Fiber Cement Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

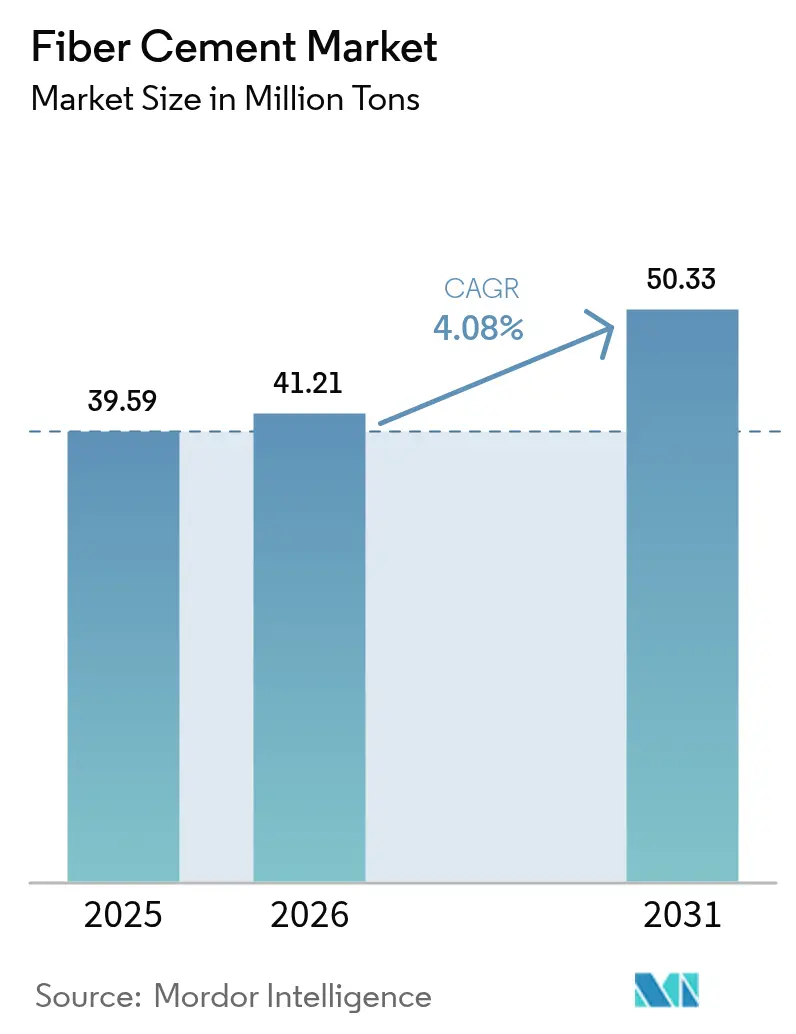

| Market Volume (2026) | 41.21 Million tons |

| Market Volume (2031) | 50.33 Million tons |

| Growth Rate (2026 - 2031) | 4.08% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fiber Cement Market Analysis by Mordor Intelligence

The Fiber Cement Market size is projected to be 39.59 million tons in 2025, 41.21 million tons in 2026, and reach 50.33 million tons by 2031, growing at a CAGR of 4.08% from 2026 to 2031. Rising insurance requirements for wind-resistant cladding in hurricane corridors, stricter fire-safety codes such as National Fire Protection Association (NFPA) 285, and the first commercial roll-outs of carbon-negative formulations are steering project owners toward fiber cement solutions. Prefabricated façade manufacturers are embedding the material into factory-built panels that cut on-site labor by 40%, while lifecycle cost analyses in wildfire and coastal zones show that fiber cement delivers a 30-40 year service life and commands double-digit insurance discounts compared with vinyl or wood. Asia-Pacific remains the anchor market on the strength of China’s prefab mandate and India’s affordable-housing schemes, whereas the Middle East and Africa deliver the fastest regional growth as Saudi megaprojects specify non-combustible envelopes. Competitive rivalry pivots on kiln energy efficiency and low-carbon chemistries, with scale leaders James Hardie, Etex Group, and Saint-Gobain reinforcing positions through alternative-fuel systems and cellulose-nanofibre blends that qualify for Leadership in Energy and Environmental Design (LEED) v5 credits.

Key Report Takeaways

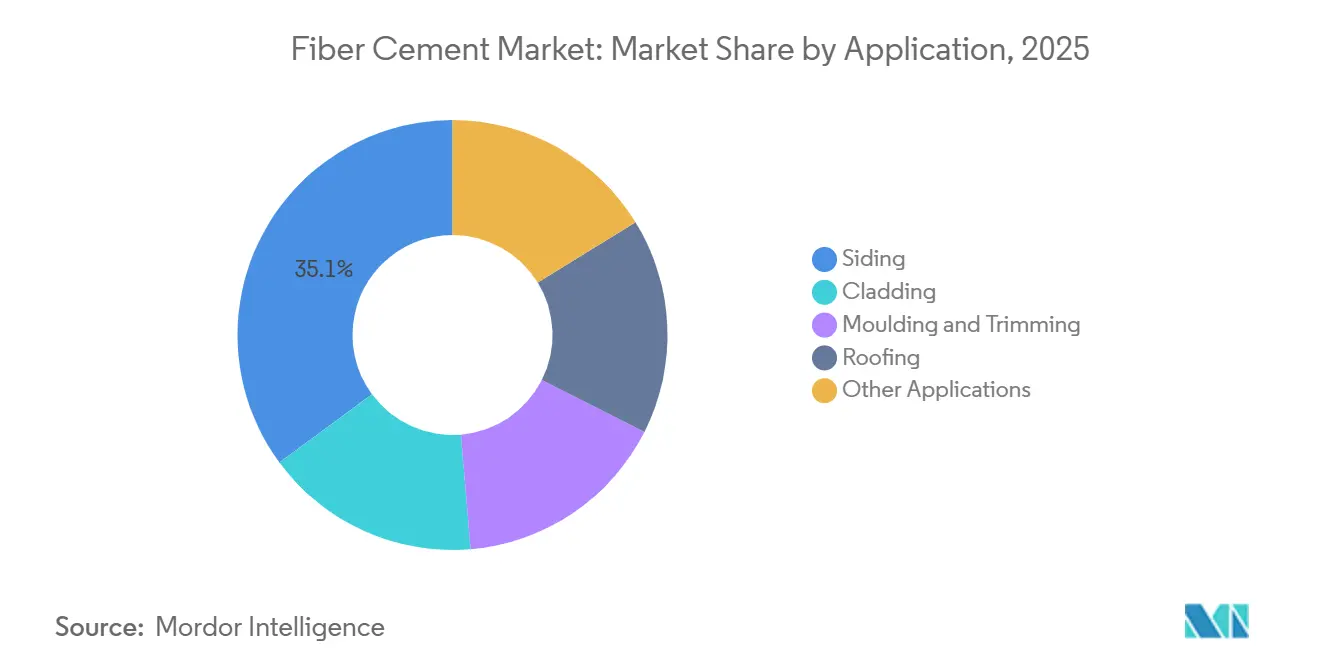

- By application, siding accounted for a 35.11% share of the Fiber Cement market in 2025, and cladding is advancing at a 4.58% CAGR during the forecast period (2026-2031).

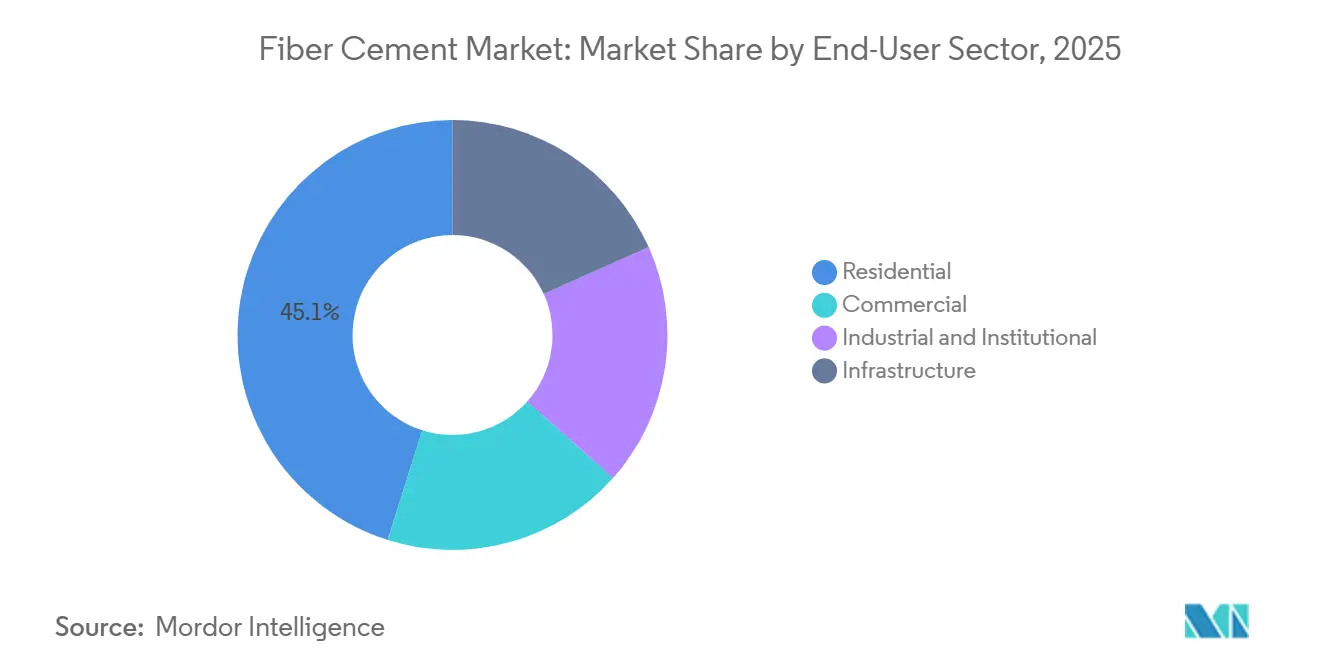

- By end-user sector, residential commanded a 45.12% share of the Fiber Cement market size in 2025; commercial is set to grow at a 4.24% CAGR during the forecast period (2026-2031).

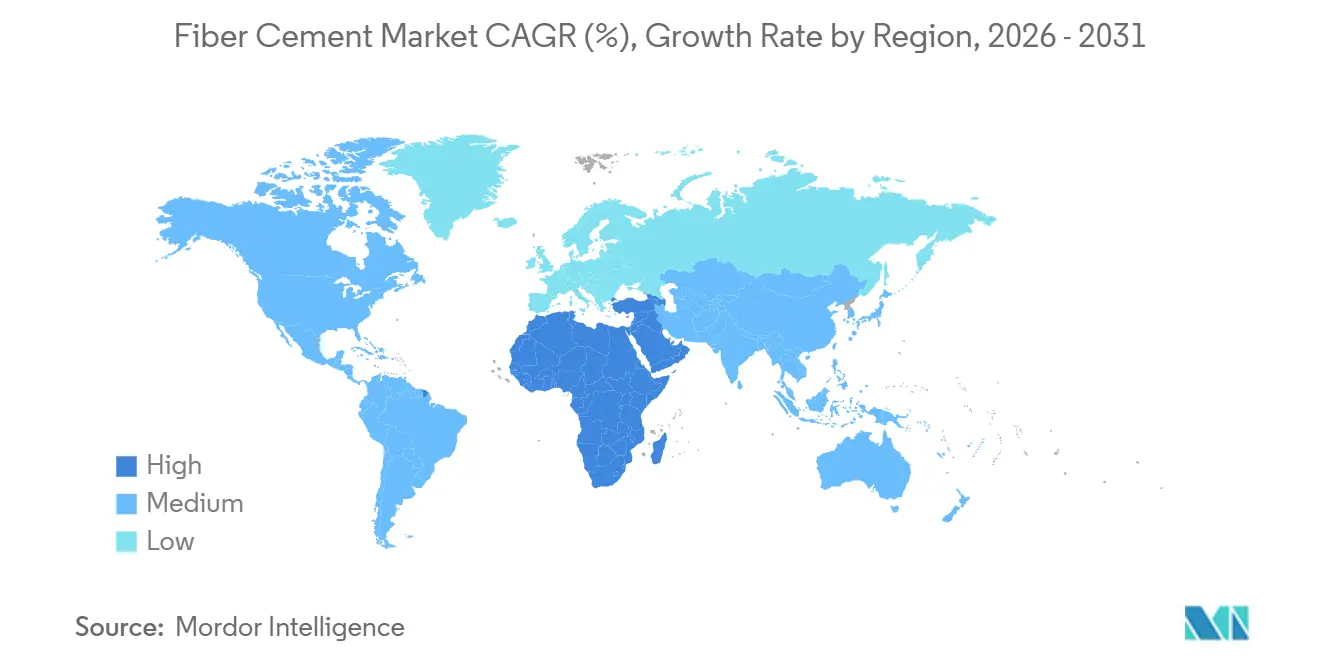

- By geography, Asia-Pacific captured 43.22% of the 2025 volume, while the Middle East and Africa region is projected to rise at a 4.41% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Fiber Cement Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent fire and acoustic performance codes | +1.2% | North America, Australia, EU | Medium term (2-4 years) |

| Lifecycle cost advantage vs. wood and vinyl | +0.9% | North America, Europe, developed Asia-Pacific | Long term (≥ 4 years) |

| Panelized prefab façade uptake | +0.8% | Asia-Pacific core, spill-over to Middle East | Short term (≤ 2 years) |

| Carbon-negative cement with nanofibres | +0.6% | Global early adoption in EU and North America | Long term (≥ 4 years) |

| Insurance-led demand in hurricane zones | +0.5% | U.S. Gulf Coast, Caribbean, parts of Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Fire and Acoustic Performance Building Codes

Fifteen additional United States jurisdictions adopted NFPA 285 in 2025, disqualifying combustible vinyl and untreated engineered wood from mid-rise projects and steering specifications toward fiber cement’s Class A rating. Australia’s National Construction Code 2025 expanded bushfire attack zones, adding 2.3 million dwellings that now require non-combustible façades. New Zealand enforced STC 50 acoustic minimums the same year, a threshold that the fiber cement market meets without multilayer assemblies. Building authorities in New York City also tightened fire-blocking rules for buildings above 23 m, a change that fiber cement rainscreens satisfy seamlessly. Collectively, these measures entrench the material as the default solution wherever fire and sound performance converge[1]National Fire Protection Association, “NFPA 285 Standard,” nfpa.org.

Lifecycle Cost Advantage Over Wood and Vinyl Siding

A 15-year study of 1,200 United States homes completed in 2025 showed fiber cement required repainting only once, whereas vinyl needed panel replacements every 8-10 years, pushing lifetime envelope costs USD 8,000-12,000 higher for vinyl-clad properties when discounted at 4%[2]Insurance Institute for Business & Home Safety, “FORTIFIED Home™ Program Annual Report 2025,” ibhs.org, reinforcing the long-term value proposition across the fiber cement market. Insurance carriers further tip the scales by granting 12-18% premium discounts on Class A fiber cement cladding in wildfire zones, savings unavailable to vinyl. Coastal builders confirm the advantage, noting salt-air corrosion shortens vinyl life by 60% compared with fiber cement, which retains integrity in hurricane-grade conditions.

Panelized Prefab Façades Uptake in Mid-Rise Buildings

China’s mandate that 30% of new urban structures use modular components by 2026 catalyzed fiber cement market growth through increased panel adoption, delivering 35% labor savings and 40% faster delivery on 8-12 story towers in Chengdu and Wuhan. India’s affordable-housing drive relies on factory-made panels embedding fiber cement, vapor barriers, and windows, cutting skilled-labor needs in half. SHERA’s PHP 2 billion (USD 34.8 million) Pampanga plant, opened January 2025, turns out 240,000 tons of pre-cut, pre-finished panels that shrink installation time from 8 hours to 2.5 hours per 100 ft². Saudi Arabia’s NEOM project now specifies off-site fabricated envelopes for 70% of surface area, reinforcing a regional pivot toward prefab solutions.

Carbon-Negative Cement Formulations with Cellulose Nanofibres

Laboratory data published in 2025 show that adding 1% cellulose nanocrystals boosts compressive strength by 18% while trimming clinker content by 20%, driving embodied-carbon reductions near 0.20 t CO₂/ton. Boral secured AUD 24.5 million (USD 15.80 million) in March 2025 to integrate coconut-husk feedstocks at its Berrima works, expected to cut clinker emissions intensity 11% by 2028. Lifecycle assessments reveal that panels containing 20% nanofibres sourced from bagasse can reach -0.05 to -0.10 ton CO₂-equivalent per ton, positioning the fiber cement market for future carbon-sink credits once scale economies bring nanofibre costs toward parity.

Restraints Impact Analysis of Fiber Cement Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Engineered-wood siding substitutes | -0.7% | North America repair market, parts of Europe | Short term (≤ 2 years) |

| Pulp-price volatility for cellulose fibre | -0.5% | Global, acute where mills rely on imported NBSK | Medium term (2-4 years) |

| OSHA silica-dust compliance cost for SMEs | -0.3% | United States, Canada, regulated EU jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Substitutes Such as Engineered-Wood Siding

LP SmartSide increased its United States share by 3.2 points between 2023 and 2025, offering installed costs 25% below fiber cement and 60% lower panel weight, which trims labor hours by a fifth. Hail-prone regions value the product’s higher impact tolerance, yet its combustibility bars usage in wildfire-interface zones covering 46 million United States homes. Consequently, the fiber cement market concedes low-margin, price-sensitive work yet retains premium positions in fire-regulated or mid-rise segments.

Fibre-Sourcing Risk Amid Global Pulp-Price Volatility

Northern Bleached Softwood Kraft (NBSK) pulp spiked to USD 1,450/ton in January 2025 after Canadian wildfires and Finnish strikes removed 1.2 million tons of annual supply. Each USD 100 rise lifts finished fiber cement cost USD 8-12/ton, clipping gross margins 2-3 points where competitive pressure limits pass-through in the fiber cement market. Integrated majors hedge exposure via long-term contracts or captive mills, whereas smaller firms scramble for recycled or agricultural fibres that demand lengthy re-certification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Fiber Cement Market Segment Analysis

By Application:

Cladding Extends Lead Through Prefab IntegrationSiding held 35.11% of global Fiber Cement volume in 2025, reflecting its entrenched position in single-family residential construction, where horizontal lap profiles dominate North American and Australian markets. Yet cladding will expand at a 4.58% CAGR during the forecast period (2026-2031), the fastest rate among applications, driven by its integration into prefabricated envelope systems for mid-rise buildings. Cladding's growth trajectory reflects a structural shift in construction procurement: developers of 6-12 story residential and commercial projects increasingly specify off-site-fabricated panels. Roofing applications, while smaller in absolute volume, benefit from fiber cement's Class A fire rating in wildfire-interface zones. Molding and trimming segments serve niche architectural applications where fiber cement's machinability and paint adhesion replicate traditional wood profiles at lower maintenance cost.

In mature North American suburbs, siding remains dominant application in the fiber cement market, yet growth slows to replacement cycles lasting 30-40 years. Roofing tiles gain share in California’s WUI zones after the 2024 code extension that mandates non-combustible roofs for 2.8 million dwellings. Moulding, trim, and partition boards see niche uptake where moisture or termite exposure disqualify wood. As cladding pulls ahead, manufacturers enjoy 15-20% higher price realization but must service fewer, larger prefab customers that wield stronger bargaining power.

By End-User Sector:

Commercial Builds Momentum on ConversionsThe residential segment held 45.12% of 2025 volume, yet office-to-apartment conversions and data-center builds lift commercial demand at a projected 4.24% CAGR during the forecast period (2026-2031). A 2025 survey of 85 Northeastern US conversions found fiber cement façades cut 10-year maintenance by 35% compared with engineered wood, easing capital-spending hurdles for adaptive-reuse developers.

Data-center operators favor fiber cement for non-conductive, fire-safe perimeter walls, supporting hyperscale builds rising 18% annually through 2027. Institutional owners of schools and hospitals gravitate to the material’s Class A rating and low particle emission, vital for sterile or high-traffic spaces. Industrial warehouses nearshored to Mexico and ASEAN likewise adopt fiber cement for durability in hot, humid climates, adding steady baseline growth beyond cyclical residential trends.

Geography Analysis

APAC and Oceania Fiber Cement Market

Asia-Pacific commanded 43.22% of 2025 volume, propelled by China’s prefab directive and India’s 20 million-unit housing push. Tier-2 Chinese developers specify pre-finished panels to win Green Building approvals, while Japan’s revised earthquake-insurance discounts drive uptake in seismic zones. SHERA’s Philippines plant supplies Southeast Asia and Oceania, leveraging lower freight costs than trans-Pacific shipments. Australia’s expanded bushfire zones add 2.3 million dwellings that must now use non-combustible façades, sustaining demand even as housing starts flatten.

North America Fiber Cement Market

In North America, James Hardie’s USD 200 million Prattville upgrade raised US capacity 15% and cut kiln energy 22%, anchoring supply for Florida and Gulf Coast retrofits that secure an average 18% premium savings under FORTIFIED Home rules. Canada’s residential slowdown is offset by hospital and education projects requiring non-combustible façades, while Mexican industrial parks use fiber cement to withstand desert climates and boost nearshoring credibility.

EMEA and South America Fiber Cement Market

Europe's market share, underpinned by renovation mandates in Germany and the EU’s near-zero-energy building code. Fiber cement rainscreens integrate external insulation to achieve sub-0.20 W/m²K U-values while meeting fire standards for buildings above 7 m. The Middle East and Africa expand fastest at 4.41% CAGR, led by Saudi Vision 2030 and Kenya’s clinker capacity build-out that lowers raw-material costs. South America benefits from infrastructure outlays in Brazil and Argentina, where humid coastal cities prefer durable, low-maintenance cladding.

Competitive Landscape

The Fiber Cement market is moderately consolidated. Product differentiation centers on pre-finished systems and carbon-negative chemistries commanding 12-18% premiums. Saint-Gobain now bundles fiber cement with high-performance adhesives acquired through Fosroc, raising project wallet share. Boral’s kiln-feed project targets an 11% emission-intensity cut, aligning with LEED v5 procurement in Australia and New Zealand. Emerging disruptors pursue cellulose-nanofibre blends that can fetch 25-35% price premiums where embodied-carbon disclosure is law, though current costs remain 40-60% above conventional formulations.

Fiber Cement Industry Leaders

Etex Group

James Hardie Building Products Inc.

SCG International Corporation

Saint-Gobain

CSR Limited

- *Disclaimer: Major Players sorted in no particular order

Fiber Cement Market Companies Covered in this Report

- Allura

- American Fiber Cement

- CSR Limited

- ELEMENTIA MATERIALS, SAB DE CV

- Eterno Ivica S.r.l.

- Etex Group

- Everest

- HIL Limited

- James Hardie Building Products Inc.

- KMEW Co., Ltd.

- Mahaphant Fibre-Cement (South Asia) Pvt. Ltd

- Maxitile Inc.

- NICHIHA

- Ramco Industries Limited

- Renaatus Group

- Saint-Gobain (Weber & Eternit)

- SCG International Corporation

- SHERA Public Company Limited

- Swisspearl Group AG

Recent Industry Developments in Fiber Cement Market

- January 2026: Saint-Gobain Africa opened its new RhinoROC fibre cement manufacturing plant in Ekurhuleni, Gauteng, for the South African construction sector.

- August 2024: Shera Public Co. Ltd., a manufacturer of fiber cement products in Thailand, announced plans to open its first Philippine manufacturing plant. Once operational, the facility will have the capacity to produce up to 240,000 tons of fiber cement annually.

Global Fiber Cement Market Report Scope

Fibre cement is a durable, versatile composite building material made from cement, sand, and cellulose fibres, commonly used for cladding, roofing, and flooring. It is fire-resistant, water-resistant, termite-proof, and low-maintenance, acting as a modern alternative to wood or traditional cement, frequently applied in both residential and commercial projects.

The Fiber Cement market is segmented by application, end-user sector, and geography. By application, the market is segmented into siding, cladding, moulding and trimming, roofing, and other applications. By end-user sector, the market is segmented into residential, commercial, industrial and institutional, and infrastructure. The report also covers the market size and forecasts for the Fiber Cement market in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

Segmentation Overview

| Siding |

| Cladding |

| Moulding and Trimming |

| Roofing |

| Other Applications |

| Residential |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Siding | |

| Cladding | ||

| Moulding and Trimming | ||

| Roofing | ||

| Other Applications | ||

| By End-User Sector | Residential | |

| Commercial | ||

| Industrial and Institutional | ||

| Infrastructure | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Market Definition

- END-USE SECTOR - Fiber cement consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of fiber cement for siding, roofing, cladding molding and trimming, and other applications are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms