Market Overview

| Study Period | 2020 - 2031 |

|---|---|

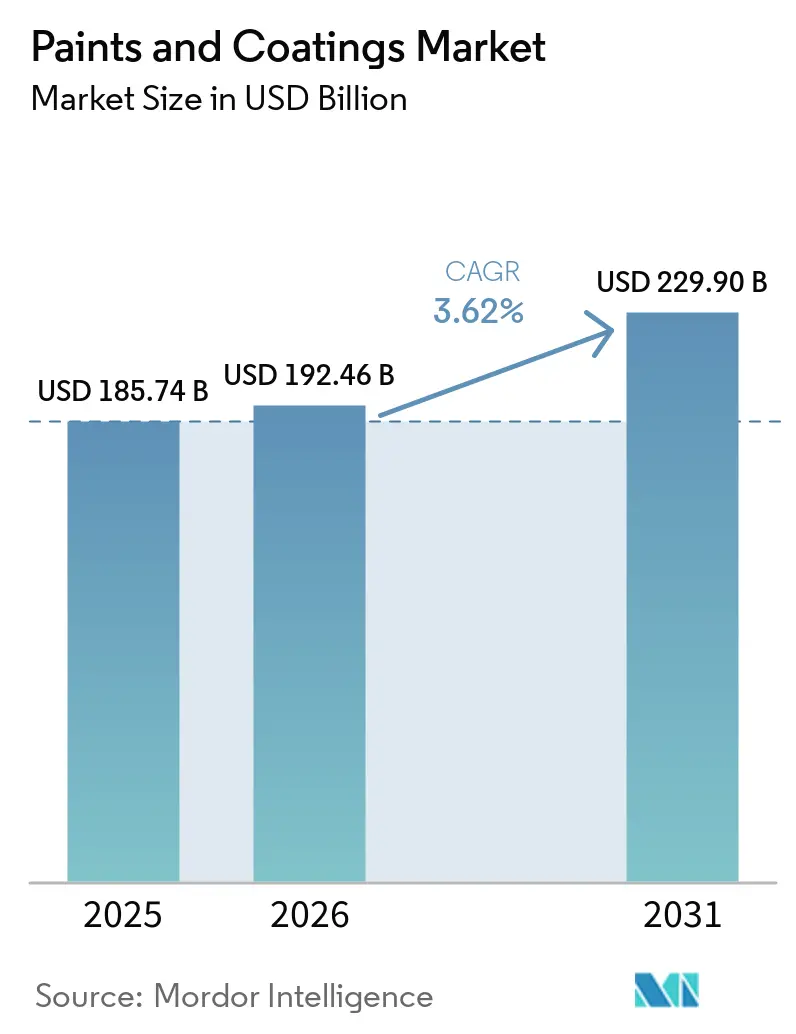

| Market Size (2026) | USD 192.46 Billion |

| Market Size (2031) | USD 229.90 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paints and Coatings Market Analysis by Mordor Intelligence

Paints And Coatings Market size in 2026 is estimated at USD 192.46 billion, growing from 2025 value of USD 185.74 billion with 2031 projections showing USD 229.9 billion, growing at 3.62% CAGR over 2026-2031. Steady demand from residential construction, infrastructure upgrades and sustainable product innovation underpins this moderate expansion even as raw-material costs swing sharply and environmental regulations tighten. Asia-Pacific holds structural advantages, rapid urban migration, large‐scale capital projects and expanding industrial output, that collectively fuel regional consumption at a noticeably faster rate than mature economies. Across technologies, the migration to low-VOC water-borne chemistries remains the single most influential trend, reinforced by government emission caps and customer preference for greener specifications. Simultaneously, producers are digitizing color-matching, plant scheduling and quality-control workflows to mitigate labor shortages and compress time-to-market. Competitive intensity is rising as the top dozen suppliers pursue targeted acquisitions and divestitures that create leaner portfolios and unlock scale efficiencies in the global paints and coatings industry.

Key Report Takeaways

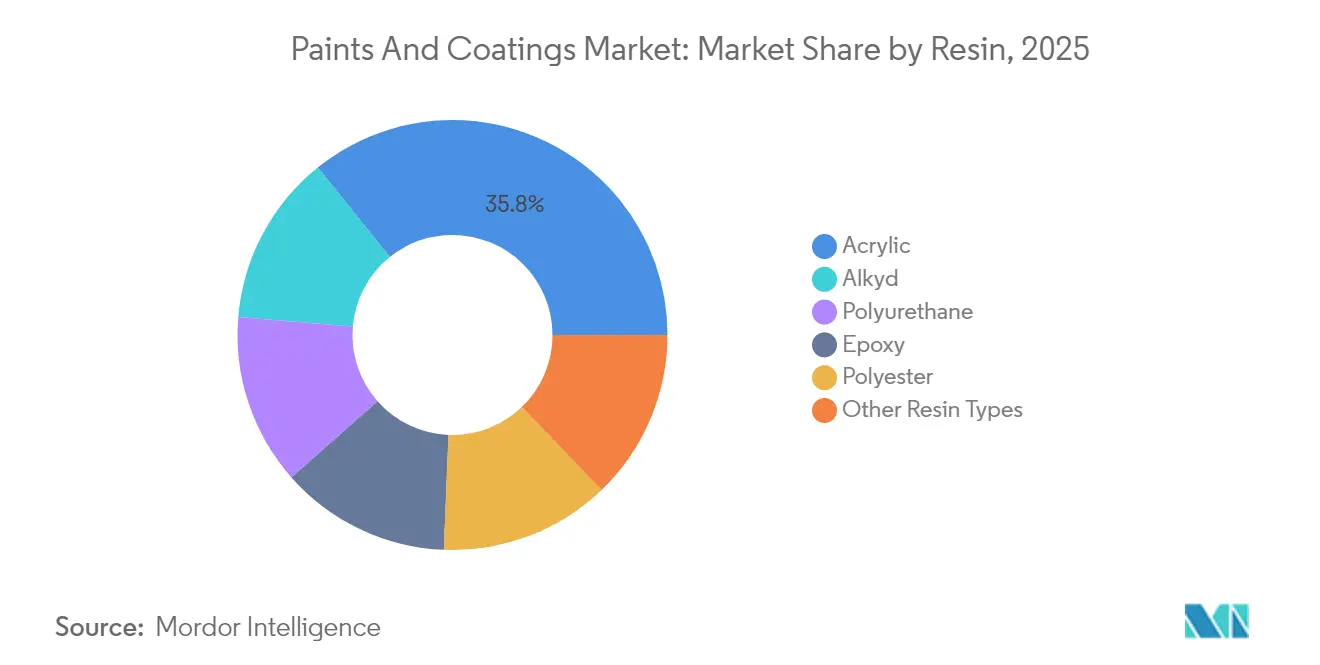

- By resin, acrylics led with 35.78% paints and coatings market share in 2025 and are projected to grow at a 3.98% CAGR through 2031.

- By technology, water-borne systems accounted for 50.62% of the paints and coatings market size in 2025 and remain the fastest-expanding technology at 4.02% CAGR to 2031.

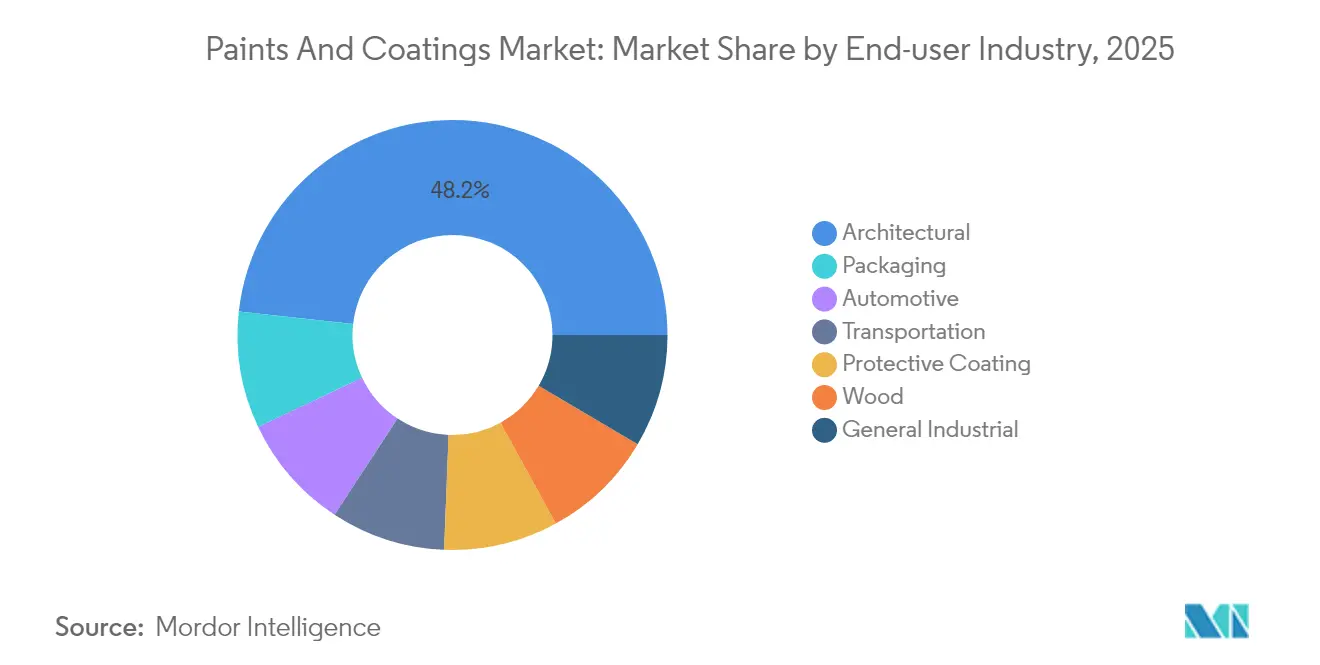

- By end-user, architectural coatings commanded 48.25% of 2025 revenue and are also pacing the segment growth at a 4.33% CAGR in the paints and coatings industry through 2031.

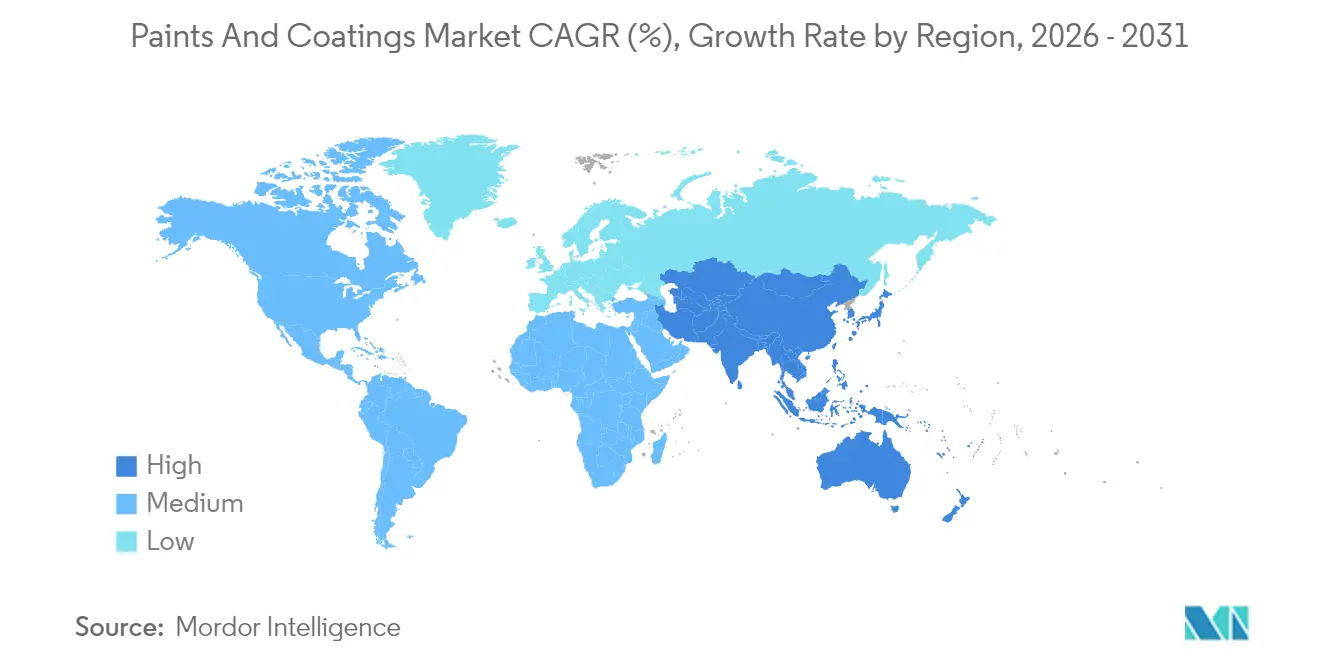

- By geography, Asia-Pacific dominated with 46.21% revenue contribution in 2025 and is expected to post the highest regional CAGR of 4.91% through 2031 in the paints and coatings industry.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Paints and Coatings Market*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in global residential construction activity | +1.2% | Global, strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Expanding automotive production volumes | +0.8% | Global, concentrated in Asia-Pacific and Europe | Medium term (2-4 years) |

| Rapid urban population growth in APAC | +1.5% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Government incentives for green building (low-VOC) | +0.9% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Emergence of AI-driven colour-matching platforms | +0.3% | Global, led by developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Global Residential Construction Activity

North American legislation such as the Infrastructure Investment and Jobs Act is funneling capital toward roads, bridges and utilities, lifting demand for protective and decorative coatings on both new and renovated assets. In parallel, Asia-Pacific governments continue to prioritize affordable housing programs that stimulate fresh residential starts and interior repaint cycles. Historically low mortgage rates in several economies have revived remodeling budgets, channeling incremental gallons into premium zero-VOC wall finishes that qualify for green-building credits. Suppliers are responding with fast-dry water-borne lines that meet stringent indoor-air benchmarks without sacrificing application speed. Combined, these factors reinforce a stable base of volume for the paints and coatings industry during the forecast window.

Expanding Automotive Production Volumes

Light-vehicle output rebounded in 2024 and is projected to regain its pre-pandemic trajectory by 2026, with China, India and Southeast Asia capturing the lion’s share of incremental capacity additions. Modern body shops increasingly specify water-borne basecoats and low-temperature bake clearcoats to cut cycle times and VOC emissions, strengthening technology convergence between OEM and refinish lines. Strategic partnerships among resin formulators, spray-booth makers and carmakers are accelerating the adoption of integrated coating platforms that lower energy use per unit sprayed. This ongoing production expansion delivers a meaningful uplift to industrial consumption boosts the paints and coatings market trends.

Rapid Urban Population Growth in APAC

Cities across India, Indonesia and the Philippines continue to absorb rural populations, mandating huge investments in transport, utilities and social infrastructure. Elevated humidity, salt spray and ultraviolet exposure in many coastal megacities increase lifecycle maintenance costs unless protective topcoats are specified at construction stage. Local producers are scaling capacity for elastomeric exterior acrylics and polysiloxane hybrids that extend repaint intervals on high-rise façades. The regional surge in data-center construction, driven by cloud computing and 5G roll-outs, creates niche demand for intumescent, anti-static and thermal-management coatings. Combined, these dynamics lock Asia-Pacific into the highest regional growth profile for the paints and coatings industry.

Government Incentives for Green Building (Low-VOC)

Federal procurement guidelines in the United States now mandate low-emitting building materials on most publicly funded projects, effectively standardizing VOC limits below 50 g/L for flat interior paints[1]U.S. Environmental Protection Agency, “VOC Emission Standards,” epa.gov. The European Union’s Energy Performance of Buildings Directive ties retrofit subsidies to demonstrable improvements in indoor-air quality, prompting project teams to specify independently certified coatings. Several provincial authorities in China have rolled out tax rebates for manufacturers of water-borne alkyds and UV-curable wood finishes that meet forthcoming national emission caps. These policy levers fast-track the market shift toward compliant chemistries and reward firms with proven sustainable portfolios, anchoring long-range growth expectations.

Restraints Impact Analysis of Paints and Coatings Market*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global VOC regulations | -0.7% | Global, strictest in EU and California | Medium term (2-4 years) |

| Volatility in titanium-dioxide feedstock prices | -0.5% | Global, supply concentrated in China | Short term (≤ 2 years) |

| Longer drying/curing times for water-borne systems | -0.3% | Global, affecting industrial applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Global VOC Regulations

California’s South Coast Air Quality Management District periodically tightens Rule 1113, forcing reformulation or withdrawal of non-compliant products and raising research and development costs for smaller suppliers[2]South Coast Air Quality Management District, “Rule 1113 Architectural Coatings,” aqmd.gov . Europe’s upcoming CLP amendments add endocrine-disruptor labeling, obliging producers to review raw-material portfolios and update safety data sheets. China’s proposed unified architectural standard will extend VOC limits to auxiliary materials such as primers and sealers, broadening compliance complexity. Collectively, these regulations compress margins in the paints and coatings industry and elevate the importance of agile product-development pipelines.

Longer Drying/Curing Times for Water-Borne Systems

Although water-borne alkyds deliver significant VOC cuts, they often require controlled temperature and humidity to achieve target hardness, limiting their appeal for cold-weather outdoor projects. Industrial applicators cite slower line speeds and higher energy expenditure in bake ovens when switching from high-solids solvent-borne to water-borne. Equipment makers are responding with forced-air IR modules and dehumidification tunnels, but capex remains prohibitive for small job shops. Until performance parity and throughput metrics align fully, these operational constraints will act as a modest drag on conversion rates within the paints and coatings industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Paints and Coatings Market Segment Analysis

By Resin:

Acrylics Sustain Wide AdoptionAcrylic chemistries delivered 35.78% paints and coatings industry share in 2025 and are projected to post a 3.98% CAGR through 2031, underpinned by proven weatherability, color retention and low-VOC credentials that meet architectural and light-industrial demands. Formulators continue to refine cross-linked structures that boost scrub resistance and stain blocking, giving do-it-yourself and professional painters longer service intervals. Growth momentum stems from emerging market urbanization where acrylic emulsion paints dominate new housing interiors. Producers are scaling regional reactor capacity to shorten lead times and localize color assortments, a strategy that enhances competitiveness against solvent-borne rivals.

The resin landscape is gradually consolidating as multinationals streamline portfolios toward high-margin acrylic dispersion platforms. Alkyds maintain niche relevance in metal and wood finishes but face margin pressure from soybean-oil price fluctuations. Epoxy demand remains steady in heavy-duty maintenance; however, price stability achieved in 2025 reflects balanced capacity rather than a structural upswing. Polyurethane and polyester systems occupy specialized performance niches, abrasion-resistant floors and powder coatings respectively, yet lack the broad-based volume of acrylics. Overall, acrylics will continue to anchor formulators’ growth strategies across the paints and coatings market.

By Technology:

Water-Borne Dominance DeepensWater-borne technology controlled 50.62% of 2025 revenue and is forecast to expand at a 4.02% CAGR, benefiting from synchronized policy moves in North America, Europe and key Asian jurisdictions that cap allowable VOC limits in architectural categories. OEM vehicle lines that once relied on solvent-based primers have installed advanced atomization nozzles and flash-off zones tailored to water-borne rheology, accelerating automotive conversion rates. Suppliers leverage global resin synthesis networks to produce compact acrylic and polyurethane dispersions that shorten dry-time and maximize gloss, attributes critical for premium interior wall paints in the paints and coatings industry.

Solvent-borne systems remain entrenched in extreme-environment coatings where high-build properties offset application challenges; nonetheless cost inflation tied to xylene and mineral spirits mounts pressure to reformulate. Powder coating is growing inside metal furniture, appliance and general-industrial segments, aided by near-zero VOC emissions and reclaim capabilities that minimize overspray waste. UV-cure technologies carve space in flooring and packaging, enabled by instant hardness and low energy draw, yet adoption is limited by substrate sensitivity and photoinitiator cost. Taken together, water-borne formulations will continue to set the commercial baseline for the paints and coatings industry during the outlook period.

By End-User Industry:

Architectural Demand Anchors RevenueArchitectural coatings captured 48.25% of global revenue in 2025 and are advancing at a 4.33% CAGR through 2031, supported by sustained residential renovation cycles and public incentives linked to energy-efficient retrofits. National and city-level procurement guidelines now list certified low-VOC paints among mandatory materials, shifting product mixes toward premium zero-VOC interior finishes and elastomeric exterior membranes. Repaint frequency is lengthening in mature economies due to superior durability, yet rising disposable income in emerging markets more than compensates through higher per-capita consumption in the paints and coatings industry.

Automotive, marine and protective sectors together form a well-diversified industrial base that buffers architects against single-sector swings in the paints and coatings industry. Electric-vehicle assembly sparks demand for thermally conductive and anti-chip clearcoats, while port expansions in Southeast Asia lift orders for high-build epoxy anti-corrosives. Packaging coatings advance along a separate regulatory path as food-contact and BPA-free mandates reshape resin selection, creating fresh research and development streams.

Geography Analysis

APAC Paints and Coatings Market

Asia-Pacific contributed 46.21% of worldwide sales in 2025 and is tracking a robust 4.91% CAGR to 2031. The region’s paints and coatings market size benefits from ongoing megacity development, industrial reshoring and sustained public infrastructure outlays that collectively require ever larger volumes of protective and decorative finishes.

North America and Europe Paints and Coatings Market

North America is buoyed by federally funded transport corridors and an accelerating residential remodeling cycle boosted by stable mortgage rates. The push for ESG-aligned assets cats up adoption of certified low-emission interior paints, positioning water-borne suppliers for incremental share gains in the paints and coatings industry. Europe shows a measured recovery as major economies work through housing shortages and energy-retrofit pipelines tied to the EU’s Green Deal; however, tightening labeling frameworks under the updated CLP regulation add costs across supply chains.

South America and MEA Paints and Coatings Market

South America provides selective upside, headlined by Brazil where Sherwin-Williams’ purchase of BASF’s decorative unit instantly enlarges store footprints and gives contractors easier access to branded formulations. The Middle-East and Africa offer early-stage growth premised on mega-projects and resource-driven infrastructure, yet political risk and financing limitations restrain volume relative to Asia-Pacific. Harsh desert and coastal climates underpin specification of high-performance polysiloxane and fluoropolymer topcoats that protect capital assets.

Competitive Landscape

The global paints and coatings industry is moderately fragmented. Private-equity investors continue to roll regional platforms, aiming to exit to strategics seeking last-mile distribution or niche technology. Innovation agendas center on bio-based resin systems, smart functional finishes and AI-centric customer interfaces that collectively support premium pricing. Raw-material cost spikes and evolving chemical-control laws favor players with deep compliance resources and global sourcing flexibility, raising the barrier to entry for small independents.

Paints and Coatings Industry Leaders

The Sherwin-Williams Company

Nippon Paint Holdings Co., Ltd.

PPG Industries, Inc.

BASF

Akzo Nobel N.V.

- *Disclaimer: Major Players sorted in no particular order

Paints and Coatings Market Companies Covered in this Report

- Akzo Nobel N.V.

- Asian Paints

- Axalta Coating Systems Ltd.

- BASF

- Beckers Group

- Benjamin Moore & Co.

- Berger Paints India

- Chugoku Marine Paints, Ltd.

- DAW SE

- Hempel A/S

- Jazeera Paints

- Jotun

- Kansai Paint Co. Ltd

- Masco Corporation

- NATIONAL PAINTS FACTORIES CO. LTD.

- Nippon Paint Holdings Co., Ltd.

- NOROO Paint & Coatings co.,Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- Russian Paints Company

- SK Kaken Co. Ltd

- The Sherwin-Williams Company

Recent Industry Developments in Paints and Coatings Market

- February 2025: Sherwin-Williams completed acquisition of BASF’s Brazilian decorative paint business for USD 1.15 billion, adding two plants and USD 525 million in annual sales.

- October 2024: PPG divested its U.S. and Canada architectural coatings division to American Industrial Partners for USD 550 million, including 750 company-owned stores.

Global Paints and Coatings Market Report Scope

Paints and coatings are homogeneous mixtures of pigments, binders, additives, and various other components. Upon application on a substrate, the products make a thin layer of the solid film through polymerization or evaporation. Paints and coatings are widely used to improve the aesthetics and protect the substrate from deterrents like corrosion and others.

The paints and coatings market is segmented by resin, technology, end-user industry, and geography. By resin, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types (PVA, fluoropolymers, and polyaspartic resins). By technology, the market is segmented into water-borne coatings, solvent-borne coatings, powder coatings, and UV-cured technologies. By end-user industry, the market is segmented into architectural, automotive, wood, protective coatings, general industrial, transportation, and packaging coatings. The report also covers the market size and forecasts for the paints and coatings market in 39 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

Segmentation Overview

Resin

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

Technology

| Water-borne |

| Solvent-borne |

| Powder Coating |

| UV-cured Coating |

End-user Industry

| Architectural |

| Automotive |

| Wood |

| Protective Coating |

| General Industrial |

| Transportation |

| Packaging |

Geography

| Asia-Pacific | China (Including Taiwan) |

| India | |

| Japan | |

| Indonesia | |

| Australia and New Zealand | |

| South Korea | |

| Thailand | |

| Malaysia | |

| Philippines | |

| Bangladesh | |

| Vietnam | |

| Singapore | |

| Sri Lanka | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Benelux | |

| Russia | |

| Turkey | |

| Switzerland | |

| Scandinavian Countries | |

| Poland | |

| Portugal | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle-East | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Kuwait | |

| Egypt | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Algeria | |

| Morocco | |

| Rest of Africa |

| Resin | Acrylic | |

| Alkyd | ||

| Polyurethane | ||

| Epoxy | ||

| Polyester | ||

| Other Resin Types | ||

| Technology | Water-borne | |

| Solvent-borne | ||

| Powder Coating | ||

| UV-cured Coating | ||

| End-user Industry | Architectural | |

| Automotive | ||

| Wood | ||

| Protective Coating | ||

| General Industrial | ||

| Transportation | ||

| Packaging | ||

| Geography | Asia-Pacific | China (Including Taiwan) |

| India | ||

| Japan | ||

| Indonesia | ||

| Australia and New Zealand | ||

| South Korea | ||

| Thailand | ||

| Malaysia | ||

| Philippines | ||

| Bangladesh | ||

| Vietnam | ||

| Singapore | ||

| Sri Lanka | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Benelux | ||

| Russia | ||

| Turkey | ||

| Switzerland | ||

| Scandinavian Countries | ||

| Poland | ||

| Portugal | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle-East | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Kuwait | ||

| Egypt | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Algeria | ||

| Morocco | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the paints and coatings market be by 2031?

The paints and coatings market size is forecast to reach USD 229.9 billion by 2031, expanding at a 3.62% CAGR.

Which region contributes the most revenue?

Asia-Pacific accounted for 46.21% of 2025 revenue and is projected to preserve leadership as urbanization and infrastructure spending accelerate.

Which technology segment is growing the fastest?

Water-borne coatings lead both share and growth, advancing at a 4.02% CAGR due to global VOC regulations and consumer sustainability preferences.

What factors could restrain future growth?

Volatile titanium-dioxide prices, stricter chemical labeling rules and longer curing times for some water-borne systems present notable challenges.

Page last updated on: