Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

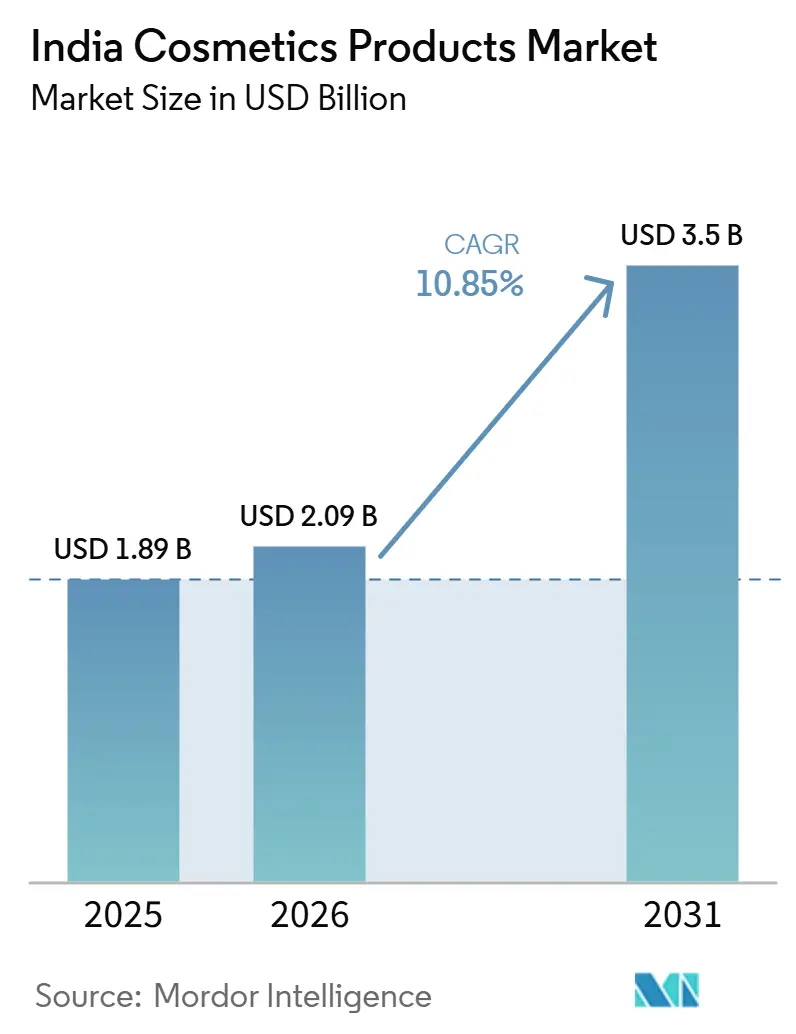

| Base Year Market Size (2025) | USD 1.89 Billion |

| Market Size (2026) | USD 2.09 Billion |

| Market Size (2031) | USD 3.5 Billion |

| Growth Rate (2026 - 2031) | 10.85% CAGR |

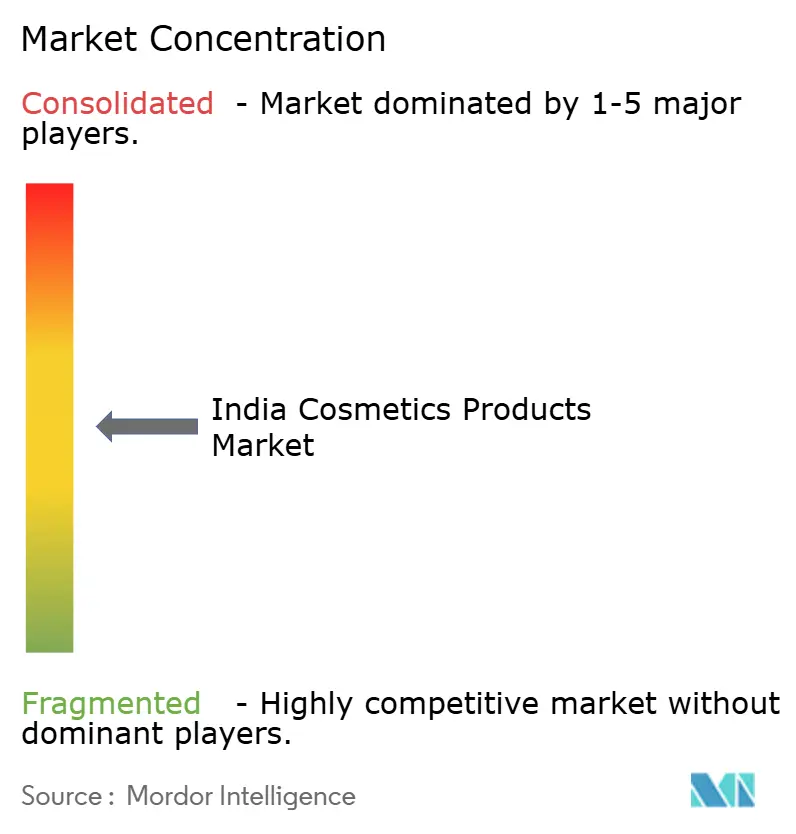

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Cosmetics Products Market Analysis by Mordor Intelligence

The India cosmetics products market size was valued at USD 1.89 billion in 2025 and estimated to grow from USD 2.09 billion in 2026 to reach USD 3.50 billion by 2031, at a CAGR of 10.85% during the forecast period (2026-2031). The pace easily exceeds the global beauty average, underscoring a structural rise in discretionary spending on personal appearance. Spending momentum is visible across income brackets because social media exposure, rising disposable incomes, and widespread urbanization have re-defined beauty as part of daily wellness rather than a luxury. Even within tight household budgets, beauty outlays receive priority, evidenced by the country recording the world’s highest percentage of consumers willing to spend more on cosmetics. Multinational and domestic brands are intensifying product launches to serve preferences for vegan formulas, clean labels, and affordable luxuries, while tightening regulatory oversight by the Central Drugs Standard Control Organization (CDSCO) and the Bureau of Indian Standards (BIS) raises compliance costs but improves consumer confidence. Together, these forces keep the India cosmetics products market on an expansion trajectory that shows no sign of plateauing.

Key Report Takeaways

- By product type, lip make-up held 36.12% of the Indian cosmetics products market share in 2025, while eye make-up is advancing at an 11.55% CAGR through 2031.

- By category, the mass segment captured 79.55% revenue share in 2025; the premium/luxury segment is projected to expand at a 12.55% CAGR to 2031.

- By distribution channel, online retail accounted for 30.95% of the Indian cosmetics products market size in 2025 and is growing at an 11.15% CAGR through 2031.

- By nature, the conventional segment held 88.74% of the Indian cosmetics products market share in 2025, while natural/organic products are projected to expand at a 12.17% CAGR through 2031.

- By region, the North commanded a 39.54% share of the Indian cosmetics products market in 2025, while the West is the fastest-growing at 11.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Cosmetics Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumisation and "Affordable-Luxury" demand surge | +2.8% | National, with early gains in North, West, and East regions | Medium term (2-4 years) |

| Increased awareness about personal grooming | +2.1% | National, stronger in urban areas and tier 2 cities | Short term (≤ 2 years) |

| Rising impact of social media and beauty trends | +1.9% | National, particularly strong in North and West regions | Short term (≤ 2 years) |

| Rise of vegan and cruelty-free cosmetics | +1.4% | National, with premium adoption in metropolitan areas | Medium term (2-4 years) |

| Growing male-grooming adoption in Gen-Z and Gen-Alpha households | +1.2% | National, with higher penetration in urban centers | Long term (≥ 4 years) |

| Brand expansion and product innovation | +1.1% | National, with focus on tier 2 and tier 3 city expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumisation and “Affordable-Luxury” demand surge

The cosmetics market in India is experiencing a significant transformation, driven by a surge in demand for premium and "affordable-luxury" products. This evolution is reshaping both consumer attitudes and industry trajectories. As beauty awareness grows and social media exerts its influence, the definition of luxury is being redefined. Notably, consumers from non-metro cities, once distant from high-end brands, are now actively pursuing them. This trend is underscored by Nykaa's revelation that 55% of prestige beauty sales in 2023 originated from these non-metro regions, signaling a democratization of luxury consumption [1]Source: Nykaa E-Retail Pvt. Ltd., "Nykaa Beauty Trends Report 2024", nykaa.com. The momentum is further bolstered by brand expansions, product innovations, and a rising preference for vegan and cruelty-free cosmetics, broadening the appeal of premium products beyond the traditional urban elite. Highlighting the shifting competitive landscape, international giants like L'Oréal are not just investing in local manufacturing but are also eyeing export opportunities. Today's consumers place a premium on organic and natural ingredients, and they're increasingly influenced by global trends, from K-beauty to clean beauty routines. This heightened awareness has amplified the value placed on product efficacy. Besides, modern shoppers are prioritizing authenticity and personalized experiences, viewing beauty products as essential lifestyle investments rather than mere discretionary purchases. Furthermore, regulatory shifts emphasizing ethical standards, combined with celebrity endorsements, are bolstering brand trust. In this digital age, where experiential shopping reigns, premium offerings have become strikingly accessible. This transformation is not just a fleeting trend; it's a fundamental shift in market dynamics, underscoring that in India's evolving beauty landscape, quality and experience are now paramount, overshadowing mere price considerations.

Increased awareness about personal grooming

The growing awareness of personal grooming is driving significant growth in the cosmetics products market in India, reshaping consumer behavior across demographics. Increased digital literacy and widespread social media penetration have made beauty education more accessible. Influencers such as Malvika Sitlani and Komal Pandey and brand-sponsored tutorials simplify complex makeup and skincare routines, reducing adoption barriers for both men and women. Urban youth are increasingly adopting advanced beauty regimens, expanding their preferences to include products like BB creams, concealers, and eyeshadows, moving beyond basic offerings. In metropolitan areas, Indian men dedicate more time to grooming, supported by evolving societal norms and the rise of male beauty influencers. Besides, corporate wellness programs and professional appearance standards further reinforce these habits, positioning grooming as a career-enhancing investment. Brands such as Lakme, Sugar Cosmetics, and Mamaearth are customizing products to suit Indian skin tones and climatic conditions, ensuring premium and innovative options are accessible even in smaller cities. Moreover, e-commerce platforms like Nykaa have democratized access to cosmetic products, driving rapid adoption and encouraging product experimentation across regions. Hence, influencer marketing has amplified the aspirational appeal of grooming, emphasizing inclusivity and authenticity. As personal grooming becomes an integral part of daily life, demand for cosmetic products remains strong, highlighting their essential role in the transformation of India's beauty landscape.

Rising impact of social media and beauty trends

The cosmetic products market has evolved significantly, with a social media user base of 462 million in 2024 in India, as per World Population Review, transforming consumer discovery and purchase patterns, as influencer content becomes a primary advertising channel [2]Source: World Population Review, "Social Media Users by Country 2025", worldpopulationreview.com . While influencer marketing investments now match traditional advertising spending, the industry faces a demographic challenge; despite women being the primary target market for beauty products, over 68% of beauty influencer followers are male, necessitating strategic adjustments in marketing approaches. Social media platforms, particularly Instagram and YouTube, have democratized beauty education across regions. Consumers in tier 2 and tier 3 cities now have equal access to makeup tutorials and techniques, accelerating product adoption cycles. This has enabled trending products, such as nude, red, and brown lipsticks from Maybelline and Nykaa, to achieve widespread market penetration within months. The market has seen significant growth in Korean beauty product demand, with Nykaa reporting increased sales for brands like COSRX and LANEIGE. However, new government regulations require virtual influencers to provide clear disclaimers, enhancing market transparency. The combination of social media monitoring and e-commerce growth has improved cosmetic products accessibility across regions, including remote areas. Furthermore, the market is expanding through increased male grooming product adoption. Brands like Sugar Cosmetics and Mamaearth have developed products specifically formulated for regional skin tones and weather conditions. The integration of social media content, user engagement, and rapid product development has established social platforms as key drivers of beauty trends in the cosmetic products market.

Rise of vegan and cruelty-free cosmetics

The demand for vegan and cruelty-free cosmetic products has increased as consumers align their beauty choices with ethical and environmental values. Consumers now prefer products with transparent ingredient lists and no animal testing. The Cosmetics Rules 2020, which prohibits animal testing, has strengthened the position of cruelty-free brands and prompted traditional companies to modify their product formulations. Companies like Juicy Chemistry and ayurvedic brands such as Forest Essentials, Just Herbs, and SoulTree have capitalized on the preference for natural ingredients. These brands use plant-based formulations that combine India's wellness heritage with modern clean beauty trends. Certifications from organizations like The Vegan Society and sustainable packaging initiatives have enhanced consumer trust in this market segment. Besides, the cosmetic products market now emphasizes ingredient sourcing, organic certification, and eco-friendly packaging to meet consumer demands for transparency. E-commerce platforms have improved access to vegan and cruelty-free cosmetics across urban and semi-urban India. Additionally, influencer marketing focused on ethical values has expanded the appeal of these products. This shift toward ethical beauty products indicates a broader change in consumer behavior. Indian consumers now carefully evaluate brand claims and seek products that align with their personal and cultural wellness preferences. This trend has compelled established brands to revise their formulations and marketing strategies to remain competitive in the cosmetic products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of counterfeit products | -1.8% | National, with higher impact in rural and tier 3 markets | Short term (≤ 2 years) |

| Reluctance to adopt new products due to skepticism about efficacy or safety | -1.1% | National, particularly strong in rural areas and among older demographics | Medium term (2-4 years) |

| Market saturation and intense competition | -0.9% | National, with highest intensity in metropolitan and tier 1 cities | Short term (≤ 2 years) |

| Limited penetration in rural markets | -1.2% | Rural India, particularly in East and North regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prevalence of counterfeit products

The counterfeit products in the cosmetic products market are expanding faster than the legitimate market, primarily due to inadequate enforcement and consumer price sensitivity. This issue is particularly severe in rural and semi-urban areas where brand authentication capabilities are limited. Companies, including Hindustan Unilever and L'Oréal, have invested in anti-counterfeiting technologies and work with law enforcement agencies to address this challenge. However, the vast and fragmented retail network makes monitoring difficult. The presence of counterfeit cosmetics containing harmful substances creates significant health risks, including allergies and infections, which diminishes consumer trust and damages authentic brand value. While e-commerce platforms have implemented authentication measures, traditional retail channels remain susceptible to counterfeit products. Common counterfeiting methods include repackaging diluted or expired products, with social media influencers unknowingly promoting questionable items. Market size, complex supply chains, and insufficient penalties impede regulatory enforcement, though organizations are implementing consumer awareness campaigns and using technologies like AI and blockchain to control counterfeiting. Recent seizures of counterfeit products imitating brands such as MAC, Lakmé, and Huda Beauty demonstrate the magnitude of this issue. Addressing this challenge requires enhanced collaboration between manufacturers, regulators, and law enforcement, along with improved consumer education about product authentication. The ongoing counterfeit trade impacts both public health and market development, representing a significant constraint for the cosmetic products market.

Limited penetration in rural markets

Limited penetration in rural markets presents a significant growth constraint for cosmetic products. This challenge stems from lower awareness, accessibility, and cultural acceptance compared to urban areas. While urban and metro cities have extensive organized retail outlets, specialty stores, and e-commerce presence, rural consumers encounter limited product variety and fewer physical stores. Cultural factors in rural regions restrict market growth, as makeup use remains largely associated with special occasions rather than daily grooming. Although companies like Lakme, Sugar Cosmetics, and Mamaearth have developed products suited to Indian skin tones and climate conditions to expand beyond urban centers, distribution and education gaps persist. Moreover, digital platforms like Nykaa are improving access and awareness in tier 2 and 3 cities. However, rural market penetration remains slow due to factors such as limited digital literacy, affordability concerns, the prevalence of counterfeit products, and consumer hesitation. Companies are implementing various strategies to address these challenges through enhanced product education initiatives, development of tailored formulations, strengthened rural supply chains, and partnerships with local retailers. While increasing exposure to social media and beauty influencers is gradually improving rural acceptance of cosmetic products, the current rural market share remains significantly lower than urban segments. This limited rural penetration continues to restrict the overall growth potential of the Indian cosmetic products market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Lip Products Drive Volume Growth

Eye make-up products are projected to grow at a robust 11.55% CAGR through 2031, driven by social media beauty trends and advancements in application techniques. Lip make-up products continue to dominate the market, holding a 36.12% share in 2025. The rapid growth in the eye segment is attributed to influencer-led tutorials that simplify complex application processes, making products like eyeliner, mascara, and kohl more accessible to a wider consumer base. Whereas, facial make-up products, including foundation and concealer, are benefiting from increasing professional appearance standards and the normalization of video conferencing, although their growth remains moderate compared to the eye and lip categories. Moreover, nail make-up products, while the smallest segment, maintain steady demand in urban markets, with nail polish and remover gaining popularity among younger demographics.

The leadership of lip products is driven by cultural preferences and ease of application. Traditional kohl and kajal usage patterns have seamlessly transitioned into modern formulations and packaging. Seasonal demand significantly impacts the product mix, with festive periods boosting premium lip color sales, while everyday use supports growth in the mass-market segment. BIS standards for cosmetic safety have strengthened consumer trust in both domestic and imported products, fostering premiumization trends across all product categories. The product innovation cycle has accelerated, with brands introducing hybrid formulations that combine skincare benefits with cosmetic products, addressing consumer demand for multifunctional products that simplify beauty routines.

By Category: Mass Market Sustains Premium Growth

The mass category commands an 79.55% market share in 2025. However, the premium/luxury segment is projected to grow at a 12.55% CAGR through 2031, signaling a bifurcated market where volume and value growth follow distinct trajectories. This premiumization trend reflects increasing disposable incomes and aspirational consumption patterns, which now extend beyond traditional affluent demographics to include middle-class households. Mass market brands sustain their dominance through extensive distribution networks and competitive pricing, with companies like Sugar Cosmetics targeting Gen Z consumers by offering affordable product ranges that emphasize functionality over prestige.

Premium/luxury segment growth is concentrated in metropolitan areas and tier 1 cities, where the presence of international brands and advanced retail infrastructure supports higher price points and sophisticated product offerings. The luxury segment benefits from omnichannel retail strategies, highlighting consumer preferences for experiential purchasing in premium categories. Brand positioning strategies have evolved to introduce affordable luxury sub-segments, bridging the gap between mass and premium categories and enabling companies to capitalize on upward mobility in consumer spending. This category segmentation reflects broader economic trends, where income inequality creates distinct consumption tiers with minimal overlap in brand preferences and purchasing behaviors.

By Distribution Channel: Digital Commerce Reshapes Retail

Online retail stores hold a 30.95% market share in 2025 and are projected to grow at an 11.15% CAGR through 2031. This shift is fundamentally reshaping traditional FMCG distribution patterns and introducing new competitive dynamics. The dominance of digital channels highlights a clear consumer preference: they prioritize product variety, competitive pricing, and unmatched convenience. Platforms such as Nykaa and Purplle are at the forefront, demonstrating that beauty-focused e-commerce can achieve both profitability and sustainability. While supermarkets/hypermarkets face challenges from online competition, they remain relevant by focusing on experiential retail. This strategy caters particularly to impulse purchases and trial-size products, offering immediate gratification. Pharmacies and drug stores capitalize on consumer trust in health and safety by positioning cosmetics alongside wellness products, effectively appealing to health-conscious consumers.

Specialty stores face intense competition from online platforms but sustain their presence through expert consultations and partnerships with premium brands, emphasizing personalized service and product education. The evolving distribution landscape reflects a broader transformation in retail, where omnichannel strategies are critical for achieving market leadership. Brands that succeed maintain a presence across all channels while tailoring their approach to channel-specific consumer behaviors. Quick commerce has emerged as a significant growth driver. In 2024, Nykaa reported that 70% of orders in major cities are delivered within a day, redefining consumer expectations for convenience and speed . This transformation in distribution is also democratizing access to premium and international brands. Consumers in smaller cities now have access to the same product range as those in metropolitan areas, accelerating market homogenization and standardizing brands across diverse geographic segments.

By Nature: Conventional Products Face Organic Challenge

The natural/organic products segment is projected to grow at a CAGR of 12.17% through 2031, challenging the conventional segment's dominant 88.74% market share in 2025. This growth is driven by increasing consumer awareness of ingredient safety and environmental sustainability. The expansion of the organic segment aligns with broader wellness trends, as consumers demand transparency in product formulations and prefer brands that align with health-conscious values. Ayurvedic and herbal brands such as Forest Essentials and Kama Ayurveda have achieved international recognition, leveraging India's traditional knowledge systems to support global expansion strategies. Additionally, the Cosmetics Rules 2020 have clarified regulations for natural and organic claims, reducing consumer confusion and strengthening authentic brand positioning.

Conventional products maintain their dominance due to established supply chains, proven efficacy, and competitive pricing, particularly in cost-sensitive mass market segments. The regulatory framework under CDSCO ensures safety standards for both conventional and natural products, creating a level playing field where efficacy and consumer preferences drive market success. Innovations in natural product formulations have enhanced performance, addressing the traditional trade-off between natural ingredients and product effectiveness. As market dynamics evolved, conventional brands launched natural sub-lines, while organic brands expanded into conventional categories to access broader market opportunities.

Geography Analysis

The North region captures a dominant 39.54% share of the market in 2025, underscoring the purchasing power concentrated in Delhi NCR and its neighboring urban hubs. Here, rising disposable incomes and a cultural inclination towards beauty experimentation fuel a steady demand surge. The North's established retail infrastructure and its closeness to import hubs grant it swift access to global brands and the latest product innovations. Meanwhile, the West, boasting a 11.82% CAGR projected through 2031, signals a shift in growth dynamics. Mumbai's financial sector is birthing affluent consumers, increasingly drawn to premium and luxury cosmetics. This Western surge mirrors urbanization trends and a corporate culture that embraces grooming investments, transcending gender and age boundaries.

Eastern India challenges traditional demographic assumptions, accounting for over a third of the nation's cosmetic sales, despite representing less than a quarter of Indian households. This anomaly points to heightened per capita consumption and a deep-rooted cultural affinity for beauty products. Consumption trends in the East highlight the weight of cultural nuances and social norms in driving cosmetic adoption, overshadowing mere economic metrics. In the South, steady growth is buoyed by a blend of educational achievements and a thriving tech sector, fostering a discerning consumer base that prioritizes brand efficacy and safety. Enforcement of regional regulatory compliance varies, with metropolitan areas adhering more rigorously to CDSCO standards. In contrast, rural and semi-urban markets grapple with challenges like counterfeit prevention and quality assurance. A closer look at the geography reveals that successful market expansion hinges on tailored strategies, attuned to cultural nuances, income trends, and retail infrastructure, rather than a one-size-fits-all national approach. Companies such as Purplle have adeptly navigated this landscape, deriving nearly half their revenue from over 78 cities, with a keen focus on tier 2 and tier 3 locales boasting household incomes between Rs 5-30 lakh. These regional dynamics underscore the importance of aligning growth strategies with cultural insights and local consumer behaviors, rather than relying solely on demographic data.

Competitive Landscape

The competitive landscape of the Indian cosmetic products market is moderately fragmented, with global leaders like L'Oréal and Estée Lauder competing against agile domestic brands such as Sugar Cosmetics and Colorbar. Multinational corporations focus on premiumization and urban market dominance by leveraging brand equity and innovation capabilities, while domestic players utilize cultural insights and affordability to penetrate tier 2 and 3 cities. This dual strategy fosters a competitive environment that presents opportunities for consolidation and new entrants targeting distinct consumer segments.

Technology adoption has emerged as a critical differentiator in this evolving market. Companies are heavily investing in AI-driven personalization, augmented reality (AR) virtual try-ons, and rapid commerce solutions to enhance customer experiences and optimize operations. Digital innovators like Nykaa have pioneered these advancements, enabling consumers in both urban and emerging markets to interact with products before purchase. This approach increases trust, reduces trial barriers, and enhances customer satisfaction. Additionally, these technologies provide real-time consumer insights, allowing companies to tailor offerings to local preferences and accelerate product adoption.

Regulatory frameworks established by the Central Drugs Standard Control Organization (CDSCO) and Bureau of Indian Standards (BIS) enforce stringent quality and safety standards, creating entry barriers that favor established players with robust compliance mechanisms. These regulations safeguard consumer interests and uphold market integrity. Companies that focus on consumer education and expand organized retail in underserved tier 2 and 3 cities can unlock significant growth potential. Moreover, brands emphasizing sustainability, ethical sourcing, and personalized solutions are well-positioned to gain competitive advantages in India's rapidly growing cosmetic products sector.

India Cosmetics Products Industry Leaders

-

L'Oréal SA

-

The Estée Lauder Companies Inc.

-

Unilever PLC

-

FSN E-Commerce Ventures Ltd (Nykaa)

-

Vellvette Lifestyle Pvt. Ltd. (Sugar Cosmetics)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Rihanna's beauty label, Fenty, entered into an exclusive partnership with Reliance Retail. This collaboration enabled the launch of Fenty's makeup and skincare lines at Sephora India and Tira Beauty. Fenty Beauty and Fenty Skin products became available both online and across Tira Beauty and Sephora India's 50 outlets in 16 cities.

- April 2025: Ananya Birla launched LOVETC, a new cosmetic products brand, marking the Aditya Birla Group's deeper entry into India's rapidly growing cosmetic market. Initially, consumers could access LOVETC on its dedicated direct-to-consumer platform and Nykaa's online store. Additionally, the brand had outlined plans for a phased retail rollout, targeting 200 stores across 20 prominent cities in India.

- February 2025: Pradeep Banerjee, a former executive director at Hindustan Unilever, and Nabeel Kadri, founder of the celebrity endorsement agency Median, introduced 'Hyue', a premium cosmetic products brand designed to meet Indian consumer preferences. Hyue commenced its retail operations with a direct-to-consumer e-commerce platform, targeting shoppers across India. The brand's initial cosmetics line included liquid lipsticks, gel nail paints, lip treatments, and lip oils, all of which were vegan and cruelty-free.

India Cosmetics Products Market Report Scope

Cosmetic is applied to conceal blemishes and enhance one's natural features, such as the eyebrows and eyelashes.

India's cosmetics market is segmented by product type and distribution channel. The market is segmented by product type into color cosmetics and hair styling and coloring products. The color cosmetics segment is further sub-segmented into facial, eye, and lip and nail make-up products. The hair styling and coloring products segment is further bifurcated into hair colors and hair styling products. The market is segmented by distribution channel into supermarkets/hypermarkets, specialty stores, pharmacies/drug stores, online retail stores, and other distribution channels.

For each segment, the market sizing and forecasts have been done based on value (in USD).

By Product Type

| Facial Make-Up Products | Foundation and Concealer | Compact and Pressed Powder |

| Blush and Highlighter | ||

| Others | ||

| Eye Make-Up Products | Kohl and Kajal | |

| Eyeliner | ||

| Mascara | ||

| Others | ||

| Lip Make-Up Products | Lipsticks | |

| Lip Gloss | ||

| Others | ||

| Nail Make-Up Products | Nail Polish | |

| Nail Polish Remover | ||

| By Category | Mass | |

| Luxury | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies/Drug Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Nature | Conventional | |

| Natural/Organic | ||

| By Region | East | |

| West | ||

| North | ||

| South | ||

| By Product Type | Facial Make-Up Products | Foundation and Concealer | Compact and Pressed Powder |

| Blush and Highlighter | |||

| Others | |||

| Eye Make-Up Products | Kohl and Kajal | ||

| Eyeliner | |||

| Mascara | |||

| Others | |||

| Lip Make-Up Products | Lipsticks | ||

| Lip Gloss | |||

| Others | |||

| Nail Make-Up Products | Nail Polish | ||

| Nail Polish Remover | |||

| By Category | Mass | ||

| Luxury | |||

| By Distribution Channel | Supermarkets/Hypermarkets | ||

| Pharmacies/Drug Stores | |||

| Specialty Stores | |||

| Online Retail Stores | |||

| Other Distribution Channels | |||

| By Nature | Conventional | ||

| Natural/Organic | |||

| By Region | East | ||

| West | |||

| North | |||

| South | |||

Key Questions Answered in the Report

How fast is the India cosmetics products market expected to grow to 2031?

The market is projected to rise from USD 2.09 billion in 2026 to USD 3.50 billion by 2031, posting a 10.85% CAGR.

Which product type holds the largest share today?

Lip make-up dominates with 36.12% share in 2025, driven by high cultural acceptance and everyday usage.

What channel is expanding the quickest?

Online retail, already at 30.95% share, is advancing at an 11.15% CAGR because of wide assortment, convenience, and rapid delivery.

Why is the premium segment gaining momentum?

Rising disposable income and affordable luxury positioning are pushing premium and luxury cosmetics at a 12.55% CAGR through 2031.

Page last updated on: