Lithium Carbonate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

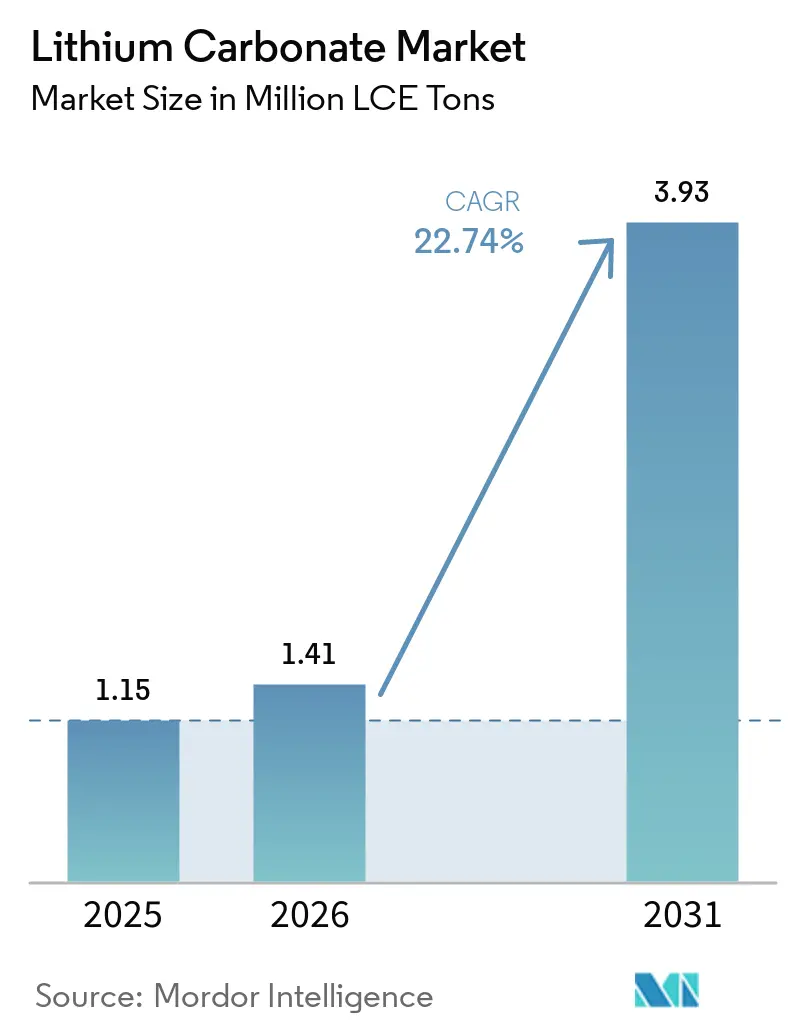

| Market Volume (2026) | 1.41 Million LCE tons |

| Market Volume (2031) | 3.93 Million LCE tons |

| Growth Rate (2026 - 2031) | 22.74% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lithium Carbonate Market Analysis by Mordor Intelligence

The Lithium Carbonate Market size is expected to increase from 1.15 Million LCE tons in 2025 to 1.41 Million LCE tons in 2026 and reach 3.93 Million LCE tons by 2031, growing at a CAGR of 22.74% over 2026-2031. Near-term growth is accelerated by automakers’ decisive pivot from nickel-manganese-cobalt (NMC) to lithium iron phosphate (LFP) cathodes, a shift that increases the absolute tonnage of lithium carbonate required per vehicle because LFP relies exclusively on carbonate rather than hydroxide. Energy-storage deployments form a second structural pull, with utility-scale installations in the United States climbing to 57.6 GWh in 2025 and projected to triple again in 2026 on the strength of grid-balancing mandates. Regional policy incentives are equally material: the U.S. Inflation Reduction Act (IRA) offers USD 35 per kWh for domestically produced cells and a 10% critical-minerals credit, steering investment toward North American mines and refineries. Capacity realignment is reshaping trade lanes, as China’s refining share of 60-70% confronts new brine-to-carbonate plants in Chile and clay-based direct-lithium-extraction (DLE) projects in Nevada.

Key Report Takeaways

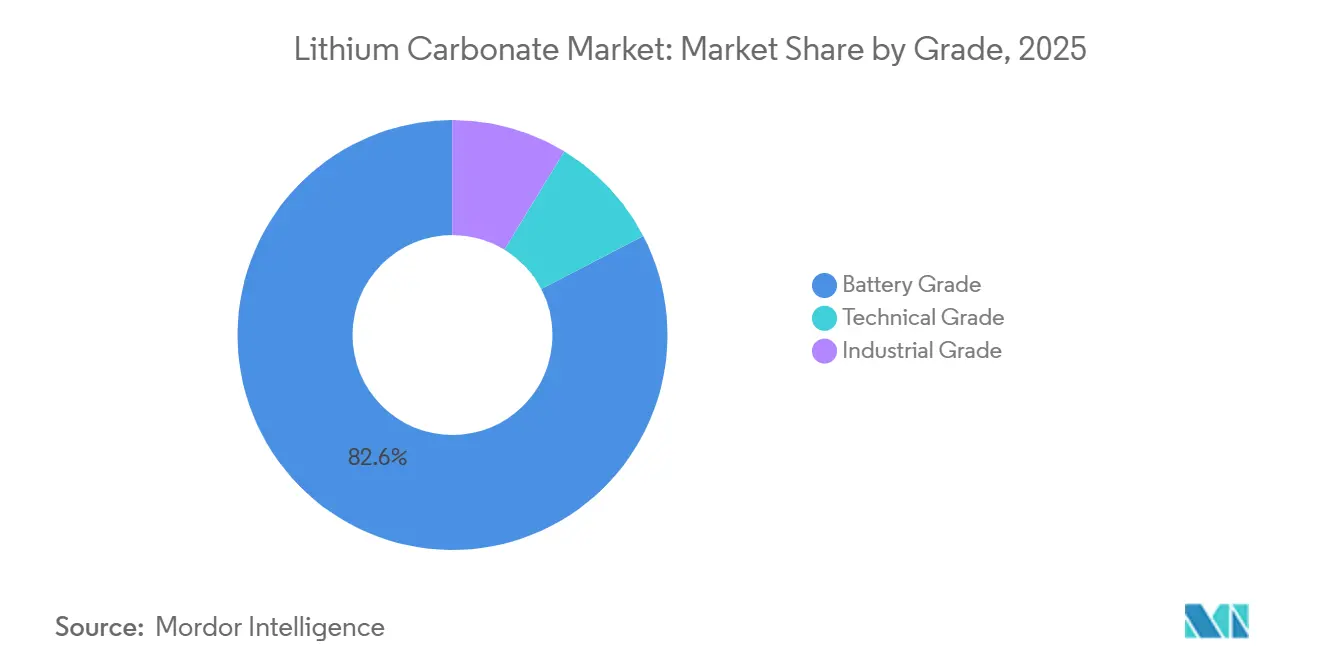

- By grade, battery-grade material accounted for 82.62% of the lithium carbonate market share in 2025 and is advancing at a 23.95% CAGR through 2031.

- By source, brine supplied 65.22% of the lithium carbonate market share in 2025, while hard-rock spodumene is forecast to contribute the fastest 23.16% CAGR through 2031.

- By application, Li-ion batteries held 89.86% of the lithium carbonate market share in 2025 and are expanding at a 23.81% CAGR through 2031.

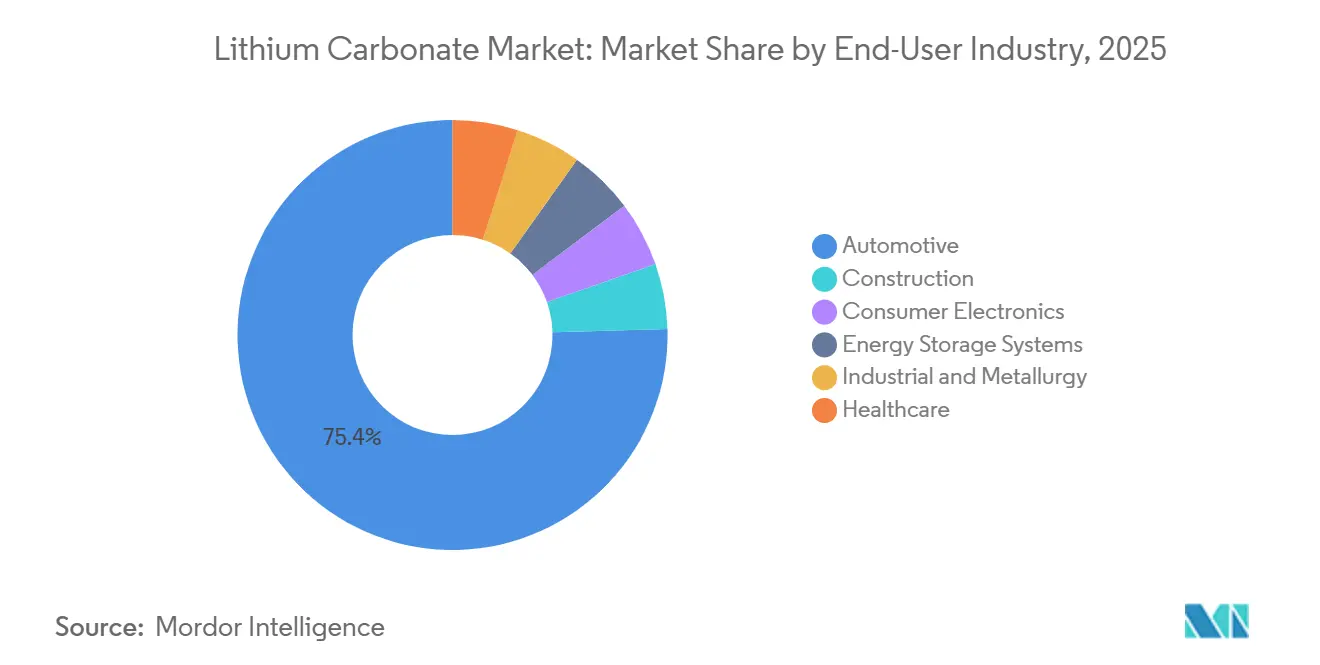

- By end-user industry, automotive captured 75.44% of the lithium carbonate market share in 2025, yet energy-storage systems lead growth with a 24.41% CAGR through 2031.

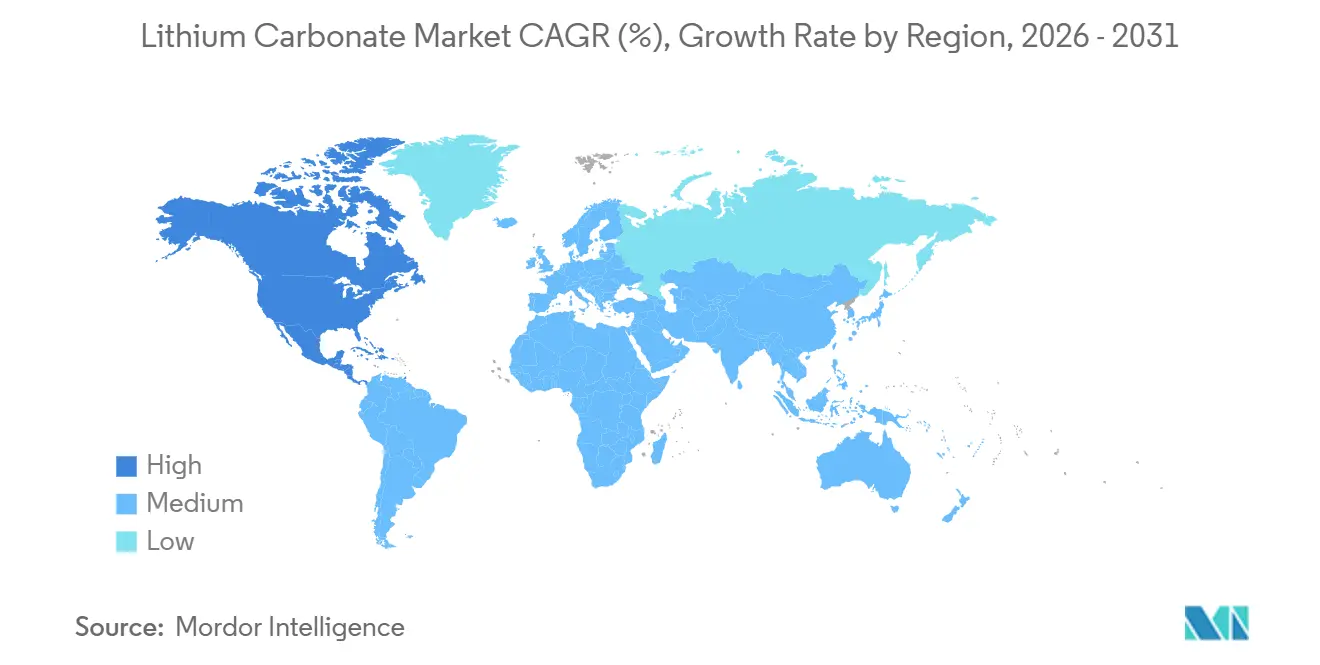

- By geography, Asia-Pacific commanded 79.13% of the lithium carbonate market share in 2025; North America is the fastest-growing region at 28.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lithium Carbonate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating EV adoption and battery manufacturing capacity expansion | +7.5% | Global, with concentration in China, North America, and Europe | Medium term (2-4 years) |

| Rapid deployment of energy storage systems for grid stabilization | +5.5% | North America, APAC core, spill-over to Europe and MEA | Medium term (2-4 years) |

| Government incentives and domestic content requirements driving localization | +5.0% | North America and Europe, secondary impact in APAC | Long term (≥ 4 years) |

| Battery chemistry transition from NMC to LFP favoring lithium carbonate | +2.5% | Global, led by China with adoption in North America and Europe | Short term (≤ 2 years) |

| Technology innovations in direct lithium extraction and recycling | +1.8% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating EV adoption and Battery Manufacturing Capacity Expansion

Global passenger-EV deliveries surpassed 15 million units in 2025, and production plans announced in 2026 will lift cell capacity additions by another 600 GWh. China’s LFP penetration exceeded 80% of domestic EV sales between January and November 2025, a chemistry tilt that swings incremental demand toward the lithium carbonate market. Ford’s BlueOval Battery Park Michigan entered mass production in Michigan during 2026, while General Motors and Samsung SDI broke ground on a 30 GWh LFP plant in Indiana, jointly locking up multi-year carbonate offtake. Long-term procurement contracts now outnumber spot transactions for automotive cathode manufacturers, helping price discovery but limiting liquidity. Automakers are also co-investing in upstream assets, as evidenced by Ford’s offtake tie-up with Lithium Americas’ Thacker Pass, reducing exposure to commodity swings.

Rapid Deployment of Energy Storage Systems for Grid Stabilization

Utility-scale battery additions in the United States rose to 57.6 GWh in 2025, four times the 2022 baseline. Front-of-meter providers favor lithium iron phosphate (LFP) modules because 6,000-plus cycle life and a USD 80-100 per kWh price point outperform NMC economics. China’s 15th Five-Year Plan calls for every province to install storage equal to at least 10% of peak renewable output, elevating stationary demand to a projected 150-180 GWh in 2026. Analysts expect energy-storage systems to consume 42% of global lithium by 2035, up from 8% in 2020, permanently diluting the automotive industry’s historical dominance[1]National Development and Reform Commission China, “Notice 136 on Energy Storage Planning,” ndrc.gov.cn. Multi-year power-purchase agreements for renewables now require firm storage capacity, and developers are increasingly embedding carbonate supply clauses in engineering-procurement-construction contracts, effectively reserving feedstock years ahead.

Government Incentives and Domestic Content Requirements Driving Localization

The IRA’s 80% domestic-content threshold for critical minerals by 2027 has accelerated North American mine permitting and refinery construction. Lithium Americas obtained a USD 2.26 billion Department of Energy loan for Thacker Pass, Albemarle restarted Kings Mountain in North Carolina, and Piedmont Lithium is advancing a Carolina-based converter. Europe’s Battery Booster Strategy earmarks EUR 300 million in grants plus a EUR 1.5 billion blended-finance facility to close the refining gap, while the European Union’s December 2026 ban on black-mass exports to non-OECD countries forces domestic recycling capacity. In Chile, the 400,000 tons per year national quota caps additional brine expansions, creating competitive space for Argentine, U.S., and Australian entrants.

Technology Innovations in Direct Lithium Extraction and Recycling

DLE is moving from pilot to commercial scale. Century Lithium achieved greater than 91% recovery from clay feedstock, while Saltworks’ dual-stage process claims a 25% capital-expenditure reduction relative to legacy evaporation. DuPont’s FilmTec LiNE-XD membrane suite lowers unit energy consumption by over 30% and is already licensed to four producers. Operating costs of USD 2,800-4,600 per ton LCE position advanced DLE favorably against both brine ponds and spodumene roasting, and life-cycle assessments indicate a 59% reduction in global-warming potential compared with traditional flowsheets. Recycling complements resource expansion: BASF’s Schwarzheide plant processes 15,000 tons per year of black mass, achieving 80-95% lithium recovery and selling battery-grade carbonate back into the European supply chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility and supply chain disruptions | -2.1% | Global, acute in spot markets for China and Europe | Short term (≤ 2 years) |

| Processing capacity bottlenecks and geographic concentration | -1.4% | Global, concentrated in China with spillover to North America and Europe | Medium term (2-4 years) |

| Environmental and water resource constraints in lithium extraction | -1.2% | South America, North America, APAC (Chile, Argentina, Nevada, Australia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Volatility and Supply Chain Disruptions

Chinese spot carbonate traded between CNY 60,000 and CNY 120,000 per ton in 2025, a 100% intrayear range that squeezed converter margins. Futures corrected from CNY 180,000 per ton to CNY 144,000 per ton in early 2026 as new Australian concentrate cargoes hit the market, only to rebound when two mid-tier mines idled. Such whiplash discourages hedging because contract structures remain illiquid, pushing smaller producers below cash-cost breakeven and amplifying the next upward spike. Policymakers in China also replaced the new-energy-vehicle purchase-tax exemption with a 5% levy in 2026, causing a front-loaded demand rush in late 2025 and a subsequent trough[2]Ministry of Finance People’s Republic of China, “Tax Policy Adjustment for NEVs,” mof.gov.cn.

Processing Capacity Bottlenecks and Geographic Concentration

China refines 60-70% of global lithium raw material but imports about 80% of its spodumene from Australia, creating a chokepoint that can be throttled by trade policy. Utilization in Jiangxi and Sichuan refineries slipped below 70% in 2025 because of oversupply, then rose when off-take-based pricing sheltered integrated players. North American and European greenfield refineries face permitting cycles exceeding three years; Thacker Pass and Kings Mountain both underwent more than 24 months of federal environmental review. Skilled labor shortages in hydrometallurgy and reagent-grade chemical handling further delay ramp-ups, and until substitute hubs scale, China retains price-setting influence.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Battery Grade Purity Dominates Margin Pools

Battery-grade controlled 82.62% of the lithium carbonate market share in 2025 and is expected to advance at a 23.95% CAGR through 2031. Purity thresholds of 99.5% minimize metal contaminants that catalyze dendrite growth, lowering cell failure rates and justifying a 15-20% price premium over 99.0% industrial grade. Multi-gigafactory operators in the United States, South Korea, and Germany now embed purity guarantees into take-or-pay clauses, effectively ring-fencing volume for high-spec suppliers.

Industrial-grade output, applied in glass, ceramics, and metallurgy, trails at mid-single-digit annual growth. Construction demand correlates with housing and infrastructure cycles rather than EV sales, so the segment experiences less volatility but lower upside. Pharmaceutical-grade carbonate represents under 1% of the lithium carbonate market size yet commands prices above USD 50,000 per ton because of U.S. Pharmacopeia compliance. Producers often maintain dedicated production lines to avoid cross-contamination, creating high fixed costs but steady niche margins.

By Source: Brine Still Leads, Hard-Rock Gains Share

Brine fields supplied 65.22% of output in 2025, but spodumene (hard-rock) from Western Australia and emerging North American hubs is the fastest-growing source, registering a 23.16% CAGR to 2031. Brine evaporation enjoys operating costs of USD 3,300-4,900 per ton LCE; however, 12-to-18-month pond cycles cannot respond quickly to demand surprises, limiting supply elasticity. Hard-rock concentrate delivers higher recovery rates, typically 70-80%, and can ramp within 6-12 months once a new crusher line is in place, though its USD 3,600-8,000 cost range makes miners sensitive to price dips.

Clay and lepidolite deposits stayed marginal until DLE breakthroughs improved extraction yields beyond 90%. Century Lithium’s Nevada pilot now logs operating costs near USD 4,000 per ton and cuts water use dramatically. Recycled carbonate contributes an estimated 3-4% today, but could reach 10-12% of the lithium carbonate market share by 2031 because the European Union’s export ban on black mass to non-OECD countries takes effect in December 2026.

By Application: Li-ion Batteries Cement a Commanding Position

Li-ion batteries absorbed 89.86% of the 2025 volume and are on track for a 23.81% CAGR through 2031. LFP surpassed NMC chemistry in total GWh deployed during 2025, and because LFP exclusively uses carbonate, the chemistry swap directly enlarges the lithium carbonate market size. Utility-scale energy-storage systems, which prefer LFP for its 6,000-plus life cycles and lower cost, accounted for 21 GWh of stationary cell output in 2025 and will triple by 2027 on grid-balancing mandates.

Non-battery applications are stable but inherently slower growing. Glass and ceramic producers employ lithium carbonate to lower melting temperatures and improve fracture toughness, while foundries use it as a flux in specialty aluminum alloys. Pharmaceutical uptake remains niche, and cement additions appear primarily in high-early-strength mixes for rapid-turnaround infrastructure pours.

By End-User Industry: Automotive Anchores, Energy Storage Surges

Automotive consumed 75.44% of the 2025 total volume, but growth moderated after subsidies in China were reduced in 2026. Even so, automakers maintain structural demand via plant-level integration: Ford, General Motors, and Tesla have collectively signed offtake exceeding 300,000 tons through 2030, securing carbonate ahead of new gigafactory lines.

Energy storage systems exhibit the fastest 24.41% CAGR through 2031, driven by renewable penetration and transmission-congestion relief. Front-of-meter deployments in the United States could climb to 180 GWh in 2026, while China’s provincial targets amplify stationary uptake. Consumer electronics stay close to replacement-cycle norms, whereas industrial metallurgy and healthcare segments remain niche.

Geography Analysis

Asia-Pacific retained 79.13% of global volume in 2025, anchored by China’s integrated value chain from refining in Jiangxi and Sichuan to cell assembly in Guangdong and Zhejiang. Although China imports 80% of its spodumene concentrate from Australia, the region’s extensive converter park keeps most value addition in-country. Margin pressure emerged in 2025 when spot prices cooled, dropping utilization below 70% in several converters. Japan and South Korea rely on imports of battery-grade carbonate for Panasonic, LG Energy Solution, and Samsung SDI, making them sensitive to Chinese export policy.

North America leads growth with a 28.13% CAGR to 2031. The IRA’s USD 35 per kWh cell credit makes domestic carbonate an economic imperative for gigafactories in Michigan, Ohio, Tennessee, and Ontario. Federal loans unlocked Thacker Pass, Kings Mountain, and Piedmont Lithium, collectively targeting over 100,000 tons per year by 2028. Permitting delays remain material, but offtake contracts with Ford and GM de-risk project finance.

Europe benefits from the EUR 1.5 billion Battery Booster Facility supporting refinery and recycling infrastructure. BASF’s Schwarzheide plant and ACC’s unit in France underpin regional demand. The December 2026 export ban on black mass will compel recyclers to localize capacity, which will back-feed carbonate into gigafactory supply chains.

South America, primarily Chile and Argentina, controlled roughly 40% of brine-based output in 2025. Chile’s 400,000 ton quota caps further expansion, while SQM’s 210,000 ton Salar de Atacama and Albemarle’s 200,000 ton La Negra III operate within that ceiling. Argentina’s Olaroz-Cauchari, Sal de Vida, and Pastos Grandes together add 87,500 tons, yet infrastructure gaps and provincial permitting could slow ramp-ups.

Competitive Landscape

The market is moderately concentrated, with the five largest firms including Albemarle Corporation, SQM, Tianqi Lithium Corporation, Ganfeng Lithium Group Co., Ltd, and Rio Tinto. Albemarle’s La Negra III expansion boosts Chilean output to 200,000 tons by 2027, while SQM’s 210,000-ton brine complex maintains scale leadership in the Atacama. Ganfeng pairs 140,000 tons of refining capacity with feedstock from Australia, China, and Argentina, then sells into long-dated offtake agreements with LG Energy Solution, among others.

Technology is the wildcard. Century Lithium’s 91%-recovery DLE, Saltworks’ 25% capex-saving flow sheet, and DuPont’s energy-cutting LiNE-XD membranes lower entry barriers for clay and oilfield brines. Recycling adds a parallel pathway: BASF’s 15,000-ton Schwarzheide plant proves commercial hydrometallurgy at scale, and Italy’s new hub hit 99.6% recovery, foreshadowing regional loops forced by the EU’s export ban. North American refining lag still offers white space; combined announced capacity meets only 40-50% of 2030 cell-grade demand, suggesting room for mid-tier entrants.

Lithium Carbonate Industry Leaders

Albemarle Corporation

Rio Tinto

SQM

Ganfeng Lithium Group Co., Ltd

Tianqi Lithium Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Several lepidolite mines in Yichun, China's primary lithium-producing region, suspended operations due to government-mandated environmental inspections and challenges related to mining license renewals. The measures included audits of boundary disputes and environmental compliance, which affected major producers such as CATL and caused a significant increase in global lithium carbonate prices.

- March 2026: Trafigura signed a binding take-or-pay offtake agreement with Smackover Lithium, a joint venture between Standard Lithium Ltd and Equinor. The agreement, facilitated through subsidiaries of Equinor ASA, pertained to the supply of battery-grade lithium carbonate from the South West Arkansas Project.

Global Lithium Carbonate Market Report Scope

Lithium carbonate is an inorganic white powder primarily used as a medication for bipolar disorder, functioning as a mood stabilizer to manage mania. It is also essential in industrial applications, particularly in the production of lithium-ion batteries and ceramics.

The Lithium Carbonate Market is segmented into grade, source, application, end-user industry, and geography. By grade, the market is segmented into battery grade, technical grade, and industrial grade. By source, the market is segmented into brine, spodumene (hard-rock), lepidolite/clay, and recycled lithium carbonate. By application, the market is segmented into Li-ion battery, glass and ceramics, pharmaceuticals and dental, aluminum production, cement industry, and other applications. By end-user industry, the market is segmented into automotive, consumer electronics, energy storage systems, industrial and metallurgy, healthcare, and construction. The report also covers the market size and forecasts for lithium carbonate in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (LCE tons).

| Battery Grade |

| Technical Grade |

| Industrial Grade |

| Brine |

| Spodumene (Hard-rock) |

| Lepidolite/Clay |

| Recycled Lithium Carbonate |

| Li-ion Battery |

| Glass and Ceramics |

| Pharmaceuticals and Dental |

| Aluminum Production |

| Cement Industry |

| Other Applications |

| Automotive |

| Consumer Electronics |

| Energy Storage Systems |

| Industrial and Metallurgy |

| Healthcare |

| Construction |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Battery Grade | |

| Technical Grade | ||

| Industrial Grade | ||

| By Source | Brine | |

| Spodumene (Hard-rock) | ||

| Lepidolite/Clay | ||

| Recycled Lithium Carbonate | ||

| By Application | Li-ion Battery | |

| Glass and Ceramics | ||

| Pharmaceuticals and Dental | ||

| Aluminum Production | ||

| Cement Industry | ||

| Other Applications | ||

| By End-user Industry | Automotive | |

| Consumer Electronics | ||

| Energy Storage Systems | ||

| Industrial and Metallurgy | ||

| Healthcare | ||

| Construction | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the lithium carbonate market?

The lithium carbonate market size stands at 1.41 million LCE tons in 2026 and is set to rise to 3.93 million LCE tons by 2031.

Which application dominated volume in 2025?

Li-ion battery accounted for 89.86% of volume in 2025, driven by LFP cathode adoption in electric vehicles and grid storage.

Which grade is expanding the fastest through 2031?

Battery-grade carbonate leads growth at a 23.95% CAGR through 2031 on tightening purity requirements from global gigafactories.

Which region offers the highest growth potential?

North America is the fastest-growing geography, advancing at a 28.13% CAGR through 2031 as the Inflation Reduction Act stimulates mine and refinery investment.

Page last updated on: