Brazil Optical Transceiver Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

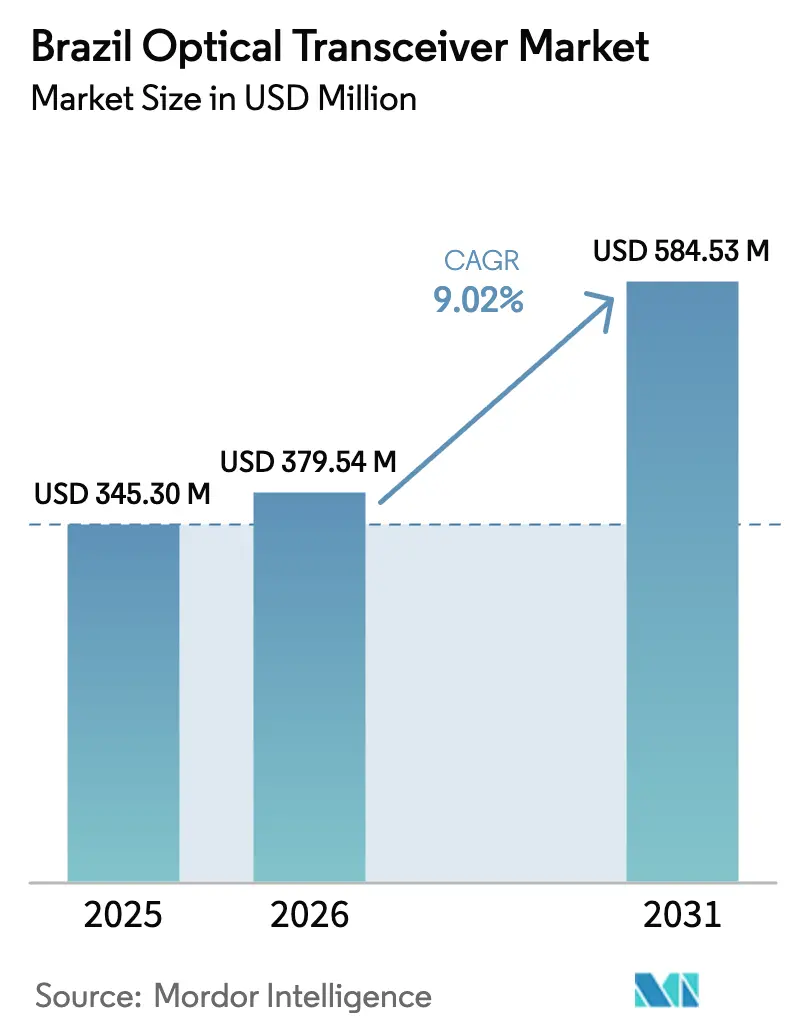

| Base Year Market Size (2025) | USD 345.30 Million |

| Market Size (2026) | USD 379.54 Million |

| Market Size (2031) | USD 584.53 Million |

| Growth Rate (2026 - 2031) | 9.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Optical Transceiver Market Analysis by Mordor Intelligence

The Brazil optical transceiver market size is expected to grow from USD 345.30 billion in 2025 to USD 379.54 billion in 2026 and is forecast to reach USD 584.53 billion by 2031 at 9.02% CAGR over 2026-2031. Heightened hyperscale data-center spending, rapid 5G backhaul densification and federally funded long-haul fiber projects together underpin the sustained expansion of the Brazil optical transceiver market. Operators added 52 million fixed-broadband fiber accesses by December 2024, while 5G coverage widened to 1,504 municipalities by mid-2025, creating steady pull-through for 25G, 100G and 400G modules. Subsea-cable upgrades in Fortaleza are funnelling record international bandwidth into the country, triggering parallel demand for 400G-800G metro optics in São Paulo and Rio de Janeiro. At the same time, Processo Productive Básico tax incentives are encouraging local assembly, partially offsetting import duties that still pressure margins for vendors serving the Brazil optical transceiver market. Supply-chain tightness in photonic-integrated circuits remains a watchpoint but does not derail the long-term growth trajectory.

Key Report Takeaways

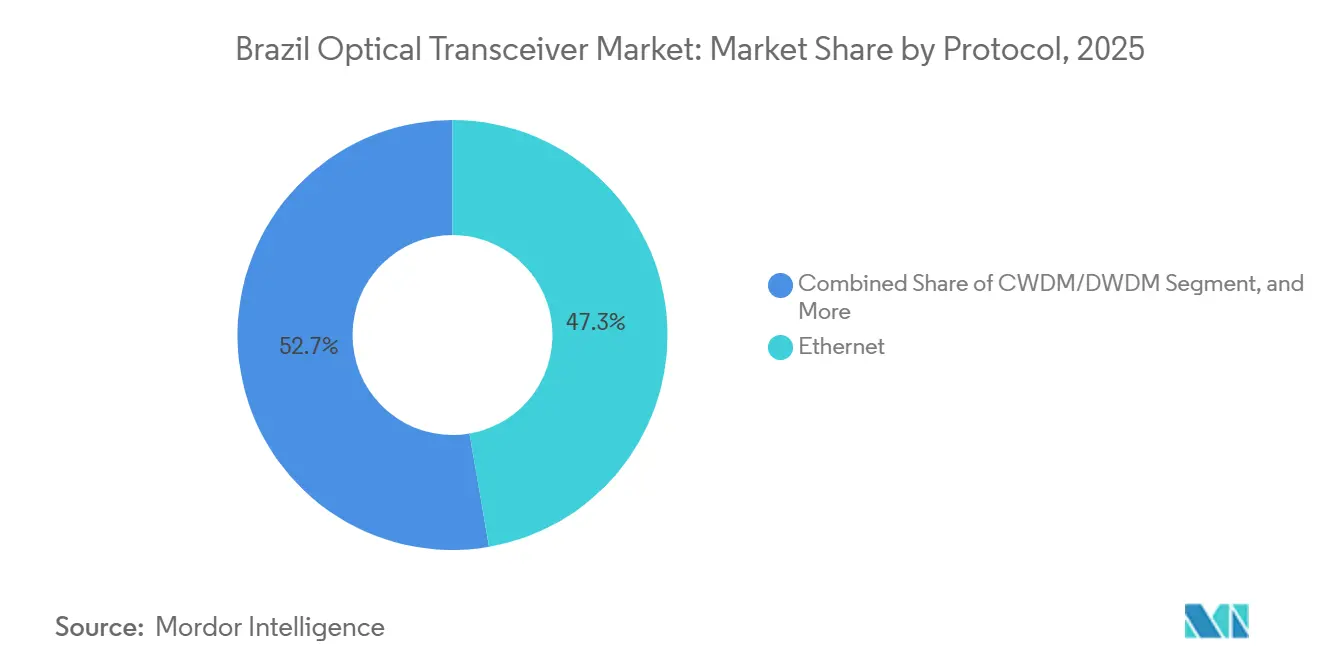

- By protocol, Ethernet led with 47.28% of the Brazil optical transceiver market share in 2025, while CWDM/DWDM is projected to expand at a 9.57% CAGR through 2031.

- By data-rate, the 41-100 Gbps tier accounted for 38.53% of the Brazil optical transceiver market size in 2025 and the More-than-100 Gbps category is forecast to advance at 9.99% CAGR to 2031.

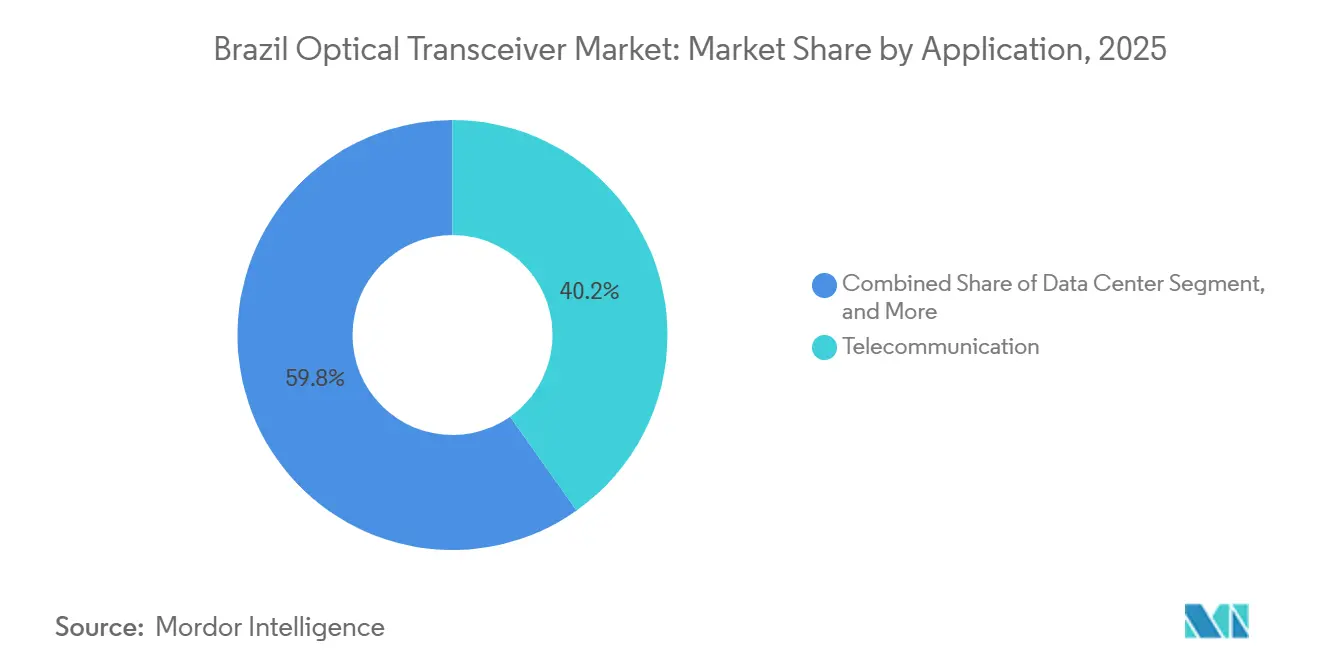

- By application, telecommunication captured 40.21% revenue in 2025; data-center interconnect is poised to grow fastest at 9.78% CAGR through 2031.

- By connector type, QSFP and QSFP-DD held 44.18% of the Brazil optical transceiver market share in 2025, whereas OSFP is set to post the highest 9.83% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Brazil representing one among them. The global report on optical transceiver market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Brazil Optical Transceiver Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Hyperscale and Colocation Data Center Footprint | +2.10% | National, concentrated in São Paulo and Rio de Janeiro | Medium term (2-4 years) |

| 5G Backhaul Densification Across Tier-1 MNOs | +1.80% | National, with early gains in state capitals and interior municipalities | Short term (≤ 2 years) |

| Government Long-Haul Fiber Backbone Initiatives | +1.50% | National, prioritizing North and Northeast regions | Long term (≥ 4 years) |

| Subsea-Cable Landing Hub Expansion in Fortaleza | +1.30% | Fortaleza and coastal Northeast | Medium term (2-4 years) |

| PPB Tax Incentives for Local Optical Assembly | +0.90% | Manaus Free Trade Zone and select manufacturing hubs | Long term (≥ 4 years) |

| Smart-Grid Fiberization by Electric Utilities | +0.70% | National, led by São Paulo, Minas Gerais, and Rio Grande do Sul | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Hyperscale and Colocation Data Center Footprint

AWS committed USD 1.8 billion and Microsoft pledged BRL 14.7 billion (USD 2.7 billion) for new Brazilian cloud regions, redirecting purchasing toward 400G and 800G QSFP-DD and OSFP modules.[1]BNamericas Staff, “LatAm deals help Ciena push optical gear deeper into Americas market,” bnamericas.com São Paulo closed 2025 with 670 MW of live capacity and a 770 MW pipeline that is locking in multi-year optical forecasts. Fortaleza’s Mega Lobster hyperscale campus, slated for 2026 commissioning, is already pre-ordering 800G DR8 transceivers to support spine-to-leaf architectures. Eletronet validated 1.6 Tb/s metro transport using Ciena WaveLogic 6 Extreme, enabling colo providers to collapse external transponders into coherent pluggables.[2]Ciena Corporation, “Eletronet sets new data transmission record in Brazil with Ciena's WaveLogic 6 Extreme,” ciena.com Consequently, vendors owning bonded warehouses near Guarulhos airport gain an execution edge, because hyperscalers dictate just-in-time deliveries with penalties for shortages.

5G Backhaul Densification Across Tier-1 MNOs

Brazil switched on 1,504 5G-served municipalities by June 2025, deploying nearly 30,000 radio sites that each draw 10-25 Gb/s of fiber capacity. Claro, Vivo and TIM redirected BRL 8.5 billion capex in 3Q 2025 toward fiber backhaul, favouring cost-efficient 25G SFP28 CWDM and 50G SFP56 DWDM optics for fronthaul aggregation. Accelink and Hisense capitalized by supplying ANATEL-certified low-power modules undercutting Western peers. Interoperability showcases at FUTURECOM 2024 signalled operator appetite for open optical ecosystems, which reduces single-vendor dependency.[3]GIGALIGHT Marketing, “GIGALIGHT showcases multiple open optical networking product lines at Brazil's FUTURECOM 2024,” gigalight.com The strategic ripple effect is sustained volume for the Brazil optical transceiver market even where purchasing budgets remain tight.

Government Long-Haul Fiber Backbone Initiatives

The Norte Conectado and Nordeste Conectado programs extended 100G-200G DWDM links to 20 interior cities and allocated BRL 654 million for school connectivity by mid-2025. Parallel PAIS submarine routes pushed fiber into Amapá, Pará and Amazonas, seeding last-mile ISP rollouts that consume 10G SFP+ and 25G SFP28 optics. Oi’s regulated-asset migration unlocked BRL 5.8 billion fresh fiber investment aimed at underserved North and Northeast clusters. Vendors adept at Brazil’s public-tender process and PPB local-content thresholds win disproportionate share of these projects. In turn, the Brazil optical transceiver market benefits from predictable multi-year order visibility tied to federal budgets.

Subsea-Cable Landing Hub Expansion in Fortaleza

Fortaleza aggregates 16 submarine systems, and recent upgrades raised the South America Crossing route to 1.2 Tb/s per channel using Ciena WaveLogic 6 Extreme. Polo Mobwire followed with an 800G coherent rollout across four landing stations, requiring matching 400G-800G terrestrial optics to prevent choke points. Google’s Firmina cable and V.tal’s 26,000 km network, backed by USD 630 million DFC funding, reinforce Fortaleza as the nation’s international bandwidth gateway. The hidden effect is a knock-on surge for metro-DCI optics in São Paulo and Rio de Janeiro, because content owners now establish direct private lines to subsea gateways for latency gains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Import Tariffs and Customs Delays | -1.20% | National, affecting all imported optical modules | Short term (≤ 2 years) |

| Photonic-IC Supply Chain Volatility | -0.90% | Global, with acute impact on advanced 400G/800G modules | Medium term (2-4 years) |

| Shortage of Coherent-Optics Engineering Skills | -0.70% | National, concentrated in São Paulo and Rio de Janeiro | Long term (≥ 4 years) |

| Legacy Copper Metro Networks in Secondary Cities | -0.50% | Interior municipalities and Tier 2/3 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Import Tariffs and Customs Delays

CAMEX duties run 12-16% on finished optical modules, while customs clearance can add up to four weeks, complicating just-in-time supply for hyperscalers. PPB incentives in Manaus trim the effective rate to 0-4% but require local assembly lines that smaller Asian suppliers lack. Padtec built a domestic pluggable plant yet still booked a 2024 net loss amid Chinese price competition. Operators hedge by stocking larger safety inventories or contracting bonded-warehouse distributors such as Vivensis, which now resells Nokia optics under a January 2025 accord. The Brazil optical transceiver market therefore incurs working-capital overheads that slightly temper its CAGR.

Photonic-IC Supply Chain Volatility

Indium-phosphide and silicon-photonics wafer shortages stretched 400G-800G lead times to 24-28 weeks during 2025, forcing project delays for new data-center halls. Brazilian operators seldom secure foundry allocations directly and depend on OEM production queues that prioritize North American and European buyers. To mitigate, carriers embrace open optical standards, qualifying multiple transceiver vendors per route segment for redundancy. Demonstrations of interoperable coherent pluggables at FUTURECOM 2024 illustrated this diversification push. Although disruptive, the constraint accelerates vendor diversity inside the Brazil optical transceiver market rather than eroding long-term demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Protocol: Ethernet Ubiquity and Coherent Momentum

Ethernet dominated 47.28% of the Brazil optical transceiver market share in 2025, sustained by 10G-100G module economies across enterprise and cloud fabrics. CWDM/DWDM, however, is forecast to climb at a 9.57% CAGR through 2031 as carriers adopt 400G ZR/ZR+ and 800G ZR coherent pluggables for metro and long-haul routes. Eletronet’s record 1.2 Tb/s single-wavelength trial over 1,500 km without regeneration underscored the spectral-efficiency dividend of modern coherent optics. Ethernet will keep a large installed base but yield incremental share to coherent protocols wherever fiber scarcity or latency targets dominate. Regulatory neutrality from ANATEL allows operators to focus strictly on total-cost-of-ownership metrics when selecting protocol stacks.

Ethernet’s extensive vendor ecosystem reduces price points, benefiting regional ISPs and enterprise campuses. Meanwhile, the Brazil optical transceiver market size linked to CWDM/DWDM will swell as hyperscalers interconnect distributed availability zones over 400G DR4 and coherent metro plugs. Fibre Channel, targeted at SAN refreshes, and FTTx variants tack on moderate gains linked to fiber-to-the-home rollouts by V.tal and Brisanet. Legacy SONET/SDH’s minimal footprint continues to wind down, though some utilities still rely on STM-64 gear pending grid-fiber modernization.

By Data Rate: 100 Gbps Plateau and 400-800 Gbps Surge

The 41-100 Gbps tier captured 38.53% of Brazil optical transceiver market size in 2025, bolstered by QSFP28 installations on carrier core routers and data-center spines. Replacement cycles for ageing 40G QSFP+ ports prolong demand through 2028. Yet the More-than-100 Gbps bracket accelerates at 9.99% CAGR as AWS and Microsoft shift to 400G QSFP-DD and 800G OSFP on new leaf-spine fabrics. Polo Mobwire’s 800G roll-out in Fortaleza confirmed commercial readiness of ultra-high-speed coherent optics. Sub-10 Gbps optics linger in SMB switch backplanes, while 10-40 Gbps remains essential for 5G fronthaul and small-cell aggregation where power budgets favour 25G SFP28.

Chinese vendors leverage scale advantages to dominate 100G SR and LR volumes, whereas Western suppliers focus on high-margin 400G-800G ZR coherent plugs. The Brazil optical transceiver market share for 400G is therefore expected to eclipse 100G by 2029, especially once 800G switches reach mainstream price points. ANATEL certification timelines of 6-9 weeks remain consistent across data-rates, so speed alone is not a regulatory bottleneck.

By Application: Telecom Base and Datacenter lift

Telecom absorbed 40.21% of 2025 shipments, anchored by backhaul expansion and fixed broadband aggregation. Nonetheless, data-center interconnect shows the fastest 9.78% CAGR through 2031 as São Paulo’s 770 MW pipeline and Fortaleza’s hyperscale campus lock in high-density optics procurement. Eletronet’s metro-DCI demonstration using 1.6 Tb/s pluggables showcased how carriers merge transport and DCI gearlines to contain opex. Enterprise and HPC pockets in financial hubs adopt 100G/200G low-latency modules for trading and AI workloads, while industrial medical and EV systems represent a niche but rising opportunity for ruggedized SFP+ and QSFP28 optics in machine-vision and telemedicine setups.

Over the forecast, telecom retains scale but cedes mix to data-center demand, shifting product development toward higher-speed, lower-power commercial-temperature modules. This pivot allows new Chinese entrants to gain footholds in the Brazil optical transceiver market, supplying bulk 400G DR4 for hyperscaler leaf rows at aggressive pricing.

By Connector Type: QSFP Dominance, OSFP Upshift

QSFP and QSFP-DD accounted for 44.18% of Brazil optical transceiver market share in 2025 due to versatility across 40G-400G lanes. OSFP, however, races ahead with 9.83% CAGR as 800G temperature and power envelopes fit its larger housing. SFP/SFP+ continues serving 1G-10G campus and access gear in secondary cities, whereas CFP families fade as coherent functionalities migrate into QSFP-DD and OSFP pluggable. Nokia’s distribution alliance with Vivensis illustrates operator need for seamless procurement of SFP+, QSFP28 and QSFP-DD within one network build.

Longer term, anticipation of 1.6 Tb/s gear cements OSFP growth, because its mechanical and electrical design scales to higher wattage. Standardized form factors simplify inventory and inter-vendor qualification, reinforcing competitive intensity in the Brazil optical transceiver market as barriers to entry decline.

Geography Analysis

Southeast Brazil commanded roughly 60% of national demand in 2025, riding on São Paulo’s dense data-center corridor and carrier core aggregation nodes. Rio de Janeiro added 10-12%, leveraging Eletronet’s OPGW backbone and V.tal’s subsea landings.

The Northeast is emerging as the fastest grower, anchored by Fortaleza’s 16-cable swaps and federal fiber grants that extended DWDM backbones into 20 additional cities by mid-2025. North and Central-West footprints expand as the PAIS program threads submarine fiber into Amazonian states, unlocking last-mile ISP builds that rely on 10G SFP+.

The South (Rio Grande do Sul, Paraná, Santa Catarina) accounts for around 15%, buoyed by Eletronet’s 1.2 Tb/s long-haul trial between São Paulo and Porto Alegre. Foreign direct investment reached USD 6.29 billion for January-November 2025, a 12.1% rise year-over-year, with a material share earmarked for North and Northeast fiber gaps. While São Paulo remains the anchor through 2031, geographical diversification tempers concentration risk and broadens the Brazil optical transceiver market footprint nationwide.

Competitive Landscape

Cisco, Huawei, Coherent and Lumentum jointly hold roughly 50-55% share, underscoring moderate concentration. They package end-to-end optical ecosystems that pair pluggables with line systems and SDN control planes. Chinese specialists Accelink, InnoLight and Hisense carve 20-25% share on the back of low-priced 25G and 100G modules that satisfy ANATEL conformance. Local player Padtec retains 2-3% via public-sector bids but faces cost compression, even after inaugurating a Manaus transceiver line financed by BNDES and FINEP.

Technology leadership shapes rivalry. Ciena’s WaveLogic 6 Extreme hit 1.6 Tb/s in Brazilian field tests, 60% above legacy benchmarks, helping secure Eletronet, BR.Digital and Polo Mobwire wins. Open optical networking threatens incumbents by enabling multi-vendor line systems, and Vivensis’ reseller pact with Nokia widens access channels for Tier-2 ISPs.

White-space opportunities persist in copper-rich Tier-3 metros and in utility smart-grid fiberization, both ripe for low-cost 10G SFP+ and 100G QSFP28 shipments. The Brazil optical transceiver market therefore balances premium coherent innovation with cut-price access optics, keeping margins mixed and competition robust.

Brazil Optical Transceiver Industry Leaders

Cisco Systems

Hewlett Packard Enterprise (HPE)

Arista Networks

Intel Corporation

Henkel AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Ministry of Science, Technology and Innovation and Finep launched 13 non-reimbursable grant calls totalling BRL 3.3 billion (USD 600 million) under the Nova Indústria Brasil program, including BRL 300 million for digital technologies and BRL 100 million earmarked for semiconductors, laying groundwork for domestic optical-component research.

- December 2026: The Ministry of Communications confirmed fiber networks now pass 4,645 municipalities, covering 83% of Brazil, while foreign direct telecom investment hit USD 6.29 billion for Jan-Nov 2025, up 12.1% year-on-year.

- August 2025: BR.Digital deployed Ciena WaveLogic 6 Extreme, achieving 1.1 Tb/s on links exceeding 800 km, improving spectral efficiency and lowering energy use across its 70,000 km backbone.

- May 2025: Eletronet and Ciena broke Brazilian records with 1.6 Tb/s over 40 km metro fiber and 1.2 Tb/s over 1,500 km long-haul without regeneration, demonstrating commercially viable ultrahigh-capacity transport.

Brazil Optical Transceiver Market Report Scope

The Brazil Optical Transceiver Market Report is Segmented by Protocol (Ethernet, Fibre Channel including FTTx, CWDM/DWDM, Other Protocols), Data Rate (Less Than 10 Gbps, 10-40 Gbps, 41-100 Gbps, More Than 100 Gbps including 400 Gbps), Application (Data Center, Telecommunication, Enterprise and HPC Networks, Industrial Medical and EV Systems), Connector Type (SFP and SFP+, QSFP and QSFP-DD, CFP/CFP2/CFP4/OSFP, XFP and CXP), and Geography (Brazil). The Market Forecasts are Provided in Terms of Value (USD).

| Ethernet |

| Fibre Channel (including FTTx) |

| CWDM/DWDM |

| Other Protocols |

| Less Than 10 Gbps |

| 10 - 40 Gbps |

| 41 - 100 Gbps |

| More Than 100 Gbps (including 400 Gbps) |

| Data Center |

| Telecommunication |

| Enterprise and HPC Networks |

| Industrial, Medical and EV Systems |

| SFP and SFP+ |

| QSFP and QSFP-DD |

| CFP/CFP2/CFP4/OSFP |

| XFP and CXP |

| By Protocol | Ethernet |

| Fibre Channel (including FTTx) | |

| CWDM/DWDM | |

| Other Protocols | |

| By Data Rate | Less Than 10 Gbps |

| 10 - 40 Gbps | |

| 41 - 100 Gbps | |

| More Than 100 Gbps (including 400 Gbps) | |

| By Application | Data Center |

| Telecommunication | |

| Enterprise and HPC Networks | |

| Industrial, Medical and EV Systems | |

| By Connector Type | SFP and SFP+ |

| QSFP and QSFP-DD | |

| CFP/CFP2/CFP4/OSFP | |

| XFP and CXP |

Key Questions Answered in the Report

How fast will hyperscaler demand grow for 400G and 800G optics in Brazil?

Shipments tied to new cloud regions push the segment at a 9.99% CAGR, making 400G-800G the main growth engine after 2026.

Why are data-center interconnect purchases outpacing telecom orders?

São Paulo and Fortaleza hyperscale campuses require high-density optics for spine-leaf fabrics, driving the fastest 9.78% CAGR through 2031.

Which connector will dominate 800G upgrades?

OSFP is favored thanks to higher thermal headroom, expanding at a 9.83% CAGR as 800G switches proliferate.

How are tariffs influencing vendor strategies?

Vendors operating PPB assembly lines in Manaus cut duties to 0-4%, gaining an edge over fully imported modules that face 12-16% tariffs.

What role do government fiber projects play?

Programs such as Norte Conectado pre-build middle-mile links, unlocking demand for 10G and 25G access optics among regional ISPs.

Will supply-chain shortages persist?

Photonic-IC tightness eases after 2027, but operators still dual-source 400G-800G plugs to mitigate future disruptions.

Page last updated on: