accessibility, routine-use positioning, and broad consumer acceptance across various age groups and lifestyles. Mass cosmetics are closely associated with convenience-based shopping, with consumers in highly urbanized areas relying on easily accessible retail formats such as supermarkets, drugstores, and pharmacy chains near residential and workplace locations. Urban populations, often maintaining faster-paced daily schedules, favor practical and time-efficient grooming habits, leading to frequent purchases of readily available beauty essentials rather than specialty or consultation-driven products. For example, according to the World Bank, the urban population of the Netherlands reached 16.81 million in 2024, an increase of 0.95% from 2023 [2]Source: World Bank, "Urban population - Switzerland", worldbank.org. This growth in urban concentration in developed European markets supports routine retail purchasing patterns.

The premium category is projected to grow at a CAGR of 5.65% through 2031, steadily expanding within the Swiss cosmetics market. Consumers increasingly associate premium beauty products with quality assurance, safety, and brand credibility. Swiss buyers, known for being highly selective and well-informed, often prefer products that offer trusted brand reputations, sophisticated presentation, and personalized shopping experiences. Additionally, gifting culture and occasion-based purchases, particularly during holidays and social events, drive higher-value sales in the premium segment, even though purchase frequency is lower compared to the mass category. Premium brands also benefit from strong brand storytelling, heritage positioning, and exclusivity, which resonate with consumers seeking differentiation and self-expression.

By Nature: Clean-Beauty Certifications Command Price Premiums

Conventional formulations accounted for 71.22% of the Switzerland cosmetics products market in 2025, maintaining dominance due to their familiarity, consistency, and proven performance, which align with consumers' preference for reliable daily-use products. Swiss consumers prioritize reliability and safety, and conventional products benefit from decades of trust and brand recognition, fostering repeat purchases. These products are deeply integrated into routine grooming habits, as consumers often continue using products that meet their expectations, leading to strong brand loyalty and stable replacement cycles. Additionally, established production standards, predictable product performance, and stable shelf life further support their dominance, particularly for everyday use where consistent results are preferred over experimentation.

The natural and organic category, projected to grow at a CAGR of 5.81% through 2031, is steadily expanding in the Switzerland cosmetics products market as consumers increasingly favor products perceived as gentle, transparent, and environmentally responsible. Swiss consumers are highly conscious of product safety and long-term skin care, driving a gradual shift from heavily processed formulations to simpler, nature-aligned alternatives. Awareness campaigns, ingredient scrutiny, and a growing interest in wellness-oriented lifestyles are influencing purchasing decisions, particularly among younger adults and families who prioritize precautionary choices in their daily grooming routines.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Supermarkets and hypermarkets accounted for 34.43% of the Switzerland cosmetics products market in 2025, establishing themselves as the leading retail channel. This dominance is attributed to their convenience-driven shopping environment and integration with routine household purchasing. Consumers in Switzerland often buy cosmetics alongside groceries and other daily essentials, benefiting from the one-stop shopping experience these stores provide. Features such as extended operating hours, easy accessibility in residential and urban areas, and organized product displays enable shoppers to quickly compare brands without requiring specialist assistance. Additionally, the availability of well-known mass brands, promotional pricing, bundled offers, and seasonal discounts further incentivizes consumers to purchase cosmetics during regular shopping trips.

The online retail stores channel, projected to grow at a CAGR of 6.54% through 2031, is gaining significant traction in the Switzerland cosmetics products market. Digital purchasing is increasingly becoming a part of everyday shopping behavior. Consumers appreciate the convenience of browsing, comparing, and purchasing cosmetics at any time without the need to visit physical stores, especially for repeat purchases of familiar products. Online platforms offer access to a broader range of brands, shades, and product variants than typically available in physical outlets. Detailed product descriptions, customer reviews, and ratings help reduce purchase uncertainty. Furthermore, promotional offers, online exclusives, and influencer-led product discovery are attracting younger, tech-savvy buyers to digital channels. For example, according to the International Telecommunication Union (ITU), approximately 97.3% of individuals in Switzerland were internet users in 2025, highlighting near-universal connectivity that supports the rapid adoption of e-commerce for beauty shopping [3]Source: International Telecommunication Union (ITU), "Individuals using the Internet", datahub.itu.int.

Geography Analysis

The geographical structure of the Switzerland cosmetics products market is influenced by regional lifestyle variations, language differences, and retail concentration patterns rather than significant territorial disparities. Major urban centers such as Zurich, Geneva, and Basel serve as key consumption hubs due to their dense retail networks, international brand presence, and high foot traffic in shopping districts and transport corridors. These cities drive strong demand for both everyday grooming products and premium beauty items, supported by professional working environments and active social lifestyles. Urban consumers frequently purchase cosmetics through supermarkets, pharmacies, and specialty beauty stores, while also adopting newer shopping formats more readily than rural populations.

In the German-speaking regions, demand is primarily shaped by practical purchasing behavior and routine shopping habits, favoring mass-market cosmetics sold through drugstores and large retail chains. The French-speaking regions, particularly in western Switzerland, exhibit a stronger preference for premium and luxury beauty products, supported by department stores, selective perfumeries, and cross-border shopping influences from neighboring European markets. The Italian-speaking region, including Ticino, reflects balanced consumption patterns, combining daily-use cosmetics with seasonal and occasion-based purchases driven by tourism and hospitality activities. Across all regions, pharmacies play a significant role, as Swiss consumers place high trust in professionally recommended personal care products.

Rural and semi-urban areas contribute stable but lower-volume demand, primarily focused on essential grooming products purchased during regular household shopping trips. However, the growth of e-commerce is gradually reducing geographic purchasing disparities by enabling consumers nationwide to access a wider range of products, regardless of local store availability. Online platforms allow smaller towns and alpine communities to purchase specialty and international brands without the need to travel to major cities, enhancing market penetration.

Regulatory Landscape

Cosmetic products in Switzerland are regulated under the Federal Act on Foodstuffs and Utility Articles and the Ordinance on Cosmetics (OCos/VKos, SR 817.023.31), under the oversight of the Federal Food Safety and Veterinary Office (FSVO/BLV). Swiss requirements broadly align with EU Regulation (EC) No. 1223/2009, but obligations also remain tied to Swiss ordinances for product safety, ingredient restrictions, and labeling. Cosmetics do not require pre-market authorization, and manufacturers and importers carry primary responsibility through self-supervision.

Competitive Landscape

The Switzerland cosmetics products market is moderately concentrated, featuring a mix of global beauty conglomerates and specialized dermatological brands competing in both mass and premium segments. Key players include L’Oréal S.A., Beiersdorf AG, The Estée Lauder Companies Inc., Shiseido Company, Limited, and Galderma S.A. These companies leverage robust brand portfolios, extensive retail partnerships, and established consumer trust. Competition in the market is primarily driven by brand credibility, product reliability, and consistent availability across pharmacies, specialty beauty retailers, department stores, and modern retail chains, rather than price. Market presence is actively maintained through frequent product updates, seasonal launches, and targeted marketing efforts. Additionally, pharmacy and dermocosmetic positioning play a significant role in fostering consumer confidence in product safety and effectiveness.

Technology has emerged as a key competitive factor, with companies differentiating themselves through research-backed formulations and advanced product development capabilities. Investments in laboratory testing, skin analysis tools, and data-driven personalization are enhancing consumer engagement and enabling tailored product recommendations both in-store and online. Digitalization further supports virtual consultations, online shade matching, and interactive brand platforms, improving the shopping experience and strengthening direct relationships with consumers. Continuous innovation and the ability to adapt quickly to evolving beauty routines and consumer expectations are critical for maintaining competitive positioning in the Swiss market

Sustainability has become a significant area of competition, with brands emphasizing environmentally responsible practices in packaging, sourcing, and production processes. Companies are adopting recyclable or refillable packaging, reducing material usage, and enhancing supply chain transparency to meet the preferences of environmentally conscious consumers. Clear labeling, responsible sourcing initiatives, and claims of reduced environmental impact are increasingly used as differentiators. As Swiss consumers prioritize ethical and ecological considerations, sustainability strategies have shifted from being a marketing tool to a core competitive requirement, influencing product development and fostering long-term brand loyalty in the Switzerland cosmetics products market.

Switzerland Cosmetic Products Industry Leaders

-

L’Oréal S.A.

-

Beiersdorf AG

-

The Estée Lauder Companies Inc.

-

Shiseido Company, Limited

-

Galderma S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premiumization and dermocosmetic positioning create scope for clinically supported, sensitive-skin and anti-aging propositions that are easier to substantiate and explain in pharmacy and consultation-led channels, where trust and safety influence buying decisions. A concrete indicator is L'Oréal Groupe's March 2025 launch of L'Oréal Act for Dermatology (a five-year EUR 20 million program), which has contributed to greater consumer attention on skin health and supports the role of science-backed claims in Switzerland's cosmetics aisle.

Industry organization and origin signaling also create room for differentiated local manufacturing and packaging propositions. Around 90% of companies are represented by the Swiss Cosmetic and Detergent Association (SKW), and SWISSCOS supports Swiss Made cosmetics by applying strict criteria, including 100% manufacturing and packaging in Switzerland, to reinforce origin-based brand value. In parallel, sustainability and circular-economy execution, including recyclable packaging, substance substitution, and CO2-neutral production initiatives highlighted by industry bodies, alongside faster innovation cycles (with SKW noting that roughly a quarter of products are redeveloped or improved annually), support opportunities for brands that can manage compliant reformulation and packaging redesign with transparent documentation under OCos/VKos while maintaining shelf availability across mass retail and fast-growing online retail.

Recent Industry Developments

- June 2026: L'Oréal announced a collaboration with OpenAI at VivaTech 2026 to scale the use of AI across marketing and research operations. The move builds on company-wide generative AI capability development and supports faster content creation and product development workflows, reinforcing competitive pressure on speed-to-market and personalization in beauty.

- May 2025: Beiersdorf announces expansion of Nivea production capacity in Switzerland to support local demand. The expansion underscores continued focus on local production and supply resilience for the Swiss market.

- September 2024: The Estee Lauder Companies expanded its Pink Ribbon campaign assortment in Switzerland with limited-edition Pink Ribbon Advanced Night Repair Serum and the Transforming Hope Lip Collection, supporting the Breast Cancer Research Foundation through June 2026. The initiative links prestige skincare and makeup demand to purpose-led merchandising and seasonal gifting, helping sustain premium category visibility at retail.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Switzerland cosmetics products market is defined as the value of cosmetic items sold in Switzerland across mass and premium positioning, tracked through key retail and online channels in value terms.

Scope exclusions: This market does not cover perfumes, deodorants, soaps, or toothpaste when they are treated as personal care or hygiene items rather than cosmetics.

Segmentation Overview

-

By Product Type

- Facial Makeup

- Eye Makeup

- Lip and Nail Cosmetics

-

By Category

- Mass

- Premium

-

By Nature

- Natural/Organic

- Conventional

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Stores

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the baseline for consumer spend patterns, category definitions, and channel structure in Switzerland, before any modeling was finalized. We relied on public sources such as the Swiss Federal Statistical Office for household expenditure indicators, the Swiss Federal Customs Administration for trade flows, Eurostat for comparable consumer and retail series, and OECD datasets for macro context that affects discretionary categories.

To make inputs practical, we also reviewed company annual reports and investor presentations for exposure cues, along with retailer and association websites that describe category merchandising and pricing architecture. When needed, a paid subscription for company financials and a shipment level trade database were used to validate revenue directionality and import intensity without forcing unrealistic granularity. The sources listed here are illustrative only, and many other public documents were also reviewed to collect data points, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to pressure test category splits, premiumization effects, and the pace of online mix change in Switzerland, since these can shift totals even when volumes look stable. We spoke with a range of manufacturers, distributors, retailers, and industry advisors, then aligned their feedback on pricing, promotions, and product mix to the desk-based model before locking the final sizing and forecast.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 19% | APAC: 43% |

| Mid tier: 49% | Functional/Unit leaders: 29% | EMEA: 31% |

| Smaller Players: 20% | Managers: 52% | Americas: 26% |

Market-Sizing & Forecasting

Sizing started with a top-down rebuild of Switzerland cosmetics demand, where national consumption signals, import trends, and retail channel weightings were converted into value pools and then apportioned across cosmetics categories. To keep the numbers grounded, we corroborated totals with selective bottom-up approximations, such as sampled price points by category multiplied by implied unit movement, and cross-checks against supplier and distributor revenue exposure.

A few inputs in this market were tracked carefully, including premium versus mass mix shifts, online share movement, promotional intensity, average selling price progression by category, and the relative momentum of makeup items versus adjacent beauty baskets. Forecasting was run using scenario analysis supported by simple time-series smoothing for stable indicators, then adjusted using interview-based expectations on pricing and channel dynamics. Where direct visibility was limited, gaps were handled by using proxy splits from comparable retail formats and then re-checking with primary responses until the implied totals stayed consistent.

Data Validation & Update Cycle

Validation was done through multiple checks, starting with a reconciliation of category totals against independent signals like trade direction, retail performance cues, and the implied price and mix movement over the period. Any sharp jumps were reviewed again, and the underlying assumptions were revisited, followed by a second analyst review before sign-off.

The model is refreshed on an annual cycle, and interim updates are triggered when material events occur, such as sharp price inflation, major channel disruptions, or regulatory changes that affect product availability. Before a report is delivered, we do a final pass to ensure the latest public information is reflected and that the numbers still tie back cleanly to the stated scope and inputs.

Mordor Intelligence's Switzerland Cosmetics Products Market Market Size Compared Against Other Published Estimates

Published market values for cosmetics in Switzerland can look far apart, even when everyone is working from the same country and similar time periods. The spread usually comes from what gets counted as cosmetics versus personal care, which channels are included, and how prices and premium mix are treated in the forecast.

Perfumes and broader beauty and personal care baskets are sometimes folded into some totals, but they sit outside Mordor Intelligence's scope here, which is why the table shows a much smaller value based on a tighter cosmetics product definition. Differences also show up when studies use aggressive pricing uplift assumptions, use retail sales panels that cover different store sets, or convert currencies at different timing points than the base year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 441.35 M (2025) | |

| Regional Consultancy A | USD 5.70 B (2024) | Uses a broader definition closer to beauty and personal care, and the value appears to reflect a wider product basket and channel coverage than cosmetics-only items. |

| Trade Journal B | USD 5.70 B (2024) | Counts manufacturing, imports, distribution, and retail sales across multiple beauty and personal care categories, which can expand scope and can lead to double counting versus an end-market cosmetics value. |

Looking across the three figures, the main takeaway is that scope and accounting treatment create most of the distance, not a disagreement on Switzerland demand direction. By tying the estimate to a clearly stated cosmetics-only basket, a consistent value definition, and repeatable checks on pricing and channel mix, the final number stays easier to trace and update year after year.

Key Questions Answered in the Report

How large will Switzerland cosmetics products market size be by 2031?

It is projected to reach USD 571.78 million, up from USD 460.81 million in 2026.

Which segment grows fastest in the next five years?

Eye makeup outpaces others at a 4.76% CAGR through 2031.

Why are natural certifications important in Swiss beauty?

Seals like NATRUE and Bio Suisse justify 18-22% price premiums and secure consumer trust.

What drives premium sales momentum?

Clinically validated anti-aging actives and sustainable packaging spur a 5.65% CAGR for prestige items.

Page last updated on: