Veneer Sheets Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

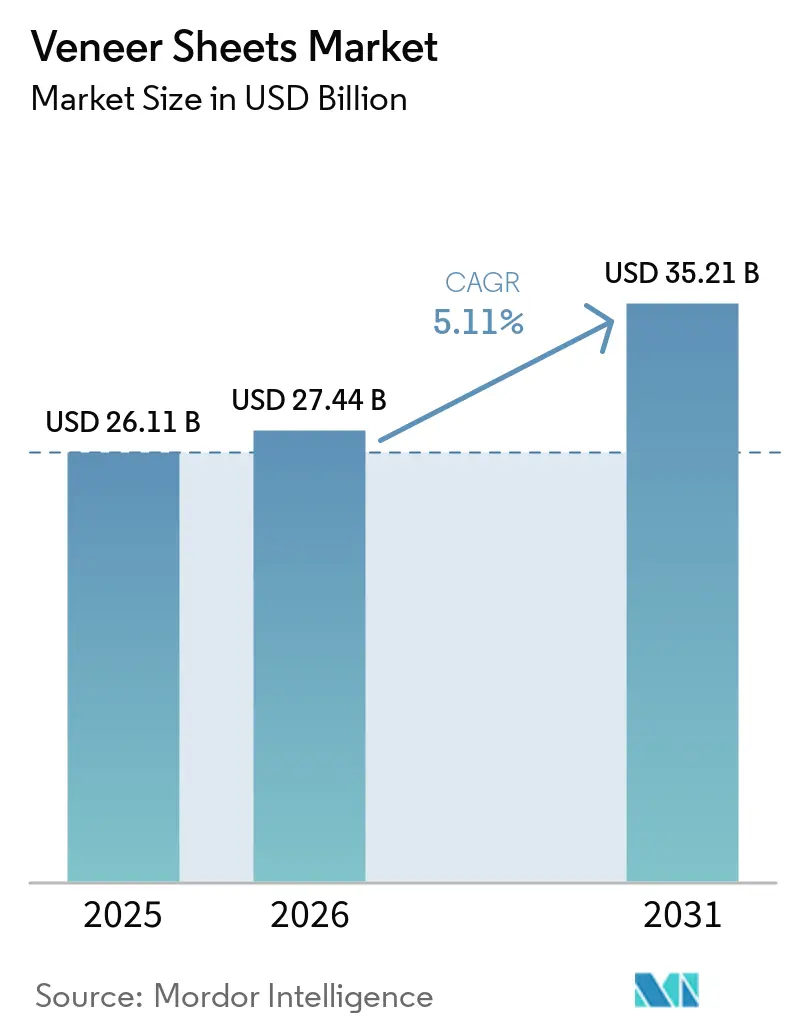

| Market Size (2026) | USD 27.44 Billion |

| Market Size (2031) | USD 35.21 Billion |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

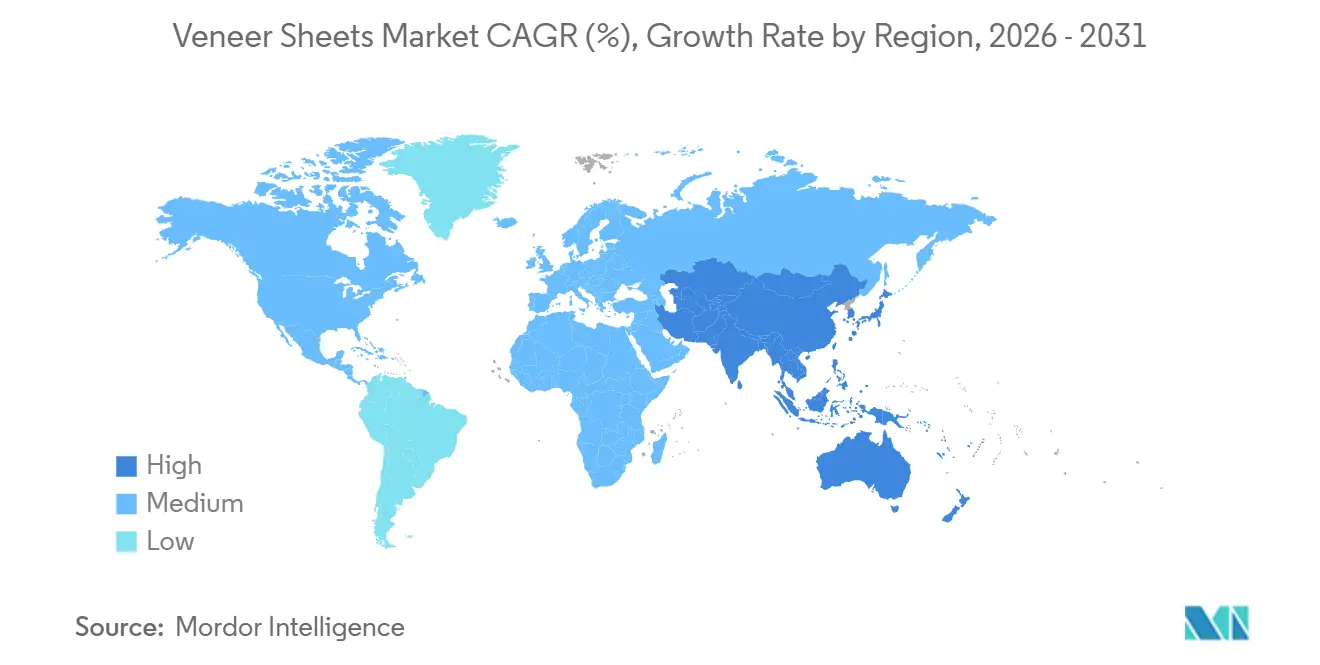

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veneer Sheets Market Analysis by Mordor Intelligence

The Veneer Sheets Market size is expected to increase from USD 26.11 billion in 2025 to USD 27.44 billion in 2026 and reach USD 35.21 billion by 2031, growing at a CAGR of 5.11% over 2026-2031. Early adoption of lignin- and tannin-based adhesives, expanding AI-driven grading systems that trim raw-material waste by up to 15%, and sustained remodeling outlays in North America and Europe together underpin the medium-term demand outlook. China’s export-oriented slicing capacity and India’s residential construction wave keep Asia-Pacific in a leadership position, while rising specification of FSC-certified species opens premium channels in automotive, yacht, and hospitality projects. Flexible-backed formats and peel-and-stick offerings are redefining customer expectations around installation speed, effectively raising the ceiling on the veneer sheets market for modular construction. At the same time, competitive pressure from digitally printed vinyl and melamine surfaces is forcing suppliers to create value through certified sourcing, zero-added-formaldehyde claims, and nano-coated durability enhancements.

Key Report Takeaways

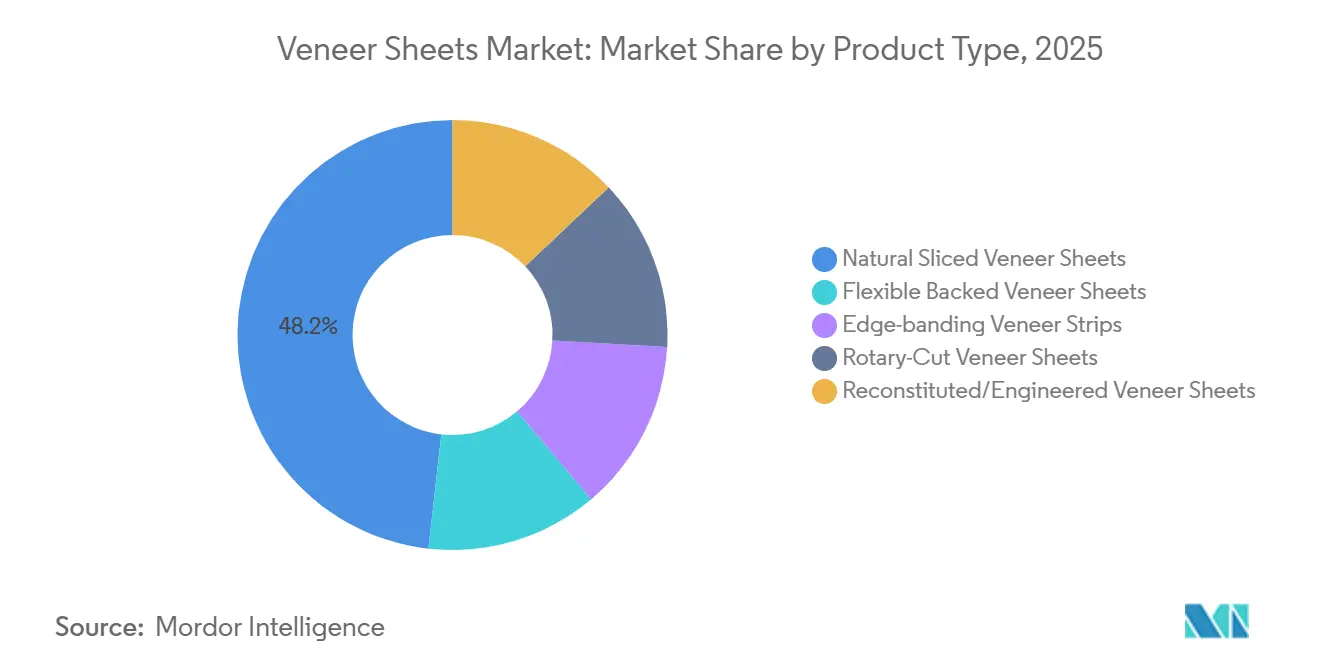

- By product type, natural sliced veneer sheets led with 48.22% of the veneer sheets market share in 2025, while flexible backed veneer sheets are forecast to post the fastest 5.48% CAGR through 2031.

- By wood species, oak retained 30.24% of the veneer sheets market share in 2025, whereas walnut is projected to expand at a 5.61% CAGR through 2031.

- By application, furniture manufacturing commanded 36.67% of the veneer sheets market share in 2025, yet automotive and yacht interiors will grow at a 5.88% CAGR through 2031.

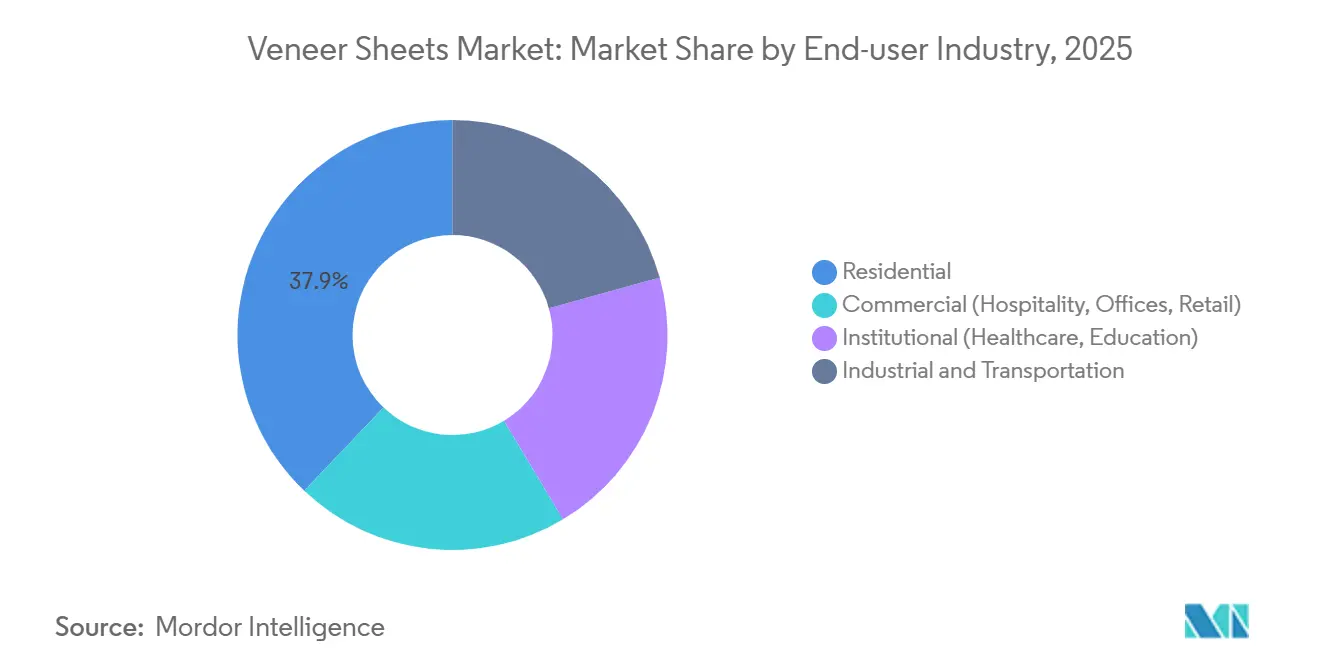

- By end-user industry, residential captured 37.89% of the veneer sheets market share in 2025 and is projected to expand at a 6.12% CAGR through 2031.

- By geography, Asia-Pacific held a 40.11% of the veneer sheets market share in 2025 and is set to accelerate at a 6.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Veneer Sheets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in residential and commercial remodeling activity | +1.2% | North America, Europe, India | Medium term (2–4 years) |

| Shift toward eco-labeled wood and low-VOC materials | +0.9% | Global, with EU and North America leading | Long term (≥ 4 years) |

| Adoption of bio-based adhesives cutting formaldehyde | +0.8% | Europe, North America, Japan | Medium term (2–4 years) |

| AI-driven veneer grain-matching and waste minimization | +0.6% | China, Germany, United States | Short term (≤ 2 years) |

| Modular off-site wall-panel systems using peel-and-stick veneers | +0.5% | Europe, North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growth in Residential and Commercial Remodeling Activity

Homeowners in the United States sustained a six-year remodeling uptrend through 2025, and kitchen or bath upgrades now consistently choose real veneer over laminates for resale value advantages. Hotel chains refreshing lobbies adopted book-matched walnut and fumed oak to create biophilic spaces that yield higher room rates in markets with occupancy above 70%. Office landlords in Tier-1 U.S. cities specify veneer wall systems to earn LEED and WELL credits, redirecting a share of commercial millwork budgets historically spent on painted gypsum. Healthcare facilities incorporated acoustic veneer panels that meet tougher 2025 noise guidelines, broadening end-market exposure. Collectively, these dynamics reinforce a stable renovation pipeline that feeds directly into the veneer sheets market.

Shift Toward Eco-Labeled Wood and Low-VOC Materials

FSC and PEFC certifications became mandatory for vendors bidding on European public-sector interiors in 2025, sidelining non-certified exporters from Indonesia and Malaysia. California tightened composite-panel formaldehyde limits, prompting U.S. finishers to switch to waterborne UV lacquers that pair well with Zero-VOC veneer offerings. Mediterranean yacht builders adopted FSC-certified teak to satisfy charterer disclosure rules, and the trend cascaded into mid-size recreational boats by early 2026. The International Tropical Timber Organization noted a 12% slide in wild teak exports from Myanmar, accelerating plantation sourcing[1]International Tropical Timber Organization, “Quarterly Market Report Q4 2025,” itto.int. Although certification adds 8-12% to landed cost, suppliers gain access to Scandinavian and German OEMs that refuse uncertified lumber, realigning revenue toward premium geographies within the Veneer sheets industry.

Adoption of Bio-Based Adhesives Cutting Formaldehyde

Lignin-based and tannin-derived resins entered commercial scale in 2024 and by 2025 allowed panel makers to hit CARB Phase 2 thresholds without urea-formaldehyde. Columbia Forest Products broadened its PureBond line using soy chemistry first developed for aerospace composites. European plants piloted 5-HMF resins from agricultural waste that cure within 10% of legacy systems, eliminating VOC off-gassing. Furniture OEMs that transition win marketing rights to “zero-added-formaldehyde” labels that command 10-15% price premiums in North America and Japan. EPA signaled in late 2025 that lower formaldehyde limits are under review, likely pulling bio-adhesive penetration deeper into the veneer sheets market by 2028.

AI-Driven Veneer Grain-Matching and Waste Minimization

KUPER released neural-network analyzers at LIGNA 2025 that lower defect rates by up to 15%. Laser-guided lathes in German and Chinese mills dynamically adjust blade pressure, capturing an extra 8% yield per log. Vision-equipped robots sort by grain orientation and color, so book-matched panels require fewer human touches, shortening lead times by 3-5 days. Premium burl inventories benefit disproportionately because a single mismatch once devalues whole cabinet sets. Early adopters report payback in under 18 months, driving rapid diffusion and further stabilizing raw-material supply for the veneer sheets market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from LVT, melamine laminates and PVC sheets | -0.7% | Global, with acute pressure in Asia-Pacific mid-tier segments | Short term (≤ 2 years) |

| Moisture/termite susceptibility without nano-coatings | -0.4% | Southeast Asia, India, Brazil | Medium term (2–4 years) |

| Prolonged global freight-capacity constraints lengthening lead-times | -0.3% | Europe, North America (import-dependent markets) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from LVT, Melamine Laminates, and PVC Sheets

Digitally printed luxury vinyl tile launched in 2025 offers oak and walnut visuals at half the installed price of real veneer, winning cost-sensitive multifamily projects. Synchronized-embossed melamine particles align texture with print, narrowing the tactile gap historically favoring veneer. Chinese PVC film suppliers scaled 3D-laminated profiles that eliminate edge-sealing and outperform veneer in terms of moisture. Kitchen cabinetry in India and Southeast Asia now hits sub-USD 150 per linear meter by opting for melamine, challenging veneer in the middle tier of the Veneer sheets industry. Authentic grain and patina still command premiums in luxury hotels, yachts, and bespoke residences, insulating the upper end of the veneer sheets market.

Moisture/Termite Susceptibility Without Nano-Coatings

Uncoated panels in humid zones show delamination rates three to four times higher than temperate installations. Brazilian developers switched to ceramic tile for wall cladding in 2025 after termite incidents raised lifecycle costs. Nano-silica and nano-zinc coatings repel water and insects but cost 20-30% more and require climate-controlled curing, limiting adoption. Suppliers offering factory-integrated coatings can amortize the premium across volume production, appealing to risk-averse builders in tropical climates. Until uptake widens, the veneer sheets market growth potential in these regions remains partially capped.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flexible Backed Veneer Sheets Drive Installation Efficiency

Natural sliced veneer sheets dominated with 48.22% of 2025 revenue, anchored in high-end cabinetry where authentic quarter-cut oak and rift-sawn walnut justify premium pricing. Flexible backed veneer sheets, however, are set to expand at a 5.48% CAGR through 2031, propelled by modular construction that requires conformable surfaces. Rotary-cut sheets serve flat-pack furniture OEMs prioritizing cost stability, while reconstituted veneers replicate scarce exotics through dyed poplar cores. Edge-banding strips climbed in 2025 as PUR adhesive lines delivered water-resistant bonds ideal for kitchens.

Automation trends accelerate the shift. Cantisa’s PVC-backed veneer edgeband, released in early 2026, runs on standard equipment and merges plastic flexibility with real-wood aesthetics[2]Cantisa S.A., “Wood Veneer Edgeband with PVC Backing,” cantisa.es . Engineered veneer thickness tolerances below ±0.05 millimeters satisfy robotic handling, positioning the veneer sheets market for higher throughput in mass production.

By Wood Species: Walnut Gains Momentum on Luxury Demand

Oak captured 30.24% of the veneer sheets market share in 2025 because of availability and quarter-sawn stability. Walnut, aided by Bentley’s 2025 shift to FSC-certified open-pore panels, will grow fastest at a 5.61% CAGR through 2031. Teak faces limited supply from Myanmar, steering yacht builders toward plantation alternatives. Maple remains a workhorse for ready-to-assemble cabinetry, while ash and cherry feed niche residential design.

Regulatory scrutiny under CITES inflates costs for mahogany and narrows its addressable base. Species diversification into certified plantation stock aligns with buyers’ sustainability pledges, reinforcing premium positioning in the veneer sheets market.

By Application: Automotive and Yacht Interiors Accelerate

Furniture manufacturing generated 36.67% of 2025 revenue, yet now grows modestly as laminates nibble share. Automotive and yacht interiors will accelerate at a 5.88% CAGR through 2031 on increased deployment of FSC-certified teak and walnut. Architectural millwork captures offices seeking LEED points, and healthcare facilities adopt acoustic veneer panels to satisfy 2025 noise standards.

CNC automation multiplied North Carolina plant output threefold, enabling curved veneer applications once limited to artisans. Floor inlays remain boutique, but door skins on engineered cores gained traction in energy-efficient European housing. These diversified applications broaden revenue streams across the veneer sheets market.

By End-user Industry: Residential Segment Lead Growth

The residential segment held 37.89% of 2025 revenue and will outpace other segments with a 6.12% CAGR through 2031. Kitchen remodels in U.S. suburbs, and first-time upgrades in India’s Tier-2 cities keep volume flowing. Commercial hospitality refreshed lobbies with walnut panels as travel rebounded, while office landlords installed veneer wall systems to command higher rents. Institutional buyers, chiefly hospitals, adopted perforated acoustic panels, turning a once-negligible niche into a stable offtake channel.

Transportation customers yield high margins due to demanding fire and sustainability certifications. Rising disposable incomes combine with aesthetic preferences to sustain residential leadership within the veneer sheets market.

Geography Analysis

Asia-Pacific retained a 40.11% veneer sheets market size in 2025 and will compound at a 6.29% CAGR through 2031. China’s Fujian and Zhejiang clusters blend automated slicing with proximity to tropical log imports, funneling output to North America and Europe. Indian demand surged in Pune, Ahmedabad, and Coimbatore, where middle-class homeowners specify oak and walnut kitchens. Japan maintains a premium import niche focused on minimalist grain aesthetics.

North America benefited from Columbia Forest Products’ 2025 acquisition of Nova Wood Lamination, which tightened Canadian supply chains and trimmed lead times for Midwest furniture OEMs. Residential remodels stabilize baseline demand, while LEED-driven office retrofits generate episodic lifts.

Europe’s appetite centers on Germany, the United Kingdom, and Scandinavia, where strict FSC rules elevate the share of integrated players such as Danzer. UPM’s 2026 review of its plywood unit hints at capacity realignment that could invite new entrants.

The Middle-East and Africa present selective growth. Dubai and Riyadh hospitality projects specify book-matched walnut, but Sub-Saharan adoption lags due to climate durability concerns. South America remains export-oriented; Brazil ships rotary-cut eucalyptus, though illegal logging curbs mahogany flows. Geographic diversification continues to define opportunity contours across the veneer sheets market.

Competitive Landscape

The market shows moderate concentration, with the top five players including Samling Timber Malaysia, Greenlam Industries Ltd., DANZER, UPM, and Sveza Group. Large incumbents continue vertical moves; Columbia Forest Products purchased Nova Wood Lamination in 2025 to secure nearby lamination assets and shorten lead times. Mid-tier firms differentiate via FSC certification, AI defect detection, and flexible peel-and-stick innovations.

Technology reshapes rivalry. KUPER’s neural-network analyzers permit Tier-2 mills to hit yields once only majors achieved, leveling quality variance. UPM’s plywood review in 2026 may trigger divestments, opening windows for private-equity roll-ups that aggregate regional mills under unified logistics. Greenlam committed INR 950 crore to plywood and particle board expansions, bundling veneers, substrates, and flooring in an integrated suite.

White-space lies in formaldehyde-free bonding and nano-coating. Producers that embed both traits at the panel level can capture 10-15% premiums in North America and Europe. Given freight volatility and certification overheads, scale will increasingly matter, yet artisan factories serving exotic species and bespoke grain-matching should retain defensible margins in luxury niches.

Veneer Sheets Industry Leaders

Greenlam Industries Ltd.

DANZER

Samling Timber Malaysia

UPM

Sveza Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: F/List introduced the aviation industry's first fully heat-release-compliant natural wood veneer sheets for premium commercial aircraft cabins. The product meets regulatory requirements while providing an alternative to synthetic finishes commonly used in aircraft interiors.

- September 2024: Duroply launched a contemporary range of dyed veneer sheets at Matecia 2024. The new range, designed in Italy, targets customers seeking elegance and sophistication in their home decor.

Global Veneer Sheets Market Report Scope

Veneer sheets are thin slices of natural wood, typically less than 3mm thick, adhered to stable substrates such as MDF, particleboard, or plywood. They provide the authentic appearance, texture, and warmth of solid wood for applications like furniture, cabinetry, and wall panels, while being more cost-effective, environmentally friendly, and resistant to warping.

The Veneer Sheets Market is segmented into product type, wood species, application, end-user industry, and geography. By product type, the market is segmented into natural sliced veneer sheets, rotary-cut veneer sheets, reconstituted/engineered veneer sheets, flexible backed veneer sheets, and edge-banding veneer strips. By wood species, the market is segmented into oak, teak, maple, walnut, birch, cherry, poplar, and other wood species (ash, mahogany, exotic). By application, the market is segmented into furniture manufacturing, architectural millwork and joinery, wall paneling and ceilings, flooring inlays, doors and windows, and automotive and yacht interiors. By end-user industry, the market is segmented into residential, commercial (hospitality, offices, retail), institutional (healthcare, education), and industrial and transportation. The report also covers the market size and forecasts for veneer sheets in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Natural Sliced Veneer Sheets |

| Rotary-Cut Veneer Sheets |

| Reconstituted/Engineered Veneer Sheets |

| Flexible Backed Veneer Sheets |

| Edge-banding Veneer Strips |

| Oak |

| Teak |

| Maple |

| Walnut |

| Birch |

| Cherry |

| Poplar |

| Other Wood Species (Ash, Mahogany, Exotic) |

| Furniture Manufacturing |

| Architectural Millwork and Joinery |

| Wall Paneling and Ceilings |

| Flooring Inlays |

| Doors and Windows |

| Automotive and Yacht Interiors |

| Residential |

| Commercial (Hospitality, Offices, Retail) |

| Institutional (Healthcare, Education) |

| Industrial and Transportation |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Natural Sliced Veneer Sheets | |

| Rotary-Cut Veneer Sheets | ||

| Reconstituted/Engineered Veneer Sheets | ||

| Flexible Backed Veneer Sheets | ||

| Edge-banding Veneer Strips | ||

| By Wood Species | Oak | |

| Teak | ||

| Maple | ||

| Walnut | ||

| Birch | ||

| Cherry | ||

| Poplar | ||

| Other Wood Species (Ash, Mahogany, Exotic) | ||

| By Application | Furniture Manufacturing | |

| Architectural Millwork and Joinery | ||

| Wall Paneling and Ceilings | ||

| Flooring Inlays | ||

| Doors and Windows | ||

| Automotive and Yacht Interiors | ||

| By End-user Industry | Residential | |

| Commercial (Hospitality, Offices, Retail) | ||

| Institutional (Healthcare, Education) | ||

| Industrial and Transportation | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the veneer sheets market?

The veneer sheets market stands at USD 27.44 billion in 2026 and is forecast to reach USD 35.21 billion by 2031.

Which region will grow the fastest through 2031?

Asia-Pacific is expected to record the quickest regional CAGR at 6.29% through 2031, thanks to China’s slicing clusters and India’s residential construction surge.

What segment shows the highest growth rate by application through 2031?

Automotive and yacht interiors are set to expand at a 5.88% CAGR through 2031 as luxury brands specify FSC-certified open-pore veneers for differentiated cabin ambiance.

How does AI affect veneer production?

Neural-network analyzers and laser-guided lathes improve yield by up to 15%, cut grading labor, and shorten lead times, enhancing profitability across mills.

Page last updated on: