Austria Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

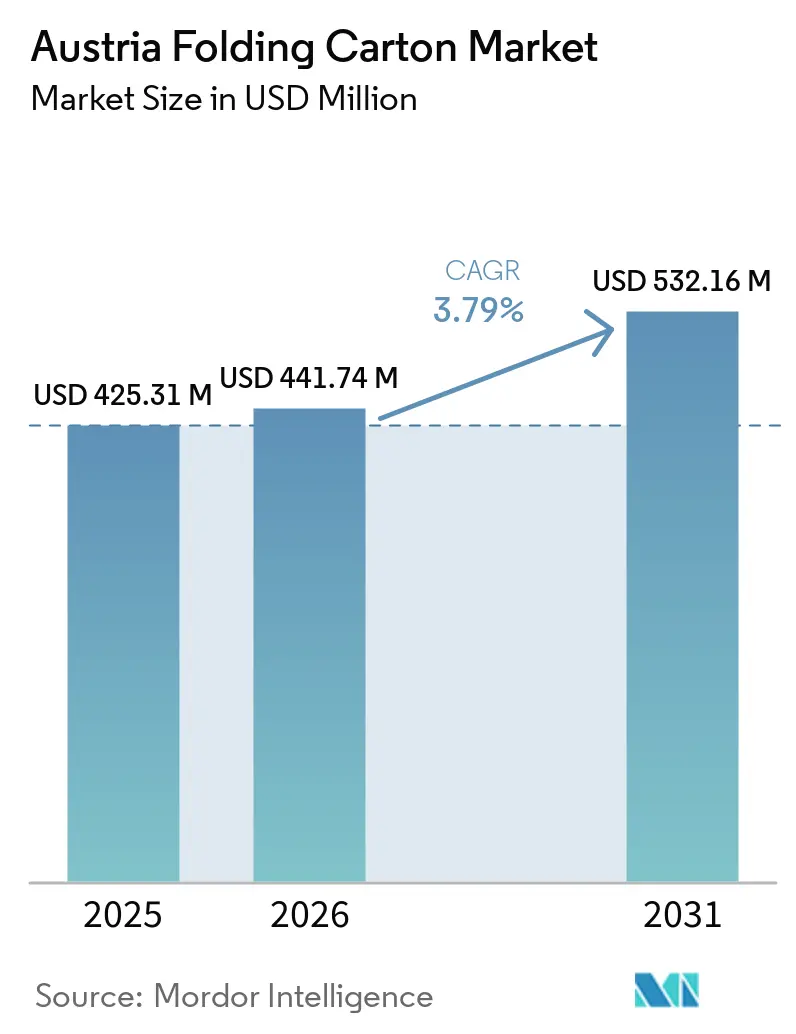

| Base Year Market Size (2025) | USD 425.31 Million |

| Market Size (2026) | USD 441.74 Million |

| Market Size (2031) | USD 532.16 Million |

| Growth Rate (2026 - 2031) | 3.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Folding Carton Market Analysis by Mordor Intelligence

The Austria folding carton market size is expected to grow from USD 425.31 million in 2025 to USD 441.74 million in 2026 and is forecast to reach USD 532.16 million by 2031 at a 3.79% CAGR over 2026-2031. Mature but still expanding, the Austria folding carton market continues to benefit from the European Union Packaging and Packaging Waste Regulation that starts to apply in August 2026, which encourages fiber-based formats through mandatory recyclability, recycled-content targets and stricter design rules. Export-oriented converters already ship roughly 80% of output to Germany and other neighbors, so any upswing in Central European consumption quickly feeds local order books. Demand also receives support from surging organic food exports, premium cosmetics launches and e-commerce transactions that together drive short-run, high-graphics cartons. At the same time, volatile pulp and energy costs alongside acute labor shortages compress operating margins, making automation and digital workflows crucial for competitiveness.

Key Report Takeaways

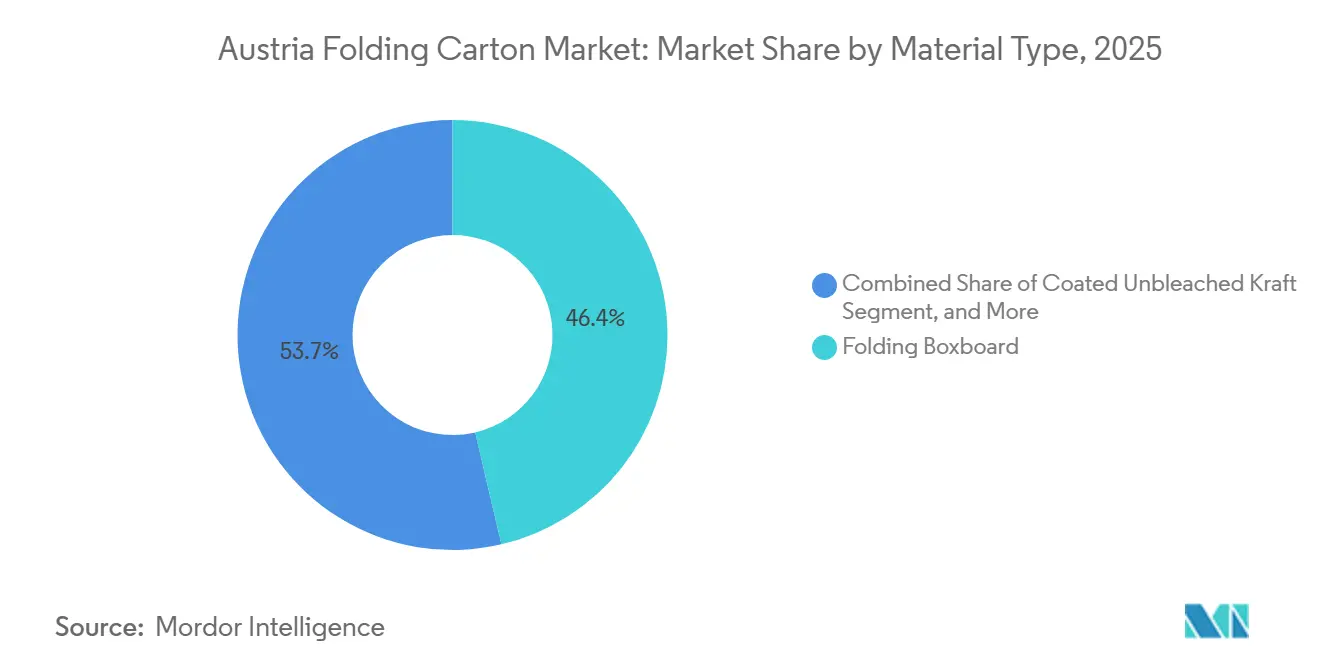

- By material type, folding boxboard captured with 46.35% of the Austria folding carton market share in 2025.

- By printing technology, the Austria folding carton market size for digital platforms is projected to grow at a 4.89% CAGR to 2031.

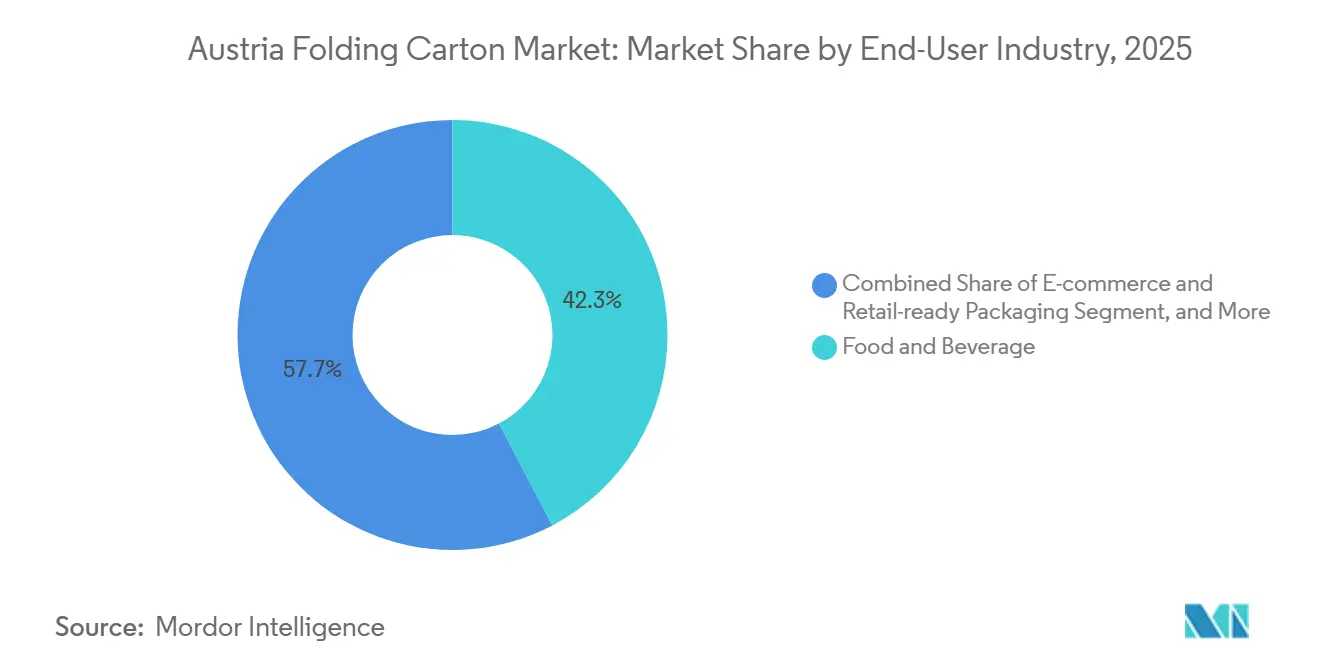

- By end-user industry, the food and beverage industry captured 42.31% of the Austria folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Austria Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability Regulations Accelerating Fiber-Based Packaging Adoption | +1.2% | Austria and broader EU compliance zone | Medium term (2-4 years) |

| Growth of Austria's Organic Food Exports Requiring Premium Carton Solutions | +0.8% | Austria with export corridors to Germany, Italy and France | Medium term (2-4 years) |

| E-Commerce Surge Driving Small-Lot Offset Carton Runs | +0.9% | Austria concentrated in Vienna and urban centers | Short term (≤ 2 years) |

| Automated Filling Lines Demanding High-Strength Carton Substrates | +0.5% | Austria regional food and beverage manufacturing hubs | Long term (≥ 4 years) |

| Brand Owner Shift Toward Plastic Replacement in Cosmetics and Personal Care | +0.6% | Austria with spillover to Central Europe | Medium term (2-4 years) |

| Smart Packaging Features Increasing Value of Digitally Printed Cartons | +0.4% | Austria early adoption in pharma and premium food | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainability Regulations Accelerating Fiber-Based Packaging Adoption

The EU Packaging and Packaging Waste Regulation obliges every package placed on the market after 2030 to demonstrate recyclability and to respect maximum empty-space ratios, so Austrian brand owners increasingly specify folding cartons that qualify for the highest recyclability grades. National rules already require a 75% recycling rate for fiber packaging and lift that target to 85% by 2030, giving domestic converters a compliance head start. Extended producer responsibility fees will soon vary by recyclability grading, so mono-material cartons will gain a clear economic advantage. The regulatory push aligns with consumer sentiment strongly favoring renewable substrates, thereby underpinning sustained growth in the Austrian folding carton market.

Growth of Austria's Organic Food Exports Requiring Premium Carton Solutions

Organic farmland already covers 27.2% of Austria’s agricultural area, and organic food sales reached EUR 3.139 billion (USD 3.54 billion) in 2024, expanding 6% year on year. Export-oriented organic dairies and meat processors need eye-catching yet sustainable packaging that communicates quality credentials through embossing, spot varnish, and certification labels. Luxury folding cartons made from solid bleached sulfate satisfy these design demands while meeting EU organic production traceability rules, a combination that reinforces premium pricing and helps expand the Austria folding carton market.

E-Commerce Surge Driving Small-Lot Offset Carton Runs

Austrian online retail generated USD 13.45 billion in 2025 and is growing at 6.13% annually through 2030, with mobile commerce accounting for 58% of transactions. E-commerce favors quick lead times and variable graphics, so converters with digital or hybrid presses secure incremental share. Vienna accounts for around 40% of national e-commerce spend, yet broadband upgrades are unlocking rural demand, enabling regional plants to expand their delivery radii. The trend to cross-border shopping, now 65% of spend, raises efficiency benchmarks set by German mega-fulfillment centers, encouraging Austrian plants to automate die-cutting, gluing, and logistics.

Brand Owner Shift Toward Plastic Replacement in Cosmetics and Personal Care

Personal care companies race to phase out single-use plastics before the PPWR ban takes effect in 2030. Stora Enso’s 750,000-tonne Oulu board line, inaugurated in 2025, specifically targets premium personal care cartons and provides lighter, high-brightness substrates that suit intricate embellishments.[1]EUWID Paper, “Stora Enso Inaugurates New Board Line in Oulu,” euwid-paper.com Mayr-Melnhof’s GreenPeel and Carton Cavity technologies eliminate the need for plastic inserts, while grease- and aroma-barrier coatings expand use in lipstick or fragrance sets. Such innovations bolster value growth in the Austria folding carton market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Pulp Prices Eroding Converter Margins | -0.7% | Austria, with exposure to European and global pulp streams | Short term (≤ 2 years) |

| Competition From Flexible Packaging in Snack and Confectionery | -0.5% | Austria, with spillover from European trends | Medium term (2-4 years) |

| Labor Shortages in Austria's Converting Sector Inflating Operating Costs | -0.4% | Austria is concentrated in Styria, Upper Austria, and Vorarlberg | Long term (≥ 4 years) |

| Limited Recycling Capacity for Poly-Coated Cartons | -0.3% | Austria has regional infrastructure gaps | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Pulp Prices Eroding Converter Margins

Natural gas prices touched EUR 68 per MWh (USD 73.44 per MWh) in March 2026, and diesel rose to EUR 2.00 per liter (USD 2.16 per liter), inflating cost bases across European mills. Recycled-based producers are hit hardest, but even virgin-fiber players such as Mayr-Melnhof reported an impairment of EUR 70.5 million (USD 74.5 million) in 2025, while operating profit margins slipped to 5%. Smaller Austrian converters lacking long-term supply contracts rely on spot board purchases and therefore experience margin whiplash whenever pulp, recovered paper, or energy markets swing.

Competition From Flexible Packaging in Snack and Confectionery

Composite film pouches still deliver unrivaled moisture and oxygen barriers at lower gram weights than folding cartons. Despite EU policy favoring recyclable materials, snack brands weigh functional and cost trade-offs carefully. European flexible packaging will ease only slightly to 19.05 million tonnes by 2031, keeping price pressure alive. To defend share, carton suppliers invest in barrier boards like ALASKA BARRIER GREASE that resist oil migration and support full fiber recyclability, yet the capital costs of such upgrades temper gains for the Austria folding carton market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Grades Anchor Volumes While Virgin Fiber Captures Premium Margins

Folding boxboard generated 46.35% of Austria's folding carton market share in 2025, thanks to its balance of stiffness, printability, and cost efficiency across food, beverage, and consumer goods. Solid bleached sulfate, though smaller in volume, is forecast to grow at 5.19% CAGR to 2031 as luxury cosmetics and pharmaceutical buyers embrace its high-brightness surface. Investments like Stora Enso’s Oulu board line expand European supply and introduce lighter grades that also lower transport emissions. Coated unbleached kraft and white-lined chipboard cater to natural-look or price-sensitive niches, thereby rounding out converter portfolios.

Rising environmental expectations should accelerate the substitution of poly-laminated structures with mono-material or aqueous-coated boards that can enter existing fiber recovery streams, an evolution that reinforces Austria's leadership in the folding carton market size of virgin fibers in premium segments. At the same time, cartonboard imports from Finland and the Baltics intensify price competition and motivate Austrian mills to differentiate through service speed and design support.

By Printing Technology: Lithographic Dominance Faces Agile Digital Contenders

Lithographic presses still account for more than half of the Austrian folding carton market for printing, delivering color consistency and unit costs that favor runs of roughly 10,000 impressions or more. Yet digital sheet-fed and roll-to-sheet platforms are expanding at 4.89% annually, driven by limited-edition SKUs and personalized cartons for e-retail fulfillment. Rondo Ganahl added an integrated press line capable of three printing processes and food-safe inks at its St. Ruprecht plant to supply micro-lots without tooling delays.

Hybrid workflows that pair flexographic priming with inkjet or electrophotography further blur boundaries, letting converters slash makeready times. Mandatory EU pictograms and QR-based disposal guidance from 2028 will multiply variable data requirements, giving digital early adopters a commercial edge. Consequently, lithographic incumbents reinvest in plate automation, color management, and robotic material handling to protect their market share in the Austrian folding carton market.

By End-User Industry: Food and Beverage Command Volumes, E-Commerce Unlocks New Formats

Food and beverage accounted for 42.31% of Austria's folding carton market demand in 2025, as bakeries, dairies, and beverage fillers seek grease- and moisture-resistant boards that maintain shelf appeal and recyclability. Organic offerings carry higher carton spend per unit because they require premium graphics and certification labels. E-commerce and retail-ready packaging, however, shows a 5.27% CAGR to 2031, mirroring Austria’s robust online retail growth.

Cartons optimized for automated filling lines, easy returns, and unboxing aesthetics gain traction, particularly among fashion and electronics sellers. Healthcare and pharmaceutical applications also strengthen, driven by stricter serialization rules and the ongoing boom in GLP-1 therapies, which Mayr-Melnhof serves through its Pharma and Healthcare division, responsible for USD 529 million in sales during the first nine months of 2025. Personal care, electronics, household goods, and tobacco sustain mature but stable volumes.[2]Mayr-Melnhof Karton AG, “Report for the First Three Quarters 2025,” marketscreener.com

Geography Analysis

Vienna’s dense consumer base and role as an e-commerce hub underpin the region's highest consumption of folding cartons, driving steady demand for retail-ready and subscription box styles. Styria hosts Austria’s largest cluster of board mills and converting plants, including Mayr-Melnhof’s Frohnleiten site and Rondo Ganahl’s St. Ruprecht printing center, ensuring short supply chains and rapid prototyping capability.[3]Packaging Austria, “New Corrugated Line at Rondo Frastanz,” packaging-austria.at

Upper Austria improves the recycling ecosystem through the TriPlast sorting plant, which processes 100,000 tonnes of packaging annually, and the Sort4cycle advanced recycling facility under construction at Ennshafen, with commissioning planned for mid-2027. Vorarlberg, home to Rondo Ganahl’s headquarters, benefits from continued investment in corrugated and folding carton capacity, most recently a USD 18.6 million high-speed line commissioned in 2025.

Cross-border logistics corridors via the Brenner Pass, the Danube waterway, and the Bavarian road network maintain export competitiveness but also expose the Austrian folding carton market to foreign demand cycles and currency shifts. Smurfit WestRock’s kraftliner mill supplies virgin linerboard into Austria, integrating the country into a wider network of containerboard flows across Western Europe.

Competitive Landscape

Mayr-Melnhof Karton AG, Stora Enso, Smurfit WestRock, Prinzhorn Group, and Rondo Ganahl together dominate the mid-sized, export-heavy Austrian folding carton market. Mayr-Melnhof’s Fit-For-Future program aims to generate USD 282 million in structural profit gains by 2027 through procurement, automation, and footprint optimization, following a 5% operating margin on 2025 sales of USD 4.38 billion. Stora Enso’s EUR 1.1 billion (USD 1.2 billion) outlay at Oulu adds large-scale virgin board capacity and exerts pricing pressure across the continent.

Prinzhorn Group pursues vertical integration, evidenced by its USD 83.5 million acquisition of three Stora Enso corrugated plants in Germany in April 2026. White-space entrants include label converters pivoting into carton production via single-pass lines that combine printing, creasing, die-cutting, and stripping, delivering faster turnarounds and reduced energy per sheet.[4]Prinzhorn Group, “Automation Project Strasswalchen,” prinzhorngroup.com Across the board, capex priorities center on digital presses, robotics for packing and inline quality control, and functional coatings that displace plastics in high-barrier uses. Labor shortages, with wages up more than 20% over three years, reinforce the need for such automation.

Additionally, advancements in digital printing technologies are enabling greater customization and shorter production runs, meeting the rising demand for personalized packaging. This trend is particularly evident in the e-commerce sector, where brands are leveraging innovative packaging designs to enhance customer engagement and brand loyalty. As a result, companies are prioritizing investments in flexible and scalable production systems to stay competitive in this evolving market landscape.

Austria Folding Carton Industry Leaders

Smurfit WestRock plc

Mayr-Melnhof Karton AG

Stora Enso Oyj

Greiner Packaging International GmbH

RATTPACK Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Prinzhorn Group agreed to acquire Stora Enso’s German corrugated plants that posted USD 83.5 million in 2025 revenue, subject to antitrust clearance.

- April 2026: Construction began on the USD 45.2 million Sort4cycle advanced plastics recycling facility at Ennshafen, scheduled for mid-2027 start-up.

- March 2026: Mayr-Melnhof Karton AG reported 2025 revenue of USD 4.38 billion and confirmed Fit-For-Future savings of USD 79 million for the year.

- March 2025: Dunapack Packaging launched a USD 13 million automated high-bay warehouse at Strasswalchen, with completion due Feb 2026.

Austria Folding Carton Market Report Scope

The Austria Folding Carton Market encompasses the production, distribution, and use of folding cartons, lightweight, paper-based packaging solutions primarily used across industries such as food and beverage, pharmaceuticals, cosmetics, and others. The scope of the study includes an in-depth analysis of market dynamics, including key trends, growth drivers, challenges, and opportunities. Additionally, the study evaluates the competitive landscape, supply chain structure, and technological innovations shaping the market during the forecast period.

The Austria Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Austrian folding carton market, and what is its predicted value for 2031?

The Austria folding carton market size stands at USD 425.31 million in 2025, is expected at USD 441.74 million in 2026 and is projected to reach USD 532.16 million by 2031.

Which material type holds the largest share of Austria’s folding carton demand?

Folding boxboard led with 46.35% of Austria folding carton market share in 2025, driven by versatility across food, beverage and consumer goods.

Which end-user area is growing fastest for Austrian folding carton converters?

E-commerce and retail-ready packaging shows the quickest expansion at a 5.27% CAGR over 2026-2031 as online retail scales.

How are EU regulations shaping folding carton design in Austria?

The PPWR requires every package sold after 2030 to be recyclable and sets recycled-content and empty-space limits, so Austrian converters are shifting to mono-material, design-for-recycling cartons to avoid higher extended producer responsibility fees.

What strategies are leading companies adopting to protect margins?

Market leaders such as Mayr-Melnhof, Stora Enso and Prinzhorn Group are investing in automation, digital printing, barrier technologies and footprint consolidation to offset pulp-price volatility and labor cost inflation.

Why is digital printing important for Austria folding carton suppliers?

Digital presses enable short runs, variable data and faster lead times demanded by e-commerce brands, giving converters flexibility to serve personalized and limited-edition cartons without high plate costs.

Page last updated on: