Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Brazil Telecom MNO Market is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, Iot and M2M Services, OTT and PayTV Services, and More), and End User (Enterprises, and Consumer). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

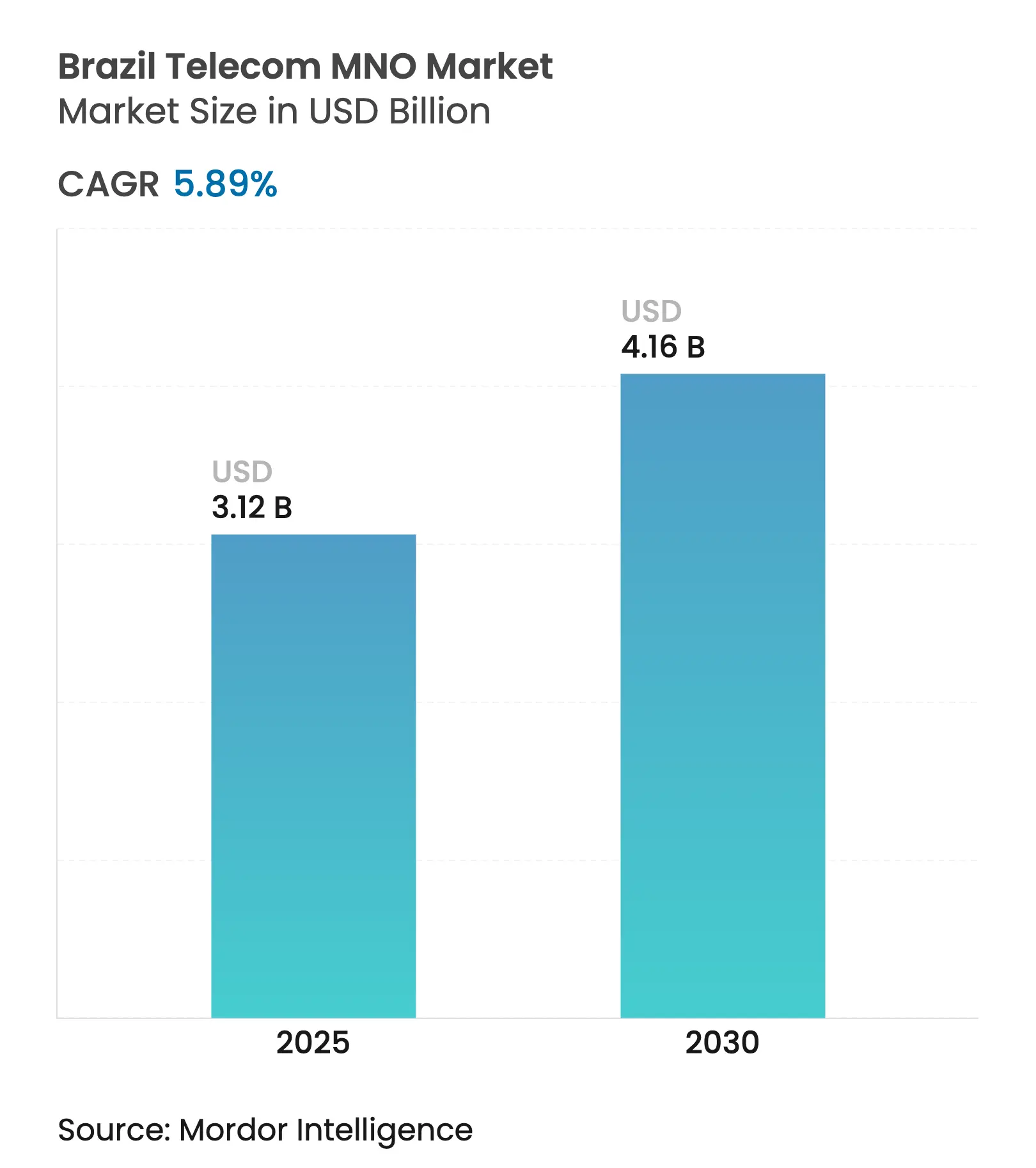

| Market Size (2025) | USD 3.12 Billion |

| Market Size (2030) | USD 4.16 Billion |

| Growth Rate (2025 - 2030) | 5.89 % CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Brazil Telecom MNO Market size is estimated at USD 3.12 billion in 2025, and is expected to reach USD 4.16 billion by 2030, at a CAGR of 5.89% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 250.31 million subscribers in 2025 to 321.68 million subscribers by 2030, at a CAGR of less than 5.15% during the forecast period (2025-2030). Robust 5G rollouts, neutral-host fiber investments, and enterprise digitization are mitigating the sector's exposure to Brazil’s high tax environment while supporting sustainable revenue growth. Consolidation after the Oi mobile asset divestment has reduced price warfare and redirected cash toward network densification and spectrum refarming. Demand for low-latency use cases in agritech and logistics is driving the adoption of premium ARPU tiers, and ANATEL’s infrastructure-sharing rules are further lowering barriers for regional ISPs. At the same time, operators are intensifying focus on AI-enabled customer care and energy-efficient RAN upgrades as utility inflation squeezes operating costs.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

5G footprint expansion accelerating premium ARPU tiers 5G footprint expansion accelerating premium ARPU tiers | +1.2% | National, early gains in São Paulo, Rio de Janeiro, Brasília | Medium term (2-4 years) | (~) % Impact on CAGR Forecast :+1.2% | Geographic Relevance :National, early gains in São Paulo, Rio de Janeiro, Brasília | Impact Timeline :Medium term (2-4 years) |

Nationwide FTTH rollout to underserved municipalities Nationwide FTTH rollout to underserved municipalities | +0.9% | Interior Northeast and North | Long term (≥ 4 years) | |||

Enterprise-grade IoT demand for logistics and agritech Enterprise-grade IoT demand for logistics and agritech | +0.8% | São Paulo industrial belt; Mato Grosso farms | Medium term (2-4 years) | |||

Tax incentives for local Open-RAN manufacturing Tax incentives for local Open-RAN manufacturing | +0.4% | Zona Franca de Manaus | Long term (≥ 4 years) | |||

Rural satellite back-haul driving wholesale bandwidth demand Rural satellite back-haul driving wholesale bandwidth demand | +0.3% | Amazon region | Medium term (2-4 years) | |||

eSIM-based nano-MVNO micro-plans for the gig economy eSIM-based nano-MVNO micro-plans for the gig economy | +0.2% | Major metropolitan areas | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

5G footprint expansion accelerating premium ARPU tiers

Stand-alone 5G now covers nearly 30% of Brazil’s population across more than 1,300 municipalities, with TIM expected to reach 64% population coverage by May 2025. Superior speeds and ultra-low latency are helping carriers upsell post-paid bundles that lifted TIM’s mobile ARPU 5% year over year in Q1 2025. Private 5G licenses granted to 35 enterprises enable the creation of tailored campus networks for ports, mines, and factories, opening up incremental revenue streams without relying on subscriber growth. Vendor partnerships, such as TIM’s radio-access deal with Nokia, underscore confidence in Brazil’s long-term data monetization outlook.[1]Capacity Media Newsroom, “Nokia and TIM expand 5G across Brazil,” capacitymedia.com

Nationwide FTTH rollout to underserved municipalities

Roughly 20,000 ISPs are registered with ANATEL, and they captured 64% of the 2024 broadband investment, pushing fiber into mid-sized interior cities that the majors previously overlooked. Neutral-host wholesaler V.tal bought Oi’s fiber operation for BRL 5.6 billion (USD 1.03 billion) and now leases capacity to smaller providers, accelerating time-to-market and lowering build costs. Combined, these moves have increased FTTH household penetration to 49%, narrowing Brazil’s urban-rural digital divide and driving data-intensive OTT consumption.[2]BNamericas Analyst Team, “How Brazil’s ISPs lead the broadband revolution,” bnamericas.com

Enterprise-grade IoT demand for logistics And agritech

Agribusiness accounts for 20% of GDP and is increasingly utilizing sensors for soil analytics, drone spraying, and cold-chain tracking. TIM’s dedicated IoT unit secured contracts worth more than BRL 300 million within 18 months and now connects 16 million hectares of farmland, four times its 2022 footprint. Freight forwarders in São Paulo are adopting telematics to reduce idle time, while beer maker Ambev has rolled out a private LTE network to digitize its brewery floors. Lower M2M taxes and the introduction of new spectrum for narrowband-IoT have kept connectivity costs under BRL 1 per device per month, reinforcing demand elasticity.

Tax incentives for local Open-RAN manufacturing

Brazil grants fiscal credits under the Manaus Free-Trade Zone to telecom vendors assembling radios and software there, thereby lowering the total cost of ownership compared to traditional single-vendor stacks. Open-RAN pilots conducted by Vivo and Claro demonstrated up to 30% capex savings in sparsely populated areas, and the government has signaled plans to prioritize open interfaces in future spectrum auctions. This policy mix diversifies the supply chain, encourages domestic research and development (R&D), and enhances long-term export prospects for Brazilian 5G components.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

40%+ sector tax burden inflating end-user prices 40%+ sector tax burden inflating end-user prices | -1.1% | Nationwide, heavier in low-income states | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast :-1.1% | Geographic Relevance :Nationwide, heavier in low-income states | Impact Timeline :Long term (≥ 4 years) |

Cord-cutting eroding traditional Pay-TV revenues Cord-cutting eroding traditional Pay-TV revenues | -0.7% | Major urban centers | Medium term (2-4 years) | |||

Energy price volatility squeezing ISP OPEX Energy price volatility squeezing ISP OPEX | -0.4% | National, small ISPs | Short term (≤ 2 years) | |||

Shortage of skilled fiber-optic technicians Shortage of skilled fiber-optic technicians | -0.3% | Northeast interior | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

40%+ sector tax burden inflating end-user prices

Telecom services incur combined federal and state levies exceeding 40% of gross revenue, prompting ANATEL to authorize fixed-line tariff hikes of up to 14% in 2024. Roughly 30% of offline households cite price as the chief barrier to subscription. Compliance complexity also diverts operator resources from capex to administration, curtailing rural rollout velocity.[3]Convergência Digital Newsdesk, “ANATEL authorizes up to 14% fixed-line hikes,” convergenciadigital.com.br

Cord-cutting eroding traditional Pay-TV revenues

Pay-TV subscriptions fell 16.7% in 2023 to 11.7 million as streaming platforms gained traction. Sky Brasil is shifting capital toward broadband, while Netflix, Disney+, and peers formed the Strima lobby to shape over-the-top regulation. As high-margin TV bundles disintegrate, operators face softer blended ARPU, intensifying pressure to monetize connectivity through value-added cloud and security services.

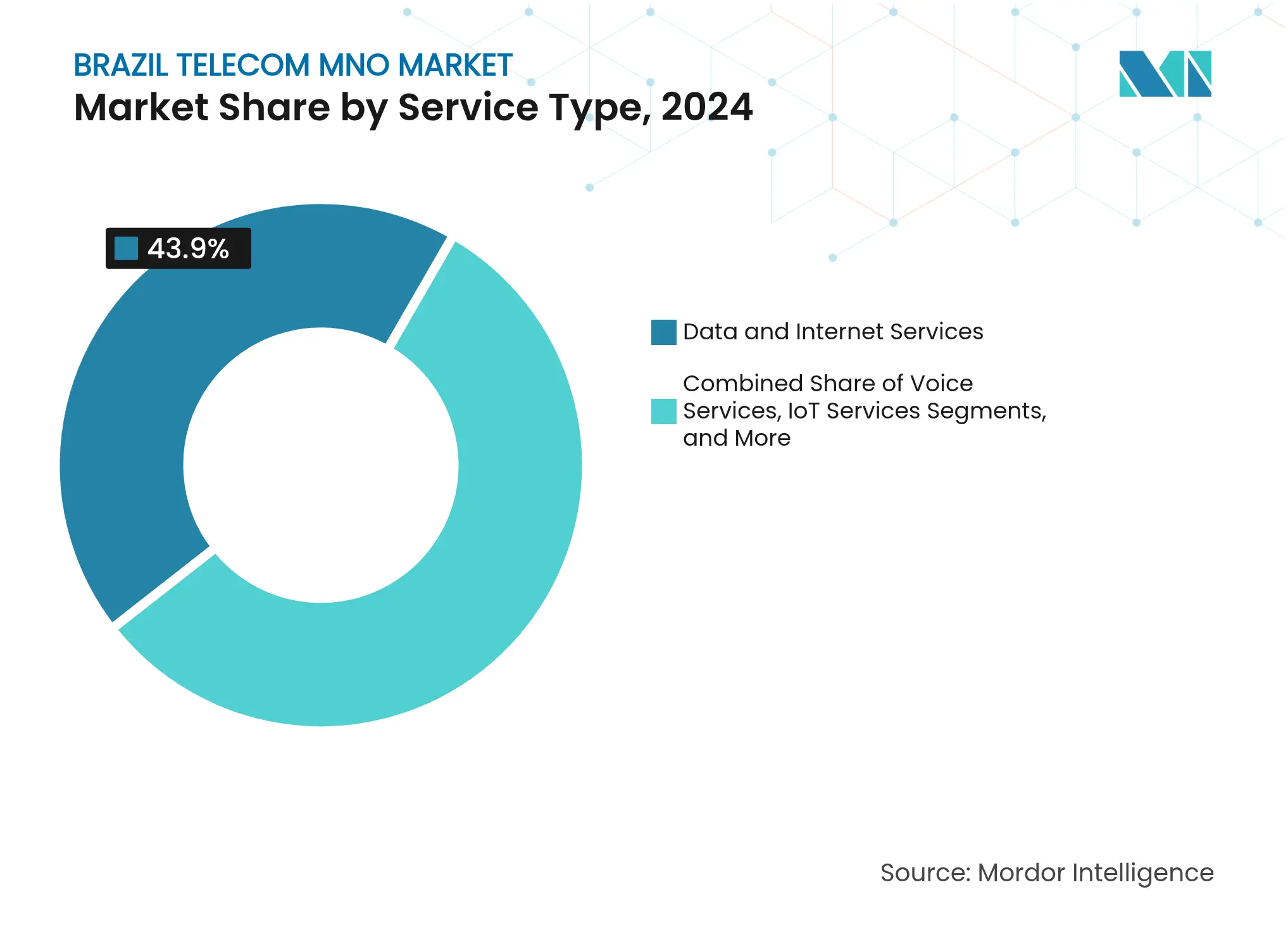

By Service Type: Data Dominance Drives Infrastructure Investment

Data and Internet Services represented 43.90% of Brazil's telecom market share in 2024, translating to USD 1.31 billion in revenue and expanding at a 5.92% CAGR to 2030, underpinned by surging video streaming and cloud workloads. IoT and M2M, at 5.60%, remain small yet the fastest-growing segment, reflecting the use of sensors in agriculture and smart-city lighting. Voice lingers with a 17.99% share but trails in growth. The Brazil telecom MNO market size attributed to OTT and Pay-TV hit USD 0.42 billion in 2024, but the segment’s migration to streaming is reshaping monetization models. Operators continue bundling content with fixed broadband to slow churn, leveraging recently installed FTTH backbones.

Another trend noticed is independent ISPs plowing more than 60% of annual broadband capex, forcing incumbents to embrace wholesale fiber. VoIP traffic is cannibalizing long-distance fixed calls, and 5G is opening premium standalone slices for latency-sensitive enterprise apps. The Brazil telecom MNO industry, therefore, sees incremental revenue migrating from raw bandwidth to managed edge and cybersecurity services.

Note: Segment shares of all individual segments available upon report purchase

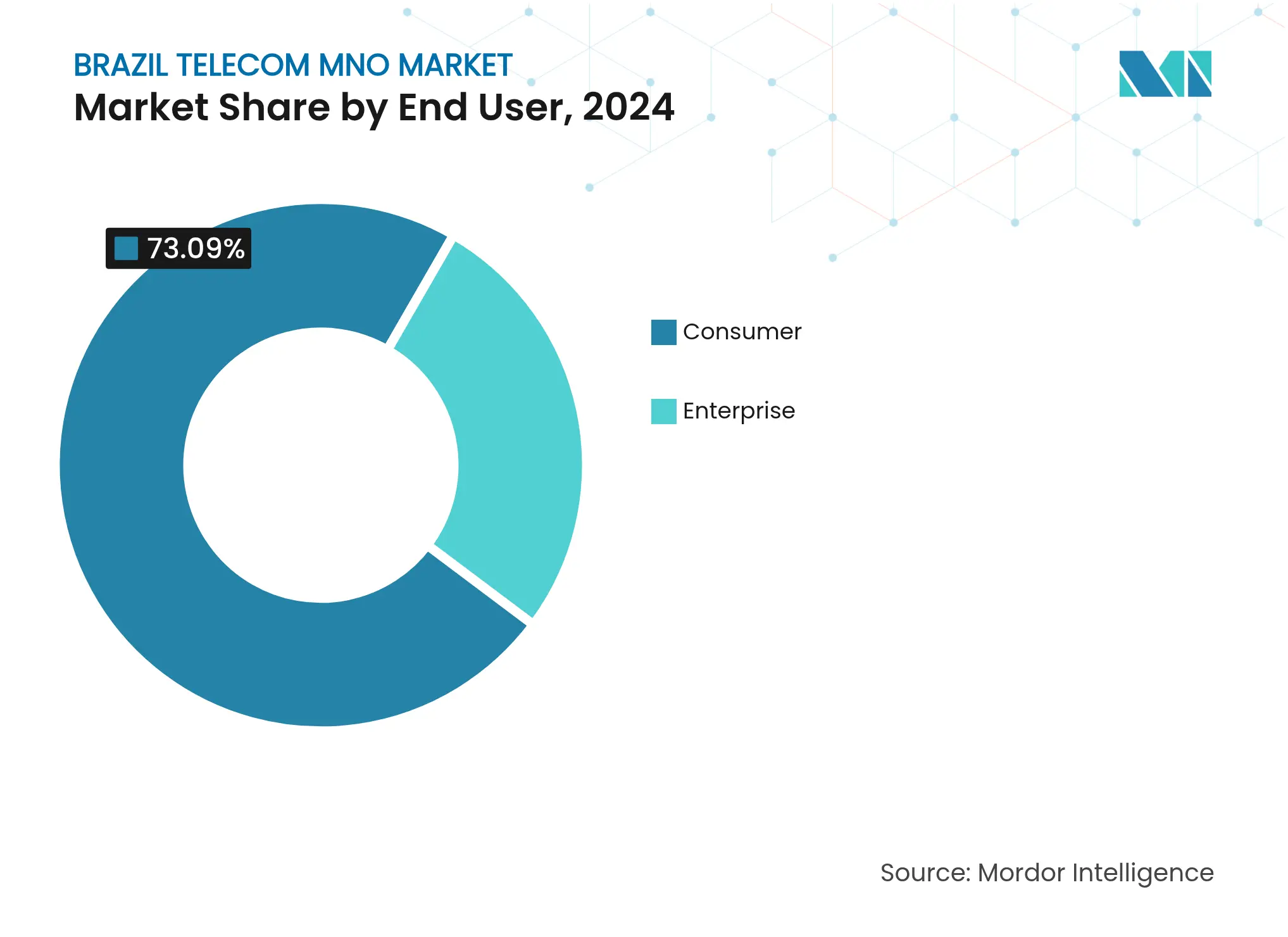

By End-User: Enterprise Acceleration Amid Consumer Maturation

Consumer services still dominate the Brazil telecom MNO market at 73.09% share but are decelerating to a 5.75% CAGR as prepaid usage declines. Enterprise lines, which contribute 26.91%, are slated for a 6.28% CAGR, driven by IoT, private 5G, and cloud-managed WAN. High inflation and interest rates suppress discretionary consumer spending, nudging carriers toward value-based pricing. Conversely, large corporates are outsourcing network operations and demanding service-level guarantees, boosting high-margin B2B revenue.

Private LTE deployments by manufacturers such as Ambev underline enterprises’ readiness to invest directly in coverage gaps. ANATEL’s 3.7 GHz carve-out for campus networks supports this pivot, enabling carriers to resell design, integration, and lifecycle management rather than mere data packages. Consequently, the Brazil telecom MNO market size attached to enterprise-managed services is expected to exceed USD 1 billion by 2030.

Revenue remains concentrated in the Southeast and South corridors, with São Paulo alone contributing roughly 25% of the national telecom turnover, driven by its large enterprise base and affluent consumer segments. Nevertheless, the Northeast and North are logging the fastest growth as wholesale fiber, neutral towers, and satellite backhaul bridge historic coverage gaps. Brisanet’s 28.3% regional share proves that proximity and localized support can outflank nationwide incumbents, particularly in second-tier towns.

Mato Grosso’s IoT-ready farms highlight the interior’s potential; TIM already blankets 16 million hectares there with NB-IoT. The Amazon region, which has long relied on high-cost microwave hops, is pivoting to LEO constellations following ANATEL’s green light for SpaceX and the Chinese newcomer SpaceSail. Infrastructure-sharing mandates enable smaller operators to utilize major operator duct and pole networks, reducing entry costs by an estimated 20%. Federal connectivity programs are funneling subsidies to municipalities with populations under 30,000, accelerating the reach of FTTH. Consequently, regional revenue disparities should narrow gradually, thereby supporting national digital inclusion goals.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Market Concentration

Telefônica Brasil (Vivo), América Móvil’s Claro, and TIM Brasil controlled more than 95% of mobile subscribers after splitting Oi’s assets in 2022, generating a high-concentration market that now prioritizes ARPU and technology leadership. Claro is earmarking USD 7.7 billion for fiber and 5G until 2029. Vivo is using Microsoft’s generative AI to slash care costs, and TIM lifted normalized Q2 2025 earnings by 25% due to disciplined pricing. Open-access wholesalers such as V.tal and FiBrasil are reshaping fixed-broadband economics by leasing dark fiber to ISPs and hyperscalers.

Brisanet leverages its early FTTH roots in the Northeast, and Brasil Tecpar reached 832,000 subscribers after acquiring GGNET in August 2024. Meanwhile, equipment vendors are expanding their local footprints; Nokia’s massive MIMO rollout with TIM covers 15 states, and Ericsson is piloting Open-RAN testbeds with Vivo. Ancillary revenue pools are forming in fintech-Claro Pay secured Central Bank approval in February 2025-and in content aggregation as carriers bundle streaming credits into post-paid plans. As a result, competition is shifting from raw connectivity toward platform ecosystems.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. Market Landscape

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.