Market Overview

| Study Period | 2020 - 2031 |

|---|---|

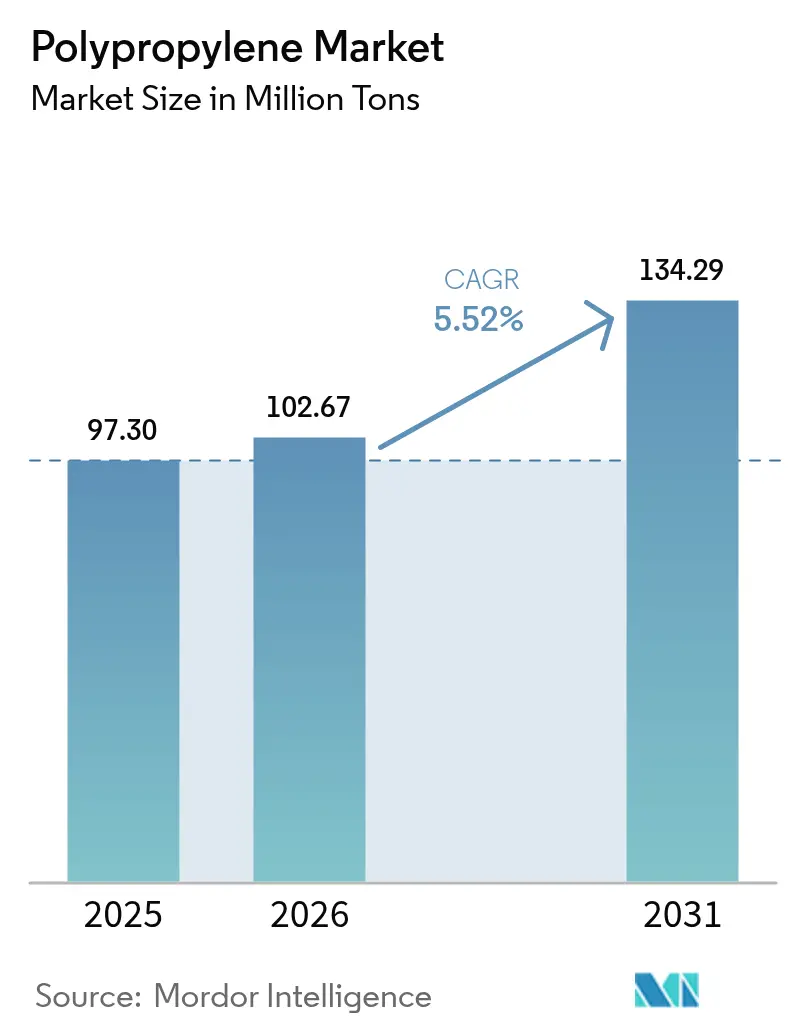

| Market Volume (2026) | 102.67 Million tons |

| Market Volume (2031) | 134.29 Million tons |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

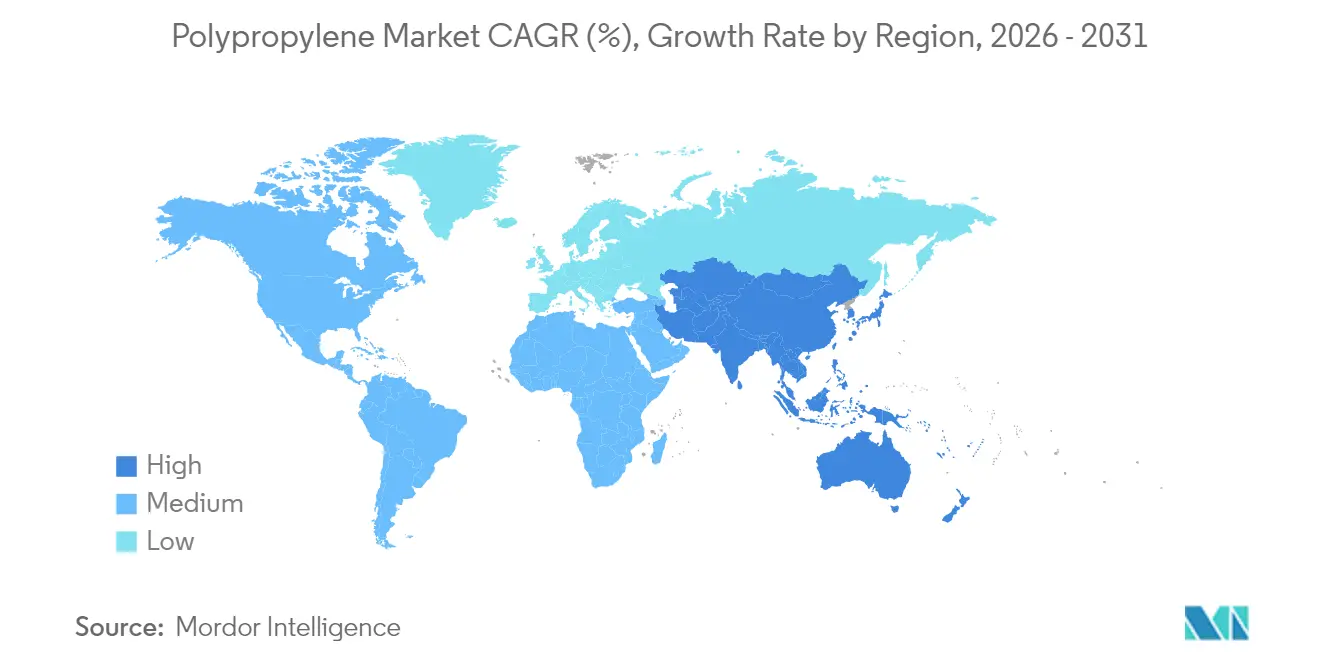

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polypropylene Market Analysis by Mordor Intelligence

The Polypropylene Market size was valued at 97.30 million tons in 2025 and estimated to grow from 102.67 million tons in 2026 to reach 134.29 million tons by 2031, at a CAGR of 5.52% during the forecast period (2026-2031). Sustained demand in flexible packaging, automotive lightweighting, and non-woven fiber applications underpins this expansion, while propane-dehydrogenation (PDH) investments compress cash costs and shore up regional competitiveness. Producers are channeling capital toward specialty catalyst systems that yield high-melt-strength grades, enabling foamed parts that cut material use and vehicle weight. Rapid scale-up of chemical-recycling supply agreements is opening premium outlets for recycled feedstocks, although virgin resin volumes still dominate. At the same time, regulatory divergence—exemplified by the EU plastics tax—nudges converters toward mono-material structures, intensifying competition with polyethylene terephthalate and advanced polyethylene films.

Key Report Takeaways

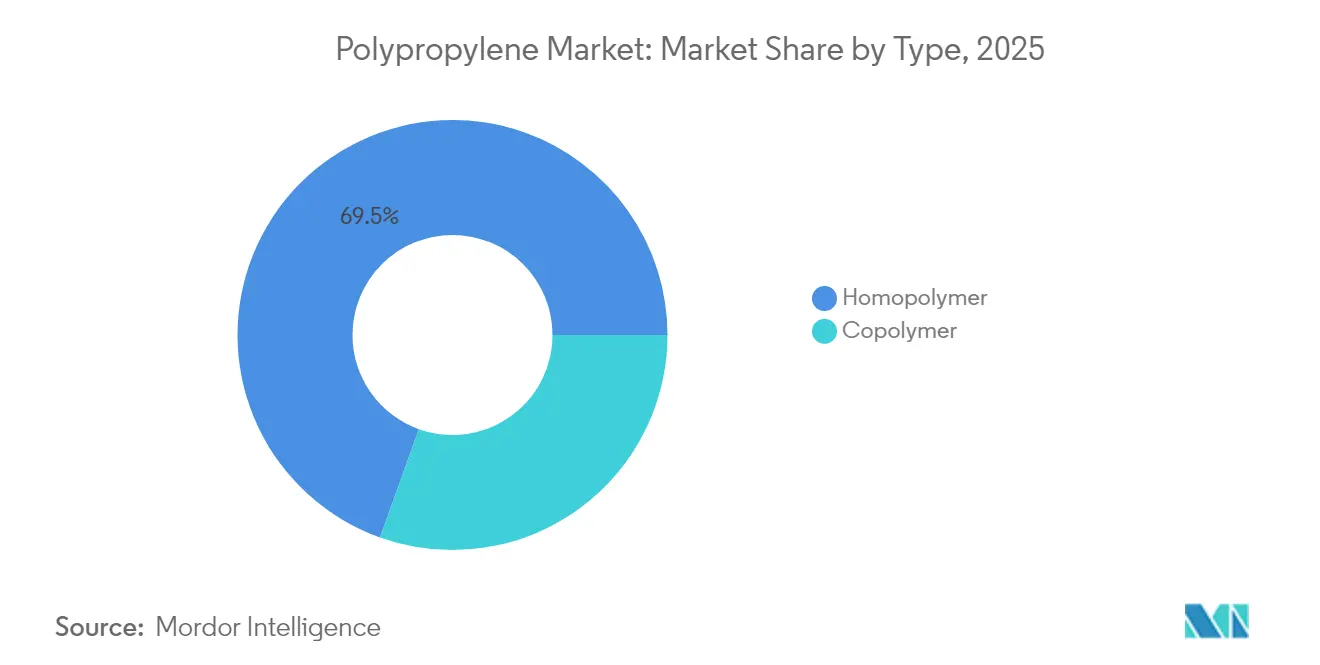

- By type, homopolymer accounted for 69.53% of polypropylene market share in 2025, while advancing at a CAGR of 5.63% to 2031.

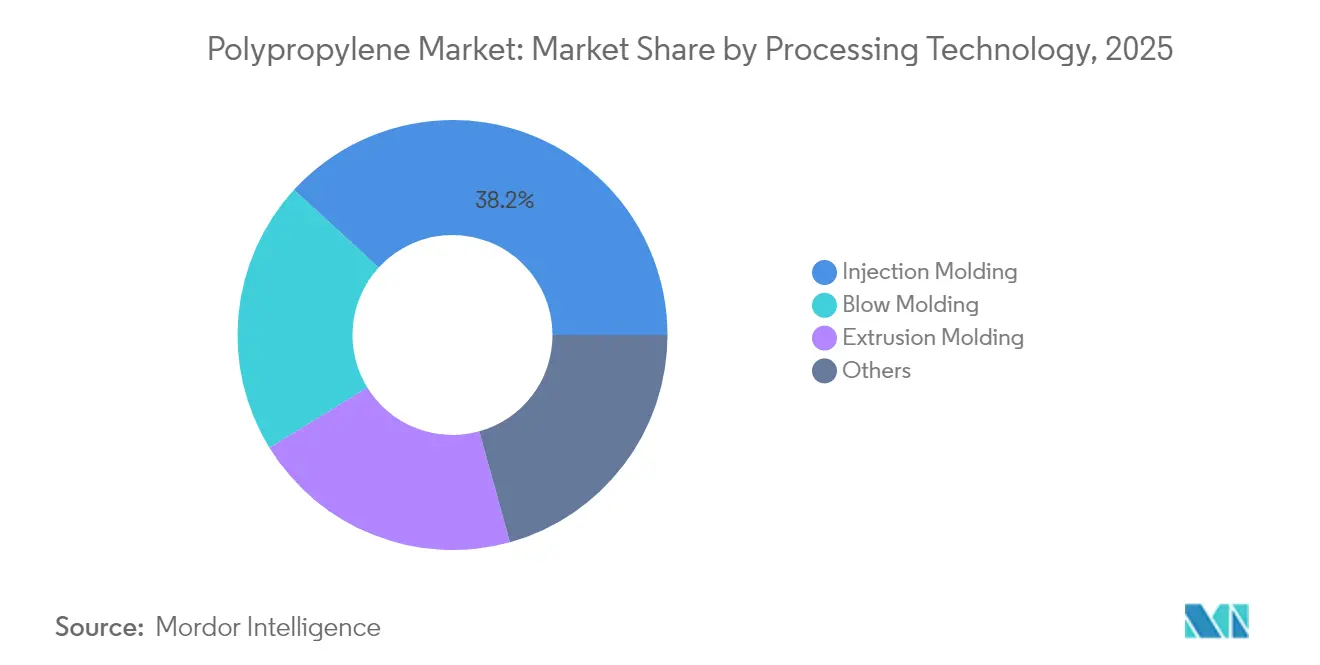

- By processing technology, injection molding captured 38.20% of the polypropylene market in 2025 and is forecast to post the fastest 5.74% CAGR to 2031.

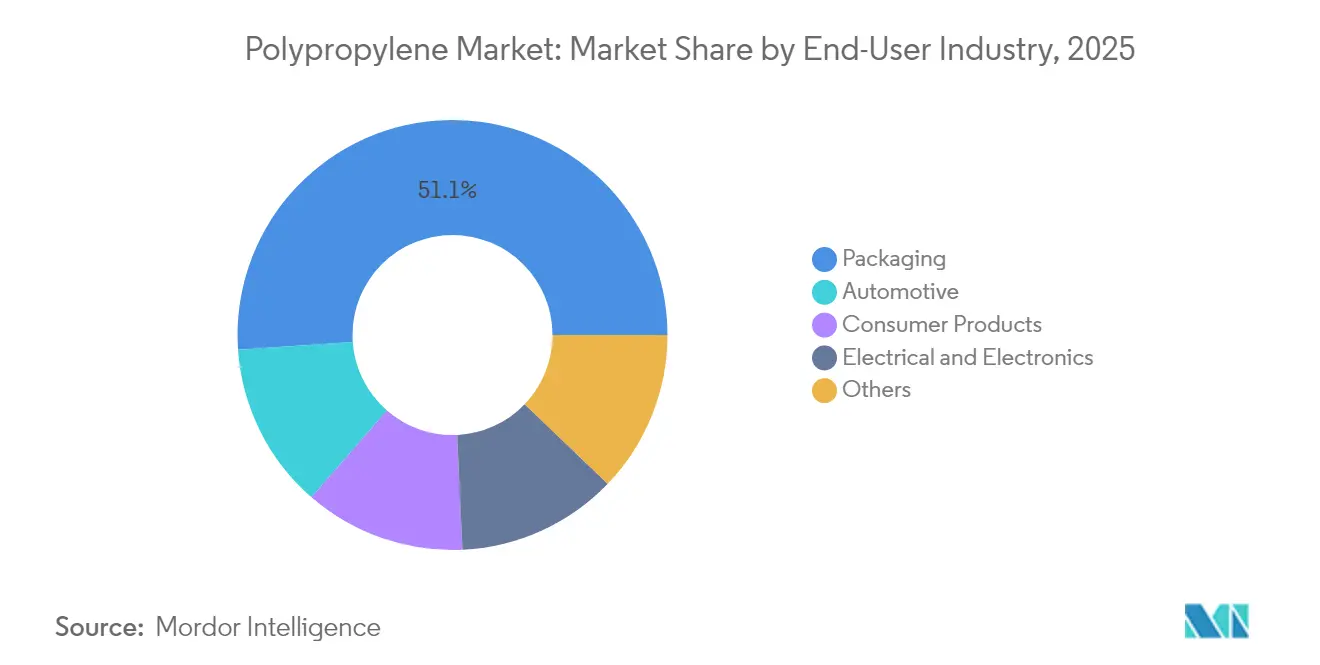

- By end-user industry, packaging led with a 51.10% revenue share in 2025, while automotive is projected to expand at a 6.05% CAGR through 2031 in the polypropylene market.

- By geography, Asia-Pacific commanded 58.78% of polypropylene market size in 2025 and is predicted to register the highest regional 6.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polypropylene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting Push in Automotive and E-Mobility | +1.2% | Global, with concentration in North America, Europe, and China | Medium term (2-4 years) |

| Exploding Demand for Mono-Material Flexible Packaging | +1.5% | Global, strongest in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Capacity Surge of Propane-Dehydrogenation (PDH) Units Lowering Cash-Cost | +0.8% | North America, Middle East, with spillover to Asia-Pacific | Long term (≥ 4 years) |

| High-Melt-Strength PP Enabling Foamed, Low-Density Applications | +0.6% | Global, early adoption in automotive-heavy regions | Medium term (2-4 years) |

| Rapid Scale-Up of Chemical-Recycling Supply Agreements | +0.4% | Europe and North America primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lightweighting Push in Automotive and E-Mobility

Automakers targeting extended battery range are replacing metal assemblies with high-melt-strength polypropylene foams that cut part mass by up to 40% while retaining crashworthiness, particularly in instrument panels and under-hood shields[1].BMW Group, “Lightweight Construction in the New Electric Mini,” bmwgroup.com Integrated catalyst systems now produce propylene-based elastomers that displace rubber grommets and seals, offering designers consolidation opportunities that trim assembly time. Tier-one suppliers are shifting tooling strategies toward thin-wall injection molding to optimize cycle times, spurring a fresh wave of press retrofits across Europe. North American OEMs are aligning resin selection matrices with end-of-life recyclability targets, giving an additional boost to mono-material interiors. The resulting 6.29% CAGR for automotive applications positions the polypropylene market as a pivotal beneficiary of electrification trends.

Exploding Demand for Mono-Material Flexible Packaging

Global brands have fast-tracked voluntary targets demanding 100% recyclable packaging by 2025, prompting converters to abandon multi-layer laminates in favor of barrier-coated polypropylene films. European supermarkets now specify shelf-ready pouches made from single-polymer structures to minimize extended-producer-responsibility fees, sparking a surge in proprietary surface-treatment lines. Asia-Pacific packagers, capitalizing on economies of scale, are adopting solvent-free lamination technologies that deliver high-speed runs while meeting food-contact compliance. As a result, packaging retains the largest volume base yet transitions toward higher-margin barrier formats that command premium pricing. The migration also elevates bale purity in mechanical recycling streams, indirectly raising demand for recycled polypropylene pellets among fast-moving consumer-goods companies in the polypropylene market.

Capacity Surge of PDH Units Lowering Cash Cost

PDH capacity additions in the United States, China, and the Arabian Gulf have re-ordered the global cost curve, slicing integrated cash costs by up to USD 130 per ton relative to naphtha crackers during propane-favorable windows in the polypropylene market. U.S. producers leveraging shale-derived propane have pushed export offers into Latin America, supplanting Asian cargoes and amplifying arbitrage flows. Chinese operators, meanwhile, are importing seaborne ethane and commissioning on-purpose propylene units to backfill domestic deficits, further insulating local polypropylene margins from crude swings. The high-purity propylene stream developed through PDH also improves catalyst efficiency, translating into narrower molecular-weight distributions coveted in medical-grade applications. These structural cost shifts underpin long-term volume growth for injection-molded goods and foster incremental investments in downstream compounding.

High-Melt-Strength PP Enabling Foamed, Low-Density Applications

Metallocene catalysts are empowering producers to engineer melt strengths exceeding 30 cN, enabling bead-foam and structural-foam technologies formerly reserved for expanded polystyrene. Automotive headliners, HVAC housings, and appliance tubs are migrating toward these low-density formulations, trimming resin usage by 15% and driving energy savings at molding plants. Appliance OEMs in Korea report double-digit scrap reductions after switching to foamed polypropylene panels, attributing the improvement to superior dimensional stability. Premium price realization, currently averaging USD 150-per-ton above commodity homopolymer, encourages resin makers to allocate swing capacity to specialty grades. The emerging supply base is still nascent, indicating headroom for further margin accretion as commercialization scales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of High-Performance Substitute Resins (PE, PET, ABS) | -0.9% | Global, particularly in packaging and consumer goods | Short term (≤ 2 years) |

| Crude-Oil and Propylene Price Volatility Squeezing Converter Margins | -1.1% | Global, most acute in price-sensitive applications | Short term (≤ 2 years) |

| EU Plastics Tax Steering Converters Toward Mono-PE Laminates | -0.7% | Europe primarily, with spillover effects in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of High-Performance Substitute Resins

Product developers in flexible packaging are increasingly testing metallized polyethylene films that match polypropylene’s oxygen barrier while delivering lower sealing temperatures, eroding polypropylene’s historic cost advantage[2]Dow, “Next-Generation Recycle-Ready PE Films,” dow.com . In beverage closures, polyester suppliers tout chemical-recycling content and superior clarity to capture sustainability-oriented brand guidelines. Acrylonitrile-butadiene-styrene (ABS) continues to win share in consumer electronics m-covers through higher surface gloss and impact resistance, pressuring polypropylene in premium aesthetics. Resin makers counter by launching inspired polypropylene grades with boosted stiffness-to-impact ratios, but adoption hinges on converter willingness to requalify molds. The tug-of-war intensifies as material selection teams weigh mechanical performance against recyclability targets, creating a net 0.9 percentage-point drag on forecast CAGR.

Crude-Oil and Propylene Price Volatility Squeezing Converter Margins

Propylene spot prices climbed 38% quarter-over-quarter in early 2025, while Brent oil advanced only 12%, underscoring the decoupling between monomer and crude benchmarks. Contract formulas in packaging and textile yarns typically adjust with a one-month lag, exposing processors to inventory losses when markets spike. Smaller converters, lacking hedging sophistication, often ride out volatility by trimming operating rates, exacerbating supply tightness downstream. Regional disparities add complexity; European converters pay higher energy surcharges on top of monomer swings, prompting some to relocate sourcing to PDH-advantaged Gulf suppliers. Persistent volatility narrows working-capital cushions, making credit insurance costlier and tempering aggressive growth plans.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Homopolymers Retain Cost Leadership

Homopolymer accounted for 69.53% of polypropylene market share in 2025, reflecting price sensitivity in caps, closures, and yarns where stiffness-to-weight ratio is paramount. The segment is forecast to post a 5.63% CAGR supported by PDH-driven cost competitiveness, with the polypropylene market size for homopolymers expected to reach 93.37 million tons by 2031. Producers are narrowing molecular-weight distributions using loop-reactor technology, enhancing clarity without sacrificing rigidity, which aids transition from random copolymer in dairy containers. Copolymers, while smaller in tonnage, secure premium pricing in impact-critical parts such as automotive bumpers and washing-machine tubs. Continuous catalyst upgrades blur the historical performance gap, enabling hybrid products that echo copolymer toughness at near-homopolymer economics. This convergence keeps procurement teams attentive to total-installed-cost rather than headline resin price, sustaining homopolymer’s dominant share even as specialty grades expand.

Second-generation gas-phase reactors allow rapid grade switches, reducing transition scrap and favoring just-in-time logistics demanded by consumer-goods converters. Impact copolymers leveraging ethylene-propylene rubber domains gain traction in cold-climate automotive fascia owing to reliable low-temperature ductility. Random copolymers maintain a niche in medical syringes requiring gamma-sterilization stability. Yet rising sterilization-resistant additives in homopolymer blends signal potential future cannibalization. As additive master-batch formulations mature, homopolymer volumes could siphon incremental growth from copolymer, cementing their scale advantage.

By Processing Technology: Injection Molding Anchors Innovation

Injection molding captured 38.20% of polypropylene market consumption in 2025 and is projected to grow at 5.74% through 2031, buoyed by electric-vehicle interior demand and advancements in thin-wall packaging. The polypropylene market size for injection-molded parts reached 37.18 million tons in 2025 and is estimated to approach 52.01 million tons by 2031. Converters deploy high-speed cavity molds to slash cycle times, aligning with e-commerce volume spikes in takeaway containers and logistics totes. Microcellular-foam injection, made feasible by high-melt-strength grades, trims part weight by up to 18%, lowering shipping costs and greenhouse-gas footprints.

Extrusion molding and blow molding reside in specialized niches—battery jar casings and hot-fill bottles—where polypropylene’s creep resistance and chemical inertness remain unmatched. Across technologies, machine builders integrate real-time rheology sensors to stabilize production, optimizing throughput despite broader monomer price volatility.

By End-User Industry: Automotive Momentum Outpaces Packaging

Packaging dominated with a 51.10% stake in 2025, yet automotive is advancing at a 6.05% CAGR on the back of light-truck electrification programs in the United States and China. Under-hood reservoirs once specified in polyamide are shifting to glass-filled polypropylene, delivering 15% weight savings and avoiding moisture absorption issues. The polypropylene market share for automotive parts is forecast to climb from 13.18% by 2031, reflecting substitution momentum. In packaging, mono-material structures extend shelf life without aluminum foil, raising functional density and mitigating overall tonnage growth. Consumer products such as large-screen television housings remain linked to discretionary spending cycles, registering steady but muted growth.

Electrical and electronics applications find renewed interest as polypropylene’s dielectric properties facilitate capacitors in renewable-energy inverters within the polypropylene market, opening specialty compounding avenues. Medical disposables continue to adopt clarifier-enhanced random copolymers allowing steam sterilization, a trend magnified by demographic shifts toward single-use healthcare items. Across end-uses, regulatory stress on recycled content fuels demand for chemically-recycled grades, incentivizing long-term offtake partnerships between brand owners and resin suppliers.

Geography Analysis

Asia-Pacific’s 58.78% share underscores the region’s manufacturing heft, but China’s 68% production surge in 2025 spawned oversupply that pressured margins and spurred anti-dumping actions in Indonesia and the Philippines. Provincial governments are now scrutinizing environmental approvals for new PDH projects, tempering future capacity creep. India’s downstream demand is accelerating as consumer-goods penetration deepens; the country’s upcoming USD 8 billion ethane cracker promises to narrow import dependency, reshuffling intra-Asian trade.

North America leverages PDH feedstock advantages and proximity to a resurgent automotive sector in the polypropylene market, translating into competitive export offerings to South America and Europe. Ethane-rich shale gas underpins low propylene cash costs, enabling Gulf Coast plants to run at high utilization despite global volatility. Canada’s Sarnia-based crackers feed into Midwestern converters through well-established rail logistics, fortifying regional supply security.

Europe faces twin headwinds of elevated energy pricing and stringent waste regulations. Producers are evaluating permanent shutdowns or conversions to recycled-feedstock platforms to stay compliant with the EU Packaging and Packaging Waste Regulation. Concurrently, polymer trade flows from the Middle East into Europe expand as integrated refinery-petrochemical hubs exploit low naphtha costs, while Turkish converters act as trading gateways into the EU customs union. South America, largely import-dependent, is courting upstream investment; however, currency volatility and policy uncertainty delay large-scale grassroots projects.

Value Chain Analysis

Polypropylene value creation starts with upstream feedstocks and monomer production, centered on refineries and steam crackers (propylene as a co-product) plus on-purpose propylene routes such as PDH, followed by PP polymerization (homopolymer and copolymer) and downstream compounding. Propylene supply can tighten abruptly when naphtha cracker operating rates fall or assets close, because crackers are often the marginal propylene source, while on-purpose propylene and integrated PP units provide a more controllable stream. This feedstock linkage is material for procurement: industry commentary in 2026 highlighted reliability overtaking price as a purchasing priority, as resin availability can hinge on single cracker and propylene logistics nodes rather than PP reactor capacity alone.

Midstream players include global PP producers and technology licensors (for example, LyondellBasell Spheripol referenced in the competitive landscape), traders, and terminal operators, which move resin via bulk, rail, and containerized channels into converting hubs. Downstream, converters (injection molding, film extrusion/BOPP, fibers and nonwovens) and brand owners increasingly pull for design-for-recycling and circular feedstock claims; this is pushing the value chain to add certified recycled PP streams alongside virgin resin. A visible example is the July 2026 PureCycle Technologies partnership with Mitsui & Co. and RM TOHCELLO to introduce recycled polypropylene into BOPP film applications in Japan, linking recycler output to high-volume flexible packaging conversion and creating a pathway for premium, circular PP offtake.

Competitive Landscape

Global polypropylene supply is moderately concentrated, with the top five producers accounting for roughly 44% of installed capacity in the polypropylene market. Integrated majors leverage propylene technology licensing revenue to offset commodity margin cycles; LyondellBasell’s Spheripol platform remains a benchmark among grassroots projects. Middle Eastern players capitalize on co-located refineries, capturing feedstock synergies that support high utilization even in down cycles. Chinese state-owned conglomerates pursue scale, yet fragmented private PDH operators inject fresh competitive intensity by pricing aggressively to win offtake contracts.

Differentiation increasingly hinges on catalyst know-how and circular-economy credentials in the polypropylene market. Early adopters of chemical recycling secure brand-owner mandates commanding premiums up to USD 200 per ton over virgin grades. Specialty compounders targeting battery casing, medical syringe, and high-clarity containers position themselves as innovation partners rather than commodity suppliers. Mergers such as Adnoc-OMV-Nova’s creation of Borouge Group International exemplify the drive toward geographic and feedstock diversification. Over the forecast horizon, the battle for market relevance will pivot on securing low-carbon propylene, scaling chemical-recycling capacity, and tailoring grades to evolving regulations.

Polypropylene Industry Leaders

Exxon Mobil Corporation

SABIC

Sinopec

LyondellBasell Industries Holdings B.V.

Borealis AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Mono-material flexible packaging and higher-function PP film structures continue to be a primary whitespace for value uplift, as converters substitute away from hard-to-recycle multi-material laminates and pursue higher barrier performance within polypropylene-based designs. Activity is extending beyond virgin resin innovation into circular feedstock integration: in July 2026, PureCycle Technologies, Mitsui & Co., and RM TOHCELLO announced a route to bring recycled PP into BOPP film applications in Japan, pointing to an addressable gap where recycled PP needs qualification pathways for demanding film and food-adjacent applications. This also connects to producer-side investments aimed at design-for-circularity and grade performance, such as Borealis expanding Borstar Nextension PP production capabilities at Burghausen, Germany (EUR 49 million announced in January 2026).

A second opportunity cluster sits at the intersection of supply security, regional rebalancing, and specialty upgrading. Europe is actively rationalizing and reconfiguring production footprints where propylene availability is constrained; for example, LyondellBasell announced plans to shut down a 260,000-ton/year PP unit at Brindisi, Italy, by end-2026 following the loss of local propylene supply after the April 2025 closure of the Eni Versalis cracker. This environment supports opportunities for PDH-advantaged exporters and for integrated projects that improve local self-sufficiency, including large new builds progressing through late-stage execution. On the technology front, published academic work in 2026 describing high-efficiency PP chemical recycling using ionic liquids underscores continued innovation in depolymerization and circular feedstock routes, providing a technical basis for future commercialization where regulatory and brand-owner requirements demand traceable recycled content.

Recent Industry Developments

- July 2026: PureCycle Technologies announced a strategic partnership with Mitsui & Co. and RM TOHCELLO to introduce recycled polypropylene (PureFive resin) into biaxially oriented polypropylene (BOPP) film applications in Japan. The collaboration links recycled PP supply to a high-throughput packaging film format, expanding end-market eligibility beyond lower-spec applications. It also raises competitive pressure on virgin PP film grades where converters and brand owners are seeking circularity claims.

- August 2025: Vioneo selected Lummus as its polypropylene partner for an industrial-scale fossil-free plastics project from a green-methanol facility in Antwerp, Belgium. The tie-up anchors process technology selection for a differentiated PP pathway, targeting low-fossil or fossil-free positioning rather than conventional propylene economics. It signals increasing technology and offtake alignment around alternative feedstocks in the PP value chain.

- April 2024: OQ SAOC introduced new impact copolymer polypropylene grades at Chinaplas 2024, including OQLUBAN EP2340L, EP2340P, EP2348R, EP2348S, and EP2348T. The launch focused on improved flowability and dimensional stability, supporting higher productivity and tighter tolerances in molded applications. Product differentiation at major Asian converting hubs reinforces the shift toward performance-led portfolios alongside commodity volumes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as global demand and supply of polypropylene (PP) resin, used as a raw material for plastic processing and conversion, tracked across major producing and consuming regions and expressed in volume terms.

The scope excludes finished goods revenues from PP-based products and non-resin services, to avoid double counting beyond base polypropylene resin demand.

Segmentation Overview

- By Type

- Homopolymer

- Copolymer

- By Processing Technology

- Injection Molding

- Blow Molding

- Extrusion Molding

- Others

- By End-user Industry

- Packaging

- Automotive

- Consumer Products

- Electrical and Electronics

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

For the desk stage, we first pull public datasets to map where PP is produced, where it is consumed, and how trade shifts volumes between regions. Sources commonly referenced include UN Comtrade trade statistics, USGS materials data, International Energy Agency indicators (used for feedstock and energy context that can influence operating rates), US EPA publications around plastics and waste trends, and peer-reviewed polymer and recycling journals.

Next, we review company annual reports, investor presentations, and reputable industry press for capacity additions, shutdowns, and application demand signals that affect PP flows. Where needed, paid subscriptions are used for company financials and intelligence, patent databases, and shipment-level import and export checks to validate trade movement at a finer level. The specific sources named here are illustrative only, and additional public documents were also used for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure test what desk sources suggest, especially where capacity utilization, grade mix, and regional trade assumptions can move totals. We gather inputs from resin producers, converters, distributors, and large end users, and we include APAC, EMEA, and the Americas so regional supply-demand realities are reflected consistently in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | APAC: 47% |

| Mid tier: 48% | Functional/Unit leaders: 39% | EMEA: 33% |

| Smaller Players: 19% | Managers: 49% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where capacity by region, typical operating rates, and net trade flows are used to reconstruct the PP resin demand pool, which is then reconciled with known application consumption patterns. To keep the totals realistic, we corroborate the outputs with selective bottom-up checks such as sampled converter throughput discussions, distributor channel checks, and indicative volume math using typical processing route splits, before the final numbers are locked.

Key inputs in the PP model include announced capacity additions and shutdowns, utilization swings linked to feedstock economics, import and export balances, packaging and automotive output indicators, and changes in consumption between homopolymer and copolymer grades in processing routes like injection molding and films. When country-level data is thin, gap handling uses trade proxies and utilization ranges that are rechecked through interviews, then carried forward consistently to avoid artificial step changes.

Forecasting uses scenario analysis supported by time-series smoothing on the historical series, followed by expert-led adjustments for expected ramp-ups, outage recovery timing, and demand elasticity during resin price swings. This keeps the model comparable year to year, while still reflecting the operational realities PP markets face.

Data Validation & Update Cycle

Validation is done through practical checks so the results are not dependent on one dataset. We compare outputs against independent signals such as implied production versus nameplate capacity, net trade consistency over time, and whether regional demand movements align with end-use activity indicators. Outliers are then investigated and corrected.

Before sign-off, the model runs through review steps focused on unit consistency, assumption stability, and cross-region comparability, followed by a final coherence check across the time series. If a material event occurs, such as a large plant outage, a delayed start-up, or a policy-driven trade shift, respondents are re-contacted to confirm the impact. Reports are refreshed annually, with a final refresh pass completed close to delivery so clients receive the latest updated view.

Mordor Intelligence's Polypropylene Market Estimate Compared With Other Published Estimates

Published polypropylene market sizes often differ because some sources report the market in USD value, while others report it in physical volume, and the chosen base year can sit in a different pricing cycle. Estimates also diverge when adjacent items like compounded materials or converted product value are included on top of resin demand, or when trade and utilization assumptions are not cross-checked region by region.

The benchmark table shows this spread. Under Mordor Intelligence's scope, the 2026 figure is stated as resin volume (million tons) built from capacity, utilization, and net trade reconciliation, not as a value total that depends on an assumed average selling price path.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 102.67 M (2026) | |

| Industry Data Publisher A | USD 136.32 B (2024) | Expressed in USD value for a different base year, so the outcome is highly sensitive to resin price level assumptions, currency timing, and whether regional price spreads are modeled in detail. |

| Global Research Publisher B | USD 193.91 B (2025) | Value-based sizing with a later base year can embed a different price cycle and grade mix, and the totals can rise further if downstream polypropylene-based product value is counted beyond base resin demand. |

Taken together, the table suggests that most of the gap is explained by unit choice, base-year timing, and how pricing is translated into value, not by a different view of where PP demand is used. Our approach stays easier to audit because key totals can be traced back to operational metrics like capacity and trade, and then checked against what market participants report.

Key Questions Answered in the Report

What is the projected global demand in polypropylene market by 2031?

Global demand is expected to reach 134.29 million tons by 2031, reflecting a 5.52% CAGR.

Which application is forecast to grow fastest through 2031?

Automotive components are slated to expand at 6.05% annually, outpacing packaging and consumer goods.

How does PDH technology influence polypropylene market costs?

PDH units offer feedstock flexibility that can lower integrated cash costs by up to USD 130 per ton versus naphtha routes, enhancing regional competitiveness.

Why are mono-material packaging structures gaining traction?

Brand-owner recyclability targets and regulatory fees on non-recyclable waste are driving converters to adopt barrier-coated mono-polypropylene films.

Page last updated on: