Portugal Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

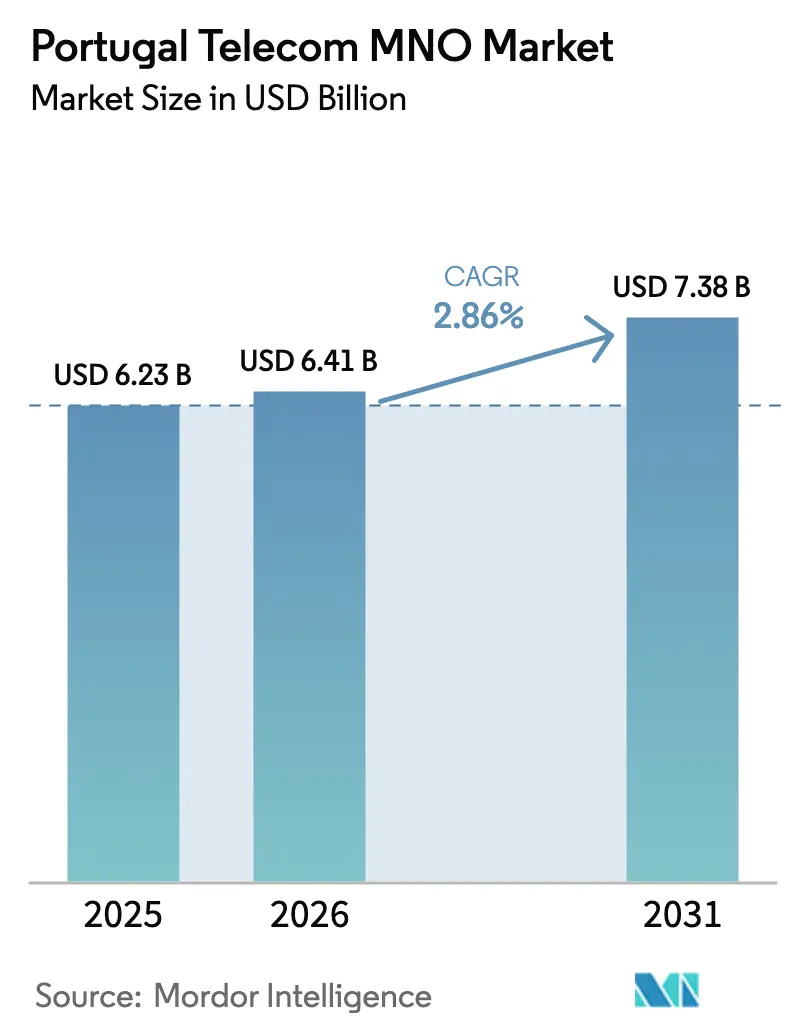

| Base Year Market Size (2025) | USD 6.23 Billion |

| Market Size (2026) | USD 6.41 Billion |

| Market Size (2031) | USD 7.38 Billion |

| Growth Rate (2026 - 2031) | 2.86% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portugal Telecom MNO Market Analysis by Mordor Intelligence

Portugal Telecom MNO Market size in 2026 is estimated at USD 6.41 billion, growing from 2025 value of USD 6.23 billion with 2031 projections showing USD 7.38 billion, growing at 2.86% CAGR over 2026-2031.

Momentum stems from 5G roll-outs, fiber densification and enterprise digitalisation, which together balance demographic softness and price competition. Operators leverage extensive fiber-to-the-home coverage, private 5G pilots and fixed-mobile convergence bundles to convert network upgrades into revenue, while government funding under the Digital Agenda 2030 underpins rural deployments. Market resilience also reflects copper-network switch-off savings, rising video traffic and new wholesale routes that strengthen Portugal’s role in trans-Atlantic connectivity.

Key Report Takeaways

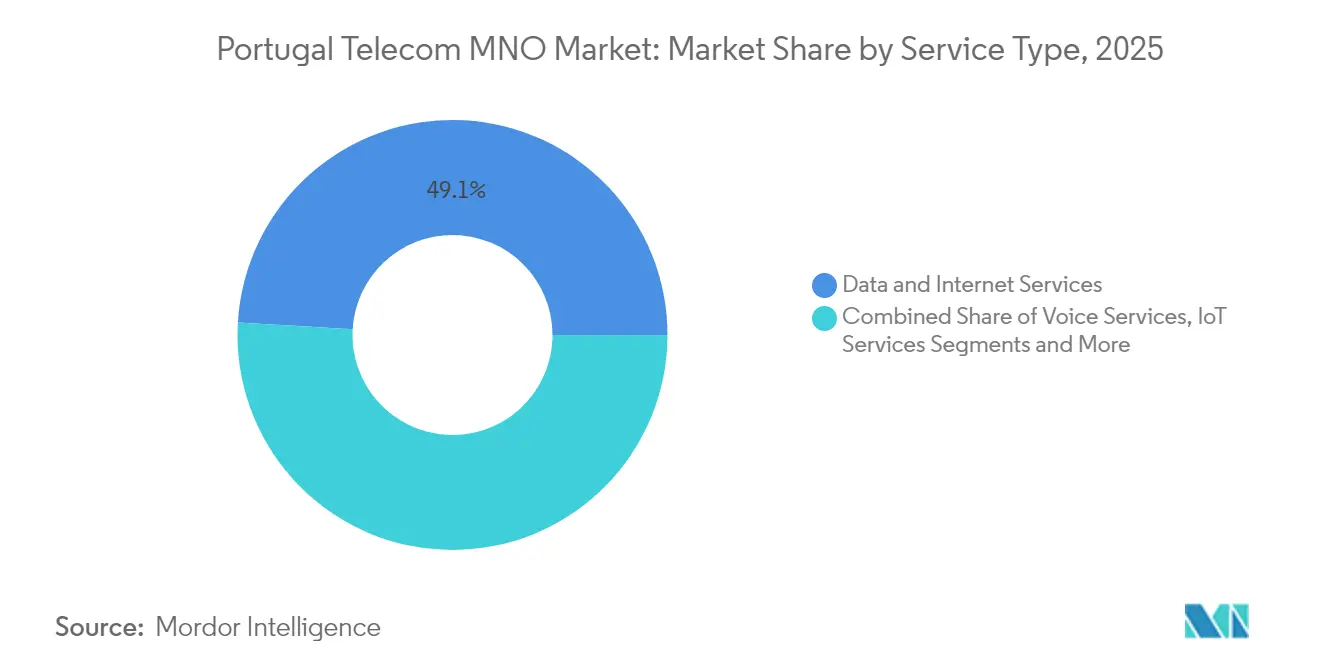

- By service type, data and internet services led with 49.08% revenue share in 2025; IoT and M2M is advancing at a 3.04% CAGR to 2031.

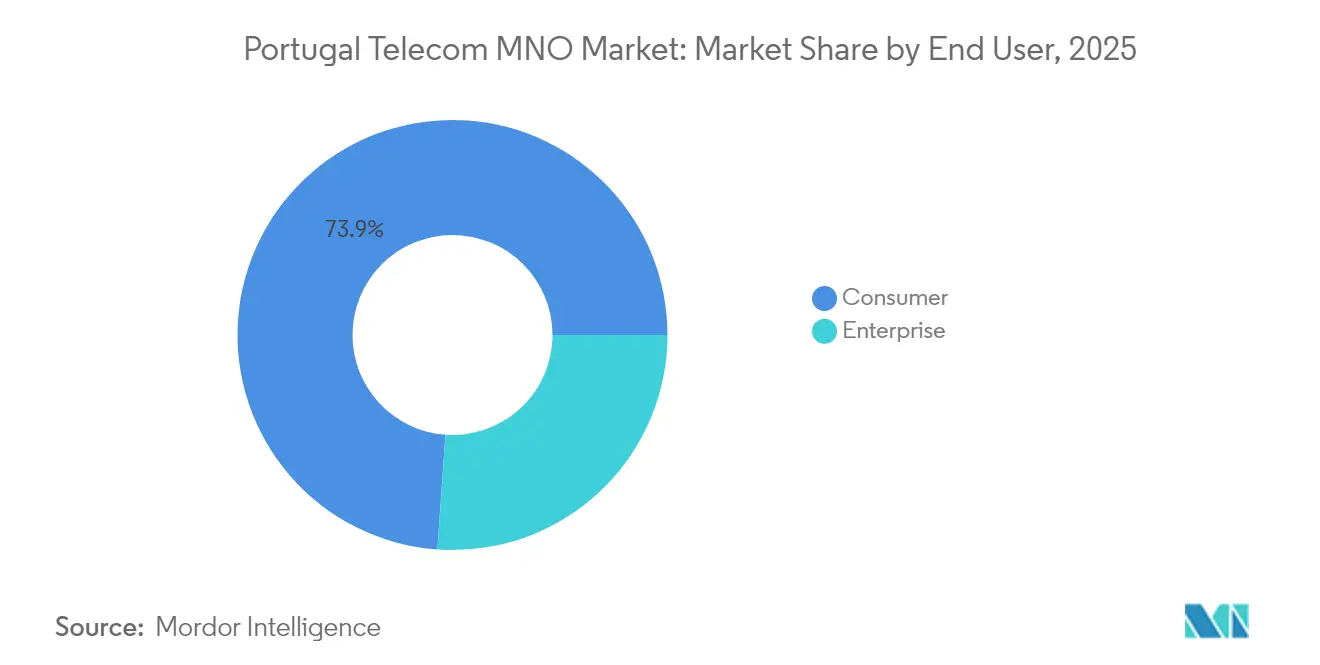

- By end user, enterprises captured 26.12% of the Portugal telecom MNO market share in 2025, while the enterprise segment is growing at a 3.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Portugal Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G roll-out reaching 90% population coverage target by 2025 | +0.8% | National, urban and industrial | Medium term (2-4 years) |

| Explosive growth in video-driven data consumption (mobile and fixed) | +0.7% | National, metros | Short term (≤ 2 years) |

| Government-backed VHCN/FTTH expansion to rural areas | +0.5% | Rural regions | Long term (≥ 4 years) |

| Enterprise digitalisation and private-network-led IoT demand | +0.6% | Industrial corridors | Medium term (2-4 years) |

| Fixed-mobile-convergence bundles boosting ARPU and churn reduction | +0.4% | National, urban | Short term (≤ 2 years) |

| Growth of wholesale data centre traffic on new submarine cables | +0.3% | Coastal landing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Roll-out Reaching 90% Population Coverage Target by 2025

Portugal activated 13,089 5G base stations by Q4 2024, blanketing all 308 municipalities and giving operators a platform to upsell ultra-low-latency use cases. NOS leads deployment with 4,786 sites, followed by Vodafone’s 4,611 and Digi’s 2,130. The government mandate for 90% population coverage by 2025 forces build-out beyond profitable urban cores, making shared-tower and subsidy models critical. MEO’s average 5G download speed of 324 Mbps showcases performance that can support cloud gaming, AR and industrial automation, yet sustainable monetisation hinges on converting enhanced mobile broadband users to premium tiers.

Explosive Growth in Video-Driven Data Consumption

Mobile data traffic climbed 25.4% year-on-year in Q4 2024 to 12.7 GB per SIM each month, with video streaming accounting for the majority. Fixed broadband traffic also increased 12%, suggesting complementary rather than substitutional usage. High-capacity FTTH backhaul—present in 95% of households—limits congestion, but continued traffic growth obliges operators to invest in spectrum refarming and network optimisation. Tiered data plans and speed-based pricing partly offset rising capacity costs.

Government-Backed VHCN/FTTH Expansion to Rural Areas

The National Strategy for Very High-Capacity Networks earmarks EU and Recovery-and-Resilience funds to subsidise gigabit fiber in low-density districts. Public tenders oblige open-access terms, enabling smaller ISPs and mobile operators to rent capacity rather than duplicate builds. Portugal’s aggressive copper switch-off—one of Europe’s fastest—frees maintenance opex for redeployment into fiber, while ensuring rural citizens and businesses gain symmetrical gigabit connectivity that underpins e-health, remote education and precision agriculture.

Enterprise Digitalisation and Private-Network-Led IoT Demand

Enterprise revenue is expanding at 3.44% CAGR, helped by factory-floor 5G pilots such as Vodafone’s private network at CIMPOR’s cement plant that enables drone inspections and AR maintenance. M2M SIMs grew 6.1% in 2024, yet still represent only 6.6% of total cards, giving runway for logistics, smart utility and agro-tech applications. Government programmes Indústria 4.0 and INCoDe 2030 add policy impetus to digital adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price wars and aggressive discounting eroding service ARPU | -0.9% | National, urban | Short term (≤ 2 years) |

| Ageing, low-growth population capping new subscriber additions | -0.6% | National, rural | Long term (≥ 4 years) |

| Intensifying OTT substitution reducing PayTV and voice revenue | -0.4% | National | Medium term (2-4 years) |

| Rising energy costs inflating network opex | -0.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Wars and Aggressive Discounting Eroding Service ARPU

Digi Portugal’s acquisition of Nowo introduced low-price bundles that prompted incumbents to counter with promotions, squeezing margins even as 5G and fiber capex peaks. PayTV ARPU stagnated in 2024 despite 97% household penetration, signalling maturity and price sensitivity. Regulatory scrutiny over retail tariffs further curtails upward pricing flexibility.

Ageing, Low-Growth Population Capping New Subscriber Additions

Portugal’s mobile penetration stands at 173.3 subscriptions per 100 inhabitants, leaving little headroom for organic adds. Rural depopulation compounds the issue, challenging operators to justify 5G roll-out economics outside urban centres. Consequently, revenue strategy pivots to ARPU uplift through premium tiers and B2B solutions rather than volume gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue While IoT Accelerates

Data and internet services accounted for 49.08% of the Portugal telecom market in 2025 at USD 3.06 billion, and are forecast to grow at 2.93% CAGR. Voice remains 23.74% of revenues, but minutes continue to decline as users adopt OTT calling inside FMC bundles. IoT and M2M revenues were USD 0.39 billion, representing the fastest sub-segment at 3.04% CAGR, powered by enterprise private 5G. OTT and PayTV kept an 11.02% slice of the Portugal telecom market size despite streaming competition, thanks to near-universal bundling with broadband. Other wholesale and value-added services supplied 9.93% of sales, providing risk diversification for operators.

By End User: Enterprise Segment Outpaces Consumer Growth

Enterprise customers produced USD 1.63 billion in 2025, or 26.12% of total revenue, and are expanding faster than consumer accounts. The segment values dedicated fiber access, SD-WAN and managed security layered on top of connectivity, which lift margins versus retail mobile. In contrast, consumer receipts grew more slowly to USD 4.60 billion as saturation and price sensitivity persist. Nevertheless, high 5G handset penetration and 89% FTTH household coverage enable operators to upsell speed-based tiers, keeping churn in check through converged quadruple-play bundles.

Geography Analysis

Lisbon and Porto metropolitan areas host 61% of 5G sites and generate the bulk of premium ARPU. These corridors also attract data-centre and hyperscale investment linked to new submarine cables such as EllaLink and Equiano, which feed wholesale bandwidth demand. Northern industrial zones around Braga exploit private 5G for Industry 4.0; while interior regions leverage public-funded fiber to close the digital gap. The Algarve and island territories register seasonal spikes from tourism, making eSIM-only packages popular among visitors. Rural Alentejo agriculture adopts smart-farming IoT, albeit from a low base, reflecting a gradual shift in operator focus beyond dense urban footprints.

Competitive Landscape

Three integrated players—MEO (36.9%), NOS (30.6%) and Vodafone (28.0%)—hold a combined 95.5% of mobile lines, creating a concentrated oligopoly. MEO exploits its legacy PSTN replacement with FTTH to cross-sell PayTV. NOS markets 93% 5G population coverage and the fastest speeds in Portugal. Vodafone differentiates in enterprise through international MPLS and private-network expertise. Digi Portugal’s Nowo acquisition injects price pressure yet its Portugal telecom market share remains below 3% so far. Strategic moves include NOS–Vodafone fiber-sharing, MEO’s ISO 22301 certification for continuity and NOS’s cloud acquisition of Claranet Portugal, all intended to broaden service mixes and protect margins amid commoditising access.

Portugal Telecom MNO Industry Leaders

Vodafone Group Plc

MEO (formerly TMN)

NOS (formerly Optimus and ZON)

Digi Portugal

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: MEO recorded average 5G download speeds of 324 Mbps, topping independent DECO PROTESTE rankings.

- February 2025: ANACOM confirmed 13,089 national 5G sites, up 24% quarter-on-quarter.

- March 2024: Telecoms company Digi, a company of Romanian origins, announced plans to launch its first telecommunications offer in Portugal. The telecoms operator has also revealed that it intends to provide fixed and mobile services, namely 5G Fibre Optic.

- November 2023: NOS, in partnership with Nokia, launched its 5G standalone network in Portugal. The operator reports having more than 4,200 5G base stations, covering over 93% of the Portuguese population.

Portugal Telecom MNO Market Report Scope

The study provides an in-depth analysis of the telecommunication industry in Portugal.

The Portuguese telecom MNO market is segmented by services, which have been further classified into voice services (wired and wireless), data and messaging services, and OTT and PayTV. The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming And International Services, Enterprise And Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming And International Services, Enterprise And Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What revenue level could telecom services in Portugal reach by 2031?

Total service revenue is projected to climb to USD 7.38 billion by 2031, reflecting a 2.86% CAGR from 2026.

Which service category currently brings in the most money?

Data and internet services contribute the largest share at 49.08% of total turnover, equal to USD 3.06 billion in 2025.

How extensive is 5G population coverage across the country?

Operators had activated 13,089 5G sites by Q4 2024, extending signals to every municipality and covering 73% of parishes.

Why is IoT viewed as a key growth engine?

IoT and M2M revenues, although only 6.23% of 2025 sales, are advancing at a 3.04% CAGR thanks to private 5G networks that support Industry 4.0, smart-city and agricultural use cases.

How concentrated is operator ownership in Portugal?

MEO, NOS and Vodafone together control about 95.5% of mobile subscriptions, underscoring an oligopolistic structure.

Page last updated on: