Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 22.97 Billion |

| Market Size (2026) | USD 23.74 Billion |

| Market Size (2031) | USD 27.68 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Telecom MNO Market Analysis by Mordor Intelligence

The Spain Telecom MNO market size was valued at USD 22.97 billion in 2025 and is estimated to grow from USD 23.74 billion in 2026 to reach USD 27.68 billion by 2031, at a CAGR of 3.12% during the forecast period (2026-2031). The measured pace reflects a pivot from voice-centric subscriptions toward data-heavy applications, fiber-mobile convergence, and enterprise connectivity. Spain now supports near-ubiquitous 5G coverage, yet headline revenue growth remains modest because unlimited-data tariffs keep average revenue per user muted. Operators therefore rely on converged bundles that combine fiber, mobile, pay-TV, and fixed telephony to protect margins, and on private 5G campus networks to unlock premium enterprise spending. Meanwhile, IoT and M2M connections continue to scale rapidly, outpacing traditional consumer lines as utilities, automotive plants, ports, and agriculture digitize their operations. Collectively, these shifts confirm that the Spain Telecom MNO market is advancing from scale-driven consumer acquisition to value-driven industrial digitization.

Key Report Takeaways

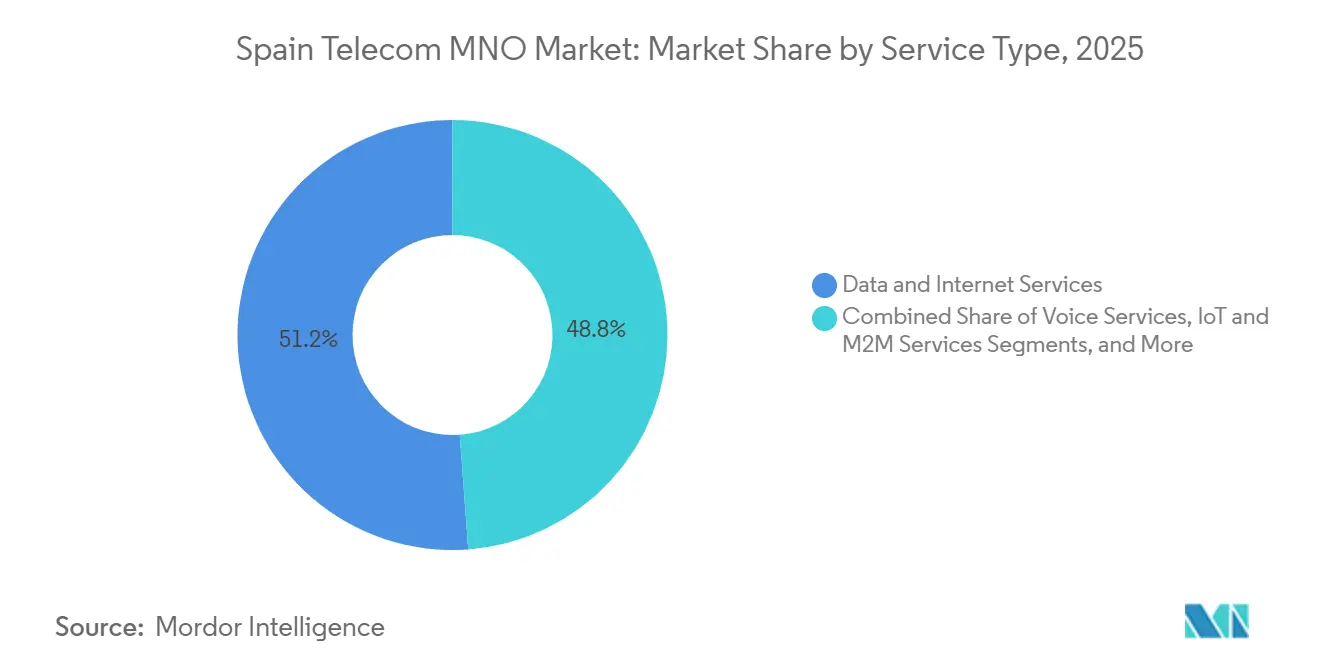

- By service type, Data and Internet Services led with 51.17% of Spain Telecom MNO market share in 2025. IoT and M2M Services are projected to register the fastest expansion, advancing at a 3.27% CAGR to 2031.

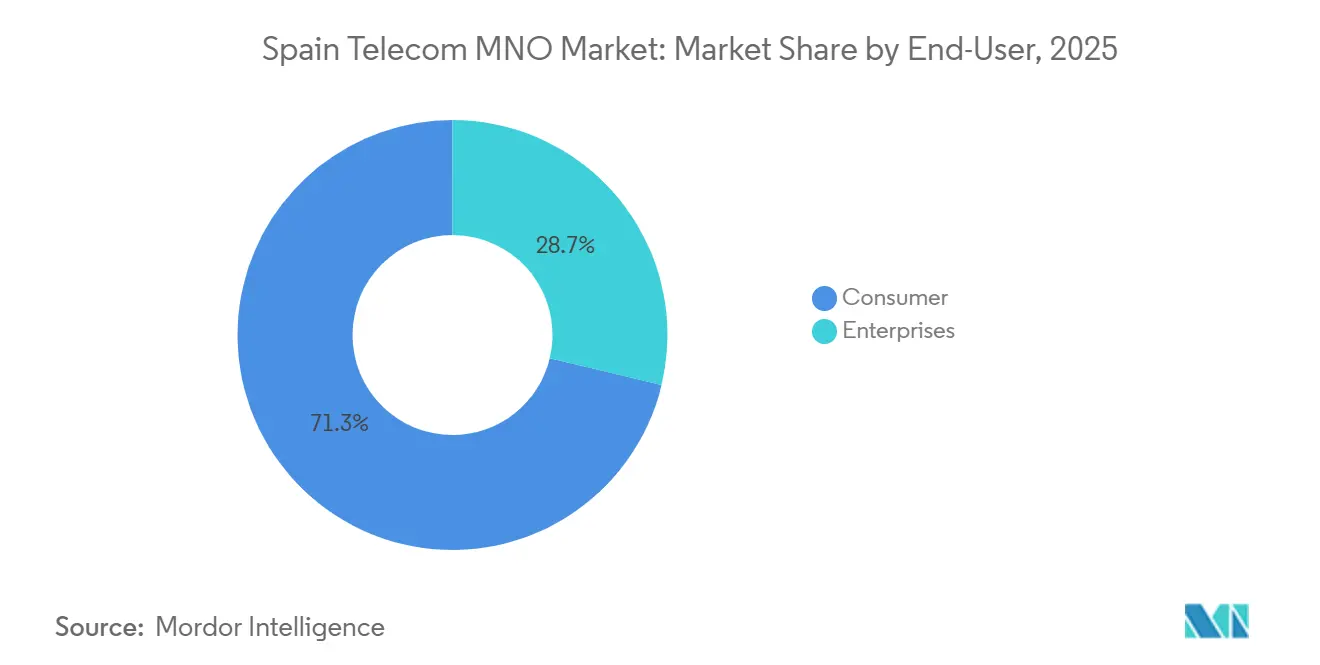

- By end-user, Consumer services accounted for 71.26% of Spain Telecom MNO market size in 2025, whereas the Enterprises segment is on track for a 3.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G Standalone Coverage Expansion and Spectrum Refarming | +0.8% | Madrid, Barcelona, Valencia Metropolitan Corridors | Medium Term (2–4 Years) |

| Rising Mobile-Data Consumption Driven by Unlimited Plans | +0.6% | Major Urban Centers Nationwide | Short Term (≤ 2 Years) |

| Fiber-to-the-Home Diffusion Enabling Converged Bundles | +0.5% | Nationwide, Rural Build-Outs Accelerating | Medium Term (2–4 Years) |

| Enterprise IoT Uptake in Energy, Transport, and Agriculture | +0.4% | Andalusia, Catalonia, Nationwide Utilities | Long Term (≥ 4 Years) |

| Industrial Private 5G Campus Network Demand | +0.3% | Catalonia Automotive Hubs, Valencia and Barcelona Ports | Long Term (≥ 4 Years) |

| Spectrum Lease Revenue from Neutral-Host Indoor DAS | +0.2% | High-Traffic Venues in Madrid, Barcelona, Seville | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

5G Standalone Coverage Expansion and Spectrum Refarming

Spain’s operators already run 8.3% of national 5G sites in standalone mode, far above the sub-3% European average. Telefónica improved capacity in Madrid and Barcelona by refarming 2.1 GHz spectrum that previously carried 3G traffic, raising spectral efficiency by 22% during 2025.[1]Telefónica, “Telefónica Spain Network Infrastructure and Financial Results Q4 2025,” telefonica.com MasOrange switched on a 5G-Advanced layer that aggregates 700 MHz, 3.5 GHz, and 26 GHz bands, delivering trial speeds above 3 Gbps.[2]Orange, “MasOrange 5G-Advanced Network Launch and Financial Performance,” orange.com Enterprises value the architecture because network slicing and edge nodes guarantee sub-10 millisecond latency for robotics and AR maintenance tools. The CNMC decision to extend 3.5 GHz licences to 2040 at no extra cost freed capital for further densification in industrial corridors.

Rising Mobile-Data Consumption Driven by Unlimited Plans

Unlimited tariffs now cover 68% of Spanish post-paid lines, lifting average monthly data use to 18.4 GB in 2025.[3]CNMC, “Spanish Telecommunications Market Report 2025,” cnmc.es DIGI’s EUR 10 offer forced incumbents to match prices, so ARPU slid to EUR 6.95 (USD 8.20) even as traffic soared. Vodafone’s network shows that video streaming represents 62% of mobile load yet adds no incremental revenue under flat-fee plans. Telefónica reported that top-decile users consumed 47 GB each month while contributing barely EUR 6.95 (USD 8.20) in revenue, compressing gross margins to 38%. Operators respond by upselling fiber-mobile bundles and premium 5G tiers priced near EUR 50 (USD 59) per month to restore profitability.

Fiber-to-the-Home Diffusion Enabling Converged Bundles

Nationwide FTTH coverage reached 95.2% in 2025, creating a platform for quad-play bundles that cut churn by 60% compared with mobile-only plans. Converged offers combining 1 Gbps fiber and mobile service sell at EUR 40-60 (USD 47-71), a 35% premium to standalone wireless. The Telefónica-Vodafone Fiberpass venture and the MasOrange-Vodafone FiberCo cover a combined 15.8 million premises while lowering per-home deployment costs by 28%. Lower capital intensity let fiber capex fall from 18% of revenue in 2023 to 14% in 2025. As rural rollouts accelerate, the addressable base for bundled mobile lines keeps expanding.

Enterprise IoT Uptake in Energy, Transport, and Agriculture

Machine-to-machine lines jumped 60.4% year-over-year to 19.95 million in July 2025 as smart meters, connected vehicles, and farm sensors came online. Spain’s traffic authority mandated V-16 roadside beacons, creating a captive market of 25 million low-band NB-IoT devices. Energy utilities installed 8.2 million cellular smart meters to meet EU real-time data rules. Orange Business pilots in Andalusia show that connected irrigation cuts water use by 22% and fertilizer by 18%. Telefónica Tech now manages 17 million Spanish IoT connections at 72% gross margins, triple its consumer mobile margin.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturated Mobile Subscriber Base Limiting Growth | -0.5% | Nationwide, Penetration >120% in Cities Such as Madrid and Barcelona | Short Term (≤ 2 Years) |

| ARPU Compression Due to Price Wars and Low-Cost Brands | -0.4% | Nationwide, Intensified in Large Metropolitan Markets | Short Term (≤ 2 Years) |

| Uncertain Litigation Over Historical Spectrum Fees | -0.2% | All Licensed Operators | Medium Term (2–4 Years) |

| Volatile Electricity Prices Increasing Network OPEX | -0.3% | Rural Base-Station Clusters Dependent on Backup Power | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Saturated Mobile Subscriber Base Limiting Organic Growth

Mobile penetration climbed to 122% in 2025 with 57.3 million active SIMs serving 47 million residents, leaving scant room for further line additions. Net new mobile subscriptions rose only 0.3% in 2025 compared with more than 2% annual growth before the pandemic. Incremental gains now stem mainly from multi-SIM devices and IoT links rather than new human users. Telefónica’s consumer ARPU fell 4.2% year-over-year despite migration efforts toward converged packages. The growth ceiling forces carriers to chase higher-value enterprise contracts to offset flat consumer volumes.

ARPU Compression Due to Price Wars and Low-Cost Brands

DIGI’s EUR 10 unlimited plan secured 1.8 million subscribers by December 2025, pushing incumbents to lower entry pricing by up to 50%. CNMC spectrum remedies now allow DIGI to target metro areas aggressively, deepening the discount gap. Vodafone Spain recorded a 5.1% ARPU contraction in 2025 as 28% of its base migrated to its own Lowi brand or defected to DIGI.[4]Vodafone, “Vodafone Spain Network Statistics and ARPU 2025,” vodafone.com Telefónica’s gross margin declined to 38% as usage-driven costs rose faster than revenue. Regulatory oversight blocks coordinated price lifts, so carriers must pursue network quality and exclusive content as non-price differentiators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Supremacy and the IoT Surge

Data and Internet Services held 51.17% of Spain Telecom MNO market revenue in 2025, far surpassing voice and messaging combined. The segment benefits from heavy video-streaming consumption and from 5G’s capacity uplift, yet flat-fee unlimited plans mute incremental monetization. IoT and M2M Services accounted for a smaller slice of Spain Telecom MNO market size but are projected to expand at a 3.27% CAGR, the fastest across all categories, as regulatory mandates embed connectivity into meters, vehicles, and agricultural sensors.

Voice and Messaging revenues continue to contract as over-the-top apps displace circuit-switched traffic, while OTT and PayTV add roughly 8% to the overall mix through churn-reducing bundles. Roaming almost returned to pre-pandemic levels in 2025, aiding the “other services” pool that still contributes meaningfully to Spain Telecom MNO market share in tourist districts. Long-term upside resides in platforms capable of managing device fleets at scale, a capability already reflected in Telefónica Tech’s high-margin IoT earnings.

By End-User: Consumer Scale Versus Enterprise Value

The Consumer segment captured 71.26% of Spain Telecom MNO market size in 2025, but its growth prospects are constrained by modest ARPU trends and full penetration. In contrast, Enterprises, though representing fewer connections, will deliver a 3.41% CAGR to 2031, outstripping consumer progress and gradually enlarging their Spain Telecom MNO market share.

Enterprise ARPU averages more than double the consumer figure because corporate clients often purchase multi-SIM fleets, secure SD-WAN overlays, and managed service wraps. Private 5G campus contracts at automotive plants and ports underscore how mission-critical latency and reliability translate into premium pricing. Even so, enterprise sales cycles are lengthy and integration-heavy, tempering the near-term scale of contribution despite the robust margin profile.

Geography Analysis

Madrid and Barcelona metropolitan zones generated more than 40% of national 5G traffic in 2025, reflecting dense small-cell grids and affluent, data-hungry demographics. Network leadership in these hubs offers a showcase for premium plans and enterprise campus networks, positioning carriers to capture early adopter revenues. Beyond the primary cities, the Catalonia industrial corridor supports the lion’s share of Spain’s private 5G deployments, leveraging proximity to automotive assembly, chemical plants, and logistics centers.

Rural provinces cover most of the landmass yet hold less than one-fifth of the population. Government grants are therefore instrumental in narrowing the digital divide, and subsidized rollouts under the Unico-5G program extend low-band coverage to thousands of small municipalities. Agrarian Andalusia illustrates the benefits, with connected irrigation and pest-monitoring networks reducing resource use and lifting crop yields.

Island territories rely on recent submarine fiber investments for backhaul, ensuring 5G parity with the mainland despite geographic isolation. Regulatory mandates on population coverage compel operators to maintain consistent service levels across archipelagos, and compliance penalties incentivize prompt rollout. As a result, even remote tourism-heavy regions now enjoy gigabit-class cellular service that underpins contactless hospitality, smart-traffic, and emergency-response solutions.

Competitive Landscape

Spain shifted to a three-operator structure after the 2024 consolidation wave, increasing market concentration but also enabling larger balance sheets to support 5G densification. Telefónica, MasOrange, and Vodafone Spain together command more than four-fifths of subscriptions, yet the disruptive presence of DIGI as a low-cost fourth entrant restrains headline price inflation. Infrastructure-sharing ventures such as Fiberpass and FiberCo illustrate the new equilibrium: carriers pool passive assets to trim capital outlays while safeguarding brand differentiation at the retail layer.

Enterprise private 5G remains a white-space opportunity. Only a dozen-plus live networks serve factories and ports today, leaving thousands of addressable sites untapped. Specialized integrators like Ericsson and Cellnex often mediate these deployments, which reduces execution risk for MNOs but diverts a portion of the value chain outside their direct control. Operators are therefore investing in edge-cloud orchestration, application marketplaces, and patented network-slicing tools to anchor more of the revenue internally.

Regulation continues to mold outcomes. The extension of 3.5 GHz licenses free of charge strengthened balance sheets, while a modest bump in mobile termination rates improved the MVNO business case. These moves enhance competitive intensity by empowering smaller challengers without undermining incumbents’ investment capacity. Against this backdrop, strategic focus centers on fiber-mobile convergence, indoor coverage monetization, and differentiated enterprise propositions capable of rebuilding ARPU momentum.

Spain Telecom MNO Industry Leaders

MASORANGE, S.L.

Zegona Communications (Vodafone Spain)

Movistar (Telefónica Spain)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Sateliot and PLD Space launched Spain’s first 5G satellite mission, deploying six LEO satellites that extend national IoT coverage to maritime zones.

- January 2026: Telefónica allocated USD 897 million for rural fiber build-outs across Castilla y León, Extremadura, and Galicia, targeting 98% household coverage by 2028.

- December 2025: MasOrange completed core-network integration and activated Spain’s first 5G-Advanced service, unlocking carrier aggregation across low-, mid-, and millimeter-wave bands.

- November 2025: Telefónica unveiled a USD 3.59 billion multi-year plan for XGS-PON upgrades, standalone-core modernization, and city-edge compute nodes.

- October 2025: Zegona closed its USD 5.6 billion purchase of Vodafone Spain and began an efficiency program slated to deliver USD 393 million in annual savings.

Spain Telecom MNO Market Report Scope

Telecom or Telecommunication is the long-range transmission of information by electromagnetic means.

The Spain Telecom MNO Market Report is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, IoT and M2M Services, OTT and PayTV Services, and Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, Rest of Service Type)), End-User (Enterprises, and Consumer), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services) |

End-User

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the projected size of the Spain Telecom MNO market by 2031?

It is forecast to reach USD 27.68 billion by 2031, reflecting a 3.12% CAGR from 2026-2031.

Which service category is expanding the fastest?

IoT and M2M Services show the quickest trajectory, advancing at a 3.27% CAGR through 2031 as utilities, automotive plants, ports, and agriculture embed connected-device solutions.

Why does average revenue per user remain low despite rising data traffic?

Unlimited-data plans dominate the post-paid base, lifting monthly usage but capping per-line revenue, so carriers rely on converged bundles and premium 5G tiers to enhance margins.

How are operators monetizing enterprise demand?

Telefónica, MasOrange, and Vodafone Spain deploy private 5G campus networks, SD-WAN, and managed IoT platforms that command enterprise ARPUs more than double consumer levels.

What regional programs support rural connectivity?

The government's Unico-5G initiative funds low-band 5G rollouts in municipalities under 5,000 inhabitants, while new fiber routes link the Balearic and Canary Islands to mainland backhaul.

How concentrated is competition after recent mergers and acquisitions?

Following the Orange-MasMovil merger and Vodafone Spain's sale to Zegona, three national operators hold roughly 86% of subscriptions.

Page last updated on: