Precipitated Calcium Carbonate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

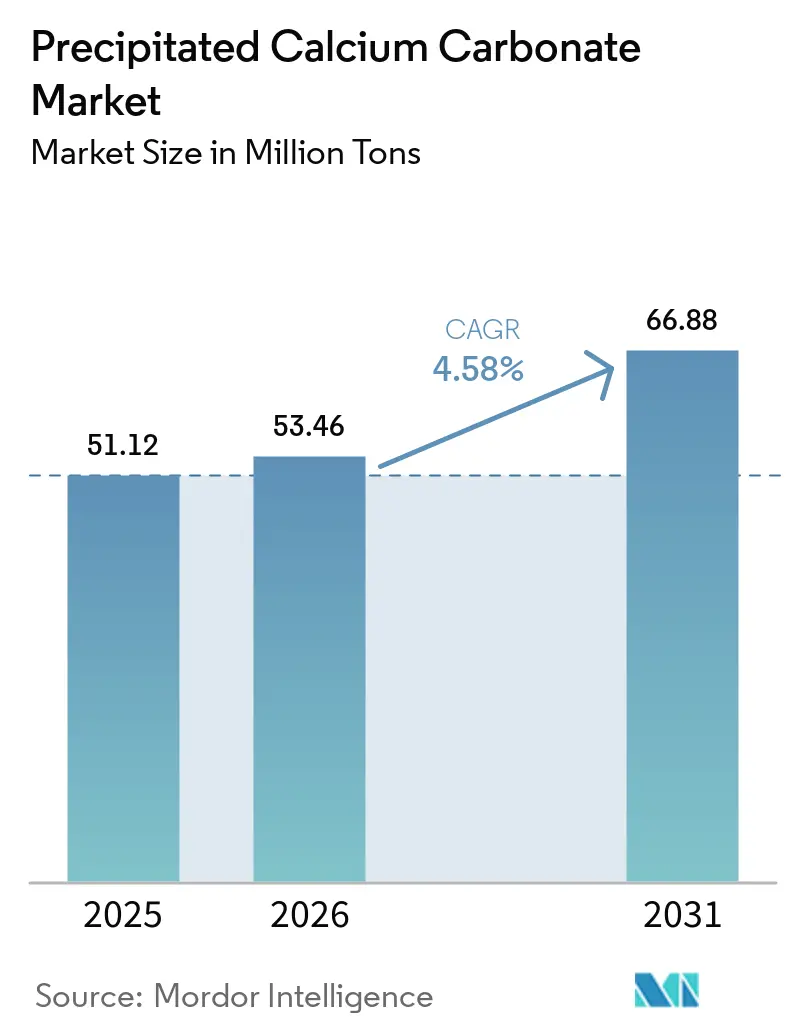

| Market Volume (2026) | 53.46 Million tons |

| Market Volume (2031) | 66.88 Million tons |

| Growth Rate (2026 - 2031) | 4.58% CAGR |

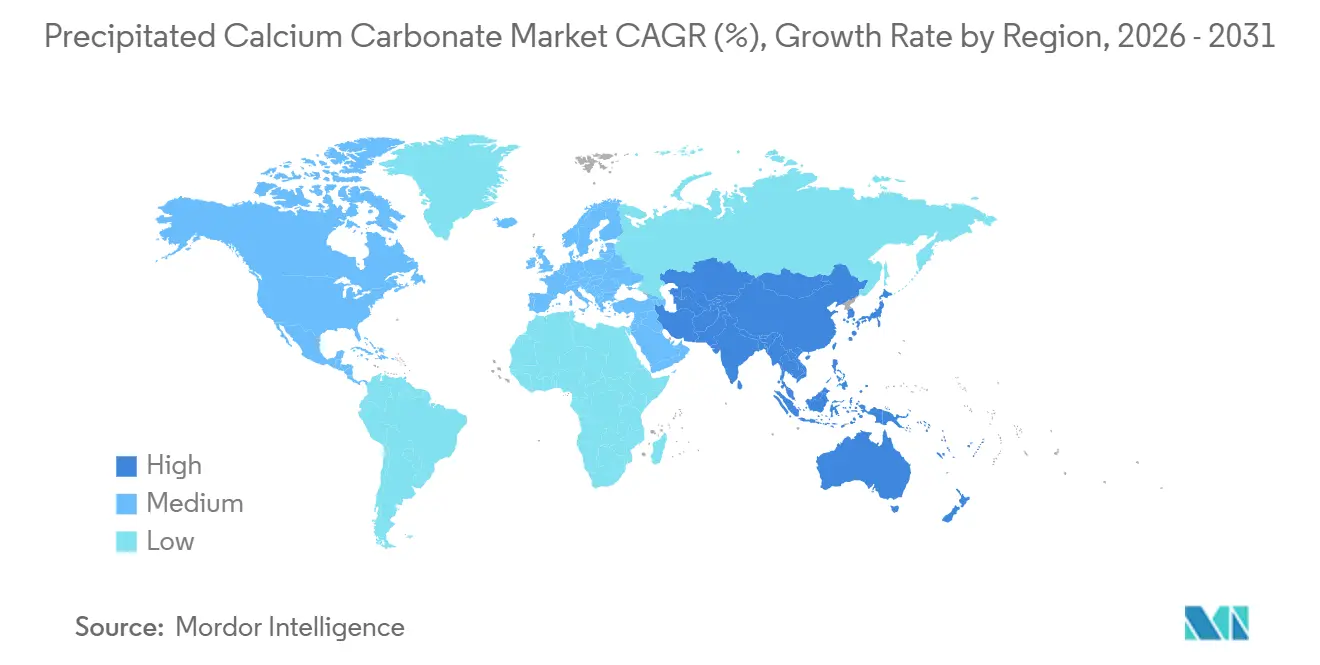

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Precipitated Calcium Carbonate Market Analysis by Mordor Intelligence

The Precipitated Calcium Carbonate Market size is projected to be 51.12 million tons in 2025, 53.46 Million tons in 2026, and reach 66.88 million tons by 2031, growing at a CAGR of 4.58% from 2026 to 2031. Long-term growth is anchored in carbon-capture utilization processes that lower the product’s embedded emissions, while nano-scale grades lift functional performance in premium paper, plastics, and pharmaceutical uses. Volume leadership remains with paper and paperboard, yet life-science demand for United States Pharmacopeia (USP)–grade material is gaining momentum as regulatory frameworks tighten around excipient purity. Asia-Pacific’s integrated limestone-to-PCC supply chains, especially in China and India, keep regional costs low and encourage on-site satellite plants that slash transport emissions. Meanwhile, North America and Europe focus on specialty PCC for lightweighting plastics and low-VOC coatings to meet stricter environmental mandates.

Key Report Takeaways

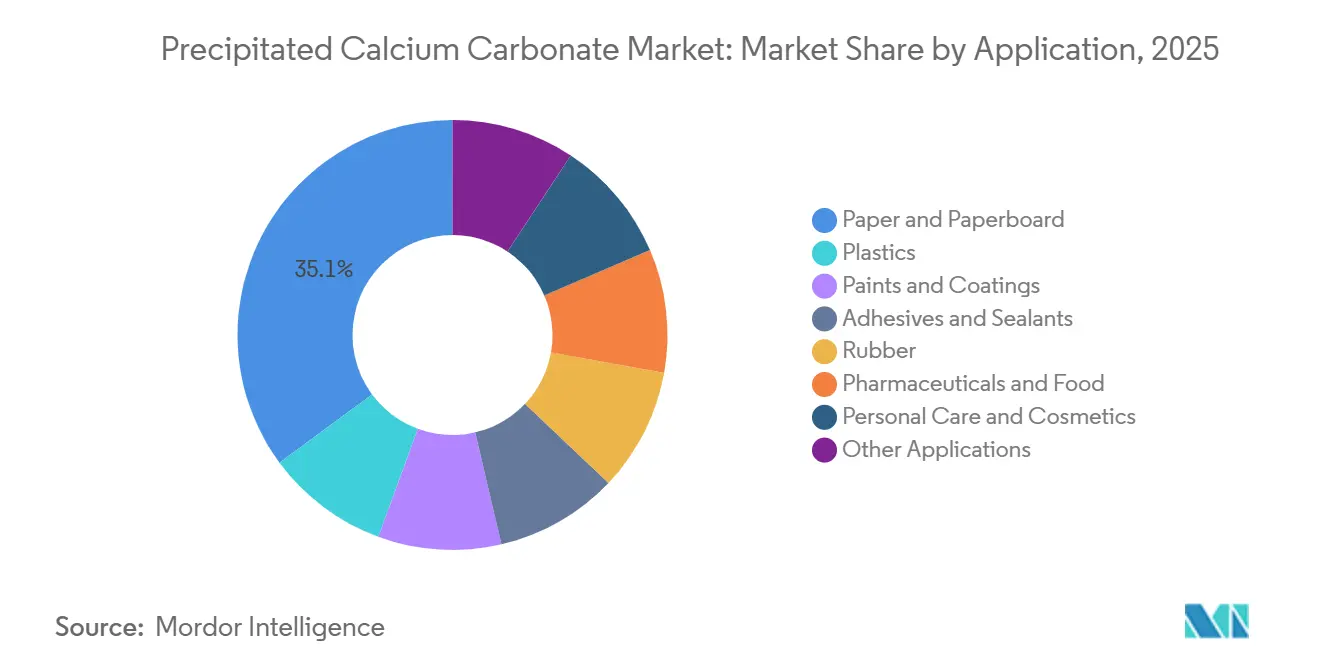

- By application, paper and paperboard captured 35.12% precipitated calcium carbonate market share in 2025, while pharmaceuticals and food applications are projected to post a 6.77% CAGR during the forecast period (2026-2031).

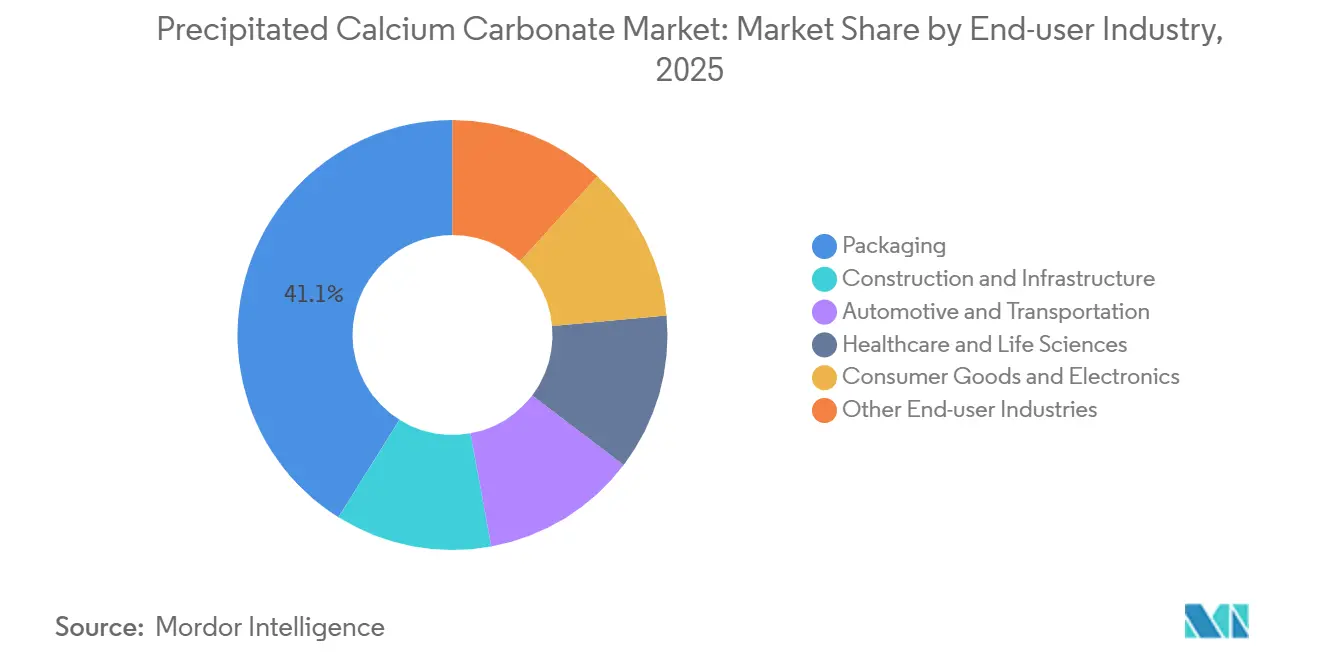

- By end-user industry, packaging accounted for 41.11% share of the precipitated calcium carbonate market size in 2025; healthcare and life sciences are set for a 5.23% CAGR during the forecast period (2026-2031).

- By geography, Asia-Pacific held 40.25% precipitated calcium carbonate market share in 2025 and is forecast to expand at a 5.05% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Precipitated Calcium Carbonate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from premium paper grades | +1.2% | Asia-Pacific, North America | Medium term (2-4 years) |

| High-fill plastics for lightweighting | +1.0% | Global automotive and packaging hubs | Medium term (2-4 years) |

| Regulatory push for VOC-free coatings | +0.8% | North America, Europe | Short term (≤ 2 years) |

| Carbon-negative PCC via CCU | +0.6% | Early adoption in North America, Europe | Long term (≥ 4 years) |

| Nano-PCC improves opacity in recycled paper | +0.5% | Asia-Pacific core, expanding to Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand From Premium Paper Grades

Brand owners are shifting toward high-opacity packaging and coated paper that rely on scalenohedral PCC to maximize light scattering, enabling filler loadings above 25% without sacrificing strength. Laboratory handsheets containing xylan-modified PCC showed brightness and opacity gains alongside improved burst and tear strength, letting mills downgrade fiber while protecting print quality. In Asia, where recycled-fiber loops dominate, nano-PCC replaces optical brightening agents that fade under UV, supporting cost-effective brightness control. Pilot trials using marble-waste-derived PCC achieved water contact angles of 103.3°, enhancing hydrophobicity for food wrappers. These results confirm that next-generation PCC provides aesthetic and sustainability benefits that pure fiber cannot match.

High-Fill Plastics for Lightweighting

Automotive and packaging converters incorporate up to 40% PCC masterbatch to curb resin costs and lower part weight, directly improving fuel economy. Polypropylene composites with 40% ground PCC posted a 69% rise in Young’s modulus, though designers balance stiffness with ductility through particle-size control. Omya’s Smartfill modified PCC sustained intrinsic viscosity in PET at 0.74 dL/g versus 0.61 dL/g for commodity PCC, boosting bottle top-load 40% at 5% filler, and enabling titanium dioxide cuts. Glass-fiber-epoxy parts filled with 6 wt% PCC reached 130.58 MPa tensile strength, opening pathways for lighter body panels in electric vehicles. Rising North American vehicle output of 15.5 million units in 2024, with 429 lb of plastics per car, underlines the latent plastics filler pull.

Regulatory Push for VOC-Free Paints and Coatings

The United States Environmental Protection Agency’s January 2025 aerosol-coatings rule tightened reactivity limits, accelerating the switch to waterborne formulations that rely on low-oil-absorption PCC for viscosity control[1]United States Environmental Protection Agency, “National VOC Emission Standards for Aerosol Coatings,” epa.gov. Stearic-acid-coated PCC disperses smoothly in high-solids paints, reducing titanium dioxide by up to 10% while maintaining hiding power, as demonstrated in independent formulation studies. California’s less than 50 g/L VOC threshold for architectural coatings and the EU’s similar ceilings expand PCC demand as formulators avoid high-reactivity solvents. Processors value PCC’s inert chemistry that avoids ozone-forming reactions and supports eco-labels such as LEED (Leadership in Energy and Environmental Design) and European Union (EU) Ecolabel.

Carbon-Negative PCC via CCU Routes

Pilot lines mineralizing industrial CO₂ streams into nano-PCC show crystallite sizes down to 45 nm, with reaction times cut nearly 50% in rotating-packed-bed reactors relative to stirred tanks. Phosphogypsum conversion recovers 99% of active calcium, producing 72 nm particles at 87.79% purity, diverting waste from landfills and embedding negative carbon intensity into the product. Aqueous-ammonia capture combined with recycled concrete aggregates stored 70.5 g CO₂ per kg aggregate per hour at costs below USD 11.06 per ton of product, undercutting European carbon-price levels. United States Steel and CarbonFree broke ground on a commercial SkyCycle unit in Gary, Indiana, in 2025, paving the way for large-scale Carbon Capture and Utilization (CCU)-based PCC in paints, plastics, and food applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limestone price volatility and availability | -0.7% | Regions dependent on imported feedstock | Short term (≤ 2 years) |

| Energy-intensive calcination and CO₂ footprint | -0.5% | Europe and North America under carbon-pricing regimes | Medium term (2-4 years) |

| PFAS scrutiny on fluorinated modifiers | -0.3% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limestone Price Volatility and Availability

The United States Geological Survey pegged lime output at 420 million tons in 2024, 72% of it from China, heightening concentration risk for importers[2]U.S. Geological Survey, “Mineral Commodity Summary: Lime,” usgs.gov. Quicklime prices rose to USD 190 per ton in 2024 as quarry permits tightened and fuel surcharges widened. High-purity deposits suitable for pharma-grade PCC are geographically scarce, forcing specialty producers to invest in beneficiation that stretches payback periods.

Energy-Intensive Calcination and CO₂ Footprint

Traditional kilns emit roughly 0.2 ton CO₂ per ton of PCC produced, clashing with net-zero pledges. EU ETS carbon prices of USD 80 per ton CO₂ in 2025 inflate cash costs, squeezing margins for European plants that rely on natural-gas-fired kilns. Electrified calciners and green-hydrogen pilots show promise but remain capital-heavy at industrial scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Pharmaceuticals Outpace Paper’s Volume Dominance

Global paper and paperboard retained 35.12% of 2025 volume as PCC fillers improved brightness and reduced fiber, a critical cost lever for mills. Nonetheless, pharmaceuticals and food applications are projected to grow at 6.77% CAGR, leveraging USP-grade purity to tap higher margins. Plastics applications, spanning Rigid Packaging, Flexible Films, and engineering resins, are expanding as lightweighting mandates and resin-cost inflation drive higher filler loadings, with surface-modified grades enabling 20-40% polymer substitution without sacrificing mechanical integrity.

Specialty excipient demand rests on clear United States FDA GRAS status under 21 CFR 184.1191 and color-additive exemptions that simplify global filings, creating barriers to entry. Controlled-release microspheres, imaging agents, and alginate, PCC hybrid carriers illustrate how particle engineering extends PCC beyond traditional antacid roles. Paper applications still anchor bulk tonnage, yet pricing power tilts toward trace-element-controlled, sub-micron grades that offer performance impossible for commodity fillers.

By End-User Industry: Healthcare Margins Offset Packaging’s Scale

Packaging absorbed 41.11% of global volume in 2025 as converters use PCC to reduce resin costs in rigid containers and flexible films without eroding mechanical integrity, accounting for the largest precipitated calcium carbonate market share within end uses. At the same time, healthcare and life-sciences applications, although smaller, log the highest growth at 5.23% CAGR during the forecast period (2026-2031), benefiting from stringent regulatory standards that lock in higher selling prices.

Automotive and transportation rely on high-fill polymer composites to trim vehicle weight, while construction employs PCC in cement and gypsum to improve rheology and strength. Consumer electronics and appliances adopt PCC for dimensional stability and flame-retardant synergy in casings and wire insulation. Diversified uptake balances cyclical risks and underscores the adaptability inherent in crystal-engineered PCC grades.

Geography Analysis

Asia-Pacific held 40.25% of global volume in 2025 and is forecast to expand at 5.05% CAGR through 2031. Minerals Technologies Inc. opened three new on-site PCC satellites in 2026 to serve Chinese and Indian paper mills, shrinking freight emissions and capturing just-in-time supply advantages. Japan and South Korea target nano-scale PCC for electronics and pharma, leveraging precise process control, while Vietnam and Indonesia welcome foreign direct investment in plastics compounding that lifts regional consumption. India’s packaging sector, propelled by e-commerce and food safety mandates, escalates demand for coated PCC that meets Bureau of Indian Standards purity benchmarks.

In North America, Domtar and Omya’s Wisconsin on-site plant, commissioned in 2024, recycles CO₂ from the mill’s lime kiln to make 27,500 dry tons per year of PCC, lowering annual transport emissions by 15,000 short tons CO₂-equivalent. Automotive lightweighting in the United States and Mexico maintains demand for modified PCC in polypropylene, polyethylene, and polyamide parts. CarbonFree’s SkyCycle project at United States Steel Gary brings the first large-scale Carbon Capture and Utilisation (CCU)-based PCC supply to North America, aligning with corporate climate targets and potentially capturing premium pricing from sustainability-focused buyers.

Europe, mixes strict environmental policy with mature demand in paints, coatings, and pharmaceuticals. European Union (EU) VOC (Volatile Organic Compound) ceilings, REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulations, and the looming PFAS (per- and polyfluoroalkyl substances) phase-out accelerate reformulation, steering formulators toward low-oil-absorption, non-fluorinated PCC grades. Germany leads automotive composites uptake, the United Kingdom advances in dietary supplements, and France and Italy anchor architectural-coating volumes. Outside the Big-Three regions, Brazil, Saudi Arabia, and South Africa post double-digit growth off small bases, though feedstock and logistics constraints moderate near-term scale-up.

Competitive Landscape

The Precipitated Calcium Carbonate market is moderately concentrated. Strategic alliances between PCC suppliers and paper or polymer producers foster captive demand, embedding long-term supply agreements that insulate both sides from feedstock and freight volatility. Consolidation remains modest because limestone deposits are geographically dispersed, and local regulations shape quarry economics differently. The precipitated calcium carbonate industry, therefore, balances global R&D scale and local sourcing advantages in an ecosystem that rewards technical differentiation and supply-chain integration.

Precipitated Calcium Carbonate Industry Leaders

Imerys

Omya

Minerals Technologies Inc.

Mississippi Lime Company d/b/a MLC

J.M. Huber Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Domtar’s Nekoosa mill inaugurated a new on-site PCC plant with Omya to restore Wisconsin supply integrity after a 2020 regional closure.

- July 2024: Imerys completed the divestiture of its Artemyn paper-sector assets for nearly EUR 150 million, reallocating resources to higher-margin specialty minerals.

Global Precipitated Calcium Carbonate Market Report Scope

Precipitated Calcium Carbonate (PCC) is a high-purity, synthetic white powder produced by calcining limestone and carbonating the resulting lime, known for its controlled particle size and high brightness. It is widely used as a functional filler in paper, plastics, rubber, paints, and pharmaceuticals to improve opacity, brightness, and durability.

The Precipitated Calcium Carbonate market is segmented by application, end-user industry, and geography. By application, the market is segmented into paper and paperboard, plastics, paints and coatings, adhesives and sealants, rubber, pharmaceuticals and food, personal care and cosmetics, and other applications. By end-user industry, the market is segmented into packaging, construction and infrastructure, automotive and transportation, healthcare and life sciences, consumer goods and electronics, and other end-user industries. The report also covers the market size and forecasts for Precipitated Calcium Carbonate in 17 countries across major regions. The market sizes and forecasts are provided in terms of volume (tons).

| Paper and Paperboard | |

| Plastics | Rigid Packaging |

| Flexible Films | |

| Paints and Coatings | |

| Adhesives and Sealants | |

| Rubber | |

| Pharmaceuticals and Food | |

| Personal Care and Cosmetics | |

| Other Applications |

| Packaging |

| Construction and Infrastructure |

| Automotive and Transportation |

| Healthcare and Life Sciences |

| Consumer Goods and Electronics |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Paper and Paperboard | |

| Plastics | Rigid Packaging | |

| Flexible Films | ||

| Paints and Coatings | ||

| Adhesives and Sealants | ||

| Rubber | ||

| Pharmaceuticals and Food | ||

| Personal Care and Cosmetics | ||

| Other Applications | ||

| By End-user Industry | Packaging | |

| Construction and Infrastructure | ||

| Automotive and Transportation | ||

| Healthcare and Life Sciences | ||

| Consumer Goods and Electronics | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What CAGR is expected for the precipitated calcium carbonate market through 2031?

The precipitated calcium carbonate market is projected to grow at 4.58% CAGR between 2026 and 2031.

Which region adds the most incremental PCC volume before 2031?

Asia-Pacific, driven by integrated Chinese and Indian supply chains and new satellite plants, is forecast at 5.05% CAGR during the forecast period (2026-2031).

Why are pharmaceuticals a fast-growing PCC application?

Regulatory clarity from US Pharmacopeia (USP) and Food and Drug Administration (FDA) for excipient and fortification use supports a 6.77% CAGR during the forecast period (2026-2031), the highest among applications.

How do CCU routes affect PCC competitiveness?

Carbon-capture mineralization produces carbon-negative PCC that can match conventional costs where carbon pricing is in force, offering new supply pathways.

What is the current market size of Precipitated Calcium Carbonate Market?

The Precipitated Calcium Carbonate Market size was valued at 51.12 Million tons in 2025 and is estimated to grow from 53.46 Million tons in 2026 to reach 66.88 Million tons by 2031, at a CAGR of 4.58% during the forecast period (2026-2031).

Page last updated on: