Denmark Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.14 Billion |

| Market Size (2026) | USD 4.32 Billion |

| Market Size (2031) | USD 5.31 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

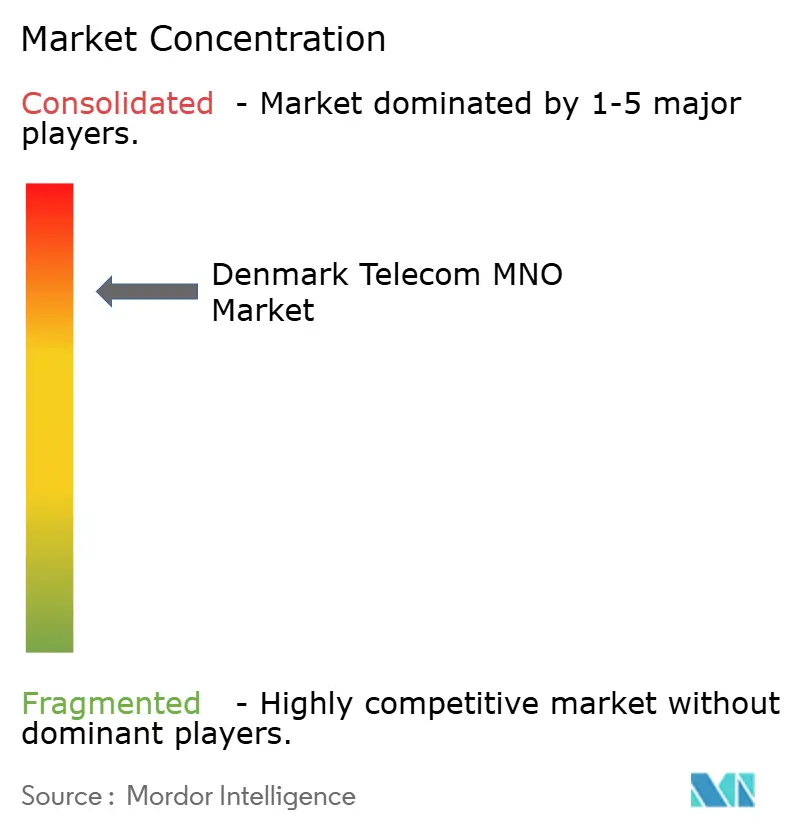

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Telecom MNO Market Analysis by Mordor Intelligence

The Denmark Telecom MNO Market size was valued at USD 4.14 billion in 2025 and estimated to grow from USD 4.32 billion in 2026 to reach USD 5.31 billion by 2031, at a CAGR of 4.23% during the forecast period (2026-2031).

Strong nationwide 5G availability, which already covers 83.9% of the population, anchors this steady expansion. [1]Ookla Insights Team, “5G Coverage in Europe: Progress Toward Goals Amid Lingering Disparities,” Ookla, ookla.com Operators benefit from government-mandated spectrum rules that tie rural obligations to every spectrum block, creating a level network playing field and speeding up coverage. Intensifying enterprise digitization, particularly inside Denmark’s large wind-energy and maritime logistics sectors, keeps data consumption high and stabilizes average revenue per user. At the same time, network-sharing frameworks have lowered capital requirements, allowing the three remaining mobile network operators, Nuuday, Telenor, and Norlys, to sustain service quality while absorbing price pressure from MVNO offers. Heightened renewable-energy surcharges on electricity still inflate operating expenses, but rapid adoption of solar power purchase agreements and radio-access-network (RAN) energy-efficiency upgrades is offsetting part of that cost burden.

Key Report Takeaways

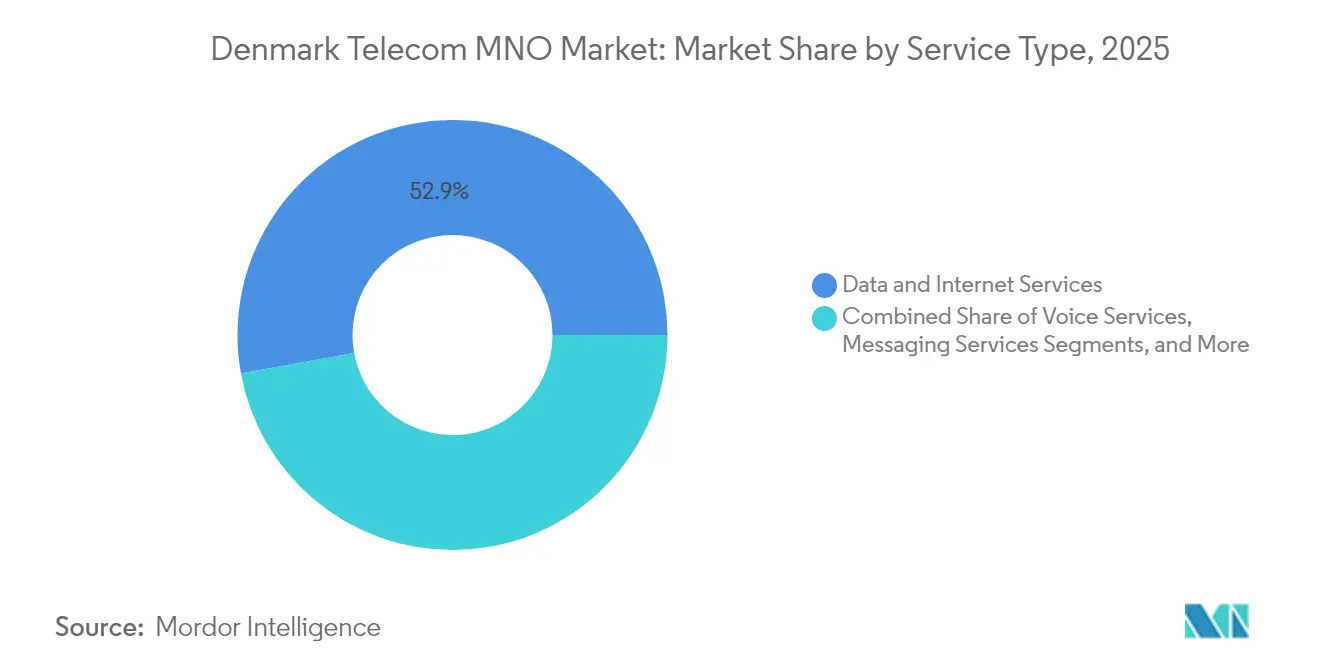

- By service type, data and internet services led with 52.87% of the Denmark telecom MNO market share in 2025, while IoT and M2M logged the fastest forecast CAGR at 4.58%.

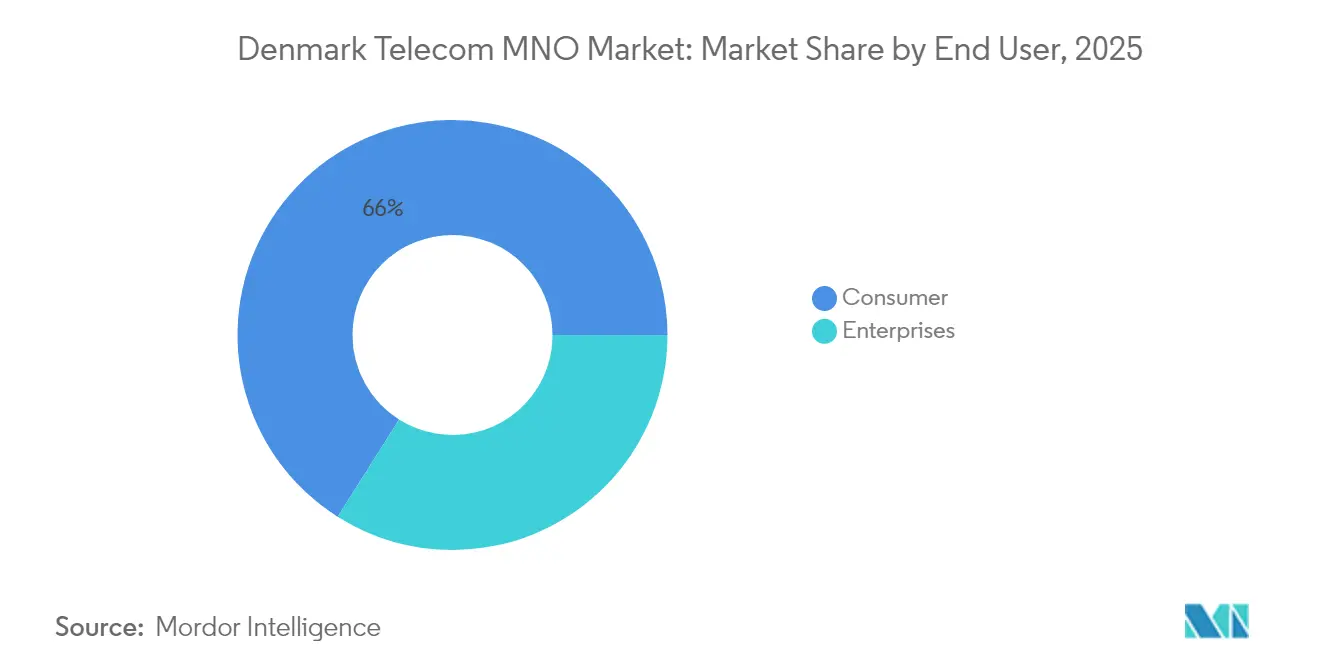

- By end user, the consumer segment held 66.03% share of the Denmark telecom MNO market size in 2025; the enterprise segment is on track for the fastest growth at a 4.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Denmark Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide 5G coverage and rapid device uptake | +1.2% | National; strongest in Copenhagen, Aarhus, Odense | Short term (≤ 2 years) |

| Surge in mobile data traffic stabilizing ARPU | +0.8% | Urban clusters | Medium term (2-4 years) |

| Pro-investment spectrum policy with rural coverage obligations | +0.6% | Rural and underserved areas | Long term (≥ 4 years) |

| Enterprise digitization fueling IoT demand | +0.9% | Industrial corridors and ports | Medium term (2-4 years) |

| Green tax incentives for energy-efficient RAN upgrades | +0.4% | High-energy cell-sites nationwide | Long term (≥ 4 years) |

| Private 5G demand from offshore-wind and smart-port corridors | +0.3% | North Sea coastal zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nationwide 5G Coverage and Rapid Device Uptake

Standalone 5G now blankets all Danish regions, with TDC NET’s network delivering peak 7 Gbps throughput during live field tests. [2]Ericsson Press Office, “TDC NET Launches First 5G SA Network in Denmark,” Ericsson, ericsson.com Unlimited-data plans tied to that coverage are prompting premium upgrades; Telenor recorded a 2.2% year-on-year ARPU increase in 2024 after moving subscribers to 5G tiers that carry 20-30% price premiums over 4G bundles. The synchronized rural-plus-urban rollout avoids the urban-first digital divide seen elsewhere in Europe, reinforcing Denmark’s reputation as an inclusive connectivity leader.

Surge in Mobile Data Traffic Stabilizing ARPU

National data usage continues to climb even as penetration tops 150%, largely because unlimited plans shift customer focus to network experience rather than megabyte quotas. Joint solar PPAs covering 75% of network power for Telenor and Telia underline the shift toward sustainability as a differentiator and mitigate the cost impact of Denmark’s rising renewable-energy levy on electricity.

Enterprise Digitization Fueling IoT Demand

Denmark’s push toward carbon neutrality by 2045 is tying real-time monitoring to every industrial process. TDC’s open IoT platform already supports nationwide smart-waste, smart-parking, and municipal utility projects, creating stickier, multi-year revenue lines than consumer voice or SMS. [3]TDC Group, “Læs hvordan IoT kan skabe værdi for jer,” TDC, tdc.dk In offshore wind farms up to 200 kilometers off Jutland, private 5G links allow autonomous operation and predictive maintenance, while Bornholm’s remote-drive plants use 5G gateways to manage industrial drives and cut onsite carbon output. [4]Teltonika Networks Editorial Team, “Industrial 5G Gateway for iC7 Drive Remote Management,” Teltonika Networks, teltonika-networks.com Each B2B contract features service-level agreements and low churn, smoothing operator cash flows.

Pro-Investment Spectrum Policy with Rural Coverage Obligations

The Danish Energy Agency’s 3.5 GHz auction attached 98% population-coverage targets to each license, forcing all winners, regardless of size, to serve remote islands and agriculture clusters. Free supplemental spectrum for underserved areas supports network-sharing frameworks, thus slashing redundant towers while preserving competition. As a side effect, Danish operators can pitch pan-Nordic or pan-European contracts to multinational enterprises that require uniform coverage across their value chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fierce price competition from SIM-only and MVNO offers | −0.7% | Dense urban markets | Short term (≤ 2 years) |

| Saturated subscriber base (>150% penetration) | −0.5% | Entire country | Medium term (2-4 years) |

| Rising renewable-energy surcharges inflating OPEX | −0.4% | National | Long term (≥ 4 years) |

| Spectrum-sharing rules eroding competitive moats | −0.3% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fierce Price Competition from SIM-Only and MVNO Offers

Low-overhead brands ride on host networks and sell identical quality at discounts that run 30-40% below flagship tariffs. Wholesale-access regulation prevents the big three from denying MVNOs capacity, so incumbents pivot toward bundled value, mobile plus fiber, TV, or cloud back-up, because those packages are harder for discounters to replicate at scale. While the tactic cushions churn, it demands sustained service innovation and marketing spend, squeezing margins.

Saturated Subscriber Base (>150% Penetration)

Penetration surpasses 1.5 SIMs per resident, leaving almost no untapped consumer pool. Operators therefore hunt growth by nudging existing customers into higher-tier 5G or content-rich plans and by monetizing connected devices in industries and public services. For challengers, expansion means luring rivals’ users, not acquiring first-time subscribers; this raises acquisition costs and reinforces the logic of recent market consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Usage Outpaces All Other Revenue Streams

Data and internet offerings captured 52.87% of 2025 revenue and underpin the Denmark telecom MNO market. The category benefited from nationwide 5G, which lets operators attach premium-tier surcharges and sell guaranteed throughput for video or gaming. Meanwhile, voice’s share eroded as over-the-top calling gains prominence, and messaging dwindled further with ubiquitous app-based chat. IoT and M2M services, though only a single-digit slice today, are projected to advance at a 4.58% CAGR, the fastest pace inside the Denmark telecom MNO market, because offshore wind farms, smart ports, and municipal utilities need low-latency connectivity. That acceleration means IoT could exceed both voice and legacy SMS revenue by 2031, especially once autonomous maritime operations scale up in Esbjerg and Aalborg harbors. Operators are therefore integrating network slices and edge-computing nodes to guarantee deterministic performance. OTT and Pay-TV add-ons broaden consumer stickiness yet face rising content-licensing costs, nudging carriers to produce local original programming or co-finance sports streaming rights. Other services, roaming, enterprise wholesale, and VAS, remain steady contributors but generate thinner margins thanks to EU roaming-charge caps.

With data representing more than half of 2025 revenue, the Denmark telecom MNO market size for data-centric products is forecast to add nearly USD 600 million in incremental income by 2031. Over the same horizon, IoT’s portion is expected to climb to 8.41% of the Denmark telecom MNO market share, propelled by private 5G campus deployments in wind farms and logistics hubs where deterministic uplink rates are mission critical.

By End User: Enterprise Adoption Accelerates

The consumer segment retained 66.03% of its income last year, yet it faces sluggish growth due to saturation. Operators now court loyalty through packaged deals, mobile, fixed, TV, and cybersecurity, as YouSee’s 5G home-broadband plan with 1 TB at DKK 349 illustrates. Those bundles lift average revenue per household but also raise content-cost exposure. In contrast, enterprise services are set to outstrip consumer growth, registering a 4.67% CAGR to 2031 on the back of Denmark’s green-transition mandates. Ports, dairies, and manufacturing groups sign multi-year IoT or private-network contracts with strict uptime clauses, which makes churn rare and margins healthier than in prepaid consumer lines. Telenor’s TrueTalk suite for business voice, SIP trunking, and mobile PBX positions the operator to chase that premium.

Enterprise uptake is also redefining investment priorities: edge-cloud nodes near Esbjerg harbor host low-latency control loops for autonomous cranes, while inland data centers support AI-driven predictive maintenance for wind-turbine supply chains. Consequently, the Denmark telecom MNO market size for B2B contracts is on track to climb from USD 1.41 billion in 2025 to USD 1.85 billion in 2031, capturing 34.85% of overall revenue by the forecast horizon.

Geography Analysis

Denmark’s compact topography and flat terrain make nationwide rollouts cost-efficient; TDC NET finished 100% 5G coverage in mid-2023, two years ahead of the European average. Copenhagen’s capital region, home to 39.62% of national telecom turnover, favors premium unlimited plans and enterprise private networks tied to government smart-city contracts such as intelligent transport systems that dynamically prioritize buses and cyclists. Aarhus and Odense together account for roughly 18.23% of service revenue, fueled by university research parks and biotech clusters that consume large uplink bandwidth for real-time data analytics. Rural Jutland, although sparsely populated, receives the same 5G service level because spectrum licenses require 98% population coverage, turning agriculture IoT, soil sensors, and livestock tracking into a viable adjacency for operators.

Coastal corridors stand out for next-generation growth. Offshore wind complexes in the North Sea demand high-resilience private 5G that supports unmanned surface vessels and drone-based blade inspection. Ports in Esbjerg and Copenhagen deploy 5G-enabled automated guided vehicles, generating low-latency traffic that garners premium SLA pricing. Border regions with Sweden and Germany offer incremental roaming and cross-border business contracts, albeit constrained by EU “roam-like-at-home” rules that cap margins.

Competitive Landscape

Following Telia’s April 2024 divestiture to Norlys, Denmark’s mobile market features three infrastructure-owning players. Nuuday leads with 6 million customer relationships and DKK 14.5 billion annual revenue, leveraging converged fixed-plus-mobile bundles and exclusive content rights to football and cycling. Telenor ranks second; its Nordic scale allows bulk gear procurement and early adoption of open-RAN pilots that could trim future vendor lock-in costs. Norlys carries momentum from its Telia assets, integrating them via RADCOM’s AI-based monitoring to optimize KPIs across 4G and 5G layers.

All three engage in extensive RAN-sharing: Telia-Telenor’s TT-Network covers 4G and expands to 5G; Nuuday deep-shares passive infrastructure with third-party towercos, accelerating rural densification. Capital-expenditure synergies help offset the 15-20% annual jump in grid-electricity costs tied to renewable-energy surcharges. Strategies now pivot toward service innovation: Nuuday trials 5G edge compute for cloud gaming, Telenor offers managed SD-WAN for SMEs, and Norlys bundles green-energy retail with mobile subscriptions to cross-sell its utility customer base. MVNOs, Hi3G’s Oister, Coop Mobil, and Lebara, continue to siphon price-sensitive users, yet limited to-scale marketing budgets restrict their incursion into enterprise or premium 5G tiers.

White-space revenue streams center on private 5G and network-as-a-service models, especially for wind-energy operators seeking OPEX-based connectivity. Early movers aim to lock in anchor tenants before EU-wide open-spectrum rules mature. Over the forecast period, operators that best align their core networks with edge-cloud and AI orchestration stand to command higher per-bit margins than those relying solely on retail price wars.

Denmark Telecom MNO Industry Leaders

Nuuday

Telenor Denmark

Norlys (Telia Denmark)

3 Denmark (Hi3G)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Macquarie Asset Management announced plans to acquire the remaining 50% of TDC Group, aiming for full ownership before year-end 2025.

- February 2025: Telenor Denmark introduced its TrueTalk B2B product, integrating voice, mobile PBX, and UC features on 5G for SME and large-enterprise clients.

- January 2025: RADCOM Ltd. secured a multi-year contract with Norlys to deploy the RADCOM ACE analytics suite for real-time 5G and 4G monitoring across Denmark, improving customer-experience KPIs.

- June 2024: Ericsson, 3 Denmark, TV 2, and Sony demonstrated cable-free live sports broadcasting over a 5G standalone mm Wave link at Copenhagen’s Parken Stadium, cutting production costs by up to 90%.

- April 2024: Telia Company finalized the USD 900 million sale of its Danish operation to Norlys, exiting the country to focus on its core Nordic and Baltic footprints.

Denmark Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means. The Danish telecom MNO market includes an in-depth trend analysis based on connectivity, such as fixed networks, mobile networks, and telecom towers. Telecom services are segmented into voice services (wired and wireless), data and messaging services, and OTT and PayTV services. Several factors, including the increasing demand for 5G, will likely drive the adoption of telecom services in Denmark.

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International, Enterprise and Wholesale, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International, Enterprise and Wholesale, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Denmark telecom MNO market in 2026?

The market is valued at USD 4.32 billion in 2026, on track to reach USD 5.31 billion by 2031.

What is the forecast CAGR for Denmark’s mobile network operators?

Aggregate revenue is projected to rise at a 4.23% CAGR over 2026-2031.

Which service category leads revenue generation?

Data and internet services contribute 52.87% of total revenue, making them the largest segment.

Why are enterprise services growing faster than consumer services?

Danish companies need reliable IoT and private-5G connectivity to meet carbon-neutrality and automation goals, driving a 4.67% CAGR for enterprise revenue.

How extensive is 5G coverage in Denmark?

5G already reaches 83.9% of the population, providing one of the widest coverages in Europe.

What competitive impact did Telia’s exit have?

Telia’s divestiture created a three-player market, intensifying infrastructure sharing but also heightening service-quality differentiation.

Page last updated on: