Zinc Chloride Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

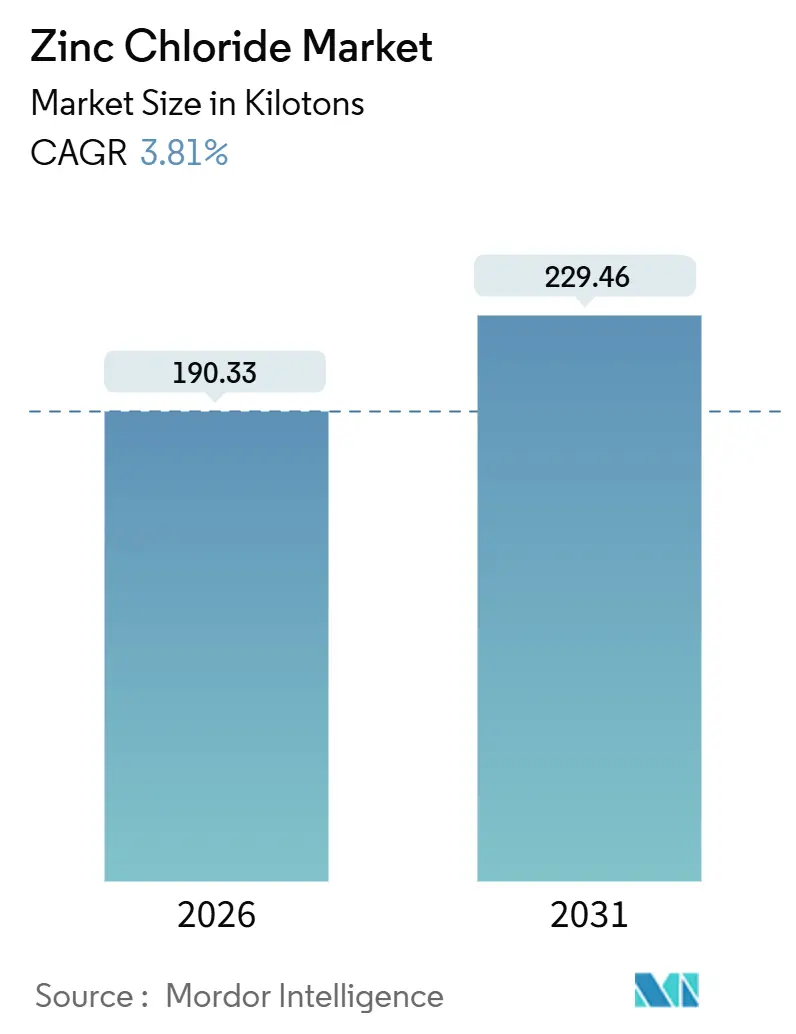

| Market Volume (2026) | 190.33 kilotons |

| Market Volume (2031) | 229.46 kilotons |

| Growth Rate (2026 - 2031) | 3.81% CAGR |

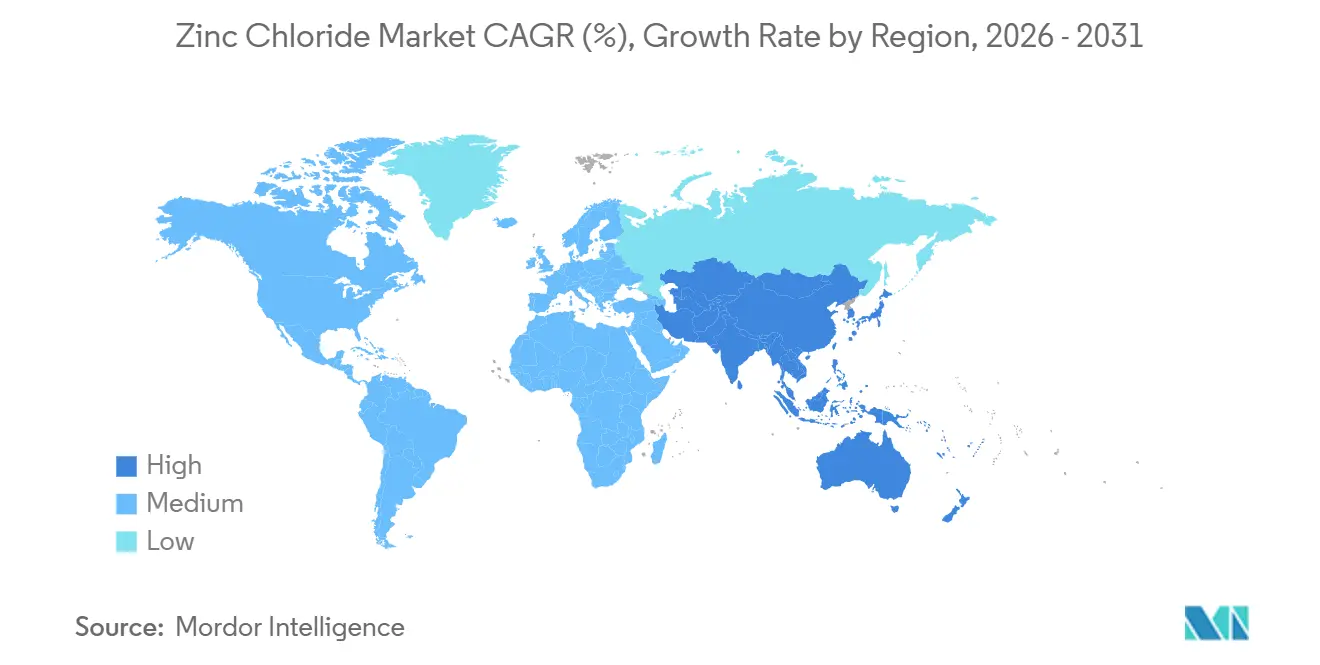

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

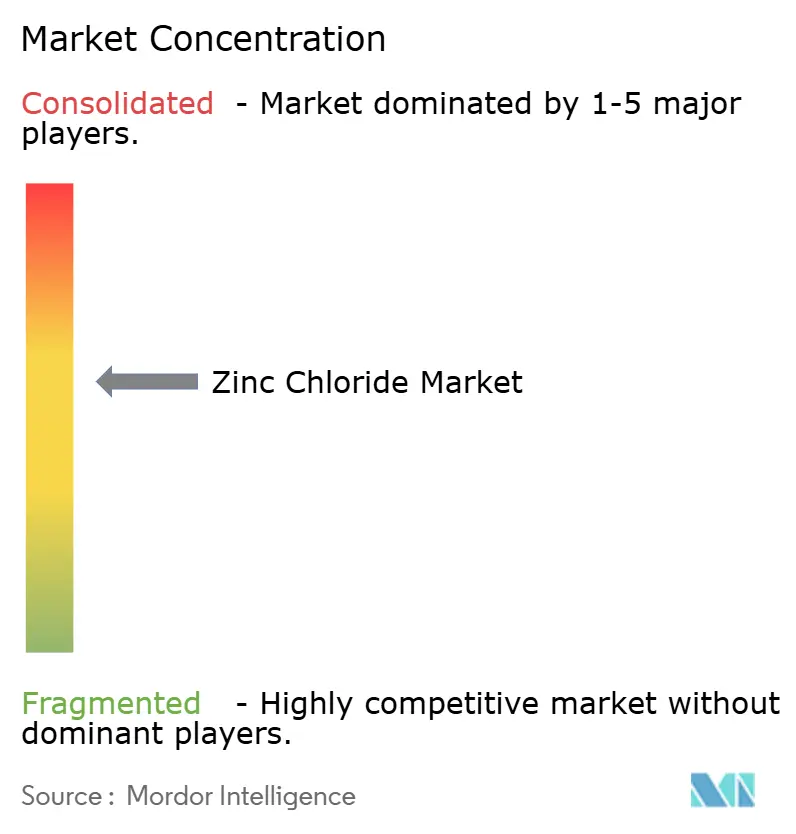

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Zinc Chloride Market Analysis by Mordor Intelligence

The Zinc Chloride Market size is estimated at 190.33 kilotons in 2026, and is expected to reach 229.46 kilotons by 2031, at a CAGR of 3.81% during the forecast period (2026-2031). Growing municipal investments in tertiary wastewater treatment, pilot-scale adoption of aqueous zinc-ion batteries, and the continuing shift from ammonium- to zinc-based galvanizing fluxes are underpinning demand growth. Integrated smelters with captive metal feedstock are shielding margins from zinc price volatility and leveraging low-carbon credentials to secure forward contracts in Europe and North America. Meanwhile, research groups in China and India are demonstrating deep-eutectic solvent and quick-setting cement formulations that widen the downstream aperture for zinc chloride, adding fresh avenues for value creation. Competitive intensity remains moderate because a handful of vertically integrated producers enjoy economies of scale, while high-purity grades command defensible premiums through stringent impurity controls and DMF filings.

Key Report Takeaways

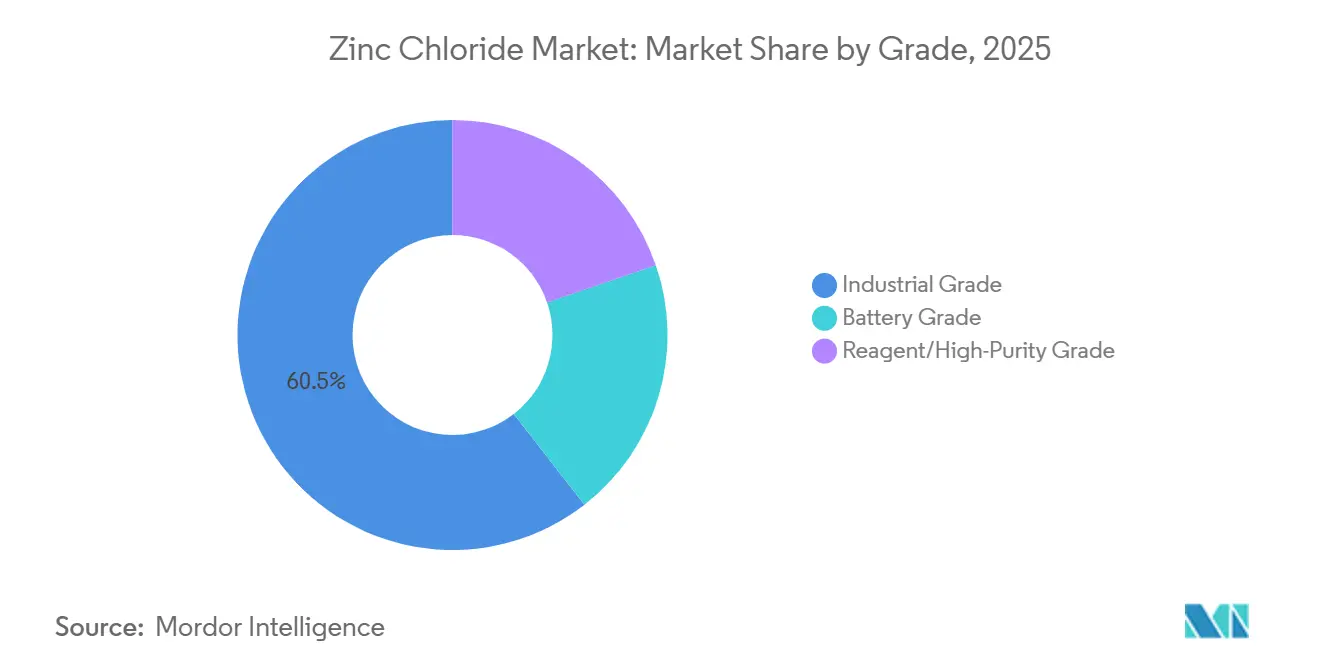

- By grade, industrial grade captured 60.51% of zinc chloride market share in 2025, whereas battery grade is forecast to expand at a 5.63% CAGR to 2031.

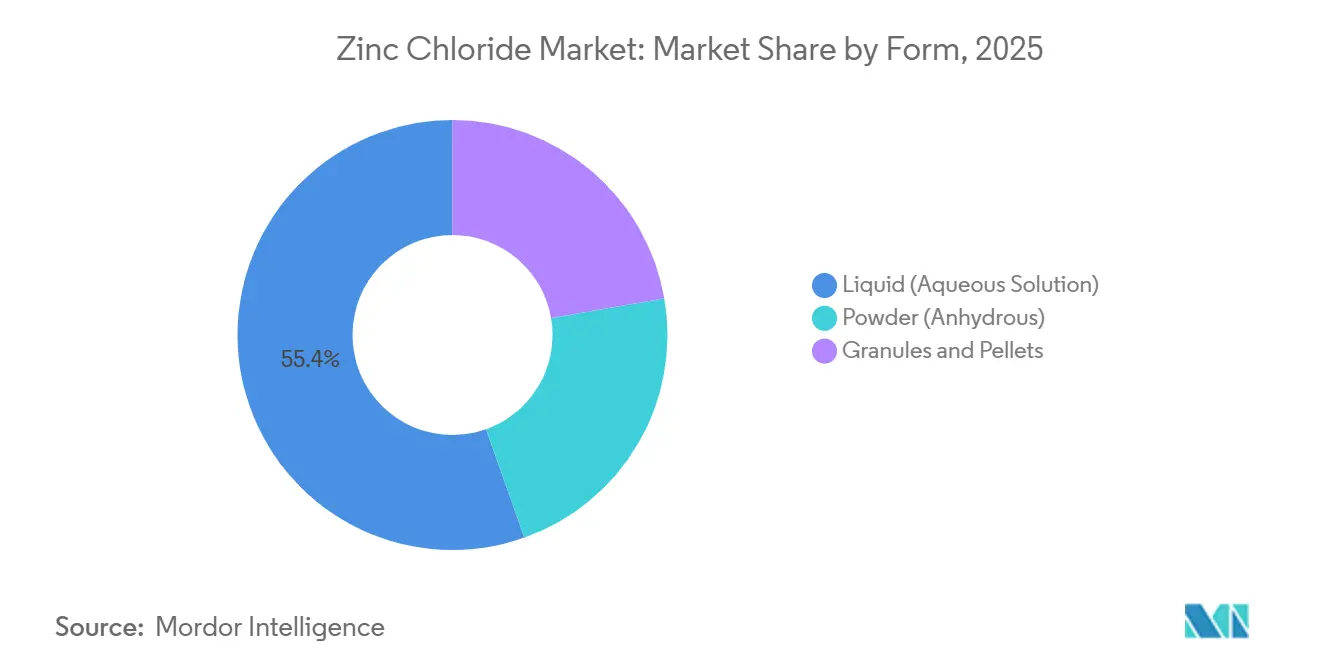

- By form, liquid (aqueous solution) accounted for 55.44% of the zinc chloride market size in 2025, while granules and pellets are pacing ahead at a 4.81% CAGR through 2031.

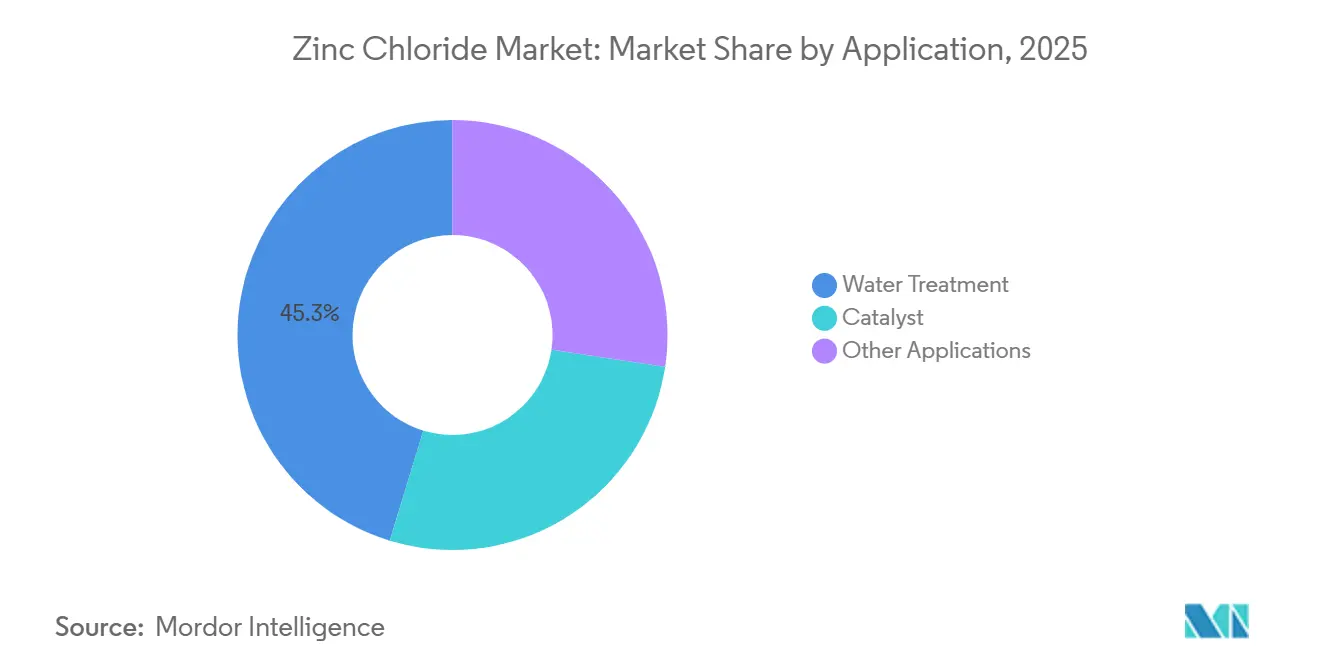

- By application, water treatment led with 45.29% revenue share in 2025; catalyst is set to grow at a 4.92% CAGR to 2031.

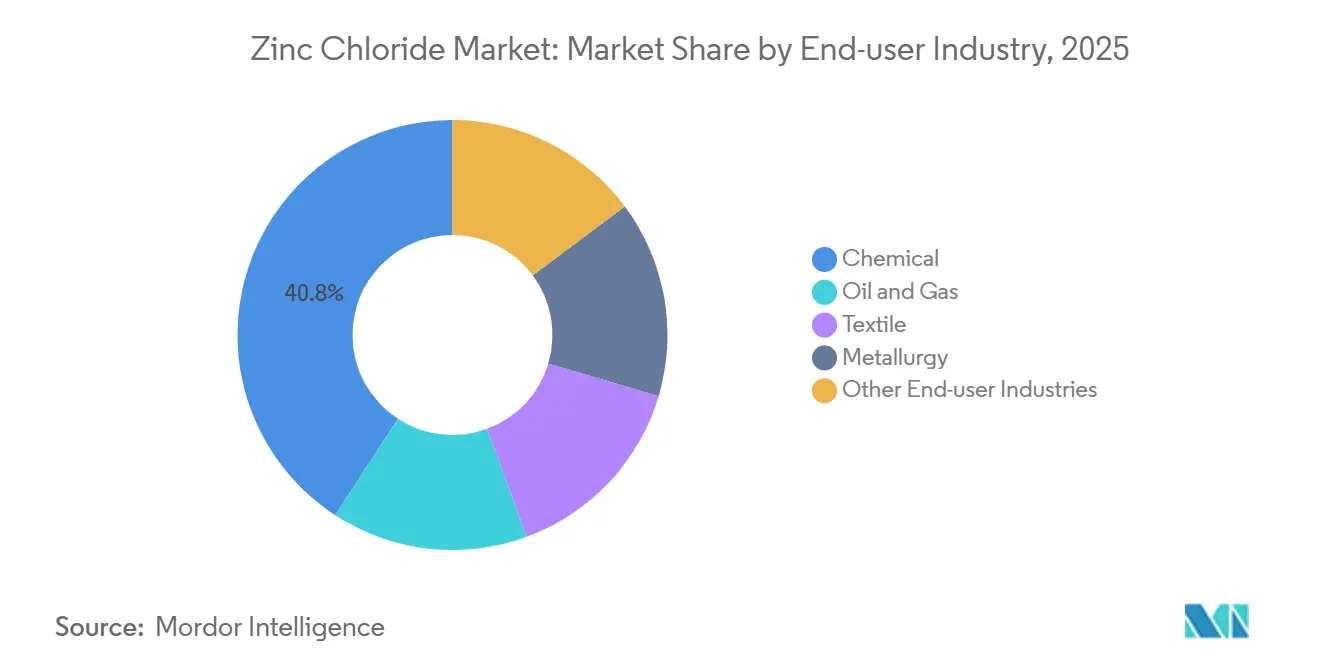

- By end-user industry, chemicals retained 40.81% of the zinc chloride market share in 2025, yet oil and gas is projected to post a 5.01% CAGR to 2031.

- By geography, Asia Pacific dominated with 45.83% zinc chloride market share in 2025 and is tracking a 4.75% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Zinc Chloride Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of water-scarce municipalities boosting ZnCl₂ wastewater disinfection | +1.2% | APAC (India, China), Middle-East, North Africa | Medium term (2-4 years) |

| Battery-grade ZnCl₂ demand from lithium-free zinc-ion pilot projects | +0.9% | Global, with concentration in China, Japan, South Korea | Long term (≥4 years) |

| Ammonium-chloride substitution by ZnCl₂ in galvanizing fluxes | +0.7% | North America, Europe, APAC (China, India) | Short term (≤2 years) |

| Emergence of ZnCl₂-based deep-eutectic solvents for biomass fractionation | +0.5% | Europe, North America, APAC (China) | Medium term (2-4 years) |

| Quick-setting low-carbon cement using ZnCl₂-activated alkali binders | +0.4% | APAC (China, India), Middle-East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Water-Scarce Municipalities Boosting ZnCl₂ Wastewater Disinfection

Acute water stress across India, North Africa, and parts of China is impelling utilities to retrofit tertiary treatment stages that rely on zinc chloride for simultaneous heavy-metal precipitation and microbial inactivation. Zinc ions form stable complexes with phosphates and sulfides, trimming chemical oxygen demand while delivering broad-spectrum antimicrobial activity. Field trials in Gujarat showed that adding 65% ZnCl₂ solution to textile effluents cut biological oxygen demand by 30% and enabled dye-house water recycling at industrial scale. Vertically integrated suppliers in South Asia are capitalizing on this pull by offering bulk liquid ZnCl₂ under long-term offtake agreements priced against a zinc LME index. Regulatory drives that mandate zero-liquid discharge in the Gulf Cooperation Council countries are accelerating uptake of the same chemistry in desalination plants. Overall, tightening freshwater budgets and escalating discharge fees reinforce this structural driver through 2031.

Battery-Grade ZnCl₂ Demand from Lithium-Free Zinc-Ion Pilot Projects

Laboratory breakthroughs in aqueous zinc-ion cells are translating into multimegawatt pilot lines in China and South Korea. A four-electron Zn-I₂ cell using 2 M ZnCl₂ delivered 20,000 stable cycles and 723 Wh/kg based on iodine mass, bringing parity with stationary lithium-iron-phosphate batteries[1]Dalian Institute of Chemical Physics, “Biphasic Electrolyte Strategy for Aqueous Zinc Batteries,” dicp.cas.cn . Because transition-metal impurities catalyze parasitic hydrogen evolution, battery developers specify ≥99.995% purity zinc chloride with total heavy metals less than 50 ppm. Producers that document Scope-3 footprints below 1 tCO₂e per tonne of ZnCl₂ are now entering approved-vendor lists for data-center backup projects in Jiangsu province. Industry association roadmaps expect cumulative global demand for battery-grade zinc chloride to grow five-fold by 2031, although ramp-up will be gated by refinery-level purification capacity.

Ammonium-Chloride Substitution by ZnCl₂ in Galvanizing Fluxes

Steel coaters in Europe, North America, and China are phasing out pure ammonium chloride fluxes in favor of zinc-ammonium chloride blends rich in ZnCl₂ to curb ammonia fume emissions. Trials on high-carbon plate showed a 12% reduction in white rust incidence when surface pre-flux ZnCl₂ content exceeded 55%. A 2024 European patent discloses recovering ZnCl₂ from galvanizer sludge via controlled chlorination, reducing virgin zinc input by 18%. As environmental permits tighten around ammoniacal emissions, flux formulators see steady conversion momentum over the next two years, adding uplift to industrial-grade zinc chloride consumption.

Emergence of ZnCl₂-Based Deep-Eutectic Solvents for Biomass Fractionation

Deep-eutectic solvents containing zinc chloride and lactic acid dissolve lignin selectively, enabling recovery of cellulose fibers for bioplastic feedstocks. Poplar wood delignification efficiencies above 97% were achieved at 120 °C, with ZnCl₂ recycled nine times without measurable loss in activity. Pilot demonstrations in Saxony and Jiangsu aim to process 50 kilotons of agricultural residues annually by 2028. The circular-bioeconomy incentives embedded in the EU Green Deal and China’s dual-carbon policy underpin medium-term adoption, especially as solvent cost curves improve through closed-loop metal recovery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU waste-brine regulations on liquid ZnCl₂ disposal | -0.6% | Europe (EU27, UK) | Short term (≤2 years) |

| Zinc metal price volatility compressing tier-2 producer margins | -0.5% | Global, acute in Asia Pacific and South America | Short term (≤2 years) |

| PFAS-like regulatory scrutiny on zinc-salt leachates | -0.3% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent EU Waste-Brine Regulations on Liquid ZnCl₂ Disposal

Revisions to the Waste Framework Directive in 2024 classified liquid zinc chloride at ≥10% concentration as an H410 chronic aquatic toxin, obligating closed-loop or high-temperature incineration with flue-gas scrubbing[2]European Chemicals Agency, “Harmonised Classification for Zinc Chloride,” echa.europa.eu . Textile processors in Portugal estimate compliance raises effluent treatment costs by 20%, nudging them toward granular zinc chloride that falls outside liquid-waste thresholds. REACH registration dossiers must now detail cradle-to-gate metal balances, encouraging galvanizers to crystallize and re-dissolve on-site rather than ship bulk solution. These measures exert immediate headwinds on European demand for liquid grades until solid handling systems scale up.

Zinc Metal Price Volatility Compressing Tier-2 Producer Margins

Spot zinc climbed to 126 cents per pound on the LME in 2024, a 4.9% year-on-year jump, before spiking above USD 3,000 per tonne during a short squeeze in October 2025. Producers without captive smelters pass through only part of the cost rise due to quarterly contracts with galvanizers and textile firms. Margins for Chinese toll converters dipped below 5% in 2025, triggering shutdowns of smaller batch plants in Hebei. By contrast, integrated players such as Korea Zinc hedge risk by reallocating metal between cathode copper foil and zinc chloride lines to balance profitability. Volatility remains a structural risk, pressing independent operators to secure long-term metal offtake or pursue forward hedging, both of which tie up working capital.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Battery-Purity Edges Toward Commercial Scale

Battery-grade is forecast to grow at a 5.63% CAGR, making it the fastest-expanding grade. Developers of zinc-iodine and zinc-air prototypes specify chloride salts with sub-ppm nickel and copper to avoid dendrite formation. A leading Chinese producer validated 30 M zinc chloride electrolyte that cuts hydration shells and raises Coulombic efficiency above 99.5%. In contrast, the bulk of the zinc chloride market size still resides in industrial grade with 60.51% market share in 2025 due to galvanizing fluxes and chemical synthesis, where impurity constraints are looser, and price sensitivity remains acute. Producers offering life-cycle-assured, low-carbon battery grade command premiums of 20-25% over commodity rates.

By Form: Granular Adoption Accelerates in Europe

Liquid (aqueous solution) remains the workhorse format with 55.44% share in 2025 due to ease of dosing, yet granular and pellet forms are registering 4.81% CAGR as galvanizers in Germany, Spain, and France shift to dry flux blends that limit ammoniacal emissions. Granules also eliminate spill-response costs, an advantage that resonates under the EU’s tightened hazardous-waste codes. Southeast Asian output is set to climb after AGC’s chlor-alkali expansion in Thailand goes on-stream in 2027, lowering the regional chlorine cost base and enlarging supply for anhydrous zinc chloride pellets. Powdered forms retain niche demand in pharmaceutical synthesis and laboratory reagents where moisture exclusion is paramount.

By Application: Catalysts Outpace the Base

Water treatment accounts for 45.29% market size in 2025, propelled by the reuse mandates in drought-stricken megacities. Yet catalyst applications for deep-eutectic solvents, Friedel–Crafts reactions, and cellulose dissolution are projected to outpace the base at 4.92% CAGR. A European pulp mill converting sawdust to cellulosic sugars with a ZnCl₂-lactic deep-eutectic solvent logged nine solvent recycles without performance drop, slashing variable cost per tonne of output. The success of such pilots underpins rapid scaling in both Europe and coastal China.

By End-user Industry: Oil and Gas Leads Growth

While the chemical sector dominates the market with 40.81% share, oil and gas present the fastest growth as offshore projects pivot back online. Completion fluids blending zinc bromide with zinc chloride reach densities up to 19.2 lb/gal, suitable for ultra-deep wells in the Gulf of Mexico and Brazil. Scale inhibitors formulated with ZnCl₂ record 90% ion-capture efficiency, extending tubing life in high-salinity reservoirs. As upstream capex rebounds, demand for oil-field-grade zinc chloride rises in tandem.

Geography Analysis

Asia Pacific maintained 45.83% zinc chloride market share in 2025, supported by Shandong’s smelting hub and India’s capacity ramp-up. China’s single-site 50,000 t/y plant delivers sub-USD 1,000/t liquid product thanks to chlorine integration and captive power. India leverages Hindustan Zinc’s renewable electricity to position low-carbon derivatives for export into Europe’s carbon-border adjustment mechanism. Robust galvanizing and water-treatment activity drives Asia Pacific’s regional CAGR of 4.75% to 2031.

North America benefits from strong oilfield fluid offtake, whereas Europe’s stricter disposal codes temper growth but spur product-mix upgrades toward pellets and reclaimed ZnCl₂. Southeast Asia gains cost advantage once Thai chlor-alkali expansions stabilize chlorine supply, permitting local pellet manufacturing for cement additives. Africa and the Middle-East exhibit steady uptake tied to desalination brine processing and municipal water reuse.

Competitive Landscape

The zinc chloride market features integrated miners such as Hindustan Zinc and Korea Zinc alongside regional chemical specialists. Together, the top five suppliers hold roughly 43% of global capacity, yielding a market concentration score of 6. Recent strategy pivots include Korea Zinc’s USD 13 billion decarbonization and battery-materials program, positioning it for captive battery-grade ZnCl₂ streams. Metrochem and ChemCon defend high-purity niches through DMF filings and ISO-accredited cleanrooms. Cost-led Chinese players focus on bulk industrial grade, while European formulators differentiate with REACH-registered, pelletized products tailored to waste-brine regulations. Emerging disruptors stem from zinc-ion battery consortia that seek audited traceability for electrolyte salts.

Zinc Chloride Industry Leaders

TIB Chemicals AG

Zaclon LLC

Global Chemical Co., Ltd.

Pan-Continental Chemical Co., Ltd.

Weifang Hengfeng Zinc Industry

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Salgenx launched a 3,000 kWh zinc chloride saltwater battery, specifically designed for cost-effective, large-scale energy storage and housed in a standard 40-foot high cube shipping container. Its design accommodated the natural expansion of zinc during the charging process, preventing short circuits and enhancing the battery's operational lifespan.

- April 2024: TIB Chemicals AG reopened its modernized zinc chloride plant in Ludwigshafen, Germany, after extensive renovations aimed at enhancing efficiency and meeting environmental standards.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the zinc chloride market as the sale of anhydrous or hydrated ZnCl2, delivered in liquid or solid forms, to downstream users in water treatment, galvanizing, catalysts, batteries, textiles, and pharmaceuticals.

Scope Exclusion: Downstream zinc derivatives such as zinc sulfate, zinc phosphate, and blended micronutrient formulations lie outside this scope.

Segmentation Overview

- By Grade

- Industrial Grade

- Battery Grade

- Reagent/High-Purity Grade

- By Form

- Liquid (Aqueous Solution)

- Powder (Anhydrous)

- Granules and Pellets

- By Application

- Water Treatment

- Catalyst

- Other Applications

- By End-user Industry

- Chemical

- Oil and Gas

- Textile

- Metallurgy

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed procurement leads at galvanizers, dry-cell makers, and municipal chemical buyers across Asia-Pacific, Europe, and North America. These conversations validated prevailing contract prices, purity splits, and expansion plans that secondary data alone could not pinpoint.

Desk Research

We blended openly available statistics from UN Comtrade (HS 282739), USGS Mineral Industry Surveys, Eurostat chemicals output, and the China Customs Yearbook with perspectives from the International Zinc Association, American Water Works Association, and World Battery Alliance. Corporate 10-Ks, tender portals, and press archives on Dow Jones Factiva rounded out capacity, contract, and plant-startup clues. Questel patent analytics and IMARC's public price dashboard supplied forward-looking signals. The sources noted are illustrative; many additional datasets were reviewed for triangulation.

Market-Sizing & Forecasting

We begin with a top-down reconstruction: global production plus net trade is cleansed of captive use and multiplied by region-specific average selling prices to set the 2025 baseline. Bottom-up roll-ups of sampled supplier shipments and average sales prices cross-verify totals. Key variables include dry-cell output, wastewater-treatment capex, zinc metal-acid spread, and import-duty shifts; forecasts to 2030 employ multivariate regression with ARIMA price paths moderated by expert consensus. Purity factors from interviews adjust customs rows that bundle other zinc salts.

Data Validation & Update Cycle

Outputs face variance checks, peer reviews, and anomaly loops; material events trigger interim patches. Reports refresh annually, and an analyst performs a final sweep before delivery, so clients always receive the most current view.

Why Mordor's Zinc Chloride Baseline Commands Reliability

Published estimates often diverge because firms apply different purity cut-offs, freight assumptions, and refresh cadences.

Our disciplined reconciliation of tonnage flows and transaction-level prices minimizes these distortions. Key gap drivers across other studies include broader chemical scope, historic (2019) price decks, or omission of captive water-treatment volumes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| Mordor Intelligence | 183.51 kt (2025) | Mordor Intelligence | - |

| Regional Consultancy A | USD 320 M (2024) | Regional Consultancy A | Includes flocculant blends; uses historic prices |

| Trade Journal B | USD 350 M (2024) | Trade Journal B | Excludes captive use; freight ignored |

These contrasts show that Mordor's transparent, annually refreshed approach gives decision-makers a balanced baseline that can be traced back to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the size of zinc chloride market?

What is the size of the zinc chloride market?

Which grade is growing fastest in the zinc chloride space?

Battery-grade zinc chloride is set to expand at a 5.63% CAGR over 2026-2031 on the back of zinc-ion battery pilots.

Why are liquid zinc chloride users in Europe shifting to pellets?

EU disposal rules classify concentrated liquid ZnCl₂ as a chronic aquatic toxin, so pellets help avoid costly waste-brine compliance.

How does zinc chloride support oilfield operations?

It densifies completion fluids and improves scale-inhibitor retention above 90%, which is critical for deep offshore wells.

Page last updated on: