Netherlands Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

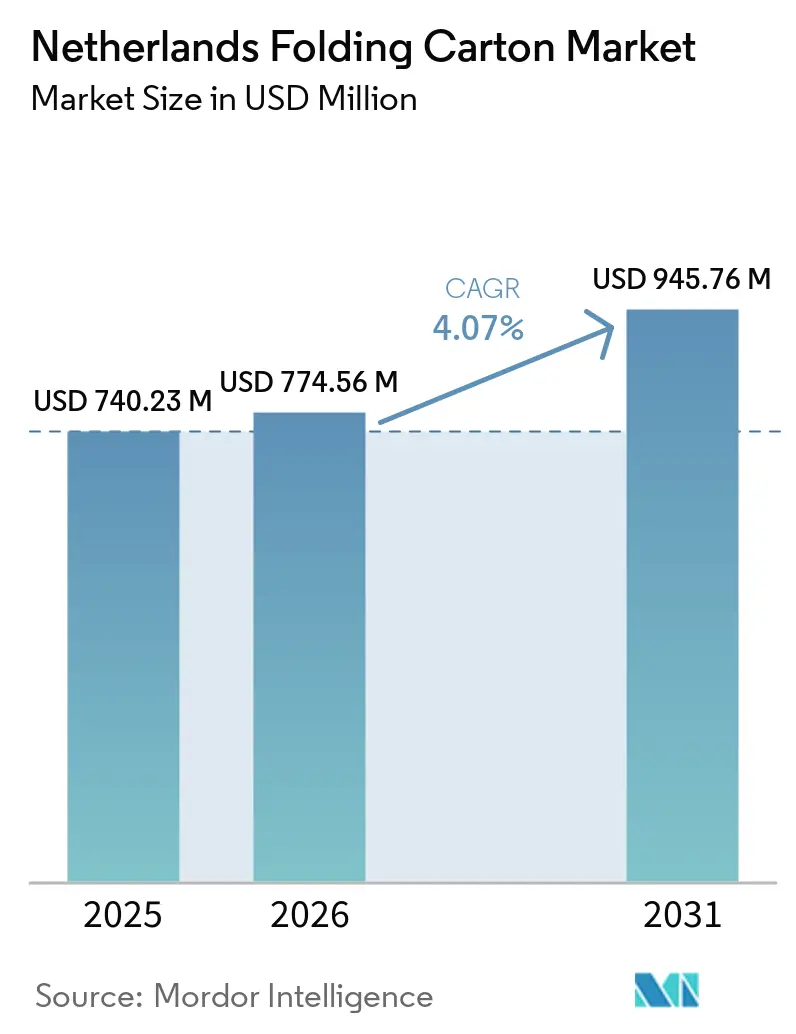

| Base Year Market Size (2025) | USD 740.23 Million |

| Market Size (2026) | USD 774.56 Million |

| Market Size (2031) | USD 945.76 Million |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

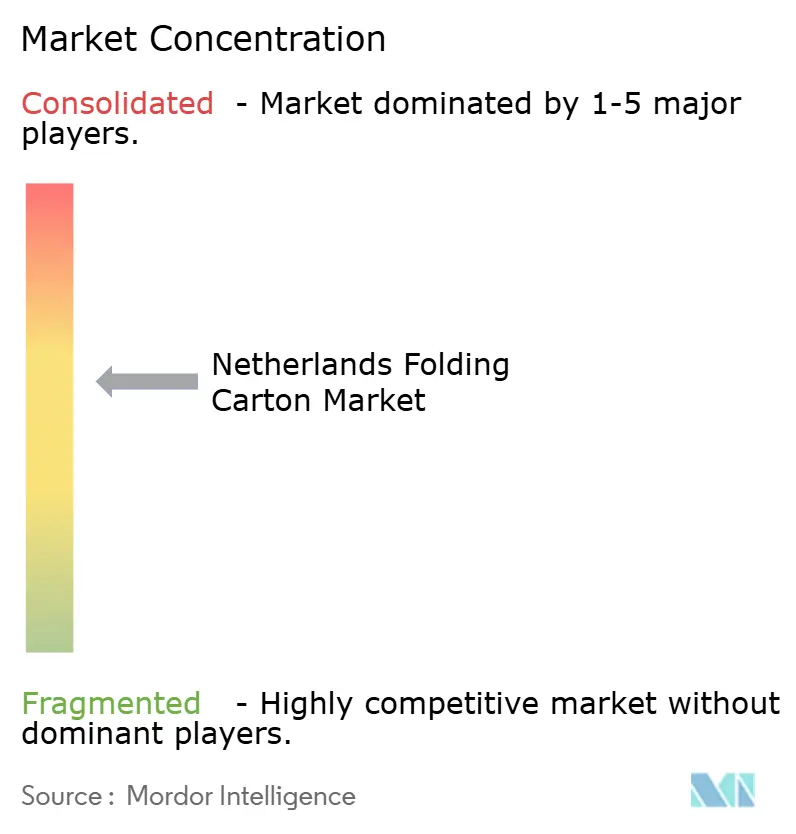

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Folding Carton Market Analysis by Mordor Intelligence

The Netherlands folding carton market size is projected to expand from USD 740.23 million in 2025 and USD 774.56 million in 2026 to USD 945.76 million by 2031, registering a CAGR of 4.07% between 2026 and 2031. Consistent e-commerce growth, tighter European Union packaging rules coming into force in August 2026, and a well-established recycling infrastructure underpin volume gains, even as price swings in recovered paper and labor shortages temper converter profitability. Online consumer spending in the country reached EUR 36 billion (USD 39.6 billion) in 2024, translating into 20% of total retail sales and spurring demand for protective, right-sized cartons. The European Union Packaging and Packaging Waste Regulation (PPWR) sets a 50% cap on empty space for e-commerce shipments starting in 2026, pushing converters toward modular designs and rapid prototyping. Material supply remains favorable because the Netherlands recycles 77% of all packaging, yet a EUR 70-per-tonne (USD 77-per-tonne) spike in Old Corrugated Containers in April 2025 illustrated the cost volatility facing paperboard users. Multinationals such as Smurfit WestRock benefit from integrated Dutch mill-to-conversion footprints, while specialist independents pursue high-graphic, short-run niches.

Key Report Takeaways

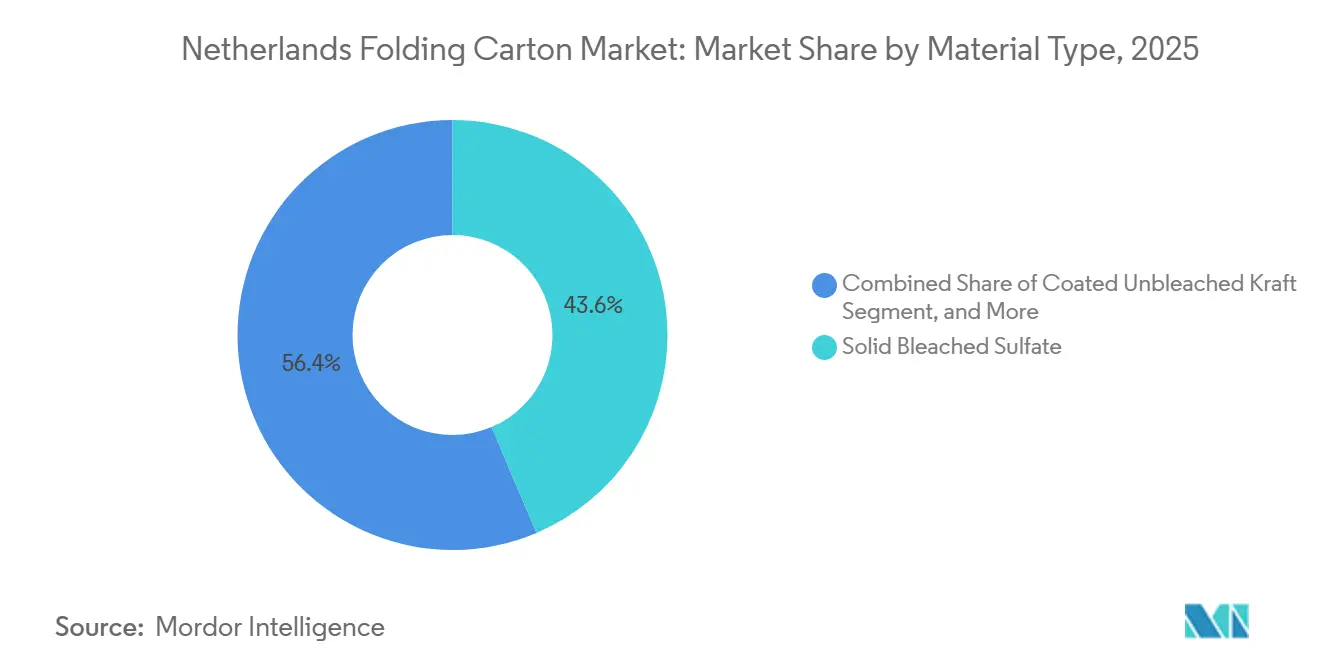

- By material type, solid bleached sulfate captured with 43.61% of the Netherlands folding carton market share in 2025.

- By printing technology, the Netherlands folding carton market size for digital printing is projected to grow at a 5.56% CAGR to 2031.

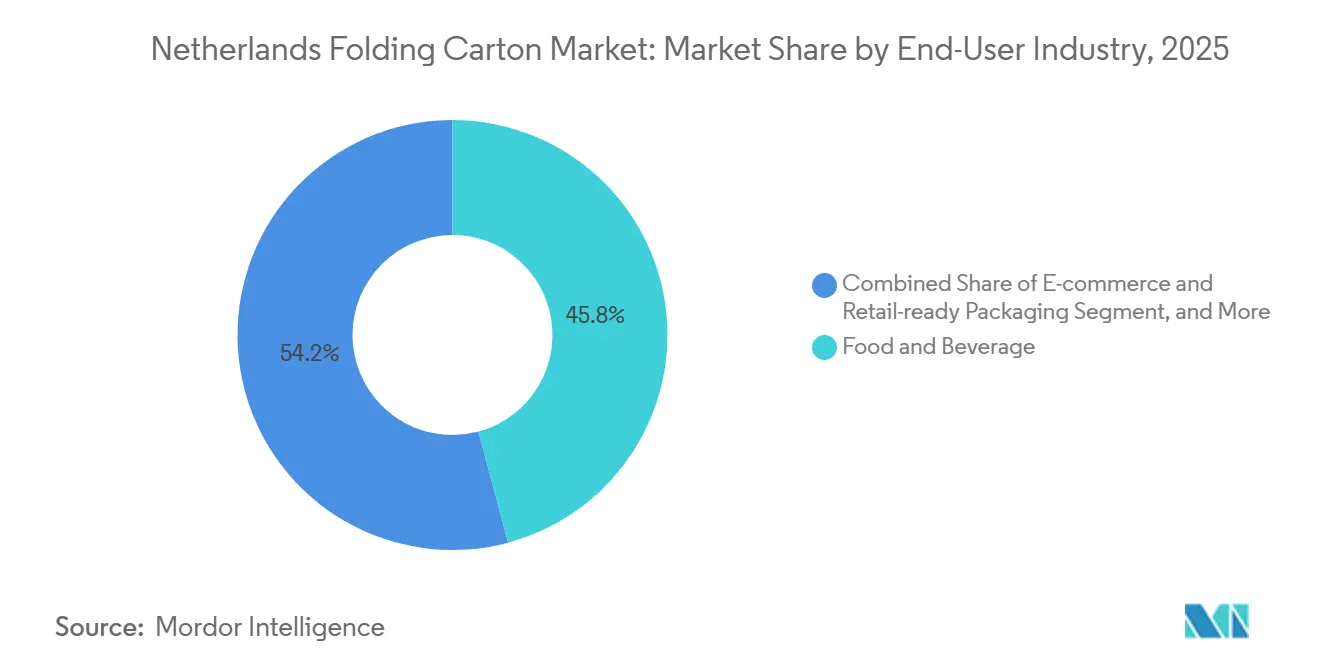

- By end-user industry, the food and beverage industry captured 45.83% of the Netherlands folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Netherlands Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing E-Commerce Penetration Fuels Demand For Protective Folding Cartons | +1.2% | National, Randstad corridor | Short term (≤ 2 years) |

| Sustainability Regulations Accelerate Shift To Recyclable Paperboard | +0.9% | National, EU-wide PPWR alignment | Medium term (2-4 years) |

| Premiumization Of Food And Beverage Packaging Boosts High-Quality Print Cartons | +0.6% | National, exports to Germany, Belgium, France | Medium term (2-4 years) |

| Retail-Ready Packaging Adoption In Dutch Supermarkets | +0.5% | National, led by major grocery chains | Short term (≤ 2 years) |

| Rise Of Pharmaceutical Cold-Chain Logistics Needs Robust Cartons | +0.4% | Life-sciences clusters | Long term (≥ 4 years) |

| Custom Short-Run Digital Printing Enables SME Branding | +0.3% | National SME base | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing E-Commerce Penetration Fuels Demand for Protective Folding Cartons

Twelve Dutch regions ranked among the 23 European Union areas where at least 80% of people aged 16-74 shopped online in 2024. Online retail already accounts for 20% of national consumer spending and is growing 7% per year, a trend strengthened by Amazon’s EUR 1.4 billion (USD 1.54 billion) three-year investment in logistics. Dutch small and medium enterprises exported EUR 894 million (USD 983 million) via online platforms in 2024, increasing parcel movements that require crush-resistant cartons. The PPWR’s 50% empty-space rule from 2026 obliges converters to engineer right-sized packs quickly, making modular footprints and CAD-driven prototyping key differentiators. Surveys from Thuiswinkel show Dutch shoppers now prefer fiber mailers over plastic, adding sustainability weight to cartonboard.

Sustainability Regulations Accelerate Shift to Recyclable Paperboard

The PPWR entered into force in February 2025 and, from August 2026, requires that every package sold in the bloc meet design-for-recycling criteria.[1]MAAK Advocaten, “The EU Packaging and Packaging Waste Regulation,” maakadvocaten.nl Paper and cardboard recycling targets climb to 85% by 2030, while extended producer responsibility (EPR) fees rise steeply for multi-material or non-recyclable packs. The Netherlands Packaging Management Decree already imposes markedly higher EPR tariffs on plastic, EUR 1.05 per kg (USD 1.16 per kg), than on paper, tilting cost structures toward mono-material cartons. CE Delft’s May 2025 study for the Dutch government urged stronger eco-modulation and even deposit-style incentives for beverage cartons, foreshadowing additional regulatory tailwinds. Retailer Albert Heijn now requires own-brand suppliers to submit packaging data and improvement plans via the TraceOne portal, effectively making recyclability a listing prerequisite.

Premiumization of Food and Beverage Packaging Boosts High-Quality Print Cartons

Craft brewers, specialty coffee roasters, and artisan chocolatiers are replacing generic sleeves with cartons that combine lithographic graphics, embossing, and tactile varnishes to justify higher price points. Smurfit WestRock Van Mierlo designed a fully recyclable E flute carton for La Trappe beer that substitutes wooden crates while retaining luxury cues, using gold foil and interior wood-grain motifs for shelf impact. Van Genechten’s Pure Packaging integrates an anti-grease barrier directly into folding boxboard, eliminating the need for an inner aluminum wrap and saving EUR 5 per 1,000 packs (USD 5.5 per 1,000). Rabobank data show branded grocery sales are widening their lead over private label, reinforcing the need for high-definition print and unique structures that signal premium quality.

Retail-Ready Packaging Adoption in Dutch Supermarkets

Supermarket groups such as Albert Heijn and Jumbo are pushing suppliers toward shelf-ready cartons that double as display units, cutting in-store labor and speeding replenishment. Albert Heijn’s packaging-reduction drive removed 13 million kg of material by 2025, largely through smarter carton dimensioning and switching from plastic clips to paper alternatives. Labor scarcity 79% of Dutch manufacturing executives cite difficulty hiring skilled shelf stockers, which adds impetus because shelf-ready formats reduce handling time. Reuse-and-refill pilots in The Hague illustrate long-term substitution risk for single-use packs, yet consumer uptake remains modest, so near-term demand for sturdy, retail-ready cartons is firm.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Recovered Paper Prices Erodes Converter Margins | -0.7% | National, linked to global waste-paper flows | Short term (≤ 2 years) |

| Competition From Flexible Plastic Pouches In Dry Food Applications | -0.5% | Snack foods and confectionery | Medium term (2-4 years) |

| Limited Domestic Paperboard Production Capacity | -0.3% | Import dependence on Germany, Finland, Sweden | Long term (≥ 4 years) |

| Labor Shortages In Skilled Press Operators | -0.2% | SMEs with legacy presses | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility In Recovered Paper Prices Erodes Converter Margins

European Old Corrugated Containers prices spiked by EUR 70 per tonne (USD 77 per tonne) within weeks in April 2025, lifting delivered rates to EUR 150 per tonne (USD 165 per tonne). Dutch recovered-paper exports declined 9% in 2024 because high energy costs forced mill outages, tightening local supply and amplifying price swings. New European Union rules restrict waste-paper shipments to non-OECD nations, which may stabilize supply long term, but demand fresh capital for domestic sorting plants. Currency and freight shifts add complexity: euro strength hurt exports to dollar-denominated markets, while container rates to Southeast Asia fell from USD 500 to USD 300, altering arbitrage.

Competition From Flexible Plastic Pouches In Dry Food Applications

Stand-up pouches offer lighter weight and resealability that attract snack and confectionery brands aiming to cut transport emissions per serving. Ceresana projects European flexible-packaging demand to reach 19.05 million tons by 2031, with films capturing share from rigid cartonboard. PPWR recyclability grades could curb multi-layer plastic if downgraded to grade C, yet converters of mono-polyethylene and mono-polypropylene structures are racing to stay compliant. HP Indigo’s USD 50 million press deal with ePac, installing ten 200K digital units in Europe and North America, amplifies the short-run, high-graphic strengths of flexible pouches, intensifying rivalry with digitally printed folding cartons.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Kraft Grades Strengthen Their Appeal

Solid Bleached Sulfate retained 43.61% of the Netherlands folding carton market share in 2025, reflecting its premium print surface and its compliance with food-contact standards that meet pharmaceutical and luxury confectionery codes. Coated Unbleached Kraft is expected to post a 5.25% CAGR to 2031, as its natural brown hue signals sustainability without sacrificing lithographic quality. The Netherlands's folding carton market benefits from Graphic Packaging’s OmniKote, which layers coatings to deliver clean printable faces while using up to 65% biomass energy in production.[2]Graphic Packaging International, “OmniKote Coated Unbleached Paperboard,” graphicpkg.com KraftPak from Smurfit WestRock, certified compostable under ASTM D6400, broadens usage into beverage carriers and foodservice, underscoring Kraft’s versatility.

White Line Chipboard and folding boxboard occupy cost-sensitive tiers for dry groceries and household items, but lightweight Solid Bleached Sulfate is beginning to cannibalize these grades as converters shave basis weight. Recycled-content boards supplying frozen or greasy foods still play a niche role, though PPWR rules encouraging higher recyclate percentages could lift their share. The Netherlands folding carton market share for materials incorporating high post-consumer fiber may expand if domestic utilization of the 2.03 million tons paper-for-recycling pool increases.

By Printing Technology: Digitization Moves from Niche to Norm

Lithographic processes commanded 39.57% revenue share in 2025, prized for consistent color and inline finishing at medium to long runs. Nevertheless, digital output is forecast to climb at a 5.56% CAGR through 2031 as brand proliferation, SKU rationalization, and localization erode the economic sweet spot for plate-based litho. Kartonplus operates Xeikon roll-fed presses with 1,000-unit minimums, supporting SMEs that demand quick changeovers and versioned graphics.

The Netherlands folding carton market is seeing real improvements in digital job output because AI-enabled defect detection on new HP Indigo 200K presses reduces waste and makeready time. Flexography keeps a foothold where high line speeds outweigh ultra-fine detail, especially in post-print corrugated. Gravure stays confined to massive, standard designs in tobacco or confectionery where cylinder amortization is justified. Hybrid flexo-digital lines are appearing at mid-size converters, shrinking changeover windows from around 45 minutes to 20 minutes and reducing substrate waste by nearly 8%.

By End-User Industry: Online Channels Lead Growth Curve

Food and beverage applications accounted for 45.83% of the Netherlands' folding carton market in 2025, spanning cereal, dairy, confectionery, and beverage multipacks. Portion control, tamper evidence, and premium finishes keep folding cartons central to freezer, chilled, and ambient aisles. E-commerce and retail-ready packaging, however, will grow fastest at 5.84% CAGR through 2031 as Amazon’s Dutch network expands and the PPWR enforces tighter void limits that favor right-sized carton geometries.

Pharmaceutical cold-chain expansion drives demand for serialization, aggregation, and temperature-indicator cartons, serviced by Valuepack’s Dutch facilities compliant with EU FMD codes. Personal care brands rely on soft-touch, foil-accented cartons to communicate efficacy and indulgence, while electronics and tobacco show structurally flat volumes amid miniaturization and public-health policies.

Geography Analysis

The Netherlands exports roughly 70% of its paper and board output to neighboring Germany, Belgium, and France, reflecting its role as a Western European logistics hub. Domestic folding-boxboard capacity remains modest at 140 kt per year, so converters import virgin and coated grades from Finland, Sweden, and Germany, exposing buyers to freight and currency fluctuations. Metsä Board’s January 2026 purchase of the Winschoten Sheeting and Distribution Hub gives Finnish fiberboard easier, just-in-time access to Dutch clients, trimming lead times and inventory risk.[3]EUWID Paper, “Metsä Board Completes Winschoten Acquisition,” euwid-paper.com

Integrated suppliers such as Smurfit WestRock leverage in-country mills at Parenco and Roermond to balance recycled and virgin furnish, ensuring continuity even when import lanes tighten. Recovered-paper exports fell 9% in 2024, increasing local availability but also amplifying price cyclicality when Asian demand weakens. Container freight rates from Rotterdam to Southeast Asia dropped to USD 300 in late 2025, temporarily improving outward competitiveness before rebounding amid vessel imbalances.

Harmonized PPWR rules across the bloc eliminate country-specific exemptions, leveling the regulatory playing field while forcing Dutch converters to meet the highest common standard by 2026. Border-free e-commerce throughout the Schengen Area means that conformity with grade-A recyclability becomes a de facto license to operate region-wide, lifting expectations on Dutch folding-carton design and labeling.

Competitive Landscape

The Netherlands folding carton market is moderately fragmented, with the top five suppliers accounting for 45% of combined revenue. Smurfit WestRock leads with vertically integrated assets ranging from recovered-fiber collection to carton converting, enabling rapid design-to-store cycles for premium projects such as La Trappe’s E-flute beer carton. Grenadier Packaging’s December 2025 acquisition of the MM Packaging Leeuwarden plant introduced a new consolidator backed by private equity, highlighting the attractiveness of Dutch capacity as a springboard to continental clientele.[4]Simon Matthis, “Grenadier Packaging Acquires MM Packaging Leeuwarden,” pulpapernews.com

Digital-first independents, including Kartonplus and UniqueCarton, capture the SME market with 48-hour turnaround and no plate charges, while midsize converters invest in hybrid lines to reduce changeovers and maintain litho quality. Labor constraints encourage automation: AI-based vision systems spot print defects in real time, and enterprise resource planning integrations reduce pre-press labor by 20%, mitigating operator shortages cited by 79% of manufacturers.

Strategic focus areas center on mono-material barrier coatings that replicate pouch functionality, cartonboard solutions for the pharmaceutical cold-chain, and shelf-ready designs that minimize in-store handling. Suppliers able to guarantee grade-A recyclability alongside high-definition print stand to command price premiums once PPWR penalties for non-recyclable laminates begin in 2030.

Netherlands Folding Carton Industry Leaders

Van Genechten Packaging NV

Clondalkin Group Holdings BV

hubergroup Deutschland GmbH

Klingele Paper & Packaging SE & Co. KG

Smurfit WestRock plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sonoco S.a.r.l. raised EMEA uncoated recycled paperboard prices by EUR 80 per ton (USD 88 per ton) and tube and core prices by 8%, citing continued energy and chemical inflation.

- March 2026: Metsä Board shareholders authorized issuance of up to 35 million Series B shares and repurchase of 1 million shares, providing funding flexibility amid market volatility.

- February 2026: HP Indigo and ePac Flexible Packaging signed a USD 50 million, three-year deal for ten HP Indigo 200K presses, boosting European digital flexible-packaging capacity.

- January 2026: Metsä Board completed the Winschoten Sheeting and Distribution Hub acquisition, deepening its Dutch downstream network.

Netherlands Folding Carton Market Report Scope

The Netherlands Folding Carton market report analyzes fiber-based packaging solutions, including virgin and recycled paperboard. The research focuses on the Dutch domestic landscape while accounting for the impact of EU-wide sustainability mandates, such as the Single-Use Plastics Directive, and local regulatory shifts, such as the Netherlands' Fee Modulation Plastic 2.0.

The Netherlands Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Netherlands folding carton market?

The Netherlands folding carton market size reached USD 774.56 million in 2026 and is projected to climb to USD 945.76 million by 2031.

Which material holds the largest share in Dutch folding cartons?

Solid Bleached Sulfate led with 43.61% share in 2025, favored for its brightness and food-contact compliance.

Why are digital presses gaining traction among Dutch converters?

Brand proliferation and frequent design changes make plate-free digital presses economical for runs as low as 1,000 units, driving a forecast 5.56% CAGR for digital printing through 2031.

How will the EU Packaging and Packaging Waste Regulation affect Dutch converters?

From August 2026, all packs must meet design-for-recycling rules and comply with stricter labeling, pushing suppliers toward mono-material, grade-A recyclable carton designs.

Which end-use segment is expanding fastest?

E-commerce and retail-ready packaging is set to advance at a 5.84% CAGR through 2031, supported by Amazon’s USD 1.54 billion Dutch logistics build-out.

What is the main cost headwind for the sector?

Volatile recovered-paper prices, which jumped EUR 70 per ton (USD 77 per ton) in early 2025, remain the biggest margin pressure for converters relying on recycled fiber.

Page last updated on: