Corrugated Board Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

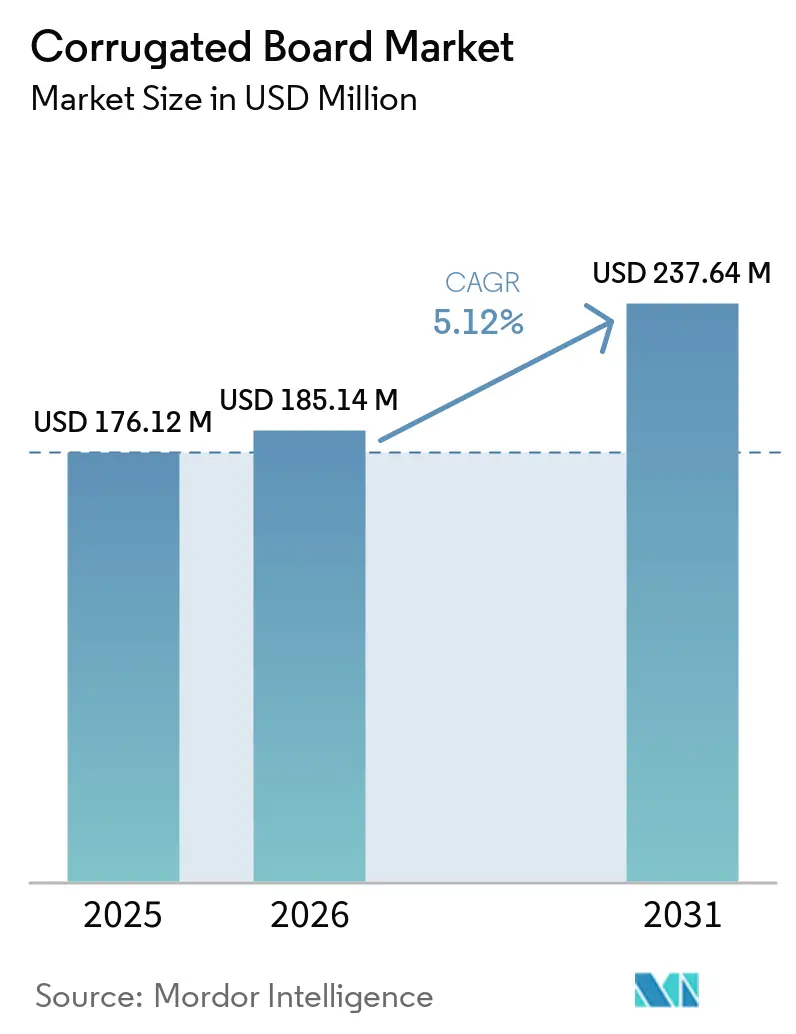

| Market Size (2026) | USD 185.14 Million |

| Market Size (2031) | USD 237.64 Million |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corrugated Board Market Analysis by Mordor Intelligence

The Corrugated Board Market size is projected to be USD 176.12 million in 2025, USD 185.14 million in 2026, and reach USD 237.64 million by 2031, growing at a CAGR of 5.12% from 2026 to 2031. Surging e-commerce parcel volumes require substrates that are both recyclable and printable at the SKU level, fueling investments in digital corrugators that laser-score, print, and glue in a single pass. Recycled-fiber linerboard is gaining ground because Europe’s Packaging and Packaging Waste Regulation 2025/40 ties brand-owner fees to virgin content, pushing mills to decarbonize by blending more recovered fiber. Asia-Pacific dominates the corrugated board market with half of global revenue, supported by China’s container exports of paper packaging and India’s manufacturing corridor expansion that attracts electronics assemblers requiring shock-resistant cartons.

Key Report Takeaways

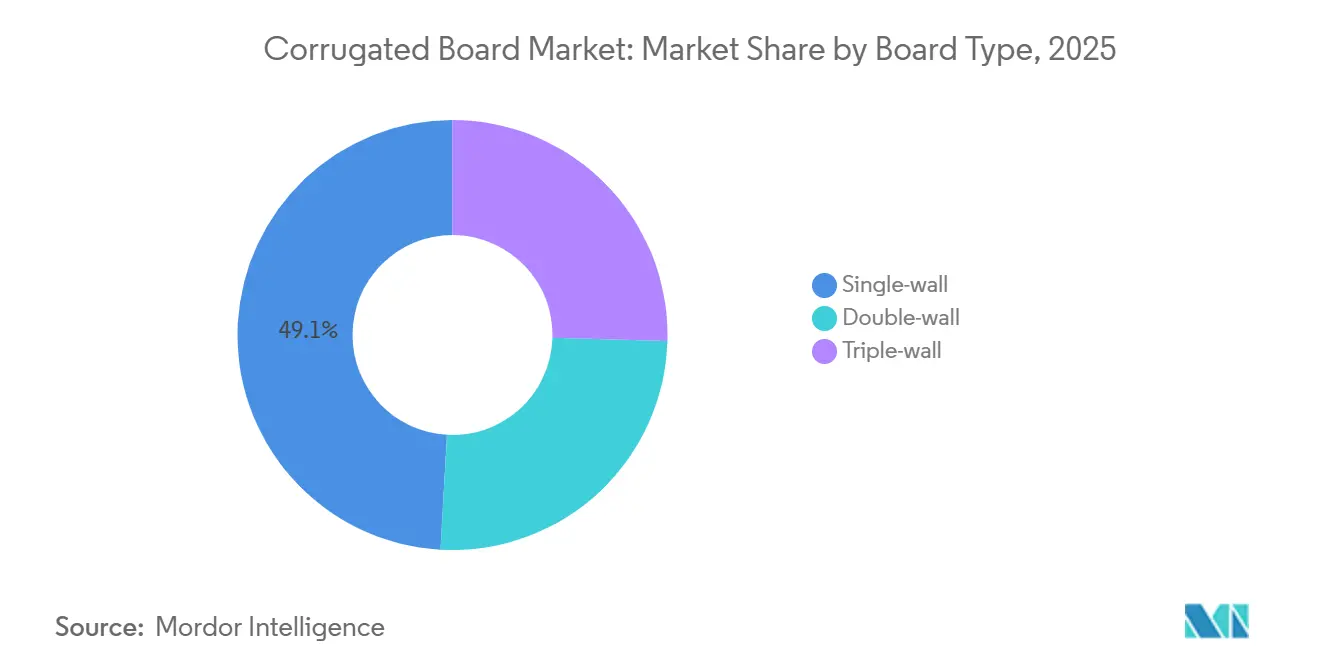

- By board type, single-wall retained 49.11% of the corrugated board market share in 2025, while double-wall is projected to expand at a 5.43% CAGR through 2031.

- By material type, linerboard held 60.34% of the corrugated board market share in 2025, while recycled fiber is projected to expand at a 5.67% CAGR through 2031.

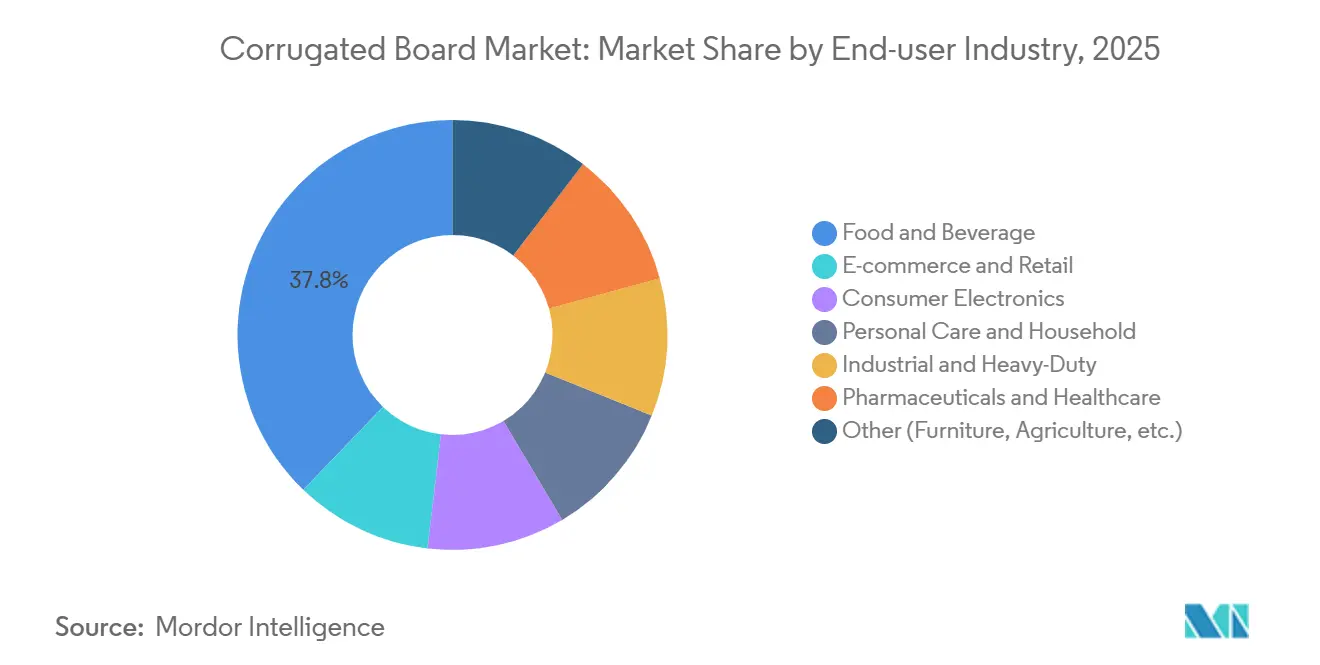

- By end-user industry, food and beverage captured 37.78% of the corrugated board market share in 2025, whereas consumer electronics is projected to advance at 6.01% CAGR through 2031.

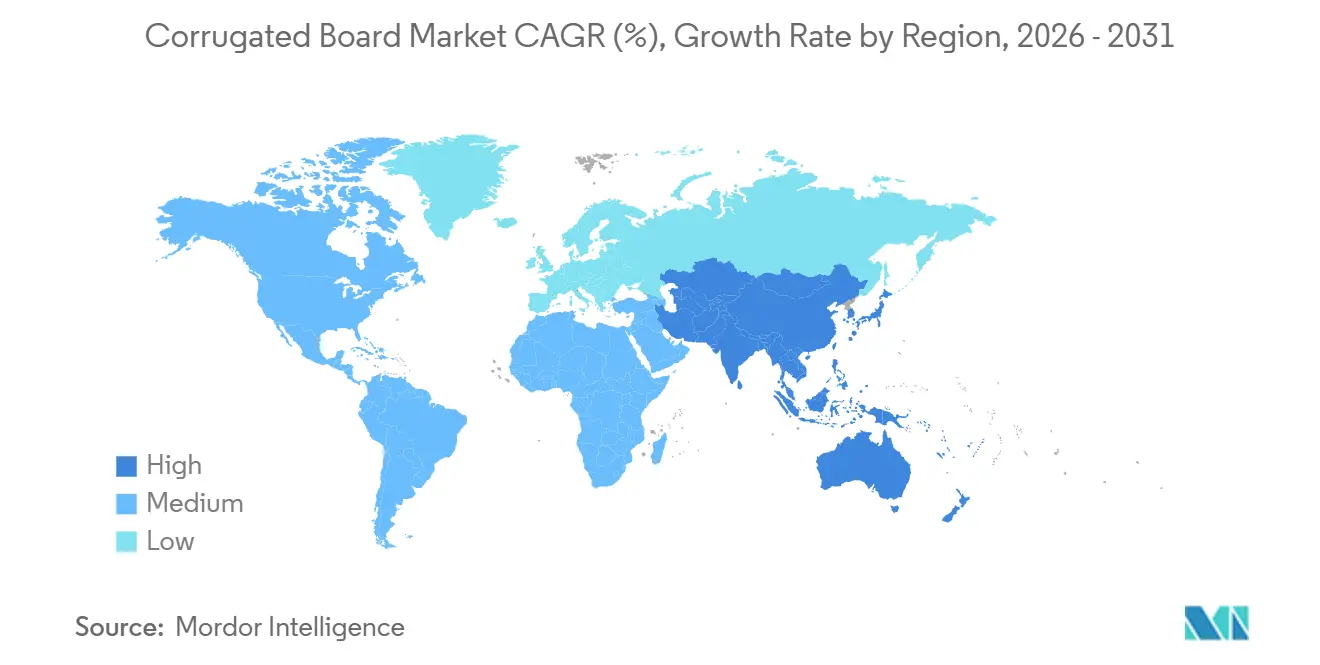

- By geography, Asia-Pacific led with 50.24% of the corrugated board market share in 2025 and is set to grow at a 5.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Corrugated Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive Growth of E-Commerce Shipments | +1.8% | Global, with APAC core accounting for 50%+ of incremental parcel volume | Medium term (2-4 years) |

| Sustainability Regulations Favouring Paper Recycling | +1.2% | North America and EU, spillover to APAC via multinational brand mandates | Long term (≥ 4 years) |

| Expansion of Food and Beverage Distribution in Emerging Markets | +0.9% | APAC (India, ASEAN), South America (Brazil, Argentina), MEA (Saudi Arabia, South Africa) | Medium term (2-4 years) |

| Shift Toward Lightweight, Cost-Efficient Packaging | +0.7% | Global, led by North America and Europe cost-reduction programs | Short term (≤ 2 years) |

| On-Demand Digital Printing Custom Packs | +0.5% | North America and EU premium consumer segments, selective APAC metro areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of E-Commerce Shipments

Integrated right-sizing systems from Packsize and Panotec cut board blanks within 5 millimeters of SKU dimensions, lowering void fill by up to 40% and reducing dimensional-weight surcharges levied by global couriers. China’s export of 1,274,503 containers of paper packaging in 2025 dwarfed India’s 272,348 tally, underscoring the region’s infrastructure depth. QR-coded single-pass digital presses from Canon and Domino now personalize B-flute and E-flute cartons at 200 meters per minute, turning shipping boxes into marketing assets. These advances collectively keep the corrugated board market aligned with parcel-volume expansion across continents.

Sustainability Regulations Favouring Paper Recycling

The EU’s Packaging and Packaging Waste Regulation 2025/40 mandates 85% collection for paper by 2030 and bans non-recyclable formats by 2030, escalating demand for recycled linerboard. U.S. states such as California, Maine, and Oregon shifted recycling costs to brand owners via extended producer responsibility schemes effective 2024-2026, steering procurement toward high-recovery substrate. Recycled-fiber capacity additions totaling 3.6 million tons since 2017 have already lowered containerboard carbon intensity by up to 20. PFAS bans in food-contact packaging, effective January 2026, further boost aqueous-coated corrugated pizza and take-out boxes. ISO 14001 certification and forest-chain traceability now appear in nearly every multinational procurement tender, embedding sustainability as a competitive necessity.

Expansion of Food and Beverage Distribution in Emerging Markets

Shelf-ready corrugated trays cut unpacking labor for Indian and Indonesian supermarkets while slashing fresh-produce spoilage by 10-15% thanks to ventilated flute design. DS Smith’s TailorTemp cold-chain pack keeps 2-8 °C for 36 hours, aiding quick-commerce grocery fulfillment that relies on last-mile scooters in humid ASEAN climates. World Health Organization vaccine guidelines that specify corrugated construction elevate carton standards in emerging pharma logistics. These forces combined raise corrugated board market penetration across food, beverage, and cold-chain lanes.

Shift Toward Lightweight, Cost-Efficient Packaging

Converters in North America and Europe have trimmed linerboard grammage from 200 g/m² to 175 g/m², lowering material spend by up to 15% while meeting parcel carriers’ 32 ECT strength requirement. Georgia-Pacific’s USD 800 million Alabama River Cellulose upgrade will supply fluff pulp to blends that cut basis weight without sacrificing stiffness by 2027. PCA’s USD 1.8 billion Greif acquisition unlocked 15% efficiency gains at Massillon and Riverville mills, supporting down-gauged medium production. TOPS and Epicor nesting software lifts pallet cube utilization to 90%, translating into USD 0.25 freight savings per carton on long-haul lanes. Lightweighting thus offsets pulp volatility and carbon-pricing pressures, sustaining corrugated board market competitiveness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Kraft Linerboard Price Volatility | -0.9% | Global, most acute in North America and Europe reliant on virgin-fiber mills | Short term (≤ 2 years) |

| Competition from Flexible Plastic Mailers | -0.4% | North America and EU e-commerce apparel and cosmetics segments | Medium term (2-4 years) |

| Carbon Border Taxes on Paper Exports | -0.3% | EU imports from non-EU mills; secondary impact on APAC and South America exporters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Flexible Plastic Mailers

Polyethylene mailers captured 8–12% of North American lightweight parcels in 2025, delivering 30–40% cost savings against single-wall corrugated in sub-2 kg bands. Dimensional shipping charges favor flexible pouches that hug apparel contours, saving USD 0.50–1.00 on residential deliveries. Yet Maine, Oregon, and Colorado now assess USD 0.02-0.05 recycling fees per plastic mailer, narrowing economics and prompting Amazon to test fiber-padded mailers eligible for curbside recycling. The EU Single-Use Plastics Directive layers similar EPR levies, nudging brands toward micro-flute cartons as thin as 1.5 millimeters that meet automated sortation rigors. Corrugated converters that match mailer thickness reclaim volumes otherwise lost to plastic.

Carbon Border Taxes on Paper Exports

The EU Carbon Border Adjustment Mechanism levies up to EUR 80 per tonne of embedded CO₂ on containerboard imports starting 2026, boosting landed cost 4-6% for coal-powered mills in Brazil, Indonesia, and China[1]European Commission, “Carbon Border Adjustment Mechanism,” ec.europa. Klabin’s biomass-powered Puma II mill cuts Scope 1 emissions 25%, positioning exports to avoid surcharges. Mondi’s EUR 1.2 billion upgrades at Štětí and Duino embed energy-efficiency to stay inside ETS caps. Upstream aluminum and steel used in die-cutting also fall within CBAM, inflating converter tooling costs. These fiscal frictions temper the corrugated board market’s price competitiveness versus domestic EU supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Board Type: Double-Wall Gains on Appliance Consolidation

Single-wall held 49.11% revenue in 2025, yet double-wall is growing at a 5.43% CAGR to 2031 as appliance shippers consolidate two cartons into one reinforced unit that still meets Amazon’s Frustration-Free 2.0 metrics. Triple-wall remains niche for chemical drums and auto parts requiring burst strength above 1,000 kPa. Engineered BC-flute replaces AC-flute in electronics, trimming impact damage by up to 40% and enhancing shelf presentation.

Micro-flute E- and F-profiles are penetrating cosmetics and pharma because they permit high-definition litho and rigid micro-cartons. Smurfit Westrock shuttered 600,000 tons of legacy C-flute capacity in 2024 while funding B-flute upgrades that serve premium direct-to-consumer channels. Fewer, stronger cartons reduce freight cube and align with sustainability goals, giving double-wall formats durable tailwinds inside the corrugated board market.

By Material Type: Recycled Fiber Narrows the Gap

Linerboard captured 60.34% of 2025 revenue, but recycled fiber is projected to advance at a 5.67% CAGR through 2031 as EPR fees penalize kraft content in U.S. coastal states. Virgin-fiber demand is limited to humid export packs where wet-strength is paramount.

OCC stabilized at USD 45 in January 2026, keeping recycled linerboard cost-competitive with kraft. Mondi’s 420,000 tpa Duino line and PCA’s newly integrated Massillon mill flex grade mixes based on pulp-to-OCC spreads. Virgin boards still dominate FDA-regulated food-contact and tropical exports, ensuring dual-supply strategies across the corrugated board market.

By End-user Industry: Consumer Electronics Outpaces Food and Beverage

Food and beverage retained 37.78% in 2025 on the back of shelf-ready trays and cold-chain packs like DS Smith TailorTemp that cut CO₂ 40% versus EPS. Yet consumer electronics is slated for 6.01% CAGR to 2031, the swiftest among verticals.

Engineered paper inserts replace polystyrene, reducing laptop damage 30-40% and meeting California’s PFAS ban effective 2026. Flexible mailers still erode e-commerce apparel volumes, but micro-flute cartons reclaim share where EPR charges bite. Industrial heavies such as auto parts grow with manufacturing output but face plastic tote substitution in closed loops, balancing segment mix within the corrugated board market.

Geography Analysis

Asia-Pacific commanded 50.24% of revenue in 2025 and is projected to grow at a 5.88% CAGR through 2031, lifted by China’s vast export base and India’s PLI-driven electronics clusters[2]UN Comtrade, “Paper Packaging Exports 2025,” comtrade.un.org. Japan’s Rengo opened a heavy-duty plant in Germany in 2025, underscoring outbound investments aimed at serving European auto clients. South Korea’s container exports back its role as electronics-packaging hub.

North America faces linerboard price hikes yet benefits from Amazon’s fulfillment build-out and nearshored Mexican manufacturing. International Paper’s USD 9.9 billion DS Smith deal adds transatlantic scale and USD 514 million. Capacity closures totaling 4 million tons keep supply tight, reinforcing disciplined pricing.

Europe grapples with PPWR recyclability mandates and CBAM levies. Mondi’s EUR 1.2 billion capex at Štětí and Duino aligns with low-carbon trends, while its EUR 634 million acquisition of Schumacher accelerates access to premium converters. Nordic mills like Stora Enso’s Oulu 750,000 tpa board line capitalize on integrated pulp energy efficiencies. South America benefits from Klabin’s Puma II export flows, whereas the Middle-East builds industrial carton capacity for Vision 2030 infrastructure. These regional dynamics jointly influence the corrugated board market trajectory.

Mordor Intelligence provides coverage of the corrugated board market across other key regional markets. Detailed country-level analysis extends to Morocco incorporating local coverage and market participation, as required.

Competitive Landscape

The corrugated board market exhibits moderate concentration with top five players including Smurfit Westrock, International Paper, Mondi, Georgia-Pacific LLC, and Nine Dragons Worldwide (China) Investment Group Co., Ltd. Vertically integrated models lock in fiber supply and enable price leadership; PCA’s Greif buy delivered 15% mill-to-box efficiencies. Independents leverage HP PageWide and Canon corrPress assets to serve sub-500-unit cosmetics runs ignored by majors, preserving regional agility.

White-space areas include cold-chain corrugated, where DS Smith TailorTemp meets WHO vaccine standards, and electronics inserts engineered for 40% damage reduction. Automation innovators such as Packsize enable real-time rightsizing, cutting void fill 40%, and reducing corrugate grams per parcel. Competitive heat remains highest in single-wall e-commerce, where plastic mailers nibble share; still, state-level EPR fees tilt the balance back toward fiber solutions.

Smurfit Westrock closed 600,000-ton legacy capacity in 2024, redirecting funds to B- and E-flute lines that target premium D2C brands. Players lacking digital print or micro-flute agility risk share erosion as corrugated board market customers demand faster, personalized runs.

Corrugated Board Industry Leaders

International Paper

Nine Dragons Worldwide (China) Investment Group Co., Ltd.

Mondi

Georgia-Pacific LLC

Smurfit Westrock

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Mondi created a customized corrugated packaging solution for Argesim Teknoloji, a Turkish technology company specializing in sensor-based products, which achieved a 10% reduction in logistics and production costs. The collaboration replaced Argesim Teknoloji's standard Abox boxes and foam-filled packaging with high-strength, tailored corrugated solutions designed for sensors used in applications such as solar energy systems and grain silos.

- March 2026: Smurfit Westrock expanded its operations in Ecuador through the acquisition of Cartomanabí, which had an annual corrugated production capacity exceeding 50,000 tons. Established in 2020 and located in Montecristi, Cartomanabí primarily catered to the FMCG, agriculture, protein, and industrial markets.

Global Corrugated Board Market Report Scope

Corrugated board is a lightweight, durable, and versatile packaging material composed of a fluted corrugated medium bonded between flat linerboards. It is extensively used for shipping, storage, and retail purposes. Additionally, 75% of corrugated board is produced from recycled pulp, making it an environmentally friendly option.

The Corrugated Board Market is segmented into board type, material type, end-user industry, and geography. By board type, the market is segmented into single-wall, double-wall, and triple-wall. By material type, the market is segmented into linerboard, medium, recycled fiber, and virgin fiber. By end-user industry, the market is segmented into food and beverage, e-commerce and retail, consumer electronics, personal care and household, industrial and heavy-duty, pharmaceuticals and healthcare, and other (furniture, agriculture, etc.). The report also covers the market size and forecasts for corrugated board in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Single-wall |

| Double-wall |

| Triple-wall |

| Linerboard |

| Medium |

| Recycled Fiber |

| Virgin Fiber |

| Food and Beverage |

| E-commerce and Retail |

| Consumer Electronics |

| Personal Care and Household |

| Industrial and Heavy-Duty |

| Pharmaceuticals and Healthcare |

| Other (Furniture, Agriculture, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Board Type | Single-wall | |

| Double-wall | ||

| Triple-wall | ||

| By Material Type | Linerboard | |

| Medium | ||

| Recycled Fiber | ||

| Virgin Fiber | ||

| By End-user Industry | Food and Beverage | |

| E-commerce and Retail | ||

| Consumer Electronics | ||

| Personal Care and Household | ||

| Industrial and Heavy-Duty | ||

| Pharmaceuticals and Healthcare | ||

| Other (Furniture, Agriculture, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the corrugated board market?

The corrugated board market stands at USD 185.14 million in 2026 and is forecast to reach USD 237.64 million by 2031.

Which region leads in revenue in 2025?

Asia-Pacific holds 50.24% of 2025 revenue and is expected to keep leading through 2031 as e-commerce and manufacturing expand.

What end-user industry is expected to grow fastest through 2031?

Consumer electronics is projected to grow at a 6.01% CAGR through 2031 to engineered paper inserts replacing polystyrene.

What threatens corrugated boxes in lightweight parcels?

Flexible plastic mailers currently serve 8–12% of North American apparel shipments, though new recycling fees narrow their cost edge.

Page last updated on: