Norway Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.09 Billion |

| Market Size (2026) | USD 3.19 Billion |

| Market Size (2031) | USD 3.73 Billion |

| Growth Rate (2026 - 2031) | 3.17% CAGR |

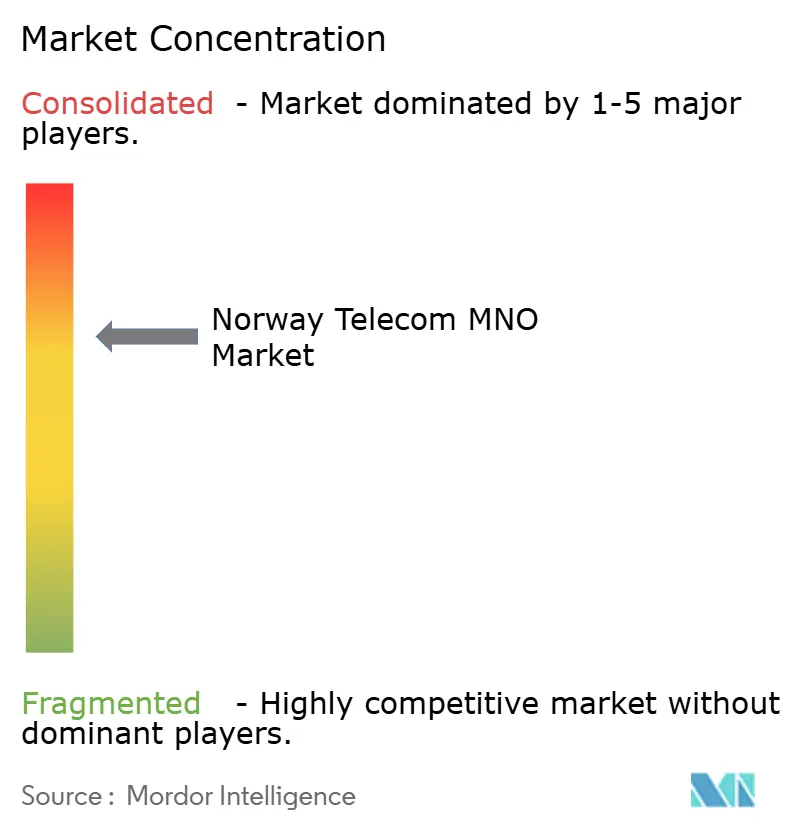

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Norway Telecom MNO Market Analysis by Mordor Intelligence

Norway Telecom MNO Market size in 2026 is estimated at USD 3.19 billion, growing from 2025 value of USD 3.09 billion with 2031 projections showing USD 3.73 billion, growing at 3.17% CAGR over 2026-2031.

Growing enterprise digitalization, accelerated 5G roll-outs and government-backed fiber programs are reinforcing steady topline growth even as overall penetration tops 110%. Data and Internet services retained nearly half of 2024 revenue, underpinned by a 375% jump in 5G download speeds that is reshaping consumer usage patterns. Industrial demand for private 5G and edge-enabled IoT is gathering momentum following the allocation of 3.8–4.2 GHz spectrum and six mobile-network codes reserved for non-public networks. At the same time, energy-utility MVNOs such as Fjordkraft are leveraging convergent bundles to grab share in residential mobile, achieving 52% subscriber growth in 2024. Regulatory interventions—ranging from mandatory wholesale broadband access in 22 regions to a phased 2G sunset—are steering operators toward value-added revenue pools rather than raw subscriber additions.

Key Report Takeaways

- By service type, Data and Internet services led with 48.02% of Norway telecom market share in 2025; IoT and M2M services are projected to grow at a 3.29% CAGR to 2031.

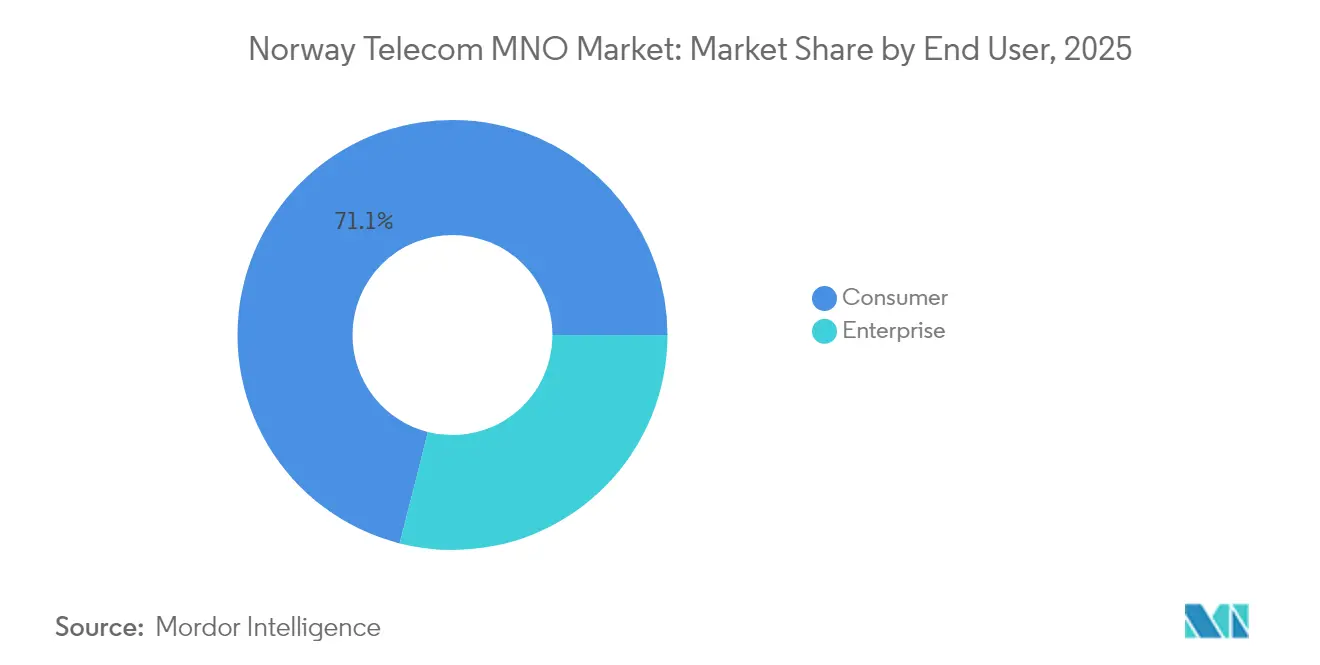

- By end-user, the consumer segment accounted for 71.05% share of the Norway telecom market size in 2025, while enterprise services are advancing at a 3.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Norway Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid nationwide 5G rollout and >99% population coverage | +0.8% | National; urban concentration in Oslo, Bergen, Trondheim | Medium term (2-4 years) |

| Surging per-capita mobile data consumption | +0.6% | National; strongest in metro areas | Short term (≤2 years) |

| Government-backed fiber broadband acceleration | +0.4% | National; rural focus | Long term (≥4 years) |

| Enterprise digitalization fuelling IoT connectivity demand | +0.5% | National; industrial clusters | Medium term (2-4 years) |

| Allocation of local 5G codes enabling private networks | +0.3% | Industrial zones | Long term (≥4 years) |

| Energy-utility MVNOs cross-selling convergent bundles | +0.2% | Residential markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid nationwide 5G rollout accelerates network modernization

Telia switched on enough sites to reach 99% population coverage by December 2024, while Telenor followed at 90%, lifting median 5G download speeds to 255.6 Mbps and creating a decisive shift in consumer expectations. This coverage race, driven by spectrum-auction obligations, has catalyzed 1.6 million new 5G device connections and opened the door to higher-value enterprise solutions such as network slicing for the Norwegian Armed Forces.

Enterprise digitalization drives IoT connectivity expansion

Norway’s data economy generated NOK 150 billion (USD 14.2 billion) in 2024 and is forecast to double by 2030, as manufacturers deploy private 5G to enable automation and real-time quality control. Six dedicated mobile-network codes have already been issued for stand-alone non-public networks, underscoring swelling demand for secure, localized connectivity. Building-management specialist ClevAir has documented 40% energy savings using IoT sensors and analytics in commercial offices, showcasing tangible ROI for enterprises.

Government fiber broadband initiative expands rural access

The state earmarked NOK 415.6 million (USD 39.4 million) for 2025 broadband subsidies to close the rural connectivity gap, aligning with the Digital Norway target of universal 1 Gbps service by 2030. Municipal tenders stipulate open-access provisions, ensuring smaller ISPs can leverage newly built fiber and preventing market foreclosure.

Energy-utility convergence creates new revenue streams

Fjordkraft migrated 115,000 mobile customers to Telia’s network in 2023 in the largest inter-operator move in Norwegian history, proving the stickiness of dual electricity-mobile bundles and trimming customer acquisition costs by 30%. Lyse’s acquisition of Ice has similarly fused power distribution, fixed broadband and mobile into one platform, signaling deeper cross-industry competition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| >110% mobile penetration limiting organic subscriber growth | -0.5% | National; urban saturation | Short term (≤2 years) |

| Wholesale-access and price-regulation pressure on margins | -0.3% | National | Medium term (2-4 years) |

| Costly 2G/3G sunsets for legacy-device verticals | -0.4% | Industrial and safety sectors | Short term (≤2 years) |

| Rising cyber-sovereignty compliance costs | -0.2% | Enterprise services | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Market saturation constrains organic growth opportunities

SIM density above 110% has curtailed net-add potential, prompting operators to extract value through premium data tiers and bundled services. Norway remains the most expensive Nordic market on large data plans despite recent price cuts, sharpening regulator scrutiny.

Legacy network shutdown costs threaten short-term profitability

Ice began shuttering 2G in May 2025, with Telia to follow in August, forcing upgrades on an estimated 120,000 safety alarms and 35,000 elevators; device replacement bills risk topping NOK 600 million (USD 56.8 million) across impacted sectors. Government discussions of a postponement add planning uncertainty for operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data services cement revenue leadership

Data and Internet services commanded 48.02% of Norway telecom market share in 2025, buoyed by surging video streaming that now accounts for 70% of mobile traffic. They are projected to track a 3.15% growth curve, mirroring overall expansion. Voice services held 23.74% as VoLTE keeps margins resilient, while IoT and M2M rose fastest at a 3.29% clip, aided by private-network adoption. The Norway telecom market size tied to IoT is expected to expand steadily as advanced analytics unlock new industrial use cases.

Operators are already monetizing millimeter-wave 5G in dense areas, registering peak speeds near 4 Gbps. Fixed broadband retains strategic heft, with fiber in 38% of homes and a government mandate for 1 Gbps universal service by 2030. OTT and Pay-TV, alongside roaming and wholesale, maintain a steady 10.93% share thanks to bundled premium content.

By End-User: Enterprise momentum eclipses consumer growth

Enterprise revenues represented 28.95% of the Norway telecom market in 2025 but are growing faster, charting a 3.55% CAGR to 2031 on the back of Industry 4.0 investments. Demand for secure private 5G, edge services and regulated cloud storage positions operators to upsell beyond connectivity. The Norway telecom market size attributable to enterprise 5G is poised for outsized gains as factories deploy automated quality-inspection video and real-time robotics.

Consumers still account for 71.05% share due to ubiquitous mobile broadband and energy-utility bundles that reduce churn. Yet ARPU uplift is now anchored in 5G premium tiers, smart-home services and digital security add-ons introduced ahead of the Digital Security Act’s enforcement deadline in October 2025.

Geography Analysis

Norway’s fjords, mountains and Arctic latitudes shape a connectivity map unlike any other. The Oslo metropolitan area alone generated 37.62% of 2025 sector revenue, supported by the country’s first mmWave trials and dense enterprise clusters. Bergen and Trondheim followed as secondary poles, with Telenor posting 277 Mbps median mobile speeds in Trondheim for H2 2024, the highest nationwide. Rural districts from Finnmark to Innlandet are catching up on back-haul quality as NOK 415.6 million in 2025 fiber grants roll out new trenches and aerial links, ensuring universal 1 Gbps targets remain on track.

Coastal zones host an outsized share of offshore energy platforms that demand ultra-reliable links for safety systems and asset telemetry. Operators are extending microwave hops and satellite back-ups to these installations, cushioning against North Atlantic weather disruptions. In the Arctic, Telenor’s base station at the Norwegian Polar Institute demonstrates operational competence in sub-zero extremes while underlining national-security imperatives. Each of Norway’s 22 regional broadband markets flagged for “limited competition” now requires incumbent wholesale access, creating fresh room for challengers and community ISPs. Northern Norway exhibits the fastest projected 4.05% CAGR as Narvik’s 230 MW Stargate AI campus spurs incremental back-haul and data-center connectivity needs.

Competitive Landscape

Norway supports three infrastructure-based mobile players that collectively commanded 82% of 2024 subscriptions, suggesting moderate concentration. Telenor remains market leader with 2.7 million subscribers, highest ARPU and the nation’s best network reliability scores. Telia closed the coverage gap by achieving 99% 5G reach ahead of schedule, stealing enterprise accounts thanks to its network-as-a-service model. Ice, now under Lyse, targets the value segment and is on track for 1 million mobile lines by 2025 after buying 10,000 Release customers in 2024[3]NTB Communication, “Ice Kjøper 10 000 Release-Kunder,” kommunikasjon.ntb.no.

Strategic differentiation hinges on vertical solutions, cloud integration and cybersecurity. Telenor’s merger with Jottacloud forms a sovereign storage alternative expected to bring in NOK 200 million revenue in 2025. Telia is trialing mmWave FWA to defend urban broadband share, while Ice leverages Mavenir’s 5G core to offer network-slicing for defense clientele. Energy majors are now credible telecom contenders: Lyse fuses electricity, fiber and mobile; Fjordkraft bundles power with mobile to reinforce loyalty, and Aker’s Stargate Norway venture requires carrier-grade connectivity into its GPU “gigafactory”.

Regulatory policy insists on preserving three robust networks; hence the next spectrum auctions will likely be structured to prevent consolidation. Wholesale obligations on both fixed and mobile assets are tightening, promoting MVNO-led price discipline without compromising infrastructure investment.

Norway Telecom MNO Industry Leaders

Telenor Group

Telia Company AB

Ice Communication

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Parliament passed the Digital Security Act, aligning with NIS2 and imposing fines up to 4% of turnover on telcos for cybersecurity lapses.

- April 2024: The Norwegian Government has put forth amendments to the Electronic Communications Act, proposing a series of changes. These changes encompass mandating data centers to register, bolstering consumer rights by ensuring transparent and non-discriminatory subscriber agreements, guaranteeing equal communication services for individuals with disabilities, providing a three-month grace period of free email access post-switching email providers, mandating GDPR-compliant consent for cookies, emphasizing universal broadband access, and fortifying security measures for electronic communication services and networks.

- May 2025: Ice kicked off its 2G shutdown, offering discounted 4G/5G devices to affected users.

- May 2025: Telenor reported NOK 16.1 billion Q1 service revenue, a 2.1% YoY rise, citing Nordic strength.

- April 2025: Telia confirmed a phased 2G decommission starting August 2025 in Buskerud County.

Norway Telecom MNO Market Report Scope

Two pivotal technologies, the Internet and mobile telephony, underpin Norway's digital economy. The country stands as a trailblazer in both developing and embracing these technologies. With a surging appetite for services like OTT, pay-TV, data, messaging, and voice, the demand for telecom services in Norway is on a steady rise. Moreover, providers of enhanced connectivity services are fast-tracking the digital evolution for countless customers nationwide.

The Norway telecom market is segmented by applications (voice services [wired and wireless], data and messaging services, and OTT and pay-TV services). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What segment is expanding the quickest?

IoT and M2M connectivity is the fastest-growing segment at a 3.29% CAGR through 2031 as enterprises adopt private 5G networks.

How will the 2G shutdown affect businesses?

Around 120,000 safety alarms and 35,000 elevators require upgrades, raising near-term costs but accelerating migration to modern LPWA and 5G devices.

Which operator has the widest 5G coverage?

Telia reached 99% population coverage by December 2024, setting the benchmark for national network reach.

What new regulations should telecom firms watch in 2025?

The Digital Security Act takes effect in October 2025, mandating stringent cybersecurity controls with potential fines of up to 4% of annual turnover.

Page last updated on: