Brucellosis Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

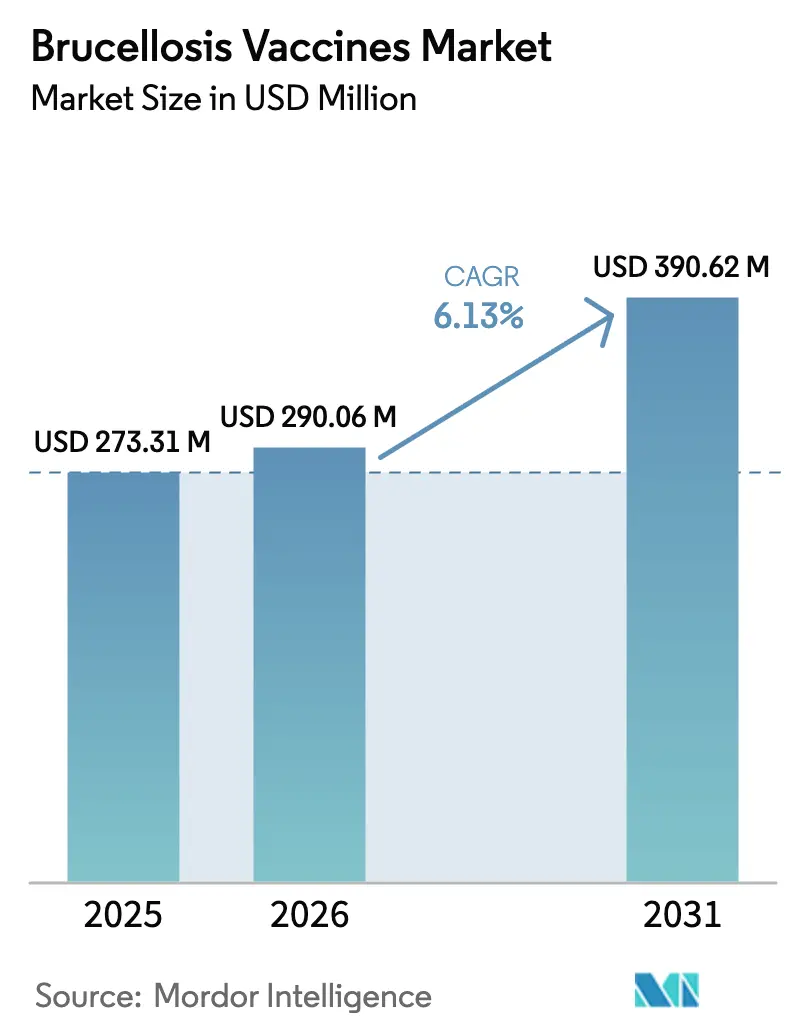

| Market Size (2026) | USD 290.06 Million |

| Market Size (2031) | USD 390.62 Million |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brucellosis Vaccines Market Analysis by Mordor Intelligence

The brucellosis vaccines market size was valued at USD 273.31 million in 2025 and estimated to grow from USD 290.06 million in 2026 to reach USD 390.62 million by 2031, at a CAGR of 6.13% during the forecast period (2026-2031). Momentum comes from the growing recognition of brucellosis as a high-impact zoonosis that depresses livestock productivity and generates avoidable human illness costs. Policy-backed immunization programs, such as USDA’s Cooperative State-Federal effort and Canada’s province-level schemes, keep demand in developed economies resilient, while multilateral funds are widening access across lower-income regions. Intensifying livestock headcounts in South and Southeast Asia, rising consumer focus on milk and meat safety, and accelerated R&D in DNA and vector platforms collectively reinforce the long-run expansion of the brucellosis vaccines market. Strategic plant upgrades—illustrated by Merck Animal Health’s USD 895 million Kansas investment—are easing supply constraints and positioning leading producers to capture share when next-generation products clear regulators.

Key Report Takeaways

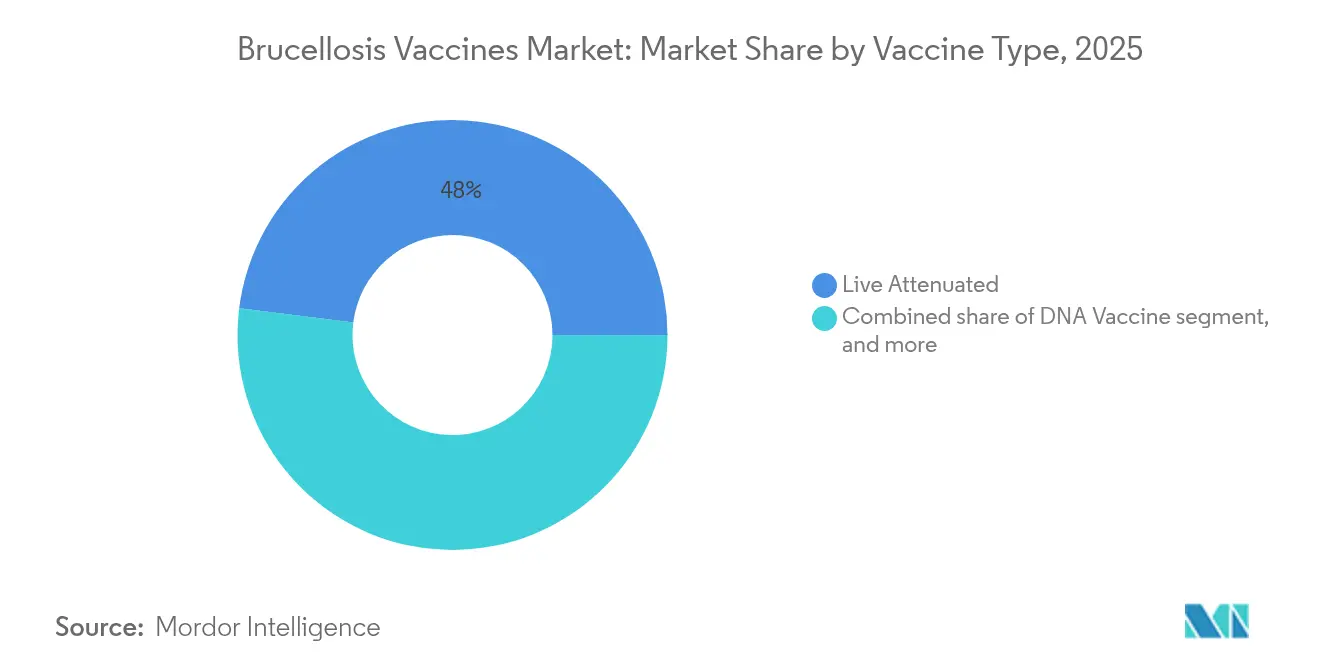

- By vaccine type, live attenuated products led with 48.02% of brucellosis vaccines market share in 2025, whereas DNA vaccines are on track for the fastest 8.21% CAGR to 2031.

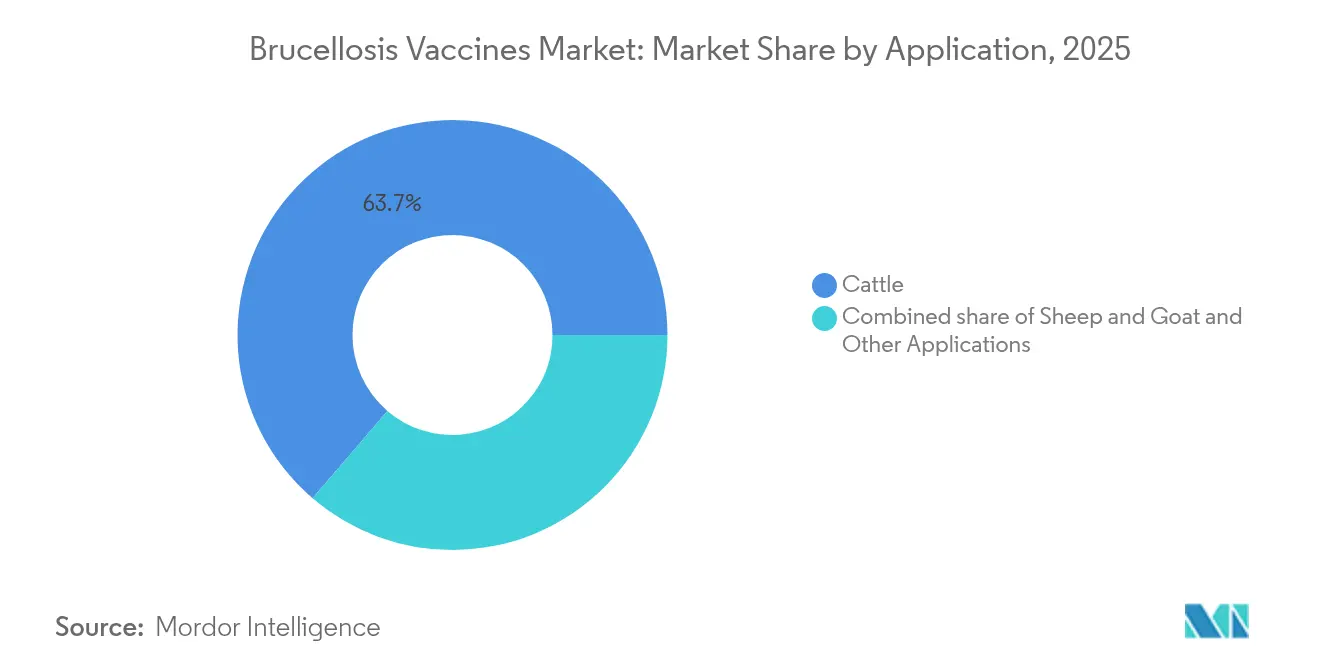

- By application, cattle commanded 63.72% share of the brucellosis vaccines market size in 2025; the sheep and goat segment is projected to expand at 9.32% CAGR through 2031.

- By end user, veterinary hospitals and clinics held 41.02% revenue share in 2025, while government and NGO campaigns record the highest 9.06% CAGR outlook.

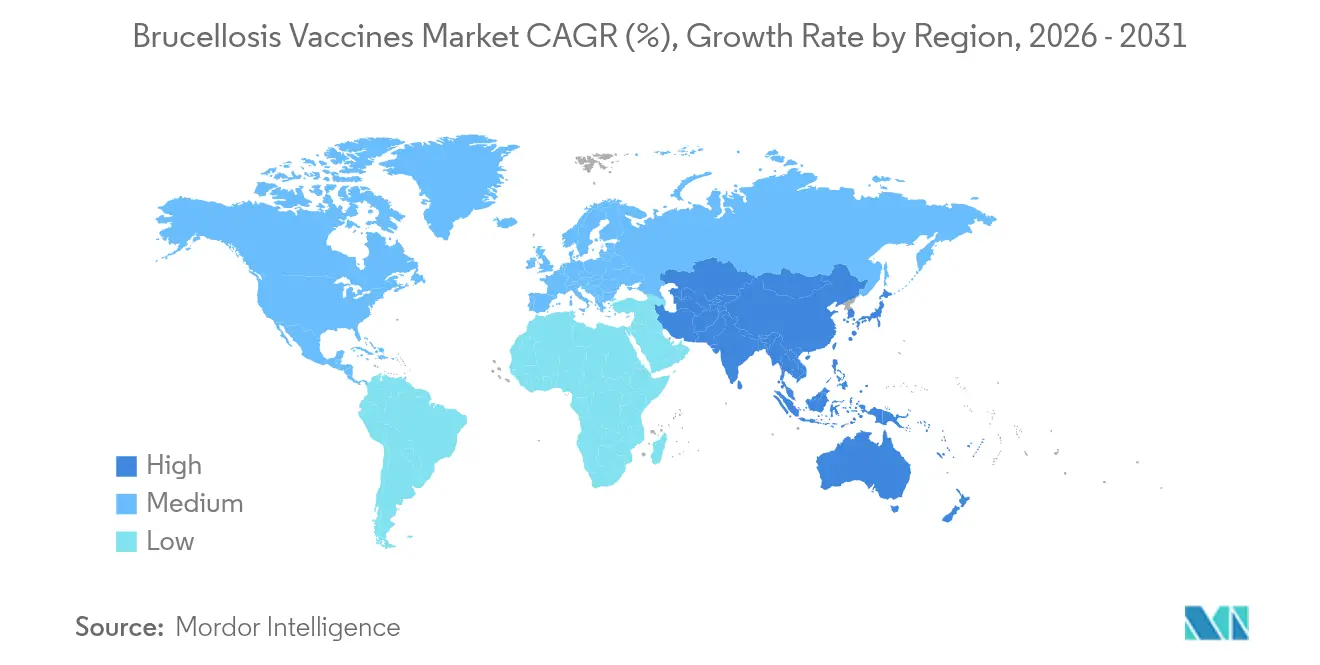

- By geography, North America accounted for 39.88% of the brucellosis vaccines market in 2025, whereas Asia-Pacific is advancing at a 7.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Brucellosis Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Incidence Of Brucellosis | +1.2% | Global, with highest impact in Asia-Pacific and Africa | Medium term (2-4 years) |

| Government Supported Livestock Vaccination Programs | +1.8% | North America, Europe, emerging markets in Asia-Pacific | Long term (≥ 4 years) |

| Rising Awareness Of Zoonotic Disease Risks | +0.9% | Global, particularly in developing countries | Medium term (2-4 years) |

| Growth In Global Livestock Population | +1.1% | Asia-Pacific, Latin America, Sub-Saharan Africa | Long term (≥ 4 years) |

| Technological Advancements In Vaccine Platforms | +0.7% | North America, Europe, with spillover to emerging markets | Long term (≥ 4 years) |

| Availability Of Funding And Incentive Initiatives | +0.5% | Global, with focus on low and middle-income countries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-Supported Livestock Vaccination Programs

Public funding is reshaping market economics by underwriting large-scale immunization drives and stipulating vaccine quality standards. In the United States, the cooperative federal program has cut infected herds from 124,000 in 1956 to single-digit counts while sustaining 3.5 million calf doses each year. Gavi’s 2026-2030 blueprint replicates this template for lower-income regions, pairing grant finance with the African Vaccine Manufacturing Accelerator[1]Gavi Secretariat, “Alliance Strategy 2026-2030,” gavi.org. Cost-benefit analyses in India show vaccination benefit-cost ratios above 10 for cattle and above 20 for buffalo, creating powerful fiscal justification for budget allocations. Partnerships tested in West and Central Africa blend public oversight with private logistics, trimming wastage and improving farmer compliance.

Rising Awareness of Zoonotic Disease Risks

The pandemic experience sensitized policymakers and producers to cross-species threats, lifting demand for validated animal vaccines. Surveys in Ethiopia revealed 100% lack of brucellosis knowledge among smallholders despite measurable seroprevalence, prompting national education campaigns. Indian One Health studies documented dangerous Brucella abortus loads in raw milk, steering authorities toward combined vaccination-plus-consumer outreach models. Tajikistan’s 2023 response, which vaccinated 5,000 animals after coordinated messaging, highlights how awareness directly affects uptake. Malaysia quantified RM 200.6 million (USD 62.9 million) losses from brucellosis, reinforcing the public health case for prevention.

Growth in Global Livestock Population

Expanding herds in dairy-dominated South Asia and mixed crop-livestock zones of Southeast Asia intensify disease pressure and enlarge the brucellosis vaccines market. Smallholders in the Mekong corridor have lifted large-ruminant holdings during the past decade, yet bio-security remains inconsistent, sustaining vaccine demand. In Mexico’s Bajío, economic modeling shows goat vaccination generating USD 3.8 per head net present value over five years, but only when integrated with test-and-slaughter protocols. Comparable analyses across Latin America and East Africa confirm similar investment returns, motivating producers to cooperate with veterinary services.

Technological Advancements in Vaccine Platforms

Next-generation platforms are upgrading safety and regulatory compliance. The European Medicines Agency (EMA) issued final DNA vaccine guidelines in January 2025, clarifying data requirements for genome-integration risk and potency assays[2]European Medicines Agency, “Guideline on Plasmid DNA Vaccines in Veterinary Use,” ema.europa.eu. IgG-FC fused multiepitope constructs have demonstrated robust protection in murine models without live organism hazards. Bovine adenoviral vectors enable intranasal dosing that triggers mucosal and systemic immunity, addressing handling concerns in high-traffic cattle settings. Diagnostic convergence matters too: time-resolved fluorescence lateral-flow tests now reach sensitivities 12,800 times superior to rose Bengal, supporting DIVA compliance in the field.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory And DIVA Compliance Requirements | -0.8% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Cold Chain And Distribution Constraints | -1.2% | Developing countries, rural areas globally | Medium term (2-4 years) |

| Safety Concerns Over Live Attenuated Vaccines | -0.6% | Global, particularly in regions with high human exposure risk | Medium term (2-4 years) |

| Limited Veterinary Infrastructure In Emerging Regions | -0.9% | Sub-Saharan Africa, rural Asia-Pacific, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cold Chain and Distribution Constraints

Temperature lapses destroy more than half of livestock vaccines shipped to remote areas, eroding program credibility and magnifying disease risk. Field work in India shows that newer solar refrigerators keep storage within range but cannot freeze ice packs for portable carriers, restricting last-mile reach. Economic reviews argue that reinforcing transport nodes may yield higher returns than solely chasing higher thermostability, because cold chain contributes a minor share to total vaccine delivery costs. Thailand’s Q-Mark standard for temperature-controlled transport sets a replicable benchmark for other tropical markets where supply integrity falters.

Stringent Regulatory and DIVA Compliance Requirements

Advanced platforms face multilayered approvals from agencies such as USDA’s Center for Veterinary Biologics, which enforces exhaustive purity, potency, and safety dossiers and vets every advertising claim. EMA’s DNA guidance adds demands for biodistribution and genome-integration studies, lengthening timelines and raising R&D budgets beyond reach for smaller innovators. DIVA protocols require paired diagnostics that distinguish infected from vaccinated animals; meeting these standards can force manufacturers to redesign antigen constructs or co-develop assay kits, adding years and millions to launch schedules. Global harmonization through VICH has reduced duplicate testing in major markets, yet gaps remain in Latin America and parts of Africa, complicating simultaneous registrations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vaccine Type: Innovation Fuels Gradual Shift from Live Attenuated Dominance

Live attenuated formulations such as RB51 and Rev-1 supplied 48.02% of brucellosis vaccines market share in 2025 thanks to field-proven 70–80% protection and lower cost of goods. These attributes will sustain baseline demand, particularly where eradication campaigns still rely on existing infrastructure. DNA candidates, however, are climbing at an 8.21% CAGR and are expected to carve measurable chunks of the brucellosis vaccines market by 2031 because they meet DIVA requirements and eliminate human infection fears associated with accidental self-inoculation. The EMA guidance released in 2025 removes much of the regulatory ambiguity that once deterred investment, encouraging firms with plasmid or multiepitope constructs to scale up pilot runs.

Sub-unit and recombinant protein lines continue serving niche users who prioritize biosafety, although their market expansion is tempered by adjuvant dependencies and cold-chain sensitivity. Vector-based platforms using bovine adenoviruses are advancing through late-stage pre-clinical milestones and could achieve field approval within the next planning cycle, especially for intranasal cattle dosing that sidesteps needle use and simplifies mass administration. Collectively, these technology streams ensure that the brucellosis vaccines market retains a diverse product mix that can respond to differing regulatory climates and herd management realities.

By Application: Small Ruminants Become the Standout Growth Frontier

Cattle immunization underpinned 63.72% of the brucellosis vaccines market size in 2025 on the back of decades-old eradication frameworks in North America and Europe and rising dairy herd upgrades in South Asia. Producers favor well-rehearsed schedules overseen by accredited veterinarians, and evidence from the United States shows roughly 3.5 million calves safeguarded annually with standardized tags and electronic record uploads. Yet small ruminant vaccination is accelerating at 9.32% CAGR, reflecting heightened concern over Brucella melitensis, which causes more severe human disease. Incentive contests such as the USD 30 million AgResults Brucellosis Vaccine Challenge channel funds toward safer Rev-1 replacements suitable for goat and sheep production in West Africa and Central Asi.

Economic modeling from Mexico’s small-scale goat systems confirms positive payback within five years, and similar analyses in North Africa suggest even faster returns where seroprevalence exceeds 8%. Wildlife vaccination remains a nascent field, but escalates in territories like the Greater Yellowstone Area, where elk and bison sustain sporadic spillover, reminding policymakers that full eradication demands cross-species vigilance.

By End User: Public-Private Mechanics Diversify Delivery Channels

Veterinary hospitals and clinics held 41.02% of total revenue in 2025, reflecting their gatekeeper position for prescription-only biologics, cold-chain custody, and official tagging. Their role will stay central as live vaccines still dominate—and professional oversight is compulsory to mitigate accidental exposure. Meanwhile, government and NGO campaigns log a 9.06% CAGR, mobilized by evidence that comprehensive coverage cuts human incidence and raises rural incomes. Tajikistan’s 2023 outbreak response is illustrative: a coordinated taskforce delivered more than 5,000 doses within weeks, arresting spread and boosting producer trust.

Animal breeding centers, though a smaller slice of the brucellosis vaccines market, are evolving into advanced bio-security hubs; large dairy collectives in India and China now bundle routine Brucella immunization with genomic selection programs, thereby enhancing both herd health and genetic merit in a single intervention cycle. These dynamics underscore how differentiated end-user strategies will underpin revenue diversification across the brucellosis vaccines industry.

Geography Analysis

North America controlled 39.88% of the brucellosis vaccines market in 2025, an outcome linked to long-running eradication programs, mandatory RFID tagging, and generous federal cost-sharing arrangements. While domestic cattle incidence has been squeezed to isolated wildlife-related flare-ups in the Greater Yellowstone Area, the region’s proactive surveillance keeps annual prophylactic demand steady. The United States retains a deep ecosystem of biologic manufacturers, contract research organizations, and university extension networks that collectively sustain innovation and high coverage.

Asia-Pacific is the performance leader with a 7.42% CAGR outlook to 2031. India alone logs estimated brucellosis-linked economic losses of USD 3.4 billion per year, and recent cost-benefit assessments show vaccination can yield ratios above 20:1 for buffalo, prompting state governments to scale procurement. China’s concentration on protein security drives substantial investment in provincial Animal Husbandry Stations that bundle Brucella vaccination with TB and FMD programs, while Indonesia and Vietnam channel donor funds toward cold-chain reinforcement and farmer extension. The pace of herd expansion across ASEAN, particularly in small ruminants, guarantees a sizeable addition to the global brucellosis vaccines market.

Europe, backed by EMA’s stringent biologics code and harmonized disease notification laws, serves as a center of excellence for advanced platform trials, though endemic prevalence is already low in EU dairy herds. Middle East and Africa exhibit heterogeneous adoption; however, donor-driven pilots such as AgResults and IDRC’s Livestock Vaccine Innovation Fund are catalyzing uptake among smallholders in Kenya, Nigeria, and Ethiopia. South America’s picture ranges from sophisticated control in Uruguay’s beef sector to higher prevalence pockets in the Andean highlands, supporting a mixed demand trajectory yet preserving upside for manufacturers willing to tailor pack sizes and formulations.

Competitive Landscape

The brucellosis vaccines market shows moderate consolidation. Zoetis posted USD 9.3 billion total revenue in 2024, with livestock vaccines accounting for roughly one-third; its divestment of 37 medicated feed lines to Phibro refocuses capital on biologics R&D and manufacturing. Merck Animal Health’s USD 895 million Kansas facility expansion secures bulk antigen capacity and advanced fill-finish suites, helping buffer the sector against the Bangs vaccine shortage experienced in late 2024. Boehringer Ingelheim’s purchase of Saiba Animal Health adds virus-like particle technology that could spawn thermostable brucellosis candidates suitable for high ambient regions.

Second-tier players include Indian-based Indian Immunologicals and China’s Qingdao Vland, which concentrate on regional bulk supply contracts and increasingly co-license technology from multinationals to accelerate regulatory clearance. Collaborative ventures between Western IP holders and Asian manufacturers lower cost curves while spreading risk. At the same time, non-profit accelerators such as IDRC’s CAD 57 million Livestock Vaccine Innovation Fund are supplying grant capital to smaller biotech firms, offsetting the elevated proof-of-concept expenses associated with DIVA-enabled constructs.

Competitive advantages are shifting toward firms that combine versatile platform technologies with validated cold-chain service packages. Field data analytics—delivered via cloud dashboards and farm-level mobile apps—are gaining traction as differentiators, because they let manufacturers prove real-world efficacy and fine-tune batch planning. Regulatory agility also counts: companies with dedicated liaison units reduce dossier-to-license cycles by exploiting the mutual recognition channels now emerging among ASEAN members, Mercosur, and the Tripartite Alliance in Africa.

Brucellosis Vaccines Industry Leaders

Ceva Santé Animale

Zoetis Inc.

Merck Animal Health

Boehringer Ingelheim Animal Health

Indian Immunologicals Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Elanco signed with Medgene to commercialize a highly pathogenic avian influenza vaccine for dairy cattle, pending USDA conditional approval.

- January 2025: Merck Animal Health and Kansas announced a USD 895 million expansion of De Soto manufacturing and R&D facilities to boost veterinary vaccine output.

- January 2025: The European Medicines Agency published comprehensive plasmid DNA vaccine guidelines, formalizing data requirements for veterinary use.

- October 2024: Phibro closed a USD 350 million acquisition of Zoetis’ medicated feed additive portfolio, deepening its animal health footprint.

- September 2024: Boehringer Ingelheim acquired Saiba Animal Health, adding virus-like particle know-how to its vaccine pipeline.

Global Brucellosis Vaccines Market Report Scope

As per the scope, brucellosis is a bacterial disease caused by various Brucella species, mainly infecting cattle, swine, goats, sheep, and dogs. Humans acquire the disease through direct contact with infected animals, eating or drinking contaminated animal products, or inhaling airborne agents. The brucellosis vaccines market is segmented by vaccine type, application, end user, and geography. By vaccine type, the market is segmented into DNA vaccine, subunit vaccine, vector vaccine, and recombinant vaccine. By application, the market is segmented into cattle, sheep and goat, and other applications. By end user, the market is segmented into veterinary hospitals and clinics, animal care centers, and other end users. Geographically, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market size is provided in terms of value (USD).

| Live Attenuated |

| DNA Vaccine |

| Sub-unit / Recombinant Protein |

| Vector-Based / Viral-Vectored |

| Cattle |

| Sheep & Goat |

| Other Applications |

| Veterinary Hospitals & Clinics |

| Animal Care / Breeding Centres |

| Government & NGO Vaccination Campaigns |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Vaccine Type | Live Attenuated | |

| DNA Vaccine | ||

| Sub-unit / Recombinant Protein | ||

| Vector-Based / Viral-Vectored | ||

| By Application | Cattle | |

| Sheep & Goat | ||

| Other Applications | ||

| By End User | Veterinary Hospitals & Clinics | |

| Animal Care / Breeding Centres | ||

| Government & NGO Vaccination Campaigns | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the brucellosis vaccines market?

The brucellosis vaccines market size is USD 290.06 million in 2026 and is projected to grow to USD 390.62 million by 2031.

Which region is expanding the fastest?

Asia-Pacific is the fastest-growing region, registering a 7.42% CAGR through 2031 on the back of rising livestock numbers and greater disease-control funding.

Which vaccine type is gaining quickest adoption?

DNA vaccines post the highest 8.21% CAGR forecast because they meet DIVA standards and eliminate live-organism safety concerns.

How concentrated is the supplier landscape?

The market is moderately concentrated; the top five companies hold about 60% of sales, yielding a concentration score of 6.

What are the main barriers to wider vaccine use in developing countries?

Cold-chain gaps and limited veterinary infrastructure cause over 50% vaccine wastage in low-income settings, restricting effective coverage.

Why are small ruminants seen as a high-growth segment?

Sheep and goats now receive greater policy focus because Brucella melitensis is a serious human pathogen, and vaccination delivers strong economic returns for smallholders.

Page last updated on: