Enzyme Replacement Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

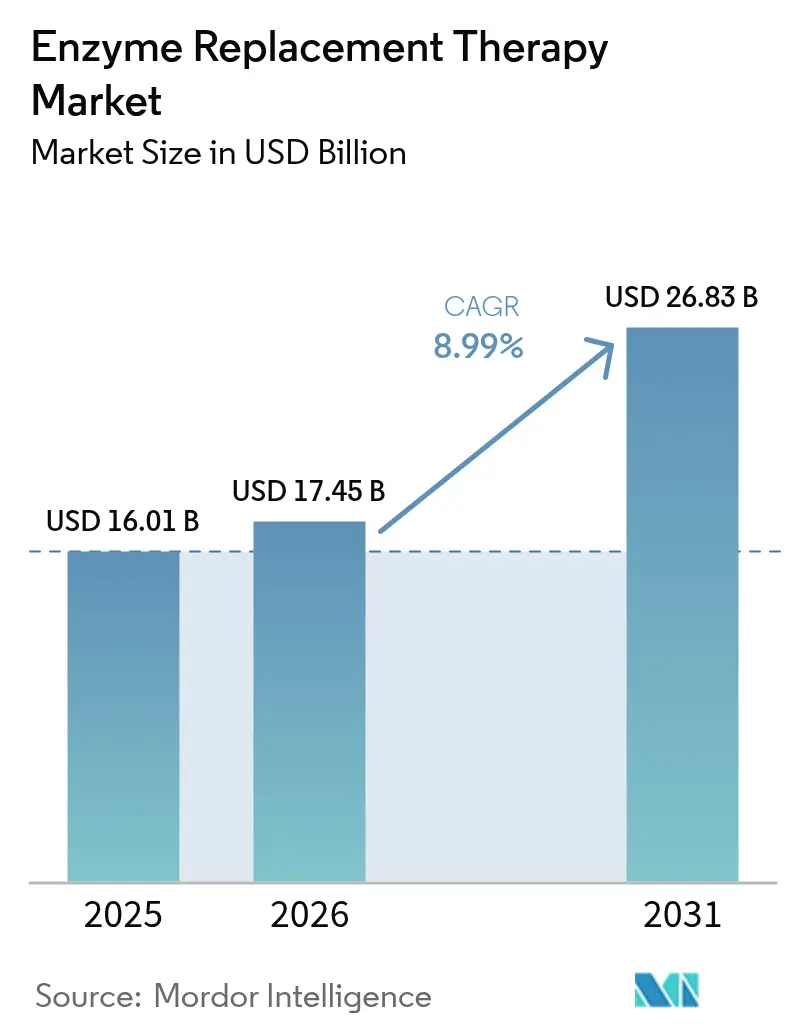

| Market Size (2026) | USD 17.45 Billion |

| Market Size (2031) | USD 26.83 Billion |

| Growth Rate (2026 - 2031) | 8.99% CAGR |

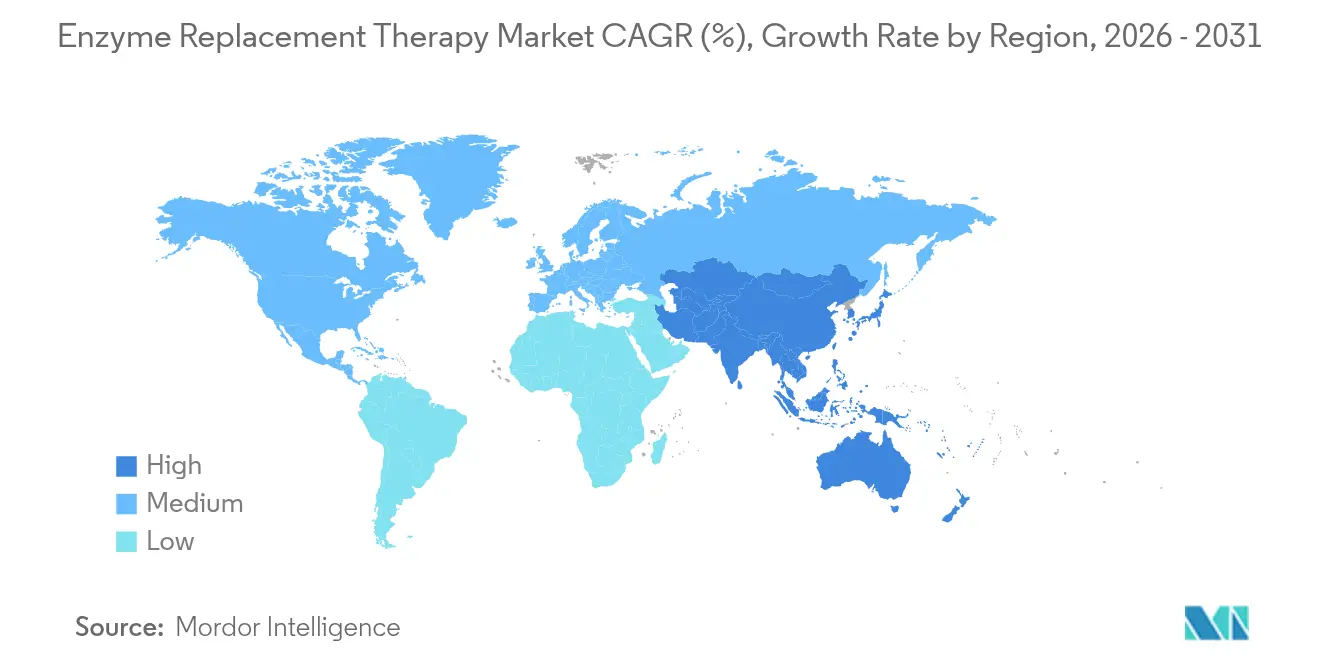

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

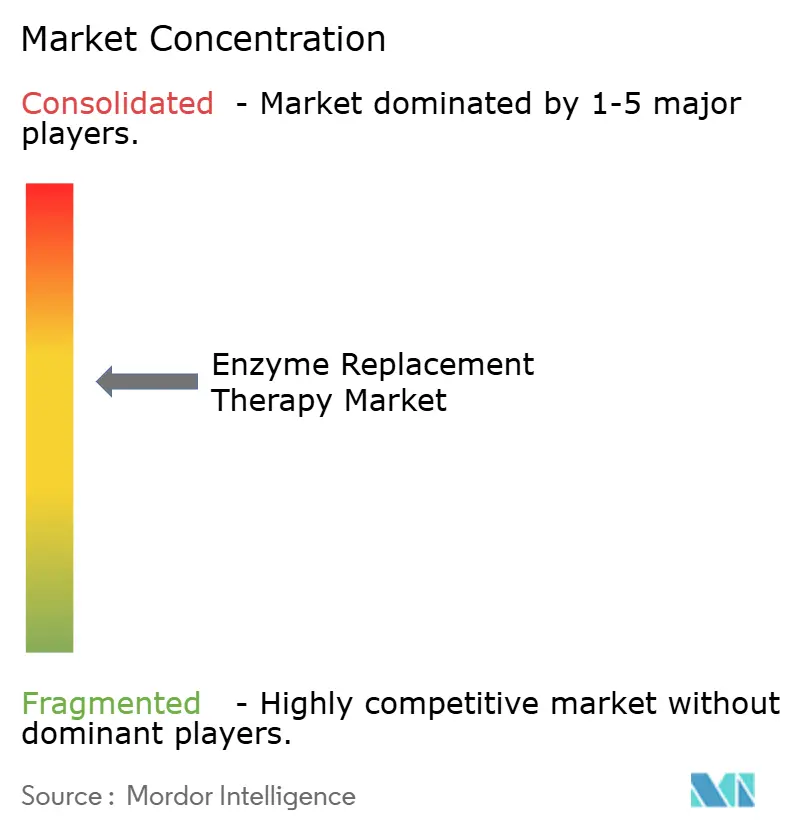

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enzyme Replacement Therapy Market Analysis by Mordor Intelligence

The enzyme replacement therapy market size is expected to grow from USD 16.01 billion in 2025 to USD 17.45 billion in 2026 and is forecast to reach USD 26.83 billion by 2031 at 8.99% CAGR over 2026-2031. Sustained expansion is tied to wider newborn screening, sharper diagnostic tools, and rising recognition of lysosomal storage disorders, which now shape clinical priorities across many health systems. Technology-enabled enzyme engineering and a clear pivot toward home-based infusion are reshaping care pathways, easing hospital congestion, and improving adherence. Regulatory agencies continue to accelerate orphan therapy approvals, while value-based contracts are testing fresh pricing methods. Supply resilience has become a strategic imperative after the global pancreatic enzyme shortage exposed vulnerabilities for more than 60,000 UK patients[1]Pharmaceutical Journal, “Pancreatic Enzyme Shortage to Persist into 2026,” pharmaceutical-journal.com.

Key Report Takeaways

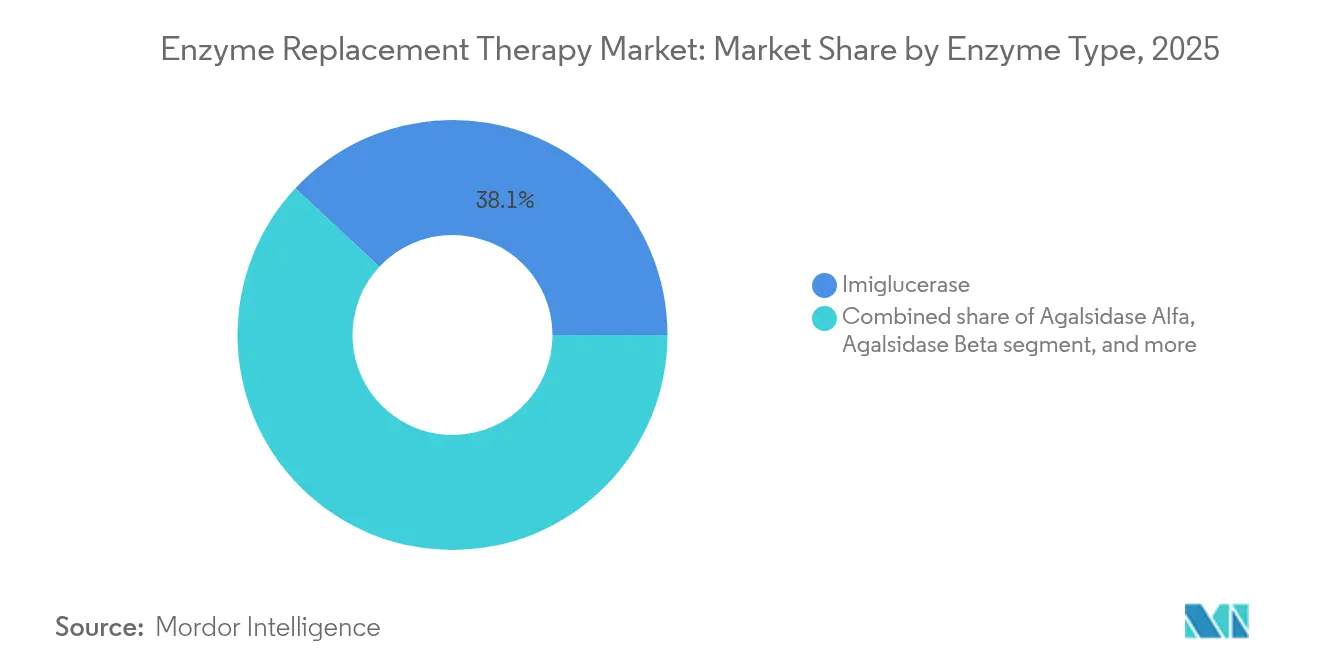

- By enzyme type, imiglucerase led with 38.05% of enzyme replacement therapy market share in 2025; avalglucosidase alfa is advancing at an 11.12% CAGR through 2031.

- By application, Gaucher disease commanded 42.87% of the enzyme replacement therapy market size in 2025, yet Pompe disease is expanding at an 11.02% CAGR to 2031.

- By route of administration, intravenous infusions captured 91.75% revenue share in 2025, whereas subcutaneous delivery is projected to rise at a 10.12% CAGR.

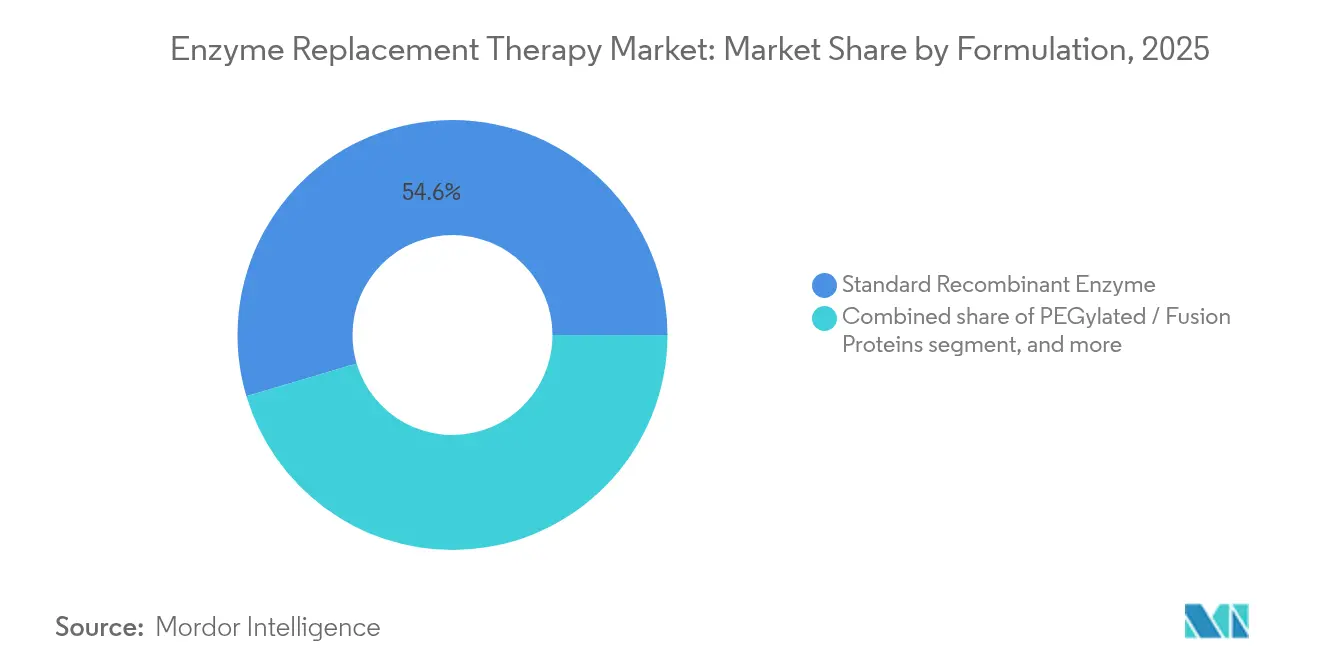

- By formulation, standard recombinant enzymes held 54.60% share of the enzyme replacement therapy market size in 2025, while PEGylated forms are set to grow at 9.85% CAGR.

- By end user, hospitals and specialty clinics accounted for 71.90% share in 2025; home healthcare is the fastest-growing channel at 12.10% CAGR.

- By geography, North America retained 38.10% share in 2025, whereas Asia-Pacific is forecast to post the highest 10.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Enzyme Replacement Therapy Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Rare Disease Prevalence | +2.1% | Global; higher impact in North America & Europe | Long term (≥ 4 years) |

| Government Incentives and Funding | +1.8% | North America & EU; expanding to Asia-Pacific | Medium term (2-4 years) |

| Expansion of Newborn Screening Programs | +1.5% | Global; early gains in developed markets | Long term (≥ 4 years) |

| Shift Toward Patient-Centric Delivery | +1.2% | North America & Europe; spill-over to Asia-Pacific | Medium term (2-4 years) |

| Technological Advancements in Enzyme Engineering | +1.7% | Global | Long term (≥ 4 years) |

| Innovative Reimbursement Models | +0.8% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Rare Disease Prevalence

Newborn genomic programs in China identified lysosomal storage disorders in 1 of every 1,512 births, revealing sizable undiagnosed cohorts and spurring sustained uptake across the enzyme replacement therapy market. Earlier diagnoses let clinicians intervene before irreversible organ damage, which lowers lifetime costs relative to late stage symptom management. Payers increasingly treat early therapy as preventive spending, realigning rare-disease budgets. As more jurisdictions adopt similar programs, the global patient pool expands and accelerates demand predictability. Early identification also facilitates long-term outcome tracking, a pre-requisite for value-based contracts that many insurers now favor.

Government Incentives and Funding

The US FDA granted six Rare Pediatric Disease Designations to M6P Therapeutics in 2024, illustrating how expedited review routes shorten development timelines for enzyme candidates. Europe’s proposal for an Orphan Genomic Therapies Fund seeks to underwrite both innovation and equitable access. Direct subsidies now target manufacturing capacity, responding to chronic shortages and boosting confidence in supply security. These policies lessen capital risk for biopharma sponsors and speed commercial launches, raising competitive intensity inside the enzyme replacement therapy market. Multinational firms leverage grants to scale regional plants, lowering landed costs and improving patient reach.

Expansion of Newborn Screening Programs

The PEARL trial at UCSF administers prenatal enzyme therapy for mucopolysaccharidosis type VI and infantile-onset Pompe disease, potentially eliminating post-natal antibody formation. Countries adding comprehensive panels now detect disease months or even years earlier, allowing clinicians to avert neurologic and skeletal damage that historically drove lifelong disability. Outcome data demonstrate lower hospitalization rates and improved growth metrics in screened infants, buttressing payer arguments for up-front program funding. Economic modeling shows screening costs are offset within three years through avoided complications, a message resonating with ministries of health in resource-limited regions.

Shift Toward Patient-Centric Delivery

Italian cohorts report 25-50% lower direct costs when enzyme infusions move from hospital to home, alongside higher adherence and markedly reduced patient stress. Only 9% of home-care recipients report treatment-related anxiety versus 40% among hospital counterparts[2]British Journal of Nursing, “Patient Experience with Home Infusion of Enzyme Replacement Therapy,” britishjournalofnursing.com. During the COVID-19 pandemic, remote monitoring technologies and nurse-led outreach validated the safety of at-home administration, embedding patient-centric models as a permanent feature of the enzyme replacement therapy market. Payers now reimburse home setups to release inpatient capacity, and device makers race to deliver portable infusion pumps that fit evolving protocols.

Restraints Impact Analysis of Enzyme Replacement Therapy Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Costs | −1.9% | Global; higher impact in emerging markets | Long term (≥ 4 years) |

| Immunogenicity Concerns | −1.3% | Global | Medium term (2-4 years) |

| Competition from Emerging Therapies | −1.1% | Global | Medium term (2-4 years) |

| Supply Chain Challenges | −0.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs

Annual outlays of USD 200,000–300,000 per patient in the United States continue to squeeze payer budgets, complicating broad adoption across emerging economies with smaller health-care spends. Surveyed insurers quote a median “fair” price of USD 256,000 for chronic enzyme therapies, a figure that scarcely aligns with public budget ceilings. European reimbursement still ranges widely—from 27% in Poland to 88% in Denmark—creating unequal access that fragments demand and tempers revenue visibility. While outcome-based contracts mitigate risk, they require sophisticated data streams that many health systems lack, slowing uptake.

Immunogenicity Concerns

Half of all enzyme-treated patients eventually mount anti-drug antibodies, some neutralizing therapeutic efficacy and others provoking infusion reactions that force discontinuation. Workarounds such as dose escalation or immune tolerance induction inflate costs and complicate care. Biosimilar entrants face added hurdles because even small manufacturing deviations can alter immunogenicity profiles, heightening regulatory scrutiny. Novel engineering, such as pegylation and glyco-switching, shows promise in dampening immune triggers, yet long-term safety data remain limited, delaying broad regulatory acceptance and slowing certain launches inside the enzyme replacement therapy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Enzyme Replacement Therapy Market Segment Analysis

By Enzyme Type:

Imiglucerase Dominance Faces Next-Generation ChallengeImiglucerase held 38.05% of enzyme replacement therapy market share in 2025, underscoring its entrenched role in Gaucher disease management over three decades. However, avalglucosidase alfa is forecast to grow at 11.12% CAGR, propelled by enhanced lysosomal targeting in Pompe disease protocols. The enzyme replacement therapy market size for next-generation agents is projected to expand rapidly as manufacturers migrate toward pegylated or glycoengineered constructs that promise longer half-life, lower immunogenicity, and reduced infusion frequency.

Competitive pressure mounts as agalsidase alfa, taliglucerase alfa, and velaglucerase alfa vie for differentiated positioning through alternative production systems and supply stability. Pegunigalsidase alfa’s phase-3 readouts show sustained plasma exposure, hinting at a paradigm shift for Fabry disease care. Manufacturers investing in yeast or plant-cell bioreactors cut upstream costs and diversify sourcing, lowering the risk of shortages that once punctuated the enzyme replacement therapy industry.

By Application:

Gaucher Disease Leadership Challenged by Pompe InnovationGaucher protocols generated 42.87% of the enzyme replacement therapy market size in 2025, courtesy of multiple approved assets and well-established dosing algorithms. Pompe disease tails closely, with an 11.02% CAGR expected through 2031 as cipaglucosidase alfa plus miglustat outperforms monotherapy benchmarks. Meanwhile, Fabry disease therapies maintain momentum through earlier diagnosis and guideline-driven initiation.

Emerging gene therapies, such as FLT201, are already trimming biomarker burdens and could squeeze enzyme uptake over the long term. Prenatal experimentation, as seen in UCSF’s PEARL trial, may rewrite intervention windows altogether. Application-specific recommendations from European consensus groups now standardize monitoring intervals, supporting payer confidence and indirectly buoying the enzyme replacement therapy market.

By Route of Administration:

Intravenous Dominance Faces Subcutaneous DisruptionIntravenous infusions accounted for 91.75% revenue share in 2025 as legacy care models and hospital infrastructure reinforced incumbent habits. Yet subcutaneous formats are steering a 10.12% CAGR, catalyzed by patients who favor autonomy and shorter appointment times. The enzyme replacement therapy market size captured by subcutaneous candidates remains modest today but carries outsized strategic weight.

Developers have optimized viscosity, osmolarity, and stabilizer content to secure bioequivalence with IV comparators, unlocking simplified regimens suitable for ambulatory or home settings. Regulators now request robust bridging data on immunogenicity and long-term exposure, elongating filings but bolstering confidence once approvals arrive. Vendors that couple product launches with remote-support platforms strengthen adherence and carve durable niches.

By Formulation:

Standard Enzymes Lead Despite PEGylated InnovationStandard recombinant enzymes held 54.60% share in 2025, reflecting three decades of clinical familiarity and streamlined regulatory pathways. Yet PEGylated constructs clock a 9.85% CAGR by extending half-life and allowing less frequent dosing. Growth also comes from fusion-protein techniques that fuse enzymes to antibody fragments, improving tissue penetration.

Market participants must weigh higher COGS and stricter quality checks against premium pricing and loyalty gains. The enzyme replacement therapy market soon features gene-activated enzymes with intrinsic targeting moieties, potentially leapfrogging PEGylation benefits. Early adopters lock in manufacturing know-how and patent depth, raising entry barriers for biosimilar challengers.

By End User:

Hospital Dominance Shifts Toward Home HealthcareHospitals and specialty clinics commanded 71.90% of revenue in 2025, but home healthcare settings post a 12.10% CAGR thanks to a clear 25-50% cost advantage and superior patient-reported outcomes. Infusion centers, a hybrid model, expand in urban zones where on-site oversight offers a compromise between convenience and medical vigilance.

Digital adherence tools, including smart pumps and cloud-based dashboards, underpin payer willingness to reimburse at-home infusions. These moves recast supply forecasts, as smaller, more frequent shipments replace bulk hospital orders. Device makers, specialty pharmacies, and nursing networks increasingly collaborate, densifying ecosystems that fuse product and service into one cohesive value proposition inside the enzyme replacement therapy market.

Geography Analysis

North America Enzyme Replacement Therapy Market

North America retained 38.10% share in 2025 and continues to benefit from well-funded insurance schemes and an FDA that accelerates rare-disease approvals such as Lenmeldy for metachromatic leukodystrophy. Outcome-based contracts have gained traction, tying annual outlays to biomarker improvements and hospitalization reductions. Manufacturers leverage specialty-pharmacy networks to execute same-day deliveries, enhancing adherence and reducing wastage. The enzyme replacement therapy market size across the United States and Canada also reflects broad newborn screening mandates, which funnel newly diagnosed infants into therapy earlier.

Europe Enzyme Replacement Therapy Market

Europe presents a mixed access picture. Denmark reimburses up to 88% of costs, yet Poland covers just 27%, producing uneven uptake that tempers aggregate revenue. Centralized approvals via the European Medicines Agency simplify filings, as seen with Xenpozyme for Niemann-Pick disease, but post-approval price negotiations can stretch for years. Cross-border treatment travel rises where domestic funding lags, adding logistical complexity to supply planning. Still, coordinated treatment guidelines for mucopolysaccharidoses support convergence in clinical practice and underpin moderate growth.

APAC Enzyme Replacement Therapy Market

Asia-Pacific is the enzyme replacement therapy market’s fastest-growing arena at a 10.08% CAGR, lifted by aggressive newborn screening, rising household incomes, and localized production hubs. China’s genomic panels uncovered higher-than-expected lysosomal incidence rates, prompting municipal funding programs that subsidize first-year treatments. Japan’s approvals for pabinafusp alfa (MPS II) and aceneuramic acid (GNE myopathy) reflect regulator openness to cutting-edge modalities. Contract manufacturers across South Korea and Singapore scale up enzyme capacity, while India leverages cost leadership to serve domestic and export demand. Collectively these initiatives lift the enzyme replacement therapy industry’s revenue baseline across the region.

Regulatory Landscape

Enzyme replacement therapies for lysosomal storage and related metabolic disorders are regulated primarily as biologics and are often developed under orphan-drug frameworks, which increases CMC oversight while providing incentives such as protocol assistance and fee reductions. In the United States, FDA rare-disease guidances continue to set evidence expectations for development programs, and in February 2026 the agency also launched a framework aimed at accelerating individualized therapies for ultra-rare diseases, reinforcing regulatory attention on genetically defined, small-population products.

In Europe, orphan designation and maintenance remain governed by Regulation (EC) No 141/2000, and centralized marketing authorization through the EMA and European Commission decision-making is still central to market entry. The EMA reported 211 orphan designation applications processed in 2025 and 17 new orphan medicinal product marketing authorizations granted by the European Commission, while it also continued its special annual contribution supporting fee reductions (including protocol assistance), which remains a lever for sponsors managing high development and lifecycle-management costs in ERTs.

Value Chain Analysis

ERT value creation begins with disease identification and patient routing (newborn screening and specialist diagnosis), then moves into biologics R&D, process development, and clinical supply, where nonclinical and clinical package requirements are shaped by FDA and EMA pathways used for rare diseases (including accelerated or conditional routes when surrogate endpoints are accepted). Manufacturing is centered on recombinant expression (commonly mammalian cell culture), followed by complex downstream purification and extensive batch release testing. This setup drives long lead times and inventory planning, and scaling constraints can directly affect development timelines, as illustrated by Travere Therapeutics pausing a late-stage ERT study in September 2024 due to production scale-up difficulties.

Commercial supply and access depend on cold-chain logistics, specialty distribution, and infusion delivery infrastructure spanning hospitals, infusion centers, and expanding home-infusion networks. Capacity and capability are increasingly managed through vertical integration and CDMO partnerships, including biosimilar-focused arrangements such as the February 2024 mAbxience and Biosidus CDMO agreement to manufacture agalsidase beta active ingredient, reflecting how manufacturers and partners use contracted production to manage cost, risk, and continuity for high-complexity enzymes.

Competitive Landscape

The enzyme replacement therapy market remains moderately consolidated, anchored by Sanofi (Genzyme), Takeda, and BioMarin, which together command robust clinical experience, patent estates, and global distribution. BioMarin posted 15% revenue growth in Q1 2025, achieving USD 484 million from enzyme assets despite growing competition. Established firms continue to refresh portfolios through pegylation, fusion-protein design, and acquisitions that deepen pipeline density. Strategic alignment with specialty pharmacies and home-care providers fortifies their service envelope.

New entrants are tilting competition toward potentially curative vectors. Spur Therapeutics’ FLT201 and REGENXBIO’s RGX-121 deploy AAV platforms to furnish durable enzyme expression, threatening erosion of chronic infusion demand. A USD 110 million upfront partnership between REGENXBIO and Nippon Shinyaku illustrates how biotech innovators pair IP with regional commercialization muscle, expediting market entry in Japan. Biosimilar developers circle expiring patents, yet face high analytical and immunogenicity hurdles, which safeguard incumbents in the near term.

Manufacturing scale is another battleground. Samsung Biologics plans 784,000-L capacity by 2025, promising faster turnarounds and lower unit costs. Capacity buffers insulate customers from shortages such as the pancreatic enzyme drought that disrupted UK therapy continuity. Companies able to guarantee uninterrupted supply clinch multiyear contracts with payers and health systems, reinforcing market share positions inside the enzyme replacement therapy market.

Enzyme Replacement Therapy Industry Leaders

Sanofi (Genzyme)

Takeda Pharmaceutical Co. Ltd

BioMarin Pharmaceutical Inc.

Amicus Therapeutics

Ultragenyx Pharmaceutical Inc.

- *Disclaimer: Major Players sorted in no particular order

Enzyme Replacement Therapy Market Companies Covered in this Report

- Sanofi

- Takeda Pharmaceuticals

- Biomarin Pharmaceutical

- Amicus Therapeutics

- Ultragenyx Pharmaceutical Inc.

- Spark Therapeutics

- JCR Pharmaceuticals Co. Ltd.

- Protalix BioTherapeutics

- Chiesi Farmaceutici

- GC Pharma (Green Cross Corp.)

- ISU Abxis

- Denali Therapeutics

- CANbridge Pharmaceuticals Inc.

- Pharming Group N.V.

- SOBI (Orphan Biovitrum)

- Avacta Group plc

- Orchard Therapeutics

- EUSA Pharma

- Idorsia Pharmaceuticals

Market Opportunities and Future Outlook

A key opportunity is expanding beyond disease manifestations that conventional ERT has not addressed, especially CNS involvement in neuronopathic lysosomal disorders. Regulatory action is reinforcing this direction: in March 2026, the US FDA granted accelerated approval to Denali Therapeutics for AVLAYAH (tividenofusp alfa-eknm) for neurologic manifestations of MPS II in pediatric patients (5 kg or heavier). The approval establishes a commercial precedent for brain-penetrant ERT platforms that use blood-brain barrier transport mechanisms and biomarker-aligned accelerated approval strategies.

Lifecycle expansion and pediatric label broadening remain clear whitespace for established franchises, supported by late-stage readouts and planned filings. Sanofi reported positive Phase 3 Baby-COMET results for Nexviazyme (avalglucosidase alfa) in June 2026 for infantile-onset Pompe disease and communicated plans to file a US supplemental BLA in the second half of 2026, highlighting how label expansion into earlier-treated cohorts can deepen treated populations while fitting the market shift toward earlier diagnosis and structured long-term monitoring. Alongside innovation, consolidation and portfolio rebalancing also create room for differentiated enzymes and delivery models within rare-disease commercial infrastructures, as larger players use M&A and partnerships to broaden specialty reach and clinical development throughput.

Recent Industry Developments in Enzyme Replacement Therapy Market

- June 2026: Sanofi announced positive results from the Phase 3 Baby-COMET study of Nexviazyme (avalglucosidase alfa) in infantile-onset Pompe disease, meeting primary and secondary endpoints. The company also stated plans to file a US supplemental BLA for a label extension in the second half of 2026, strengthening its lifecycle strategy in Pompe disease and reinforcing investment in earlier-treated patient segments.

- April 2026: BioMarin completed its acquisition of Amicus Therapeutics at USD 14.50 per share. The transaction expands BioMarin's rare-disease footprint and adds additional commercial and development capabilities that can be leveraged across enzyme and adjacent rare-metabolic therapy areas.

- May 2025: BioMarin entered a definitive agreement to acquire Inozyme Pharma for approximately USD 270 million, adding INZ-701 and strengthening its enzyme-therapy portfolio. The deal illustrates continued capital allocation toward rare-disease metabolic programs and complements BioMarin's strategy of broadening late-stage assets that fit specialty distribution and long-duration patient management models.

Enzyme Replacement Therapy Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the enzyme replacement therapy market is defined as revenue generated from prescribed enzyme products used to replace or supplement a missing or faulty enzyme in patients, where therapy is delivered under medical supervision and reimbursed through healthcare channels.

Scope exclusions: This sizing excludes over-the-counter digestive enzyme supplements, pharmacy compounding, and pre-commercial pipeline products that are not yet approved for sale.

Segments Covered in This Report

- By Enzyme Type

- Imiglucerase

- Agalsidase Alfa

- Agalsidase Beta

- Velaglucerase Alfa

- Taliglucerase Alfa

- Alglucosidase Alfa

- Avalglucosidase Alfa

- Galsulfase

- Idursulfase

- Other Enzymes

- By Application

- Gaucher Disease (Type I, II, III)

- Pompe Disease (Infantile & Late-Onset)

- Fabry Disease

- MPS I (Hurler Syndrome)

- MPS II (Hunter Syndrome)

- MPS IV (Morquio Syndrome)

- Other Applications

- By Route of Administration

- Intravenous Infusion

- Sub-Cutaneous

- By Formulation

- Standard Recombinant Enzyme

- PEGylated / Fusion Proteins

- Gene-Activated Next-Generation Enzymes

- By End User

- Hospitals & Specialty Clinics

- Home Healthcare Settings

- Infusion Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping approved ERT indications and therapy standards, and then aligning them to measurable demand and pricing signals by country. Public sources were used to anchor the disease and treatment pool, including US FDA drug labels and approvals, European Medicines Agency public assessment reports, and Centers for Disease Control and Prevention references on rare diseases where available.

To ground volumes and access, we also reviewed OECD health statistics, World Health Organization health expenditure indicators, and peer-reviewed publications on prevalence, diagnosis rates, and treatment patterns for lysosomal storage and related metabolic disorders. Company annual reports, investor presentations, and reputable press coverage helped validate launch timing, label expansions, and geographic presence, and a paid subscription focused on company financials and a patent database was used selectively to clarify product maturity and competitive intensity. These examples are not exhaustive, and many other public sources were reviewed to collect data points, validate assumptions, and close research gaps.

Primary Interviews and Surveys

Primary discussions were run with clinicians, hospital and infusion-center administrators, payor-linked stakeholders, and distribution-channel contacts so key assumptions could be checked against real prescribing and access behavior. For a global view, inputs were balanced across major regions, and follow-ups were used to reconcile gaps around diagnosis rates, switching, persistence, and net price movement after discounts and reimbursement rules.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 19% | APAC: 47% |

| Mid tier: 53% | Functional/Unit leaders: 24% | EMEA: 32% |

| Smaller Players: 19% | Managers: 57% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand-pool approach where diagnosed prevalence is filtered into treated patients by indication, and then converted into value using typical dosing, infusion frequency, and country-level net price logic. Since published prevalence can be broad for rare diseases, the treated pool was adjusted using practical access signals, including the share of patients seen at specialist centers and observed treatment uptake shared by interviewees.

To keep totals realistic, we cross-checked using selective bottom-up approximations, including sampling therapy-level annual cost ranges and matching them to the treated pool, along with channel checks on infusion activity and product availability by market. Inputs that most influenced the model included the diagnosed vs. undiagnosed split, treatment eligibility by label, average patient weight assumptions where dosing is weight-based, persistence and discontinuation rates, and discount and rebate levels that shift net revenue from list prices.

For forecasting, scenario analysis was applied and then narrowed using expert consensus on the timing of label expansions, earlier diagnosis trends, and the pace of access improvements in emerging markets. Where a country lacked a direct data point, proxy indicators (health spending per capita, rare-disease reimbursement maturity, and specialist-center density) were used to scale uptake, and totals were then reviewed again at the regional level.

Data Validation & Update Cycle

After the first model run, outputs were tested against independent signals such as known therapy cost ranges, regional patient pool reasonableness, and year-over-year growth patterns that align with launch and access timelines. Outliers were investigated by checking whether they came from an unrealistic treated rate, a dosing assumption that was too aggressive, or a net price that did not reflect local reimbursement practice.

Before sign-off, the estimates go through multi-step internal review, and we re-contact relevant experts when a key variable changes materially or a country result conflicts with known market behavior. Reports are refreshed annually, and interim updates are made when major events occur, such as approvals, safety restrictions, or meaningful pricing and access changes. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Enzyme Replacement Therapy Market Estimate Compared With Other Published Estimates

Published numbers for enzyme replacement therapy can vary because teams do not always size the same set of diseases, use the same treatment settings, or apply the same price basis, and those differences compound quickly in rare-disease markets. Another driver is timing, since approvals, reimbursement updates, and patient-finding programs can shift treated volumes within a short period.

Over-the-counter digestive enzyme supplements sit outside Mordor Intelligence's scope, which is one reason the 2025 value can diverge from estimates that blend prescription therapies with broader enzyme product sales. Gaps also come from whether pricing is modeled on list price or net realized price after discounts, how quickly treatment uptake is assumed to rise with better diagnosis, and whether home infusion and hospital channels are counted consistently across countries.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.01 B (2025) | |

| Industry Research Publisher A | USD 15.89 B (2025) | Uses a similar year but appears to broaden indication coverage to include pancreatic insufficiency products and may apply a different netting approach for discounts, which can slightly lower or raise revenue totals depending on the country mix. |

| Industry Research Publisher B | USD 11.23 B (2025) | Anchors estimates from a 2024 base year and may apply more conservative treated-rate assumptions for ultra-rare indications, and differences in regional inclusion and currency conversion timing can further compress the 2025 value. |

Looking across the table, the spread is largely explained by what gets counted as ERT, how net price is handled, and how quickly treated patient pools are assumed to expand. By keeping each step traceable to treated patients, dosing cadence, and net price checks, the resulting number stays practical to replicate and easier to pressure-test during planning.

Key Questions Answered in the Report

What is the current size of the enzyme replacement therapy market?

The market is valued at USD 17.45 billion in 2026 and is expected to reach USD 26.83 billion by 2031.

Which therapeutic area holds the largest share within enzyme replacement therapy?

Gaucher disease applications lead with 42.87% market share, thanks to multiple approved enzymes and mature treatment protocols.

Why is Asia-Pacific considered the fastest-growing region?

Expanding newborn screening, broader insurance coverage, and local manufacturing capacity drive a 10.08% CAGR in the region.

How are rising treatment costs being addressed?

Payers are adopting value-based contracts and outcome-based agreements to tie reimbursement to measurable clinical improvements.

What delivery trend is reshaping patient care models?

Home-based infusion is gaining traction, cutting direct treatment costs by 25-50% and improving adherence versus hospital settings.

Which innovation could most disrupt enzyme replacement therapy over the next decade?

Gene therapies such as FLT201 and RGX-121 aim to provide durable single-dose cures, potentially reducing demand for lifelong infusions.

Page last updated on: