Calcium Propionate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

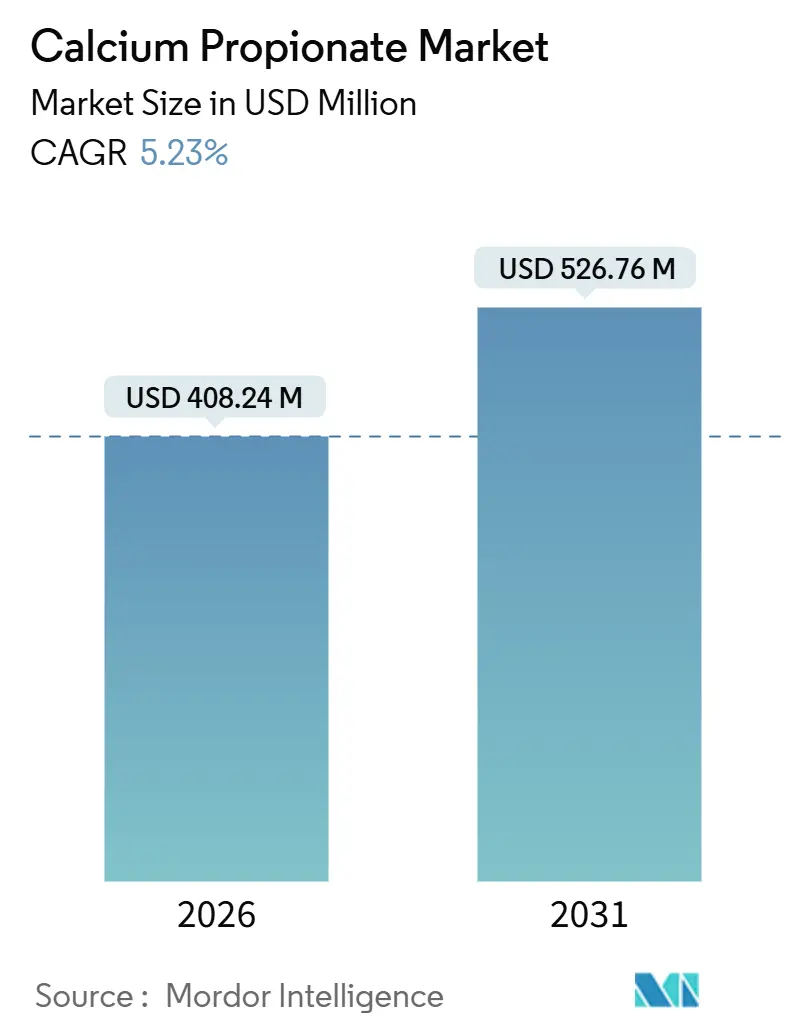

| Market Size (2026) | USD 408.24 Million |

| Market Size (2031) | USD 526.76 Million |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

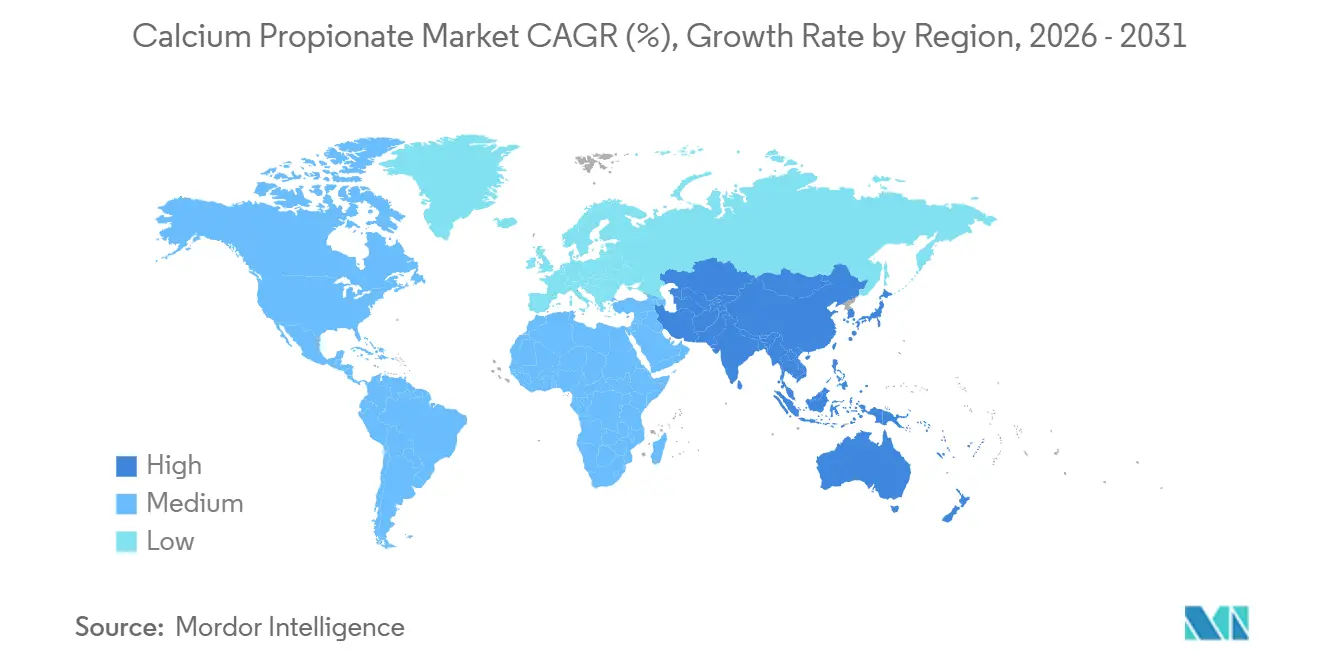

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

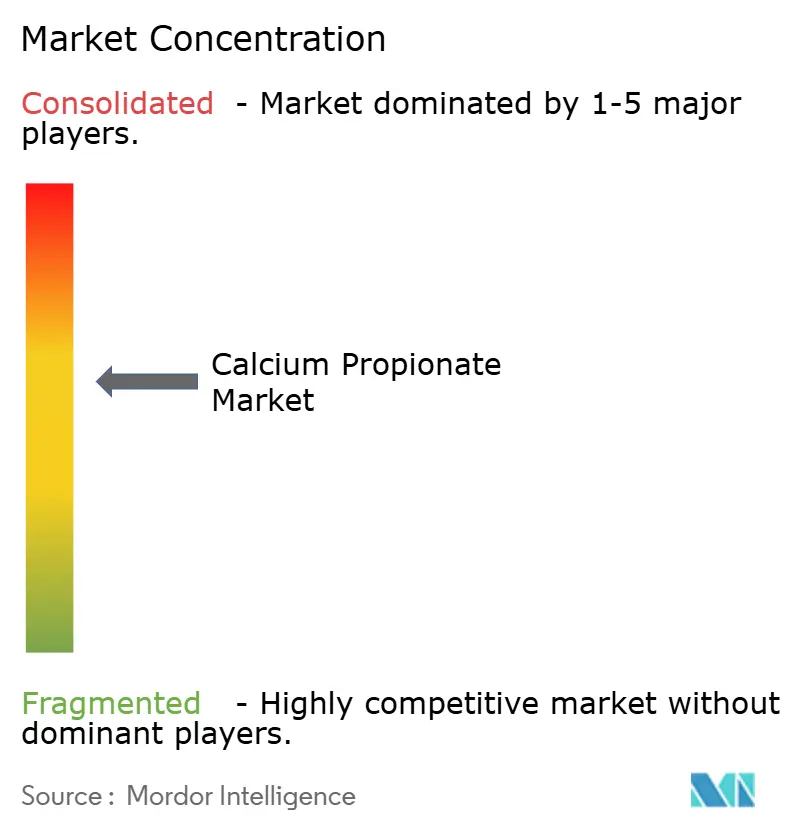

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Calcium Propionate Market Analysis by Mordor Intelligence

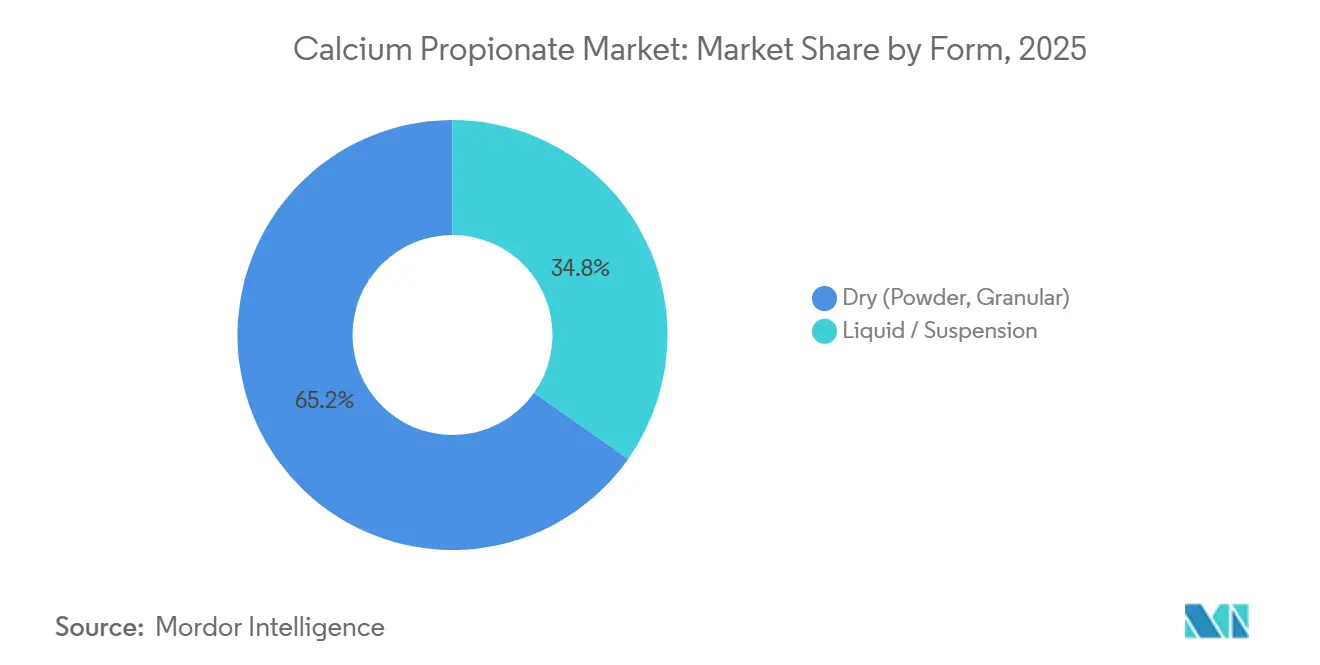

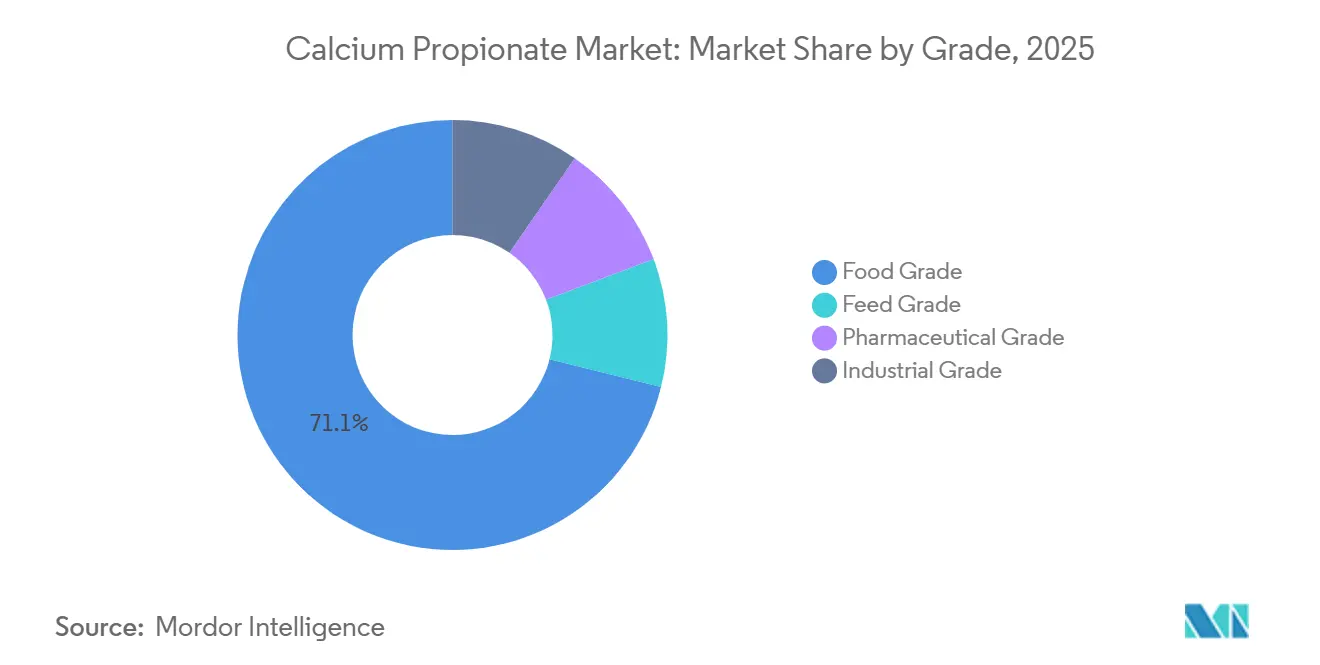

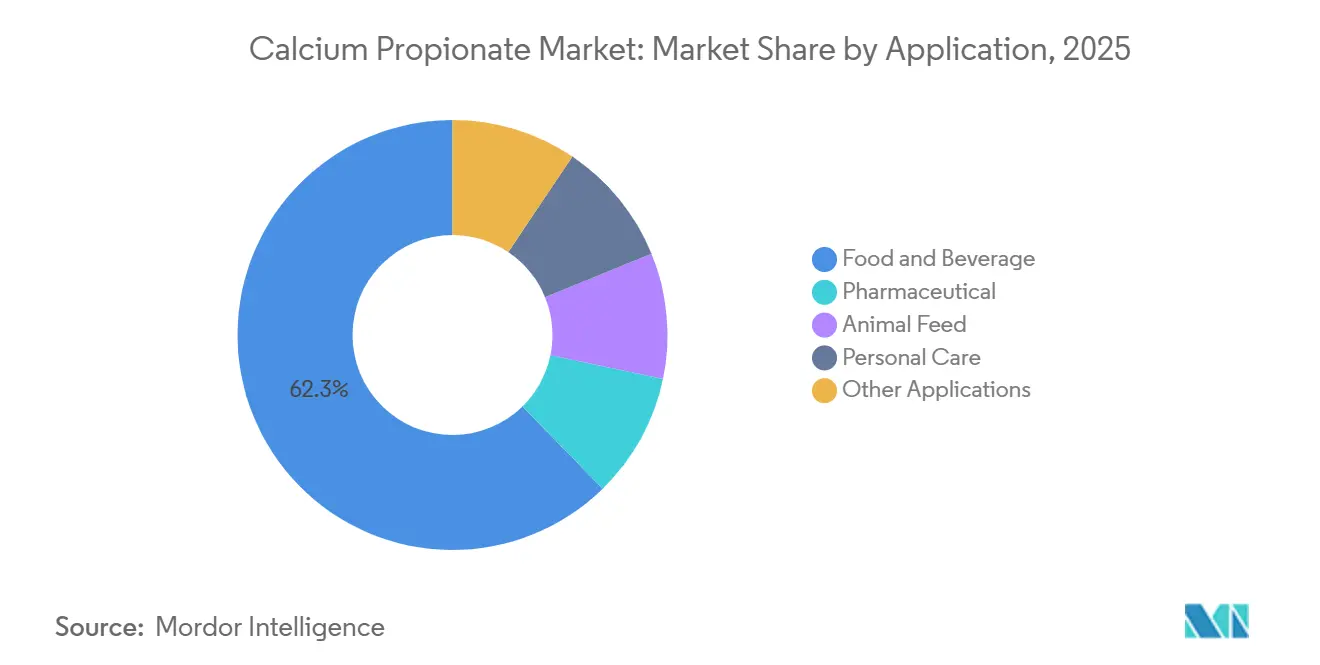

The Calcium Propionate Market size is estimated at USD 408.24 million in 2026, and is expected to reach USD 526.76 million by 2031, at a CAGR of 5.23% during the forecast period (2026-2031). Momentum rests on industrial bakeries and feed producers that balance longer shelf life with demand for cleaner labels, cost-effective preservation and consistent regulatory acceptance across regions. Dry form, valued for proven handling economics, retained 65.22% revenue share in 2025, while liquid/suspension will expand at 5.68% CAGR thanks to precision-dosing systems in automated bakery lines and aquaculture feed mills. Food-grade dominated with 71.12% of 2025 sales, yet pharmaceutical grade is the fastest mover at 6.24% CAGR as film-coated excipients mask the salt’s inherent odor in tablets. Regionally, North America contributed 40.23% of 2025 revenue due to U.S. bakery chain demand and long-standing FDA GRAS status, whereas Asia-Pacific is accelerating at 5.98% CAGR following China’s GB 2760-2024 standard that harmonizes allowable use levels and simplifies nationwide formulations. Supply-side consolidation by BASF-YPC and Perstorp, plus emerging bio-based propionic acid routes, is reshaping competitive strategies even as feedstock cost volatility continues to squeeze margins for smaller producers.

Key Report Takeaways

- By form, dry held 65.22% of calcium propionate market share in 2025, whereas liquid/suspension will grow fastest at a 5.68% CAGR to 2031.

- By grade, food-grade captured 71.12% revenue share in 2025; pharmaceutical grade is on track to register a 6.24% CAGR through 2031.

- By application, food and beverage led with 62.34% share in 2025, while animal feed is poised to expand at a 5.89% CAGR during 2026-2031.

- By geography, North America commanded 40.23% revenue in 2025; Asia-Pacific is the quickest regionally with a 5.98% CAGR set to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Calcium Propionate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial-Scale Asia-Pacific Bakeries Raising Mold-Inhibitor Uptake | +1.4% | China, India, ASEAN core, spill-over to South Korea and Japan | Medium term (2-4 years) |

| European Union Approval in Aquaculture Diets Widens Feed Demand | +0.9% | Europe (primary), North America (secondary adoption) | Long term (≥ 4 years) |

| GCC Convenience-Food Retail Boom Requiring Longer Shelf Life | +0.7% | Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman | Short term (≤ 2 years) |

| Electro-Synthetic Bio-Based Propionic Acid Routes Lowering Scope-3 Emissions | +1.1% | Global, with early adoption in EU and North America | Long term (≥ 4 years) |

| Micro-Encapsulated Calcium Propionate Enabling pH-neutral "No-Off-Taste" Dairy | +0.8% | North America, Europe, premium dairy segments in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Industrial-Scale Asia-Pacific Bakeries Raising Mold-Inhibitor Uptake

China’s GB 2760-2024 permits up to 2.5 g/kg calcium propionate in bread and pastries, eliminating regional inconsistencies and enabling national bakeries to aggregate volume and cut preservative costs by about 15%. BASF-YPC’s 69,000-tonne-per-year Nanjing facility underpins robust local supply for both food and feed uses. India’s Food Safety and Standards Authority maintains allowances under the Prevention of Food Adulteration Act, yet periodic reviews encourage multinational producers to diversify formulations. Within ASEAN, Indonesia and Vietnam align with Codex guidelines, whereas Thailand’s strict labeling has prompted premium bakeries to trial fermented replacements. The net outcome is heightened baseline demand in mainstream segments of the calcium propionate market even while boutique brands pivot to natural claims.

European Union Approval in Aquaculture Diets Widens Feed Demand

EFSA’s October 2024 renewal for propionic acid and its salts through 2034 reassures feed-mill investors, particularly in Norway, Scotland and Spain where automated liquid-dosing systems favor suspensions over powders[1]European Food Safety Authority, “Opinion on Propionic Acid in Feed,” efsa.europa.eu. Perstorp’s Castellanza expansion aligns capacity with anticipated aquafeed uptake. Water-solubility ensures uniform dispersion in shrimp and fish pellets stored in humid coastal climates, reducing aflatoxin risk. Long shelf life and proven safety support steady growth for feed-grade volumes inside the calcium propionate market. North American aquaculture players continue to monitor FDA guidance on residue limits, but European clarity already drives capital commitments.

GCC Convenience-Food Retail Boom Requiring Longer Shelf Life

Gulf Cooperation Council countries import over 85% of baked goods and routinely operate supply chains in 40 °C ambient temperatures, necessitating higher dosages of 0.3–0.4% calcium propionate to achieve 30-day shelf life. Codex-aligned regulations in Saudi Arabia and UAE ease use, whereas consumer focus remains on safety and freshness rather than natural credentials. Kerry’s ProBake range leverages crystalline and suspension variants tailored for high-heat stability and quick dissolution. Demand is price-inelastic because mold incidents carry greater reputational risk than additive perception. Growing tourism and convenience retail hubs transform the GCC into one of the more resilient demand pockets for the calcium propionate market.

Electro-Synthetic Bio-Based Propionic Acid Routes Lowering Scope-3 Emissions

Pilot-scale electrochemical conversion of biomass intermediates to propionic acid promises carbon-intensity reductions of 35-40% versus petrochemical oxidation routes, fitting well with Europe’s Carbon Border Adjustment Mechanism, which is due to start in 2026. BASF’s eco-efficiency studies positioned propionic acid preservation as less energy-intensive than grain drying, supporting broader corporate net-zero roadmaps. Corbion’s Thailand lactic acid complex and fermentation know-how set the stage for hybrid preservative blends that pair bio-based acids with calcium salts. Early adopters among multinational food brands are willing to pay 5-10% premiums for verified low-carbon material, elevating differentiation prospects in the calcium propionate market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Preservative-Free Foods | -1.2% | North America, Europe, premium segments in Asia-Pacific | Short term (≤ 2 years) |

| Feedstock (Propylene/Acid) Price Volatility Squeezing Margins | -0.8% | Global, with acute impact in Asia-Pacific and Europe | Medium term (2-4 years) |

| Surge in Fermented Mold-Inhibitors Cannibalising Synthetics in Asia-Pacific | -1.0% | China, Japan, South Korea, ASEAN premium bakery channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Preservative-Free Foods

Clean-label positioning has migrated from niche to mainstream, pressuring synthetic additives in fresh bakery and dairy aisles. Cultured dextrose, wheat and buffered vinegar systems from Corbion offer dosage parity at modest price premiums and now compete head-to-head in premium loaf bread and artisan buns. Sunson Biotechnology’s NaturalGARD line carries propionic acid levels above 40% and achieves 2:1 replacement efficiency compared with synthetic calcium propionate, improving taste perception in up-market patisserie. European and North American retailers increasingly request “no artificial preservatives” panels, diverting a share of value toward fermented alternatives even as conventional brands protect volume through price and broad distribution.

Feedstock Price Volatility Squeezing Margins

Propionic acid derives largely from propylene oxidation, tying costs to petrochemical swings. BASF enacted price hikes across regions in late 2020 when propylene rallied, exposing how thin EBITDA margins can erode for non-integrated formulators. New carbon costs in the EU-ETS and future CBAM duties raise delivered expenses for fossil-based chemicals, giving integrated players such as BASF-YPC and Perstorp a cushion while regional toll manufacturers face compression. Forward integration into propionic acid or diversification into fermentation routes is thus becoming critical to strategic resilience in the calcium propionate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Suspensions Build Momentum in Automated Facilities

Liquid/suspension will outpace the overall calcium propionate market at 5.68% CAGR between 2026 and 2031, propelled by industrial bakeries that run high-speed dough mixers and value automated pipe-fed dosing over manual bag tipping. Dry (powder, granular) still captured 65.22% of 2025 revenue because they travel well, suit batch mixing and offer long shelf life without refrigeration. Yet as bakery complexes scale past 10,000 loaves per hour, uniform preservative dispersion becomes mission-critical: liquids cut localized mold recalls and shave 20–30% off labor, justifying investment in corrosion-resistant tanks.

Dry powders will keep hold in small and mid-size bakeries and feed mills that cannot justify extra capex. Granular variants also remain relevant for tablet-coating and feed-pellet lines where controlled flowability determines dosing accuracy. The rising popularity of encapsulated powders that hide off-tastes in dairy illustrates how form diversification supports niche gains.

By Grade: Pharmaceutical Purity Spurs High-Value Growth

Food-grade accounted for 71.12% of 2025 revenue, underpinned by global GRAS and Codex approvals that enable broad application in bread, cheese and processed meat. In contrast, pharmaceutical grade calcium propionate will expand at 6.24% CAGR owing to higher purity (more than 99%) and stringent heavy-metal limits that support film-coated tablets distributed in humid climates. Feed-grade enjoys EFSA renewal through 2034 for silage and aquafeed uses and will track broader livestock expansion, especially in Asia-Pacific.

Industrial-grade remains a niche consumed in construction admixtures and water-based coatings. Nonetheless, rising net-zero commitments place emphasis on lower-carbon precursors, elevating bio-based pharmaceutical and food grades within the wider calcium propionate market. Pricing disparities—USD 4–6/kg for pharma versus USD 2–3/kg for food grade—create ample margin room that supports dedicated production lines even at smaller volumes.

By Application: Feed Gains Traction as Food Faces Clean-Label Shifts

Food and beverage led with 62.34% revenue share in 2025 as sliced bread, sweet pastries and processed cheese rely on proven mold inhibition at modest dose levels. Yet animal feed is forecast to outgrow food at a 5.89% CAGR, powered by aquaculture in Europe and expanding pork and poultry sectors in China and India. Granular or liquid calcium propionate provides an easy-to-dose, water-soluble means to prevent mycotoxins in grain and silage, reinforcing safety throughout the feed chain.

Pharmaceutical uses, while smaller in tonnage, draw premium pricing and immunity from consumer ingredient backlash. Personal care remains emergent but illustrates diversification potential. Taken together, the calcium propionate market size for feed is expected to grow, closing the gap with food even as bakery formulators test fermented alternatives.

Geography Analysis

North America retained 40.23% revenue in 2025 on the strength of long-shelf-life sliced bread and buns, all protected by FDA-affirmed GRAS status under 21 CFR 184.1221[2]U.S. Food and Drug Administration, “21 CFR 184.1221 Calcium Propionate,” fda.gov . The U.S. market shows early signs of clean-label drift, pressing some premium bakeries toward cultured vinegar; yet price-sensitive mainstream brands hold to synthetic salts, protecting tonnage. Canada’s boutique bakers accelerate natural transitions, whereas Mexico’s tortilla sector favors calcium propionate for cost and hot-climate distribution stability.

Asia-Pacific will post the fastest regional growth at 5.98% CAGR. China’s GB 2760-2024 aligned maximum-use levels nationwide in February 2025, eliminating compliance uncertainty and enabling chain bakeries to standardize recipes. BASF-YPC’s integrated 69,000-tonne facility and expanding feedgrain preservation have consolidated supply. India’s regulatory reviews inject some caution, but rising urban bread consumption keeps demand robust. Japan and South Korea maintain strict purity codes, ensuring a fait-accompli for certified multinationals. ASEAN dynamics are mixed: Vietnam and Indonesia are receptive, whereas Thailand’s labeling steers premium bakers toward fermented options.

Europe balances robust regulatory support for feed with consumer pressure in food. EFSA’s 2024 feed approval creates a stable runway for animal nutrition in Norway, Scotland and Spain. Meanwhile, northern retailers push for “no artificial” labels, generating openings for Corbion’s fermented blends. Southern Europe keeps calcium propionate entrenched in cured meats and traditional loaves. South America and the Middle-East and Africa contribute smaller shares, with Brazil’s growing bakery chains and GCC shelf-life challenges offering reliable though modest upside for the calcium propionate market.

Value Chain Analysis

The calcium propionate value chain starts upstream with petrochemical feedstocks (propylene) converted into propionic acid, followed by neutralization with calcium hydroxide or calcium carbonate to produce calcium propionate in dry (powder/granular/agglomerated) and liquid/suspension forms. Integrated propionic acid players, notably BASF-YPC and Perstorp, typically secure cost and continuity advantages versus non-integrated producers, which are more exposed to propylene and energy price swings.

In the midstream, producers focus on crystallization and drying, particle engineering (granular and agglomerates for flow and solubility), and quality systems to meet food, feed, and pharmaceutical specifications. Downstream, calcium propionate is sold directly to industrial bakeries, feed mills, and formulators, as well as through distribution channels that help provide destination-market regulatory documentation, Kosher/Halal and food safety certifications where required, and application support for dosing and dispersion. Key bottlenecks include feedstock volatility, cross-border compliance paperwork on additive rules and labeling, and the need for technical service to help customers balance mold control with clean-label constraints.

Competitive Landscape

Global supply is moderately concentrated. Integrated majors such as BASF, Dow, Eastman and Perstorp collectively control close to half of global propionic acid capacity, translating to cost leadership downstream. BASF-YPC’s Verbund in Nanjing anchors Asia-Pacific logistics, while Perstorp’s Castellanza upgrade in early 2024 boosts European redundancy. Formulators like Kerry Group differentiate through application-specific crystals, powders and suspensions that fit customer processing constraints.

Fermentation specialists—Corbion in particular—are reshaping premium channels with cultured dextrose, wheat and buffered vinegar systems that can halve synthetic dosages without taste penalties. Sunson Biotechnology targets Asia-Pacific patisserie with high-potency NaturalGARD lines exceeding 40% propionic acid, strengthening clean-label credibility. Patents from Takeda (US8846101B2) reveal micro-encapsulation techniques that secure dairy adoption by removing off-odors.

Distribution agreements enhance reach: Azelis widened ties with Perstorp in 2024 for animal nutrition, underscoring the importance of technical sales support in regulatory-heavy applications. Overall, the calcium propionate market tilts toward incumbents for bulk bakery and feed volumes, while innovators siphon value in high-margin, brand-conscious niches.

Calcium Propionate Industry Leaders

Perstorp

Macco

ADDCON GmbH

Kerry Group plc

Impextraco NV

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities concentrate where buyers pay for measurable functionality, compliance readiness, and process efficiency rather than lowest unit price. Automated industrial bakeries and aquafeed mills are expanding liquid/suspension offerings and higher-functionality dry formats (granular/agglomerated), which support accurate dosing and uniform dispersion, consistent with the report context on precision-dosing systems and EFSA clarity for feed uses through 2034. Alongside this, documentation-led differentiation has become more commercial, with suppliers bundling calcium propionate with food safety and certification stacks (including Kosher and packaging-contact readiness referenced in market documentation updates) to reduce switching friction for multinational accounts managing multi-country SKUs.

A second whitespace area sits at the interface between conventional salts and bio-based or fermentation-derived preservation systems. Corbion and BRAIN Biotech announced an August 2025 partnership to develop novel biobased antimicrobial compounds, and BioVeritas has communicated 1:1 bakery efficacy for a fermentation-derived alternative (July 2024), both indicating active investment in next-generation mold inhibition for clean-label-sensitive channels. This supports hybrid portfolio building across incumbents and distributors, including combinations of calcium propionate with cultured or fermentation-based components, as carbon accounting and procurement scrutiny rise.

Recent Industry Developments

- January 2026: Perstorp issued updated product documentation for Profina CP (calcium propionate), detailing compliance positioning and quality specifications used by regulated food customers. The update supports qualification workflows for multinational accounts that require consistent documentation, traceability, and audit-ready data across regions.

- August 2025: Corbion and BRAIN Biotech announced a partnership to develop novel biobased antimicrobial compounds for mold inhibition in bakery applications. The collaboration signals active investment in next-generation preservatives and could broaden options for clean-label formulations.

- July 2024: BioVeritas, LLC announced a 1:1 clean-label alternative to calcium propionate made through fermentation by upcycling surplus biomass. The development underscores competitive pressure from fermentation-derived mold inhibitors in premium bakery segments, highlighting emphasis on label strategy and performance claims.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of calcium propionate sold for use as a preservative and mold inhibitor across food, feed, pharmaceutical, and industrial uses, counted as product revenue at the selling level and tracked in USD across major regions.

Scope exclusions: We exclude premixes and multi-ingredient blends where calcium propionate is not priced and reported as a separate line item, and we also exclude other propionate salts and propionic acid.

Segmentation Overview

- By Form

- Dry (Powder, Granular)

- Liquid/Suspension

- By Grade

- Food Grade

- Feed Grade

- Pharmaceutical Grade

- Industrial Grade

- By Application

- Food and Beverage

- Pharmaceutical

- Animal Feed

- Personal Care

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the real demand pool and the rules that shape usage levels before the model converts those inputs into market numbers. We referenced public sources such as food additive standards and maximum-use guidance from regulators, customs statistics for trade flows, and broad production and industrial indicators from organizations such as the World Bank and UN agencies.

We also reviewed company annual reports, investor presentations, technical datasheets, and trade press to identify capacity signals, application trends, and the packaging and purity conventions that show up in pricing. Where available, paid subscriptions for financials and intelligence, shipment-level import-export records, and patent databases were used to cross-check supplier presence and technology activity. These desk research sources are illustrative only, and we used additional references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating where calcium propionate is actually consumed, how pricing differs by grade and by form, and how procurement decisions change by end user. We spoke with manufacturers, distributors, formulators, and downstream buyers across APAC, EMEA, and the Americas to correct desk assumptions, fill gaps in grade mix and end-use allocation, and confirm final totals from more than one angle.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | APAC: 46% |

| Mid tier: 47% | Functional/Unit leaders: 33% | EMEA: 32% |

| Smaller Players: 15% | Managers: 55% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where bakery and packaged food output, along with compound feed production, is translated into a demand pool using typical calcium propionate use rates and then reconciled with visible supply and trade direction. To keep totals realistic, we also use selective bottom-up approximations as a cross-check, including rolling up sampled supplier volumes by region and validating implied average selling prices using grade-level price points.

Inputs used in the model include packaged bakery throughput trends, feed output momentum, the split between dry versus liquid or suspension formats, grade mix (food, feed, pharmaceutical, and industrial), and price movement linked to upstream propionic acid and energy costs. Forecasting is built around scenario analysis supported by multivariate relationships between end-use output indicators and realized pricing. We then pressure-test forward assumptions with primary experts so short-term price swings are not carried too far into the forecast. Where visibility is weaker in smaller countries, we apply proxy ratios from similar markets and then correct back to regional supply and trade totals.

Data Validation & Update Cycle

Outputs are validated through multiple checks, including reconciling regional totals with import-export direction, comparing implied per-ton pricing against observed quotes and historical ranges, and reviewing demand shares across end uses for logical stability. Variances that do not match known events, such as capacity changes or regulatory shifts, are flagged and reworked, and follow-up calls are triggered when a critical assumption moves materially.

Each dataset and calculation step is reviewed by another analyst before sign-off, and the final narrative is checked to ensure it matches the numbers. The report is refreshed annually, and interim updates are made when material events occur, followed by a final pass right before delivery so clients receive the most current view.

Mordor Intelligence's Calcium Propionate Market Estimate Compared With Other Published Estimates

Published market sizes for calcium propionate often do not match because the studies are not counting the same things, even when the titles look similar. Differences usually come from what is included in the product scope, the year used as the starting point, and how price and volume are combined when public reporting is limited.

The largest gap drivers in this market are whether multi-ingredient preservative blends are counted, how grade mix is treated when moving from food to feed and industrial demand, and whether demand is modeled from end-use output indicators or inferred from broad chemical additives baskets. Some estimates also rely on older currency timing and do not re-check price shifts tied to propionic acid and energy, which can move value meaningfully in a short period.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 408.24 M (2026) | |

| Industry Publisher A | USD 428.50 M (2025) | Uses a different base year and a longer forecast window, and it appears to include adjacent uses such as personal care that can lift totals versus a tighter preservative and feed demand pool. |

| Research Firm B | USD 291.36 M (2024) | Starts from an earlier base year and may apply narrower application boundaries and older average pricing, which can understate value when later grade mix and price increases are not fully carried through. |

The table shows that timing and scope choices explain most of the spread, especially around whether blend revenues and adjacent applications are counted. By tying volumes to bakery output and feed production signals, and then re-checking grade-level pricing assumptions in each refresh cycle, the totals stay anchored to observable demand drivers in Mordor Intelligence.

Key Questions Answered in the Report

How big is the calcium propionate market today?

The calcium propionate market size reached USD 408.24 million in 2026 and is on course to hit USD 526.76 million by 2031 at a 5.23% CAGR.

Which application will grow fastest over the next five years?

Animal feed is projected to expand at 5.89% CAGR, outpacing food and beverage due to EU aquaculture approvals and Asia-Pacific livestock demand.

What regulatory changes are most important for market growth?

EFSA’s 2024 feed renewal and China’s GB 2760-2024 harmonization both remove compliance uncertainty, unlocking long-term volume commitments.

How does bio-based propionic acid influence purchasing decisions?

Electro-synthetic and fermentation routes lower carbon footprints by up to 40%, enabling food brands with net-zero targets to pay sustainability premiums.

Page last updated on: