Plastisols Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.15 Billion |

| Market Size (2031) | USD 9.67 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plastisols Market Analysis by Mordor Intelligence

The Plastisols Market size is estimated at USD 7.15 billion in 2026, and is expected to reach USD 9.67 billion by 2031, at a CAGR of 6.22% during the forecast period (2026-2031). Steady uptake in textile screen-printing, automotive underbody coatings, and construction sealants sustains headline expansion, yet ongoing reformulation toward non-phthalate plasticizers is reshaping raw-material cost structures. A PVC resin surplus in Europe and Asia kept basic-feedstock prices soft through 2025, but specialty plasticizers such as DOTP and DINCH remained costly, squeezing gross margins for compounders. Asia-Pacific retains manufacturing primacy, supporting a dominant revenue share and attracting both capacity additions and foreign investment in protective coatings and textile inks. Regulatory compliance in North America and Europe is accelerating product differentiation, with ISO-certified suppliers moving fastest to launch GOTS-approved, RoHS-compliant inks that command premium pricing. Substitution threats from powder and water-borne systems are intensifying, yet plastisol continues to win in applications demanding extreme flexibility, sound damping, or thick film build.

Key Report Takeaways

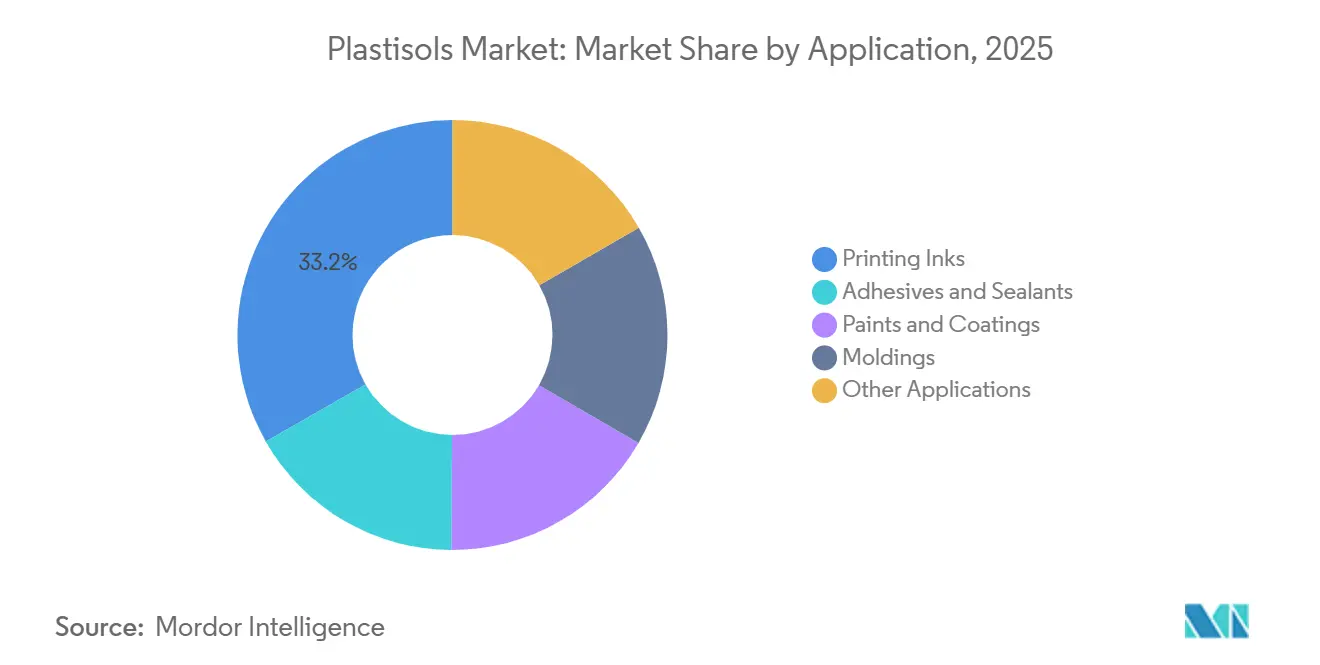

- By application, Printing Inks held 33.24% of the 2025 plastisol market share and are advancing at a 7.18% CAGR through 2031.

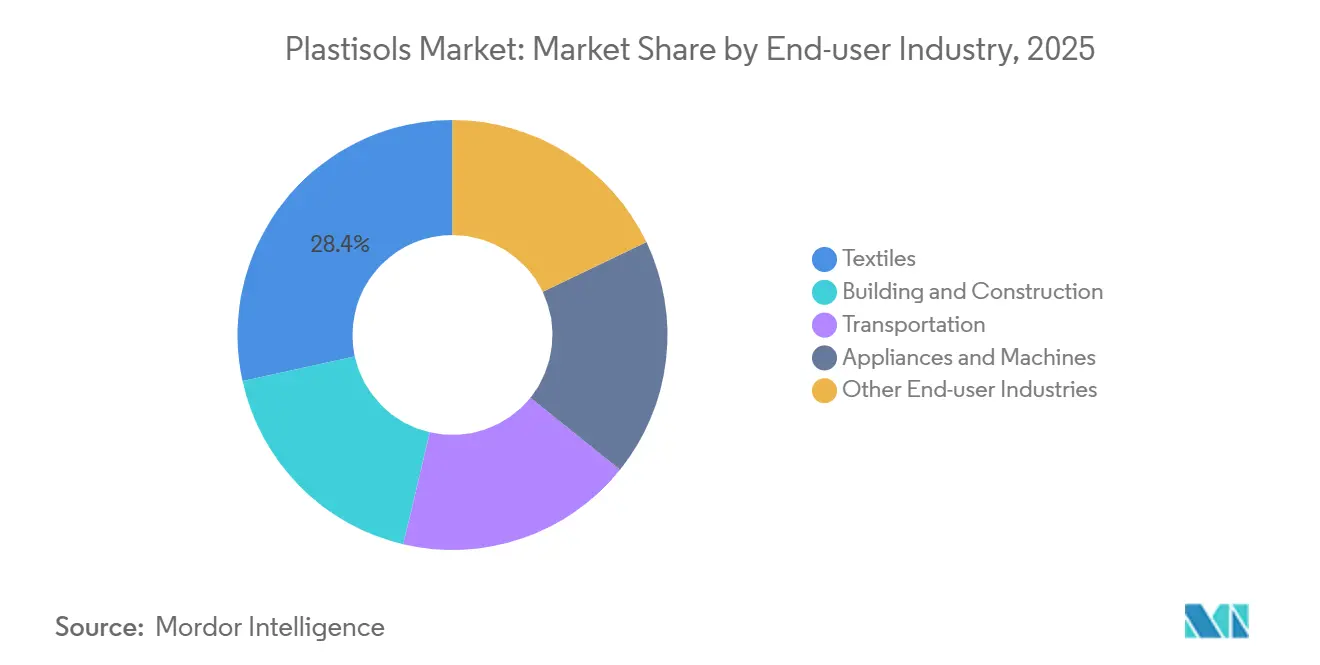

- By end-user industry, Textiles accounted for a 28.44% share of the plastisol market size in 2025 and are set to expand at a 6.97% CAGR to 2031.

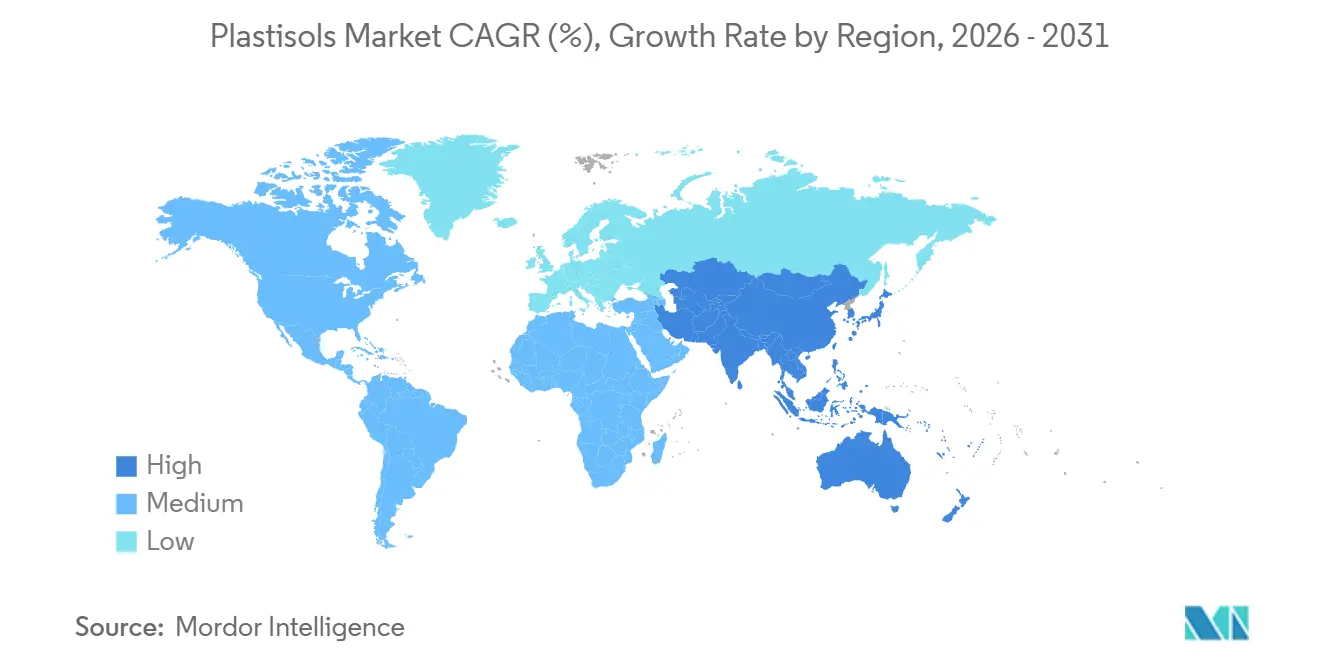

- By geography, Asia-Pacific captured 51.12% revenue in 2025 and is progressing at a 6.33% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Plastisols Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction boom driving coatings and sealants demand | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Expansion of textile screen-printing capacity in Asia-Pacific | +1.8% | China, India, ASEAN Countries | Short term (≤ 2 years) |

| Automotive corrosion-protection and lightweighting needs | +0.9% | Global, with concentration in North America and Europe | Long term (≥ 4 years) |

| Shift to phthalate-free plastisols for toys and childcare goods | +1.1% | North America and Europe, emerging in APAC | Medium term (2-4 years) |

| Emergence of 3-D-printable and smart-functional plastisols | +0.6% | North America and Europe Research and Development hubs, pilot adoption in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction Boom Driving Coatings and Sealants Demand

Saudi Arabia's Vision 2030 emphasizes the use of flexible plastisol sealants, ideal for the region's high-temperature desert climate[1]Vision 2030 Authority, “Saudi Infrastructure Megaprojects,” vision2030.gov.sa. In Brazil, an infrastructure initiative is driving up the demand for plastisol roofing membranes and bridge-joint compounds. ASEAN's spending on protective coatings was bolstered by AkzoNobel's takeover of Kansai Paint's assets in Southeast Asia and Jotun's expansion of capacity in Indonesia[2]Jotun Group, “Protective Coatings Solutions,” jotun.com. Coated-steel roofing and cladding increasingly prefer plastisol, as its impact resistance justifies the premium over polyester finishes. However, macro-projects in Argentina face challenges due to currency fluctuations and delays in import licenses, curbing short-term growth prospects.

Expansion of Textile Screen-Printing Capacity in Asia-Pacific

India's Production Linked Incentive scheme has infused significant investment into the textile manufacturing sector. This, in conjunction with seven PM MITRA mega-parks, aims to boost the domestic screen-printing output. China's printing-and-dyeing sector saw a rise in export volume in 2025, despite a dip in unit prices. This trend hints at capacity defense strategies, which, in turn, amplify ink consumption. A reduction in GST on man-made fiber has slashed input costs. This move promotes the use of plastisol inks, which cure at lower temperatures, potentially cutting per-run energy consumption. Vietnam and Bangladesh are poised to drive up the demand for plastisol formulations as they target substantial textile exports by 2030. Inks certified under GOTS and RoHS are gaining traction among regional buyers, steering formulators towards premium non-phthalate chemistries.

Automotive Corrosion-Protection and Lightweighting Needs

Sika AG's plastisol coatings shield aluminum battery enclosures in electric vehicles from galvanic corrosion, even at curing windows below 180 °C. North American assembly remains steady, projected to continue through 2028. With EV penetration expected to increase, each unit will demand more underbody coating surface area. In Europe, CO₂ mandates are steering OEMs towards aluminum and magnesium. This shift is driving up the demand for flexible, sound-damping plastisol layers, which can handle varying thermal expansions. While coatings vie with electrocoat and powder technologies, known for their lower VOC profiles, plastisol maintains its edge in intricate geometries and seams. Additionally, the rising NVH (noise, vibration, harshness) standards for luxury EVs are increasingly leaning towards thick-film plastisol solutions.

Shift to Phthalate-Free Plastisols for Toys and Childcare Goods

Wholesale reformulations, prompted by REACH and CPSIA's cap on total phthalate content, have led to a surge in raw-material costs when substituting DOTP or DINCH for DINP. Avient's 2024 debut of non-phthalate inks has spurred quicker adoption among GOTS-audited suppliers catering to European fast-fashion giants. Fujifilm's Pioneer Ultra YC, a PVC-free line, is now favored by brands imposing strict bans on all phthalates, regardless of their concentration. The intricate compliance landscape is elevating entry barriers, benefitting ISO 14001-certified plants equipped with in-house toxicology labs. Meanwhile, regulators in the Asia-Pacific are crafting similar restrictions, hinting at a potential sales boost for approved alternatives in the medium term.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent PVC and phthalate regulations (REACH, RoHS, CPSIA) | -1.3% | North America and Europe, emerging in APAC | Short term (≤ 2 years) |

| Volatile PVC resin and plasticizer feedstock prices | -0.8% | Global | Medium term (2-4 years) |

| Competition from powder and water-borne coatings | -1.0% | North America and Europe, pilot adoption in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent PVC and Phthalate Regulations (REACH, RoHS, CPSIA)

Effective 2023, ECHA's bans on DINP, DIDP, and DnOP in toys and childcare goods necessitate dual inventories, inflating working-capital needs. In the U.S., TSCA notifications introduce administrative burdens, with small compounders incurring costs for mandated third-party phthalate testing. China's GB 6675 aligns with European standards, and India is on the verge of finalizing its IS 9873 rules, underscoring a global regulatory convergence. The rising complexity of compliance has fueled mergers and acquisitions activity, highlighted by Novolex's acquisition of Pactiv Evergreen in 2024, aiming to bolster regulatory spending and intensify competition in the mid-tier market.

Volatile PVC Resin and Plasticizer Feedstock Prices

In 2024, European spot PVC prices dipped before bouncing back with an increase in early 2025, a movement attributed to energy market shocks. Premium non-phthalate plasticizers command a price higher than the traditional DINP. This pricing dynamic heightens the risk of cost pass-throughs, especially when end-users push back against price hikes. A case in point: in China, average ink unit prices fell even with rising volumes. Producers in Asia, positioned close to ethylene crackers, benefit from freight savings. In contrast, global suppliers grapple with the challenge of quarterly fixed-price contracts amidst fluctuating input costs. Notably, if there's a delay in passing through a spike in PVC costs, formulator margins could take a hit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Screen-Printing Dominance Fuels Ink Leadership

Printing Inks led 2025 revenue with 33.24% plastisol market share and will maintain the top position by expanding at a 7.18% CAGR through 2031. India's PLI incentives, China's aggressive export strategies, and ASEAN's sourcing diversification have fueled a surge in garment-decoration demand. This uptick has led to consistent re-orders for plastisol formulations, known for their opacity and elasticity on cotton and polyester blends. These formulations not only outpace water-based inks in flash-curing speed but also in color saturation. In premium niches, there's a clear preference for phthalate-free, GOTS-approved versions, allowing apparel exporters to seamlessly navigate European chemical-management audits.

The unwavering dominance of screen-printing ensures a steady demand for raw materials, bolstering capacity expansions among global ink manufacturers. The industry's shift towards non-phthalate, partially bio-based chemistries is evident. While Paints and Coatings, Adhesives and Sealants, and Moldings play a smaller role, their strategic importance is undeniable. Automotive underbody coatings, based on plastisol, provide sound-damping and corrosion protection. Meanwhile, dip-molded tool handles and electrical connectors benefit from enhanced thick-film qualities. In high-insolation areas, outdoor signage utilizes UV-resistant plastisol coats, extending its service life.

By End-User Industry: Textile Sector Anchors Demand

Textiles controlled 28.44% of 2025 revenue and are poised for a 6.97% CAGR, anchoring the consumption base for plastisol inks worldwide. India aims for a significant textile output by 2030, while China's vast installed base provides a stable foundation. A reduced GST on man-made fibers, coupled with energy savings from low-temperature curing, bolsters cost advantages over water-based systems. Ink producers and garment exporters are forming tighter partnerships, with GOTS accreditation becoming essential for accessing European fast-fashion supply chains.

Construction, transportation, and appliance manufacturers form the second tier of consumption. In Saudi Arabia, megaprojects are turning to flexible plastisol sealants for steel roofing. Meanwhile, electric vehicle platforms are opting for underbody layers that work seamlessly with aluminum substrates, avoiding galvanic corrosion. Consumer appliance manufacturers are choosing dip-molded grips and strain-relief gaskets, especially in areas where mechanical flexing rules out powder-coated options. Both healthcare and signage sectors are early adopters of antimicrobial and UV-stable plastisols, suggesting potential growth as they navigate regulatory approvals.

Geography Analysis

Asia-Pacific posted 51.12% of the global plastisol market revenue in 2025 and will climb at a 6.33% CAGR through 2031. India's PLI scheme backs new printing lines, while China, despite facing unit-price erosion, staunchly defends its export volume, collectively bolstering ink sales growth. Construction expenditures in ASEAN fuel a surge in sealant demand, prompting AkzoNobel and Jotun to expand their regional capacities. As Japan and South Korea enhance their automotive corrosion-protection layers, they cater to the burgeoning EV fleets. A reduced GST on synthetic yarn solidifies the region's cost leadership.

North America reaps benefits from a consistent light-vehicle output. With an increasing mix of EVs, each vehicle demands a larger underbody coating area. In response to CPSIA phthalate bans, there's a notable shift towards non-phthalate plastisol in toys and childcare products, bolstering the market share of ISO-certified manufacturers. Mexico's assembly sector capitalizes on tariff-free coatings under the USMCA. Meanwhile, Canadian construction projects require niche roofing applications that must withstand challenging freeze-thaw cycles.

Europe grapples with tempered growth due to REACH restrictions, which necessitate maintaining dual inventories and inflate compliance costs. Stricter CO₂ regulations push automakers towards lighter metals, consequently boosting the demand for adhesion-enhanced plastisols. Germany, France, and the UK lead the charge in regional applications spanning automotive, construction, and textile sectors. While Russia faces supply constraints due to sanctions, the Nordics leverage plastisol for offshore wind installations, emphasizing the need for fatigue-resistant coatings.

Regulatory Landscape

Regulation of plastisols is shaped primarily by restrictions on PVC additives, notably phthalate plasticizers, alongside product-specific chemical compliance regimes across consumer goods, electronics, and building materials. In Europe, REACH and RoHS continue to push reformulation away from restricted phthalates in sensitive applications such as toys and childcare goods. European Chemicals Agency-linked controls also support dual-inventory practices for legacy and non-phthalate grades. In the United States, TSCA adds a parallel layer, where the US EPA finalized risk evaluations for DEHP and DIBP in December 2025, flagging unreasonable worker risks in industrial settings relevant to plasticizer and coatings manufacturing. This has lifted the compliance and documentation demands facing plastisol compounders and their upstream suppliers.

Food-contact and packaging rules increasingly influence plastisol supply chains serving coated substrates and specialty coatings. The EU Commission updated the authorized substances list under Regulation (EU) 2026/245 in February 2026 (within the framework of (EU) No 10/2011 on food contact materials), reinforcing the need for more frequent positive-list checks, migration testing, and updated Declarations of Conformity for exporters and converters. Separately, the EU Commission amended REACH Annex XVII via Regulation (EU) 2026/1168 in June 2026 to clarify derogations for synthetic polymer microparticles when permanently incorporated into solid matrices. This affects how certain additive packages and functional fillers are screened for compliance in plastisol formulations.

Value Chain Analysis

The plastisols value chain starts with upstream feedstocks and intermediates, led by dispersion-grade PVC resin producers and plasticizer manufacturers, followed by additive suppliers providing stabilizers, commonly CaZn and BaZn systems, fillers (for example, calcium carbonate), pigments, and performance modifiers. Formulators and compounders combine these inputs using high-intensity mixing, vacuum deaeration, and controlled cooling to manage viscosity and prevent premature gelation, and then downstream processors apply plastisols via screen printing, coating, molding, or sealing processes. Gelation and fusion typically occur during end-use processing at roughly 150-210 degrees C. Regulatory-driven reformulation has also increased the importance of higher-value plasticizers, for example DINCH in phthalate-sensitive applications, alongside tighter incoming quality controls across resin and additive lots.

Distribution usually runs through direct supply to large end users, including textile ink producers, automotive underbody coating suppliers, and construction sealant formulators, as well as through regional distributors that bundle compliance support, testing, and just-in-time logistics. Industry bodies such as the Plastics Industry Association (PLASTICS), including its Flexible Vinyl Products Division, provide technical resources and testing methods that help standardize performance and compliance approaches for flexible vinyl formulations. Key pressure points sit at the interface of raw-material availability and certification readiness, where volatility in PVC and specialty plasticizers can shape contract structures. Customers increasingly require traceability documentation aligned with REACH and RoHS expectations for restricted substances.

Competitive Landscape

The plastisol market is fragmented. Economies of scale in PVC resin procurement and the expense of ISO 9001 and 14001 certifications deter small entrants. Market leaders pivot on two fronts: reformulating to meet global phthalate bans and launching premium, value-added grades. Specialty challengers are cropping up with PVC-free polyurethane or silicone inks, but they currently lack the global distribution and testing infrastructure that large incumbents wield. Technology adoption, notably digital viscosity-control and closed-loop color matching, is trimming batch variation and working-capital needs, reinforcing the advantage of multi-site producers able to amortize capital investment. White-space opportunities center on smart-functional plastisols. Antimicrobial, conductive, and UV-stable variants remain lightly patented, presenting a runway for first movers. However, the cost of securing FDA, CE, or other regulatory clearances, coupled with the need for expensive nano-additives, has delayed mass roll-outs. Players with strong balance sheets and existing medical-device relationships are best positioned to harvest these adjacencies once standards crystallize.

Plastisols Industry Leaders

Avient Corporation

Fujifilm Holdings Corporation

International Coatings

Carlisle Plastics Company

Huber Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premium, compliance-forward plastisol systems that reduce or eliminate restricted additives while maintaining thick-film build, opacity, and flexibility remain a major opportunity area for suppliers. In textiles, brand and audit requirements have pulled certifications and restricted-substance screening into procurement, which strengthens the business case for non-phthalate and lower-migration plasticizer packages. It also favors suppliers that can provide consistent documentation and third-party testing support. This compliance pull aligns with the report's demand centers in printing inks and textiles, where higher-spec inks, including GOTS- and RoHS-aligned variants referenced in the report context, create room for differentiated formulations rather than purely price-led competition.

Another whitespace is in functional and lower-emission grades for transportation and building products, where plastisols compete against powder and water-borne alternatives on VOC and sustainability metrics but retain advantages in seam coverage, sound damping, and performance in complex geometries. Product stewardship requirements are also becoming more operationally digital, as reflected by the US Consumer Product Safety Commission requirement for mandatory eFiling of test data for imported products, effective July 8, 2026. That development increases the value of suppliers that can package compliant test data and support importers and converters with faster documentation cycles. On innovation, peer-reviewed research on greener plasticizers, including published work in 2026 on multi-component green plasticizers with improved thermal stability and reduced migration, points to ongoing reformulation pathways that preserve performance while addressing migration and exposure concerns that are central to toys, childcare, and sensitive-contact applications.

Recent Industry Developments

- July 2026: FUJIFILM finalized the sale of its North American screen and flexographic ink business to Nazdar, with transition activities scheduled for completion by mid-July 2026. The transfer shifts customer support, legacy product lines, and distribution capabilities to a specialist ink supplier, reshaping competitive positioning for plastisol-related printing inks in North America.

- September 2025: Protech Group acquired Loes Enterprises, Inc., a custom compounder of PVC plastisol and related products in Saint Paul, Minnesota. The deal expands Protechs compounding footprint and customer access in plastisol formulations, supporting broader participation across inks, coatings, and specialty PVC compound applications.

- March 2024: Avient Corporation introduced Wilflex Revive bio plastisol inks containing 50% to 59% bio-derived content for screen printing. The launch broadened commercial options for lower fossil-content plastisol ink systems while targeting equivalent printability and wash durability to conventional formulations, reinforcing differentiation around sustainability and compliance themes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the plastisols market covers the revenue generated from plastisol formulations sold for industrial and commercial use, where a polymer dispersion in plasticizer is supplied for further processing into a final part or coating.

Scope exclusions: We exclude downstream finished goods value (such as completed flooring, coated fabrics, or assembled components) and count only the plastisol material itself at the point of sale.

Segmentation Overview

- By Application

- Adhesives and Sealants

- Paints and Coatings

- Printing Inks

- Moldings

- Other Applications

- By End-user Industry

- Building and Construction

- Transportation

- Textiles

- Appliances and Machines

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean picture of how plastisols are produced, traded, regulated, and consumed across major regions. We rely on public sources such as the US International Trade Commission trade data, UN Comtrade, and USGS minerals and materials statistics (to support upstream linkage assumptions). For compliance context, we also review documentation from the EPA and the European Chemicals Agency around plasticizer and related chemical requirements.

To translate industry context into usable model inputs, we also review company annual reports and investor presentations, trade association publications, and coverage from reputed industry press. Where needed, paid subscriptions for company financials and a shipment-level import and export database are used to cross-check directional volumes and pricing signals. This list is not exhaustive, and other public sources were also reviewed to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focuses on filling the gaps that desk sources cannot cover well, especially pricing logic, application-level demand shifts, and how regulations are changing formulation choices. We speak with raw material suppliers, compounders, distributors, and downstream converters across APAC, EMEA, and the Americas, so assumptions on volumes, typical price ranges, and substitution trends can be confirmed and adjusted.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 13% | APAC: 51% |

| Mid tier: 51% | Functional/Unit leaders: 40% | EMEA: 30% |

| Smaller Players: 14% | Managers: 47% | Americas: 19% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where production and trade indicators are used to reconstruct apparent consumption for key regions, which is then translated into market value using application-linked price bands. To keep the totals realistic, we corroborate the result with selective bottom-up checks, such as sampled supplier and distributor revenue signals, channel checks on typical selling prices, and volume sanity checks for high-usage applications.

A few inputs that matter in this market include PVC and plasticizer cost movements, the split between phthalate and non-phthalate formulations, construction and renovation activity (a proxy for coatings and sealants pull), textile and screen-printing output trends, and auto production and underbody coating demand. When a country-level data series is thin, we use regional averages and trade flow proxies, then validate the implied per-capita or per-industry consumption with interview feedback.

For forecasting, we use scenario analysis supported by short cycle indicators (construction output, industrial production, and auto build rates) and then apply application-level adoption and pricing assumptions. Those assumptions are reviewed with experts so the final growth path stays practical instead of being driven by one single variable.

Data Validation & Update Cycle

Outputs are checked in more than one way, including triangulation across independent signals like trade trends, upstream input pricing, and downstream activity levels. If a region shows unusual jumps, we re-check currency timing, price assumptions, and any one-off trade distortions before the numbers are accepted.

Before sign-off, the model goes through multi-step analyst reviews where key totals and growth rates are compared against historical patterns and known capacity additions or shutdowns. Reports are refreshed annually, and interim updates are triggered when material events occur, such as regulatory changes affecting plasticizers or a major shift in construction or automotive demand. Right before delivery, a fresh review pass is completed so clients receive the most current view available.

Mordor Intelligence's Plastisols Market Size Compared Against Other Published Estimates

Different published market sizes for plastisols can vary widely because the underlying counting point is not always the same, and because price assumptions move quickly with PVC and plasticizer cycles. Some studies also use a longer forecast window with a more aggressive scenario, which lifts the current-year implied value when back-calculated.

Finished coated products (for example, coated textiles or flooring) are outside Mordor Intelligence's scope, which keeps the 2026 value tied to material-level plastisol revenue rather than downstream product turnover. Other figures often expand scope to include broader plastisol-like coatings or count value at a later point in the chain, and they may also apply a different currency conversion timing and slower refresh cadence, which can widen the spread in fast-moving input cost periods.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.15 B (2026) | |

| Industry Publisher A | USD 22.90 B (2024) | Uses a much broader coverage that appears to include wider application and end-use baskets and may reflect later-stage value capture, which inflates the total versus material-only plastisol revenue. |

| Industry Publisher B | USD 23.50 B (2024) | Reports a larger starting value with a long horizon forecast, and the scope description suggests wider end-use inclusion, so the number can reflect a different counting point and pricing set than a material-level model. |

The table shows that scope and where value is counted in the chain are the biggest reasons for the gap, followed by how pricing and currency timing are handled. By keeping assumptions anchored to observable demand signals and checking them with real-world pricing and usage inputs, the estimate remains traceable to repeatable steps and easier to reconcile across regions and applications.

Key Questions Answered in the Report

What is the current size of the plastisols market?

The plastisols market size stood at USD 7.15 billion in 2026.

How fast is the plastisol market expected to grow?

It is forecast to advance at a 6.22% CAGR, reaching USD 9.67 billion by 2031.

Which application category generates the most revenue?

Printing Inks lead, holding 33.24% of 2025 revenue and expanding at a 7.18% CAGR.

Why does Asia-Pacific dominate plastisol demand?

The region hosts extensive textile printing and infrastructure programs, capturing 51.12% revenue in 2025 and maintaining the highest forward momentum.

What substitution threats does plastisol face?

Powder and water-borne coatings are taking share where low VOC and ambient-temperature curing are critical, yet plastisol remains preferred for high-flexibility and thick-film needs.

Page last updated on: