Pneumococcal Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.69 Billion |

| Market Size (2031) | USD 12.33 Billion |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pneumococcal Vaccines Market Analysis by Mordor Intelligence

The Pneumococcal Vaccines Market size is expected to grow from USD 9.23 billion in 2025 to USD 9.69 billion in 2026 and is forecast to reach USD 12.33 billion by 2031 at 4.95% CAGR over 2026-2031.

Uptake is migrating from near-saturated pediatric programs in high-income economies to fast-growing adult schedules, a shift triggered by the 2024 U.S. approval of Merck’s Capvaxive (PCV21) that introduced eight serotypes absent from legacy formulations. GAVI’s decision to lock in a USD 2.75 dose ceiling through 2029 expanded procurement capacity across 57 low-income countries, while innovators such as Vaxcyte and Affinivax continue to chase ultra-valent conjugates that promise broader coverage and longer commercial life cycles. Adult vaccination momentum, local fill-finish partnerships in Asia-Pacific, and AI-driven serotype surveillance together underpin medium-term growth, yet manufacturing cost inflation, price negotiations under the Inflation Reduction Act, and cold-chain fragility in low-resource settings remain material constraints.

Key Report Takeaways

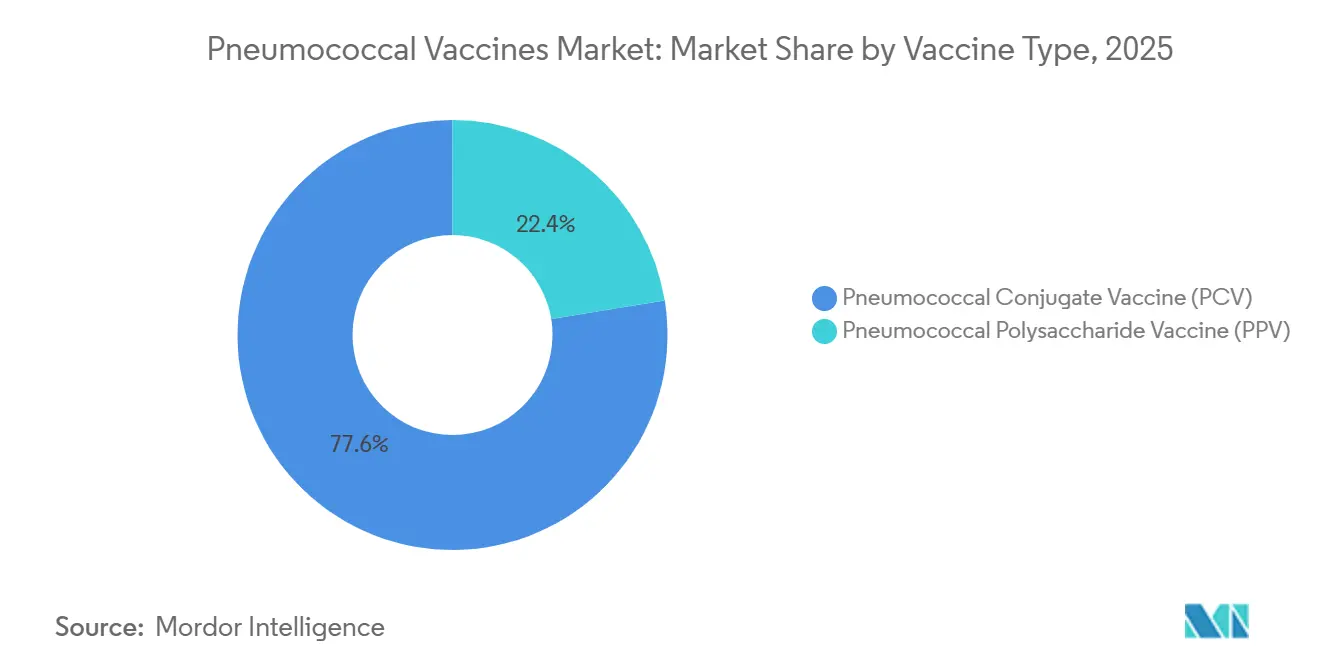

- By vaccine type, pneumococcal conjugate vaccines led with 77.56% of pneumococcal vaccines market share in 2025 and are advancing at an 8.25% CAGR through 2031.

- By product type, Prevnar 13 controlled 47.53% of the pneumococcal vaccines market size in 2025, while Prevnar 20 is forecast to post a 15.85% CAGR to 2031.

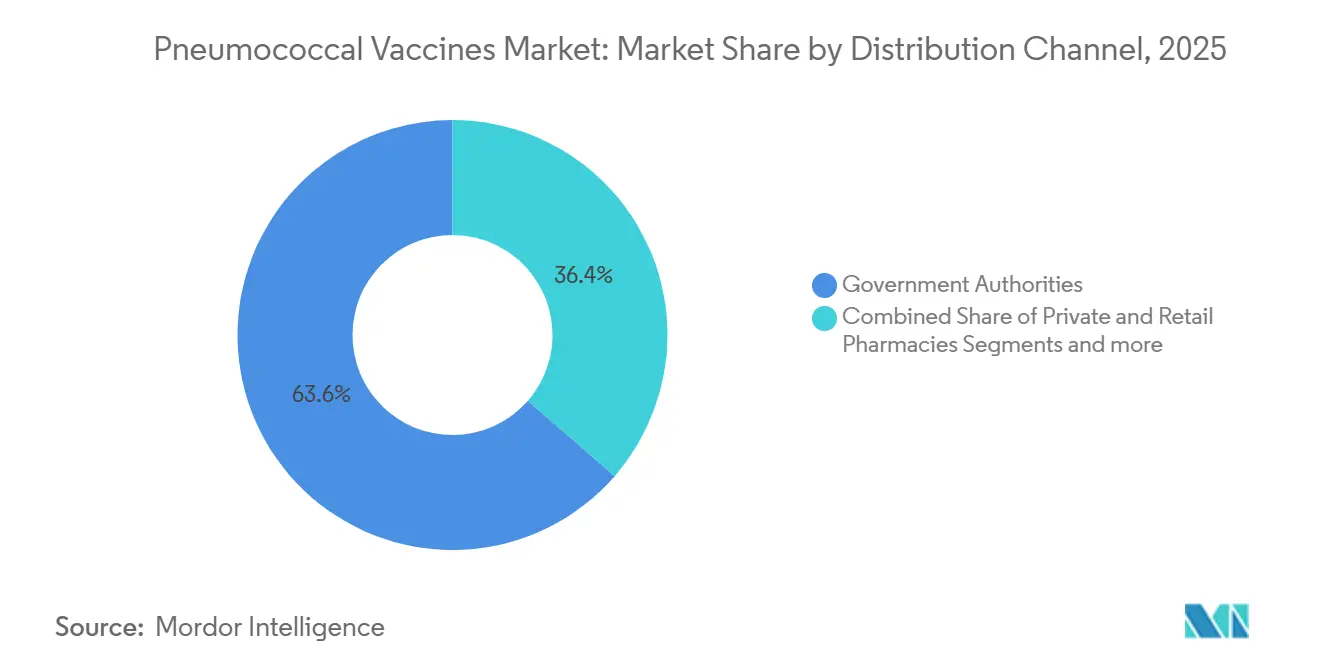

- By distribution channel, government authorities purchased 63.63% of 2025 doses, yet private and retail pharmacies are set to deliver a 10.87% CAGR to 2031.

- By age group, pediatric use captured 61.23% of 2025 demand, whereas the adult 19-64 cohort is on track to expand at a 6.7% CAGR through 2031.

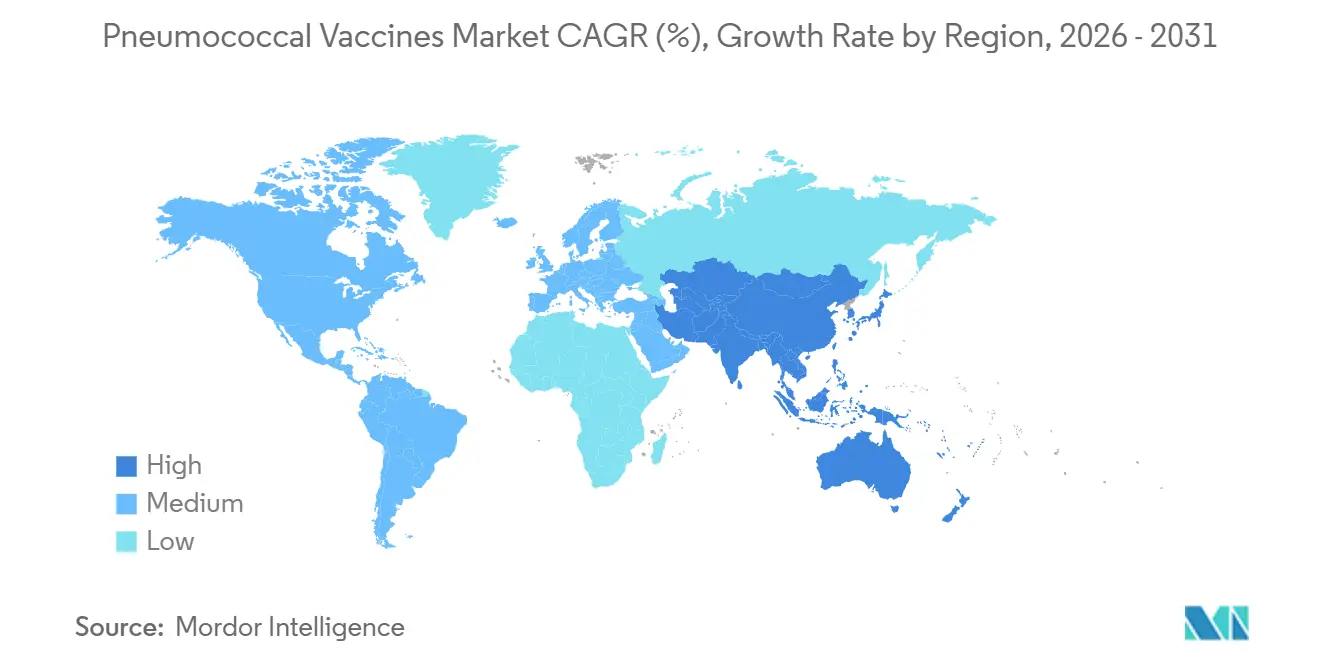

- By geography, North America contributed 38.53% revenue share in 2025, with Asia-Pacific forecast to be the fastest-growing region at 6.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pneumococcal Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased GAVI-funded uptake in LICs after USD 2.75/dose tender price | +1.2% | Sub-Saharan Africa, South Asia, select Latin America LICs | Medium term (2-4 years) |

| Rising prevalence of pneumococcal infections | +0.8% | Global, acute burden in APAC and MEA | Long term (≥ 4 years) |

| Launch of higher-valent PCVs (PCV15/20/21) | +1.5% | North America, Europe, Japan, China | Short term (≤ 2 years) |

| Pipeline of ultra-valent PCVs (≥ 30-valent) accelerating due-diligence deals | +0.9% | Global, early adoption in North America and EU | Long term (≥ 4 years) |

| AI-enabled serotype surveillance speeding label expansions | +0.6% | North America, Europe, select APAC hubs | Medium term (2-4 years) |

| Local fill-finish partnerships unlocking tariff-free entry in APAC | +1.0% | China, India, Southeast Asia; spill-over to MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increased GAVI-Funded Uptake in LICs After USD 2.75/Dose Tender Price

GAVI’s 2024 renewal of its Advance Market Commitment fixed pneumococcal conjugate vaccine procurement at USD 2.75 per dose, sustaining routine immunization in 57 low-income countries and injecting predictable volume that lifts the forecast CAGR by 1.2 percentage points. WHO prequalification of SK bioscience’s GBP301 in 2024 diversified supply and mitigated single-source risk. Long-run impact depends on governments co-financing doses as GAVI’s graduation schedules advance, a transition that could expose fragile health budgets to shortfalls. Manufacturers meanwhile pursue volume over margin, delaying ultra-valent launches in donor markets until new economics emerge.

Rising Prevalence of Pneumococcal Infections

CDC surveillance confirmed that invasive pneumococcal disease rates in U.S. adults 65+ remained above pre-pandemic baselines through 2024 despite PCV13 coverage, underscoring ongoing unmet need. Similar patterns persist in Asia-Pacific and Middle East & Africa where aging populations collide with historically low adult vaccination. The driver adds 0.8 percentage points to CAGR and is long term because building adult immunization infrastructure and reimbursement pathways is a slow, policy-heavy process. Emergent serotypes not covered by PCV13 further raise clinical urgency and validate higher-valent pipeline strategies.

Launch of Higher-Valent PCVs (PCV15/20/21)

Capvaxive’s approval in June 2024 brought eight new serotypes covering roughly 30% of U.S. adult disease burden, while Prevnar 20 won clearances in Japan and China, catalyzing guideline updates that have already widened adult eligibility. Rapid formulary inclusion in North America and Europe delivers a 1.5 percentage-point lift to CAGR. Health agencies moved swiftly; ACIP widened indications to adults 19-64 with risk factors, doubling the addressable base and accelerating commercial uptake[1]Centers for Disease Control and Prevention, “ACIP Recommendations,” CDC, cdc.gov.

Pipeline of Ultra-Valent PCVs (≥ 30-Valent) Accelerating Due-Diligence Deals

Vaxcyte secured USD 1.2 billion in 2024 to advance VAX-31, a 31-valent candidate employing cell-free synthesis that could cut production timelines and costs. GSK’s acquisition of Affinivax and its MAPS platform highlights incumbent anxiety over disruptive technology. The driver adds 0.9 percentage points to CAGR but materializes in the long term because regulatory pathways for 30-plus valencies remain undefined.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High manufacturing cost of conjugate vaccines | -0.7% | Global, acute in LMICs reliant on donor funding | Long term (≥ 4 years) |

| Serotype-replacement diminishing long-term efficacy | -0.5% | North America and Europe | Medium term (2-4 years) |

| IRA-linked U.S. price negotiations compressing adult-dose ASPs | -0.4% | United States | Short term (≤ 2 years) |

| Short-term cold-chain power outages tied to energy transition volatility | -0.3% | Sub-Saharan Africa, South Asia, select island nations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Manufacturing Cost of Conjugate Vaccines

Conjugation chemistry remains capital intensive, with 2024 U.S. estimates placing total capitalized development costs at USD 886.8 million per vaccine, shaving 0.7 percentage points off CAGR[2]U.S. Department of Health and Human Services, “Vaccine Development Costs,” HHS, hhs.gov. Scale economies help incumbents, yet donor markets demand sub-USD 3 pricing, capping margins and slowing diffusion of higher valencies. Disruptive platforms like cell-free synthesis have potential but will not be validated at scale before 2028.

Serotype-Replacement Diminishing Long-Term Efficacy

Surveillance shows rising disease from serotypes 22F, 33F, and 35B five to ten years after PCV13 adoption, eroding confidence in legacy products and knocking 0.5 percentage points from CAGR. The phenomenon presses manufacturers into perpetual reformulation, raising R&D spend and regulatory workload.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vaccine Type: Conjugate Chemistry Dominates, Polysaccharides Fade

Pneumococcal conjugate vaccines held 77.56% of pneumococcal vaccines market share in 2025, a position supported by T-cell–dependent immunity that sustains herd protection in infants. Their 8.25% CAGR through 2031 reflects strong adoption in both pediatric and newly eligible adult cohorts. Pneumococcal polysaccharide vaccines trail because they lack memory response and face utility erosion as conjugate alternatives gain adult indications, particularly after ACIP’s 2024 recommendation favoring PCV20 or PCV15 before PPSV23. Emerging-market payers still deploy polysaccharides to contain budgets, but WHO prequalification trends and cost-reducing tech may ultimately accelerate their displacement.

Conjugate production costs remain higher, yet payers in high-income markets accept premium prices knowing that reduced boosters offset long-run expenses. GAVI programs exclusively source conjugates for infants, while many middle-income countries use polysaccharides for seniors only, creating a dual-track procurement landscape. New platforms like Vaxcyte’s cell-free synthesis could cut cost curves and entrench conjugate leadership by widening the price-efficacy gap.

By Product Type: Prevnar Franchise Faces Disruption

Prevnar 13 accounted for 47.53% of pneumococcal vaccines market size in 2025, but Prevnar 20 is expanding at a 15.85% CAGR on the strength of its seven extra serotypes and rapid approvals in Japan and China[3]Pfizer Inc., “Pfizer Receives Approval in Japan for Prevnar 20,” Pfizer, pfizer.com. Merck’s Capvaxive (PCV21) entered the adult segment in 2024 and positions itself as a direct competitor with eight unique serotypes. Lower-valent Synflorix holds on in GAVI markets because of price advantages, yet efficacy-conscious middle-income buyers are gradually trading up.

Domestic Chinese producers such as Walvax and Beijing Minhai provide cost-competitive options, but their lower valency constrains penetration in urban private segments. The imminent arrival of VAX-31 could upend the hierarchy; if approved, its 31 valencies would reset the competitive baseline and hasten obsolescence of existing products in premium markets.

By Distribution Channel: Government Procurement Dominates, Private Retail Surges

Government authorities purchased 63.63% of 2025 doses, reflecting entrenched pediatric mandates and GAVI-funded campaigns. Nonetheless, private and retail pharmacies will grow at a 10.87% CAGR because adults often self-pay or rely on employer insurance, especially in the United States where pharmacies administer most adult vaccines. Retail access expanded in Europe after 2024 legislation authorized pharmacist administration in multiple member states, shifting volume away from hospital clinics.

Hospital-based vaccine clinics remain important for immunocompromised patients but cannot match the convenience of community outlets. NGOs and multilateral tenders, though smaller in revenue terms, set global price anchors, forcing manufacturers to fine-tune channel-specific pricing.

By Age Group: Pediatric Saturation Drives Adult Pivot

The pediatric cohort (< 5 years) retained 61.23% share in 2025, but growth is plateauing in high-income nations where coverage already exceeds 95%. The adult 19-64 segment will expand at a 6.7% CAGR through 2031 because new guidance and employer wellness programs create reimbursed demand. Merck’s Capvaxive was filed exclusively for adults to exploit this momentum, signaling a strategic pivot toward higher-priced adult doses. The geriatric segment remains steady as long-standing policies recommend vaccination for all adults 65+, yet payer negotiations are compressing price premiums.

Emerging markets present contrasting patterns: pediatric gaps persist, but adult immunization infrastructure is only nascent, producing a two-speed ecological map that requires tailored commercial approaches.

Geography Analysis

North America contributed 38.53% of 2025 revenue, propelled by Medicare’s 2024 elimination of cost-sharing for adult vaccines and rapid inclusion of PCV20 and PCV21 on formularies at USD 200-plus reimbursement levels. Canada and Mexico maintain high pediatric coverage, yet adult penetration lags. The Inflation Reduction Act will pressure prices from 2026, narrowing margins but likely expanding volume as co-pays fall.

Asia-Pacific is forecast to log a 6.21% CAGR through 2031, benefiting from multi-national approvals, domestic production, and tariff-free fill-finish operations. China and Japan now offer Prevnar 20, challenging domestic 13-valent competitors. India’s Serum Institute and South Korea’s SK bioscience supply GAVI at sub-USD 3 pricing, while private segments in Indonesia and Vietnam are beginning to pay premiums for higher valency. ASEAN regulatory harmonization could streamline clearances but remains uneven.

Europe sustains demand through centralized tenders that secure volume discounts; Germany, the United Kingdom, France, Italy, and Spain together represent the bulk of regional consumption. EMA’s 2024 acceptance of AI-generated serotype models may shorten timelines for ultra-valent approvals. Middle East & Africa and South America rely on donor or government tenders; cold-chain gaps and fiscal volatility limit uptake of premium products, yet localization projects like South Africa’s Biovac are slowly improving resilience.

Mordor Intelligence provides coverage of the pneumococcal vaccines market across other key regional markets. Detailed country-level analysis extends to Germany incorporating local coverage and market participation, as required.

Competitive Landscape

Pfizer, GSK, and Merck collectively held a significant share of the 2025 revenue, yet competitive tension is intensifying as higher-valent and ultra-valent entrants emerge. Pfizer’s Prevnar franchise remains pivotal, but Merck’s Capvaxive has moved quickly to secure adult share, and GSK’s 2024 Affinivax acquisition signals an appetite for technology that can leapfrog current valencies. Vaxcyte’s USD 1.2 billion financing and SK bioscience’s 2024 WHO prequalification demonstrate investor and regulatory openness to new players.

Two strategic archetypes are visible: incumbents defend margins in high-income markets with premium, high-valency launches, while regional manufacturers attack price-sensitive donor segments with cost-advantaged 10- and 13-valent options. Patent cliffs for PCV13 beginning 2026 may encourage biosimilar exploration, but technical hurdles are high. If VAX-31 or other ≥ 30-valent vaccines win approval, incumbents will have to accelerate pipelines or risk rapid erosion of premium franchises.

Pneumococcal Vaccines Industry Leaders

Pfizer Inc.

CSL Ltd.

Serum Institute of India Pvt. Ltd.

GSK plc

Merck & Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Merck announced positive Phase 3 STRIDE-13 results for Capvaxive at the ESCMID Vaccine Conference.

- August 2025: Pfizer launched Prevnar 20 for adults in India, its first higher-valent entry in a large self-pay market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global pneumococcal vaccines market as manufacturer-level revenue from licensed pneumococcal conjugate vaccines (PCV10 through PCV21) and the polysaccharide vaccine PPSV23 that are supplied to pediatric, adult, and geriatric cohorts through public procurement, multilateral agencies, and private channels during 2019-2030.

Scope Exclusion: We exclude therapeutic antibiotics, diagnostic assays, and pipeline candidates not yet approved for sale.

Segmentation Overview

- By Vaccine Type

- Pneumococcal Conjugate Vaccine (PCV)

- Pneumococcal Polysaccharide Vaccine (PPV)

- By Product Type

- Prevnar 13

- Prevnar 20

- Synflorix

- Pneumovax 23

- Other PCVs

- By Distribution Channel

- Government Authorities

- GAVI/Multilateral & NGO Procurement

- Private & Retail Pharmacies

- Hospital-based Vaccine Clinics

- By Age Group

- Pediatric (<5 years)

- Adults (19-64 years)

- Geriatric (?65 years)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We held structured interviews with national immunization managers in the United States, Germany, India, and Brazil, procurement leads at multilateral agencies, and scientists steering PCV15/20 trials. These discussions clarified adult revaccination practices, forthcoming tender sizes, and realistic price corridors that shaped final assumptions.

Desk Research

We began with authoritative public sources that map disease burden, dose demand, and immunization financing. World Health Organization MI4A demand studies, UNICEF supply dashboards, CDC and ECDC vaccine coverage surveys, and peer-reviewed articles in The Lancet provided incidence curves and uptake ratios across age groups.

Our team then blended UN Comtrade trade codes, tender price filings, and company revenue splits from 10-Ks with intelligence taken from D&B Hoovers and Dow Jones Factiva to benchmark average selling prices and manufacturer footprints. The sources listed are illustrative rather than exhaustive.

Market-Sizing & Forecasting

We apply a top-down rebuild of 2024 sales by reconciling reported manufacturer revenue with regional dose volumes and price bands, which is then cross-checked against WHO demand curves. Select bottom-up checks (for example, country birth-cohort × coverage and adult high-risk prevalence) are layered in to fine-tune totals.

Key variables driving the model include annual live-birth trends, population over sixty-five, Gavi graduation timelines, launch years for higher-valent PCVs, historic tender price erosion, and currency movements. A multivariate regression paired with scenario analysis projects these drivers through 2030, giving a midpoint CAGR that primary experts review before sign-off.

Data Validation & Update Cycle

Our analysts run variance scans against quarterly earnings releases, UNICEF award data, and regulatory approvals. Any material divergence starts a recalibration loop and may trigger fresh respondent contact. Reports refresh each year, with mid-cycle updates when landmark approvals or supply disruptions occur.

Why Mordor's Pneumococcal Vaccines Baseline Commands Reliability

We recognize that published market values differ because firms vary product scope, price deflators, and refresh cadence. By limiting scope to currently approved PCV and PPSV products, valuing revenue at ex-factory level, and fixing 2024 exchange rates, we anchor a transparent baseline.

Key Gap Drivers: some publishers fold pipeline vaccines into current sales, others model only pediatric uptake or ignore Latin American currency shifts. Mordor updates annually and re-interviews payers before finalizing adult penetration, which keeps our 2025 value balanced while more aggressive figures depend on swift PCV20 roll-outs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.23 B (2025) | Mordor Intelligence | - |

| USD 8.49 B (2024) | Global Consultancy A | Excludes private adult market, relies solely on reported volume |

| USD 8.50 B (2024) | Industry Analytics Firm B | Assumes flat price erosion, omits Latin America currency adjustments |

| USD 9.63 B (2024) | Trade Journal C | Counts pipeline vaccines in base-year value |

Together, these comparisons show that our disciplined variable selection and yearly stakeholder validation deliver a dependable, reproducible baseline for decision-makers.

Key Questions Answered in the Report

How large is the pneumococcal vaccines market in 2026?

The pneumococcal vaccines market size stands at USD 9.69 billion in 2026.

What is the expected growth rate through 2031?

Revenue is forecast to expand at a 4.95% CAGR between 2026 and 2031.

Which vaccine type holds the largest share?

Pneumococcal conjugate vaccines account for 77.56% of 2025 sales, reflecting strong pediatric and growing adult uptake.

Why is adult vaccination gaining momentum?

ACIP widened eligibility in 2024 and higher-valent products like Prevnar 20 and Capvaxive offer broader serotype coverage that meets unmet adult need.

What regions will grow fastest?

Asia-Pacific is projected to record a 6.21% CAGR through 2031, helped by local manufacturing and expanding middle-class demand.

Who are the key emerging competitors?

Vaxcyte with its 31-valent VAX-31 and SK bioscience with its WHO-prequalified GBP301 are prominent challengers to established players.

Page last updated on: