Calcium Aluminate Cement Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Volume (2026) | 4.16 Million tons |

| Market Volume (2031) | 5.39 Million tons |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

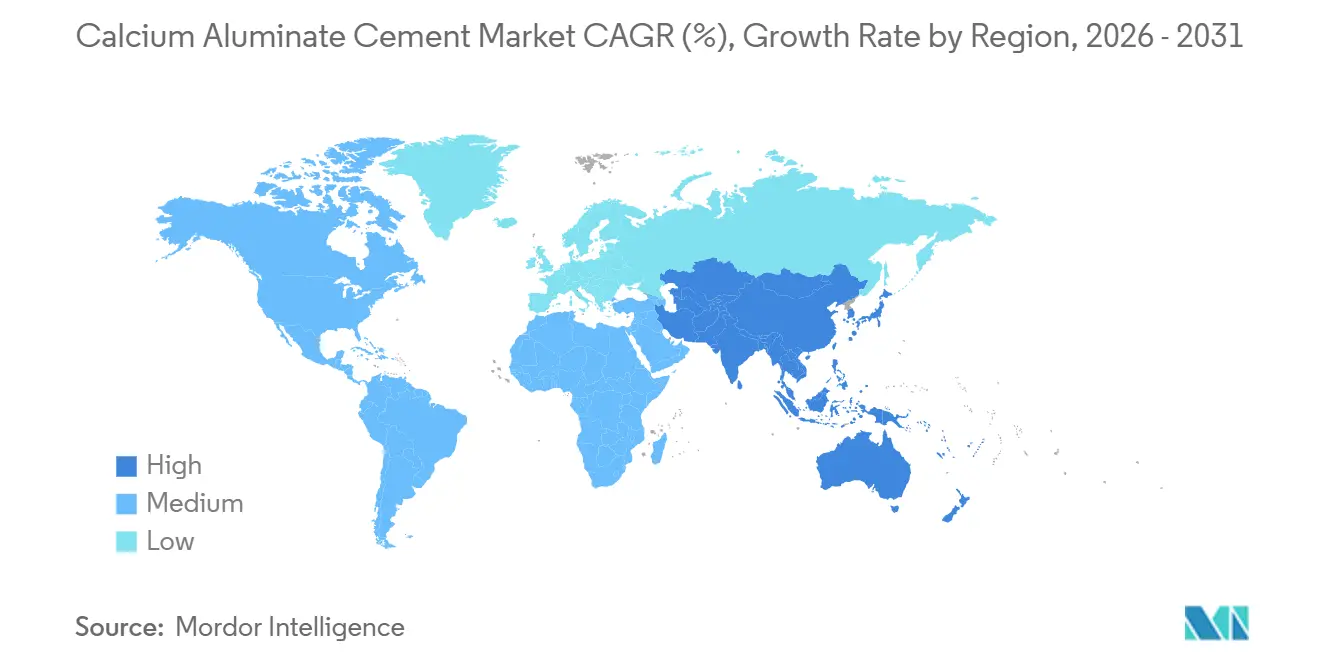

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

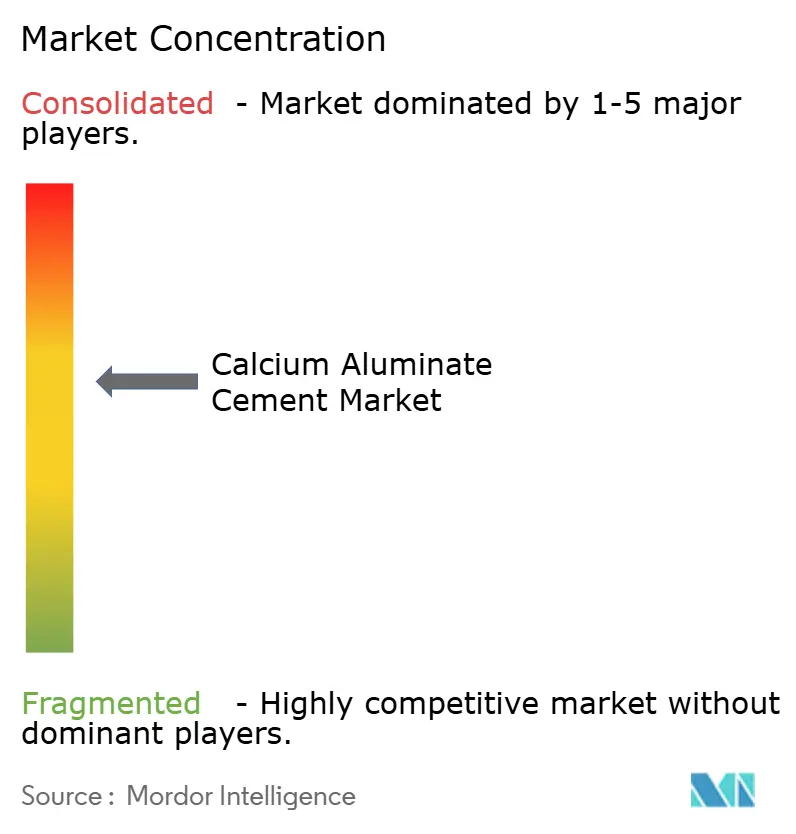

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Calcium Aluminate Cement Market Analysis by Mordor Intelligence

The Calcium Aluminate Cement Market size is expected to increase from 3.96 million tons in 2025 to 4.16 million tons in 2026 and reach 5.39 million tons by 2031, growing at a CAGR of 5.32% over 2026-2031. Growth in the calcium aluminate cement market is driven by three structural factors: the transition by steelmakers to electric-arc furnaces, which require alumina-rich refractory linings capable of withstanding temperatures above 1,700°C; the inclusion of sulfate-resistant calcium aluminate mortars in wastewater standards, such as Australia’s WSA 160:2021; and the increasing adoption of thermal energy storage systems, which demand matrices that can endure hundreds of 600-650°C cycles without losing mechanical strength. Unlike commodity Portland cement, this market benefits from price stability, as purchasing decisions are driven by performance rather than volume. However, the concentration of bauxite feedstock in Guinea and China introduces cost fluctuations, despite an 8% alumina price decline projected for 2025.

The Asia-Pacific region accounted for the largest market share, representing 46.50% of the 2025 volume, and is expected to grow at a compound annual growth rate (CAGR) of 6.15% through 2031. This growth is driven by India’s 22% increase in refractory castables during 2023-24 and China’s anticipated calcined-alumina surplus, which is set to become fully operational by early 2026. Industry consolidation continues as major producers focus on vertical integration to secure control over raw materials and logistics. However, no single player holds more than a 15% global market share, maintaining a high level of competitive intensity.

Key Report Takeaways

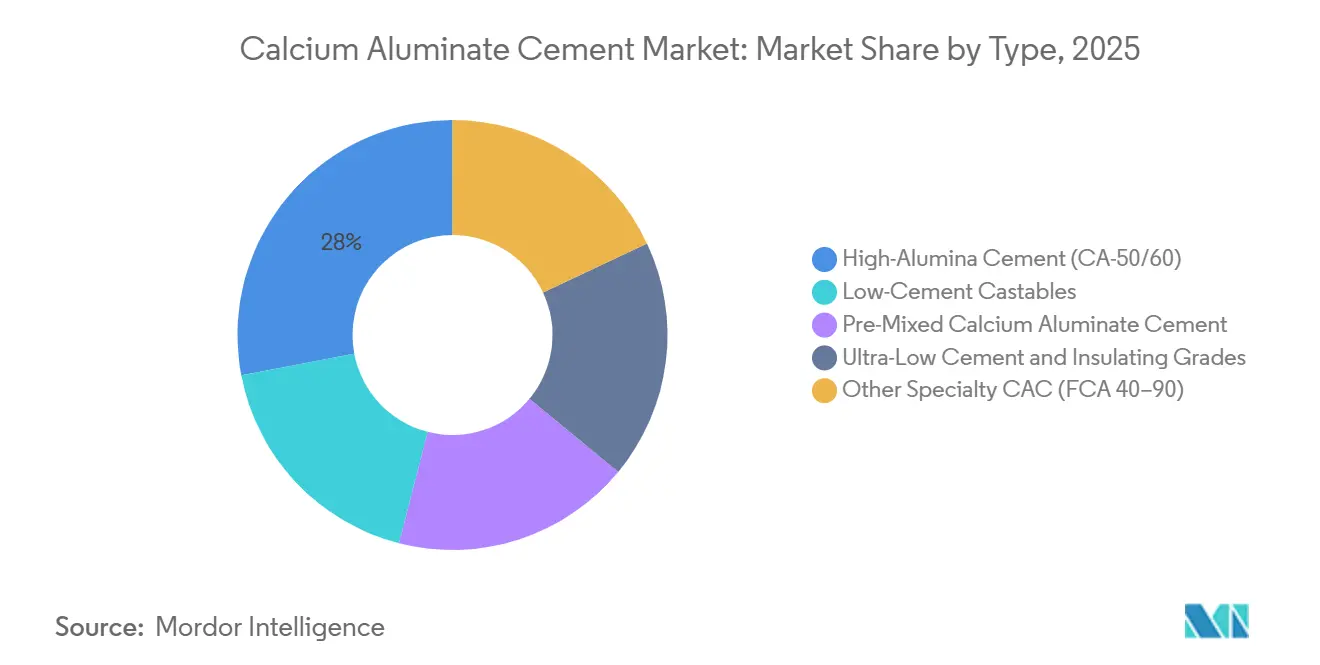

- By type, Other Specialty CAC held 28.00% of 2025 volume, while High-Alumina grades are forecast to post the fastest 6.12% CAGR to 2031.

- By form, Powder retained 46.00% of the calcium aluminate cement market share in 2025; Premixed Bags are projected to expand at a 6.23% CAGR through 2031.

- By application, Refractories accounted for 42.00% of the calcium aluminate cement market size in 2025, and Construction & Rapid-Repair is advancing at a 6.30% CAGR through 2031.

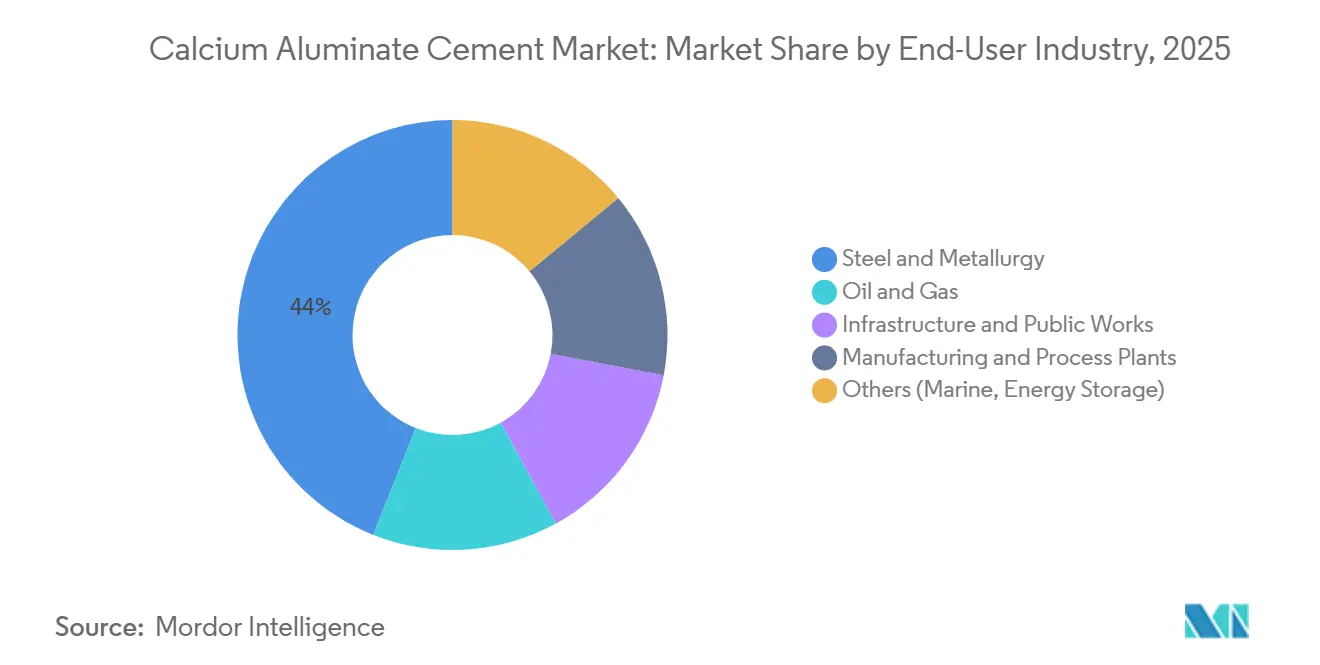

- By end-user industry, Steel & Metallurgy led with 44.00% of 2025 volume, whereas the Marine & Energy Storage segment is the fastest riser at a 6.20% CAGR to 2031.

- By geography, Asia-Pacific dominated with 46.50% share in 2025 and is expected to register the quickest regional CAGR at 6.15% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Calcium Aluminate Cement Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand in refractory applications | +1.8% | Global, with concentration in Asia-Pacific (China, India) and select Middle East markets | Medium term (2-4 years) |

| Rapid-setting/high-performance concrete adoption | +1.2% | North America, Europe, ASEAN infrastructure corridors | Short term (≤ 2 years) |

| Expanding use in sewerage and waste-water infrastructure | +0.9% | Australia, Europe (Germany, UK, NORDIC), select US municipalities | Medium term (2-4 years) |

| 3-D printed refractory shapes enable new CAC binders | +0.6% | North America (ORNL, industrial R&D hubs), Europe (Germany, Spain) | Long term (≥ 4 years) |

| Low-CO₂, energy-efficient CAC production processes | +0.7% | Europe (France, Spain), select North American facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand in Refractory Applications

India's transition to electric-arc furnaces increased the demand for refractory castables by 22% in 2023-24, driving higher consumption of calcium aluminate cement (CAC) due to its ability to maintain strength where Portland binders fail[1]RHI Magnesita, “2025 Full-Year Results,” rhimagnesita.com. This shift also results in energy savings of 60-70% per ton of steel, while compliance with India's Perform, Achieve, and Trade (PAT) scheme for mandated decarbonization supports sustained demand growth. Similarly, petrochemical cracker upgrades in the Middle East and China are adopting ultra-low cement castables, which combine CAC with reactive alumina to achieve a hot modulus of rupture exceeding 12 megapascals (MPa) at 1,400 degrees Celsius (°C), extending lining lifespans by 15-20%.

Rapid-Setting/High-Performance Concrete Adoption

Calcium sulfoaluminate variants achieve a strength of 35-40 MPa within 72 hours when using seawater, eliminating the need for freshwater in coastal precast yards and reducing carbon dioxide (CO₂) emissions by up to 48% compared to Ordinary Portland Cement (OPC). In the United States, bridge-deck overlays funded under the Infrastructure Investment and Jobs Act require such fast-setting materials. Similarly, the Association of Southeast Asian Nations (ASEAN) Connectivity Master Plan permits the use of Calcium Aluminate Cement (CAC) binders to address a USD 210 billion infrastructure gap by 2030.

Expanding Use in Sewerage and Waste-Water Infrastructure

Australia's WSA 160:2021 standard specifies the use of calcium aluminate cement (CAC) linings for high-sulfate sewers, as calcium aluminate hydrates do not contain portlandite, thereby preventing the formation of expansive ettringite[2]Water Services Association of Australia, “WSA 160:2021,” wsa.org.au. Similarly, Germany's Deutsche Vereinigung für Wasserwirtschaft, Abwasser und Abfall-A 143 (DWA-A 143) and the United Kingdom's Water Industry Specification 4-08-02 (WIS 4-08-02) adopt this approach, enabling municipal retrofits in cities such as Hamburg, Munich, and London.

3-D Printed Refractory Shapes Enable New CAC Binders

Oak Ridge National Laboratory has demonstrated that calcium aluminate additives enhance layer adhesion in robotic extrusion, reducing refractory installation labor by 60-70% and enabling the creation of complex geometries for kiln burners and glass-furnace tap holes. Recent patents from Calderys and Refratechnik describe printable alumina castables that retain over 85% of their cast strength after sintering at 1,500 degrees Celsius. However, the high capital expenditure of printers currently limits adoption to large original equipment manufacturers (OEMs).

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs vs Portland cement | -0.9% | Global, most acute in price-sensitive markets (India, China, Southeast Asia) | Short term (≤ 2 years) |

| Energy-intensive, CO₂-heavy manufacturing process | -0.5% | Europe (CBAM compliance), North America (California, Washington state) | Medium term (2-4 years) |

| Supply risk of high-purity bauxite feedstock | -0.4% | Global, with acute exposure in Europe and North America dependent on Guinea/China imports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production Costs vs Portland Cement

Sintering at temperatures 100-150°C higher than Portland variants increases Calcium Aluminate Cement (CAC) energy consumption by 15-20% and results in a 25-30% price premium, limiting its adoption in applications where Ordinary Portland Cement (OPC) with accelerators is sufficient. In 2025, Indian buyers faced Chinese imports priced 10-15% lower, which impacted domestic margins and delayed capacity expansions.

Energy-Intensive, CO₂-Heavy Manufacturing Process

Plant emissions typically range from 0.85 to 1.05 tons of carbon dioxide (CO₂) per ton of clinker. Starting in 2026, Europe’s Carbon Border Adjustment Mechanism (CBAM) will introduce carbon levies, adding USD 15-25 per ton to imports from coal-powered regions. This is expected to increase substitution pressure toward geopolymers or magnesium oxide (MgO) binders, particularly in applications where thermal resistance is less critical.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Specialty Grades Dominate, High-Alumina Accelerates

Other Specialty Calcium Aluminate Cement (CAC) is projected to account for 28.00% of the 2025 volume, while High-Alumina Cement is expected to grow at an annual rate of 6.12%, driven by the demand for monolithic refractories capable of withstanding thermal shocks of greater than or equal to 1,600 °C, particularly in electric-arc furnace retrofits. Companies in the segment utilize their market size advantage by offering design support, with High-Alumina Cement's market share anticipated to increase as steel producers focus on achieving longer campaign lifespans. Commodity grades with 40-50% alumina content face margin pressures due to competition from Chinese manufacturers. However, sustainability-focused products, such as EcoCaltrix, command a 15-20% price premium in Europe’s public procurement channels.

Powder forms are expected to remain dominant, accounting for 46.00% of 2025 demand, as refractory formulators require flexibility to adjust water demand, flow characteristics, and hot strength. Premixed bags, on the other hand, are forecasted to grow at a compound annual growth rate (CAGR) of 6.23%, driven by contractors seeking labor efficiency and consistent batch quality, particularly for emergency pavement repairs. Paste and slurry forms will remain niche products but achieve 25-30% gross margins due to their pumpability and strong adhesion to hot substrates, which are essential for applications such as ladle and kiln-shell patching.

By Form: Powder Prevails, Premixed Bags Gain Traction

Powder accounted for 46.00% of the projected 2025 volume, indicating its significance in bulk refractory castable mixing. Producers use powder to blend calcium aluminate with alumina aggregates, silica fume, and dispersants to achieve specific rheology and setting time requirements. Premixed bags are expected to grow at a CAGR of 6.23%, driven by contractor demand for consistent, single-source formulations, particularly in rapid-repair and emergency-response applications. Paste/Slurry forms, which are typically thixotropic formulations designed for gunning or troweling, cater to maintenance and repair segments. These forms are valued for their pumpability and ability to adhere to hot substrates (up to 800 degrees Celsius), making them suitable for applications such as kiln-shell repairs and ladle patching. The segmentation by form reflects a balance between customization and convenience: powder allows for precise mix designs tailored to refractory applications, while premixed bags focus on ease of use and reduced labor skill requirements, with some trade-offs in performance potential.

By Application: Refractories Lead, Rapid-Repair Surges

Refractories are projected to account for 42.00% of the calcium aluminate cement (CAC) market size in 2025, driven by demand from the steel, non-ferrous metals, and petrochemical industries. The Construction & Rapid-Repair segment is expected to grow at a faster rate of 6.30%, as infrastructure projects such as airports, bridges, and ports increasingly adopt fast-track overlays that can reopen within 24 hours, reducing lane-closure costs by 40-50%. Additionally, water treatment upgrades mandated by EU wastewater regulations are boosting demand for CAC linings, which offer a service life three times longer than Portland cement alternatives. Meanwhile, demand from the chemicals sector remains stable due to CAC's resistance to acids, including concentrations of up to 10% H₂SO₄.

By End-User Industry: Steel Dominates, Energy Storage Emerges

The Steel and Metallurgy segment is projected to account for 44.00% of the total volume in 2025. The other category, which primarily includes Marine and Energy Storage applications, is expected to grow at a rate of 6.20% annually. This growth is driven by the demand for crack-resistant matrices with a compressive strength of 88.77 MPa, capable of withstanding repeated cycles at 600 degrees Celsius, as required for offshore wind foundations and calcium-looping thermal batteries. Additionally, Oil and Gas wells operating above 300 degrees Celsius represent a niche segment where the acid and temperature resistance of Calcium Aluminate Cement (CAC) supports a price premium of 25-30%.

Geography Analysis

Asia-Pacific is projected to retain its 46.50% market share through 2031, with an annual growth rate of 6.15%. This growth is driven by India’s 18-percentage-point increase in electric-arc furnace penetration, boosting refractory demand, and capacity expansions by Chinese producers despite competitive pricing pressures. Japan and South Korea prioritize quality over volume, while ASEAN (Association of Southeast Asian Nations) countries depend on imported bagged calcium aluminate cement (CAC) to support infrastructure projects, particularly bridge construction programs.

North America is expected to benefit from RHI Magnesita’s acquisition of Resco in 2025. Federal infrastructure funding is anticipated to drive demand for rapid-repair solutions, while Calderys’ new plant in Missouri is projected to reduce lead times by 30-40% for buyers in the Midwest region.

Europe continues to lead in sustainability innovations, but experienced a 12% contraction in industrial cement production in 2025. Despite this, sewer upgrades under DWA-A 143 standards and the Carbon Border Adjustment Mechanism’s (CBAM) carbon pricing framework indicate long-term growth potential for low-carbon dioxide (CO₂) cement grades. High per-capita spending in Nordic countries supports niche demand for premium CAC, despite relatively low production volumes.

South America’s market outlook hinges on Brazil’s pending antidumping duties, which could protect local producers. Additionally, Argentina’s mining sector provides a stable, though modest, baseline for refractory demand.

Growth in the Middle East and Africa is concentrated in Saudi Arabia and South Africa. In Iran, a dominant local supplier meets over 90% of domestic demand and exports to neighboring petrochemical hubs, contributing to regional market stability.

Competitive Landscape

The calcium aluminate market is moderately concentrated. Even after Imerys acquires Kerneos, the combined entity will hold less than 18% of the global market share. RHI Magnesita’s acquisition of Resco demonstrates a "local-for-local" strategy, which addresses tariff risks and reduces lead times. Sustainability-focused companies such as Almatis and Calucem secure European municipal tenders by publishing third-party Environmental Product Declarations (EPDs). Meanwhile, Oak Ridge’s open-source binder recipe indicates a future where digital manufacturing creates new value opportunities. However, feedstock security remains a priority for integration strategies. Imerys’ ownership of Greek bauxite mines helps safeguard the European Union (EU) supply chain against disruptions, while Calucem’s dross substitution strategy reduces reliance on imports. Emerging opportunities are focused on energy storage, where no incumbent has yet introduced a dedicated product line, despite the existence of laboratory proofs-of-concept.

Calcium Aluminate Cement Industry Leaders

Imerys

Almatis

Çimsa

Molins

DDenka Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Calderys established a lightweight monolithics facility in Fulton, Missouri, increasing regional capacity by 60% and reducing delivery times by 30-40%. This development is expected to support the growing demand for calcium aluminate cement in the region.

- June 2025: Research published by Oak Ridge National Laboratory in Energy & Fuels indicated that the use of calcium aluminate cement binders resulted in a 176% capacity improvement in calcium-based thermal storage pellets after 60 cycles.

Global Calcium Aluminate Cement Market Report Scope

Calcium aluminate is a hydraulic binder manufactured by heating calcium oxide (CaO) and aluminum oxide (Al2O3). It is known for its rapid-setting properties, high-temperature resistance, and corrosion resistance. This material is primarily utilized in specialty concrete, refractory castables for furnaces, and construction repair applications. Compared to Portland cement, it demonstrates resistance to chemicals and heat.

The calcium aluminate market is segmented by type, power, application, end-user industry, and geography. By type, the market is segmented into high-alumina cement (CA-50/60), low-cement castables, pre-mixed calcium aluminate cement, ultra-low cement and insulating grades, and other specialty CAC (fca 40–90). By power, the market is segmented into powder, paste/slurry, and premixed bags. By application, the market is segmented into refractories, construction and rapid-repair, chemicals and petrochemicals, water and wastewater treatment, and mining and power generation. By end-user industry, the market is segmented into steel and metallurgy, oil and gas, infrastructure and public works, manufacturing and process plants, and others (marine, energy storage). The report also covers the market size and forecasts for calcium aluminate in 17 countries across major regions. The market sizes and forecasts are provided in terms of volume (tons).

| High-Alumina Cement (CA-50/60) |

| Low-Cement Castables |

| Pre-Mixed/Premixed CAC |

| Ultra-Low Cement and Insulating Grades |

| Other Specialty CAC (FCA 40–90) |

| Powder |

| Paste / Slurry |

| Premixed Bags |

| Refractories |

| Construction and Rapid-Repair |

| Chemicals and Petrochemicals |

| Water and Waste-Water Treatment |

| Mining and Power Generation |

| Steel and Metallurgy |

| Oil and Gas |

| Infrastructure and Public Works |

| Manufacturing and Process Plants |

| Others (Marine, Energy Storage) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | High-Alumina Cement (CA-50/60) | |

| Low-Cement Castables | ||

| Pre-Mixed/Premixed CAC | ||

| Ultra-Low Cement and Insulating Grades | ||

| Other Specialty CAC (FCA 40–90) | ||

| By Form | Powder | |

| Paste / Slurry | ||

| Premixed Bags | ||

| By Application | Refractories | |

| Construction and Rapid-Repair | ||

| Chemicals and Petrochemicals | ||

| Water and Waste-Water Treatment | ||

| Mining and Power Generation | ||

| By End-user Industry | Steel and Metallurgy | |

| Oil and Gas | ||

| Infrastructure and Public Works | ||

| Manufacturing and Process Plants | ||

| Others (Marine, Energy Storage) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How great will global demand for calcium aluminate cement be by 2031?

The calcium aluminate cement market size is forecast to reach 5.39 million tons by 2031, up from 4.16 million tons in 2026.

Which region contributes the most volume?

Asia-Pacific supplies 46.50% of global demand and is growing at a 6.15% CAGR through 2031.

What application segment is expanding the fastest?

Construction and rapid-repair materials are projected to rise at a 6.30% CAGR on the back of infrastructure rehabilitation programs.

Why are steel producers central to future consumption?

Electric-arc furnaces need alumina-rich refractories that tolerate ≥1,700 °C, pushing steel to 44% of 2025 consumption and sustaining long-term demand.

Page last updated on: