Germany Pneumococcal Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

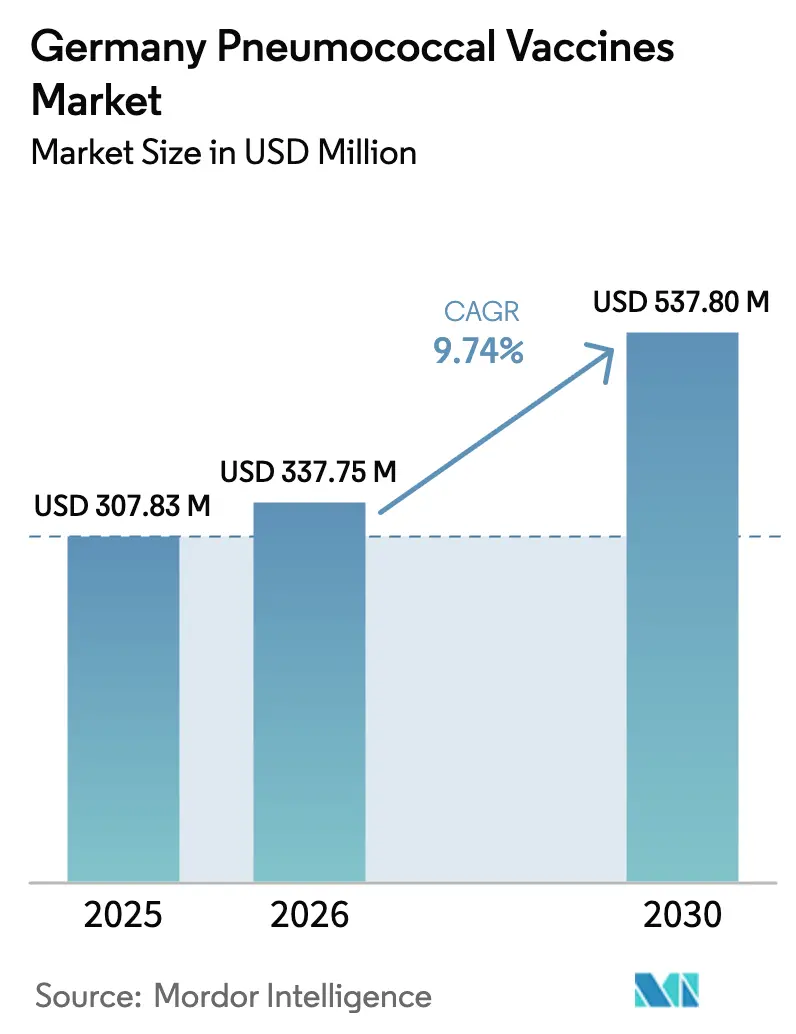

| Base Year Market Size (2025) | USD 307.83 Million |

| Market Size (2026) | USD 337.75 Million |

| Market Size (2030) | USD 537.80 Million |

| Growth Rate (2026 - 2031) | 9.74% CAGR |

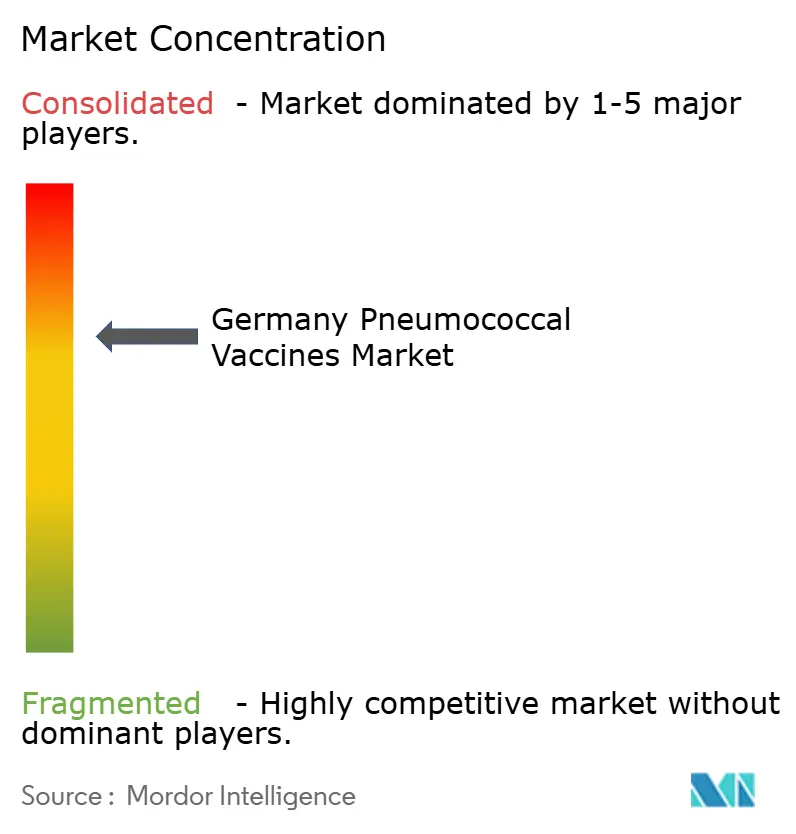

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Pneumococcal Vaccines Market Analysis by Mordor Intelligence

The Germany Pneumococcal Vaccines Market size is expected to grow from USD 307.83 million in 2025 to USD 337.75 million in 2026 and is forecast to reach USD 537.80 million by 2030 at 9.74% CAGR over 2026-2030.

Demand is rising because the Standing Committee on Vaccination (STIKO) now recommends PCV20 for routine adult use, replacing PPSV23, while the European Medicines Agency approved Merck’s 21-valent Capvaxive in March 2025, widening serotype protection across senior cohorts. Uptake also benefits from Germany’s EUR 1.2 billion immunization budget for 2026 that prioritizes pneumococcal shots within the National Prevention Strategy. Even so, low adult coverage persists at 21% among 60-69 year-olds because primary-care touchpoints remain fragmented, especially in rural East German Länder where general-practitioner density trails the national average by 18%. Competitive intensity is rising as Pfizer pivots from Prevenar 13 to Prevenar 20, Merck scales Capvaxive capacity, and Vaxcyte advances a cell-free 24-valent candidate that could compress production timelines and reset price points.

Key Report Takeaways

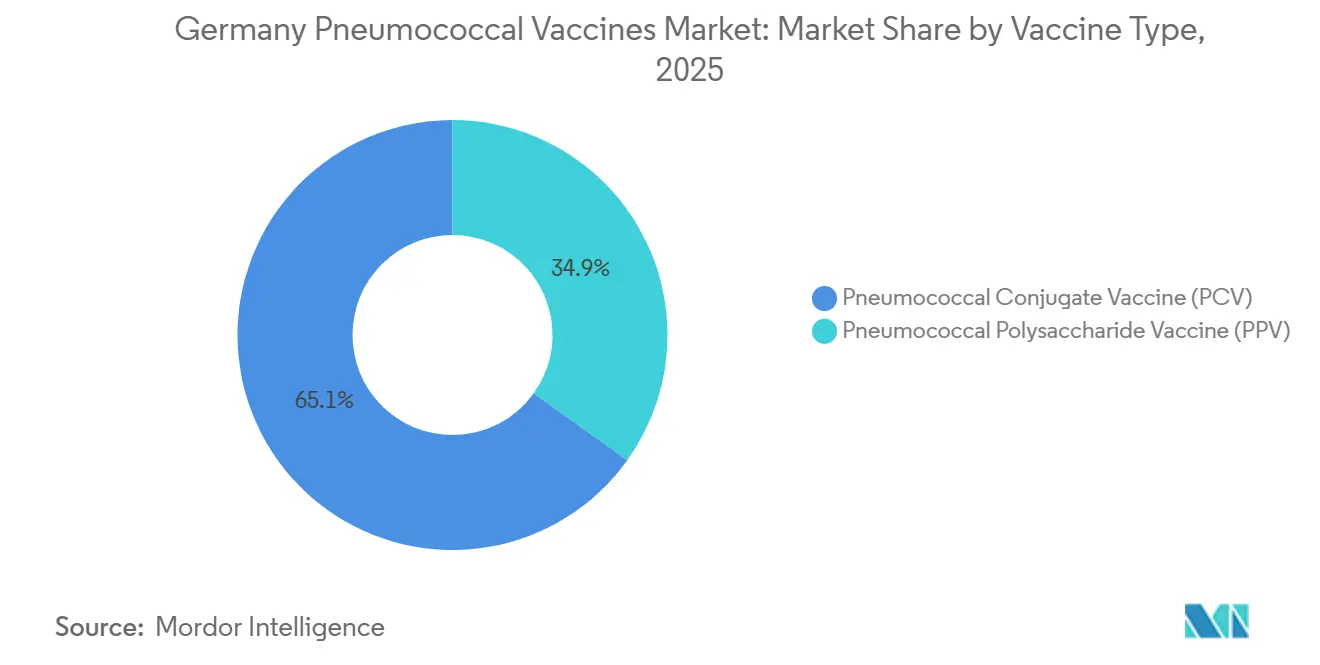

- By vaccine type, pneumococcal conjugate vaccines led with 65.11% of Germany pneumococcal vaccines market share in 2025, while the polysaccharide segment is forecast to expand at a 10.23 % CAGR to 2031.

- By product, Prevenar 13 accounted for 41.23% share of the Germany pneumococcal vaccines market size in 2025, yet Pneumovax 23 is advancing at a 11.14% CAGR through 2031.

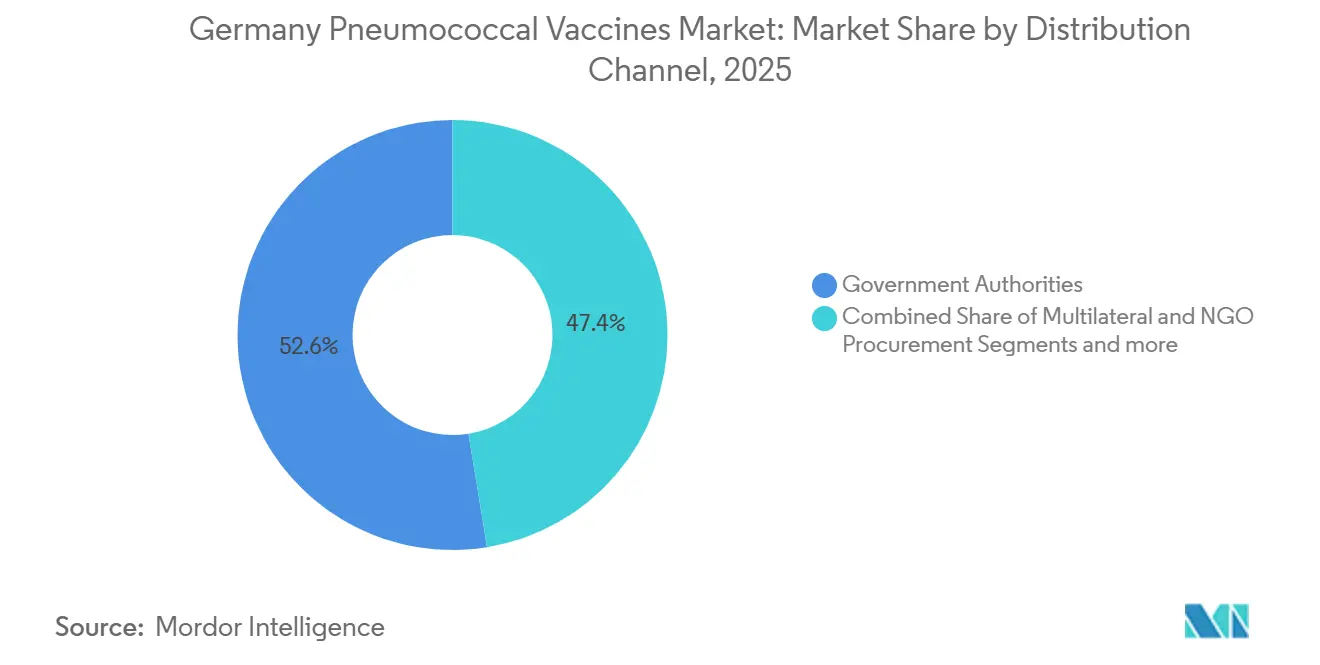

- By distribution channel, government authorities captured 52.56% revenue in 2025; multilateral and NGO procurement is the fastest-growing route at 10.98% CAGR to 2031.

- By age group, adults supplied 57.87% of the 2025 volume, whereas the pediatric cohort is projected to grow at a 12.32% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Germany representing one among them. The global report on pneumococcal vaccines market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Germany Pneumococcal Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Government Immunization Budgets & Awareness Campaigns | +2.1% | National, with higher allocations in Bavaria, Baden-Württemberg | Medium term (2-4 years) |

| Escalating Pneumonia Incidence In ≥65 Yrs & Pediatric Cohorts | +1.8% | National, pronounced in urban agglomerations (Berlin, Hamburg, Munich) | Long term (≥ 4 years) |

| Rapid Roll-Out Of Higher-Valent PCVs (15-, 20-, 21-Valent) | +2.3% | National, early adoption in Western Länder | Short term (≤ 2 years) |

| STIKO Reimbursement Backing PCV20 Adult Program | +1.6% | National, implementation led by statutory health insurers | Medium term (2-4 years) |

| Regional Pharmacy-Based Vaccination Pilots Expanding Adult Access | +1.2% | Pilot regions: North Rhine-Westphalia, Saxony, Hesse | Short term (≤ 2 years) |

| ePA-Integrated Digital Reminders (2027) Lifting Series Completion | +0.9% | National rollout, contingent on opt-in rates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Government Immunization Budgets & Awareness Campaigns

Federal and Länder health ministries increased immunization funding by 14% in 2025, earmarking EUR 1.2 billion for vaccine procurement and awareness initiatives that prioritize adults aged 60 and above [1]Bundesministerium für Gesundheit, “Nationale Präventionsstrategie,” bundesgesundheitsministerium.de. Partnerships with the German Medical Association and regional payers produced multimedia campaigns that highlight IPD risks, mirroring COVID-19 tactics that achieved high coverage among priority groups. Bavaria’s 2025 pilot, which bundled general-practitioner incentives with pharmacy vouchers, lifted adult uptake by nine percentage points within six months. While financial nudges help, behavioral inertia remains because pneumococcal disease lacks the immediacy that drove pandemic vaccination. Sustained funding will therefore focus on reinforcing risk perception and simplifying appointment logistics to convert awareness into completed doses.

Escalating Pneumonia Incidence In ≥65 Yrs & Pediatric Cohorts

Invasive pneumococcal disease incidence among senior Germans rose to 18.3 per 100,000 in 2024, up from 15.7 in 2020, a trend echoed among children under 5 where rates reached 11.2 per 100,000 [2]Robert Koch Institut, “Epidemiologisches Bulletin,” rki.de. The post-pandemic immune gap and the rise of non-vaccine serotypes such as 8, 12F, and 22F underpinned these jumps, prompting STIKO to endorse higher-valent products. Capvaxive’s coverage of serotypes 22F and 33F offers meaningful protection because both together account for 19% of adult IPD cases. Hospital stays linked to pneumonia already cost Germany’s statutory health system USD 3.1 billion annually, so vaccines that avert hospitalization have become a fiscal imperative. Consequently, epidemiological pressure is likely to keep higher-valent formulations on fast-track procurement lists across Länder.

Rapid Roll-Out Of Higher-Valent PCVs

Germany adopted higher-valent conjugates at record speed in 2025. PCV20 captured 34% of new adult prescriptions by the fourth quarter, while Capvaxive secured conditional tenders in six Länder even amid supply constraints. Each additional serotype costs manufacturers USD 15–20 million in trials and filings, yet trial data show meaningful reductions in vaccine-type disease, reinforcing payer willingness to accept higher list prices. Vaxcyte’s cell-free VAX-24, now in Phase 3, promises faster batch release and lower cost of goods, a factor that could reset competitive economics if results remain favorable. Procurement committees are therefore recalibrating cost-effectiveness models in anticipation of more entrants.

STIKO Reimbursement Backing PCV20 Adult Program

STIKO’s August 2025 revision made PCV20 the default for adults aged 60 and above and eliminated routine PPSV23 use, closing a reimbursement gap that had fragmented adult coverage. Statutory insurers now pay in full without prior authorization, removing a co-pay deterrent that previously affected nearly one quarter of eligible adults. Harmonization with France and the Netherlands enables larger multi-country tenders that shave 8–12% off unit costs, though administrative friction lingers because practitioners must enter a new billing code that adds consultation time. Streamlining electronic claims remains a priority to translate reimbursement clarity into sustained uptake gains.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High COGS & Long Biological Manufacturing Cycle | -1.4% | Global, with supply bottlenecks affecting German procurement | Long term (≥ 4 years) |

| Persistently Low Adult Uptake Despite Revised Guidelines | -1.1% | National, acute in rural East German Länder | Medium term (2-4 years) |

| Procurement Caution Amid mRNA-PCV Pipeline Uncertainty | -0.8% | National, influencing multi-year tender strategies | Medium term (2-4 years) |

| Supply Bottlenecks For 21-Valent Capvaxive During Scale-Up | -0.6% | National, temporary constraints in 2025-2026 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High COGS & Long Biological Manufacturing Cycle

Conjugate vaccines require separate fermentation, purification, and conjugation streams for each serotype, stretching production to as long as 18 months and pushing the cost of goods to USD 18–24 per dose for 20-plus valent products. When Merck’s Pennsylvania conjugation facility experienced yield losses in 2025, German deliveries slipped eight weeks, forcing public buyers to substitute with higher-priced alternatives and underscoring the fragility of single-source supply.

Persistently Low Adult Uptake Despite Revised Guidelines

Coverage among 60-69 year-olds remains flat at 21% despite full reimbursement because 41% of adults remain unaware of STIKO’s update, 28% downplay disease risk, and 19% face logistical barriers. Rural East German Länder show the widest gaps where practitioner density is lowest. Behavioral interventions such as default appointment scheduling could lift uptake, but German data-protection law requires explicit consent, limiting the tactic’s scalability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vaccine Type: Conjugate Platforms Dominate While Polysaccharide Demand Persists

Pneumococcal conjugate vaccines held 65.11% Germany pneumococcal vaccines market share in 2025, anchored by pediatric schedules that reach 73% completion at 24 months. Their T-cell-dependent response builds durable immunity, a clear edge over polysaccharide products whose antibody titers fade within five years. The Germany pneumococcal vaccines market size for conjugates is projected to expand as higher-valent PCV15 and PCV20 displace legacy PCV13, while Capvaxive adds incremental coverage in adults. Polysaccharide vaccines still serve immunocompromised adults and cost-sensitive export channels, keeping the segment relevant even as STIKO phases out PPSV23 for healthy seniors.

Residual PPSV23 inventory will sustain value growth through 2027 because some Länder plan to exhaust stockpiles before switching fully to PCV20. Conjugate suppliers therefore face a two-speed market: rapid pediatric uptake of PCV15 and steady adult migration to PCV20 or PCV21. Manufacturers that can flex volumes between paediatric and adult presentations will capture the broadest demand across the forecast period.

By Product: Prevenar Franchise Under Siege While Capvaxive Gains Traction

Prevenar 13 commanded 41.23% share in 2025 thanks to entrenched contracts, yet Pfizer has announced a managed drawdown that will cut production by 2027[3]Pfizer Inc., “Prevenar 20 Product Information,” pfizer.com. The Germany pneumococcal vaccines market size tied to Prevenar 13 will therefore shrink as purchasers pivot to Prevenar 20, which already captured one third of new adult scripts in Q4 2025. Merck’s Capvaxive differentiates with 21-valent coverage that addresses serotype replacement, winning tenders in six Länder at a 9% price premium.

Pneumovax 23’s 11.14% forecast CAGR reflects humanitarian and export demand plus select use among the immunocompromised. Synflorix remains a budget choice in price-sensitive pediatric tenders but lacks coverage for serotypes now driving German IPD, limiting upside. Competitive positioning hinges on either superior valency or lower cost; mid-range products such as Vaxneuvance risk getting squeezed unless repositioned for catch-up cohorts.

By Distribution Channel: Public Procurement Anchors Volume, NGOs Expand Fast

Government authorities distributed 52.56% of doses in 2025 because pediatric shots flow through state programs and adult claims are reimbursed by statutory insurers. Multilateral and NGO channels, however, will post the fastest growth as Germany hosts 1.8 million refugees who obtain vaccines funded by UNICEF and Gavi. Pharmacy pilots show promise but need higher administration fees to scale nationally.

The Germany pneumococcal vaccines market will therefore keep a predominantly public profile, but manufacturers courting NGO procurement must tailor pricing and packaging to humanitarian specifications such as single-dose vials, extended shelf life, and simplified cold-chain logistics.

By Age Group: Adult Segment Leads, Paediatric Demand Accelerates

Adults accounted for 57.87% of value in 2025 because STIKO expanded eligibility to all persons aged 60 and above plus younger adults with chronic disease. The paediatric segment is poised for the fastest revenue growth, helped by catch-up drives among under-vaccinated migrants and by birth-rate increases in immigrant communities. The Germany pneumococcal vaccines market size for paediatrics will benefit from re-vaccination of children who first received PCV13 and now qualify for higher-valent boosters.

Long-term-care residents remain under-served despite high disease burden. Programs that supply mobile vaccinators to nursing homes are demonstrating strong uptake, suggesting an opportunity for suppliers willing to package smaller lot sizes suited for on-site clinics.

Geography Analysis

Western Länder such as North Rhine-Westphalia, Hesse, Rhineland-Palatinate, and Saarland together consumed the majority of national doses in 2025 because dense provider networks and mature digital registries streamline adherence. North Rhine-Westphalia’s integrated registry lifted adult PCV20 uptake by eight percentage points within a year, highlighting the payoff from coordinated data systems. Southern powerhouses Bavaria and Baden-Württemberg spend the most per capita on immunization and aggressively adopted Capvaxive, securing the majority of Germany’s initial PCV21 supply at premium prices.

Northern Länder blend extremes: Hamburg leverages urban density and ePA adoption to reach high opt-in, enabling home-visit programs that cover homebound seniors. Meanwhile, Mecklenburg-Vorpommern’s sparse population faces long travel times to providers, depressing adult coverage despite full reimbursement. Eastern Länder lag even more because of low practitioner density and residual vaccine hesitancy, although Berlin bucks the trend by using 87 community vaccination centers repurposed from COVID-19 campaigns.

Disease burden and coverage often misalign. Saxony shows one of the highest IPD rates but one of the lowest adult coverage levels, underscoring the need for mobile clinics and pharmacy involvement. Bavaria’s higher spend correlates with the lowest IPD incidence among large Länder, supporting the fiscal case for proactive vaccination. The national rollout of ePA reminders could narrow regional gaps provided opt-out rates remain contained, yet privacy fears could localize benefits to tech-savvy western metro areas.

Competitive Landscape

The Germany pneumococcal vaccines market is moderately concentrated. Pfizer and Merck captured majority of revenue in 2025, but patent expiries, biosimilars, and next-generation platforms are eroding share moats. Pfizer is shelving Prevenar 13 in Europe by 2027 and invested EUR 240 million to double PCV20 capacity in Belgium. Merck differentiates Capvaxive through unique serotypes that drive emerging disease, and is adding German capacity to hedge against U.S. plant risks.

White-space opportunities lie in elderly long-term-care residents, where coverage is just 18% despite high risk, in thermostable formulations suitable for rural logistics, and in mRNA platforms that promise rapid serotype updates. BioNTech’s preclinical mRNA candidate delivered non-inferior titers in mice, and Moderna began Phase 1 trials in 2025. EMA guidance for platform vaccines allows serotype swaps without full trials, potentially accelerating mRNA entry and shifting competitive advantage from fermentation capacity to design and regulatory agility.

Mid-tier players such as GSK’s Synflorix, Serum Institute’s Pneumosil, and upcoming SK Bioscience or Walvax candidates are targeting cost-conscious tenders or humanitarian channels. Success hinges on hitting price points at least 15% below PCV20 while demonstrating non-inferior immunogenicity for common serotypes. Supply security will remain pivotal after the 2025 Capvaxive shortfall exposed the fragility of single-plant conjugation networks.

Germany Pneumococcal Vaccines Industry Leaders

GlaxoSmithKline plc

Pfizer Inc.

Merck & Co., Inc

CSL Ltd.

Serum Institute of India Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Vaxcyte dosed first participants in the OPUS-3 Phase 3 trial of VAX-31, a 31-valent PCV candidate in previously vaccinated adults

- October 2025: STIKO designated PCV20 as the adult standard of care and ended routine PPSV23 use for immunocompetent adults

- March 2025: The European Medicines Agency granted marketing authorization for Merck’s 21-valent Capvaxive, covering serotypes responsible for 84% of German adult IPD cases.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Germany pneumococcal vaccines market as the sale, within German borders, of all conjugate and polysaccharide vaccines that actively immunize against Streptococcus pneumoniae across pediatric, adult, and geriatric cohorts, whether procured by public programs or dispensed through private channels.

Scope exclusion: travel-only prophylactic packs and pipeline combination shots that have not yet received a German or EU marketing authorization are left outside this sizing.

Segmentation Overview

- By Vaccine Type

- Pneumococcal Conjugate Vaccine (PCV)

- Pneumococcal Polysaccharide Vaccine (PPV)

- By Product

- Prevenar 13

- Synflorix

- Pneumovax 23

- Apexxnar / Prevenar 20

- Vaxneuvance (PCV15)

- Capvaxive (PCV21, pipeline)

- By Distribution Channel

- Government Authorities

- Multilateral & NGO Procurement

- Private-sector Distributors & Pharmacies

- By Age Group

- Paediatric

- Adults

- Geriatric

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed infectious-disease clinicians, regional public-health officers, and supply-chain managers across Bavaria, North-Rhine Westphalia, and Saxony to verify adult revaccination rates, typical private-sector price mark-ups, and the adoption pace of higher-valent products. Structured surveys with pharmacy groups helped us refine channel splits and discount ladders.

Desk Research

We began by compiling publicly available epidemiology and coverage statistics from the Robert Koch Institute, STIKO advisories, Eurostat population tables, and WHO's Immunization Monitoring data, which anchor disease incidence, target-group size, and historical uptake. Procurement volumes and price caps were traced through Federal Ministry of Health budget lines, GEMEINSAME BUNDESAUSSCHUSS tender notices, and press releases. Company filings and investor decks augmented list prices and launch timelines, while paid databases such as Dow Jones Factiva and D&B Hoovers supplied financial context. This list is illustrative; many additional open and subscription sources were reviewed.

Market-Sizing & Forecasting

A top-down incidence-to-demand build was executed. Reported invasive pneumococcal disease cases were adjusted for under-diagnosis, multiplied by STIKO-recommended coverage ratios, and converted to doses using adherence factors. Monetary value arose from weighted average selling prices that capture public-procurement rebates and private-office premiums. Select bottom-up supplier roll-ups validated totals, and gaps were aligned. Key variables modeled include adult vaccination penetration, pediatric birth-cohort size, ASP drift as 20- and 21-valent conjugates displace PCV13, federal immunization budget growth, and exchange-rate movements. Multivariate regression, stress-tested through scenario analysis, generated the 2025-2030 forecast band.

Data Validation & Update Cycle

Outputs pass a two-layer analyst review, anomaly checks against independent shipment data, and client-side sense testing before sign-off. We refresh every twelve months, re-opening the model sooner if STIKO guidance, major product launches, or tender awards materially shift inputs.

Why Mordor's Germany Pneumococcal Vaccines Baseline Stands Firm

Published estimates often diverge because firms pick different product baskets, age-group emphasis, and valuation dates. Our disciplined scope, yearly refresh, and transparent variable selection narrow this gap for decision-makers.

Key gap drivers include: some publishers exclude private-clinic revenue, others lock adult uptake at historic lows, several rely on static 13-valent ASPs, and refresh cycles longer than two years miss post-2024 guidance that lifted adult demand.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 705.16 million (2025) | Mordor Intelligence | - |

| USD 209.5 million (2023) | Global Consultancy A | Omits private channels and applies flat adult coverage |

| USD 170.01 million (2018) | Industry Association B | Pediatric-only scope, outdated base year, no inflation indexing |

These comparisons show that, by capturing the full buyer mix, updated ASPs, and the latest STIKO policy shift, Mordor delivers a balanced, traceable baseline clients can rely on.

Key Questions Answered in the Report

How fast will sales of pneumococcal shots grow in Germany through 2031?

Sales are forecast to rise from USD 337.75 million in 2026 to USD 537.8 million by 2031 at a 9.74% CAGR, driven by guideline changes and higher-valent launches.

Which vaccine type dominates current demand?

Conjugate products hold 65.11% of value because they are embedded in pediatric schedules and now cover routine adult immunization.

What could disrupt the conjugate segment before 2031?

MRNA candidates from BioNTech and Moderna may reach market after 2028 with faster production and potentially lower costs, prompting payers to shorten tender cycles.

Which regions lead and lag in vaccination coverage?

Bavaria and Baden-Württemberg top the list thanks to higher spending and digital registries, while Saxony-Anhalt and Mecklenburg-Vorpommern trail because of sparse provider networks.

Page last updated on: