Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

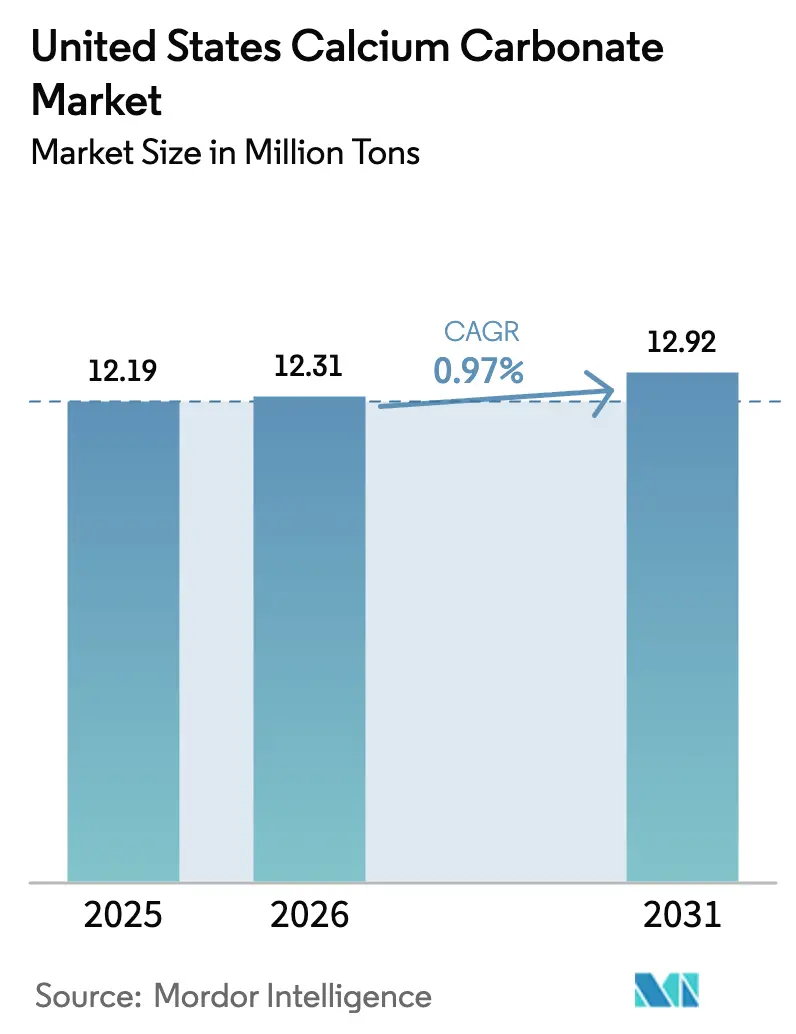

| Base Year Market Size (2025) | 12.19 Million tons |

| Market Volume (2026) | 12.31 Million tons |

| Market Volume (2031) | 12.92 Million tons |

| Growth Rate (2026 - 2031) | 0.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Calcium Carbonate Market Analysis by Mordor Intelligence

The United States Calcium Carbonate Market size is expected to grow from 12.19 million tons in 2025 to 12.31 million tons in 2026 and is forecast to reach 12.92 million tons by 2031 at 0.97% CAGR over 2026-2031. Recent growth in volume terms has been modest, but there is a notable shift in value creation towards carbon-capture-derived precipitated calcium carbonate (PCC) and ultrafine specialty grades, both commanding premium pricing. Ground calcium carbonate (GCC) continues to dominate high-tonnage concrete and aggregate outlets. However, on-site PCC satellites at paper mills, along with emerging CCU facilities, are expanding the profit pool while cutting down transport emissions. Infrastructure projects, bolstered by the federal Infrastructure Investment and Jobs Act (IIJA), are tightening limestone supply chains, nudging converters towards higher-performance PCC grades. In the paints and plastics sector, formulators have increased calcium carbonate loadings to offset the structurally elevated costs of titanium dioxide and polymers, thus strengthening demand resilience. Moreover, heightened regulatory scrutiny on respirable crystalline silica is driving dust-suppression investments at quarries, giving a competitive edge to dust-free synthetic PCC.

Key Report Takeaways

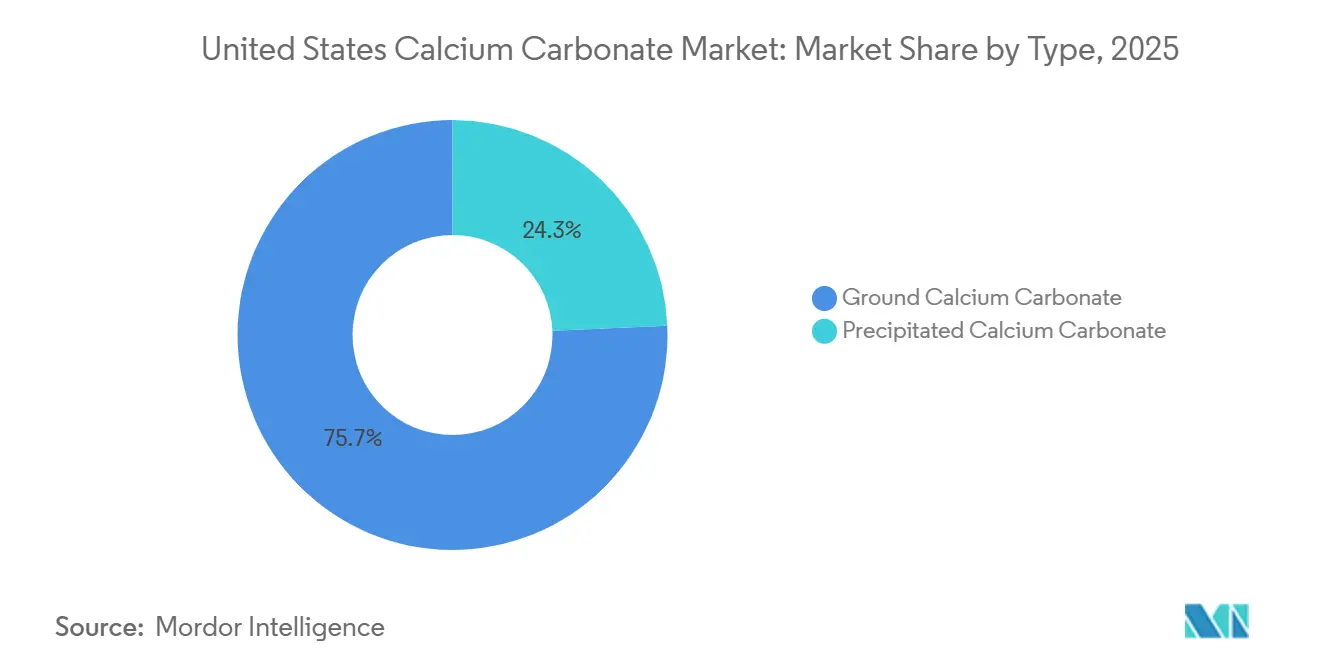

- By type, ground calcium carbonate led with 75.69% of the United States calcium carbonate market share in 2025, while precipitated calcium carbonate is projected to expand at a 2.26% CAGR through 2031.

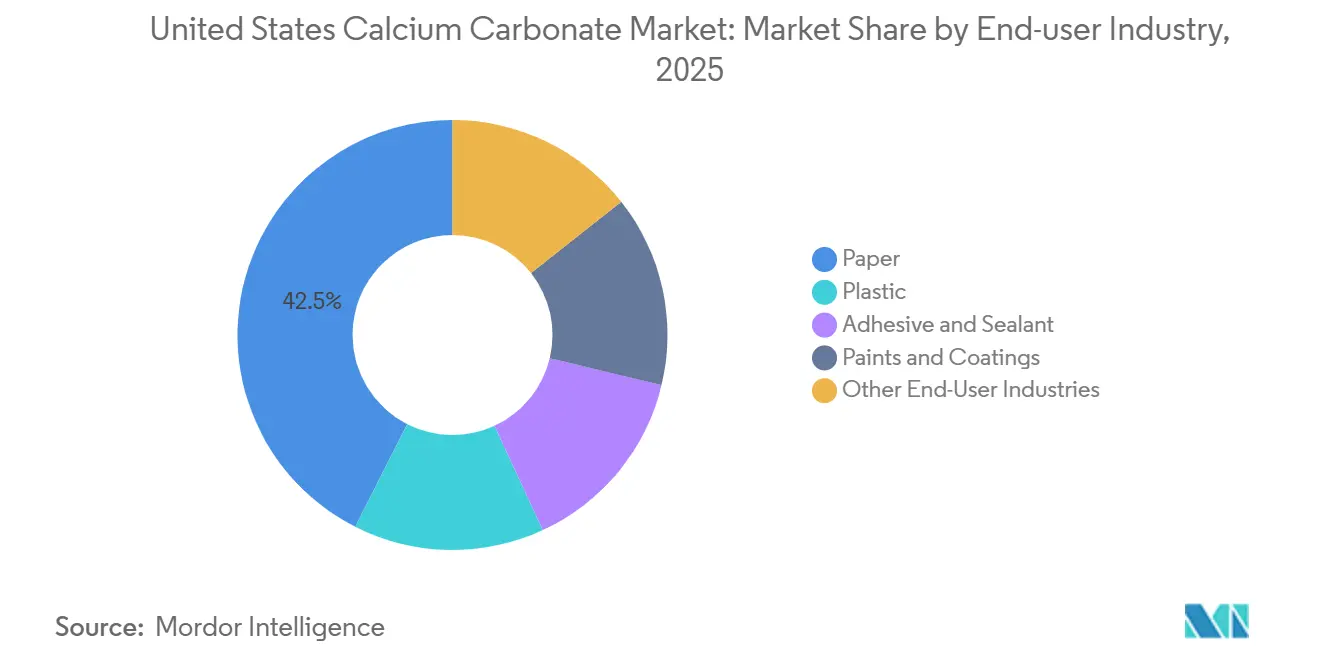

- By end-user industry, paper accounted for 42.53% of the United States calcium carbonate market size in 2025, but paints and coatings are forecast to record the fastest 3.57% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Calcium Carbonate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from paints and coatings | +0.35% | National, concentrated in Gulf Coast and Great Lakes industrial corridors | Medium term (2-4 years) |

| Growth in paper and packaging industry | +0.15% | National, with legacy capacity in Wisconsin, Michigan, and Southern states | Long term (≥ 4 years) |

| Plastics industry adoption of CaCO₃ fillers | +0.25% | National, with masterbatch hubs in Texas, Louisiana, and Ohio | Medium term (2-4 years) |

| United States infrastructure spending (IIJA) boosting GCC demand | +0.20% | National, prioritizing highway corridors and airport expansions | Short term (≤ 2 years) |

| On-site PCC produced via carbon-capture utilization | +0.10% | Regional, pilot-scale in Indiana (Gary Works) and Texas (San Antonio SkyMine) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Paints and Coatings

Formulators are increasing calcium carbonate extender ratios in paints and coatings to counteract persistently high titanium dioxide prices. This move comes as paints and coatings emerge as the fastest-growing outlet in the industry. A significant portion of the IIJA’s allocation is directed to the Highway Trust Fund, boosting demand for protective coatings on bridges, overpasses, and airport facilities. Suppliers are ramping up sub-2 micron grinding capacity and investing in stearic-acid surface modification to achieve stringent rheology targets in high-performance architectural paints. Ultrafine and surface-treated grades enhance dispersion and reduce viscosity, allowing for greater filler loading without compromising film integrity. Notably, this substitution trend is pronounced in value-tier formulations, where increased extender levels lead to reduced raw-material costs.

Growth in the Paper and Packaging Industry

Thanks to decades of integrating PCC satellites, paper remains the dominant consumer, with on-site PCC constituting a substantial portion of a typical sheet. Domtar’s Nekoosa Mill in Wisconsin, fed by a satellite launched in 2024, has successfully reduced carbon emissions annually and avoided significant trucking miles through its co-location strategy. While graphic paper has seen a decline, containerboard and e-commerce packaging are on the rise, bolstered by calcium carbonate coatings that enhance printability on corrugated boxes. Minerals Technologies, with numerous satellites globally, is channeling more capital into emerging Asia-Pacific, hinting at a maturing North American base. Yet, domestic mills are enhancing PCC particle-size control to compete for high-brightness specialty packaging orders, ensuring steady demand.

Plastics Industry Adoption of CaCO₃ Fillers

In recent years, the U.S. filler-masterbatch sector has expanded, with polyethylene and polypropylene films incorporating calcium carbonate to reduce resin usage and cut costs. Producers of PVC window profiles are increasing their calcium carbonate loading to meet competitive price points without sacrificing impact performance. Hybrid talc-calcium carbonate systems are now common in many new formulations, capitalizing on talc’s rigidity and calcium carbonate’s cost advantages. Nano-precipitated calcium carbonate is gaining traction in engineering plastics for consumer electronics housings, where its larger surface area enhances impact strength. However, economic constraints limit its wider adoption. Given calcium carbonate's compatibility and compostability, the surge of bio-resins like PLA and PHA presents a promising long-term opportunity.

United States Infrastructure Spending (IIJA) Boosting GCC Demand

Projected increases in cement consumption from the IIJA’s funding will heighten limestone demand for clinker production. Producers of GCC, strategically located near key highway corridors in Kentucky, Missouri, and Michigan, are operating close to their nameplate capacity, tightening the availability of filler-grade material. Michigan quarries, benefiting from freight savings via Great Lakes shipping, enjoy a competitive advantage in delivering to Midwest construction markets. This tight supply has already pushed spot GCC prices upward, leading converters in plastics and coatings to explore higher-margin PCC. Imports from Canada and Mexico, historically a significant source of crushed-stone imports, now play a crucial role in balancing the supply.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health hazards from respirable CaCO₃ dust | -0.15% | National, acute in quarry-intensive regions (Kentucky, Michigan, Missouri) | Short term (≤ 2 years) |

| Competition from talc, kaolin, and synthetic fillers | -0.10% | National, concentrated in specialty plastics and high-performance coatings | Medium term (2-4 years) |

| Stricter United States quarrying and emission regulations | -0.20% | National, with state-level variability (California, New York most stringent) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Talc, Kaolin, and Synthetic Fillers

Thanks to its superior heat resistance and dimensional stability, talc has become the preferred choice for polypropylene automotive parts. Kaolin, with its brightness advantage, is preferred in paper-coating niches. Meanwhile, precipitated silica and alumina fillers are gaining traction in high-gloss plastics and scratch-resistant coatings. Formulators are increasingly blending talc with calcium carbonate in new plastic recipes to enhance stiffness and impact properties. In the coatings sector, while synthetic silica matting agents challenge calcium carbonate in premium wood finishes, cost considerations limit their widespread adoption. Regional supply chains play a pivotal role: talc is mainly sourced from Montana and Texas, while calcium carbonate's nationwide availability offers a freight advantage in numerous high-volume applications.

Stricter United States Quarrying and Emission Regulations

Under EPA’s 40 CFR Part 60 Subpart OOO, crushers and screens are held to strict particulate limits. Recent amendments have expanded these regulations, introducing HCl and mercury caps on lime kilns, which have led to heightened compliance costs[1]U.S. Environmental Protection Agency, “40 CFR Part 60 Subpart OOO – Nonmetallic Mineral Processing,” EPA.GOV . States like California and New York have imposed even stricter measures, extending permit cycles to a daunting ten years, effectively deterring new greenfield quarries. As smaller operations exit, industry giants - Omya, Imerys, Minerals Technologies, Huber, and Carmeuse - are capitalizing, bolstering their volume leverage. With domestic capacities on the decline, there is an increased dependence on imports from Canada and Mexico, leaving downstream buyers vulnerable to exchange-rate fluctuations and tariff complications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Carbon-Capture PCC Challenges GCC Dominance

In 2025, Ground Calcium Carbonate (GCC) dominated the market, accounting for 75.69% of the total volume. For example, Michigan’s Port Calcite ships millions of tons annually via lake freighters, achieving low unit costs for clients in the Midwest cement and aggregate sectors. While Precipitated Calcium Carbonate (PCC) holds a smaller market share, its output is on the rise, growing at a 2.26% CAGR through the forecast period of 2026-2031. This growth is fueled by the emergence of satellite plants near paper mills and various CCU projects. Even though starting from a smaller base, the U.S. market for PCC is on a steady upward trajectory. CarbonFree’s Gary Works project is not only capturing CO₂ but also marketing it as premium food-grade PCC. This strategy aligns with 45Q incentives and highlights CCU's transformative potential. Fortera and Graymont’s ReAct partnership is introducing vaterite PCC, which can serve as a partial substitute for cement clinker, addressing the increasing demand for green concrete. However, the supply chain faces hurdles: the processes of capturing, purifying, and liquefying CO₂ elevate capital expenditures. Fortunately, federal grants and state cap-and-trade credits are helping to level the playing field with mined GCC.

Commercial-scale PCC, known for its finer particle size, elevated purity, and customizable morphology, commands a premium over commodity GCC. This makes it highly desirable in sectors such as food, pharmaceuticals, and high-gloss coatings. Meanwhile, upgraded grinding circuits producing ultrafine GCC are enhancing GCC’s average unit value, especially in matte architectural coatings. In the realm of digital-print papers and low-VOC water-based paints, hybrid filler systems are emerging. Here, ultrafine GCC provides volume, while PCC contributes opacity or brightness. While GCC is likely to retain its volume leadership, the distinct advantages of PCC and the benefits from CCU are set to bridge the historical price-to-performance gap in the U.S. calcium carbonate market.

By End-User Industry: Paints Drive Growth as Paper Stabilizes

In 2025, paper accounted for 42.53% of the demand, supported by established PCC satellites that economically enhance sheet composition. While domestic growth faced challenges due to digital alternatives diminishing graphic grades, a slight rise in containerboard demand - spurred by e-commerce and specialty packaging - mitigated the overall decline. Minerals Technologies is broadening its global satellite presence, underscoring the technology's strength, yet its U.S. volumes have plateaued. Coatings derived from recycled fiber grades, augmented with calcium carbonate, ensure satisfactory print quality for direct-to-box graphics, bolstering baseline demand. Consequently, while the U.S. calcium carbonate market's paper segment will gradually transition to faster-growing sectors, it will remain a significant player.

The paints and coatings sector boasts the most promising outlook, projected to grow at a 3.57% CAGR through the forecast period of 2026-2031. This growth is fueled by raw-material inflation and heightened extender usage. Architectural paints are now incorporating a blend of ultrafine GCC and surface-treated PCC, allowing for a reduction in titanium dioxide without sacrificing opacity. Furthermore, there is heightened demand from infrastructure-related protective coatings and a rebound in auto-refinish volumes post-pandemic. In the plastics sector, high-filler masterbatches are rapidly gaining traction for applications such as polyethylene bags, agricultural films, and PVC siding. Calcium carbonate is stepping in as a cost-effective alternative to pricier polymers, all while preserving mechanical integrity. Although still emerging, adhesives and sealants are carving a niche in construction and electric vehicles, leveraging the dispersibility of coated PCC. Lastly, while specialty sectors such as pharmaceutical excipients, food additives, animal feed supplements, and drilling fluids may represent a smaller tonnage, they continue to show a strong preference for premium PCC.

Geography Analysis

States like Kentucky, Michigan, Missouri, and Utah, rich in high-purity limestone, lead the production scene, thanks to their high CaCO₃ content and multimodal transport advantages. In Kentucky, formations such as High Bridge and Ste. Genevieve supplies lime kilns and filler mills. This strategic positioning allows vertically integrated firms, including Carmeuse, to serve markets like steel, flue-gas desulfurization, and water treatment from a centralized hub. Michigan leverages Great Lakes shipping, with Port Calcite managing substantial volumes. These volumes primarily cater to Chicago, Cleveland, and Detroit, benefiting from freight rates much lower than trucking costs. Such logistical benefits cement Michigan’s crucial role in the Midwest's aggregate and steel flux markets.

Demand centers span the Gulf Coast's petrochemical corridor, the Great Lakes' automotive hub, and the swiftly growing construction triangle in the Southwest. States such as Texas, California, and Florida, reaping rewards from IIJA-funded highway and airport enhancements, are witnessing increased volumes, particularly towards the Sun Belt. California's stringent environmental regulations, underscored by SB 20 and overlapping EPA NESHAP guidelines, stretch quarry permit timelines to almost a decade[2]California Air Resources Board, “California Cement Industry Emissions,” ARB.CA.GOV . Consequently, cement producers are turning to imports for limestone and clinker, a trend that has been on the rise. The Pacific-Northwest, dependent on Columbia River barge logistics, procures ultrafine GCC from Columbia River Carbonates for its paper and plastics sectors. Simultaneously, local quarries serve the construction markets in Oregon and Washington.

Regulatory differences are prompting consolidations: California and New York impose tighter dust and HAP controls, contrasting with the lenient regulations in Wyoming and Montana. These compliance expenses are steering a shift towards imports, with Canada and Mexico recently accounting for a large portion of crushed-stone imports. Given these factors, fluctuations in exchange rates and potential trade disputes present challenges for downstream manufacturers reliant on a consistent filler supply. Despite a nationwide resource availability, the U.S. calcium carbonate market is distinctly localized, influenced by regional supply disparities and transportation economics.

Competitive Landscape

The United States calcium carbonate market is moderately consolidated. The industry's leading players command a significant market volume share, leaving room for regional specialists. Omya's collaboration with Domtar’s Nekoosa Mill, producing PCC, achieved a commendable annual emissions reduction. This highlights the advantages of co-location: improved sustainability and reduced transport costs. Graymont's partnership with Fortera in 2025 unveiled reactive vaterite PCC in low-carbon concrete, marking a strategic pivot towards carbon-negative materials. On the other hand, Minerals Technologies is boosting its PCC capacity in India and setting up a fourth satellite in China, signaling a bold offshore expansion as U.S. volumes stabilize.

Regional independents are flourishing by capitalizing on their proximity and service agility. For example, Columbia River Carbonates, a joint venture of Omya and Bleeck, employs barge logistics for ultrafine GCC deliveries across the Pacific-Northwest. Meanwhile, Blue Mountain Minerals caters to agricultural and industrial fillers in Northern California. GLC Minerals' CalPro line serves sealant and plastics converters in the Upper Midwest. Expanding its reach, CIMBAR Resources took over Imerys’ Sahuarita site in Arizona in 2024, enhancing its presence in the Southwest's coating and plastic sectors. The industry's technological focus is on finer grinding, surface tweaks, and CCU integration. Imerys’ ReMined recycled calcium carbonate, though attractive for LEED-centric projects, is still in its early growth phase. The competitive landscape showcases a slow consolidation trend, peppered with niche innovators emphasizing carbon-negative PCC, ultrafine GCC, and recycled feedstock.

United States Calcium Carbonate Industry Leaders

Imerys

Minerals Technologies Inc.

Omya AG

Mississippi Lime Company

J.M. Huber Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Graymont and Fortera have entered a strategic partnership to produce Fortera's ReAct low-carbon cement, utilizing Graymont's lime production expertise and sustainable material innovations. This collaboration results from extensive testing, validation, and joint efforts.

- March 2025: Domtar, in partnership with Omya, has opened a new precipitated calcium carbonate (PCC) plant at its Nekoosa, Wisconsin site. The facility ensures a steady PCC supply for paper production while delivering environmental, operational, and economic benefits.

United States Calcium Carbonate Market Report Scope

Calcium carbonate is a naturally occurring substance found in rocks such as minerals aragonite and calcite. Calcium carbonate is insoluble in water and generally appears as an odorless white powder.

The United States Calcium Carbonate Market is segmented by type and end-user industry. By type, the market is segmented into ground calcium carbonate and precipitated calcium carbonate. By end-user industry, the market is segmented into paper, plastic, adhesive and sealants, paint and coatings, and other end-user industries. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

By Type

| Ground Calcium Carbonate |

| Precipitated Calcium Carbonate |

By End-user Industry

| Paper |

| Plastic |

| Adhesive and Sealant |

| Paints and Coatings |

| Other End-User Industries |

| By Type | Ground Calcium Carbonate |

| Precipitated Calcium Carbonate | |

| By End-user Industry | Paper |

| Plastic | |

| Adhesive and Sealant | |

| Paints and Coatings | |

| Other End-User Industries |

Key Questions Answered in the Report

How large is the United States calcium carbonate market in 2026?

The United States calcium carbonate market size stands at 12.31 million tons in 2026, and it is projected to reach 12.92 million tons by 2031 at a 0.97% CAGR.

Which type of calcium carbonate is growing the fastest?

Precipitated calcium carbonate, especially CCU-based PCC, is forecast to expand at 2.26% CAGR through 2031.

Which end-user segment leads consumption?

Paper remains the largest outlet, holding 42.53% of 2025 demand, though its growth is modest.

Why are paints and coatings increasing calcium carbonate usage?

Formulators are raising extender levels to offset high titanium dioxide costs and meet infrastructure-related protective-coating demand.

How will carbon-capture utilization influence future supply?

CCU projects such as CarbonFree’s SkyCycle will add carbon-negative PCC capacity and could reshape cost curves as 45Q incentives expand.

Page last updated on: