Polymerase Chain Reaction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

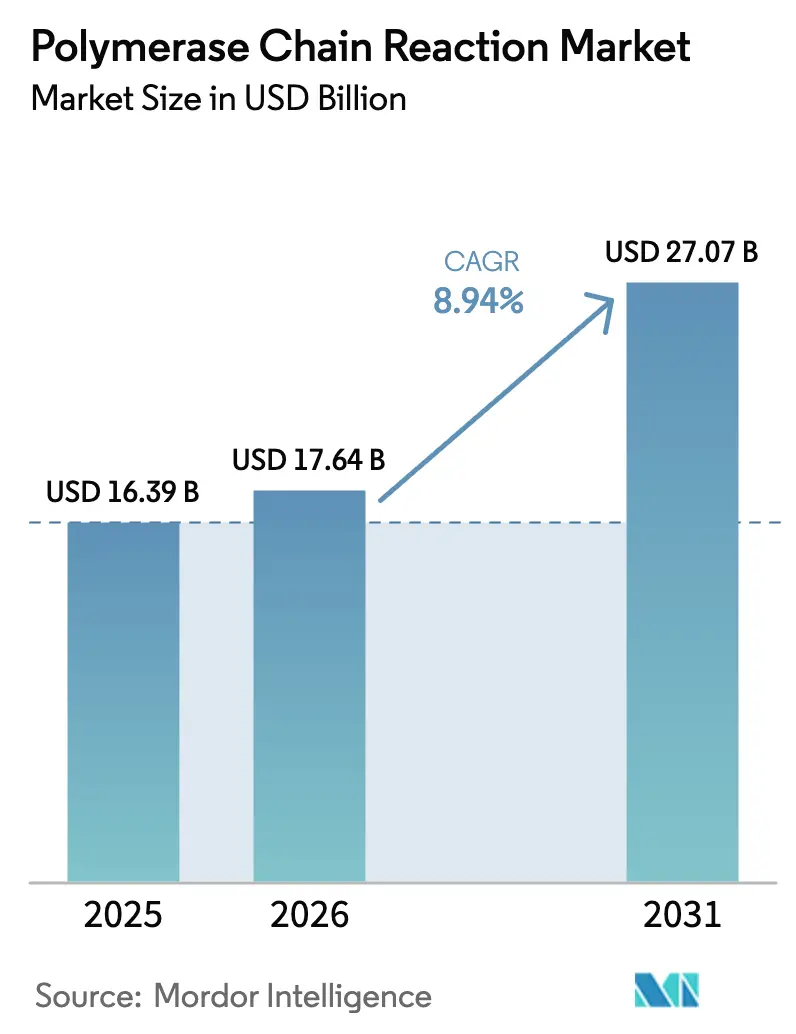

| Market Size (2026) | USD 17.64 Billion |

| Market Size (2031) | USD 27.07 Billion |

| Growth Rate (2026 - 2031) | 8.94% CAGR |

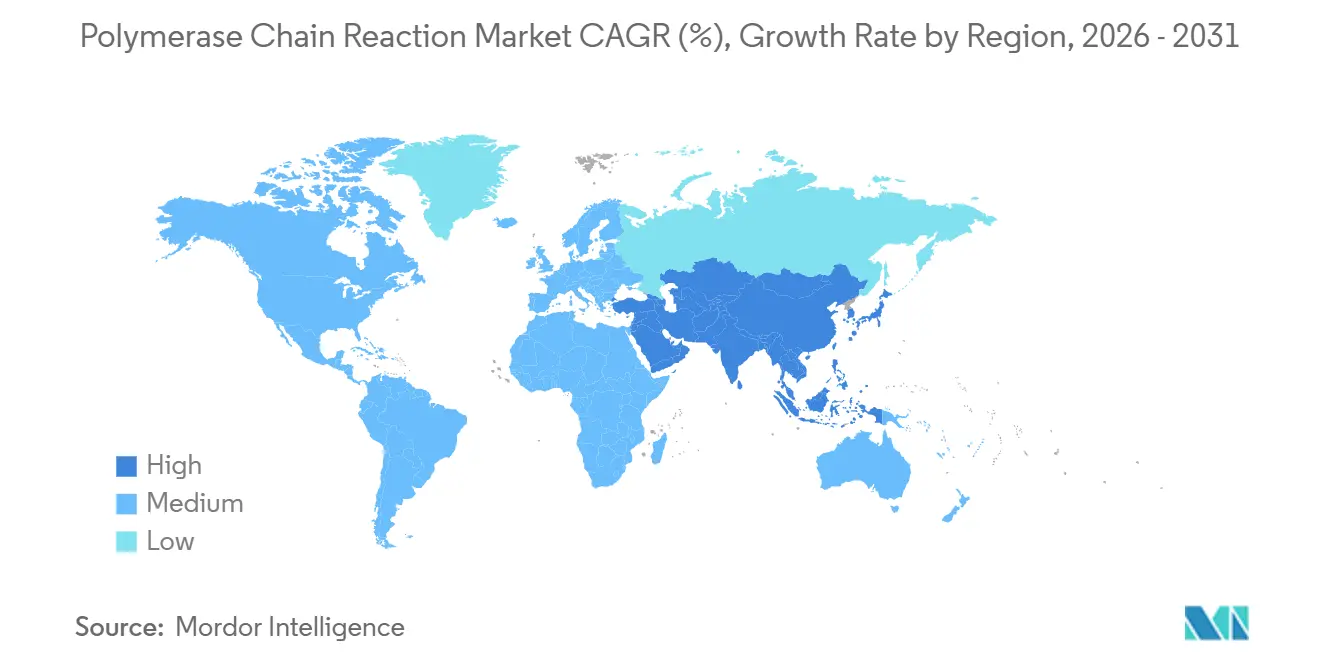

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

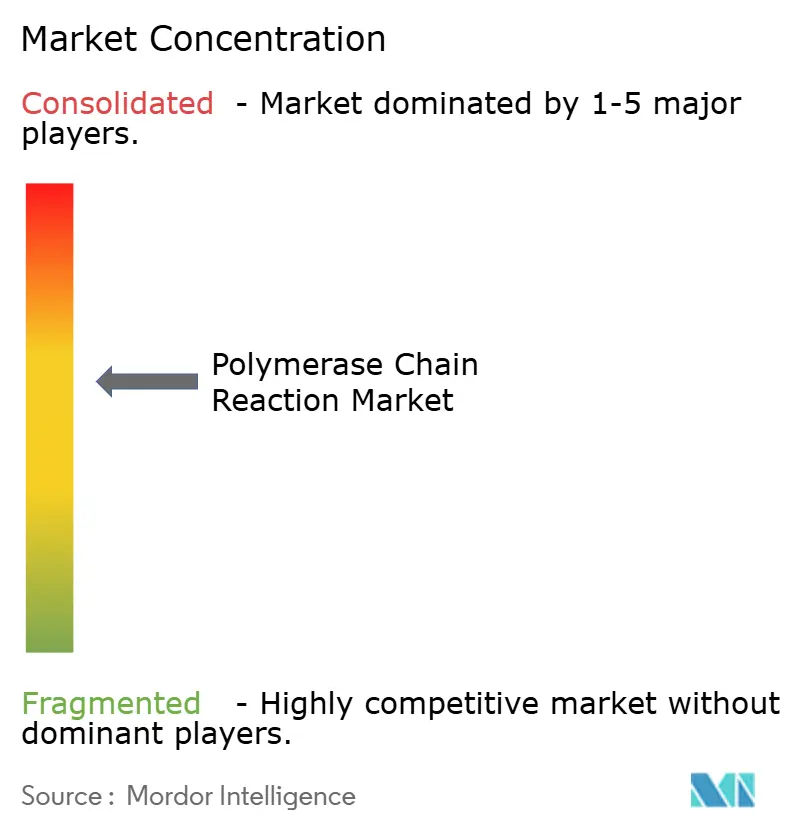

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polymerase Chain Reaction Market Analysis by Mordor Intelligence

The Polymerase Chain Reaction Market size is expected to increase from USD 16.39 billion in 2025 to USD 17.64 billion in 2026 and reach USD 27.07 billion by 2031, growing at a CAGR of 8.94% over 2026-2031.

Durable pandemic-era laboratory networks now underpin routine precision diagnostics, agricultural biosecurity, and forensic workflows, keeping instrument utilization high and broadening end-market exposure. Reagents and consumables remain the economic engine, yet cloud analytics and AI-driven assay design tilt differentiation toward software and services that integrate seamlessly with legacy cyclers. Real-time quantitative instruments dominate installed bases, but digital PCR is migrating rapidly into liquid-biopsy protocols where single-molecule resolution supports premium reimbursement. Regulatory momentum, especially the FDA’s 2024 laboratory-developed test rule, favors turnkey kits over bespoke assays, prompting laboratories to reassess build-versus-buy decisions. Meanwhile, sustainability levies on single-use plastics in the EU nudge laboratories toward reusable plate systems, reshaping consumable demand without curbing overall test volumes.

Key Report Takeaways

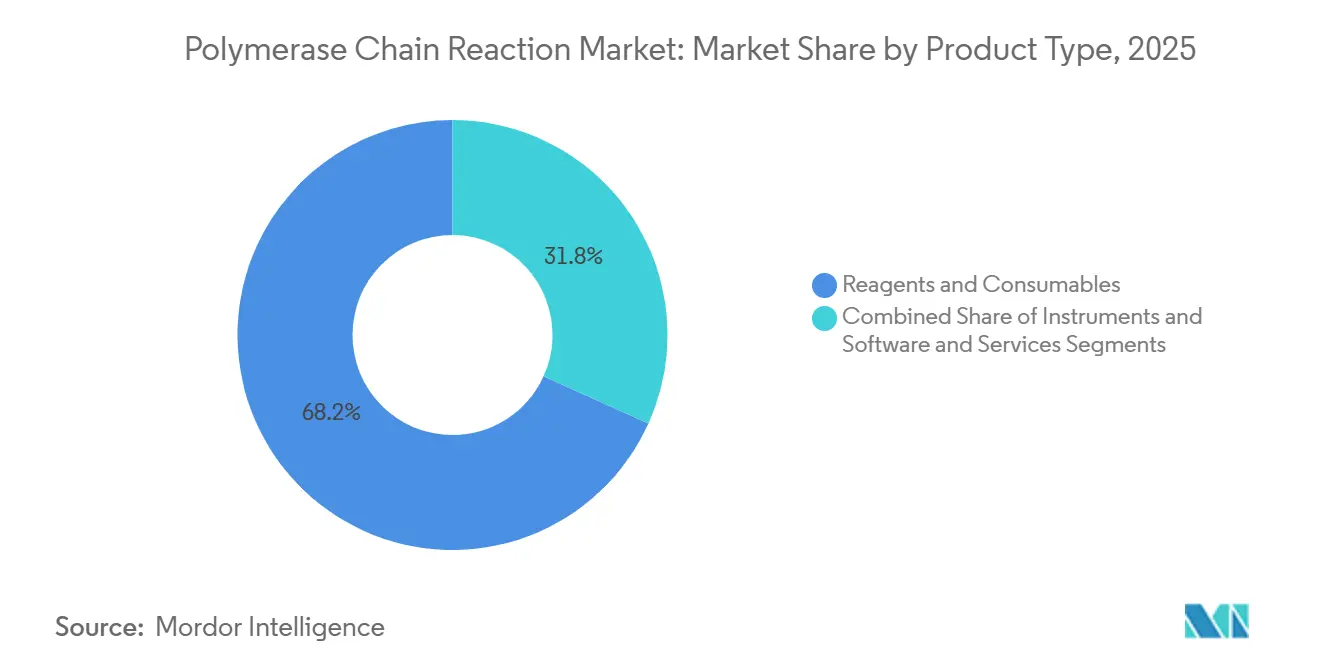

- By product type, reagents and consumables led with 68.24% revenue share in 2025, while software and services are projected to expand at an 11.97% CAGR through 2031.

- By technology, real-time quantitative PCR commanded 54.84% of 2025 revenue; digital PCR is forecast to grow at a 12.73% CAGR to 2031.

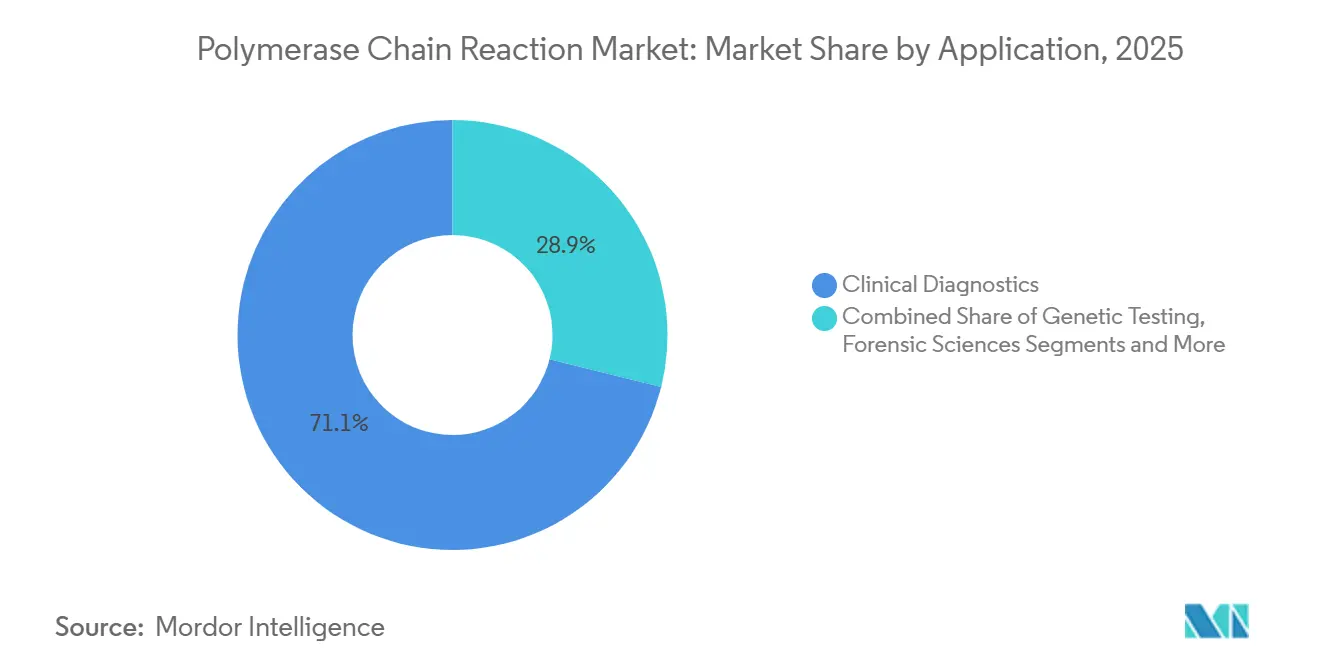

- By application, clinical diagnostics held 71.12% of 2025 revenue, whereas environmental and food testing is poised for an 11.42% CAGR through 2031.

- By indication, infectious diseases accounted for 42.48% share in 2025, yet oncology and liquid biopsy is expected to advance at a 10.53% CAGR during 2026-2031.

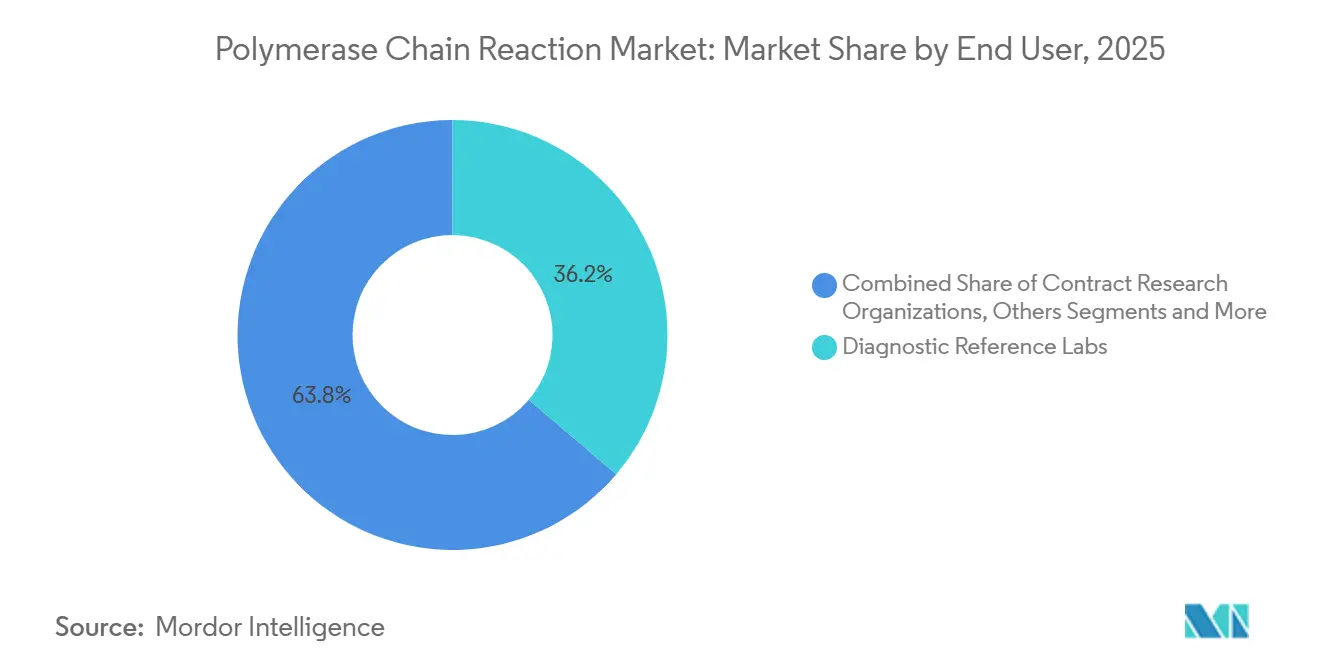

- By end user, diagnostic reference laboratories captured 36.22% revenue share in 2025; contract research organizations are set to rise at a 13.52% CAGR over the forecast period.

- By geography, North America retained 38.41% share in 2025, while Asia-Pacific is projected to log the fastest 11.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polymerase Chain Reaction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Infectious-Disease Testing Post-COVID | +1.8% | Global, with peak demand in APAC and Sub-Saharan Africa | Medium term (2-4 years) |

| Rising Oncology & Genetic-Disorder Diagnostics Demand | +1.5% | North America & EU, expanding to APAC urban centers | Long term (≥ 4 years) |

| Technological Advances in qPCR & dPCR Platforms | +1.3% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Increased Life-Science R&D & Personalized-Medicine Funding | +1.2% | North America, EU, China | Long term (≥ 4 years) |

| AI-Driven Assay Design & Cloud-Based Analytics Adoption | +0.9% | North America & EU core, gradual APAC uptake | Long term (≥ 4 years) |

| Field-Deployable Microfluidic PCR for Agri-Biosecurity | +0.6% | APAC agriculture hubs, Latin America, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Infectious-Disease Testing Post-COVID

Respiratory-virus surveillance built during the pandemic now functions as a permanent safeguard, sustaining demand across the polymerase chain reaction market.[1]World Health Organization, “Global Influenza Surveillance and Response System Expands to 158 National Laboratories,” World Health Organization, who.int The CDC’s USD 3 billion Respiratory Virus Response program funds state laboratories to expand multiplex qPCR panels that detect influenza, SARS-CoV-2, and RSV in one run.[2]Centers for Disease Control and Prevention, “CDC Launches USD 3 Billion Respiratory Virus Response Program to Modernize State PCR Capacity,” Centers for Disease Control and Prevention, cdc.gov January 2026 FDA clearance for Cepheid’s six-pathogen gastrointestinal cartridge demonstrates that sample-to-answer systems can rival central labs in menu breadth. Decentralized testing therefore redistributes revenue toward integrated consumables while keeping total reaction volumes high. Together, these forces secure a stable baseline for the polymerase chain reaction market, cushioning it against cyclical downturns in elective procedures.

Rising Oncology & Genetic-Disorder Diagnostics Demand

Liquid-biopsy PCR assays monitor minimal residual disease and therapy resistance, validated by the FDA’s March 2025 label expansion of Roche’s cobas EGFR Mutation Test v2. Companion-diagnostic approvals link PCR biomarkers to targeted therapies, embedding the technology in drug-development economics and bolstering polymerase chain reaction market growth. Expanded newborn screening for spinal muscular atrophy and severe combined immunodeficiency widens routine testing volumes, while uneven reimbursement spurs vendors to bundle assays with pharmaceutical partners willing to subsidize testing to enlarge treatable patient pools.

Technological Advances in qPCR & dPCR Platforms

Bio-Rad’s QXDx AutoDG, launched July 2025, automates droplet generation and cuts hands-on time below 10 minutes per 96-well plate. QIAGEN’s QIAcuity platform became the first nanoplate-based dPCR cleared by the FDA in March 2025. Six-color detection on Roche’s LightCycler PRO enables concurrent quantification of viral load, host markers, and internal controls without sensitivity loss. ISO 20395:2024 now harmonizes validation criteria, reducing time-to-market for multiplex assays.[3] International Organization for Standardization, “ISO 20395:2024 Biotechnology—Requirements for Evaluating qPCR and dPCR Performance,” International Organization for Standardization, iso.org Workflow simplification means dPCR no longer requires PhD-level expertise, propelling adoption in community oncology centers and boosting polymerase chain reaction market size across mid-tier hospitals.

AI-Driven Assay Design & Cloud-Based Analytics Adoption

Thermo Fisher’s Design Studio AI screens 10 million primer combinations in minutes, shrinking assay-development cycles and lowering entry barriers for niche panels. Roche’s navify platform overlays PCR readouts onto histology images, offering integrated molecular-pathology dashboards that pathologists access remotely. Pending European Health Data Space rules enforce interoperability yet tighten consent requirements, driving vendors toward federated-learning architectures that train algorithms without transferring raw PCR curves. These advances move value from plasticware to software subscriptions, a shift that sustains margin expansion within the polymerase chain reaction market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Consumable Costs | -1.1% | Emerging markets in APAC, MEA, Latin America | Short term (≤ 2 years) |

| Competition from NGS & Isothermal Amplification | -0.8% | Global, most acute in oncology and research segments | Medium term (2-4 years) |

| Sustainability Taxes on Single-Use PCR Plastics (EU) | -0.5% | EU member states, potential spillover to UK and Canada | Short term (≤ 2 years) |

| GDPR Limits on Cloud PCR Data-Sharing | -0.4% | EU, with indirect effects on multinational biobanks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Consumable Costs

Digital PCR instruments list at USD 80,000-150,000, while annual service and reagents add USD 25,000-40,000 for mid-volume sites, constraining uptake in lower-income regions. Generic master mixes undercut branded reagents by up to 40%, but bundled purchasing locks many labs into proprietary ecosystems that resist price competition. Leasing and reagent-rental options spread costs yet impose minimum-volume thresholds that punish laboratories during seasonal demand dips, limiting polymerase chain reaction market penetration in frontier economies.

Competition from NGS & Isothermal Amplification

Illumina’s FDA-cleared TruSight Oncology 500 profiles 523 genes in three days at costs approaching targeted PCR panels, eroding PCR’s oncology moat. Isothermal methods eliminate thermal cyclers, driving instrument prices below USD 5,000 and opening true point-of-care niches. PCR retains speed and quantification precision for single-gene assays, but hybrid workflows that pair sequencing for discovery with PCR for longitudinal monitoring are narrowing incremental gains for older qPCR platforms across the polymerase chain reaction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables Dominate while Software Surges

Reagents and consumables produced 68.24% of 2025 revenue, reflecting razor-and-blade economics embedded in the polymerase chain reaction market. Proprietary master mixes command sticky margins, though generic alternatives have seized 12-15% share in price-sensitive regions, compressing profits. Closed-system cartridges guarantee pull-through yet face sustainability taxes in the EU, spurring a pivot toward plate-reuse programs and biodegradable plastics. Instruments growth moderates as replacement cycles lengthen to 8-10 years, but installed-base saturation secures steady consumable demand.

Software and services are forecast to grow at 11.97% CAGR through 2031, outpacing hardware as laboratories prioritize traceability, automated compliance, and multi-site data integration. Annual cloud-dashboard subscriptions of USD 15,000-50,000 per lab carry gross margins above 70%, shifting profit pools toward informatics and bolstering overall polymerase chain reaction market size. Outcome-based contracts that charge per reportable result also align vendor incentives with laboratory throughput, embedding long-term annuity streams.

By Technology: Digital PCR Accelerates as qPCR Plateaus

Real-time quantitative platforms delivered 54.84% of technology revenue in 2025, anchoring routine diagnostics due to widespread CPT codes and technician familiarity. However, incremental fluorescence-channel upgrades no longer spur large-scale fleet replacements, leaving qPCR growth near clinical-market averages. Digital PCR, by contrast, will climb at a 12.73% CAGR through 2031, leveraging single-molecule resolution that justifies premium coverage for minimal-residual-disease testing and transplant-rejection surveillance. Hybrid instruments that toggle between qPCR and dPCR modes preserve capital budgets and future-proof menus, nudging conservative labs toward partial digital adoption.

Multiplex PCR expands as regulators approve syndromic panels detecting up to 22 pathogens, shortening diagnostic odysseys and curbing empiric antibiotic use. Conventional endpoint PCR persists in forensic and veterinary settings where quantification is unnecessary and budget constraints dominate. Together these shifts maintain a healthy polymerase chain reaction market even as qPCR growth decelerates.

By Application: Clinical Diagnostics Anchor while Environmental Testing Gains Pace

Clinical diagnostics accounted for 71.12% of application revenue in 2025, driven by persistent infectious-disease mandates and expanding oncology companion diagnostics. Hospitals and reference labs rely on qPCR for respiratory and gastrointestinal pathogens where same-day results guide therapy. Yet payer scrutiny is rising; Medicare bundled payments trimmed respiratory-panel reimbursement 12% in 2025, pushing labs to chase efficiency gains to protect margins.

Environmental and food testing is projected to advance at an 11.42% CAGR through 2031 as the Food Safety Modernization Act Section 204 requires PCR-based traceability for high-risk foods from January 2026. EU wastewater directives mandate PCR monitoring of antibiotic-resistance genes by 2027, prompting municipal tenders for 96-well automation. Agricultural and veterinary users adopt portable cyclers for border inspection of African swine fever and avian influenza, further diversifying revenue across the polymerase chain reaction market.

By Indication: Infectious Diseases Lead while Oncology Builds Momentum

Infectious diseases generated 42.48% of 2025 indication revenue, underscoring PCR’s entrenched role in tuberculosis, HIV, and multi-virus respiratory testing. Routine surveillance delivers stable consumable pull-through, though payer compression signals commoditization risk. Oncology and liquid biopsy are expanding at a 10.53% CAGR, aided by circulating-tumor-DNA panels reimbursing at USD 500-1,500 per test and FDA recognition of PCR-measured minimal-residual disease as a valid endpoint. Genetic-disorder screening in newborns and pharmacogenomics panels for pain management add incremental volumes, sustaining upward momentum for the polymerase chain reaction market.

By End User: Reference Labs Dominate, CROs Surge

Diagnostic reference laboratories held 36.22% of end-user revenue in 2025 by leveraging economies of scale and nationwide logistics that hospitals cannot replicate. ISO 15189 accreditation and 24-hour turnaround attract complex oncology send-outs, yet payer bundling squeezes margins, pushing labs toward high-value digital assays and AI triage tools. Contract research organizations are forecast to grow at a 13.52% CAGR through 2031 as pharmaceutical sponsors outsource PCR-based biomarker validation to compress development timelines, commanding price premiums for 48-hour data delivery. Hospitals invest selectively in point-of-care cyclers for emergency departments, but low daily volumes limit ROI on advanced dPCR setups, highlighting the segmented nature of demand within the polymerase chain reaction market.

Geography Analysis

North America retained 38.41% of 2025 revenue, the highest regional polymerase chain reaction market share worldwide. Medicare reimbursement expansions and over 260,000 CLIA-certified labs keep consumable demand robust. The FDA’s laboratory-developed test rule increases demand for pre-validated kits, while Canada’s Pan-Canadian Health Data Strategy standardizes PCR menus and procurement, enhancing bulk-buy leverage. Mexico earmarked USD 700 million in 2025 to upgrade rural molecular labs, expanding infectious-disease coverage and reagent pull-through.

Europe grows steadily but confronts 8-12% plastics levies under the EU Single-Use Plastics Directive, adding cost pressure for labs clinging to disposable plates. Germany and France reimburse digital PCR for circulating-tumor DNA, stimulating premium-test volumes, while the UK’s National Health Service rolled out PCR-based pharmacogenomics in primary care in 2025, reducing adverse-drug reactions. GDPR’s data-transfer limits, however, slow multinational biobank collaborations, delaying AI model training that depends on pooled PCR curves.

Asia-Pacific is projected to post an 11.22% CAGR through 2031, the fastest worldwide. China’s Healthy China 2030 dedicates USD 126 billion to precision-medicine infrastructure, including regional PCR hubs linked via telemedicine. India’s National Health Mission deployed 1 200 GeneXpert instruments to district hospitals between 2024 and 2025, raising tuberculosis PCR coverage to 72%. Japan approved liquid-biopsy PCR reimbursement for colorectal and gastric cancers in April 2025, adding around 180 000 eligible patients a year. South Korea aggregates PCR results from 350 hospitals onto a national cloud, while Australia halves assay-approval timelines, accelerating vendor entry. Outside core economies, GCC states, South Africa, and Brazil invest in PCR for epidemic control, but technician shortages and power instability limit throughput in parts of Africa and Latin America, tempering polymerase chain reaction market size gains.

Regulatory Landscape

In the United States, FDA actions are tightening the compliance envelope for PCR-based diagnostics through both device classification updates and quality-system modernization. The FDA LDT final rule (published May 6, 2024) began its staged phaseout of enforcement discretion on May 6, 2025, pushing laboratories to reassess build-versus-buy decisions and increasing the value of pre-validated PCR kits with established device submissions.

On manufacturing and market-access requirements, the FDA Quality Management System Regulation (QMSR), which incorporates ISO 13485:2016 by reference, became fully effective in February 2026, increasing emphasis on harmonized QMS documentation across global supply chains. Separately, a new FDA classification for a simple point-of-care device to directly detect SARS-CoV-2 viral targets (21 CFR 866.3982) became effective June 11, 2026, reinforcing the regulatory pathway clarity for certain rapid nucleic-acid detection systems. In Europe, the EU IVDR (Regulation (EU) 2017/746) governs PCR IVDs and companion diagnostics, with notified body conformity assessment and consultation frameworks involving authorities such as the EMA; for Class C devices, a key transition milestone occurs by May 26, 2026, shaping how legacy PCR assays are maintained or converted to IVDR-compliant dossiers.

Value Chain Analysis

The PCR value chain starts upstream with specialty biochemical inputs (recombinant polymerases, dNTPs, buffers, dyes/probes, and oligonucleotides), alongside medical-grade plastics for plates, tubes, and cartridges. Enzyme production relies on high-yield microbial fermentation (commonly E. coli), and consumables manufacturing is exposed to concentrated polypropylene supply, which can translate into extended lead times, notably for plates. These upstream constraints flow into midstream formulation, fill-finish, and packaging, where cold-chain distribution for master mixes raises landed costs and increases complexity for global distribution.

Downstream, OEMs and assay developers integrate instruments (qPCR and dPCR), assay kits, and informatics into validated workflows sold through direct sales, distributors, and channel partners serving clinical laboratories, reference labs, CROs, and food/environmental testing customers. Recent partnering activity highlights a value-chain shift toward end-to-end workflow bundles and co-developed menus: Cepheid expanded a partnership with Oxford Nanopore in April 2026 to develop a rapid pathogen identification workflow, with an early access program planned for Q3 2026, while Countable Labs and Promega announced a co-marketing agreement in June 2026 linking extraction (Promega Maxwell) with PCR instrumentation. In parallel, collaborations such as EDGC and Targetnos (May 2026) to validate and commercialize digital PCR-based NIPT signal point to growing emphasis on specialized clinical applications that require coordinated assay design, validation, and commercialization across multiple tiers.

Competitive Landscape

The polymerase chain reaction market is consolidated yet still contestable. Thermo Fisher filed 14 digital-PCR patents in 2024-2025 targeting multiplexing and automated partitioning, signaling a bid to erode Bio-Rad’s droplet dominance. Roche’s 2024 integration of GenMark’s ePlex system extends its sample-to-answer menu into emergency departments. QIAGEN’s Sample to Insight contract, launched January 2025, charges per reportable result, forging annuity-style cash flows. Abbott re-entered women’s health panels when its Alinity m STI assay gained CE-IVD status in December 2024, reclaiming European share.

Mid-tier challengers exploit white space. Stilla Technologies’ Naica crystal partitions offer ultra-precise minimal-residual-disease testing prized by oncology centers. Syndex Bio unveiled mcPCR in February 2026, promising methylation detection without bisulfite conversion, potentially shortening lab workflows. In India, CoSara secured CDSCO clearance for its PCR Pro point-of-care cycler, pairing local manufacturing with reagent-rental models that undercut multinationals. Generic master-mix producers in China and India sell at 40-50% discounts, forcing branded firms to differentiate via technical support and regulatory dossiers.

Regulation shapes rivalry. The FDA’s laboratory-developed test rule phases out enforcement discretion by 2028, compelling reference labs to buy commercial kits or run full clinical trials—an advantage for suppliers with turnkey portfolios. ISO 15189:2022 tightens documentation standards, steering purchasing toward vendors offering plug-and-play quality-system templates. Sustainability pressures in the EU spur pilots of reusable aluminum PCR blocks, a trend incumbents monitor before investing in new tooling. Meanwhile, sequencing firms hedge by launching targeted PCR panels, blurring technology lines and intensifying cross-category competition within the polymerase chain reaction market.

Polymerase Chain Reaction Industry Leaders

Abbott Laboratories

Thermo Fisher Scientific Inc.

Bio-Rad Laboratories

F. Hoffmann-La Roche Ltd

QIAGEN N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory and standardization anchors are creating clear whitespace for vendors that can deliver compliant, turnkey PCR workflows. The FDA QMSR (fully effective February 2026) increases the premium on ISO 13485-aligned quality systems for IVD manufacturers, while the EU IVDR framework and associated EUDAMED requirements (with key modules becoming mandatory from 28 May 2026) reinforce demand for robust technical documentation, post-market processes, and traceability across PCR kits, software, and connected workflows. Alongside ISO 20395:2024 performance evaluation requirements for qPCR and dPCR, these shifts support opportunities in validated multiplex panels, companion diagnostics, and laboratory adoption of software layers that streamline auditability and multi-site standardization.

Capacity build-outs and partnership activity also points to where new spending concentrates. bioMerieux announced a EUR 250 million investment (May 2026) in a new facility in La Balme-les-Grottes, France to manufacture BIOFIRE molecular diagnostics for the European market, reinforcing localized supply and expanding output for sample-to-answer PCR workflows. Integrated DNA Technologies completed an April 2026 expansion in Coralville, Iowa, tripling oligonucleotide synthesis capacity and supporting assay development and high-volume molecular workflows that depend on primers and probes. Platform and workflow partnerships such as Cepheid and Oxford Nanopore (April 2026), together with dPCR clinical collaborations (for example, digital PCR-based NIPT validation programs), create opportunities in integrated sample prep-to-result solutions, higher-plex dPCR applications (oncology MRD, prenatal and rare variant detection), and informatics subscriptions that connect PCR outputs to clinical decision support and remote review.

Recent Industry Developments

- June 2026: Countable Labs and Promega announced a co-marketing agreement linking Promega Maxwell extraction with PCR instrumentation, enabling integrated sample prep-to-result workflows for high-throughput molecular testing. The arrangement expands end-to-end automation in molecular labs and aligns consumables with instrument ecosystems, potentially boosting demand for Maxwell kits and compatible PCR assays.

- May 2026: EDGC and Targetnos announced a collaboration to validate and commercialize digital PCR-based NIPT signal, expanding access to high-sensitivity prenatal testing workflows. The partnership emphasizes coordinated assay design and validation across digital PCR platforms to enable scalable NIPT testing in clinical settings.

- May 2026: BioMerieux announced a EUR 250 million investment in a new BIOFIRE manufacturing facility in La Balme-les-Grottes, France to support European demand for sample-to-answer molecular diagnostics. The project strengthens localized supply chains and increases output for European PCR workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from polymerase chain reaction tools used to amplify DNA or RNA for testing and analysis, across clinical and non-clinical uses. It includes core PCR workflows that rely on instruments, reagents and consumables, and related enabling software and services.

Scope exclusions: Outsourced PCR testing service labor and bundled sequencing platform revenues are excluded from the market totals.

Segmentation Overview

- By Product Type

- Instruments

- Reagents & Consumables

- Software & Services

- By Technology

- Conventional / Standard PCR

- Real-Time / qPCR

- Digital PCR

- Multiplex & Other PCR

- By Application

- Clinical Diagnostics

- Genetic Testing

- Drug Discovery & Research

- Forensic Sciences

- Environmental & Food Testing

- Agricultural & Veterinary

- By Indication

- Infectious Diseases

- Oncology & Liquid Biopsy

- Genetic Disorders

- Other Indications

- By End User

- Hospitals & Clinics

- Diagnostic Reference Labs

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Contract Research Organizations

- Forensic & Security Agencies

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the guardrails for what should be counted, and to build the starting demand picture by region and end user. We referenced public health and lab testing statistics, such as the US CDC and WHO, along with FDA device databases and safety notices, to understand how widely PCR platforms were adopted and how product cycles typically evolve.

To keep assumptions grounded, we also reviewed sources such as NIH and PubMed for publication trends that indicate research intensity. Where available, we used trade and shipment indicators from customs statistics to track instruments and key consumables. Company annual reports, investor decks, and reputable press coverage were used to cross-check product mix changes and the direction of pricing, and then selective paid databases for company financials and patents helped validate supplier coverage and ongoing technology activity. These examples are not exhaustive, and we also consulted other public and paid sources to support data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on cross-checking PCR demand drivers in diagnostics and research, then pressure-testing model inputs that desk research cannot fully confirm. We spoke with a mix of instrument suppliers, reagent and consumable stakeholders, lab managers, and procurement and quality teams across APAC, EMEA, and the Americas, to validate adoption rates, replacement cycles, and realistic price movement by workflow type.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 18% | APAC: 44% |

| Mid tier: 51% | Functional/Unit leaders: 33% | EMEA: 37% |

| Smaller Players: 18% | Managers: 49% | Americas: 19% |

Market-Sizing & Forecasting

Our sizing logic starts with a top-down build where lab activity and testing demand are reconstructed into an addressable PCR demand pool, then translated into spend using workflow level pricing. We corroborate results through selective bottom-up approximations, such as sampling instrument placements, applying typical consumables attachment rates, and running channel checks on average selling price ranges to adjust totals where needed.

Key model inputs included reported molecular testing volumes, the share of tests and research protocols that rely on PCR, instrument installed base and replacement timing, average run frequency in high throughput settings, and consumables usage per run (including assay intensity differences between clinical diagnostics and research). For forecasts, scenario analysis was used so upside and downside cases reflect changes in infectious disease testing intensity, research funding signals, and the pace of workflow automation that interviewees expect. Where supplier level visibility was thin in certain countries, gaps were handled through proxy penetration rates tied to lab count, import trends, and healthcare and research spending indicators, and then re-checked with local expert feedback.

Data Validation & Update Cycle

Validation is done through multiple checks so the final outputs stay consistent with real-world signals. Model results are compared against independent indicators like instrument shipment direction, test volume trends, and regional spend capacity, and then large variances are investigated before sign-off.

When an anomaly shows up, assumptions are revisited and respondents are re-contacted to confirm whether the issue is scope, pricing, timing, or a sudden demand shift. Reports are refreshed annually, and interim updates are made when material events occur, such as regulatory actions, major reimbursement changes, or sudden outbreaks. Before delivery, a final analyst pass is completed so clients receive an updated view aligned to the latest available data.

Mordor Intelligence's Polymerase Chain Reaction Market Size Measured Against Other Published Estimates

Published PCR market sizes do not always align, even when the headline topic looks identical. The differences usually come from what is counted in the product basket, how COVID-era testing peaks are treated, and how quickly assumptions like pricing and installed base are updated.

Some sources treat the PCR space as a narrower basket centered on instruments plus core reagents and consumables, which can pull totals down in the early years. In Mordor Intelligence, outsourced PCR testing service labor and sequencing platform bundles are not counted, so the number reflects standalone PCR workflow revenue that can be traced back to instrument placement, run intensity, and consumables usage by end user.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.39 B (2025) | |

| Global Consultancy A | USD 10.75 B (2025) | Uses a tighter product scope focused mainly on instruments and reagents/consumables, and it can also smooth post-pandemic demand more conservatively, which reduces the near-term total versus a workflow-based spend build. |

| Industry Research Group B | USD 10.89 B (2024) | Anchors sizing on a different base year and often emphasizes type level segmentation without clearly separating one-time COVID testing surges from recurring lab run rates, which can shift the starting point and the implied pricing path. |

Taken together, the spread is mostly explained by what gets included in the counted revenue pool, the base year selected, and how fast pricing and usage rates are updated. By tying the total back to observable demand signals like test volume, installed base movement, and consumables attachment, the model stays transparent and repeatable even when certain inputs must be proxied.

Key Questions Answered in the Report

How fast is global demand for polymerase chain reaction products expected to grow through 2031?

Total revenue is forecast to advance at an 8.94% CAGR from 2026 to 2031, moving from USD 17.64 billion to USD 27.07 billion.

Which product group delivers the highest recurring revenue for laboratories?

Reagents and consumables provided 68.24% of 2025 sales, reflecting razor-and-blade economics that drive steady cash flow.

Why is digital PCR gaining more clinical traction lately?

Single-molecule resolution supports premium reimbursement in liquid-biopsy monitoring, helping digital formats post a projected 12.73% CAGR through 2031.

What regulation is reshaping U.S. reference-lab purchasing decisions?

The FDA’s 2024 rule ending enforcement discretion for laboratory-developed tests pushes labs toward pre-validated commercial PCR kits.

Which region shows the fastest projected growth?

Asia-Pacific is expected to expand at an 11.22% CAGR, buoyed by China’s Healthy China 2030 funding and India’s nationwide GeneXpert rollout.

How are sustainability policies affecting European laboratories?

The EU Single-Use Plastics Directive adds 8-12% fees to disposable PCR plates, prompting a shift to reusable blocks and closed cartridges.

Page last updated on: