Market Overview

| Study Period | 2021 - 2031 |

|---|---|

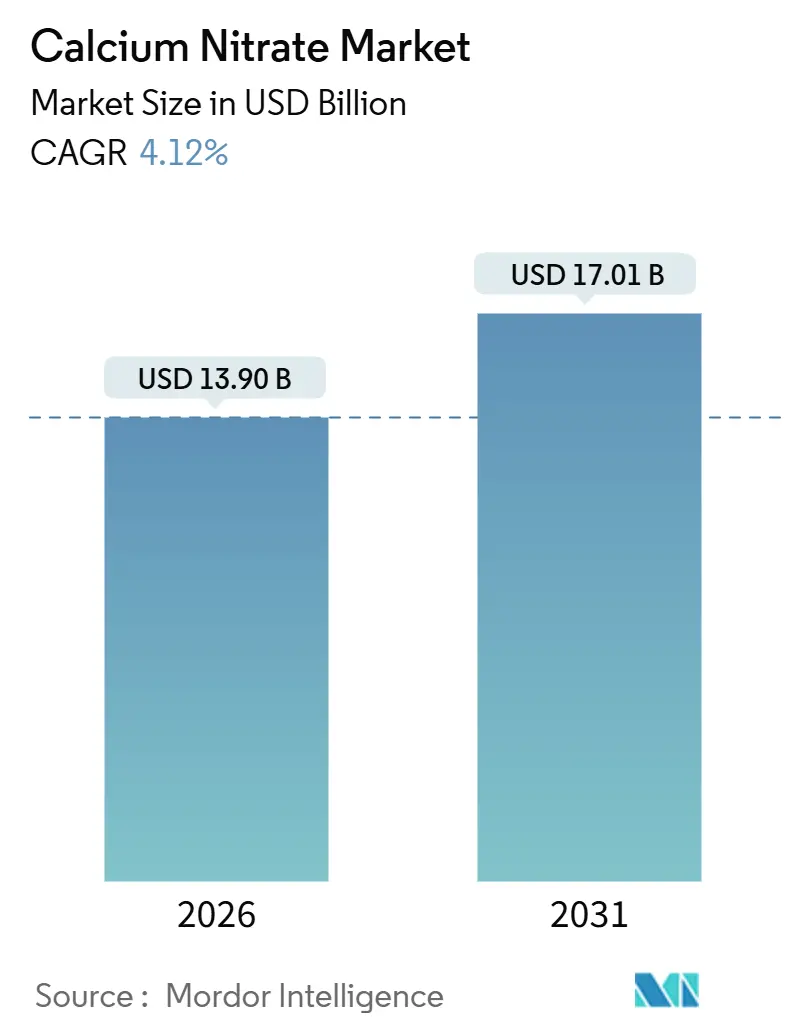

| Market Size (2026) | USD 13.90 Billion |

| Market Size (2031) | USD 17.01 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Calcium Nitrate Market Analysis by Mordor Intelligence

The Calcium Nitrate Market size is estimated at USD 13.90 billion in 2026, and is expected to reach USD 17.01 billion by 2031, at a CAGR of 4.12% during the forecast period (2026-2031). Widespread adoption of drip, micro-sprinkler, and pivot systems is steering growers toward fully water-soluble nitrate sources that integrate smoothly with fertigation equipment. The European Union’s carbon-adjustment levy on high-emission nitrogen fertilizers is widening the price gap between conventional and low-carbon options, rewarding producers that have invested in renewable-ammonia or carbon-capture routes. Urban vertical-farm operators and greenhouse vegetable producers in Asia-Pacific and North America prefer chloride-free calcium nitrate solutions to avert blossom-end rot and tip burn in premium produce. Meanwhile, wastewater utilities worldwide are scaling up nitrate dosing to curb hydrogen-sulfide generation, creating a complementary industrial demand stream.

Key Report Takeaways

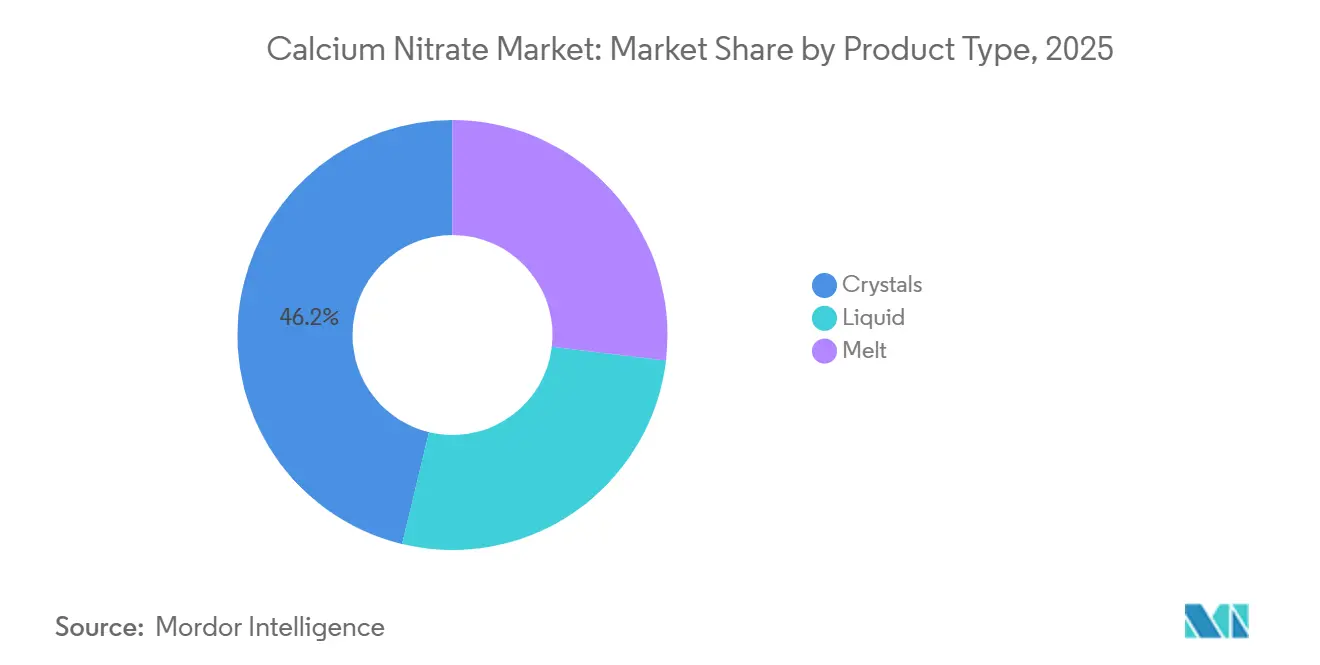

- By product type, crystals accounted for 46.22% revenue share of the calcium nitrate market in 2025; liquid is expanding at a 4.21% CAGR through 2031.

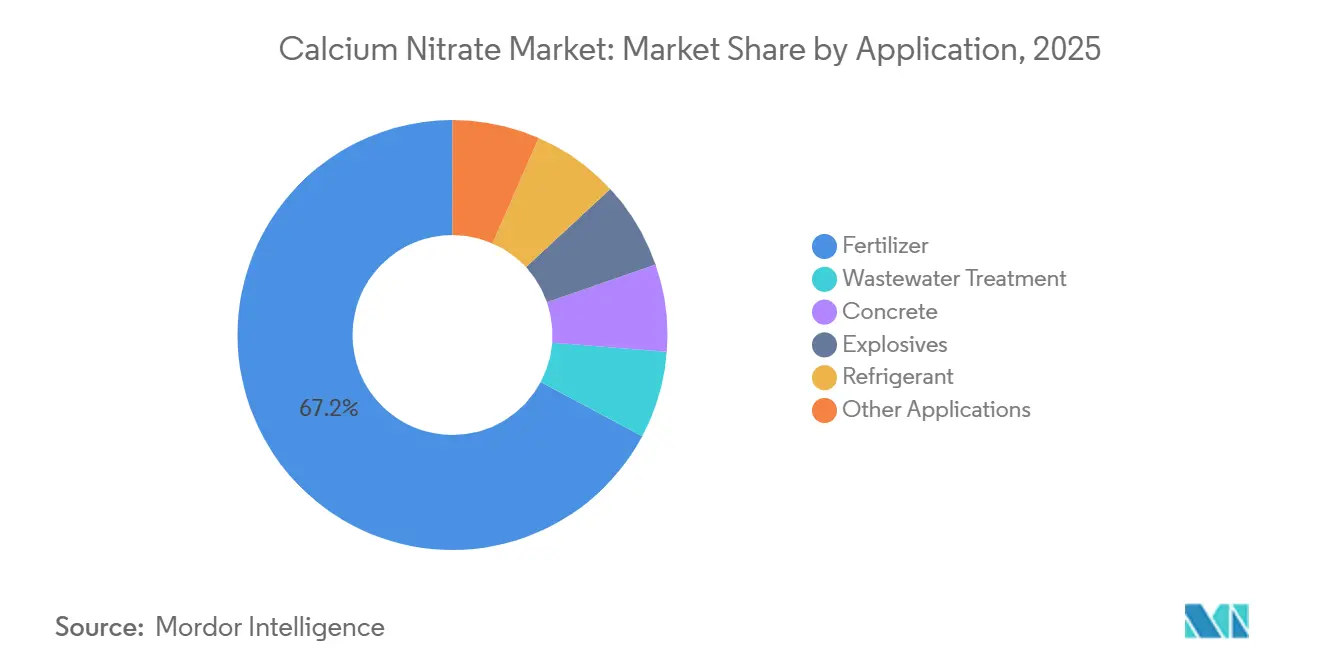

- By application, fertilizer represented 67.18% of demand in 2025, while wastewater treatment is advancing at a 4.78% CAGR to 2031.

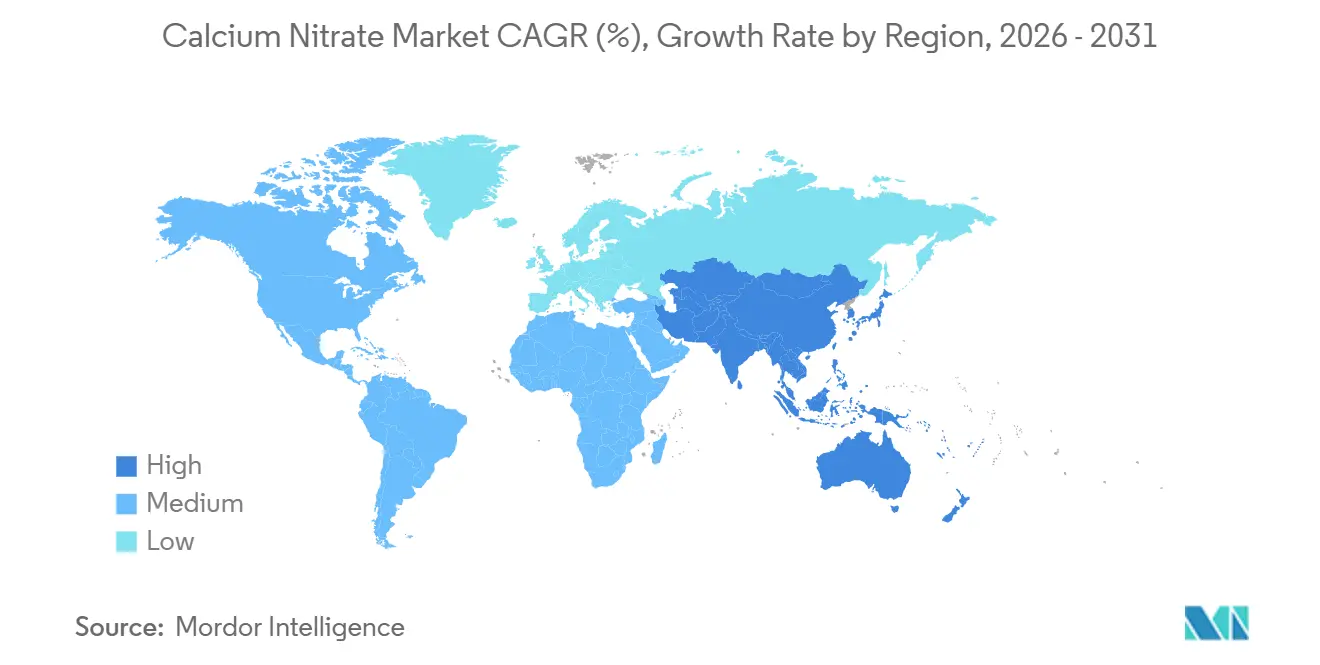

- By geography, Asia-Pacific led with 41.98% calcium nitrate market share in 2025 and is forecast to grow at 5.41% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Calcium Nitrate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Specialty Water-Soluble Fertilizers Boom | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2–4 years) |

| Urban Vertical-Farm Fertigation Demand | +0.8% | North America, Europe, ASEAN urban clusters | Medium term (2–4 years) |

| Calcium-Deficiency Disorders in High-Value Crops | +0.7% | Global, particularly Mediterranean and tropical zones | Short term (≤ 2 years) |

| EU CBAM-Ready Low-Carbon Nitrate Push | +0.6% | Europe, with spillover to export-oriented producers globally | Long term (≥ 4 years) |

| On-Site Anhydrous Calcium Nitrate for CSP Salts | +0.3% | Middle East, North Africa, Southwestern United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Specialty Water-Soluble Fertilizers Boom

Precision irrigation is replacing broadcast spreading in water-scarce regions. Because calcium nitrate dissolves completely and contains no chloride, it is the preferred source of nitrogen and calcium for fertigation. Commercial grades such as Haifa’s Cal Prime deliver 17.0% total nitrogen—nearly all in nitrate form—and 23.5% water-soluble calcium, enabling concentrated stock solutions that lower freight costs and stabilize nutrient pH. Asia-Pacific governments subsidize micro-irrigation under China’s 14th Five-Year Plan and India’s Pradhan Mantri Krishi Sinchayee Yojana, lifting demand for fully soluble grades. Formulation innovation, exemplified by Croda Agriculture’s PiNT technology that slows ureic nitrogen release, bolsters overall adoption of complementary calcium nitrate inputs.

Urban Vertical-Farm Fertigation Demand

Vertical farms, rooftop greenhouses, and plant factories operate closed-loop hydroponic or aeroponic systems that mandate ultra-pure nutrient salts. Calcium nitrate, typically supplied in two-part recipes to prevent phosphate or sulfate precipitation, is central to these formulations. Yara’s greenhouse-grade Calcinit dissolves at 1,200 g L⁻¹ at 20 °C, leaving no residue that could clog emitters. New facilities in Singapore, the Netherlands, and the United States consume 5–10 kg of calcium nitrate per cubic meter of nutrient solution per crop cycle, providing steady, season-independent demand. Venture capital funding and corporate investments in metropolitan food production amplify this structural pull.

Calcium-Deficiency Disorders in High-Value Crops

Physiological disorders such as blossom-end rot and tip burn emerge when rapidly growing tissues lack calcium, even in calcium-rich soils. Foliar or fertigation treatments with calcium nitrate address both nutrient deficiency and nitrate supply, improving translocation efficiency and cell-wall strength. Ases Chemical Works recommends pre-plant applications of 4–8 kg acre⁻¹ and foliar sprays at 15% weight-per-volume to prevent these disorders. Economic stakes are high: a single blossom-end-rot episode can render up to 40% of a tomato crop unmarketable, prompting consistent inclusion of calcium nitrate in greenhouse and open-field nutrition programs.

On-Site Anhydrous Ca-Nitrate for CSP Salts

Concentrated solar power plants in arid regions blend anhydrous calcium nitrate with sodium and potassium nitrates to create ternary eutectic salts that melt near 130 °C. While these mixtures lower freezing points, they restrict the upper working temperature to roughly 450 °C, necessitating careful thermal-cycle design[1]National Oceanic and Atmospheric Administration, “Chemical Hazards—Calcium Nitrate,” noaa.gov . New projects in the Middle-East and North Africa adopt on-site nitrate synthesis to secure supply, adding incremental demand for industrial-grade calcium nitrate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Organic and Bio-Based Fertilizers | -0.5% | Europe, North America, niche segments in Asia-Pacific | Medium term (2–4 years) |

| Ammonia/Nitric-Acid Price Volatility | -0.7% | Global, with acute exposure in import-dependent regions | Short term (≤ 2 years) |

| Denitrifying Bioreactors Replacing Nitrate Dosing | -0.2% | North America (Midwest), Europe (agricultural drainage zones) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Organic and Bio-Based Fertilizers

Policy incentives and consumer preferences are pushing land toward certified organic production in Europe and North America, where organic acreage grew by up to 10% annually in recent years. Organic standards prohibit synthetic nitrates, diverting demand to composts and microbial inoculants. The European Farm to Fork Strategy targets a 20% fertilizer-use reduction by 2030, with subsidies that reward low-input regimes. Although organic nutrient sources still account for a small slice of total nitrogen consumption, they displace calcium nitrate in premium vegetables, fruits, and wine grapes, particularly in Northern Europe and California.

Denitrifying Bioreactors Replacing Nitrate Dosing

Some U.S. Midwest and European drainage projects are installing wood-chip or substrate-filled bioreactors that foster denitrifying bacteria, reducing the need for chemical nitrate addition in municipal sewer lines. While adoption remains localized, successful pilots show 50%-plus hydrogen-sulfide reduction without external nitrate, posing a long-run substitution threat to calcium nitrate in odor-control applications[2]U.S. Geological Survey, “Wood-chip Bioreactors for Nitrate Removal,” usgs.gov . Scaling hinges on land availability and maintenance costs, so market impact will unfold gradually.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Crystals Anchor Bulk Use, Liquids Gain in Precision Systems

Crystals held 46.22% of revenue in 2025, underscoring their role in broad-acre and orchard nutrition programs. Growers appreciate the cost-efficiency of crystalline calcium nitrate tetrahydrate delivered in moisture-resistant bags that dissolve quickly in mix tanks. The calcium nitrate market size for crystals is expected to expand steadily, supported by greenhouse operators that dissolve crystals in stock tanks. Liquid formulations, sold at 9%–11% nitrogen and 14%–19% calcium, are advancing at a 4.21% CAGR. Precision fertigation adopters value the labor savings and uniformity that pre-dissolved solutions provide, especially when injected through computerized dosing pumps. Norkem’s 2024 launch of granular calcium nitrate illustrates continued innovation in the crystals category by offering a slower nutrient-release profile that mitigates leaching in high rainfall zones.

Industrial buyers form a niche but stable outlet. Anhydrous calcium nitrate melt blends into ternary CSP salts such as Hitec XL, enabling lower melting points but capping operating temperatures at 450 °C. Concrete admixture producers rely on calcium nitrate as a non-chloride set accelerator compliant with ASTM C494 Type C and Type E, a use reaffirmed in the Federal Highway Administration’s 2024 technical brief. Collectively, these industrial channels diversify demand and cushion the calcium nitrate market against agricultural cycles.

By Application: Fertilizer Dominates, Wastewater Treatment Surges

Fertilizer represented 67.18% of overall consumption in 2025, reflecting calcium nitrate’s dual nutrient benefit in intensive horticulture. The calcium nitrate market size for fertilizer applications will continue to climb as growers pursue higher nutrient-use efficiency. Wastewater treatment is the fastest-growing application at 4.78% through 2031. Utilities dose 50–200 mg L⁻¹ nitrate-nitrogen to suppress sulfate-reducing bacteria and to supply readily available carbon for denitrification, a practice endorsed by several U.S. state water agencies. Concrete, explosives, and refrigeration each account for smaller but persistent shares, with concrete admixture demand receiving fresh validation from the 2024 FHWA guidance that emphasized proper dosage control.

Industrial versatility sustains the calcium nitrate market during agricultural downturns. For instance, explosives manufacturers blend calcium nitrate into ammonium-nitrate-fuel-oil (ANFO) formulations to boost detonation velocity, while refrigeration engineers explore eutectic phase-change slurries that leverage calcium nitrate’s latent-heat properties for cold-chain logistics. This portfolio effect underpins a resilient growth outlook even amid regulatory and feedstock headwinds.

Geography Analysis

Asia-Pacific controlled 41.98% of the calcium nitrate market in 2025 and is forecast to grow at 5.41% through 2031. China’s 1.2 million ha greenhouse base is pivoting toward soilless systems that rely on ultrapure calcium nitrate in hydroponic mixes. National subsidies for water-saving irrigation accelerate fertigation adoption. India’s protected-cultivation acreage is rising under the National Horticulture Mission, with high uptake in Maharashtra and Rajasthan. Vertical-farm investment in Japan and South Korea, paired with expanding greenhouse clusters in Vietnam and Thailand, further underpins regional demand.

North America remains a core market. Greenhouse clusters in Arizona, California, and the Great Lakes region incorporate calcium nitrate in tomato and pepper nutrition programs to avert blossom-end rot. Municipalities in Florida and Texas continuously dose nitrate to manage hydrogen-sulfide odors in long sewer force mains. Canada’s greenhouse belt in Ontario and British Columbia sources calcium nitrate both domestically and from European suppliers. Mexico’s drip-irrigated vegetable exports from Sinaloa and Baja California increasingly rely on liquid grades that integrate easily with existing injection equipment.

Europe’s market is characterized by advanced greenhouse technology and tightening carbon policy. Dutch growers demand high-purity calcium nitrate to maintain electrical-conductivity thresholds in recirculating nutrient systems, while German and French producers follow suit. The CBAM framework, enforced in 2026, advantages local low-carbon producers and encourages Nordic investment in green-ammonia projects that will supply future nitrate production. South America’s emerging role is underscored by Yara’s off-take agreement for renewable calcium ammonium nitrate from Paraguay, signaling Mercosur’s potential as a low-carbon supply hub. In the Middle East and Africa, Saudi Arabia’s Vision 2030 and South Africa’s export-oriented greenhouse clusters are adopting calcium nitrate solutions to support water-efficient, high-yield cultivation.

Competitive Landscape

The calcium nitrate market is moderately concentrated. Yara, Nutrien, EuroChem, URALCHEM JSC and Haifa Negev Technologies leverage vertically integrated ammonia and nitric-acid capacity to secure raw-material cost advantages. Yara’s 165,000 t yr⁻¹ low-carbon fertilizer deal with PepsiCo Europe and its full off-take of ATOME’s upcoming 264,000 t yr⁻¹ renewable calcium ammonium nitrate plant exemplify first-mover positioning in premium, certified low-emission products. Nutrien and EuroChem are modernizing nitric-acid units with nitrous-oxide abatement technology to meet tightening emission limits, while Haifa focuses on ultra-low-ammonium formulations for greenhouse markets.

Smaller entrants differentiate through specialized formats or regional distribution. Norkem’s granular grade targets growers seeking season-long nutrient release, and specialty distributors in Asia-Pacific offer micronized powders tailored for foliar sprays. Digital agronomy tools are reshaping service models: Yara’s AtFarm platform provides satellite imagery and soil-analysis integration to optimize calcium nitrate dosing, embedding product usage within a broader advisory ecosystem. Emerging disruptors include start-ups exploring bio-based calcium sources and wastewater-technology firms promoting denitrifying bioreactors that reduce chemical nitrate dosing, signaling gradual competitive shifts.

Calcium Nitrate Industry Leaders

URALCHEM JSC

Yara

Nutrien

EuroChem Group

Haifa Negev technologies LTD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ADOB developed new calcium nitrate products featuring ultra-low ammonium content and added amino acids. These products included calcium nitrate combined with glycine, one of the 20 standard amino acids present in the proteins of living organisms.

- August 2024: Acron increased its production of granulated calcium nitrate (CN) in Veliky Novgorod by 29% year-on-year, reaching 65,000 tonnes. The company also set a record for monthly output at 11,800 tonnes, with total production surpassing 187,000 tonnes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the calcium nitrate market as the annual sales value of virgin, industrial and agriculture-grade calcium nitrate in solid, melt, and liquid forms that reach end uses such as fertilizers, wastewater odor control, concrete acceleration, refrigeration brines, and explosives. Imports, re-exports, recycled streams, and blended calcium ammonium nitrate are outside this scope.

Scope exclusion: downstream compound fertilizers that merely contain calcium nitrate as a trace constituent are not sized.

Segmentation Overview

- By Product Type

- Crystals

- Liquid

- Melt

- By Application

- Fertilizer

- Wastewater Treatment

- Concrete

- Explosives

- Refrigerant

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

To validate secondary indicators, we spoke with agronomists across Asia-Pacific, procurement heads at ready-mix concrete plants in Europe, and municipal odor-control specialists in North America. Their feedback on real-world application rates, seasonal purchasing, and emerging regulatory caps adjusted several preliminary assumptions. These conversations also yielded consensus views on likely adoption of liquid grades over the next five years.

Desk Research

Mordor analysts began with national customs codes for calcium nitrate to gauge trade flows, followed by agriculture input statistics from FAOSTAT, USDA, and Eurostat that show crop-wise nutrient uptake. Industry balance sheets in company 10-Ks, patent filings captured through Questel, and construction chemical demand tallies from the Global Cement Directory helped refine non-farm demand. Supplemental insights were drawn from wastewater treatment handbooks published by the American Water Works Association and periodic price series reported by Dow Jones Factiva. This mix built a reliable historical baseline while keeping every figure traceable to open datasets. The sources named are illustrative; many additional references informed the desk work.

Market-Sizing and Forecasting

The model starts with a top-down reconstruction that converts crop hectares, wastewater capacity, cement output, and explosive demand into potential calcium nitrate consumption pools. Penetration rates observed in interviews are then applied. Supplier roll-ups and sampled average selling prices provide a bottom-up sense check before totals are locked. Key variables include irrigated horticulture acreage, greenhouse expansions, municipal biogas installations, regional cement start-up curves, and benchmark calcium nitrate contract prices. A multivariate regression, refreshed each cycle, links those drivers to historical consumption and projects forward to 2030. Scenario analysis captures fertilizer subsidy shifts and concrete admixture standards. Data gaps, especially for unreported traded melt, are bridged using three-year moving averages aligned to trade partner mirror data.

Data Validation and Update Cycle

Outputs undergo discrepancy checks against independent import tallies and price bands; anomalies trigger re-contact with at least one domain expert before sign-off. A second analyst reviews every calculation file. The report is fully refreshed each year and reopened mid-cycle if raw material prices or policy changes move the market materially.

Why Mordor's Calcium Nitrate Baseline Inspires Decision-Maker Confidence

Published estimates often diverge because each firm chooses different compound definitions, regional mixes, and refresh cadences.

By anchoring our base year on 2024 trade data and field-verified penetration, Mordor delivers a balanced view that neither inflates volumes with blended nitrates nor ignores fast-rising liquid solutions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.85 B (2025) | Mordor Intelligence | - |

| USD 14.81 B (2025) | Global Consultancy A | Bundles calcium ammonium nitrate and derives totals largely from vendor press releases with limited primary checks |

| USD 13.11 B (2024) | Sector Publisher B | Converts traded volumes to value using a single global ASP and omits Asia liquid grades |

The comparison shows that figures swing when scope or price assumptions drift. By selecting transparent variables, validating them with domain experts, and updating models every year, Mordor Intelligence offers a dependable baseline that managers can trace, question, and reproduce with confidence.

Key Questions Answered in the Report

What is the current value of the calcium nitrate market?

The calcium nitrate market size reached USD 13.90 billion in 2026 and is forecast to reach USD 17.01 billion through 2031.

Which region leads demand for calcium nitrate?

Asia-Pacific accounted for 41.98% of global demand in 2025 and is projected to expand at a 5.41% CAGR to 2031.

Why are vertical farms interested in calcium nitrate?

Vertical-farm operators favor chloride-free calcium nitrate that dissolves completely, preventing emitter clogging while supplying both nitrate-nitrogen and calcium.

How does CBAM influence calcium nitrate trade?

The EU Carbon Border Adjustment Mechanism imposes levies on high-emission imports, giving a cost advantage to low-carbon calcium nitrate produced within Europe or with certified low-emission ammonia.

Page last updated on: