C-reactive Protein Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.34 Billion |

| Market Size (2031) | USD 3.75 Billion |

| Growth Rate (2026 - 2031) | 2.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

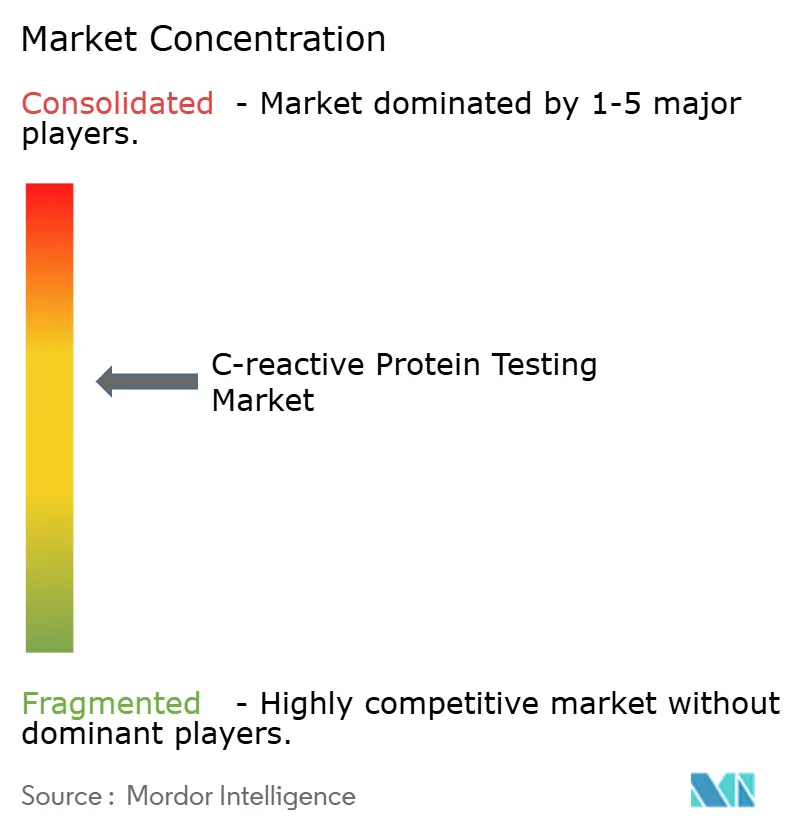

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

C-reactive Protein Testing Market Analysis by Mordor Intelligence

C-Reactive Protein testing market size in 2026 is estimated at USD 3.34 billion, growing from 2025 value of USD 3.26 billion with 2031 projections showing USD 3.75 billion, growing at 2.34% CAGR over 2026-2031. This steady growth stems from the pivot toward precision diagnostics, where high-sensitivity assays, multi-analyte inflammation panels and point-of-care formats command pricing power. Heightened regulatory scrutiny—such as the 2025 CLIA acceptance limits that tightened analytical tolerances—favors premium platforms able to deliver trace-level accuracy. In parallel, reimbursement caps that limit repeat testing in the United States are steering laboratories toward value-based utilization models, accelerating adoption of decision-support software bundled with assays. Across mature and emerging markets alike, rapid decentralization of testing to primary care clinics, pharmacies and home-monitoring programs is redefining competitive boundaries within the C-Reactive Protein testing market.

Key Report Takeaways

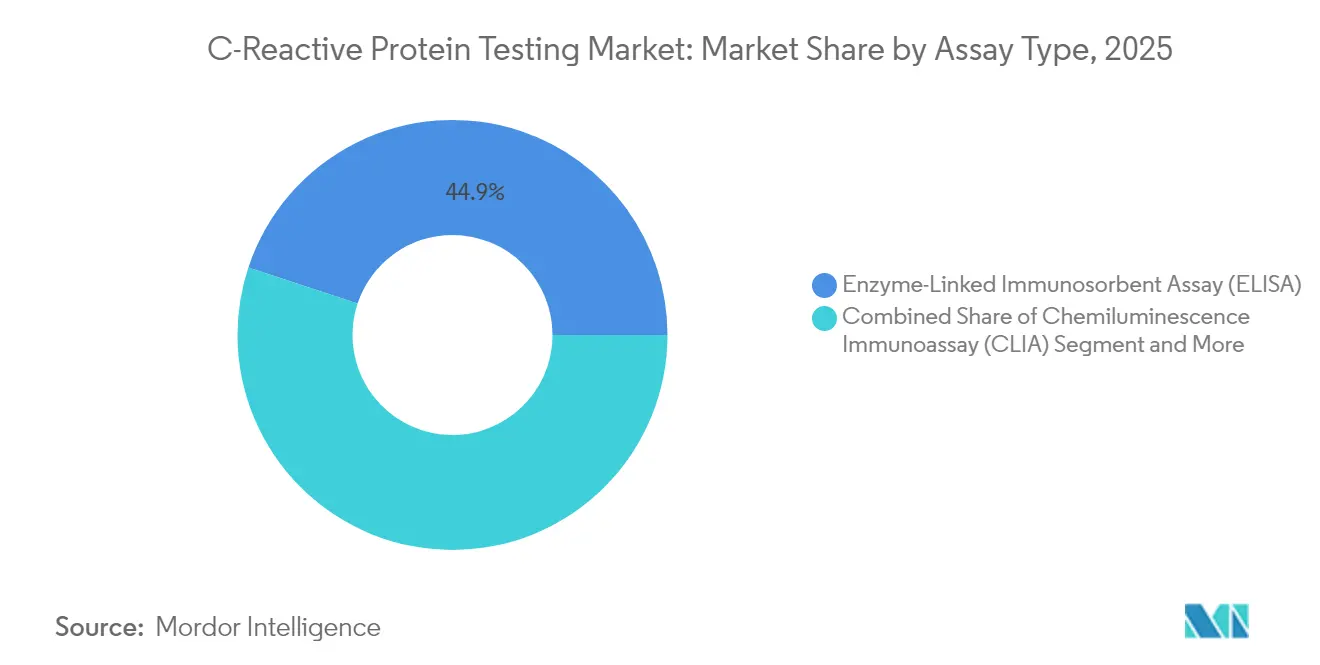

- By assay type, Enzyme-Linked Immunosorbent Assay led with 44.92% of C-Reactive Protein testing market share in 2025, while the Lateral-Flow Immunoassay segment is projected to advance at a 6.96% CAGR to 2031.

- By detection range, high-sensitivity CRP platforms accounted for 60.08% share of the C-Reactive Protein testing market size in 2025 and are forecast to expand at a 6.63% CAGR through 2031.

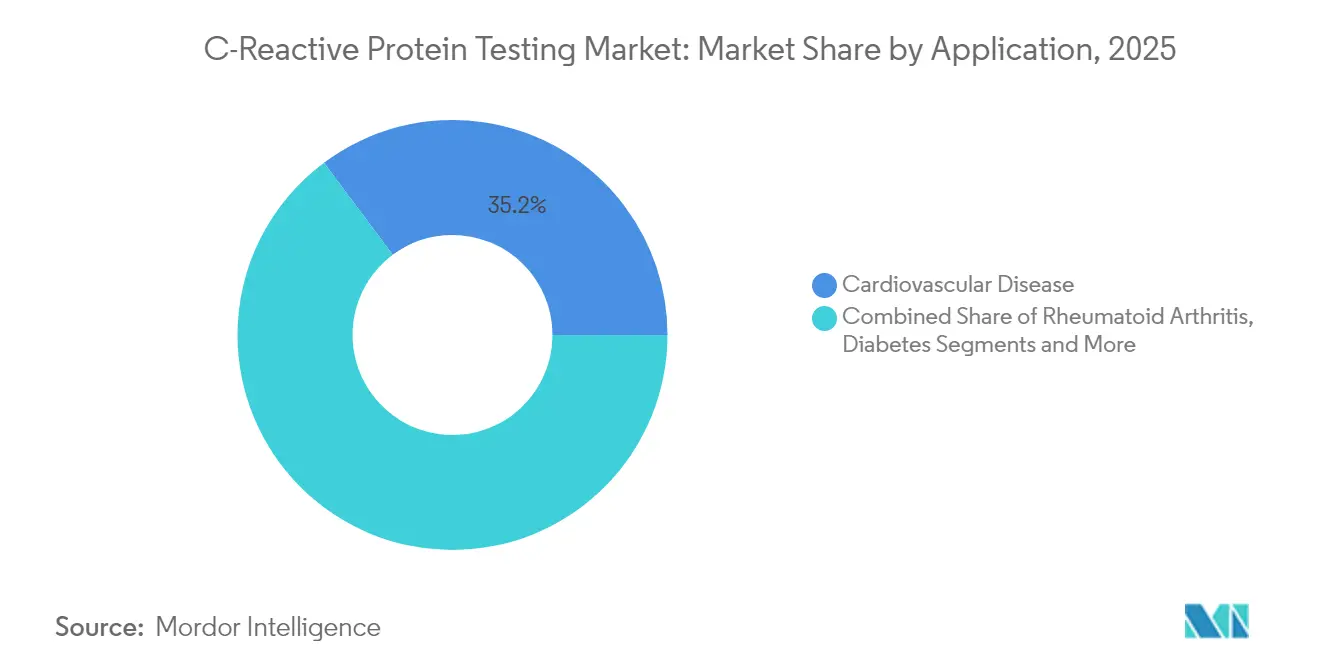

- By application, cardiovascular disease dominated with 35.20% revenue share in 2025; sepsis and acute infection testing is the fastest-growing application at a 7.28% CAGR.

- By end user, hospitals and clinics held 41.30% of 2025 revenues, whereas point-of-care settings are set to grow at an 8.22% CAGR.

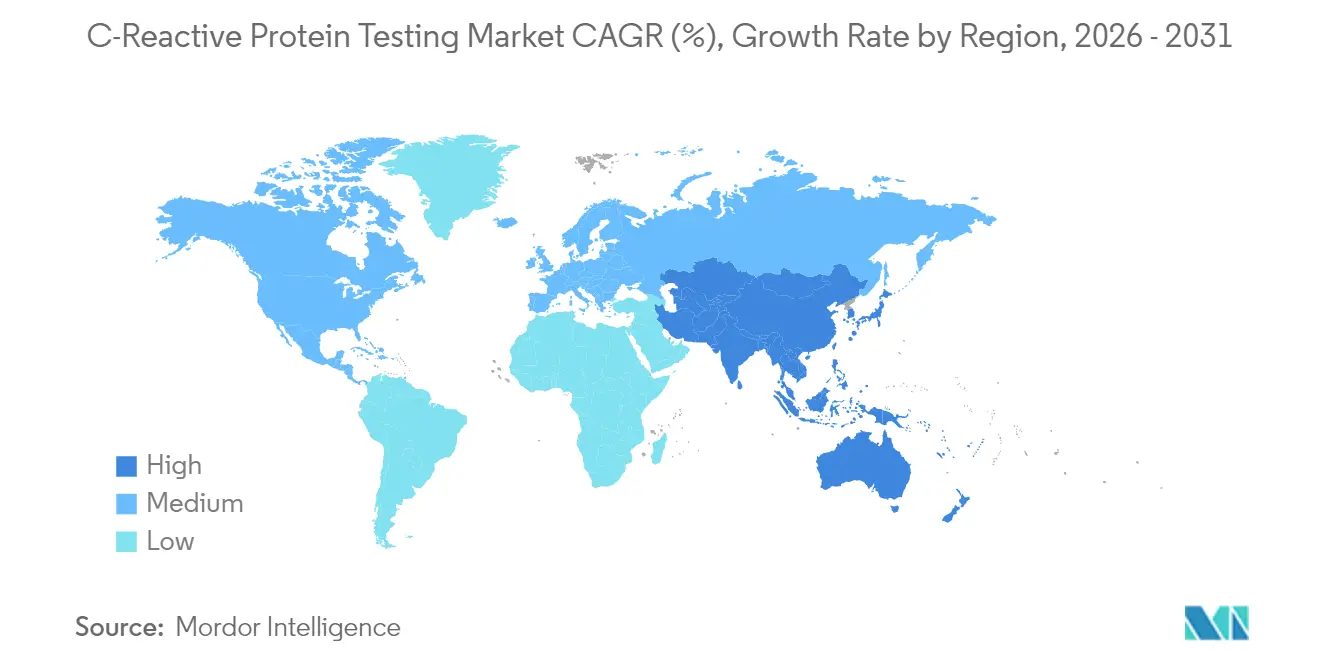

- By geography, North America commanded 38.40% of global revenues in 2025; Asia-Pacific is expected to post the highest regional CAGR of 6.92% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global C-reactive Protein Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic disease & inflammatory-disorder burden | +0.8% | North America, Europe (aging cohorts) | Long term (≥ 4 years) |

| High-sensitivity CRP in CVD-risk guidelines | +0.6% | North America, EU, expanding Asia-Pacific | Medium term (2-4 years) |

| Rise in endometriosis screening | +0.3% | Developed markets, global rollout | Medium term (2-4 years) |

| Surge in point-of-care roll-outs | +0.7% | Asia-Pacific core, spill-over to MEA & Latin America | Short term (≤ 2 years) |

| Connected home-diagnostic platforms | +0.4% | North America, EU, pilot programs in urban Asia-Pacific | Long term (≥ 4 years) |

| Nanoparticle-enhanced ultrafast ELISA chips | +0.5% | United States, EU, East Asia technology hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Disease & Inflammatory-Disorder Burden Accelerates CRP Testing Adoption

High prevalence of chronic inflammatory disorders is transforming how health systems use CRP. Gastroenterologists increasingly monitor ulcerative colitis remission with threshold CRP levels below 10 mg/L to adjust biologic therapy schedules[1]Sailish Honap, “Biomarkers in Inflammatory Bowel Disease: A Practical Guide,” journals.sagepub.com. Rheumatologists rely on longitudinal CRP trends to titrate disease-modifying drugs, reducing costly imaging studies. Aging demographics mean larger patient pools need recurring tests, creating predictable demand that offsets slower volume growth from acute-care episodes. Payers also view CRP as a cost-effective surrogate marker that can triage patients toward or away from advanced imaging, preserving budgets without sacrificing care quality. Collectively these factors bolster long-run volumes in the C-Reactive Protein testing market.

High-Sensitivity CRP Endorsed in Major CVD-Risk Guidelines

The American Heart Association embedded hsCRP into its cardiovascular-kidney-metabolic health framework in 2025, formalizing its role alongside LDL-C and HbA1c. Medicare’s Local Coverage Determination L34856 reimburses hsCRP up to three lifetime tests when used for lipid-lowering therapy optimization, creating a revenue baseline for laboratories. Guideline endorsement standardizes ordering behavior, reducing physician hesitation and expanding test penetration among intermediate-risk patients who previously lacked actionable biomarkers. Diagnostic manufacturers thus prioritize precision calibration at 0.1 mg/L increments and integrate decision-support analytics that translate hsCRP values into therapy algorithms, supporting premium pricing within the C-Reactive Protein testing market.

Rising Incidence of Endometriosis and Women’s Health Screening Programs

Blood-based panels incorporating CRP achieved 99.7% diagnostic accuracy for severe endometriosis in Australian trials, with regulatory clearance expected late 2025. Because laparoscopic confirmation is invasive and often delayed seven years, payers and clinicians anticipate rapid uptake of non-invasive screens. CRP’s correlation with deep infiltrative disease provides an objective marker for severity grading and therapy monitoring. Incorporating CRP into reproductive health check-ups opens a wide, underserved market segment beyond the cardiology core, diversifying revenue streams for C-Reactive Protein testing market participants.

Surge in Point-of-Care Testing Roll-Outs at Primary-Care Settings

Pharmacy-based pilots in Vietnam demonstrated 96.5% patient acceptance, while reducing unnecessary antibiotics in 81.4% of visits using five-minute CRP strips[2]Oxford University Clinical Research Unit, “New Point-of-Care Testing to Improve Antibiotic Use in Vietnam,” ndm.ox.ac.uk. Abbott’s Afinion system delivers quantitative CRP values in under four minutes and tolerates four-week room-temperature reagent storage, key for clinics with limited cold-chain capacity. These platforms shift test execution from central labs to first-contact points, accelerating clinical decision-making and expanding test volumes among populations previously underserved.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Poor public & physician awareness outside cardiology | -0.4% | Global, developing markets | Medium term (2-4 years) |

| Competing multi-analyte inflammatory panels | -0.6% | North America, EU, expanding Asia-Pacific | Short term (≤ 2 years) |

| Inter-platform analytical variability | -0.3% | Global | Long term (≥ 4 years) |

| Medicare lifetime three-test cap | -0.5% | United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Poor Public & Physician Awareness Outside Cardiology

Despite broad evidence, many clinicians limit CRP ordering to cardiovascular contexts. Specialty societies are now publishing quick-reference algorithms clarifying when CRP outperforms ESR and procalcitonin. Until awareness improves, non-cardiology demand will lag potential, tempering growth in regions lacking continuing-medical-education resources.

Competing Multi-Analyte Inflammatory Panels With Superior Accuracy

Siemens Healthineers’ seven-marker cytokine panel provides richer clinical insight than single-analyte tests, eroding standalone CRP revenue in tertiary centers[3]Siemens Healthineers, “Taking Cytokine Testing by Storm,” siemens-healthineers.com. Hospitals weighing capitated budgets may switch to comprehensive panels even at higher per-test prices, redistributing spend away from traditional CRP analyzers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Assay Type: Rapid Lateral-Flow Tests Narrow ELISA Lead

Enzyme-Linked Immunosorbent Assay held 44.92% of 2025 revenues thanks to entrenched analyzers and standardized protocols across integrated delivery networks. However, lateral-flow innovation lifted this segment’s 6.96% CAGR, compressing ELISA’s dominance. DNA nanotechnology tripled detection sensitivity, narrowing the accuracy gap with centralized methods and unlocking pharmacy-based testing lanes. Chemiluminescence instruments preserve relevance in high-throughput core labs where 200-sample racks and auto-reagent loading reduce labor costs. Looking ahead, ELISA bench-tops will focus on bundled multi-analyte menus and connectivity hooks, while rapid cassette suppliers court decentralized buyers. The bifurcation underscores how the C-Reactive Protein testing market rewards both high-volume lab integration and ultrafast near-patient convenience, with few middle-ground options remaining.

Growing patient preference for instant answers continues to pull testing outside hospital walls. Lateral-flow suppliers now bundle digital readers that sync to electronic health records, delivering traceable quantitative values rather than subjective color bands. In rural Southeast Asia, government immunization clinics adopted disposable cassettes to guide antibiotic stewardship without waiting days for reference-lab confirmation. Meanwhile, ELISA vendors defend share by embedding reflex-testing algorithms that auto-trigger cytokine panels when CRP surpasses 3 mg/L, positioning central labs as one-stop inflammation hubs. This dual-track evolution highlights why the C-Reactive Protein testing market remains one of diagnostics’ most technology-diverse arenas.

By Detection Range: Premium High-Sensitivity Platforms Capture Value

High-sensitivity reagents captured 60.08% of 2025 revenue and are pacing a 6.63% CAGR as clinicians value sub-1 mg/L precision for preventive cardiology. Regulatory bodies mandate tighter proficiency thresholds, pushing vendors to standardize calibrators traceable to IFCC reference material. Conventional range tests still anchor acute-care workflows, diagnosing pneumonia or appendicitis where CRP exceeds 50 mg/L. Yet reimbursement differentials increasingly incentivize labs to report hsCRP for borderline cardiovascular cases, reinforcing premiumization. Suppliers therefore redesign photometric optics and reagent chemistries to hold coefficient-of-variation below 3% at 0.5 mg/L, justifying higher prices.

Muted growth in conventional assays stems from antibiotic stewardship programs that limit unnecessary bacterial screens. Still, emerging markets rely on low-cost conventional kits to meet basic clinical needs. Dual-range analyzers capable of switching analytical modes offer a hedge, letting laboratories consolidate purchasing. These dynamics keep both tiers relevant, but margin expansion clusters around high-sensitivity innovations, demonstrating how detection-range segmentation shapes competitive advantage in the C-Reactive Protein testing market.

By Application: Sepsis Use-Cases Outpace Cardiovascular Mainstay

Cardiovascular disease remained the top revenue generator at 35.20% in 2025, buoyed by entrenched guideline recommendations. Sepsis testing, however, logged a 7.28% CAGR and is eroding share from slower cardiac growth. Emergency departments adopt 15-minute CRP panels alongside lactate and procalcitonin to triage suspected sepsis, accelerating antibiotic initiation when levels exceed 100 mg/L. Rheumatology, inflammatory bowel disease and oncology deploy serial CRP monitoring to track biologic response, producing predictable, subscription-like volumes.

Expansion of sepsis testing stems from heightened awareness of antimicrobial resistance. Hospitals integrate CRP algorithms that override empirical antibiotic orders when levels stay below 20 mg/L at admission, reducing broad-spectrum use. Vendors seize this opportunity by co-marketing CRP cartridges with stewardship software, adding value beyond raw biomarker output. Such application-specific platforms illustrate how participants in the C-Reactive Protein testing industry translate clinical pain points into differentiated product offerings.

By End User: Point-of-Care Channels Lead Growth Curve

Hospitals and clinics retained 41.30% revenue leadership in 2025, but the 8.22% CAGR in point-of-care settings signals a structural shift toward decentralized diagnostics. Community pharmacies, urgent-care centers and telehealth hubs embrace handheld analyzers that combine CRP, HbA1c and lipid profiles, monetizing quick health-checks. Home-care adoption remains nascent, yet connected devices embedding CRP chips position chronic-care management programs for subscription consumables. Reference labs counter with automated high-throughput systems that batch 1,000 samples nightly, enhancing cost per result to defend high-volume contracts.

Growth catalysts in near-patient segments include simplified CLIA-waived workflows and rising patient self-advocacy. As consumers track vitals via wearables, on-demand CRP complements holistic health dashboards. Vendors designing smartphone-paired cartridges capture this behavioral shift, embedding QR-coded calibrations to maintain traceability. Consequently, the C-Reactive Protein testing market size attached to decentralized channels will continue outpacing hospital budgets through 2031.

Geography Analysis

North America’s 38.40% revenue share in 2025 stems from insurer reimbursement clarity and clinician familiarity with hsCRP. Medicare’s three-test lifetime cap reduces routine repeat ordering, nudging labs to focus on first-time precision and digital decision support. Consolidation among service providers—such as Quest Diagnostics’ LifeLabs takeover—intensifies purchasing power, steering analyzer contracts toward end-to-end automation suites. Canadian provinces are integrating hsCRP into cardiovascular screening for individuals aged 45-75, anchoring baseline volumes across public labs.

Asia-Pacific delivers the fastest 6.92% CAGR, fueled by primary-care modernization and infectious-disease applications. China’s CRP-based tuberculosis triage among HIV-positive populations achieved 72.23% sensitivity and 77.66% specificity, showcasing locally tailored use-cases. Vietnam’s pharmacy pilots trimmed antibiotic misuse, bolstering government support for wider CRP rollout. Japan’s healthy-aging policies subsidize hsCRP for adults in metabolic screening programs, wid¬ening the addressable base. Regional suppliers leverage domestic manufacturing incentives to lower unit costs, penetrating rural clinics previously priced out of branded assays, which expands the C-Reactive Protein testing market footprint.

Europe maintains stable demand through rigorous standardization. IFCC’s laboratory medicine guideline initiatives harmonize calibrators across member states, shrinking inter-lab variability and raising clinician confidence. National Health Services in the United Kingdom added CRP to primary-care respiratory infection bundles, reimbursing tests that support antibiotic stewardship. Emerging regions in Middle East & Africa and South America collectively add single-digit share but post double-digit growth where mHealth programs piggyback CRP on multiparameter diagnostic vans servicing remote areas. Each geography thus maps distinctly onto the evolving C-Reactive Protein testing market, creating localized opportunities for agile players.

Competitive Landscape

Moderate consolidation characterizes the field, with top five vendors controlling significant revenue in 2024. Siemens Healthineers differentiates through an automated seven-marker inflammation panel offering results in 35-65 minutes, bundling CRP with cytokines IL-1β, IL-8 and TNFα for richer profiling. Roche posted 8% diagnostics growth in 2024 after launching 21 assays augmented by machine-learning analytics that predict disease flare-ups 48 hours earlier than single-threshold methods. Abbott fortifies its near-patient franchise with the Afinion CRP module that integrates into multi-assay primary-care workstations.

Strategic activity centers on connectivity and menu breadth rather than price cuts. Vendors embed HL7/FHIR interoperability to auto-populate electronic health records, reducing manual entry errors. Some firms pilot subscription models where analyzer placement is free but consumable cartridges carry per-test fees, mirroring printer-ink economics. White-space entrants focus on nanoparticle sensors and home-monitoring platforms, aiming to leapfrog incumbents tied to central-lab workflows. Regulatory pathways favor established players’ quality-system track records, yet nimble startups attract venture funding for disruptive at-home formats that could capture incremental C-Reactive Protein testing market share.

Future competition will hinge on ecosystem positioning: platforms that anchor broader inflammation panels stand to cross-sell cytokine, ferritin and D-dimer assays, deepening account stickiness. Conversely, pure-play CRP devices risk commoditization unless they pivot toward differentiated clinical decision support or niche applications such as pediatrics or obstetrics. The competitive chessboard is thus defined by bundled value propositions rather than isolated analyte performance.

C-reactive Protein Testing Industry Leaders

Abbott Laboratories

F. Hoffmann-La Roche AG

Danaher Corp (Beckman Coulter)

Siemens Healthineers

Thermo Fisher Scientific Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Roche introduced the Elecsys PRO-C3 test for liver fibrosis assessment in metabolic dysfunction-associated steatotic liver disease, returning results in 18 minutes.

- August 2024: Quest Diagnostics completed the USD 1.0 billion acquisition of LifeLabs, expanding diagnostic coverage across North America.

- May 2024: Siemens Healthineers launched its automated seven-test inflammation panel integrating CRP and six cytokines for 35-65-minute turnaround.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global C-reactive protein (CRP) testing market as revenues generated from reagent kits, controls, calibrators, and analyzer cartridges that quantitatively measure standard, high-sensitivity, or cardiac-specific CRP in serum, plasma, or whole-blood samples across laboratory and point-of-care settings. According to Mordor Intelligence, ancillary hardware sales are counted only when packaged with consumables, ensuring the figure reflects recurring diagnostic demand rather than capital equipment outlays.

Scope exclusion: stand-alone benchtop analyzers sold without CRP reagents and any service-only laboratory fees are kept outside this market view.

Segmentation Overview

- By Assay Type

- Enzyme-Linked Immunosorbent Assay (ELISA)

- Chemiluminescence Immunoassay (CLIA)

- Immunoturbidimetric Assay

- Lateral-Flow Immunoassay

- Other Assay Types

- By Detection Range

- High-Sensitivity CRP

- Conventional CRP

- By Application

- Cardiovascular Disease

- Rheumatoid Arthritis

- Diabetes

- Inflammatory Bowel Disease

- Cancer

- Sepsis & Acute Infection

- Other Applications

- By End User

- Hospitals & Clinics

- Reference & Central Laboratories

- Point-of-Care Settings

- Academic & Research Institutes

- Home-Care Settings

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed immunoassay product managers, hospital lab directors, and cardiologists in North America, Europe, Asia-Pacific, and Latin America. The discussions clarified kit utilization patterns, point-of-care adoption, and average selling prices, then validated secondary assumptions before final triangulation.

Desk Research

We started with publicly available registries such as the U.S. FDA 510(k) database, European CE mark archives, and WHO Global Health Observatory for incidence and testing-rate benchmarks. Statistics from the American Heart Association, OECD Health Data, and national infectious-disease dashboards supplied prevalence inputs. Company filings accessed through D&B Hoovers, peer-reviewed articles indexed on PubMed, and news flows gathered via Dow Jones Factiva provided pricing signals and pipeline clues. These sources are illustrative; many additional open datasets informed smaller model blocks.

Market-Sizing & Forecasting

A top-down and bottom-up blend underpins our model. Country-level test volumes were reconstructed from chronic-disease admissions, outpatient panel frequencies, and population screening guidelines, then multiplied by validated average reagent prices. Supplier roll-ups and channel checks offered a bottom-up sense check and gap fill. Key variables include cardiovascular hospitalization rates, diabetes prevalence, point-of-care device installed base, kit ASP progression, and guideline-driven hsCRP adoption. Multivariate regression, supported by expert consensus, projects these drivers to 2030, while scenario analysis handles policy or reimbursement shocks.

Data Validation & Update Cycle

Outputs pass variance and anomaly checks, followed by senior analyst review. Reports refresh each year, with interim updates when material events occur. Before publication, we run a fresh validation sweep so clients obtain the latest view.

Why Mordor's C-Reactive Protein Testing Baseline Earns Decision-Maker Trust

Published estimates often diverge because firms adopt different scopes, pricing assumptions, and refresh cadences.

Key gap drivers include whether reagent-only revenues are isolated, if point-of-care kits are counted, currency year fixes, and the depth of primary interviews that temper model inputs. Mordor's disciplined scope and frequent refresh narrow these gaps, giving planners a steadier compass.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.26 B (2025) | Mordor Intelligence | - |

| USD 5.58 B (2024) | Global Consultancy A | Combines analyzer hardware and multiyear service bundles; limited primary validation |

| USD 2.42 B (2024) | Industry Journal B | Excludes point-of-care kits and models only Tier 1 countries with 2022 exchange rates |

These comparisons show that, by centering on clear revenue streams and refreshed driver sets, Mordor Intelligence delivers a balanced, transparent baseline clients can reproduce and defend in strategy sessions.

Key Questions Answered in the Report

What is the current size of the C-Reactive Protein testing market?

The market generated USD 3.34 billion in revenue in 2026 and is projected to reach USD 3.75 billion by 2031.

Which segment is growing fastest within the C-Reactive Protein testing market?

Point-of-care settings lead growth with an 8.22% CAGR, driven by rapid tests deployed in pharmacies and primary-care clinics.

Why are high-sensitivity CRP assays gaining traction?

HsCRP offers sub-1 mg/L precision, now recommended in cardiovascular guidelines and supported by reimbursement, enabling earlier risk detection.

How will regulatory changes in the United States affect test volumes?

Medicare limits hsCRP to three lifetime tests, steering labs toward value-based utilization and favoring platforms delivering richer decision support.

Which region offers the greatest growth opportunity?

Asia-Pacific, expanding at a 6.92% CAGR, benefits from healthcare modernization, point-of-care adoption and infectious-disease applications.

Page last updated on: