Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 30.46 Billion |

| Market Size (2026) | USD 31.53 Billion |

| Market Size (2031) | USD 36.98 Billion |

| Growth Rate (2026 - 2031) | 3.24% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UK Telecom MNO Market Analysis by Mordor Intelligence

The UK Telecom MNO Market size is expected to grow from USD 30.46 billion in 2025 to USD 31.53 billion in 2026 and is forecast to reach USD 36.98 billion by 2031 at 3.24% CAGR over 2026-2031. In terms of subscriber volume, the market was valued at 101.57 million subscribers in 2025 and is expected to grow from 103.93 million subscribers in 2026 to 115.62 million subscribers by 2031, at a CAGR of 2.13% during the forecast period (2026-2031). Rapid 5G-stand-alone deployment, mounting demand for fixed-mobile convergence bundles, and proactive rural-coverage schemes are widening revenue pools even as headline growth rates appear modest. Consolidation following the 2025 Vodafone-Three merger unlocked scale efficiencies that immediately pushed average 4G speeds up by 40% for 7 million customers and set a foundation for dense 5G roll-outs. Enterprise appetite for network slicing and multi-access edge computing is beginning to translate into premium contract wins, while stringent Ofcom rules against inflation-linked price rises are forcing operators to lean on transparent tariffs and value-added services. Capital intensity remains high because millimeter-wave spectrum fees, energy tariffs, and net-zero commitments are advancing in parallel with traffic volumes.

Key Report Takeaways

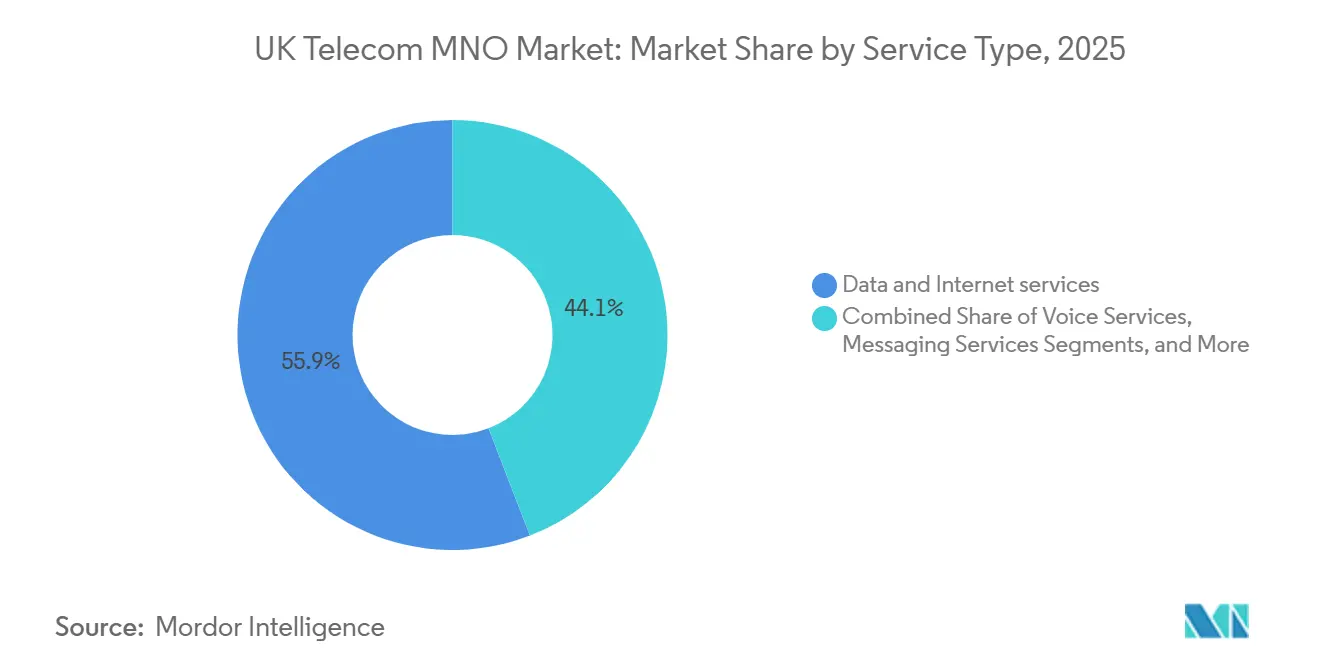

- By service type, data and internet services captured 55.87% of UK Telecom MNO Market share in 2025, whereas IoT and M2M services are forecast to post a 4.42% CAGR through 2031.

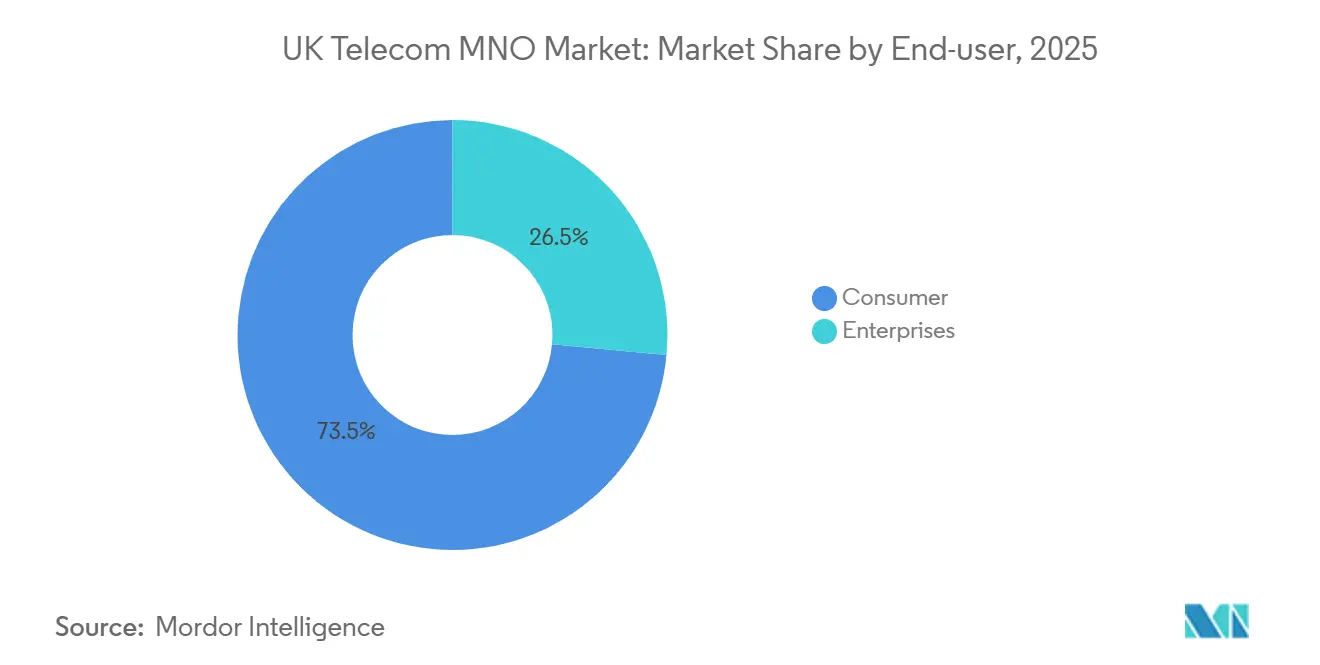

- By end-user, the consumer segment led with 73.52% revenue share in 2025; the enterprise segment is expected to register the fastest 3.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UK Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G Stand-Alone Roll-Out Accelerates Premium ARPU Uplift | +0.8% | National, led by London, Manchester, Birmingham | Medium term (2-4 years) |

| Fixed-Mobile Convergence Bundles Deepen Churn Reduction | +0.7% | National, strongest in Virgin Media O2 cable and BT Openreach FTTP zones | Short term (≤ 2 years) |

| Shared Rural Network Expands Coverage into New Demand Pockets | +0.3% | Rural England, Scotland, Wales, Northern Ireland | Medium term (2-4 years) |

| CPI+3.9% Tariff Indexing Previously Protected Top-Line Growth | +0.5% | National, future impact capped by 2025 ban | Short term (≤ 2 years) |

| Network-Slicing Guarantees for MEC-Based Verticals Unlock New Revenue Streams | +0.4% | National, early uptake in Midlands manufacturing hubs and NHS trusts | Long term (≥ 4 years) |

| Ofcom OpenRAN Rules Shorten 5G Small-Cell Permitting | +0.2% | Urban areas and transport corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Stand-Alone Roll-Out Accelerates Premium ARPU Uplift

Standalone architecture went live nationwide in 2025, removing 4G anchors and cutting end-to-end latency below 10 milliseconds for eligible enterprise workloads. EE now markets guaranteed-slice packages at three to five times consumer postpaid ARPU, while Virgin Media O2 and the merged Vodafone-Three entity funnel a combined GBP 11 billion (USD 14.74 billion) into densification over the next decade. Manufacturing, logistics, and healthcare early adopters validate willingness to pay for deterministic performance, signaling a structural uplift in blended revenue per user. Spectrum depth across 3.4–3.8 GHz plus fresh 26 GHz blocks enables operators to isolate traffic with minimal interference, which raises perceived service quality and stickiness. As more devices ship with Release-17 firmware, premium tiers are expected to capture a rising share of new activations, pushing overall UK Telecom MNO Market yields higher despite retail-price caps.

Fixed-Mobile Convergence Bundles Deepen Churn Reduction

Operators bundle gigabit broadband, 5G data, and streaming perks into a single invoice, cutting household churn by up to 30% against single-play tariffs. Virgin Media O2’s Volt base already accounts for roughly one-quarter of its residential customers, averaging 40-50% more monthly revenue than mobile-only users. BT exploits Openreach fiber to pull EE subscribers into long-term contracts, which reduces acquisition cost and unlocks handset financing flexibility. Converged homes consume more data across fixed and mobile screens, accelerating volume growth without cannibalizing margins. Because Ofcom enforces wholesaling rules on fixed access but not on cable, integrated players retain an economic edge that is difficult for pure-play mobile rivals to replicate.

Shared Rural Network Expands Coverage into New Demand Pockets

The public-private Shared Rural Network hit its 95% geographic target one year early, extending 4G to remote areas in Scotland, Wales, and Northern England. Joint tower builds lowered per-site capex by about 40%, making sparse regions economically viable for the first time in a decade. Coverage gains unlock latent demand among agriculture and tourism businesses, while remote workers replace unreliable satellite links with mobile broadband. Ofcom’s streamlined site-acquisition code slashed permitting times below 12 months, accelerating small-cell roll-outs on rural roads and rail corridors. Although rural ARPU lags urban levels, incremental usage drives higher spectrum utilization and satisfies universal-service mandates that influence future license renewals.

Network-Slicing Guarantees for MEC-Based Verticals Unlock New Revenue Streams

Dedicated network slices paired with multi-access edge computing now support telemedicine, predictive maintenance, and autonomous-vehicle coordination at sub-10-millisecond latency. BT’s enterprise unit secured annual contracts worth GBP 1.5 million in 2025 (USD 2.01 million), while Vodafone’s NHS pilots demonstrated congestion-free high-definition diagnostics. Pricing ranges from GBP 500-2,000 per slice per month, decoupling revenue from consumer data bundles. Operators face a consultative sales cycle, but once embedded, mission-critical slices exhibit near-zero churn and strong upsell potential. Over the forecast horizon, slice monetization is projected to outstrip basic connectivity growth, cushioning EBITDA against inflationary cost inputs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum and Energy Costs Squeeze EBITDA Margins | -0.6% | National, acute for legacy copper operators | Short term (≤ 2 years) |

| MVNO Migration Dilutes Headline ARPU in Cost-of-Living Crisis | -0.4% | National, prepaid and low-income segments | Short term (≤ 2 years) |

| Net-Zero Targets Front-Load Capex for Greener Networks | -0.3% | National, dense urban small-cell zones | Medium term (2-4 years) |

| Net Neutrality and Environmental Levies Limit Differential Pricing | -0.2% | National, under Ofcom oversight | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Spectrum and Energy Costs Squeeze EBITDA Margins

The 2025 millimeter-wave auction added GBP 343 million (USD USD 460 million) in license fees, bringing annual spectrum charges to roughly GBP 200 million per operator.[1]Ofcom, “Telecoms Data Tables Q3 2025,” ofcom.org.uk Source: Vodafone plc, “Enterprise IoT Performance 2025 Update,” vodafone.com Simultaneously, electricity prices for radio sites rose 15-20%, inflating network opex just as traffic volumes accelerate. Operators with legacy copper incur higher watts-per-gigabyte than fiber-centric rivals, eroding competitive leverage. EE and Vodafone are testing AI-based energy-management software that dynamically powers down carriers during off-peak windows, but savings will take several years to scale. Until then, elevated cost of service narrows margin headroom and may delay discretionary investments in rural densification.

MVNO Migration Dilutes Headline ARPU in Cost-of-Living Crisis

Discount virtual operators such as Giffgaff, Smarty, and Lebara undercut incumbent tariffs by up to 50%, attracting price-sensitive shoppers during 2024-2025 inflation spikes. Virgin Media O2 logged 122,800 postpaid losses in early 2025, a direct consequence of SIM-only bargains that entice budget-constrained households. Ofcom statistics show industry-wide ARPU sliding from GBP 14.20 (USD 19.03) to GBP 13.58 (USD 18.18) year on year, despite steady growth in data volumes. Merger-related remedies freeze MVNO wholesale rates through 2028, limiting carriers’ ability to raise transfer prices and protecting the low-cost segment’s appeal. Although incumbents have launched flanker brands to recapture churners, these offerings compress blended margins and entrench promotional pricing behavior throughout the UK Telecom MNO Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: IoT Acceleration Reshapes Revenue Mix

Data and internet services controlled 55.87% of UK Telecom MNO market share in 2025, reflecting the migration of household and enterprise workloads to mobile broadband as well as the substitution of fixed lines in fiber-poor areas. Quarterly mobile traffic hit 1,257 petabytes in Q3 2025, an 18% year-on-year jump fueled by high-definition video, cloud gaming, and remote-work applications that require multi-gigabyte allowances. Yet IoT and M2M connections are projected to expand at a 4.42% CAGR from 2026 to 2031, outpacing every other service line inside the UK Telecom MNO market size. Narrowband IoT and LTE-M smart-meter roll-outs priced at GBP 1-3 (USD 1.27-3.81) per device per month offer predictable recurring revenue and minimal incremental traffic load. Voice and SMS continue a secular decline as over-the-top apps displace traditional calls and texts, turning both into retention features bundled with unlimited data rather than standalone cash generators.

Messaging revenue faces identical pressure, while OTT and PayTV partnerships add ancillary income through bundled streaming rights that raise perceived value with little extra cost to carriers. Hybrid fixed-mobile bundles deepen wallet share by lowering churn 20-30% and lifting household spend 40-50%, reinforcing the structural tilt toward converged propositions. IoT momentum benefits from the government mandate to fit 53 million smart meters nationwide by 2025 and from automakers embedding cellular modems for over-the-air software updates. Industrial clients pay two to three times consumer rates for guaranteed uptime and dedicated support, underscoring why IoT will capture a growing slice of UK Telecom MNO market share through 2031. As 5G Release-17 modules gain scale, connected-device volumes are set to multiply, embedding cellular connectivity across manufacturing, healthcare, and logistics workflows.

By End-User: Enterprise Margin Expansion Outpaces Consumer Volume

Consumer lines represented 73.52% of UK Telecom MNO market share in 2025, supported by more than 80 million active SIMs nationwide. Despite that scale, enterprise revenue is projected to grow at a 3.66% CAGR through 2031 because private 5G, network slicing, and multi-access edge computing command far richer unit economics than postpaid handset plans. BT’s business mobile arm recorded GBP 1.202 billion (USD 1.53 billion) in FY25, while its consumer unit delivered GBP 3.509 billion (USD 4.46 billion), illustrating how a smaller user base can still wield strategic pricing power. Private 5G factories routinely pay GBP 2,000-5,000 (USD 2,540-6,350) per month for dedicated slices that guarantee sub-10-millisecond latency, dwarfing the GBP 20-30 (USD 25.40-38.10) average consumer ARPU.

Vodafone’s NHS pilots proved that network-sliced telemedicine can support congestion-free high-definition diagnostics, validating premium price points for mission-critical traffic. Enterprises also deploy thousands of IoT endpoints that each yield GBP 5-10 (USD 6.35-12.70) monthly with multi-year contract visibility, a scaling model independent of handset churn. Consumer profitability, meanwhile, is squeezed by MVNO discounting, pushing incumbents to defend share with converged bundles like Virgin Media O2’s Volt, which lowers churn by roughly one-quarter. As more enterprises embrace stand-alone 5G and edge computing, the services segment is set to command a larger slice of UK Telecom MNO market size even while consumer lines continue to dominate volume metrics.

Geography Analysis

Urban corridors generate a disproportionate share of revenue, with London, Manchester, Birmingham, and Glasgow responsible for roughly 40% of 2025 mobile turnover. Dense small-cell grids and abundant fiber backhaul permit carrier aggregation that drives superior user throughput. EE’s 5G-plus footprint spans 66% of the population, anchored by these metropolitan strongholds. [2]Liberty Global. "Investor Relations - Financial Results." Accessed January 19, 2026. https://www.libertyglobal.com/investor-relations/financial-results/

Rural Scotland, Wales, and Northern England benefited from the Shared Rural Network, which met its 95% coverage goal in 2025, translating into fresh SIM activations among agriculture, tourism, and home-office users. Economic return in these territories is thinner, yet regulatory and reputational factors compel continued investment. Early OpenRAN pilots in Wales demonstrated 20-30% cost savings, creating a template for Highlands deployments that can stretch capex budgets.

Northern Ireland introduces cross-border competitive tension because Irish tariffs often undercut UK plans, especially on roaming. The Vodafone-Three merger pooled spectrum to strengthen coverage in lower-density regions, promising future efficiency gains. Over the forecast horizon, urban areas will continue to fund rural obligations, maintaining a balanced yet unequal revenue map across the UK Telecom MNO Market.

Regulatory Landscape

The UK telecom market is regulated primarily by Ofcom, with rules covering spectrum licensing, competition remedies, and consumer pricing transparency. Ofcom also governs the operating conditions attached to recent spectrum awards such as the 26 GHz and 40 GHz bands, auctioned in 2025, which include build and service obligations that affect the economics of 5G densification in major cities.

From April 2026 to March 2031, Ofcom set a new fixed-market framework through the Telecoms Access Review (2026-31), aimed at balancing competition with investment incentives for gigabit-capable networks. Separately, the UK government updated its Statement of Strategic Priorities on April 30, 2026, directing Ofcom toward pro-growth, investment-supporting regulation, while ongoing policy work on telecoms supply chain diversification and Open RAN interoperability continues to shape vendor strategies and network security risk management across UK operators.

Value Chain Analysis

The UK telecom MNO value chain runs from spectrum access and licensing (Ofcom) to network build and operations (RAN, core, transport/backhaul, sites and power). It also includes service enablement (OSS/BSS, security, roaming, billing), distribution through direct digital channels, retail, and partners, and the device and enterprise solution ecosystem (handsets, IoT modules, managed services).

Operator execution depends on a mix of in-house assets and strategic suppliers. BT Group anchors fixed-mobile propositions through Openreach as a wholly owned full-fibre platform, while VodafoneThree leans on large-scale vendor partnerships for RAN and core modernization, including Ericsson, and Virgin Media O2 uses a converged fixed and mobile footprint to package services. Supply chain diversification efforts, especially around open and interoperable RAN, are reshaping procurement and integration workstreams, increasing the role of systems integration, testing, and multi-vendor lifecycle management alongside traditional equipment sourcing. The government has also highlighted the breadth of the domestic ecosystem through its Advanced Connectivity Technologies mapping, which notes around 11,812 active firms in related telecoms activity, including specialist and hybrid companies supporting deployment, integration, and operations.

Competitive Landscape

Market structure shifted decisively with the May 2025 Vodafone-Three merger that produced a 28.8 million-subscriber leader pledging GBP 11 billion (USD 14.74 billion) of network investment over a decade. Virgin Media O2 retains a convergence moat by uniting cable broadband with mobile, generating 40-50% higher household spend versus single-play offers.[3]Financial Reporting and News." Accessed January 19, 2026. https://www.bt.com/about/bt/our-company/bt-group-plc/financial-reporting-and-news BT’s EE brand exploits Openreach fiber reach to cross-sell mobile, lowering acquisition costs and locking multi-play accounts.

Regulatory conditions insisted on frozen MVNO wholesale rates for three years, protecting discount brands that siphon price-sensitive traffic yet keeping competitive pressure alive. Operators now chase white-space enterprise opportunities such as private 5G factories and hospital networks. BT targets GBP 50 million (USD 67 million) in annual private-slice revenue by 2027, while Vodafone’s OpenRAN pilots trimmed site costs by up to 30%, promising faster urban densification. Competitive differentiation will increasingly hinge on the ability to monetize 5G stand-alone capabilities and converged propositions faster than rising costs dilute operating margins in the UK Telecom MNO Market.

The three incumbents are also racing to unlock fresh efficiencies through vendor diversification and software-defined infrastructure. Vodafone’s OpenRAN rollout, which trimmed site costs by roughly 30%, is pressuring Ericsson and Nokia to sharpen pricing and support models as contracts come up for renewal. EE is piloting AI-driven energy-management software across 20,000 radio sites, a move expected to cut electricity use 15% by 2027 and narrow opex gaps with cable-powered rivals. Virgin Media O2 must balance convergence advantages against millimeter-wave coverage obligations that require dense small-cell grids in at least 10 cities by 2028, stretching integration resources even as fixed-line upgrades soak up capital. Meanwhile, Ofcom’s push for greater supplier diversity is nudging all operators toward multi-vendor cores that can mix and match best-of-breed functions without lock-in risks. Collectively, these strategic pivots signal a shift from pure scale economics to technological agility as the critical success factor in the UK Telecom MNO Market.

UK Telecom MNO Industry Leaders

-

EE Limited (BT Group)

-

Virgin Media O2

-

VodafoneThree

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

New monetization whitespace is forming around performance-assured 5G stand-alone capabilities that combine network slicing with multi-access edge computing for vertical use cases such as healthcare, manufacturing, and logistics. In 2025, BT secured enterprise slice contracts and Vodafone ran NHS pilots, giving operators proof points that mission-critical connectivity can be sold as a managed outcome rather than a commodity data plan, with pricing that decouples revenue from consumer ARPU pressure.

Coverage-extension and resilience offers are also widening the product frontier, where terrestrial networks are supplemented by satellite direct-to-device connectivity. Virgin Media O2 moved in February 2026 with the launch of O2 Satellite (direct-to-device), aligning with Ofcom work on authorisation approaches for satellite-to-handset use in mobile spectrum bands. Public policy that promotes supply chain diversification and open, interoperable network approaches is expanding the addressable market for Open RAN software, integration, and managed services in the UK, particularly as operators pursue densification programs under merger and license obligations.

Recent Industry Developments

- July 2026: Virgin Media O2 deployed its 500th Giga Site, part of Mobile Transformation Plan. The high density site rollout and Massive MIMO deployment expand network capacity and urban coverage. This strengthens ARPU potential and competitive differentiation.

- April 2026: EE expanded its 5G+ network to cover more than 50 million people across 610 towns and cities. This major coverage expansion improves service quality and supports premium bundle offerings while reinforcing BT/EE market position.

- February 2026: Virgin Media O2 launched O2 Satellite, direct-to-device satellite-to-mobile service powered by Starlink Direct to Cell. This first mover satellite-to-mobile capability extends rural coverage and complements terrestrial networks, enabling new service propositions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers telecom service revenues generated in the United Kingdom from providing connectivity and communication services to end users, across consumer and business accounts, including both retail and wholesale where it is directly linked to telecom service delivery.

Scope exclusions: We exclude handset device sales, pure IT services, media content subscriptions, and unrelated equipment installation revenues that are not billed as telecom services.

Segmentation Overview

- Overall Telecom Revenue and ARPU

-

Service Type

- Voice Services

- Data and Internet Services

- Messaging Services

- IoT and M2M Services

- OTT and PayTV Services

- Other Services (VAS, Roaming and International, Enterprise and Wholesale, etc.)

-

End-User

- Enterprises

- Consumer

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping the UK telecom revenue pool and usage patterns using public statistics and regulatory datasets, and then lining them up with operator disclosures so the totals make sense in real world terms. For this market, references such as Ofcom communications market datasets, the UK Office for National Statistics releases on communications services, HM Revenue and Customs trade statistics (for selected network equipment signals), and spectrum and licensing publications are useful anchors.

We also review annual reports, investor presentations, and audited filings to understand reported service revenue splits and how they changed with pricing, churn, and mix. When we need a consistent view of company financials, news flow, patents, contracts, and shipment or tender signals, we use approved paid subscriptions that help fill gaps without changing the market boundary. The sources listed above are illustrative and not exhaustive, and many other public documents were also checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to sanity check what secondary sources cannot fully explain, especially on current ARPU movement, bundle discounts, wholesale pass-through, and timing of price changes. We interview a mix of operators, infrastructure stakeholders, enterprise buyers, and channel-side experts across the UK so that assumptions on subscribers, service mix, and pricing are grounded and can be rechecked when variances show up.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 17% | |

| Mid tier: 47% | Functional/Unit leaders: 34% | |

| Smaller Players: 17% | Managers: 49% |

Market-Sizing & Forecasting

Sizing starts from a top-down revenue reconstruction, where regulated reporting series and operator service revenue disclosures are used to build the total addressable service pool, followed by allocating it across service groups based on usage and billing patterns. To keep the result realistic, we then corroborate it with selective bottom-up checks, such as sampled ARPU multiplied by subscriber bases, and channel checks on typical bundle price points and discounting.

Inputs used in the model include mobile and fixed subscriber counts, ARPU by plan type, share of bundled offers, churn and porting trends, and the pace of fiber and 5G adoption that shifts traffic and pricing. For forecasting, scenario analysis is applied around price rises, competitive intensity, and macro pressure on household spend, and these scenarios are reviewed against what primary respondents expect on near term plan mix and promotional activity. Where company level splits are not consistently disclosed, gaps are handled by using proxy ratios from comparable service lines and then rebalancing to match known totals.

Data Validation & Update Cycle

Validation is done in layers so errors do not pass through quietly. Model outputs are compared against independent signals like regulatory revenue series, subscriber totals, and ARPU direction, and then any large variance is traced back to a specific assumption before sign-off.

If a metric moves outside the expected range, we recheck definitions, rerun currency conversions, and re-contact relevant interviewees to confirm whether a one-off event or pricing action explains it. Reports are refreshed annually, and interim updates are made when material events occur, such as major pricing resets, merger actions, or policy changes. Before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's United Kingdom Telecom Market Estimate Compared With Other Published Estimates

Published UK telecom market numbers can look far apart even when they are trying to describe the same space, because the boundaries and timing choices are not always consistent. The biggest differences usually come from whether pay-TV or devices are bundled into the total, how wholesale is treated, and which calendar or fiscal cut is used for currency conversion.

In a refresh-led approach, the currency timing and the way ARPU is stepped forward (price-rise months versus full-year averages) can shift the market value meaningfully, and Mordor Intelligence keeps this controlled by aligning exchange rates and validation checks to the same update window used for subscriber and revenue inputs.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 30.46 B (2025) | |

| Industry Association A | USD 34.10 B (2025) | Often reported in GBP as total communications revenues and then converted using a different rate window, and it may blend adjacent services such as content-linked bundles, which inflates the service-only pool. |

| Trade Journal B | USD 28.20 B (2024) | May use partial-year ARPU trends and promotional price points without fully normalizing for price-rise timing, and it can undercount wholesale-linked service revenues that still belong to telecom delivery. |

The comparison shows that the spread is mainly explained by refresh timing, currency conversion windows, and whether bundle-adjacent revenues are pulled into the total. By sticking to a repeatable revenue build, then cross-checking it with subscriber and ARPU math, we can give a balanced number that is easier to trace and update.

Key Questions Answered in the Report

How large is the UK Telecom MNO Market in 2026?

The UK Telecom MNO Market size stood at USD 31.53 billion in 2026 with a 3.24% CAGR outlook to 2031.

Which service type leads revenue?

Data and internet services held 55.87% of UK Telecom MNO Market share in 2025, driven by rising video and cloud-gaming traffic.

What segment is growing fastest?

IoT and M2M services are projected to expand at a 4.42% CAGR through 2031 as smart-meter roll-outs and connected-device adoption accelerate.

How will enterprise demand shape growth?

Private 5G networks and network-slicing guarantees for manufacturing and healthcare are lifting the enterprises segment at a 3.66% CAGR.

What impact does the Vodafone-Three merger have?

The merger created the largest operator with 28.8 million customers and committed GBP 11 billion to densify 5G, enhancing capacity and scale efficiencies.

Why are energy costs a restraint?

Spectrum fees and a 15-20% jump in electricity tariffs during 2024-2025 increased operating expenses, squeezing EBITDA margins for operators with legacy infrastructure.

Page last updated on: