Influenza Vaccine Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

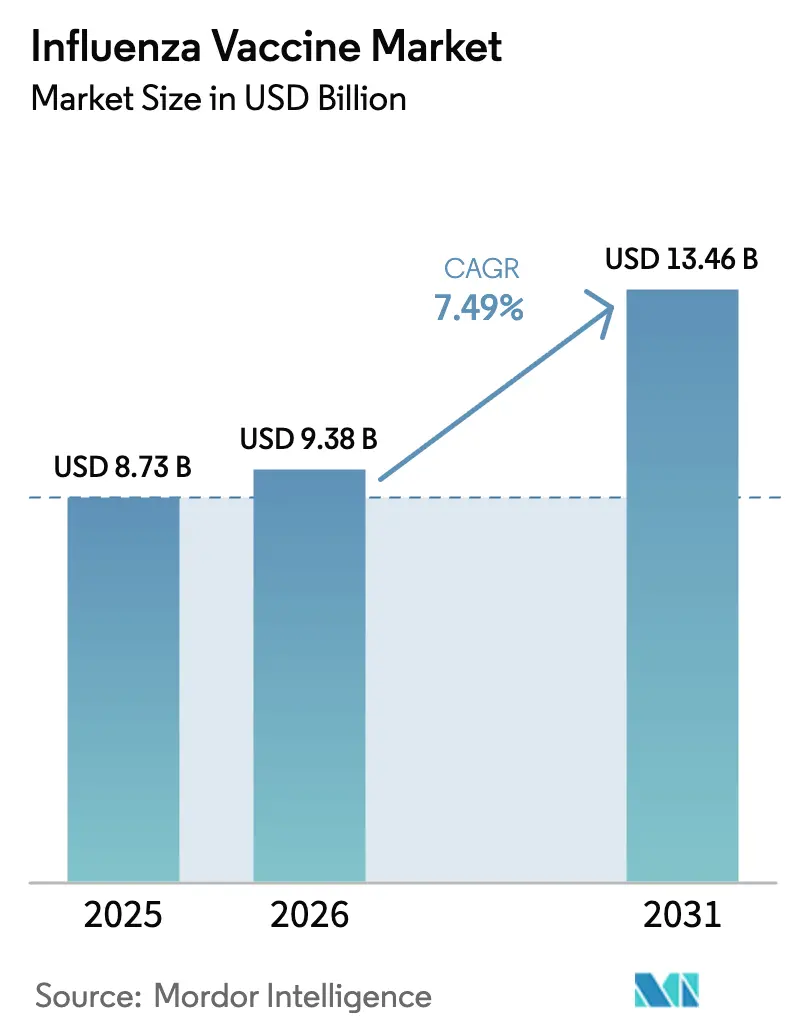

| Market Size (2026) | USD 9.38 Billion |

| Market Size (2031) | USD 13.46 Billion |

| Growth Rate (2026 - 2031) | 7.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

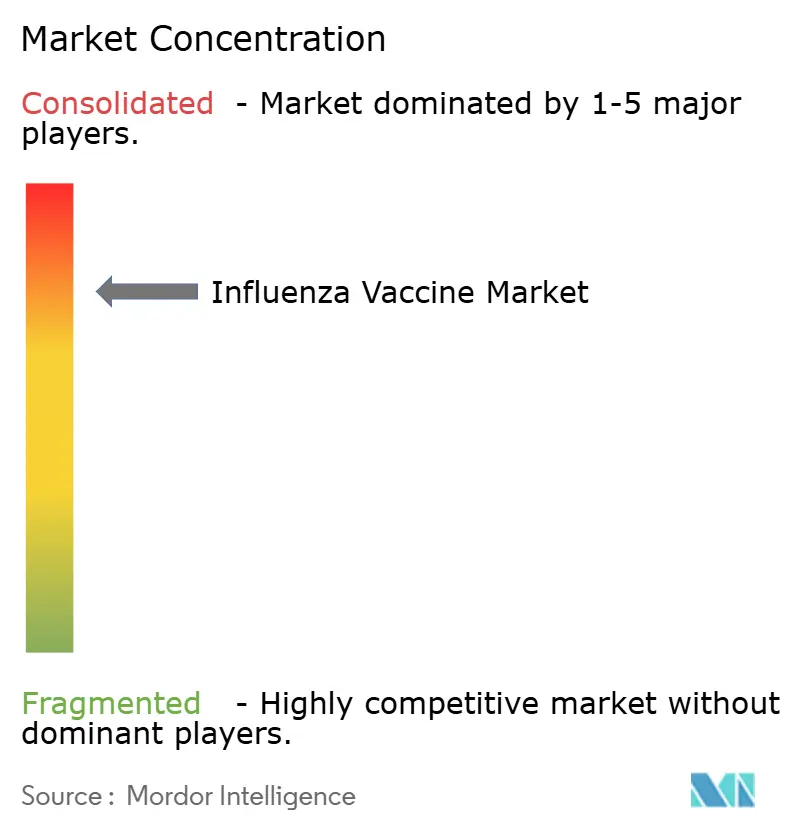

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Influenza Vaccine Market Analysis by Mordor Intelligence

The Influenza Vaccine Market size was valued at USD 8.73 billion in 2025 and is estimated to grow from USD 9.38 billion in 2026 to reach USD 13.46 billion by 2031, at a CAGR of 7.49% during the forecast period (2026-2031).

This acceleration reflects pandemic-preparedness spending, fast platform diversification, and wider coverage mandates that now position the influenza vaccines market for sustained expansion. Direct contracts with mRNA and cell-based producers, regulatory simplification that drops the dormant B/Yamagata lineage, and consumer-centric formats such as self-administered nasal sprays together reinforce demand visibility. Procurement volumes are no longer constrained by seasonal epidemiology but by national security objectives, giving manufacturers predictable offtake and justifying capital-intensive upgrades. At the same time, the influenza vaccines market benefits from demographic tailwinds as the global population ages into higher-risk cohorts, while emerging economies build first-time domestic capacity that broadens geographic consumption.

Key Report Takeaways

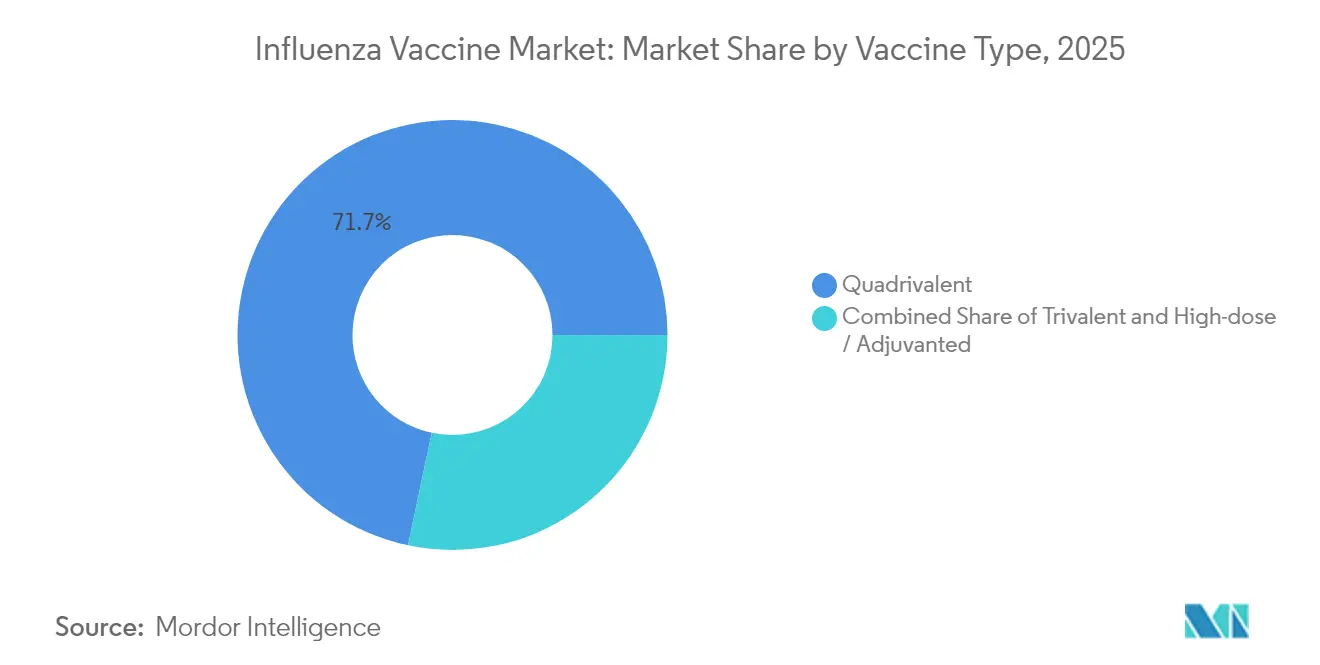

- By vaccine type, quadrivalent products held 71.68% of the 2025 influenza vaccines market share, whereas trivalent formulations are advancing at a 7.81% CAGR through 2031 as manufacturers realign to updated strain recommendations.

- By form, inactivated formulations accounted for 90.95% of the influenza vaccines market size in 2025 and are projected to expand at a 7.71% CAGR between 2026-2031.

- By age group, adults represented 64.88% of the influenza vaccines market size in 2025, while pediatric uptake is forecast to grow at 7.84% CAGR on the back of school-based immunization programs.

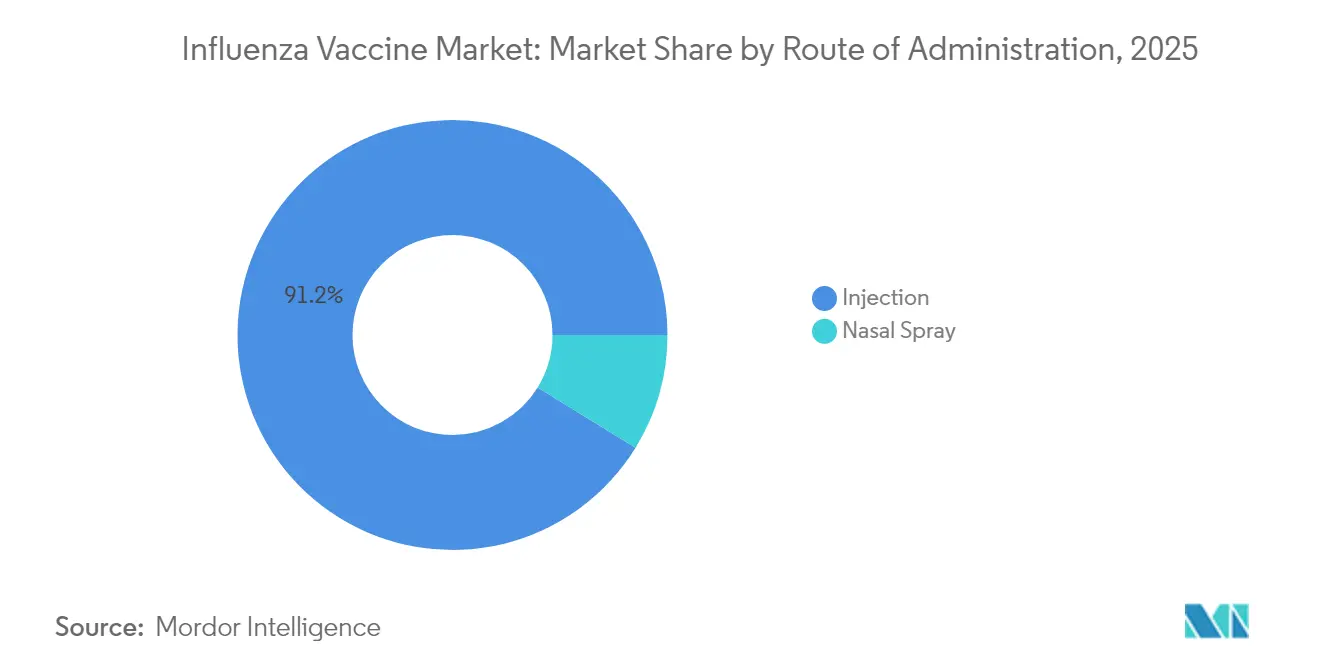

- By route of administration, injections dominated with 91.21% revenue share in 2025; nasal spray delivery is the fastest-growing route, advancing at 8.37% CAGR through 2031 after FDA approval for home use.

- By geography, North America led with 47.10% of influenza vaccines market share in 2025, whereas Asia-Pacific records the highest regional CAGR at 7.92% to 2031, supported by capacity additions and expanded reimbursement.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Influenza Vaccine Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating government-funded immunization targets & procurement | 1.8% | Global, with early gains in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rapid adoption of cell- and recombinant-based production platforms | 1.5% | North America & EU, spill-over to APAC core | Long term (≥ 4 years) |

| Heightened pandemic-preparedness stockpiling budgets | 1.4% | National, with early gains in US, UK, Canada | Short term (≤ 2 years) |

| Expanding geriatric high-risk population base | 1.2% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Regulatory shift back to trivalent formulations lowers mismatch risk | 0.9% | Global | Short term (≤ 2 years) |

| Approval of at-home nasal spray vaccines unlocks D2C channel | 1.1% | North America, expanding to EU and APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Government-Funded Immunization Targets & Procurement

National procurement programs have moved beyond routine seasonal ordering toward strategic stockpiling for pandemic readiness in the influenza vaccine market. Washington’s USD 176 million award to Moderna for an mRNA pandemic-influenza candidate underscores this shift, while London’s purchase of more than 5 million H5N1 doses from CSL Seqirus signals a similar stance in the United Kingdom. Ottawa followed suit by securing 500,000 doses of GSK’s Arepanrix H5N1, aligning North American preparedness strategies. Governments now frame influenza vaccines as security assets rather than basic public-health inputs. The World Health Organization’s Global Action Plan expanded collective pandemic capacity to 1.3 billion doses a year by 2016, laying the groundwork for today’s larger procurement ambitions.

Rapid Adoption of Cell- and Recombinant-Based Production Platforms

Manufacturers are diversifying beyond egg-based methods to improve supply security and vaccine performance across the influenza vaccine market. Data from CSL Seqirus show cell-based products outperformed egg-derived comparators across several age groups during the 2022-23 season [SEQIRUS.COM]. Moderna’s new Australian plant, the Southern Hemisphere’s only dedicated mRNA facility for respiratory vaccines, will be able to supply 100 million doses annually, broadening geographic reach for advanced platforms. The WHO’s mRNA Technology Transfer Program further signals institutional support for non-traditional production. Even so, more than 80% of global output still originates from chicken eggs, underscoring the scale of change now under way.

Expanding Geriatric High-Risk Population Base

Population aging is strengthening demand for enhanced formulations, especially high-dose and adjuvanted options in the influenza vaccine market. U.S. guidelines now recommend these products for adults ≥65 years, and Sanofi’s Fluzone High-Dose delivered 24.2% higher relative efficacy than standard vaccines in that cohort. Medicare-based analyses confirm lower cardiopulmonary hospitalizations and mortality among high-dose recipients. In Denmark, the DANFLU-1 trial found a 70% drop in pneumonia or influenza hospitalizations with high-dose quadrivalent vaccines versus standard-dose versions. Still, economic studies note that high-dose shots cost roughly five times more, with variable incremental benefit season to season.

Heightened Pandemic-Preparedness Stockpiling Budgets

Preparedness funding now appears in concrete line items and facilities. Washington’s National Influenza Vaccine Modernization Strategy (2020-2030) sets priorities for domestic capacity gaps. CSL Seqirus’s Holly Springs plant can supply 150 million doses within six months of an emergency declaration, illustrating industrial-scale readiness. The Biomedical Advanced Research and Development Authority has allocated USD 160 million under Project NextGen to modernize manufacturing processes for next-generation influenza vaccines. Meanwhile, Gavi’s African Vaccine Manufacturing Accelerator, backed by roughly USD 1.2 billion, aims to build regional capacity that will serve both seasonal and pandemic needs.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographical Relevance | Impact Timeline |

|---|---|---|---|

| High clinical & manufacturing investment for next-gen vaccines | -1.3% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Persistent vaccine hesitancy & misinformation | -0.8% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Fragile global egg supply chain vulnerable to avian-flu shocks | -0.9% | Global, with acute impact in North America, Europe | Short term (≤ 2 years) |

| Capital burden of re-tooling to mRNA/cell facilities | -0.7% | North America & EU, spill-over to APAC manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Clinical & Manufacturing Investment for Next-Gen Vaccines

Switching to advanced platforms demands capital-intensive trials and facility upgrades influenza vaccines market. Novavax’s Phase 3 COVID-influ combo study alone carries a USD 500 million clinical bill for fiscal 2025. Converting egg-based plants to cell-based or mRNA systems can cost multiple billions, while CSL’s USD 11.7 billion Vifor deal illustrates the scale of corporate outlays aimed at diversifying beyond legacy models. Complex regulatory pathways stretch timelines; mRNA flu candidates remain in Phase 3 despite the technology’s COVID-19 success. Smaller firms often struggle to raise such sums, which may accelerate consolidation among cash-rich incumbents.

Persistent Vaccine Hesitancy & Misinformation

Post-pandemic fatigue has eroded uptake, most sharply among younger cohorts. Analysis of the Epic Cosmos database recorded vaccination declines of 13.92% for 5- to 18-year-olds and 9.91% for 19- to 26-year-olds compared with pre-COVID seasons. Provider endorsement remains pivotal: 76.6% of vaccinated individuals cited clinician recommendations, versus 49% among the unvaccinated [MDPI.COM]. Misinformation campaigns that question safety and efficacy feed skepticism about yearly flu shots, and the World Health Organization still lists hesitancy among the leading global health threats. Political polarization adds another layer, with self-identified Republicans displaying higher reluctance than Democrats, producing uneven regional coverage that continues to influence the influenza vaccines market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vaccine Type: Trivalent Surge Follows Regulatory Simplification

Trivalent products captured 28.32% of sales in 2025 but now post the segment’s quickest expansion at 7.81% CAGR after regulatory alignment removed B/Yamagata. Quadrivalents still dominate revenue yet face gradual erosion as payers question the necessity of an inactive lineage. Manufacturers accelerated validation runs to meet the 2024-25 season, demonstrating flexible bulk-antigen capacities that safeguard supply continuity. The influenza vaccines market size for trivalent doses is expected to widen as emerging economies prefer lower-cost three-strain presentations for public tenders. High-dose and adjuvanted trivalent versions aimed at seniors will further boost value. In contrast, quadrivalent offerings will pivot to combination formats, bundling respiratory syncytial virus or COVID-19 antigens to maintain premium positioning.

Volume swings affect raw-material procurement, notably embryonated eggs, potentially stabilizing prices as trivalent output requires fewer eggs. The transition also reduces fill-finish complexity, freeing line time for other biologics during off-peak months. While providers may face short-term confusion, clear CDC guidance has minimized substitution errors. Global health agencies anticipate improved strain match rates, lowering breakthrough infection risk and reinforcing trust in vaccination. As these benefits materialize, the influenza vaccines market will likely recalibrate pricing tiers to reflect simplified compositions and differential effectiveness evidence.

By Form: Inactivated Dominance Faces mRNA Innovation Challenge

Inactivated vaccines represented 90.95% of 2025 sales yet also record a 7.71% CAGR as proprietary cell-based and recombinant versions enter tender lists. Their broad regulatory familiarity and cold-chain compatibility sustain hospital ordering preferences. Within this class, cell-derived antigens circumvent egg-adaptation mutations, lifting effectiveness and supporting premium bids. Recombinant HA constructs, such as Flublok, shorten lead times and reduce contamination risk, offering strategic value for pandemic pivoting.

Live attenuated solutions lag in adult uptake due to contraindications but gain new life via at-home nasal sprays. Meanwhile, pipeline mRNA candidates target licensure from 2026 onward. Early readouts show parity with licensed comparators on A-strains but weaker responses against B lineages, prompting formulation fine-tuning. If successful, mRNA could compress manufacturing to weeks, slash changeover costs, and enable bespoke regional compositions. Stakeholders therefore weigh capex now to avoid obsolescence later, a calculus that influences capital allocation across the influenza vaccines market.

By Age Group: Pediatric Growth Accelerates Despite Coverage Gaps

Adults held 64.88% of revenue in 2025, yet pediatric doses are ascending at 7.84% CAGR as ministries extend school-entry mandates. Uptake programs employing mobile clinics and digital consent have narrowed access barriers, but data still show only 49.2% pediatric coverage, leaving a sizable headroom. Two-dose regimens in first-time recipients aged 6-35 months yield stronger seroprotection, adding units per child and raising the influenza vaccines market size for this cohort.

Adult strategies increasingly segment by comorbidity and workplace. Employers subsidize on-site shots to cut sick leave, while payers waive copays for high-risk conditions. The CDC’s updated schedule folds influenza vaccination into routine wellness visits, nudging opportunistic uptake. Yet vaccine fatigue persists among healthy young adults, indicating that targeted messaging remains essential to close gaps. Collectively, demographic shifts mean that by 2030 seniors will account for a larger revenue slice despite slower headcount growth, reflecting premium per-dose pricing.

By Route of Administration: Injection Stability Contrasts Nasal Innovation

Intramuscular injections dominate at 91.21% share thanks to provider familiarity and validated pharmacokinetics. High-dose, adjuvanted, and recombinant variants all rely on this route, reinforcing its entrenched position. However, nasal sprays now post the fastest 8.37% CAGR, propelled by FDA-cleared at-home use and needle-averse consumers. Self-administration shifts distribution cost to e-pharmacies and logistics firms, potentially shortening lead times between purchase and immunization.

Japan’s migration from subcutaneous to intramuscular administration illustrates practice harmonization; national data after COVID-19 campaigns showed stronger immunogenicity and fewer local reactions via muscle injection. Limitations remain: nasal sprays are contraindicated in children under 2 and immunocompromised adults. Cold-chain requirements mirror injectables, muting logistics advantages. Yet scenario modeling suggests that if even 10% of current injection recipients switch to home sprays, the influenza vaccines market could unlock USD 500 million in incremental consumer revenue annually through retail margins.

By Distribution Channel: Hospital Dominance Faces Pharmacy Expansion

Hospitals and clinics secured 44.30% of the influenza vaccines market 2025 sales, but pharmacies dispensed 37 million flu shots versus 25 million from medical offices in the U.S., underscoring retail traction. Convenience, extended hours, and synergistic merchandise drives adoption. Yet chain consolidation—Rite Aid’s bankruptcy and CVS store closures—creates regional service gaps that public health departments must fill. Pharmacies also trial decentralized clinical research; Walgreens’ BARDA collaboration enrolls participants via store sites, illustrating diversification of value pools.

Government procurement is the fastest-expanding at 7.62% CAGR. Advance purchase agreements lock in multi-year volume, smoothing manufacturer utilization and anchoring the influenza vaccines market against seasonality. Online channels are nascent but promising as prescription digital platforms integrate telehealth consults, point-of-care diagnostics, and doorstep delivery. Regulatory frameworks enforce identity verification and adverse-event reporting, maintaining pharmacovigilance while broadening reach.

Geography Analysis

North America held 47.10% of revenue in 2025 owing to universal CDC recommendations, insurance mandates, and corporate clinics. The U.S. couples large-scale purchasing with rapid distribution; Canada supplements domestic output with GSK contracts, securing 500,000 pandemic doses while aligning regulatory reviews through the Canada-U.S. Regulatory Cooperation Council. Mexico leverages USMCA to streamline cross-border antigen shipments, supporting joint North American preparedness.

Asia-Pacific is expanding at 7.92% CAGR. All 11 WHO South-East Asia Region countries now maintain National Influenza Centers, improving surveillance and strain selection. China’s atypical late 2024 season revealed timing gaps that manufacturers addressed by staggering release lots, highlighting adaptive supply chains. Japan, after decades of subcutaneous preference, endorsed intramuscular administration, improving dose efficacy and standardizing global protocols. Australia’s mRNA factory de-risks hemispheric supply and could export to Southeast Asia, making the region less reliant on Northern Hemisphere production.

Europe possesses mature coverage yet faces demographic stagnation. EMA centralized approvals facilitate cross-border trade, and the U.K. continues deep stockpiling despite Brexit through early tenders for 5 million H5N1 doses. Middle East and Africa trail but benefit from Gavi’s manufacturing accelerator, which will underwrite capacity for both seasonal and pandemic needs. South America builds readiness via PAHO simulation drills that test deployment plans for respiratory pandemics. Collectively, these dynamics diversify demand, making the influenza vaccines market less dependent on any single geography.

Competitive Landscape

The influenza vaccines market is oligopolistic. Sanofi, GSK, and CSL Seqirus collectively exceed 60% revenue, while newer mRNA entrants jostle for share. Sanofi partnered with Novavax in a USD 1.2 billion deal to co-develop protein-based combo shots, adding breadth to its Fluzone and Flublok franchises. CSL Seqirus exploits cell-culture differentiation via its Holly Springs site, a pandemic-ready facility that can swing output within six months. GSK leverages its AS03 adjuvant platform across flu and other pathogens, increasing cross-portfolio synergies.

Moderna secured a USD 176 million federal contract and broke ground in Australia, signaling intent to leapfrog incumbents with mRNA flu products. Pfizer-BioNTech face technical challenges on influenza B immunogenicity, demonstrating that COVID-19 success does not guarantee flu translation[3]Fierce Biotech, “Pfizer-BioNTech mRNA Flu Trial Results,” fiercebiotech.com. AstraZeneca created a first-mover moat in home delivery through FluMist, enabling direct-to-consumer positioning that others must navigate regulatory pathways to emulate.

Barriers include stringent GMP, strain-specific potency assays, and cold-chain logistics. Egg-based vulnerabilities—avian outbreaks can decimate supply—drive diversification to cell or mRNA lines, favoring capital-rich sponsors. Regional partnerships with local fill-finish contractors in Southeast Asia or Africa allow incumbents to comply with localization requirements while keeping antigen production centralized. M&A remains a lever, although antitrust scrutiny increases as concentration inches upward.

Influenza Vaccine Industry Leaders

CSL Limited

Sanofi

Moderna, Inc.

AstraZeneca plc

GSK plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Novavax reported robust immune responses for its COVID-19–influenza combo and stand-alone trivalent flu candidates in a Phase 3 cohort of 2,000 seniors.

- December 2024: Sanofi obtained FDA Fast Track for two combo shots pairing Fluzone High-Dose or Flublok with Novavax’s COVID-19 antigen for adults ≥ 50 years.

- December 2024: Moderna inaugurated its Victoria mRNA facility, the Southern Hemisphere’s first large-scale site, with 100 million-dose capacity for respiratory vaccines.

- September 2024: FDA approved self-administered FluMist for people aged 2-49, pioneering at-home influenza vaccination.

Global Influenza Vaccine Market Report Scope

As per the scope of the report, Influenza is a viral infection that attacks the human respiratory system, including the nose, throat, and lungs. Influenza is recognized as a crucial cause of morbidity and mortality across the world. The increasing prevalence of influenza and the growth in research funding for developing new medications are the major factors driving the Influenza Vaccine Market.

The Influenza Vaccine Market is Segmented by Vaccine Type (Quadrivalent and Trivalent), Type (Seasonal and Pandemic), Technology (Egg-based and Cell-based), Age Group (Pediatric and Adults), Route of Administration (Injection and Nasal Spray), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (USD million) for the above segments.

| Quadrivalent |

| Trivalent |

| High-dose / Adjuvanted |

| Inactivated |

| Live Attenuated |

| mRNA / Recombinant |

| Pediatric |

| Adults |

| Injection |

| Nasal Spray |

| Hospitals & Clinics |

| Pharmacies & Retail Chains |

| Government & NGO Procurement |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Vaccine Type | Quadrivalent | |

| Trivalent | ||

| High-dose / Adjuvanted | ||

| By Form | Inactivated | |

| Live Attenuated | ||

| mRNA / Recombinant | ||

| By Age Group | Pediatric | |

| Adults | ||

| By Route of Administration | Injection | |

| Nasal Spray | ||

| By Distribution Channel | Hospitals & Clinics | |

| Pharmacies & Retail Chains | ||

| Government & NGO Procurement | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the influenza vaccines market in 2026?

The influenza vaccines market size reached USD 9.38 billion in 2026 and is projected to grow steadily through 2031.

What CAGR is expected for global influenza vaccine revenues through 2031?

Revenues are forecast to rise at a 7.49% CAGR over 2026-2031, supported by pandemic-preparedness budgets and new technology platforms.

Which region is expanding the fastest in influenza vaccine uptake?

Asia-Pacific records the highest growth, with a 7.92% CAGR driven by capacity additions and wider immunization programs.

What is the impact of self-administered nasal spray vaccines?

FDA-approved at-home FluMist enables direct-to-consumer delivery and supports the fastest-growing 8.37% CAGR for nasal routes.

Why are trivalent vaccines gaining traction after years of quadrivalent dominance?

Regulators dropped the dormant B/Yamagata strain for the 2024-25 season, simplifying formulations and boosting trivalent demand at 7.81% CAGR.

Which companies lead the shift toward mRNA influenza vaccines?

Moderna and Pfizer-BioNTech are front-runners, with Moderna backed by a USD 176 million U.S. contract to launch H5N1 mRNA trials in 2025.

Page last updated on: