Gene Synthesis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 6.09 Billion |

| Growth Rate (2026 - 2031) | 16.38% CAGR |

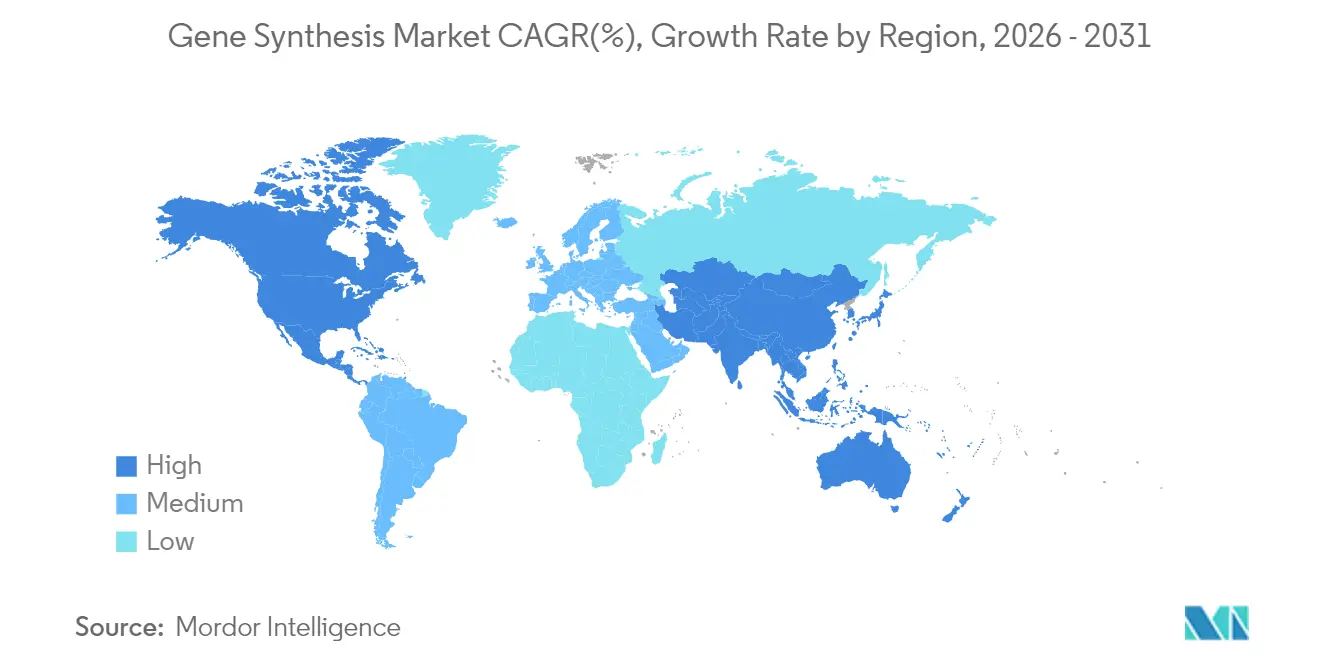

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

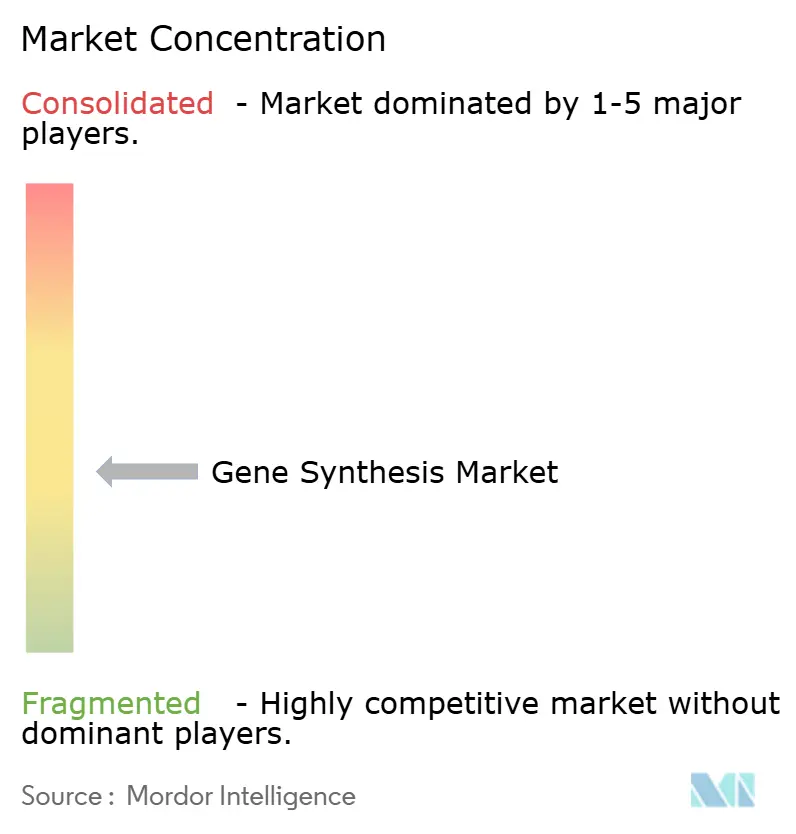

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gene Synthesis Market Analysis by Mordor Intelligence

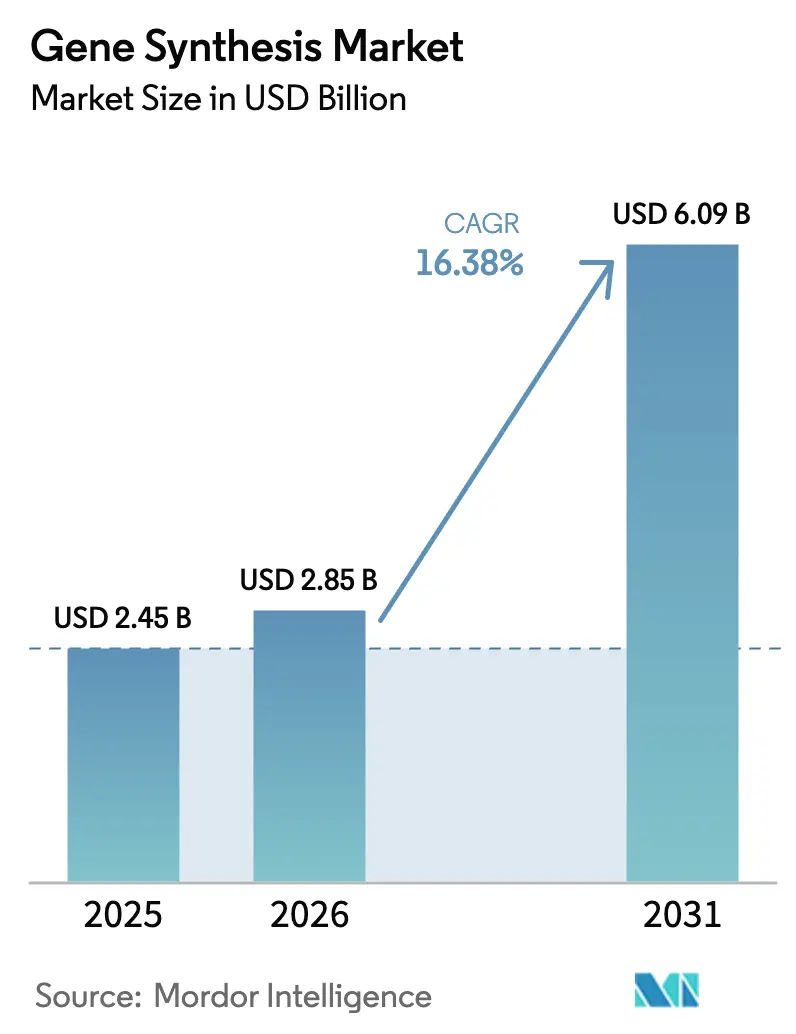

The Gene Synthesis Market size was valued at USD 2.45 billion in 2025 and is estimated to grow from USD 2.85 billion in 2026 to reach USD 6.09 billion by 2031, at a CAGR of 16.38% during the forecast period (2026-2031).

This rapid expansion reflects sustained breakthroughs in enzymatic oligonucleotide production, larger research budgets for precision genomics, and surging demand from biopharmaceutical companies seeking faster design-build-test cycles [1]NHGRI, “Genomic Technology Grants,” genome.gov . Growing regulatory clarity also supports the gene synthesis market, with the Biden administration’s Executive Order on AI and biotechnology outlining new federal screening rules that create common operating standards for providers. Manufacturing capacity is playing catch-up because oligonucleotide demand is rising 30% each year even as synthesis productivity improves more slowly than sequencing throughput. In parallel, 10 gene therapies gained FDA approval in 2024—twice the prior year’s figure—showing how regulatory momentum accelerates commercial orders for long, high-fidelity constructs.

Key Report Takeaways

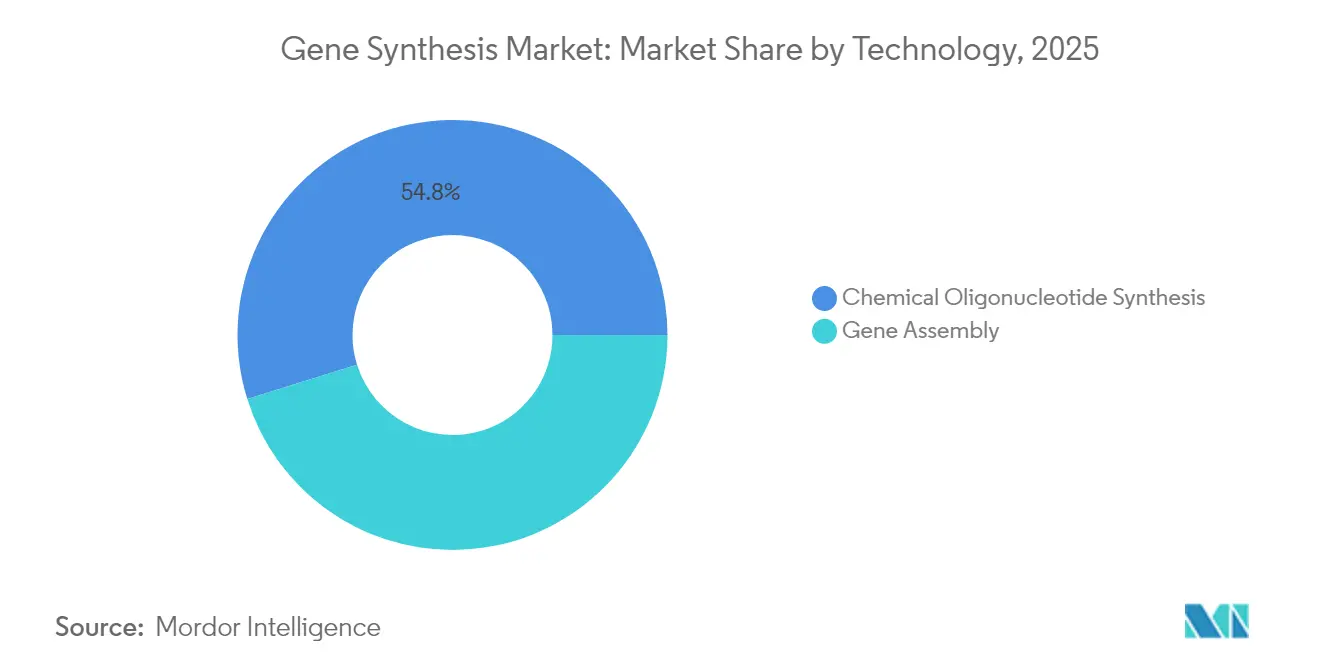

- By synthesis method, chemical oligonucleotide synthesis held 54.82% gene synthesis market share in 2025, while gene assembly technologies are projected to expand at a 17.06% CAGR through 2031.

- By service type, antibody DNA synthesis accounted for 47.76% of the gene synthesis market size in 2025; viral gene synthesis are on track for a 17.06% CAGR to 2031.

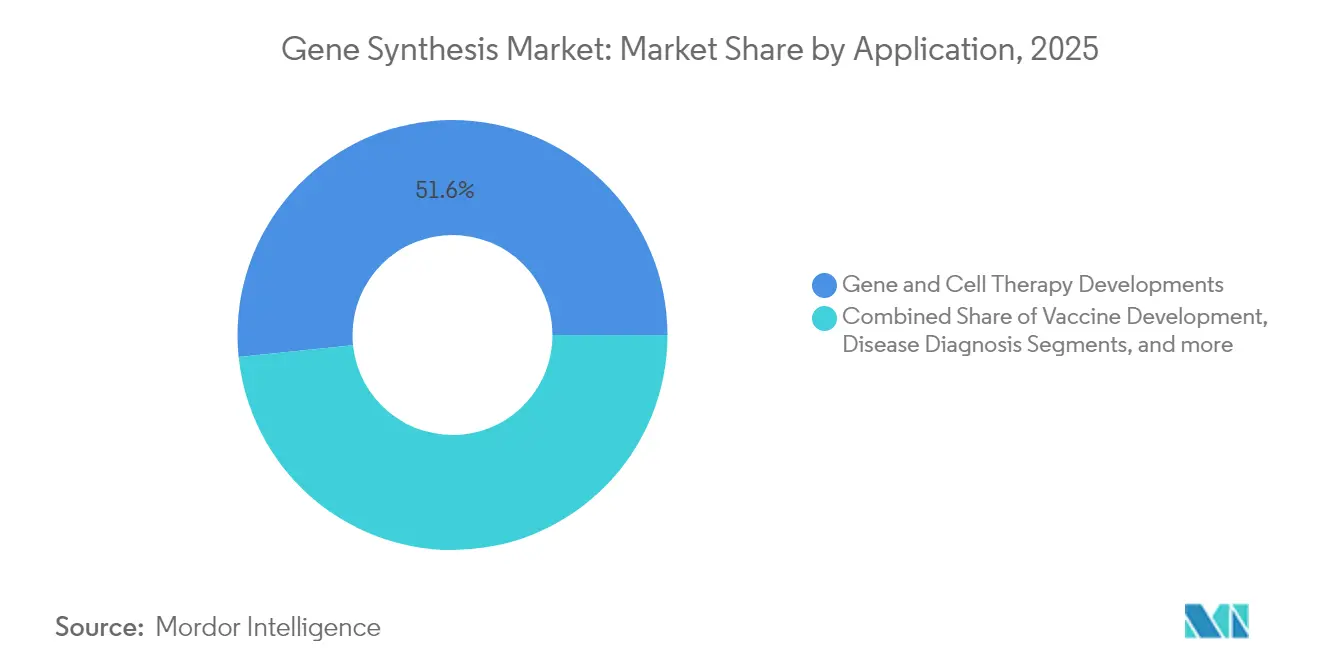

- By application, gene and cell therapy accounted for 51.64% of the gene synthesis market size in 2025; disease-diagnosis uses are on track for a 17.12% CAGR to 2031.

- By end user, biopharmaceutical companies generated 45.71% of revenue in 2025, whereas CROs and CDMOs are poised for the fastest 17.18% CAGR as outsourcing accelerates.

- By geography, North America commanded 41.88% of the gene synthesis market size in 2025, yet Asia-Pacific is set to grow the quickest at a 17.29% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Gene Synthesis Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging genomics & NGS-driven R&D pipelines | +3.2% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Expanding biopharma demand for synthetic genes | +4.1% | Global, led by North America, Asia-Pacific growth | Short term (≤ 2 years) |

| Government genomics-funding initiatives | +2.8% | North America, Europe, China, India | Long term (≥ 4 years) |

| Rapid drop in DNA-synthesis cost & turnaround | +3.5% | Global, manufacturing hubs in Asia-Pacific | Medium term (2-4 years) |

| Emerging enzymatic DNA-synthesis platforms | +2.9% | North America & Europe development, Global adoption | Medium term (2-4 years) |

| Venture-capital rush into bio-foundries & cloud labs | +1.7% | North America, Europe, selective Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Genomics & NGS-Driven R&D Pipelines

More than 900 active clinical trials in North America now incorporate synthetic DNA constructs, underscoring how next-generation sequencing pushes laboratories toward higher-throughput build capabilities. CEPI has committed USD 4.7 million to automate DNA Script’s template production so vaccine developers can move from design to bench in days rather than weeks [2]CEPI, “Funding Award to DNA Script,” cepi.net . Academic progress supports the driver: University of Hawaii researchers achieved 96% editing success when using high-fidelity templates, demonstrating direct links between synthesis quality and therapeutic efficacy [3]University of Hawaii, “High-Fidelity Gene Editing Study,” hawaii.edu. NHGRI’s USD 2.2 million grant for multiplex oligo synthesis further embeds synthetic DNA as critical research infrastructure. Together, these elements enlarge sample backlogs and create premium opportunities for providers able to guarantee error-free sequences on demand.

Expanding Biopharma Demand for Synthetic Genes

Biopharmaceutical pipelines now depend on custom genes for cell therapies, mRNA vaccines, and antibody-drug conjugates. The FDA cleared five gene therapies in 2024, including the first CRISPR-edited treatment, and each approval validates commercial need for precise, viral-vector-ready inserts. GSK invested USD 35 million in Elegen to secure linear DNA that fits its mRNA vaccine portfolio. Clinically, Casgevy prevented severe vaso-occlusive crises in 93.5% of treated sickle-cell patients, proving that accurate template design translates into therapeutic success. Investor sentiment mirrors demand; Constructive Bio attracted USD 58 million in Series A funding as synthetic genomics promises to ease global peptide shortages. These developments shorten development timelines and intensify competition for trustworthy synthesis partners.

Government Genomics-Funding Initiatives

The NHGRI has allocated USD 1.5 million annually through 2029 to accelerate platform technologies, including enzymatic oligo production. India’s BioE3 framework backs precision biotherapeutics and biomanufacturing with fiscal incentives and regulatory streamlining. The European Union’s SYNBEE project offers grants that help startups integrate AI with DNA design. Japan targets a biotechnology market worth 15 trillion yen by 2030 and emphasizes induced pluripotent stem-cell research that relies on long synthetic genes. Public funding reduces commercial risk, expands installed synthesis capacity, and lifts regional adoption rates.

Rapid Drop in DNA-Synthesis Cost & Turnaround

Enzymatic platforms now allow same-day oligo printing without hazardous solvents, narrowing the gap between sequencing and synthesis speeds. Ribbon Biolabs recently demonstrated 20 kb fragments featuring 0.33% error rates, which expands addressable gene length beyond what chemical methods routinely manage. The University of California Irvine’s proof-of-concept 10-92 TNA polymerase shows academia’s role in boosting both yield and fidelity. WuXi STA has scaled to 27 oligonucleotide lines, underscoring global moves to industrial volumes. Cost declines encourage wider experimentation, sustaining double-digit growth for the gene synthesis market.

Restraints Impact Analysis of Gene Synthesis Market*

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of skilled synthetic-biology workforce | -2.1% | Global, acute in Europe & emerging markets | Long term (≥ 4 years) |

| High capital cost for large-scale synthesis capacity | -1.8% | Global, particularly challenging for new entrants | Medium term (2-4 years) |

| IP-ownership uncertainty for de-novo constructs | -1.3% | Global, complex in multi-jurisdictional operations | Long term (≥ 4 years) |

| Biosecurity & dual-use regulatory scrutiny | -1.6% | Global, stringent in North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Skilled Synthetic-Biology Workforce

Synthetic biology blends molecular biology, engineering, and computation, yet most academic curricula still emphasize traditional wet-lab skills. NHGRI earmarked USD 5.25 million to boost workforce diversity, signalling institutional recognition of the shortage. European biotechnology contributes EUR 31 billion to GDP but already suffers talent bottlenecks that curtail start-up scaling. Japan’s venture funding remains low relative to the United States, partly because of limited entrepreneurial depth. Continuous retraining is essential because enzymatic platforms require new skill sets compared with phosphorus-based chemistry. Without enough qualified staff, production lines risk under-utilization, slowing revenue accrual for the gene synthesis market.

High Capital Cost for Large-Scale Synthesis Capacity

Solid-phase synthesis equipment, purification columns, and waste-handling systems demand multimillion-dollar investments before a single order ships. Molecular Assemblies raised USD 25.8 million solely to commercialize fully enzymatic flow-platforms. Thermo Fisher committed USD 2 billion to expand United States manufacturing and R&D through 2028, revealing the size of budgets required to stay competitive. FDA’s Advanced Manufacturing Technologies program provides regulatory support yet still requires extensive validation, adding expense and time. Smaller entrants that cannot amortize equipment quickly may exit or become acquisition targets, tempering fresh innovation within the gene synthesis market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Gene Synthesis Market Segment Analysis

By Synthesis Method:

Enzymatic Platforms Challenge Chemical DominanceChemical oligonucleotide synthesis retained 54.82% gene synthesis market share in 2025 thanks to decades of process optimization and reliable supply chains. Solid-phase phosphoramidite reactions remain standard for short strands, and microchip-based approaches improve batch throughput. Yet the gene synthesis market is pivoting as assembly technologies post a 17.06% CAGR through 2031, propelled by the need for longer constructs in CRISPR and viral vectors.

Enzymatic platforms such as DNA Script’s SYNTAX produce up to 96 oligos within hours, offering laboratories instant access without toxic solvents. Molecular Assemblies’ fully enzymatic flow technology further reduces error rates while extending read length, positioning it to steal share from incumbent methods. Hybrid strategies that combine chemical speed for short primers with enzymatic assembly for long genes are emerging, ensuring the gene synthesis market continues to diversify rather than converge on a single technique.

By Service Type:

Viral Gene Synthesis Accelerates Vaccine DevelopmentAntibody DNA synthesis contributed 47.76% of the gene synthesis market size in 2025 because of rising antibody-drug conjugate pipelines and CAR-T cell interest. Viral gene synthesis is set for a 17.06% CAGR as mRNA platforms and viral vectors dominate vaccine and gene-therapy arenas.

CEPI funding of automated template production confirmed strategic urgency to shorten vaccine R&D cycles. Johnson & Johnson’s collaboration with GenScript on approved CAR-T therapies exemplifies how proprietary antibody sequences generate recurring orders. Service providers capable of bundling sequence design, enzymatic synthesis, and AI-based optimization stand to capture premium contracts, expanding overall revenue for the gene synthesis market.

By Application:

Diagnosis Adoption Broadens Commercial BaseGene and cell therapy represented 51.64% of demand in 2025, strengthened by the FDA’s accelerating approval cadence for one-time genetic treatments. Disease-diagnosis applications will expand at a 17.12% CAGR as hospitals embed genomic assays into routine care.

Rapid neonatal genome sequencing now proves clinically necessary in 60% of level IV NICU cases, creating daily demand for custom probes and controls. AI-designed regulatory sequences developed by the Centre for Genomic Regulation enable ultra-selective expression, opening new markets for design-plus-build services. Together, these forces sustain diversity in application mix, keeping the gene synthesis market resilient to therapeutic-pipeline volatility.

By End User:

Outsourcing Propels CRO and CDMO GrowthBiopharmaceutical firms still drove 45.71% of revenue in 2025 by ordering large volumes for internal programs. However, CROs and CDMOs are forecast to record the swiftest 17.18% CAGR as sponsors externalize synthesis to focus on clinical strategy.

GenScript’s USD 224 million raise earmarked for CDMO expansion signals supplier confidence in the outsourcing wave. Twist Bioscience posted USD 92.8 million revenue for Q2 2025 on the back of diversified customer pools in both synthetic biology and next-generation sequencing. Academic consortia funded by NHGRI further diversify revenue streams, ensuring broad demand stability for the gene synthesis market.

Geography Analysis

North America Gene Synthesis Market

North America commanded 41.88% of the gene synthesis market size in 2025 because of strong venture capital flows, mature biopharmaceutical clusters, and supportive regulation. The NHGRI’s USD 1.5 million annual commitment to platform technologies fosters public-private partnerships, while the FDA’s coordinated gene-therapy review pathway removes regulatory uncertainty. Private firms mirror policy confidence; Thermo Fisher is spending USD 2 billion on domestic capacity expansions through 2028.

APAC Gene Synthesis Market

Asia-Pacific is projected to log a 17.29% CAGR through 2031 and is the fastest-growing region in the gene synthesis market. China classifies biotechnology as a strategic pillar and channels generous subsidies into synthetic genetics ventures. India’s BioE3 policy prioritizes precision biotherapeutics and positions local biofoundries to serve global clients. Japan plans to double private drug-discovery investment by 2028, with induced pluripotent stem-cell projects demanding long synthetic sequences. South Korea’s cell-therapy initiatives further reinforce regional momentum.

EMEA and South America Gene Synthesis Market

Europe remains a steady growth contributor as coordinated policy frameworks such as the EU Bioeconomy Strategy back industrial biotechnology. SYNBEE grants help startups combine AI and DNA design, while the continent’s pharmaceutical giants deliver consistent order volumes. Middle East and Africa along with South America are early in adoption cycles, yet rising healthcare spending and agricultural biotech needs are widening the addressable base for the gene synthesis market.

Competitive Landscape

Competitive intensity is moderate. Market leaders—Twist Bioscience, GenScript Biotech, Thermo Fisher Scientific, and Integrated DNA Technologies—compete on accuracy, turnaround, and platform breadth rather than price. Twist reported 49.6% gross margin during Q2 2025, demonstrating healthy economics once scale is achieved. GenScript’s funding round earmarked for CDMO expansion shows incumbents reinvesting to hold share. Patent filings such as CRISPR Therapeutics’ genomic-editing compositions (11,332,760) protect technological edges and create licensing revenue streams.

Disruptors pursue enzymatic, microfluidic, and automation-rich solutions. DNA Script secured USD 165 million in Series C for its SYNTAX printer and now partners with pharmaceutical firms on same-day oligo supply. Constructive Bio’s USD 58 million raise focuses on rewriting genetic codes to synthesize non-canonical amino acids, challenging current chemical capacity limits. Ribbon Biolabs targets long-fragment niches, while Molecular Assemblies builds proprietary enzymes that extend read length and purity.

Strategic acquisitions accelerate capability stacking. Johnson & Johnson bought Ambrx for USD 2 billion to add antibody-drug conjugate know-how, reflecting big-pharma appetite for upstream genetics. Maravai LifeSciences intends to acquire Officinae Bio’s DNA and RNA assets to broaden AI-enabled mRNA prototyping. Such moves consolidate expertise and raise entry barriers, yet they also validate long-term value within the gene synthesis market.

Gene Synthesis Industry Leaders

Merck KGaA

Eurofins Genomics

Thermo Fisher Scientific

GenScript

Azenta Life Sciences (Genewiz)

- *Disclaimer: Major Players sorted in no particular order

Gene Synthesis Market Companies Covered in this Report

- ATUM

- Bio Basic

- Beijing SBS Genetech Co.

- Eurofins

- Azenta Life Sciences (Genewiz)

- GenScript Biotech

- Merck KGaA (Sigma GeneArts)

- OriGene Technologies

- Thermo Fisher Scientific (GeneArt)

- Integrated DNA Technologies

- Twist Bioscience

- DNA Script

- Ansa Biotechnologies

- Evonetix

- Telesis Bio

- Synbio Technologies

- Bioneer

- ProteoGenix

- Bio-Synthesis

- ATLATL Innovations

Recent Industry Developments in Gene Synthesis Market

- May 2025: Ansa Biotechnologies launched a 50 kb DNA-synthesis early-access program, promising complex sequences within four weeks.

- March 2025: Telesis Bio secured up to USD 21 million to accelerate Gibson SOLA enzymatic DNA-synthesis adoption, enabling on-site production while safeguarding intellectual property.

- February 2025: CEPI awarded DNA Script USD 4.7 million to speed automated DNA template production for mRNA vaccines, supporting the 100 Days Mission.

- September 2024: Constructive Bio closed a USD 58 million Series A with Nobel Laureate Sir Gregory Winter joining the board to advance custom-genome engineering.

Gene Synthesis Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the gene synthesis market as the commercial value generated when providers assemble double-stranded DNA fragments base by base, without a template, and deliver full genes ready for cloning, screening, or therapeutic use. According to Mordor Intelligence, the sizing covers service fees and kits for fragments up to 200 kb, regardless of downstream application or delivery vector.

Scope Exclusion: We intentionally leave out equipment sales for benchtop DNA printers and any revenue from short oligonucleotide orders below sixty base pairs.

Segments Covered in This Report

- By Synthesis Method

- Chemical Oligonucleotide Synthesis

- Solid-Phase Phosphoramidite

- Microchip-based Oligonucleotide Synthesis

- Gene Assembly

- PCR-mediated

- Ligation-mediated

- Chemical Oligonucleotide Synthesis

- By Service Type

- Antibody DNA Synthesis

- Viral Gene Synthesis

- Others

- By Application

- Gene and Cell Therapy Developments

- Vaccine Development

- Disease Diagnosis

- Others

- By End User

- Biopharmaceutical Companies

- Academic & Government Institutes

- CROs and CDMOs

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed manufacturing engineers, market-development managers, academic core-facility heads, and procurement leads across North America, Europe, and Asia-Pacific. These conversations tested assumptions on sequence length limits, regional turn-around norms, and average selling price movements, helping us refine cost curves and future uptake thresholds.

Desk Research

We started with public datasets from sources such as the National Center for Biotechnology Information, the International Genetically Engineered Machine registry, OECD biotechnology statistics, United States customs trade codes, and peer-reviewed journals tracking synthetic biology funding. Annual reports, 10-K filings, investor decks, and reputable press releases let our team benchmark service pricing and capacity shifts. Premium inputs from D&B Hoovers and Dow Jones Factiva enriched company-level splits and recent expansion updates. This list is illustrative; many additional open datasets supported fact checks throughout our work.

Market-Sizing & Forecasting

Our model begins with a top-down rebuild of global demand using published synthesis volume, average price per base pair, and regional funding flows. It then corroborates results through selective bottom-up supplier roll-ups. Variables such as NIH and Horizon Europe grant commitments, gene-therapy trial starts, average fragment length, and microarray throughput rates feed a multivariate regression that projects revenues through 2030. Gaps where vendor disclosures are partial are bridged with triangulated ASP trends and shipment patterns before totals are finalized.

Data Validation & Update Cycle

Our outputs undergo multi-level variance checks, peer review, and senior analyst sign-off. The dataset refreshes annually, with interim updates triggered by funding shocks, regulatory shifts, or major capacity additions.

How Mordor Intelligence's Gene Synthesis Market Size Compares to Other Published Estimates

Published estimates often diverge because some firms mix oligo synthesis, exclude kit revenues, or freeze prices at a single region and year. We select a consistent scope, apply transparent unit economics, and update our model more frequently, which is why clients lean on us.

Key gap drivers include narrower application coverage elsewhere, outdated currency conversions, and volume estimates that ignore the rapid microarray adoption visible in patent filings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.45 B (2025) | Mordor Intelligence | - |

| USD 1.76 B (2022) | Global Consultancy A | Excludes kit revenue, uses static 2022 prices |

| USD 2.28 B (2023) | Research Firm B | Omits Asia-Pacific capacity expansion, limited primary checks |

| USD 2.55 B (2025) | Trade Journal C | Counts short oligo sales within totals |

Together, these comparisons show that Mordor's disciplined scope, timely refresh cycle, and dual-layer validation give decision-makers a balanced, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the current size of the gene synthesis market?

The gene synthesis market size is USD 2.85 billion in 2026, with a forecast value of USD 6.09 billion by 2031 at a 16.38% CAGR.

Which region leads the gene synthesis market?

North America leads with 41.88% of 2025 revenue, buoyed by strong biopharma demand, generous federal funding, and a clear regulatory pathway.

Which synthesis method is growing the fastest?

Gene assembly and other next-generation methods are projected to grow at a 17.06% CAGR, outpacing traditional chemical approaches thanks to longer read lengths and lower error rates.

Why are CROs and CDMOs gaining share in gene synthesis?

Pharmaceutical firms increasingly outsource synthesis to specialized providers, driving a projected 17.18% CAGR for CRO and CDMO revenue over the forecast period.

What major regulatory trends affect market growth?

The FDA’s doubling of annual gene-therapy approvals and the U.S. Executive Order on biotechnology screening both increase demand while clarifying compliance expectations.

How are enzymatic platforms influencing cost and speed?

Enzymatic DNA printers such as SYNTAX can produce purified oligos in hours, cutting turnaround time and reducing hazardous waste, which is accelerating adoption among research and manufacturing users.

Page last updated on: