Romania Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

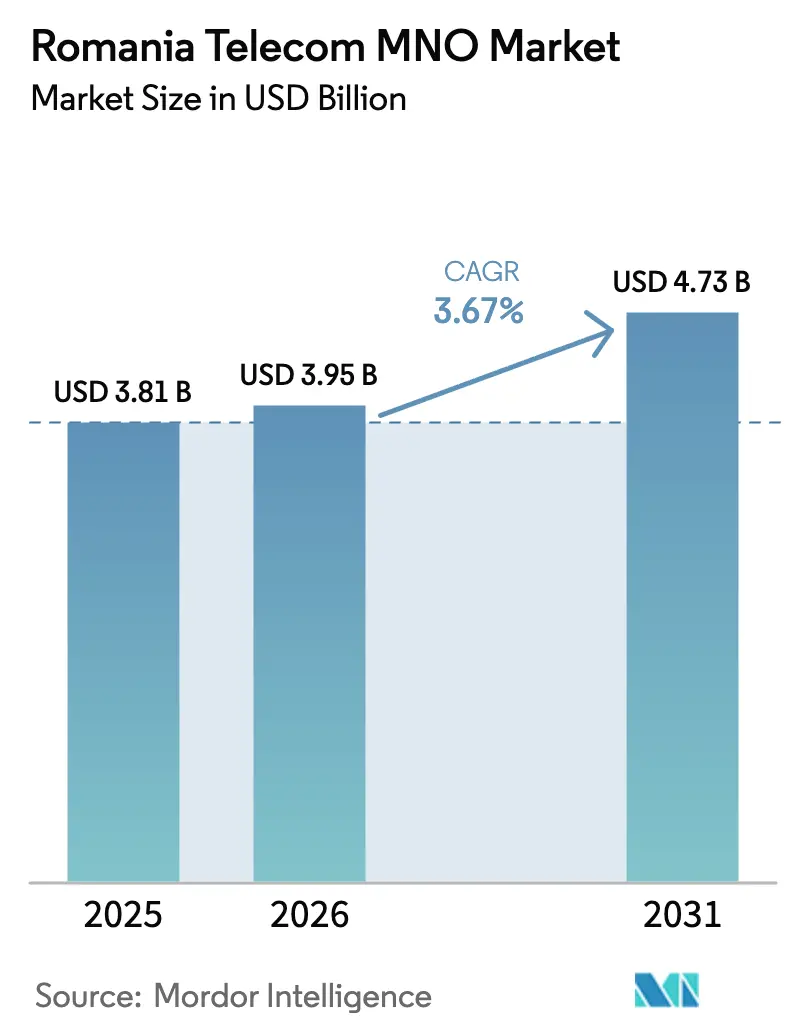

| Base Year Market Size (2025) | USD 3.81 Billion |

| Market Size (2026) | USD 3.95 Billion |

| Market Size (2031) | USD 4.73 Billion |

| Growth Rate (2026 - 2031) | 3.67% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Romania Telecom MNO Market Analysis by Mordor Intelligence

Romania Telecom MNO Market size in 2026 is estimated at USD 3.95 billion, growing from 2025 value of USD 3.81 billion with 2031 projections showing USD 4.73 billion, growing at 3.67% CAGR over 2026-2031.

This trajectory shows a measured expansion phase in which operators shift from pure subscriber growth to value-creation strategies that revolve around nationwide 5G deployment, enterprise digitalization, and fixed-mobile convergence. The country’s 96.5% fiber-to-home penetration, Europe’s highest, gives carriers an unparalleled platform for gigabit backhaul, seamless service bundling, and average-revenue-per-user improvement. Extremely low tariffs, USD 6.58 PPP for unlimited 4G and USD 8.29 PPP for 5G, have compressed margins but encouraged data-usage elasticity that widened total mobile traffic and facilitated a three-fold jump in 5G connections to 2.5 million in 2023. Competitive dynamics intensified in 2024 and 2025 after Orange finalized its fixed-mobile merger and Digi Communications moved to acquire Telekom Romania Mobile, raising the importance of scale, technology diversification, and differentiated enterprise portfolios. Meanwhile, EU Recovery and Resilience Facility grants worth EUR 29.2 billion are underwriting 5G roll-outs, rural broadband, and digital-government services, creating long-run demand tailwinds even as operators navigate capex pressure from mandatory Huawei equipment replacement.

Key Report Takeaways

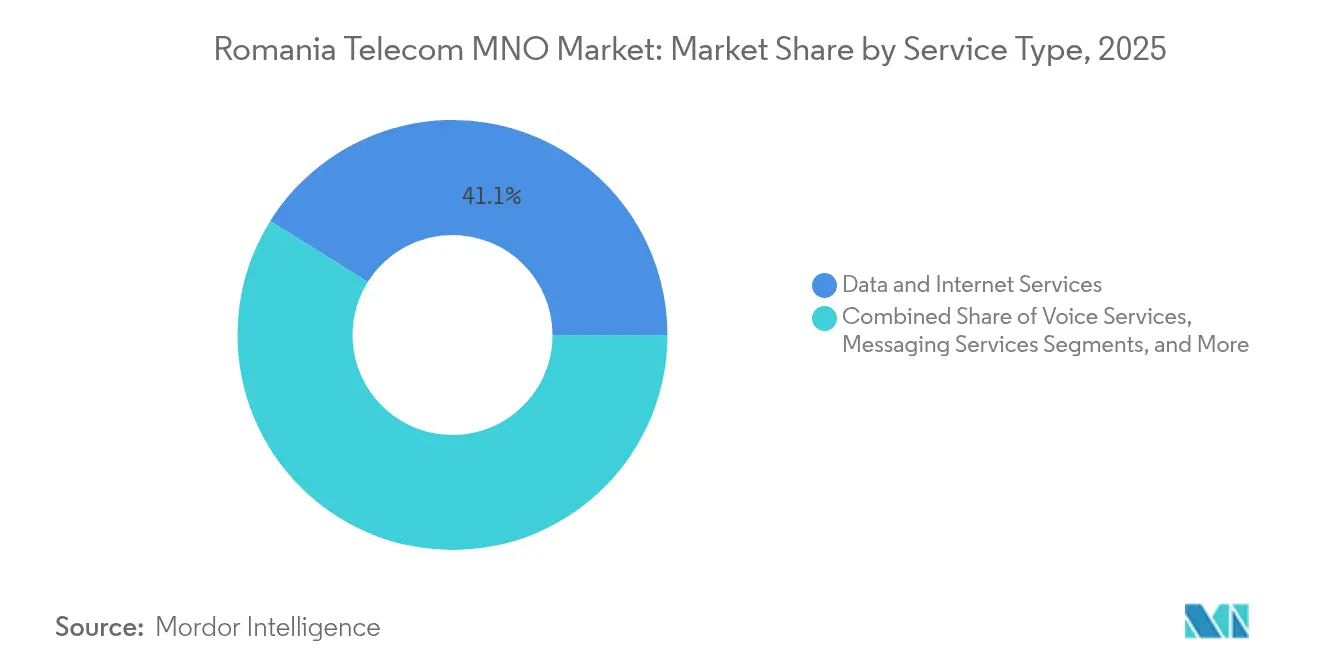

- By service type, Data and Internet services led with 41.10% of Romania telecom MNO market share in 2025, while IoT and M2M services are poised to expand at a 4.10% CAGR through 2031.

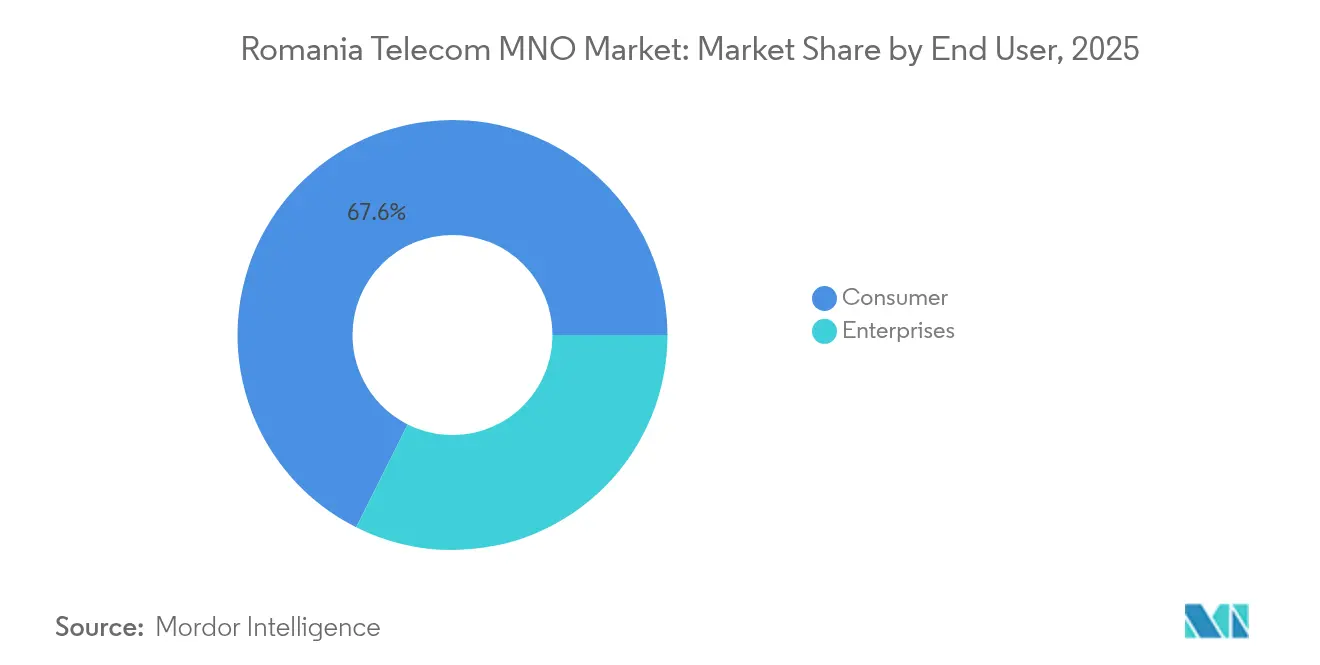

- By end user, the Consumer segment accounted for 67.60% share of the Romania telecom MNO market size in 2025, whereas the Enterprise segment is projected to advance at a 4.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Romania Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G roll-out supported by EU Recovery funds | +0.8% | National, with priority in Bucharest, Cluj-Napoca, Timișoara | Medium term (2-4 years) |

| Fixed–mobile convergence driving ARPU uplift | +0.6% | National, concentrated in urban areas | Long term (≥ 4 years) |

| Fiber backbone densification by municipal dark-fiber initiatives | +0.4% | National, with focus on Tier-1 cities | Medium term (2-4 years) |

| Cloud/edge demand from near-shoring IT services sector | +0.5% | National, with concentration in Bucharest and major cities | Long term (≥ 4 years) |

| EU-mandated elimination of roaming surcharges | +0.3% | National with EU-wide impact | Short term (≤ 2 years) |

| Sub-EUR 0.50/GB data pricing stimulating usage elasticity | +0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid 5G roll-out supported by EU Recovery funds

Romania secured EUR 5.97 billion for digital and telecom projects under the National Recovery and Resilience Plan, a package that raises the ceiling for nationwide 5G availability by underwriting spectrum fees, radio-access equipment, and transport-layer modernization [1]European Commission, “National Recovery and Resilience Plan—Romania,” europa.eu. Orange already delivers 5G in 50 cities with download speeds near 260 Mbps after channeling USD 288 million into 3.4–3.8 GHz licenses and RAN upgrades, while Vodafone has partnered with Ericsson and Samsung to accelerate Open-RAN roll-outs aimed at faster rural coverage. The government’s target to blanket transport corridors and all urban areas by 2025 compresses network-build timelines but positions the Romania telecom MNO market as a 5G frontrunner in Central and Eastern Europe. As spectrum utilization rises, operators gain capacity for low-latency enterprise use cases that expand high-margin service revenue, offsetting the short-term strain on free cash flow.

Fixed-mobile convergence driving ARPU uplift

Orange’s integrated entity and Digi’s fiber-centric model illustrate how convergence converts ultra-fast fiber backbones into bundled cloud, content, and mobility propositions that reduce churn and lift unit economics. Bundled households typically generate 15-25% greater lifetime value than single-play customers, according to internal operator benchmarks shared with regulators, because subscribers consolidate spending on broadband, mobile voice, pay-TV, and IoT add-ons under one invoice. Romania’s unique nationwide GPON footprint simplifies convergent roll-outs by eliminating last-mile bottlenecks that delay similar strategies in neighboring markets. The tactic also shields operators from price-only competition by shifting purchasing criteria from tariff to service breadth, although success depends on marketing execution and the ability to migrate legacy prepaid customers to contract bundles.

Fiber backbone densification via municipal dark-fiber initiatives

Local authorities are underwriting passive-infrastructure projects that target 945 villages for gigabit connectivity by December 2025, enabling carriers to lease dark fibre instead of financing their backhaul in sparsely populated zones [2]Ministry of Research, Innovation and Digitalization, “Guide for Municipal Dark Fibre Projects,” mcid.gov.ro . Because 91% of Romania’s 6.5 million fixed-broadband lines already qualify as ultra-fast, dark-fibre builds now focus on industrial parks, suburban clusters, and regional logistics corridors where edge-compute nodes will reside. Shared passive assets shrink capex per kilometer and improve investment returns that duplicative metro loops in Bucharest, Cluj-Napoca, and Timișoara have squeezed. The model mirrors successful wholesale fiber plays in Sweden and Portugal, accelerating time-to-revenue while letting municipalities earn utility-style annuities from telecom leases.

Cloud/edge demand from near-shoring IT sector

Romania’s IT services industry grows around 8% annually, generated EUR 3.2 billion in software exports during 2023, and now employs nearly 192,000 developers who cluster around Bucharest, Cluj, Iași, and Timișoara. Multinationals shifting workstreams from Western Europe prioritize low-latency links to regional data centers, on-prem edge appliances, and secure multicloud gateways. Telcos are therefore packaging connectivity with SD-WAN, private 5G, and managed security services that command double-digit EBITDA margins versus sub-30% margins in retail prepaid. Google’s memorandum of understanding with the Romanian government to co-develop digital infrastructure signals that global Hyperscalers will anchor additional availability zones, multiplying wholesale backhaul and peering revenue for carriers willing to evolve from voice-and-data utilities into edge-cloud facilitators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Huawei rip-and-replace CAPEX overhang | -0.7% | Nationwide | Medium term (2-4 years) |

| Labor-skill exodus of RF engineers | -0.4% | Major urban centers | Long term (≥4 years) |

| Persistent prepaid dominance | -0.3% | National | Long term (≥4 years) |

| Fiber overbuild in Tier-1 cities | -0.2% | Bucharest, Cluj-Napoca, Timișoara | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Huawei rip-and-replace CAPEX overhang

Security legislation enacted in 2021 obliges operators to remove Huawei hardware from core networks by 2026 and from RAN layers by 2028, forcing Orange and Vodafone to allocate unbudgeted capex and professional-services fees that divert funds away from revenue-bearing product innovation [3]Light Reading Editorial Team, “Vodafone, Orange Face 5G Rip-and-Replace as Romania Bans Huawei,” lightreading.com. Swapping equipment without service disruption entails parallel networks, spectrum re-farming, and extensive field-engineer scheduling that inflate the cost per site. The drag on free cash flow is particularly acute because the transition overlaps with accelerated 5G expansion schedules tied to EU grants. While operators with lower Huawei exposure, such as Digi, face fewer direct costs, the industry collectively shoulders the delayed monetization of advanced features like network slicing until replacement cycles conclude.

Labor-skill exodus of RF engineers

Romanian RF engineers capture premium wages in Germany, France, and the Nordics, leaving domestic operators short-staffed during the most complex era of Open-RAN, standalone 5G core, and edge-cloud integration. To maintain roll-out velocity, carriers now outsource optimization and integration functions to equipment suppliers’ managed-service arms, lifting opex and curbing in-house innovation. The shortage also undermines service-quality differentiation because benchmarking reports increasingly favor operators that can tune cell-level parameters weekly rather than quarterly. Unless wage structures or on-the-job upskilling programs narrow the compensation gap with Western Europe, Romania telecom MNO market operators risk a structural talent deficit that erodes long-term competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data-centric consumption reshapes the portfolio

Romania telecom MNO market size for Data and Internet services translates into a 41.10% Romania telecom MNO market share on the back of traffic elasticity enabled by sub-EUR 0.50 per gigabyte tariffs. IoT and M2M contributed just 4.6% of revenue but will post the fastest 4.10% CAGR to 2031 as smart-city pilots in Cluj-Napoca and industrial-automation projects in Ploiești demand low-latency SIMs. Voice and messaging continue a secular slide yet retain relevance for enterprise PBX interconnect and rural households that lack substitute fixed lines. OTT and Pay-TV services, bolstered by Vodafone’s Disney+ exclusivity and Orange’s Orange TV Go upgrades, enrich ARPU through content aggregation, though packaging success depends on copyright economics and device bundling.

Operator tactics now favor spectrum-efficiency and edge-cache placement to contain per-gigabyte cost, given that daily mobile data usage per subscriber surpassed 9 GB in Q1 2025, three times the EU-27 average, while end-user pricing remains the continent’s lowest. Orange’s 3G shutdown, already covering seven regions, releases 900 MHz and 2100 MHz capacity that migrates to LTE and 5G, reducing energy draw by 11% and elevating rural throughput. Meanwhile, enterprise IoT penetration stands at 10%, far below the 29% European average, leaving a sizable addressable market for NB-IoT, LTE-M, and private 5G solutions once ecosystem fragmentation around device certification and systems integration eases.

By End User: Enterprise momentum builds on digital-transformation mandates

Consumer accounts delivered 67.60% of the Romania telecom MNO market size in 2025. The enterprise segment is predicted to rise at a 4.05% CAGR, underwritten by cloud migration, remote-work enablement, and cyber-resilience spending in banking, automotive, and shared-services centers. Telcos are bundling SD-WAN, managed firewall, and Microsoft 365 tiers with 5G connectivity to capture this value, mirroring Vodafone’s 5.3% year-on-year Romanian business-service revenue growth recorded in Q3 2025.

New large-enterprise contracts increasingly stipulate service-level guarantees below 20 milliseconds round-trip latency, prompting carriers to co-locate mobile-edge computing nodes inside Hyperscalers' data centers in Bucharest. For micro-enterprises, off-the-shelf converged packages combine POS gateways, cloud storage, and unlimited 5G data starting at USD 23 per month, up from USD 14 in 2022, illustrating the shift from price-per-gigabyte to service-quality monetization. Continued public-sector digital-agenda funding, EUR 4.1 billion earmarked for e-government and cybersecurity, acts as a volume anchor for advanced connectivity orders. However, operators must overcome procurement complexities and extended sales cycles typical in government verticals to unlock full contract values.

Geography Analysis

Regional performance highlights Romania telecom MNO market size concentration in Bucharest, which generates 63% of national ICT revenue and hosts the densest 5G macro-cell grid . The capital’s median 5G download speed reached 270 Mbps in H1 2025, underpinning early enterprise-edge pilots in media production and telemedicine. Cluj-Napoca and Timișoara form the second-tier cluster where Digi, Orange, and Vodafone focus small-cell and mmWave trials that supply campus-network pilots in automotive R&D facilities.

In rural regions, government-funded dark-fiber corridors and 700 MHz spectrum allocations aim to lift 5G population coverage from 70% in 2025 to 98% by 2027, fulfilling EU Digital Decade targets. Carriers now weigh the economic merits of macro-cell sharing and Open-RAN architecture to meet obligations without inflating cost per covered citizen. Northern counties such as Suceava still lag in average LTE throughput at 22 Mbps, so Orange’s decision to decommission 3G must synchronize with LTE 900 refarming to avoid service gaps. Ookla speed-test datasets place Oradea top for mobile latency at 23 milliseconds, illustrating pockets of excellence that carriers advertise in regional B2B pitches.

EU milestone tracking shows Romania met 39 of 43 connectivity deliverables by Q4 2024, unlocking a second EUR 2.8 billion disbursement that subsidizes rural tower builds and transport-corridor 5G. The inflow mitigates capex risk and motivates further consolidation as smaller tower-co projects and MVNOs seek partnership with larger network owners to handle compliance audits and reporting requirements. Nevertheless, fiber overbuild in Bucharest, Cluj-Napoca, and Timișoara exerts downward pressure on wholesale rates, challenging return on invested capital for operators lacking scale to amortize network costs over diverse revenue streams.

Competitive Landscape

The Romania telecom MNO market features four nationwide operators in a consolidation cycle that gradually raises market concentration without eliminating competitive intensity. Orange Romania became the integrated market leader after merging Orange Romania SA with Orange Romania Communications, inheriting 6.9 million mobile users, 1.2 million broadband lines, and a 20% government stake that stabilizes regulatory relations. Digi Communications, historically a fixed-line powerhouse, now targets a second-place ranking by acquiring Telekom Romania Mobile’s 1.9 million subscribers; the deal pushes Digi’s combined base to 6.4 million and boosts spectrum holdings in the 1800 MHz and 2100 MHz bands. Vodafone Romania retains a differentiated stance through early adoption of Open-RAN, winning regulatory praise for vendor diversification amid Huawei exit rules; its Disney+ partnership further nurtures family-bundle stickiness.

Technology roadmaps emphasize Open-RAN and cloud-native 5G core to keep network cost per bit in check. Orange and Vodafone jointly expanded a shared Open-RAN rural pilot to 230 sites, running Samsung vRAN software atop Wind River Linux and Dell PowerEdge hardware, while Digi signals interest in the same stack as it digests its new subscriber assets. Concurrently, tower-company carve-outs loom as likely next steps: the market’s roughly 24,000 macro sites could be transferred into independent entities to unlock balance-sheet flexibility needed to finance Huawei replacements and new metro-cell deployments.

Romania Telecom MNO Industry Leaders

Orange Romania SA

Vodafone Romania SA

Digi Romania S.A.

Telekom Romania Mobile SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Orange Romania became the first operator with 5G/5G+ in 50 cities after investing EUR 265 million in spectrum and RAN assets.

- March 2025: Digi Romania secured EUR 54.76 million in export-credit loans with four-year maturities to enhance networks in Romania and Portugal, supporting expansion after 13.9% revenue growth to EUR 1.93 billion in 2024.

- February 2025: Regulators imposed strict service-quality conditions as Vodafone and Digi negotiated the Telekom Romania Mobile acquisition that affects 1.9 million users.

- May 2024: Orange finalized the merger of its fixed and mobile entities following governmental approval, creating a fully converged operator from June 2024.

- May 2024: Orange and Vodafone extended their shared Open-RAN 4G network pilot with Samsung vRAN software, Wind River infrastructure, and Dell hardware across rural Romania.

- February 2024: Vodafone Romania expanded its commercial Open-RAN network with Samsung, adding sites in 20 cities to boost 2G, 4G, and 5G capacity.

Romania Telecom MNO Market Report Scope

The study provides an in-depth analysis of the telecommunication sector in Romania.

The Romanian telecom MNO market is segmented by services (voice services (wired and wireless), data and messaging services, OTT, and PayTV services). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Romania telecom MNO market in 2026?

It is valued at USD 3.95 billion in 2026 and is forecast to reach USD 4.73 billion by 2031.

What is the expected growth rate of Romania’s mobile-network operators?

The market’s 3.67% CAGR reflects the transition from volume expansion to value-added 5G and enterprise services.

Which service line dominates carrier revenue?

Data and Internet services lead with 41.10% Romania telecom MNO market share in 2025, driven by heavy usage at Europe’s lowest tariffs.

Why are operators focusing on enterprise customers?

Enterprise revenue grows at a 4.05% CAGR to 2031 and offers higher ARPU through bundled connectivity, cloud, and cybersecurity solutions.

How does government funding influence 5G roll-out?

EU Recovery grants worth EUR 5.97 billion finance spectrum and infrastructure, accelerating 5G deployment while easing capex burdens.

What challenge does the Huawei ban create?

Carriers must replace Huawei gear by 2028, imposing an estimated 0.7-percentage-point drag on market CAGR due to extra capex.

Page last updated on: