Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 45.52 Billion |

| Market Size (2026) | USD 47.01 Billion |

| Market Size (2031) | USD 55.23 Billion |

| Growth Rate (2026 - 2031) | 3.28% CAGR |

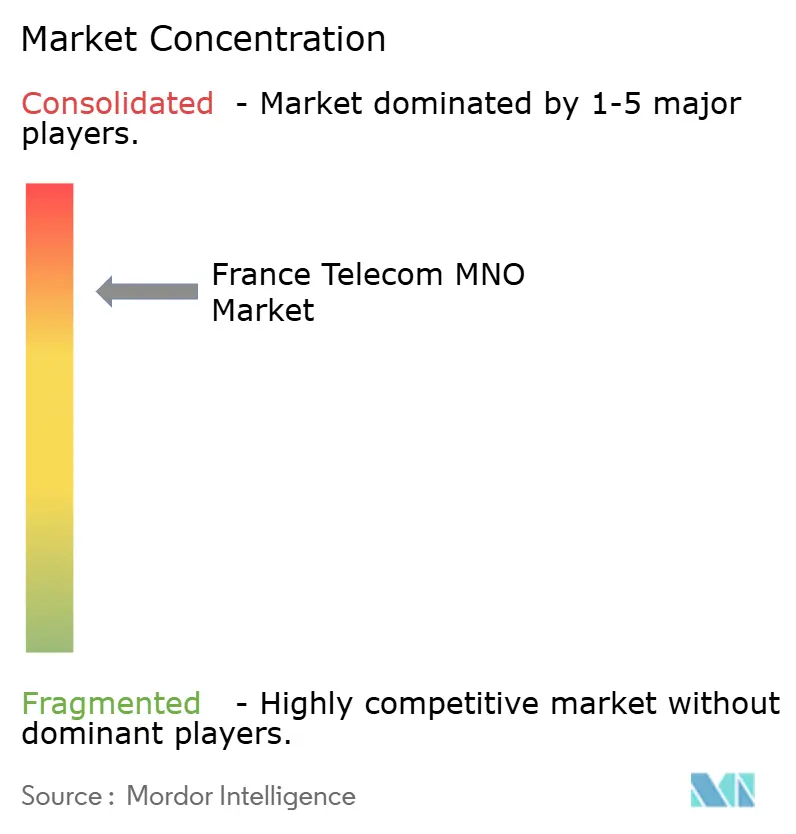

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Telecom MNO Market Analysis by Mordor Intelligence

The France Telecom MNO Market size is expected to grow from USD 45.52 billion in 2025 to USD 47.01 billion in 2026 and is forecast to reach USD 55.23 billion by 2031 at 3.28% CAGR over 2026-2031.

Near-term momentum comes from rapid 5G standalone rollouts, fiber-backed fixed–mobile bundles, and a pivot toward enterprise digitization services, all of which are reshaping revenue composition. Operators are channeling capital into 3.5 GHz spectrum, private 5G zones, and edge platforms that enable differentiated quality for data-heavy applications. Regulatory directives on network sharing and eco-design are sharpening cost discipline, while cyber resilience and energy efficiency requirements are altering investment priorities. Intensifying competition among Orange, SFR, Bouygues Telecom, and Free Mobile sustains price pressure even as data usage rises, pushing carriers to unlock new value from IoT, cloud connectivity, and managed services.

Key Report Takeaways

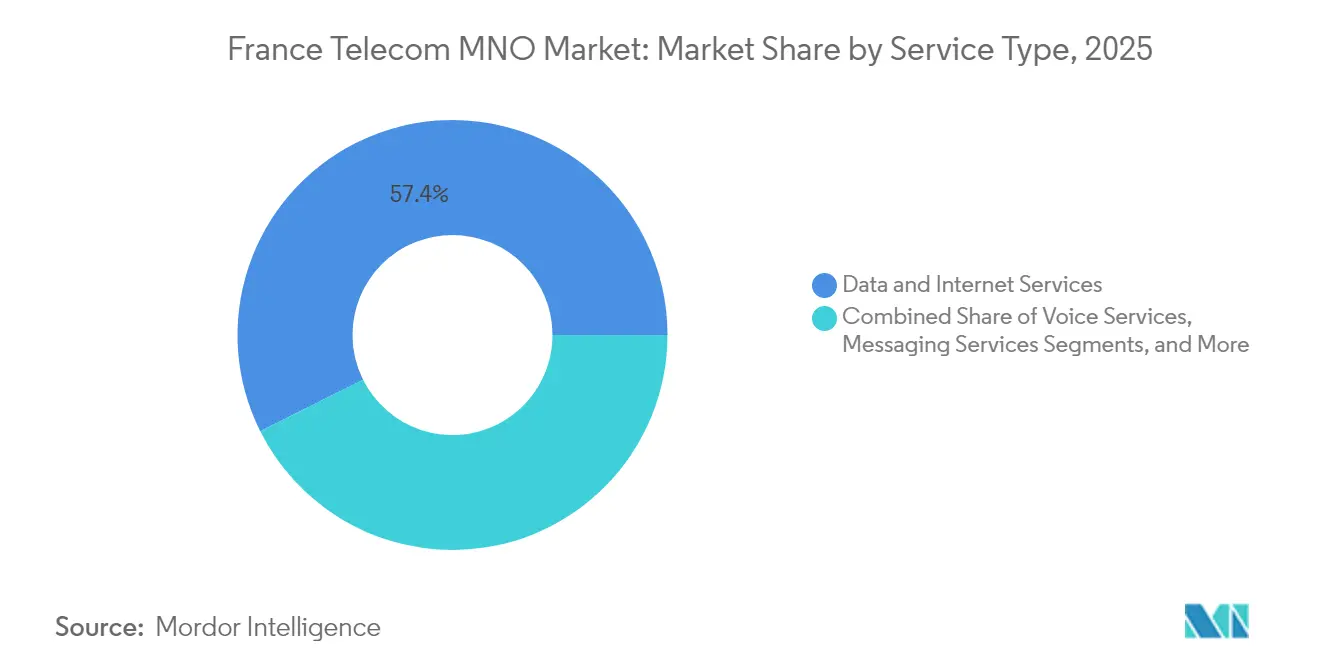

- By service type, data and internet services held 57.39% of the France telecom MNO market share in 2025, while IoT and M2M services are projected to grow at a 3.39% CAGR through 2031.

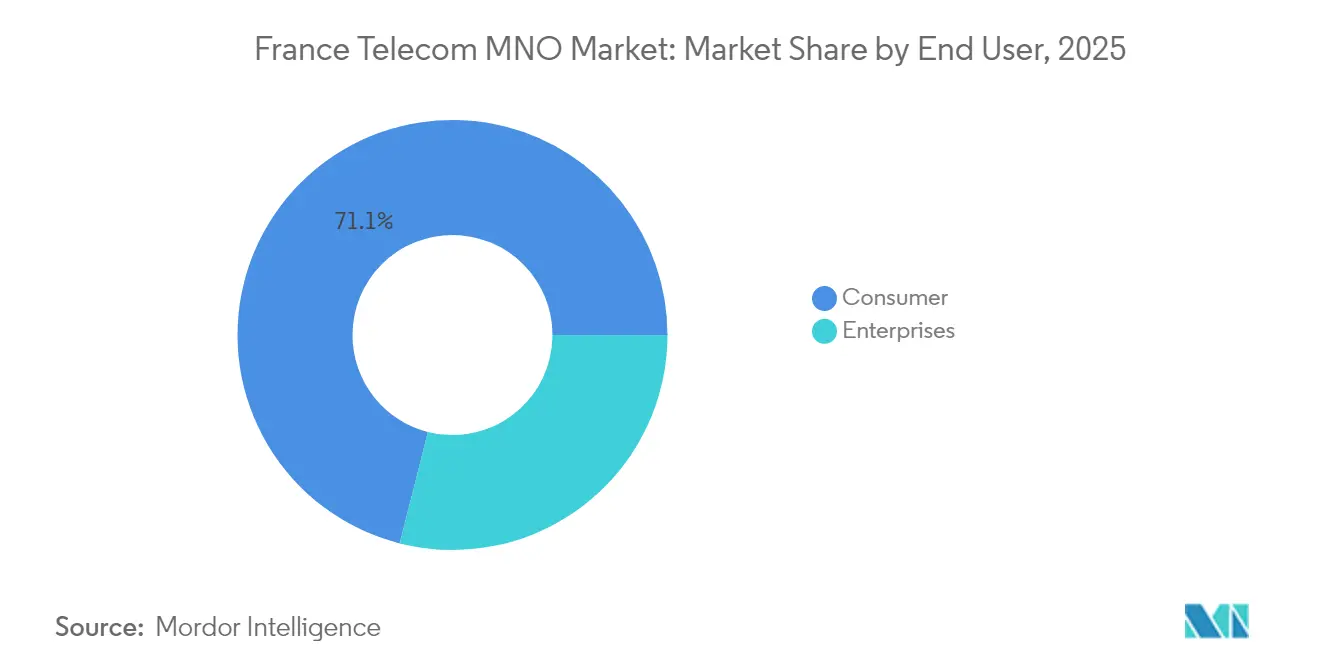

- By end user, the consumer segment accounted for 71.05% of the France telecom MNO market size in 2025; the enterprise segment is advancing at a 3.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G coverage expansion and FWA drives data-centric wallets | +0.8% | National, early gains in Paris, Lyon, Marseille | Medium term (2-4 years) |

| Fiber-backed FMC bundles boost fixed/mobile ARPU uplift | +0.6% | National, accelerated in rural areas | Short term (≤ 2 years) |

| Video-streaming and cloud gaming fuel mobile data demand | +0.5% | National, concentrated in urban centers | Short term (≤ 2 years) |

| Enterprise Industry 4.0 projects accelerate IoT SIM uptake | +0.4% | Industrial regions, Île-de-France, Auvergne-Rhône-Alpes | Medium term (2-4 years) |

| Release of 3.5 GHz spectrum for private 5G SA networks | +0.3% | Major industrial zones | Long term (≥ 4 years) |

| eSIM-only handset channels reduce churn and acquisition cost | +0.2% | National, premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Coverage Expansion and FWA Drives Data-Centric Wallets

Early 5G standalone launches are shifting mobile economics as premium network slicing elevates ARPU and alleviates peak-hour congestion [1]The Fast Mode, “iPhone 15 Users Get First Taste of Orange 5G+,” thefastmode.com. Fixed Wireless Access leverages existing radio assets to serve rural households that lack fiber, enabling carriers to monetize spectrum more efficiently while extending competitive reach. Orange’s 5G Core Network-as-a-Service offer lowers entry costs for regional operators, accelerating nationwide coverage and fostering service innovation. As latency-sensitive workloads migrate to the edge, the France telecom MNO market will favor providers that can pair low-latency access with cloud adjacency.

Fiber-Backed FMC Bundles Boost Fixed/Mobile ARPU Uplift

Seamless bundling of gigabit FTTH and 5G is raising household spend and reducing churn as 20.6 million homes now subscribe to FTTH with a 78% take-up rate [2]Deepomatic, “FTTH Council Fiber Market Panorama Key Takeaways,” deepomatic.com . Bouygues Telecom has demonstrated an EUR 33 fixed ARPU while stabilizing mobile prices by promoting all-inclusive plans, confirming that convergent offers can insulate revenue from pure-price plays [3]Bouygues, “H1 2024 Presentation,” bouygues.com. Operators that integrate intelligent service orchestration and cross-channel care will capture the highest lifetime value.

Video-Streaming and Cloud Gaming Fuel Mobile Data Demand

Average monthly consumption rose to 14.3 GB per user in 2024, up 18% year on year, with video accounting for the bulk of traffic. Cloud gaming raises latency and jitter requirements, prompting operators to adopt edge caching and satellite backhaul partnerships with Eutelsat to preserve quality of experience [4]Telecoms.com, “Orange Buys Into Eutelsat’s LEO Capabilities,” telecoms.com. Successful price tiering now depends on guaranteed speeds and bundled content rather than unlimited volume alone, reinforcing the need for granular network analytics in the France telecom MNO market.

Enterprise Industry 4.0 Projects Accelerate IoT SIM Uptake

Manufacturing and logistics firms are piloting private 5G and sensor networks to enable real-time monitoring and automation. Orange Business supports these deployments with its Live Objects platform that combines device management, analytics, and security in one stack. As global cellular IoT lines are expected to reach 6.4 billion by 2029, French operators that master vertical solutions will convert connectivity into multi-layer contracts that boost margin.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fierce price competition keeps blended ARPU flat | -0.9% | National, most pronounced in urban areas | Short term (≤ 2 years) |

| >110% SIM penetration limits organic subscriber growth | -0.5% | National, saturation in all regions | Long term (≥ 4 years) |

| Eco-design and energy-efficiency regulation lift opex | -0.3% | National, compliance-driven | Medium term (2-4 years) |

| Uncertainty over mmWave auction timing delays capex plans | -0.2% | National, affects 5G strategy | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fierce Price Competition Keeps Blended ARPU Flat

Since Free Mobile disrupted pricing, the nominal price of a typical bundle has fallen 45% between 2011 and 2016, and operators still struggle to pass network-quality premiums to consumers. Opensignal continues to rank Orange at the top on download speed and coverage yet its mobile ARPU remains broadly flat because price-sensitive users switch quickly when promotions appear. This perpetual discounting forces carriers to chase efficiency and service diversification rather than headline price increases across the France telecom MNO market.

>110% SIM Penetration Limits Organic Subscriber Growth

There are 83.4 million active SIMs versus 68 million residents, leaving no room for first-time buyers and turning subscriber gains into zero-sum share shifts. SFR’s recent 1.3 million subscriber loss shows how quickly churn can erode scale in a saturated environment. Operators must therefore pivot to ARPU-enhancing products like IoT lines, private networks, and cybersecurity services that uncouple growth from raw SIM counts within the France telecom MNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Dominance Drives IoT Innovation

Data and Internet services secured 57.39% of the France telecom MNO market share in 2025, displacing voice as the primary revenue pillar. The France telecom MNO market size for IoT and M2M is set to expand at a 3.39% CAGR through 2031, reflecting enterprise appetite for connected machinery and smart city grids. OTT and PayTV bundles broaden stickiness as carriers integrate Netflix, Disney+, and local streaming apps into unified interfaces that curb out-of-bundle churn. Voice and messaging revenues slide as customers shift to over-the-top alternatives, yet remain relevant for inbound roaming and regulatory emergency obligations.

Continued data traffic growth obliges operators to densify radio sites and introduce edge compute, while IoT project momentum encourages investment in lightweight cores and device-management platforms. As private 5G networks emerge for the Paris Olympics and industrial campuses, the France Telecom MNO market will see higher revenue per bit for specialized slices than for best-effort mobile broadband. Operators that bundle analytics, security, and cloud integration alongside connectivity will capture the bulk of value in this ascending segment of the France telecom MNO market.

By End User: Enterprise Growth Accelerates Digital Transformation

The consumer segment still contributes 71.05% of 2025 revenue, yet its growth is modest due to price competition and SIM saturation. In contrast, the France telecom MNO market size linked to enterprise services is rising at a 3.62% CAGR owing to Industry 4.0 rollout, SD-WAN adoption, and cloud migration. Orange Business illustrates the shift with its SD-WAN Essentials launch that embeds security and AI-based performance management for smaller offices.

Tech-centric offers such as managed GenAI, hybrid cloud, and zero-trust security are estimated to capture 87% of the B2B telecom wallet by 2027. As enterprises seek unified connectivity and IT stacks, carriers that provide consultative expertise will outperform those that deliver pure bandwidth. The France telecom MNO market, therefore, rewards incumbents that can blend infrastructure resilience with solution-centric go-to-market capabilities tailored to sector-specific needs.

Geography Analysis

Nationwide, the France telecom MNO market benefits from advanced infrastructure and universal 4G coverage, yet regional disparities shape revenue profiles. Île-de-France generates the highest ARPU, fueled by dense urban usage and a concentration of headquarters that adopt premium enterprise connectivity. Auvergne-Rhône-Alpes and Hauts-de-France contribute materially through manufacturing digitalization, logistics hubs, and smart mobility pilots. Rural departments gain coverage through the New Deal for Mobile program, which lifted the 4G footprint from 45% to 88% between 2018 and 2023.

As fiber deployment accelerates, operators leverage Fixed Wireless Access to address isolated villages while maintaining return on spectrum. The France Telecom MNO market size in overseas territories remains smaller but shows outsized growth potential thanks to fresh spectrum releases in Martinique and Guadeloupe that support improved 4G and nascent 5G rollouts. Population-weighted 5G coverage varies sharply: Free Mobile claims 94% reach while Orange focuses on depth in high-traffic corridors, attaining 60% of metropolitan areas with faster mid-band layers.

Copper switch-off plans introduce regional transition complexity because legacy PSTN serves niche enterprise use cases in low-density regions. Operators thus stage migrations alongside fiber build-outs to avoid service gaps and regulatory penalties. Geography, therefore, intersects with service innovation and regulatory duties, steering capital to locales where fixed and mobile synergies maximize lifetime yield within the France telecom MNO market.

Competitive Landscape

Four operators dominate the France telecom MNO market, yet none exceed a one-third share, keeping rivalry intense. Orange leads with 31% mobile and 39% fixed share, leveraging superior network metrics and enterprise breadth to command selective premiums. SFR controls 24% but faces debt overhang and recent churn, prompting asset reviews that could catalyze market consolidation. Bouygues Telecom pursues quality-focused differentiation, recently acquiring La Poste Telecom to add 2.3 million customers and enhance retail reach. Free Mobile remains the low-price disruptor, pushing unlimited plans and broad 5G availability to entice switchers.

Strategic initiatives reflect varied strengths. Orange’s satellite alliance with Eutelsat extends coverage to maritime, aviation, and remote government sites, diversifying revenue beyond terrestrial footprints. Bouygues Telecom unveiled its B.IG brand to reinforce family bundles and pursue mid-market upsell. SFR’s network modernization hinges on capex relief from potential spectrum-sharing pacts, while Free Mobile exploits infrastructure-light expansion and competitive wholesale agreements. Diversification into IoT, private 5G, and cybersecurity is common across all players as they seek resilience beyond commodity data in the France telecom MNO market.

France Telecom MNO Industry Leaders

Orange S.A.

SFR (Altice France)

Bouygues Telecom

Free Mobile (Iliad)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Orange strengthened its OneWeb partnership to extend low-Earth-orbit satellite reach for enterprise and government clients.

- March 2025: Orange launched the world’s first 5G Core Network-as-a-Service model.

- March 2025: Inherent Group acquired CONEXIO Telecom, signaling ongoing consolidation in enterprise connectivity.

- January 2025: Nokia completed the sale of Alcatel Submarine Networks to the French State.

- February 2024: Bouygues Telecom closed the EUR 950 million purchase of La Poste Telecom, adding 2.3 million customers.

France Telecom MNO Market Report Scope

The study provides an in-depth analysis of the telecommunication industry in France. The French telecom market is segmented by services, which are further classified into voice services (wired, wireless), data and messaging services, and OTT and pay TV.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current value of the France telecom MNO market?

The market is worth USD 47.01 billion in 2026 and is projected to rise to USD 55.23 billion by 2031.

How fast is 5G coverage expanding in France?

Free Mobile claims 94% population coverage while Orange focuses on deep mid-band layers that now reach 60% of metropolitan areas.

Which service segment is growing the quickest?

IoT and M2M services are expanding at a 3.39% CAGR through 2031, outpacing voice and messaging segments.

Why is blended ARPU flat despite rising data traffic?

Prolonged price competition among four national operators offsets the impact of higher usage, limiting the ability to raise prices.

What regions present the strongest enterprise connectivity demand?

Île-de-France, Auvergne-Rhône-Alpes, and Hauts-de-France lead due to dense manufacturing and logistics activities that need private 5G and IoT solutions.

How will fiber deployment affect mobile operators?

Fiber-backed FMC bundles raise customer lifetime value and enable cross-selling of premium 5G and OTT services, improving margin resilience.

Page last updated on: