Wood-based Panel Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

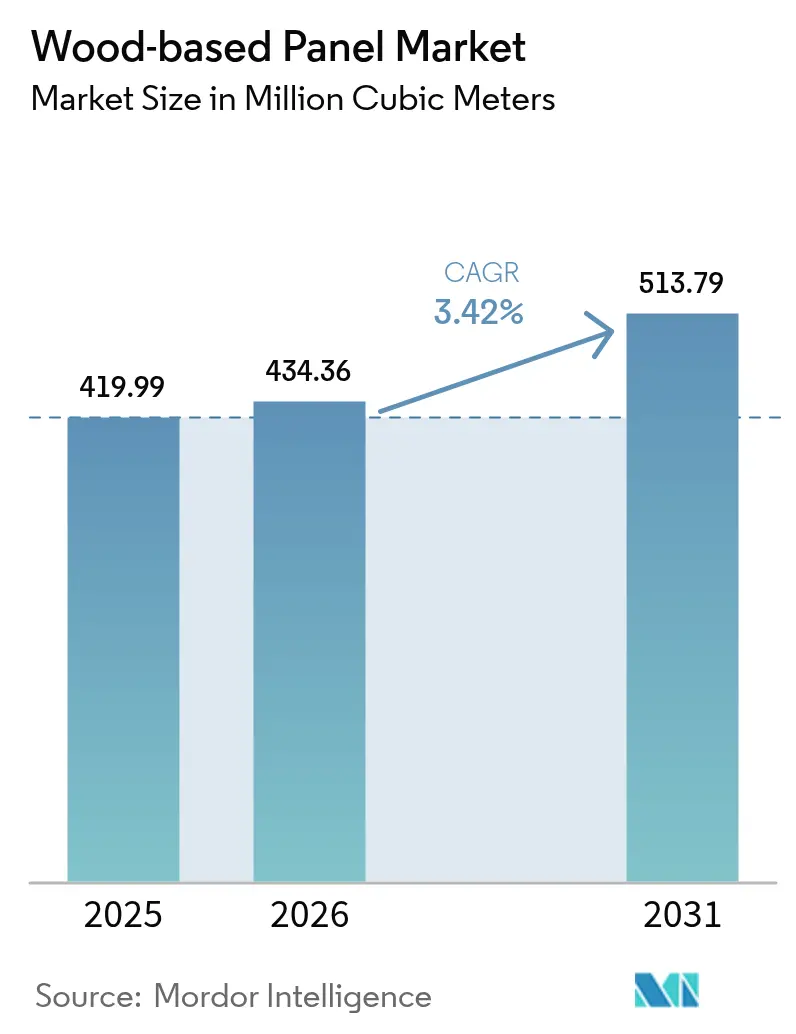

| Market Volume (2026) | 434.36 Million cubic meters |

| Market Volume (2031) | 513.79 Million cubic meters |

| Growth Rate (2026 - 2031) | 3.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wood-based Panel Market Analysis by Mordor Intelligence

The Wood-based Panel Market size in 2026 is estimated at 434.36 million cubic meters, growing from 2025 value of 419.99 million cubic meters with 2031 projections showing 513.79 million cubic meters, growing at 3.42% CAGR over 2026-2031. Robust residential construction, e-commerce-driven furniture demand, and circular-economy regulations anchor this growth even as manufacturers contend with tightening emission norms and volatile fiber costs. Abundant timber resources in Asia-Pacific, capacity expansions across Eastern Europe and the U.S. South, and the rapid uptake of structural insulated panels (SIPs) in modular housing provide additional tailwinds. Competitive strategies now center on vertical integration, resin innovation, and investments in recycling lines that recover fiber from end-of-life boards. These moves aim to capture value as transparent-wood glazing, photoluminescent façades, and other high-performance applications expand the total addressable market.

Key Report Takeaways

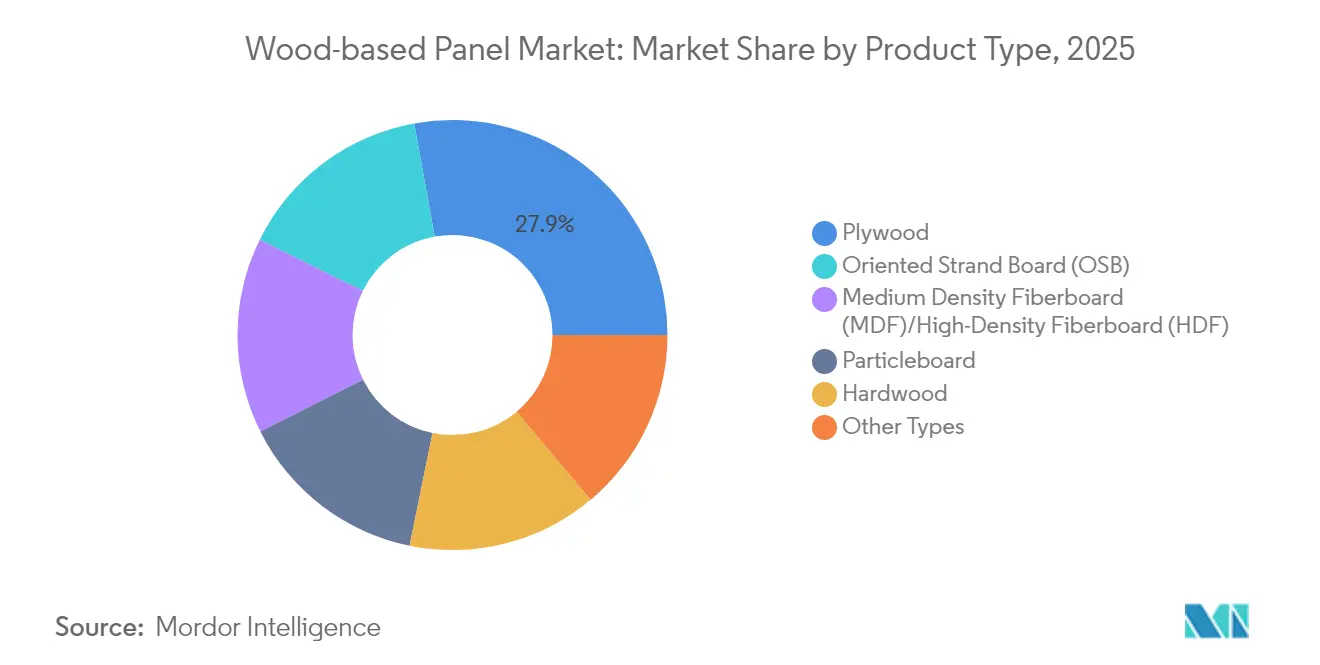

- By product type, plywood led with 27.85% of wood-based panel market share in 2025, while medium- and high-density fiberboard posted the fastest 4.12% CAGR to 2031.

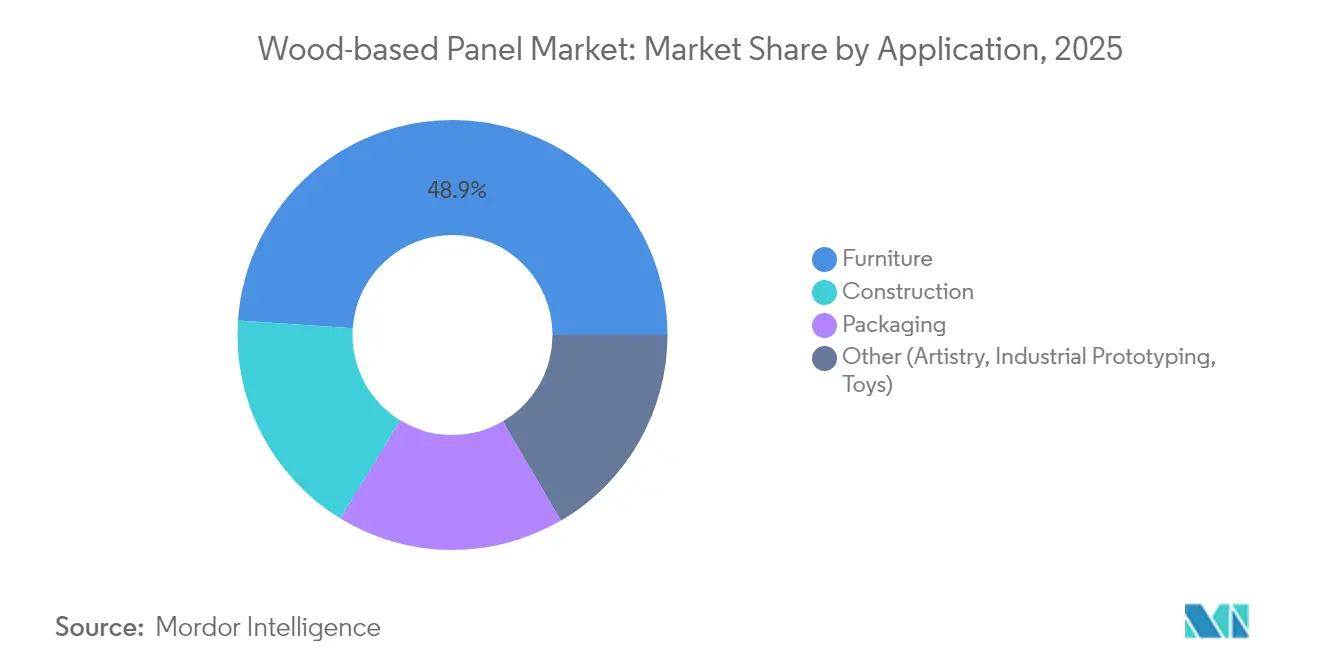

- By application, furniture accounted for 48.92% of the wood-based panel market size in 2025, whereas construction is projected to progress at a 3.63% CAGR through 2031.

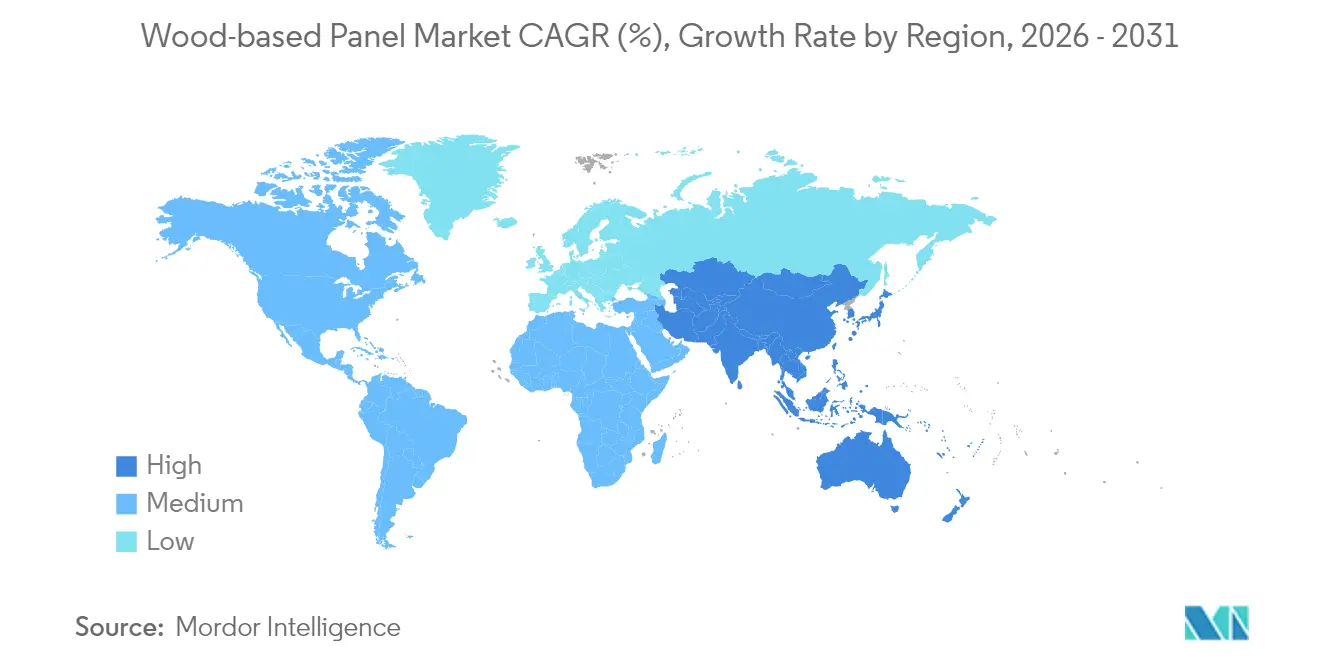

- By geography, Asia-Pacific commanded 52.12% revenue in 2025 and is poised to grow at a 3.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wood-based Panel Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction up-cycle in emerging economies | +1.2% | Asia-Pacific, Latin America, Middle East | Medium term (2-4 years) |

| Furniture e-commerce boom | +0.8% | Global | Short term (≤ 2 years) |

| Circular-economy mandates favoring engineered wood | +0.6% | Europe, North America | Long term (≥ 4 years) |

| Transparent-wood façades and automotive glazing | +0.4% | North America, Europe, Japan | Long term (≥ 4 years) |

| Rapid uptake of OSB-based SIPs in modular housing | +0.5% | North America, Northern Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Construction Up-cycle in Emerging Economies

Governments across Asia-Pacific and parts of Latin America are doubling infrastructure outlays, triggering sustained demand for plywood, MDF, and oriented strand board. India’s federal highway program and Indonesia’s new capital project underpin multi-year procurement cycles, while Turkey’s earthquake reconstruction tripled imports of Russian sawn timber to 292,200 m³ in early 2024. Manufacturers are stockpiling logs despite near-term demand softness to hedge against future supply squeezes, as evidenced by India’s 40% import surge over two quarters. Japanese conglomerates such as Sumitomo Forestry are committing to building 7,000 Southeast-Asian homes within five years, signaling confidence in regional housing pipelines. These developments cement an upward consumption trajectory across structural panels through at least 2028.

Furniture E-commerce Boom

Rising online furniture sales reduce geographic barriers, prompting quicker model turnover and small-lot production that favors flexible panel suppliers. U.S. residential furniture orders rose 22% year-on-year in April 2024, even as domestic wood-furniture shipments are 48% below 2000 levels. Import-oriented value chains still depend heavily on particleboard, MDF, and plywood substrates, sustaining bulk panel volumes. Malaysia leveraged e-commerce logistics to lift wood exports to RM 22.7 billion in 2021, with plywood the top item. Agile mills capable of just-in-time lamination and digital-print décor delivery continue capturing share within this fast-moving channel.

Circular-Economy Mandates Favoring Engineered Wood

Europe’s Circular Economy Action Plan and the 2024/1781 Ecodesign Regulation oblige products to be durable, repairable, and recyclable, tilting material selection toward engineered wood[1]European Commission, “Chemicals: The EU restricts exposure to carcinogenic substance formaldehyde in consumer products,” ec.europa.eu. Portugal will commission the world’s first industrial-scale fiberboard recycling line in 2025, capable of converting post-consumer MDF into virgin-grade fiber. Concurrently, demolition-waste regulations seek 70% recycling rates, accelerating the adoption of panels with high recycled-fiber content. North America’s voluntary green-building credits echo these requirements, encouraging producers to certify PEFC or FSC chains of custody to secure premium contracts.

Rapid Uptake of OSB-based SIPs in Modular Housing

National energy codes that entered force across the U.S. federal-financed housing system in 2024 virtually mandate high-R-value wall assemblies, triggering a spike in SIPs usage. SIPs cut job-site labor by up to 70% while slashing heating loads 40-60%. European and Australian builders now specify SIP envelopes for mid-rise projects as labor shortages intensify. These efficiency gains bolster long-run OSB demand even if traditional stick-frame construction plateaus.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Formaldehyde-emission regulations tightening | -0.9% | Global (stringent in EU, U.S.) | Short term (≤ 2 years) |

| Volatile log and fiber costs | -0.7% | Northern Europe, British Columbia | Short term (≤ 2 years) |

| EU Deforestation Regulation compliance burden | -0.4% | Europe-focused, global chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Formaldehyde-Emission Regulations Tightening

The EU will cap indoor-air formaldehyde at 0.062 mg/m³ from August 2026, compelling mills to switch to no-added-formaldehyde resins that cost 15-25% more[2]European Parliament and Council, “Regulation 2023/1115,” europa.eu . Germany’s harmonization with the EU rule eliminates domestic carve-outs, while U.S. EPA limits remain at similar thresholds, leaving little room for avoidance. Capital upgrades to continuous-press lines and alternative adhesive systems squeeze cash flows, especially at smaller particleboard facilities that already operate on slim spreads.

EU Deforestation Regulation Compliance Burden

From December 2024, exporters to the EU must geolocate harvest plots and file due-diligence statements, or face penalties up to 4% of annual turnover. Chinese plywood suppliers express data-security concerns that could curtail shipments, potentially tightening European inventories. Updated 2025 guidance allows annual, rather than per-shipment, declarations yet still demands granular chain-of-custody proof, raising administrative costs particularly for smallholders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Medium Density Fiberboard (MDF) Innovation Drives Growth

Global MDF/HDF shipments are projected to expand at a 4.12% CAGR, outpacing overall wood-based panel market growth. China continues to supply roughly 60% of the world’s MDF, yet new mills in Vietnam and Eastern Europe are closing distance through lower-cost fiber, automated sanding lines, and digital-print décors. Mekong Wood’s 600,000 m³ press in Cam Khe entered service in July 2024, immediately targeting Japanese importers seeking CARB-compliant board. In mature economies, sustainability labeling steers demand toward MDF blended with up to 24% recycled fiber without compromising bending strength.

Plywood retains a commanding 27.85% share thanks to universality in sheathing and cabinet carcasses. Yet OSB volumes are rising faster on the back of SIPs and code-compliant shear panels, while particleboard holds relevance in value-priced furniture. Hardwood plywood captures premium kitchen and RV interiors, leveraging exotic veneers despite supply tightness linked to the EUDR. Producers are diversifying feedstocks, using plantation teak offcuts in India and rubberwood in Malaysia to cut log costs and improve lifecycle scores.

By Application: Construction Momentum Accelerates

Construction will grow 3.63% yearly as governments allocate stimulus toward affordable housing and climate-resilient infrastructure. The wood-based panel market size for construction is projected to reach 90.8 million m³ in 2031, supported by building codes that reward high-R-value envelopes and carbon-sequestering materials. SIPs, CLT infill walls, and tongue-and-groove sub-floors anchor this uptake, especially in the U.S., Canada, Scandinavia, and Japan, where labor scarcity magnifies prefabrication’s value.

Furniture keeps primacy at nearly 48.92% of the total volume, albeit with slower expansion as online channels mature. Designers shifting to ready-to-assemble (RTA) wardrobes and modular sofas rely on thin MDF and melamine-laminated particleboard to balance cost and aesthetics. Packaging, particularly reusable engineered-wood pallets and temperature-stable boxes for e-commerce groceries, adds a resilient demand node, while niche uses in acoustic panels, toys, and 3-D carved art diversify revenue streams.

Geography Analysis

Asia-Pacific generated 52.12% of 2025 shipments and is set to expand at a 3.85% CAGR through 2031. China’s plywood exports reached 13.27 million m³ valued at USD 5.27 billion in 2024, bolstered by tariff concessions into ASEAN and the Middle East. Europe’s panel makers confront mixed conditions. Mills must retrofit formaldehyde-free resins and implement EUDR tracing, elevating cost curves. Yet post-pandemic renovation booms in Germany and France, plus biomass subsidies for panel offcuts, cushion demand. Eastern European plants, such as Kronospan’s 700,000 m³ OSB line in Rivne, enjoy proximity to conifer stands and EU end-users, positioning them to backfill supply gaps.

North America exhibits bifurcated trends. Structural panel output fell 4.6% for OSB and 1.0% for plywood in 2023. Mills in the U.S. South leverage low stumpage and upgraded continuous presses to export surplus OSB to Europe. British Columbia capacity rationalization continues due to stumpage hikes and wildfire disruptions. Latin America, led by Brazil, is the emergent supply base; abundant Pinus plantations and currency advantages permit price-competitive exports, while domestic consumption grows alongside prefabricated social housing schemes.

Regulatory Landscape

Regulatory focus for wood-based panels increasingly centers on emissions compliance and deforestation-free sourcing, with requirements converging across major importing markets. In North America, TSCA Title VI remains a key benchmark for composite wood products, and in February 2026 the US EPA proposed an update to its voluntary consensus standards approach by incorporating ISO 12460-2:2024(en) as an additional small-scale chamber method for quality-control testing. This would expand practical compliance pathways for mills and fabricators.

In Europe, the EU Deforestation Regulation (EU 2023/1115) drives chain-of-custody, geolocation, and due-diligence documentation requirements for wood-based products placed on the EU market. Regulation (EU) 2025/2650 postponed EUDR application to 30 December 2026 for large and medium-sized operators, and the European Commission followed with updated guidance plus an implementing act for the EUDR Information System in July 2026 to operationalize reporting and compliance workflows. Canada also tightened alignment with US practice in December 2024 through SOR/2024-256 amendments that updated formaldehyde testing requirements for routine quality control.

Value Chain Analysis

The value chain spans forest ownership and timber harvesting, through log sorting, chipping/stranding/peeling, and resin and additive supply (including formaldehyde-based and no-added-formaldehyde systems). Panel manufacture (particleboard, MDF/HDF, OSB, plywood) is followed by finishing (sanding, lamination, coating), and then distribution to furniture, construction, and packaging end users through wholesalers, home-improvement channels, and OEM supply contracts. Large producers increasingly integrate upstream fiber access and downstream value-added surfaces, including investments that add lamination capability (for decorative boards) and upgrades to continuous-press and energy systems to improve yield and cost per cubic meter.

Key friction points include fiber availability, compliance documentation, and energy and logistics costs. Supply-side constraints cited for 2025 included logging restrictions and moratoriums (for example, a cited 20% logging moratorium in Poland) alongside persistent input-price pressure, with GTI-WBP reporting the raw-material purchase price index staying above 50% for 18 consecutive months as of December 2025. On the compliance side, EU requirements such as the EUDR increase documentation needs for exporters and importers, while circular-economy initiatives bring end-of-life wood back into the chain through recycling processes (for example, Tafisa Canada Rewood capacity referenced at up to 244,000 tons annually), creating a secondary fiber stream alongside roundwood and mill residues.

Competitive Landscape

The market is highly fragmented. Top producers operate multi-continent asset portfolios that hedge regional risks. Kronospan, Swiss Krono, and Egger expanded U.S. and Eastern European mills to diversify away from saturated Western European markets. Swiss Krono’s USD 230 million South Carolina upgrade adds MDF and waste-heat generation, improving both mix and cost. New entrants focus on niche technologies. Start-ups backing transparent-wood composites, photoluminescent façades, and nanocellulose-reinforced panel skins attract venture funding as architects pursue lightweight, carbon-negative cladding. Established firms respond by setting up corporate-venture units or licensing intellectual property. Overall, the industry’s moderate concentration leaves room for technology-centric disruptors, especially in high-value applications where price premiums outweigh scale economies.

Wood-based Panel Industry Leaders

Arauco

Egger

Georgia-Pacific

Kronoplus Limited

West Fraser

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory pressure for lower-emission and traceable panels is creating whitespace for producers that can document sourcing and reduce adhesive-related emissions without sacrificing productivity. With the EU Deforestation Regulation timeline anchored to 30 December 2026 for many operators, global supply chains are moving toward geolocation-enabled due diligence, which favors panel makers that can provide verified chain-of-custody and product data to EU-facing furniture and construction customers. In North America, the compliance toolkit is also evolving, as the US EPA proposal in February 2026 to recognize ISO 12460-2:2024(en) as an additional small-scale chamber method for quality control supports more flexible testing programs for composite wood products under TSCA Title VI.

Capacity modernization and value-added finishing are also shaping opportunity areas across MDF, particleboard, and OSB. Examples include EGGER starting lamination of decorative boards at Markt Bibart in January 2026 as part of a more than EUR 200 million multi-stage investment, and Uniboard beginning a new continuous particleboard production line at Val-d Or (Quebec) in February 2026, lifting annual capacity to 272 million square feet. On the structural side, Swiss Krono announced in July 2026 that it will convert particleboard production at Sully-sur-Loire, France, to OSB, ending particleboard manufacturing by August 2026, which signals an asset shift toward construction-oriented panel demand. These steps expand the addressable market for surface-ready boards, traceable low-emission grades, and OSB-linked building systems (including SIPs), while raising competitive intensity in regions where new finishing and OSB capacity comes online.

Recent Industry Developments

- July 2026: Swiss Krono announced plans to convert its Sully-sur-Loire, France site from particleboard to oriented strand board (OSB), with particleboard production scheduled to end by August 2026. The conversion reallocates capacity toward construction-led demand for structural panels and can tighten local particleboard availability while increasing OSB supply options for European buyers.

- May 2026: The government of Ontario announced a CAD 10 million contribution supporting Georgia-Pacifics CAD 191 million modernization and expansion project at the Englehart OSB facility in Ontario, including a thermal energy system and a stated 14% production-capacity increase. Public co-funding helps accelerate mill upgrades that improve throughput and energy efficiency, reinforcing OSB supply competitiveness in North America.

- July 2024: Arauco announced a USD 100 million investment to commission and operate an OSB manufacturing line within its Trupan-Cholguan Complex in Chile (Nuble), targeting start of operations in Q2 2026. The project adds structural-panel capability closer to Latin American demand centers and diversifies OSB supply beyond the traditional North American and European production bases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the wood based panel market covers factory-made engineered wood boards used as structural or surface materials across construction, furniture, and packaging applications. The market is quantified in volume, so results are expressed in million cubic meters (MMCM) of panels consumed.

Scope exclusions: We exclude non-wood substitute boards and purely on-site carpentry woodwork that is not sold as standardized panels.

Segmentation Overview

- By Product Type

- Medium Density Fiberboard (MDF)/High-Density Fiberboard (HDF)

- Oriented Strand Board (OSB)

- Particleboard

- Plywood

- Hardwood

- Other Types

- By Application

- Furniture

- Residential

- Commercial

- Construction

- Floor and Roof

- Wall

- Door

- Other Construction (Décor, Frames, Accessories)

- Packaging

- Other (Artistry, Industrial Prototyping, Toys)

- Furniture

- By Geography

- Asia Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Rest of Asia Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Nordic Countries

- Turkey

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Egypt

- South Africa

- Nigeria

- Rest of Middle-East and Africa

- Asia Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public production and trade data so we could map where panels are made and where they flow. Sources reviewed include official forestry and wood products statistics, customs and tariff line trade releases, building and housing starts data, and energy and industrial output indicators from organizations such as FAO, UN Comtrade, the World Bank, and national statistical offices.

Along with this, we used company annual reports, investor presentations, and plant or capacity announcements reported by reputed press outlets and industry associations to confirm product mix and expansion timing. A paid subscription for company financials and intelligence was used selectively to standardize entity level details, and a shipment-level import-export database was used in targeted cases to sanity check trade signals. These sources are illustrative, and we also consulted many other public references during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was done through expert interviews and structured surveys with manufacturers, distributors, raw material and resin ecosystem participants, and large buyers in construction and furniture. This step was used to confirm conversion factors, utilization patterns, and practical demand shifts across APAC, EMEA, and the Americas, then to stress test the assumptions taken from desk research against what participants saw in day-to-day buying and production.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 15% | APAC: 41% |

| Mid tier: 48% | Functional/Unit leaders: 38% | EMEA: 34% |

| Smaller Players: 18% | Managers: 47% | Americas: 25% |

Market-Sizing & Forecasting

The sizing logic begins with a top-down reconstruction of panel demand by linking national wood products output and trade balances to downstream pull from construction and furniture activity, then converting these into panel volume using use-rate assumptions. We corroborate the totals with selective bottom-up checks, such as sampled producer capacity and utilization, plus channel checks on typical shipments, before locking the final numbers.

Key inputs used in the model include housing starts and renovation intensity, furniture production trends, panel substitution patterns (for example, MDF versus plywood in interior uses), announced capacity additions and closures, and trade shifts by major importing and exporting countries. Where local data was thin, we handled gaps with regional proxies and cross-checked them with expert feedback so the final volumes remained realistic.

For forecasting, scenario analysis was used around construction cycles and capacity ramp-ups, and we reviewed the paths with interview respondents so short-term swings and longer-term normalization were reflected without overreacting to one-year noise.

Data Validation & Update Cycle

Outputs were validated by comparing model totals against independent signals such as regional trade direction, capacity utilization commentary, and construction activity trends, then by checking for sharp discontinuities that did not match real events. When a variance was large, assumptions were revisited, and where needed respondents were re-contacted to clarify what changed in production mix, pricing incentives, or supply constraints.

A multi-step internal review is followed so definitions, math, and units are consistent across geographies and time. The report is refreshed annually, and interim updates are made when material events occur, such as major capacity moves or policy changes affecting wood supply. Before delivery, we do a final pass so the published view reflects the latest available information.

Mordor Intelligence's Wood Based Panel Market Size Measured Against Other Published Estimates

It is normal to see different market size numbers for wood based panels because not every publisher uses the same unit, market boundary, and update timing. Some focus on revenue, others focus on physical volume, and differences can widen further when prices move.

The table also shows that the largest gap often comes from scope choices, such as whether the estimate is based on cubic meters shipped and consumed or on USD revenue that depends on product mix and regional pricing. Differences in how plywood versus fiberboard grades are converted into common units, how trade re-exports are treated, and how fast capacity additions are assumed to ramp can also push totals up or down.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 434.36 M (2026) | |

| Global Consultancy A | USD 213.10 B (2025) | Reported in revenue terms, which expands the total through price and mix effects, and it can also include a broader set of board categories and channels compared to a pure volume construct. |

| Industry Publisher B | USD 198.54 B (2024) | Uses a revenue-only framing with limited visibility into conversion factors and trade adjustments, so the value can shift with currency timing and assumed average selling prices. |

The table points to a unit mismatch first, and then to scope detail as the next driver. In the Mordor Intelligence model, the market is measured as million cubic meters of wood based panels, so the outcome stays tied to production, trade balance, and end-use pull rather than price swings. With those choices made explicit, users can trace the result back to clear activity indicators and repeat the steps during updates.

Key Questions Answered in the Report

What is the projected volume for wood-based panels by 2031?

Global demand is forecast to reach 513.79 million m³ by 2031.

Which region leads consumption of engineered panels?

Asia-Pacific held 52.12% of 2025 shipments and remains the fastest-growing geography.

Why are structural insulated panels gaining popularity?

SIPs cut on-site labor up to 70% and meet tightened energy codes, boosting OSB demand.

How will formaldehyde rules affect producers?

EU and U.S. limits oblige mills to adopt costlier no-added-formaldehyde resins before August 2026.

What innovations could disrupt traditional plywood?

Transparent-wood glazing and recycled-fiber MDF open high-margin niches beyond commodity panels.

Page last updated on: